Attached files

| file | filename |

|---|---|

| 8-K - 8-K - Sunstone Hotel Investors, Inc. | sho-20150806x8k.htm |

| EX-99.1 - EX-99.1 - Sunstone Hotel Investors, Inc. | sho-20150806ex99185f80c.htm |

|

|

Supplemental Financial Information |

|

|

|

||||||||

|

|

|

||||||||

|

Supplemental Financial Information For the quarter ended June 30, 2015 August 6, 2015

|

|

||||||||

|

|

Supplemental Financial Information |

Table of Contents

|

3 |

|||||||||

|

4 |

|||||||||

|

5 |

|||||||||

|

6 |

|||||||||

|

9 |

|||||||||

|

10 |

|||||||||

|

12 |

|||||||||

|

Reconciliation of Net Income to EBITDA and Adjusted EBITDA Q2 & YTD 2015/2014 |

13 |

||||||||

|

14 |

|||||||||

|

Pro Forma Consolidated Statements of Operations Q2 2015 – Q3 2014, FY 2014 |

15 |

||||||||

|

16 |

|||||||||

|

17 |

|||||||||

|

19 |

|||||||||

|

20 |

|||||||||

|

21 |

|||||||||

|

22 |

|||||||||

|

23 |

|||||||||

|

24 |

|||||||||

|

|

Supplemental Financial Information |

|

|

Supplemental Financial Information |

CORPORATE PROFILE, FINANCIAL DISCLOSURES,

AND SAFE HARBOR

|

CORPORATE PROFILE, FINANCIAL DISCLOSURES, AND SAFE HARBOR |

|

|

Page 3 |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

Supplemental Financial Information |

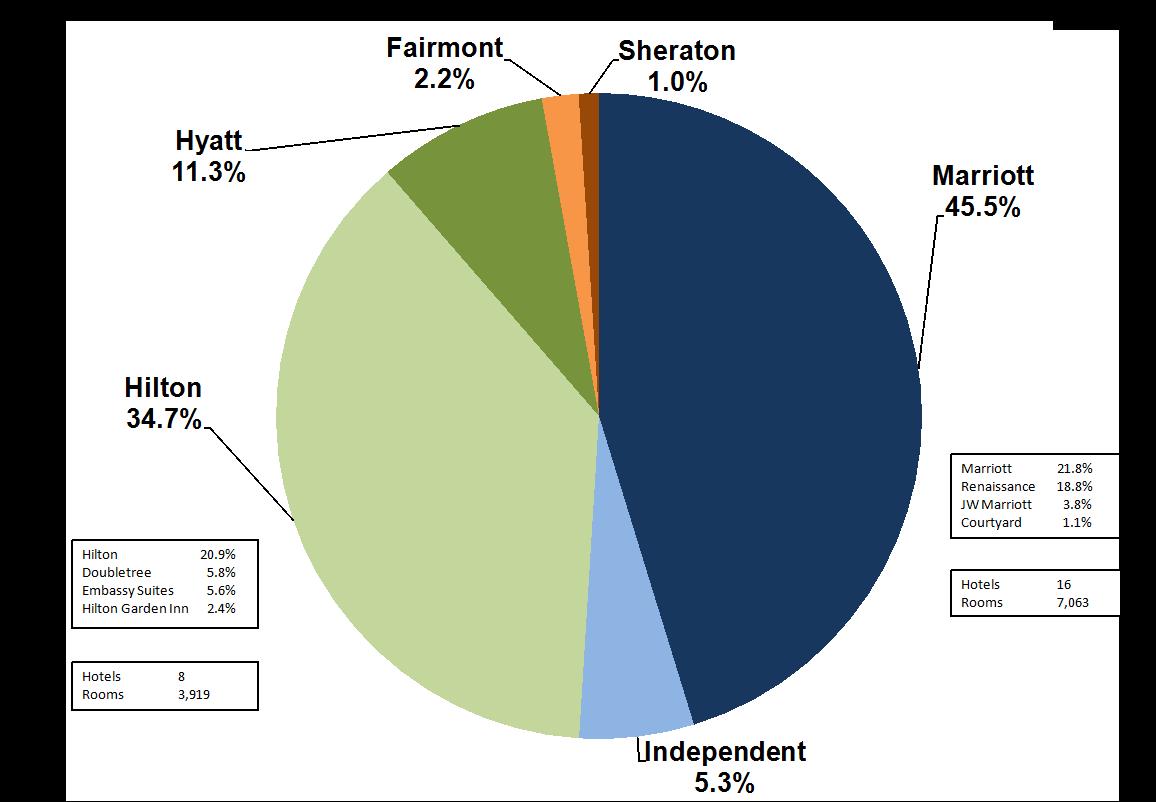

Sunstone Hotel Investors, Inc. (NYSE:SHO) is a lodging real estate investment trust (REIT) that, as of August 6, 2015, has interests in 30 hotels held for investment comprised of 14,313 rooms. Sunstone’s hotels are primarily in the urban, upper upscale segment and are operated under nationally recognized brands, such as Marriott, Hilton, Hyatt, Fairmont and Sheraton.

Sunstone’s mission is to create meaningful value for our stockholders by becoming the premier hotel owner. Our values include transparency, trust, ethical conduct, communication and discipline. As demand for lodging generally fluctuates with the overall economy, we seek to employ a balanced, cycle-appropriate corporate strategy that encompasses the following:

|

· |

Proactive portfolio management; |

|

· |

Focused asset management; |

|

· |

Disciplined external growth; and |

|

· |

Continued balance sheet strength. |

Corporate Headquarters

120 Vantis, Suite 350

Aliso Viejo, CA 92656

(949) 330-4000

Company Contacts

John Arabia

President and Chief Executive Officer

(949) 382-3008

Bryan Giglia

Chief Financial Officer

(949) 382-3036

|

CORPORATE PROFILE, FINANCIAL DISCLOSURES, AND SAFE HARBOR |

|

|

Page 4 |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

Supplemental Financial Information |

This presentation contains forward-looking statements within the meaning of federal securities laws and regulations. These forward-looking statements are identified by their use of terms and phrases such as “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “predict,” “project,” “should,” “will” and other similar terms and phrases, including opinions, references to assumptions and forecasts of future results. Forward-looking statements are not guarantees of future performance and involve known and unknown risks, uncertainties and other factors that may cause the actual results to differ materially from those anticipated at the time the forward-looking statements are made. These risks include, but are not limited to: volatility in the debt or equity markets affecting our ability to acquire or sell hotel assets; international, national and local economic and business conditions, including the likelihood of a U.S. recession or global economic slowdown, as well as any type of flu or disease-related pandemic, affecting the lodging and travel industry; the ability to maintain sufficient liquidity and our access to capital markets; potential terrorist attacks or civil unrest, which would affect occupancy rates at our hotels and the demand for hotel products and services; operating risks associated with the hotel business; risks associated with the level of our indebtedness and our ability to meet covenants in our debt and equity agreements; relationships with property managers and franchisors; our ability to maintain our properties in a first-class manner, including meeting capital expenditure requirements; our ability to compete effectively in areas such as access, location, quality of accommodations and room rate structures; changes in travel patterns, taxes and government regulations, which influence or determine wages, prices, construction procedures and costs; our ability to identify, successfully compete for and complete acquisitions; the performance of hotels after they are acquired; necessary capital expenditures and our ability to fund them and complete them with minimum disruption; our ability to continue to satisfy complex rules in order for us to qualify as a REIT for federal income tax purposes; and other risks and uncertainties associated with our business described in the Company’s filings with the Securities and Exchange Commission. Although the Company believes the expectations reflected in such forward-looking statements are based upon reasonable assumptions, it can give no assurance that the expectations will be attained or that any deviation will not be material. All forward-looking information in this presentation is as of August 6, 2015, and the Company undertakes no obligation to update any forward-looking statement to conform the statement to actual results or changes in the Company’s expectations.

This presentation should be read in conjunction with the consolidated financial statements and notes thereto included in our most recent reports on Form 10-K and Form 10-Q. Copies of these reports are available on our website at www.sunstonehotels.com and through the SEC’s Electronic Data Gathering Analysis and Retrieval System (“EDGAR”) at www.sec.gov.

|

CORPORATE PROFILE, FINANCIAL DISCLOSURES, AND SAFE HARBOR |

|

|

Page 5 |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

Supplemental Financial Information |

We present the following non-GAAP financial measures that we believe are useful to investors as key supplemental measures of our operating performance: earnings before interest expense, taxes, depreciation and amortization, or EBITDA; Adjusted EBITDA (as defined below); funds from operations attributable to common stockholders, or FFO attributable to common stockholders; Adjusted FFO attributable to common stockholders (as defined below); hotel adjusted EBITDA; and hotel adjusted EBITDA margin. These measures should not be considered in isolation or as a substitute for measures of performance in accordance with GAAP. EBITDA, Adjusted EBITDA, FFO attributable to common stockholders, Adjusted FFO attributable to common stockholders, hotel adjusted EBITDA and hotel adjusted EBITDA margin as calculated by us, may not be comparable to other companies that do not define such terms exactly as the Company. These non-GAAP measures are used in addition to and in conjunction with results presented in accordance with GAAP. They should not be considered as alternatives to operating profit, cash flow from operations, or any other operating performance measure prescribed by GAAP. These non-GAAP financial measures reflect additional ways of viewing our operations that we believe, when viewed with our GAAP results and the reconciliations to the corresponding GAAP financial measures, provide a more complete understanding of factors and trends affecting our business than could be obtained absent this disclosure. We strongly encourage investors to review our financial information in its entirety and not to rely on a single financial measure.

EBITDA is a commonly used measure of performance in many industries. We believe EBITDA is useful to investors in evaluating our operating performance because this measure helps investors evaluate and compare the results of our operations from period to period by removing the impact of our capital structure (primarily interest expense) and our asset base (primarily depreciation and amortization) from our operating results. We also believe the use of EBITDA facilitates comparisons between us and other lodging REITs, hotel owners who are not REITs and other capital-intensive companies. In addition, certain covenants included in our indebtedness use EBITDA as a measure of financial compliance. We also use EBITDA as a measure in determining the value of hotel acquisitions and dispositions.

Historically, we have adjusted EBITDA when evaluating our performance because we believe that the exclusion of certain additional items described below provides useful information to investors regarding our operating performance and that the presentation of Adjusted EBITDA, when combined with the primary GAAP presentation of net income, is beneficial to an investor’s complete understanding of our operating performance.

We believe that the presentation of FFO attributable to common stockholders provides useful information to investors regarding our operating performance because it is a measure of our operations without regard to specified non-cash items such as real estate depreciation and amortization, amortization of lease intangibles, any real estate impairment loss and any gain or loss on sale of real estate assets, all of which are based on historical cost accounting and may be of lesser significance in evaluating our current performance. Our presentation of FFO attributable to common stockholders conforms to the National Association of Real Estate Investment Trusts’ (“NAREIT”) definition of “FFO applicable to common shares.” This may not be comparable to FFO reported by other REITs that do not define the terms in accordance with the current NAREIT definition, or that interpret the current NAREIT definition differently that we do.

We also present Adjusted FFO attributable to common stockholders when evaluating our operating performance because we believe that the exclusion of certain additional items described below provides useful supplemental information to investors regarding our ongoing operating performance, and may facilitate comparisons of operating performance between periods and our peer companies.

|

CORPORATE PROFILE, FINANCIAL DISCLOSURES, AND SAFE HARBOR |

|

|

Page 6 |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

Supplemental Financial Information |

We adjust EBITDA and FFO attributable to common stockholders for the following items, which may occur in any period, and refer to these measures as either Adjusted EBITDA or Adjusted FFO attributable to common stockholders:

|

· |

Amortization of favorable and unfavorable contracts: we exclude the non-cash amortization of the favorable management contract asset recorded in conjunction with our acquisition of the Hilton Garden Inn Chicago Downtown/Magnificent Mile, along with the favorable and unfavorable tenant lease contracts, as applicable, recorded in conjunction with our acquisitions of the Boston Park Plaza, the Hilton Garden Inn Chicago Downtown/Magnificent Mile, the Hilton New Orleans St. Charles, the Hyatt Regency San Francisco and the Wailea Beach Marriott Resort & Spa. The amortization of favorable and unfavorable contracts does not reflect the underlying performance of our hotels. |

|

· |

Ground rent adjustments: we exclude the non-cash expense incurred from straightlining our ground lease obligations as this expense does not reflect the underlying performance of our hotels. |

|

· |

Gains or losses from debt transactions: we exclude the effect of finance charges and premiums associated with the extinguishment of debt, including the acceleration of deferred financing costs from the original issuance of the debt being redeemed or retired because, like interest expense, their removal helps investors evaluate and compare the results of our operations from period to period by removing the impact of our capital structure. |

|

· |

Acquisition costs: under GAAP, costs associated with completed acquisitions are expensed in the year incurred. We exclude the effect of these costs because we believe they are not reflective of the ongoing performance of the Company. |

|

· |

Non-controlling interests: we deduct the non-controlling partner’s pro rata share of any EBITDA or FFO adjustments related to our consolidated Hilton San Diego Bayfront partnership, as well as any preferred dividends earned by investors in an entity that owns the Doubletree Guest Suites Times Square, including related administrative fees. |

|

· |

Cumulative effect of a change in accounting principle: from time to time, the FASB promulgates new accounting standards that require the consolidated statement of operations to reflect the cumulative effect of a change in accounting principle. We exclude these one-time adjustments because they do not reflect our actual performance for that period. |

|

· |

Impairment losses: we exclude the effect of impairment losses because we believe that including them in Adjusted EBITDA and Adjusted FFO attributable to common stockholders is not consistent with reflecting the ongoing performance of our remaining assets. |

|

· |

Other adjustments: we exclude other adjustments such as executive severance costs, lawsuit settlement costs, prior year property tax assessments and/or credits, management company transition costs, lease buyouts, any gains or losses we have recognized on redemptions of assets other than real estate investments, and restructurings and departmental closing costs, including severance, because we do not believe these costs reflect our actual performance for that period and/or the ongoing operations of our hotels. |

|

CORPORATE PROFILE, FINANCIAL DISCLOSURES, AND SAFE HARBOR |

|

|

Page 7 |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

Supplemental Financial Information |

In addition, to derive Adjusted EBITDA we exclude the non-cash expense incurred with the amortization of deferred stock compensation as this expense does not reflect the underlying performance of our hotels. We also include an adjustment for the cash ground lease expense recorded on the Hyatt Chicago Magnificent Mile’s building lease. Upon acquisition of this hotel, we determined that the building lease was a capital lease, and, therefore, we include a portion of the capital lease payment each month in interest expense. We include an adjustment for ground lease expense on capital leases in order to more accurately reflect the operating performance of the Hyatt Chicago Magnificent Mile. We also exclude the effect of gains and losses on the disposition of depreciable assets because we believe that including them in Adjusted EBITDA is not consistent with reflecting the ongoing performance of our assets. In addition, material gains or losses from the depreciated value of the disposed assets could be less important to investors given that the depreciated asset value often does not reflect its market value.

To derive Adjusted FFO attributable to common stockholders, we also exclude the non-cash gains or losses on our derivatives, as well as any federal and state taxes associated with the application of net operating loss carryforwards. We believe that these items are not reflective of our ongoing finance costs.

Reconciliations of net income to EBITDA and Adjusted EBITDA are set forth on page 13 of this supplemental package. Reconciliations of net income to FFO attributable to common stockholders and Adjusted FFO attributable to common stockholders are set forth on page 14 of this supplemental package.

Our 30 comparable hotels include all hotels held for investment by the Company as of June 30, 2015, and also include prior ownership results for the Wailea Beach Marriott Resort & Spa acquired in July 2014. We obtained prior ownership information from the Wailea Beach Marriott Resort & Spa's previous owner during the due diligence period before acquiring the hotel. We performed a limited review of the information as part of our analysis of the acquisition.

Presentation of 2014 information conforms to changes stipulated by the industry’s Uniform System of Accounts for the Lodging Industry, Eleventh Revised Edition, which became effective in January 2015.

|

CORPORATE PROFILE, FINANCIAL DISCLOSURES, AND SAFE HARBOR |

|

|

Page 8 |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

Supplemental Financial Information |

CORPORATE FINANCIAL INFORMATION

|

CORPORATE FINANCIAL INFORMATION |

|

|

Page 9 |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

Supplemental Financial Information |

Condensed Consolidated Balance Sheets

Q2 2015 – Q2 2014

|

(In thousands) |

June 30, 2015 (1) |

March 31, 2015 (2) |

December 31, 2014 (3) |

September 30, 2014 (4) |

June 30, 2014 (5) |

||||||||||||

|

Assets |

|||||||||||||||||

|

Investment in hotel properties: |

|||||||||||||||||

|

Land |

$ |

570,011 |

$ |

570,011 |

$ |

570,011 |

$ |

570,011 |

$ |

450,304 | |||||||

|

Buildings & improvements |

3,276,598 | 3,245,398 | 3,237,596 | 3,216,923 | 3,013,911 | ||||||||||||

|

Furniture, fixtures, & equipment |

471,193 | 457,249 | 450,057 | 447,712 | 432,572 | ||||||||||||

|

Other |

233,753 | 242,508 | 217,389 | 236,739 | 218,300 | ||||||||||||

| 4,551,555 | 4,515,166 | 4,475,053 | 4,471,385 | 4,115,087 | |||||||||||||

|

Less accumulated depreciation & amortization |

(1,019,399) | (978,041) | (936,924) | (924,857) | (884,192) | ||||||||||||

| 3,532,156 | 3,537,125 | 3,538,129 | 3,546,528 | 3,230,895 | |||||||||||||

|

Other assets, net |

36,286 | 31,832 | 32,091 | 32,292 | 47,449 | ||||||||||||

|

Current assets: |

|||||||||||||||||

|

Cash and cash equivalents |

98,760 | 156,972 | 222,096 | 135,427 | 360,702 | ||||||||||||

|

Restricted cash |

88,456 | 87,260 | 82,074 | 93,124 | 87,975 | ||||||||||||

|

Other current assets, net |

65,140 | 68,168 | 50,575 | 61,959 | 55,939 | ||||||||||||

|

Total assets |

$ |

3,820,798 |

$ |

3,881,357 |

$ |

3,924,965 |

$ |

3,869,330 |

$ |

3,782,960 | |||||||

*Footnotes on following page.

|

CORPORATE FINANCIAL INFORMATION |

|

|

Page 10 |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

Supplemental Financial Information |

Condensed Consolidated Balance Sheets

Q2 2015 – Q2 2014 (cont.)

|

(In thousands) |

June 30, 2015 (1) |

March 31, 2015 (2) |

December 31, 2014 (3) |

September 30, 2014 (4) |

June 30, 2014 (5) |

||||||||||

|

Liabilities |

|||||||||||||||

|

Current liabilities: |

|||||||||||||||

|

Current portion of notes payable |

$ |

135,825 |

$ |

235,970 |

$ |

121,328 |

$ |

159,696 |

$ |

122,835 | |||||

|

Other current liabilities |

118,601 | 115,668 | 177,656 | 119,683 | 107,198 | ||||||||||

|

Total current liabilities |

254,426 | 351,638 | 298,984 | 279,379 | 230,033 | ||||||||||

|

Notes payable, less current portion |

1,182,832 | 1,187,447 | 1,307,964 | 1,226,796 | 1,269,587 | ||||||||||

|

Capital lease obligations, less current portion |

15,576 | 15,576 | 15,576 | 15,576 | 15,576 | ||||||||||

|

Other liabilities |

35,265 | 34,670 | 33,607 | 34,934 | 34,106 | ||||||||||

|

Total liabilities |

1,488,099 | 1,589,331 | 1,656,131 | 1,556,685 | 1,549,302 | ||||||||||

|

Equity |

|||||||||||||||

|

Stockholders' equity: |

|||||||||||||||

|

8% Series D cumulative redeemable preferred stock |

115,000 | 115,000 | 115,000 | 115,000 | 115,000 | ||||||||||

|

Common stock, $0.01 par value, 500,000,000 shares authorized |

2,076 | 2,075 | 2,048 | 2,035 | 1,994 | ||||||||||

|

Additional paid in capital |

2,456,604 | 2,454,720 | 2,418,567 | 2,397,196 | 2,335,709 | ||||||||||

|

Retained earnings |

355,702 | 304,525 | 305,503 | 292,250 | 260,410 | ||||||||||

|

Cumulative dividends |

(650,014) | (637,279) | (624,545) | (547,851) | (535,281) | ||||||||||

|

Total stockholders' equity |

2,279,368 | 2,239,041 | 2,216,573 | 2,258,630 | 2,177,832 | ||||||||||

|

Non-controlling interest in consolidated joint ventures |

53,331 | 52,985 | 52,261 | 54,015 | 55,826 | ||||||||||

|

Total equity |

2,332,699 | 2,292,026 | 2,268,834 | 2,312,645 | 2,233,658 | ||||||||||

|

Total liabilities and equity |

$ |

3,820,798 |

$ |

3,881,357 |

$ |

3,924,965 |

$ |

3,869,330 |

$ |

3,782,960 | |||||

|

(1) |

As presented on Form 10-Q to be filed in August 2015. |

|

(2) |

As presented on Form 10-Q filed May 8, 2015. |

|

(3) |

As presented on Form 10-K filed February 19, 2015. |

|

(4) |

As presented on Form 10-Q filed November 4, 2014. |

|

(5) |

As presented on Form 10-Q filed August 8, 2014. |

|

CORPORATE FINANCIAL INFORMATION |

|

|

Page 11 |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

Supplemental Financial Information |

Consolidated Statements of Operations

Q2 & YTD 2015/2014

|

|

|

|

Three Months Ended June 30, |

|

|

Six Months Ended June 30, |

||||||

|

(In thousands, except per share data) |

|

|

2015 |

|

|

2014 |

|

|

2015 |

|

|

2014 |

|

Revenues |

|

|

|

|

|

|

|

|

|

|

|

|

|

Room |

|

$ |

239,678 |

|

$ |

214,940 |

|

$ |

432,969 |

|

$ |

383,067 |

|

Food and beverage |

|

|

79,265 |

|

|

68,733 |

|

|

151,449 |

|

|

128,644 |

|

Other operating |

|

|

20,324 |

|

|

17,179 |

|

|

39,234 |

|

|

32,624 |

|

Total revenues |

|

|

339,267 |

|

|

300,852 |

|

|

623,652 |

|

|

544,335 |

|

Operating expenses |

|

|

|

|

|

|

|

|

|

|

|

|

|

Room |

|

|

57,568 |

|

|

53,418 |

|

|

111,410 |

|

|

102,337 |

|

Food and beverage |

|

|

52,812 |

|

|

45,109 |

|

|

103,031 |

|

|

88,017 |

|

Other operating |

|

|

5,337 |

|

|

5,006 |

|

|

10,468 |

|

|

10,001 |

|

Advertising and promotion |

|

|

15,567 |

|

|

13,655 |

|

|

30,927 |

|

|

26,626 |

|

Repairs and maintenance |

|

|

11,381 |

|

|

10,706 |

|

|

22,939 |

|

|

21,587 |

|

Utilities |

|

|

8,377 |

|

|

7,788 |

|

|

17,362 |

|

|

16,077 |

|

Franchise costs |

|

|

10,818 |

|

|

10,261 |

|

|

19,418 |

|

|

18,338 |

|

Property tax, ground lease and insurance |

|

|

23,151 |

|

|

21,413 |

|

|

46,764 |

|

|

40,465 |

|

Property general and administrative |

|

|

37,107 |

|

|

31,963 |

|

|

71,556 |

|

|

60,885 |

|

Corporate overhead |

|

|

6,923 |

|

|

7,674 |

|

|

21,176 |

|

|

14,233 |

|

Depreciation and amortization |

|

|

40,873 |

|

|

37,973 |

|

|

81,580 |

|

|

75,588 |

|

Total operating expenses |

|

|

269,914 |

|

|

244,966 |

|

|

536,631 |

|

|

474,154 |

|

Operating income |

|

|

69,353 |

|

|

55,886 |

|

|

87,021 |

|

|

70,181 |

|

Interest and other income |

|

|

1,828 |

|

|

891 |

|

|

2,774 |

|

|

1,607 |

|

Interest expense |

|

|

(17,289) |

|

|

(18,331) |

|

|

(34,615) |

|

|

(36,614) |

|

Loss on extinguishment of debt |

|

|

(2) |

|

|

— |

|

|

(2) |

|

|

— |

|

Income before income taxes and discontinued operations |

|

|

53,890 |

|

|

38,446 |

|

|

55,178 |

|

|

35,174 |

|

Income tax provision |

|

|

(233) |

|

|

(110) |

|

|

(318) |

|

|

(334) |

|

Income from continuing operations |

|

|

53,657 |

|

|

38,336 |

|

|

54,860 |

|

|

34,840 |

|

Income from discontinued operations |

|

|

— |

|

|

5,199 |

|

|

— |

|

|

5,199 |

|

Net income |

|

|

53,657 |

|

|

43,535 |

|

|

54,860 |

|

|

40,039 |

|

Income from consolidated joint ventures attributable to non-controlling interests |

|

|

(2,480) |

|

|

(1,667) |

|

|

(4,661) |

|

|

(3,901) |

|

Preferred stock dividends |

|

|

(2,300) |

|

|

(2,300) |

|

|

(4,600) |

|

|

(4,600) |

|

Income attributable to common stockholders |

|

$ |

48,877 |

|

$ |

39,568 |

|

$ |

45,599 |

|

$ |

31,538 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic and diluted per share amounts: |

|

|

|

|

|

|

|

|

|

|

|

|

|

Income from continuing operations attributable to common stockholders |

|

$ |

0.23 |

|

$ |

0.19 |

|

$ |

0.22 |

|

$ |

0.14 |

|

Income from discontinued operations |

|

|

— |

|

|

0.03 |

|

|

— |

|

|

0.03 |

|

Basic and diluted income attributable to common stockholders per common share |

|

$ |

0.23 |

|

$ |

0.22 |

|

$ |

0.22 |

|

$ |

0.17 |

|

Basic and diluted weighted average common shares outstanding |

|

|

207,577 |

|

|

182,604 |

|

|

207,091 |

|

|

181,836 |

|

Dividends declared per common share |

|

$ |

0.05 |

|

$ |

0.05 |

|

$ |

0.10 |

|

$ |

0.10 |

|

CORPORATE FINANCIAL INFORMATION |

|

|

Page 12 |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

Supplemental Financial Information |

Reconciliation of Net Income to EBITDA and Adjusted EBITDA

Q2 & YTD 2015/2014

|

|

|

Three Months Ended June 30, |

|

|

Six Months Ended June 30, |

|||||||

|

(In thousands) |

|

|

2015 |

|

|

2014 |

|

|

2015 |

|

|

2014 |

|

Net income |

|

$ |

53,657 |

|

$ |

43,535 |

|

$ |

54,860 |

|

$ |

40,039 |

|

Operations held for investment: |

|

|

|

|

|

|

|

|

|

|

|

|

|

Depreciation and amortization |

|

|

40,873 |

|

|

37,973 |

|

|

81,580 |

|

|

75,588 |

|

Amortization of lease intangibles |

|

|

1,029 |

|

|

1,030 |

|

|

2,057 |

|

|

2,058 |

|

Interest expense |

|

|

17,289 |

|

|

18,331 |

|

|

34,615 |

|

|

36,614 |

|

Income tax provision |

|

|

233 |

|

|

110 |

|

|

318 |

|

|

334 |

|

Non-controlling interests: |

|

|

|

|

|

|

|

|

|

|

|

|

|

Income from consolidated joint ventures attributable to non-controlling interests |

|

|

(2,480) |

|

|

(1,667) |

|

|

(4,661) |

|

|

(3,901) |

|

Depreciation and amortization |

|

|

(854) |

|

|

(824) |

|

|

(1,701) |

|

|

(1,645) |

|

Interest expense |

|

|

(385) |

|

|

(568) |

|

|

(763) |

|

|

(1,135) |

|

EBITDA |

|

|

109,362 |

|

|

97,920 |

|

|

166,305 |

|

|

147,952 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Operations held for investment: |

|

|

|

|

|

|

|

|

|

|

|

|

|

Amortization of deferred stock compensation |

|

|

1,786 |

|

|

1,944 |

|

|

4,681 |

|

|

3,316 |

|

Amortization of favorable and unfavorable contracts, net |

|

|

42 |

|

|

46 |

|

|

(179) |

|

|

92 |

|

Non-cash straightline lease expense |

|

|

491 |

|

|

500 |

|

|

995 |

|

|

1,012 |

|

Capital lease obligation interest - cash ground rent |

|

|

(351) |

|

|

(351) |

|

|

(702) |

|

|

(702) |

|

Gain on sale of assets, net |

|

|

(1) |

|

|

(49) |

|

|

(1) |

|

|

(55) |

|

Loss on extinguishment of debt |

|

|

2 |

|

|

— |

|

|

2 |

|

|

— |

|

Gain on redemption of note receivable |

|

|

(939) |

|

|

— |

|

|

(939) |

|

|

— |

|

Closing costs - completed acquisitions |

|

|

— |

|

|

102 |

|

|

— |

|

|

158 |

|

Prior year property tax adjustments, net |

|

|

88 |

|

|

(357) |

|

|

(100) |

|

|

(3,235) |

|

Boston Park Plaza relaunch costs |

|

|

— |

|

|

— |

|

|

683 |

|

|

— |

|

Lease termination costs |

|

|

— |

|

|

— |

|

|

300 |

|

|

— |

|

Costs associated with CEO severance |

|

|

— |

|

|

— |

|

|

5,257 |

|

|

— |

|

Non-controlling interests: |

|

|

|

|

|

|

|

|

|

|

|

|

|

Non-cash straightline lease expense |

|

|

(112) |

|

|

(112) |

|

|

(225) |

|

|

(225) |

|

Prior year property tax adjustments, net |

|

|

— |

|

|

— |

|

|

— |

|

|

696 |

|

Discontinued operations: |

|

|

|

|

|

|

|

|

|

|

|

|

|

Gain on sale of assets, net |

|

|

— |

|

|

(5,199) |

|

|

— |

|

|

(5,199) |

|

|

|

|

1,006 |

|

|

(3,476) |

|

|

9,772 |

|

|

(4,142) |

|

Adjusted EBITDA |

|

$ |

110,368 |

|

$ |

94,444 |

|

$ |

176,077 |

|

$ |

143,810 |

|

CORPORATE FINANCIAL INFORMATION |

|

|

Page 13 |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

Supplemental Financial Information |

Reconciliation of Net Income to FFO Attributable to Common Stockholders and Adjusted FFO Attributable to Common Stockholders

Q2 & YTD 2015/2014

|

|

|

Three Months Ended June 30, |

|

|

Six Months Ended June 30, |

|||||||

|

(In thousands, except per share data) |

|

|

2015 |

|

|

2014 |

|

|

2015 |

|

|

2014 |

|

Net income |

|

$ |

53,657 |

|

$ |

43,535 |

|

$ |

54,860 |

|

$ |

40,039 |

|

Preferred stock dividends |

|

|

(2,300) |

|

|

(2,300) |

|

|

(4,600) |

|

|

(4,600) |

|

Operations held for investment: |

|

|

|

|

|

|

|

|

|

|

|

|

|

Real estate depreciation and amortization |

|

|

40,477 |

|

|

37,575 |

|

|

80,787 |

|

|

74,801 |

|

Amortization of lease intangibles |

|

|

1,029 |

|

|

1,030 |

|

|

2,057 |

|

|

2,058 |

|

Gain on sale of assets, net |

|

|

(1) |

|

|

(49) |

|

|

(1) |

|

|

(55) |

|

Non-controlling interests: |

|

|

|

|

|

|

|

|

|

|

|

|

|

Income from consolidated joint ventures attributable to non-controlling interests |

|

|

(2,480) |

|

|

(1,667) |

|

|

(4,661) |

|

|

(3,901) |

|

Real estate depreciation and amortization |

|

|

(854) |

|

|

(824) |

|

|

(1,701) |

|

|

(1,645) |

|

Discontinued operations: |

|

|

|

|

|

|

|

|

|

|

|

|

|

Gain on sale of assets, net |

|

|

— |

|

|

(5,199) |

|

|

— |

|

|

(5,199) |

|

FFO attributable to common stockholders |

|

|

89,528 |

|

|

72,101 |

|

|

126,741 |

|

|

101,498 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Operations held for investment: |

|

|

|

|

|

|

|

|

|

|

|

|

|

Write-off of deferred financing fees |

|

|

455 |

|

|

— |

|

|

455 |

|

|

— |

|

Amortization of favorable and unfavorable contracts, net |

|

|

42 |

|

|

46 |

|

|

(179) |

|

|

92 |

|

Non-cash straightline lease expense |

|

|

491 |

|

|

500 |

|

|

995 |

|

|

1,012 |

|

Non-cash interest related to (gain) loss on derivatives, net |

|

|

10 |

|

|

(125) |

|

|

10 |

|

|

(234) |

|

Loss on extinguishment of debt |

|

|

2 |

|

|

— |

|

|

2 |

|

|

— |

|

Gain on redemption of note receivable |

|

|

(939) |

|

|

— |

|

|

(939) |

|

|

— |

|

Closing costs - completed acquisitions |

|

|

— |

|

|

102 |

|

|

— |

|

|

158 |

|

Prior year property tax adjustments, net |

|

|

88 |

|

|

(357) |

|

|

(100) |

|

|

(3,235) |

|

Boston Park Plaza relaunch costs |

|

|

— |

|

|

— |

|

|

683 |

|

|

— |

|

Lease termination costs |

|

|

— |

|

|

— |

|

|

300 |

|

|

— |

|

Costs associated with CEO severance |

|

|

— |

|

|

— |

|

|

5,257 |

|

|

— |

|

Amortization of deferred stock compensation associated with CEO severance |

|

|

— |

|

|

— |

|

|

1,623 |

|

|

— |

|

Non-controlling interests: |

|

|

|

|

|

|

|

|

|

|

|

|

|

Non-cash straightline lease expense |

|

|

(112) |

|

|

(112) |

|

|

(225) |

|

|

(225) |

|

Non-cash interest related to loss on derivative |

|

|

(2) |

|

|

— |

|

|

(2) |

|

|

— |

|

Prior year property tax adjustments, net |

|

|

— |

|

|

— |

|

|

— |

|

|

696 |

|

|

|

|

35 |

|

|

54 |

|

|

7,880 |

|

|

(1,736) |

|

Adjusted FFO attributable to common stockholders |

|

$ |

89,563 |

|

$ |

72,155 |

|

$ |

134,621 |

|

$ |

99,762 |

|

FFO attributable to common stockholders per diluted share |

|

$ |

0.43 |

|

$ |

0.39 |

|

$ |

0.61 |

|

$ |

0.56 |

|

Adjusted FFO attributable to common stockholders per diluted share |

|

$ |

0.43 |

|

$ |

0.39 |

|

$ |

0.65 |

|

$ |

0.55 |

|

Basic weighted average shares outstanding |

|

|

207,577 |

|

|

182,604 |

|

|

207,091 |

|

|

181,836 |

|

Shares associated with unvested restricted stock awards |

|

|

183 |

|

|

475 |

|

|

291 |

|

|

473 |

|

Diluted weighted average shares outstanding |

|

|

207,760 |

|

|

183,079 |

|

|

207,382 |

|

|

182,309 |

|

CORPORATE FINANCIAL INFORMATION |

|

|

Page 14 |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

Supplemental Financial Information |

Pro Forma Consolidated Statements of Operations

Q2 2015 – Q3 2014, FY 2014

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Three Months Ended (1) |

Year Ended (1) |

|||||||||||||||||

|

(Unaudited and in thousands) |

June 30, |

March 31, |

Dec. 31, |

Sept. 30, |

Dec. 31, |

|||||||||||||

|

2015 |

2015 |

2014 |

2014 |

2014 |

||||||||||||||

|

Revenues |

||||||||||||||||||

|

Room |

$ |

239,678 |

$ |

193,291 |

$ |

204,208 |

$ |

224,926 |

$ |

833,383 | ||||||||

|

Food and beverage |

79,265 | 72,184 | 71,190 | 69,134 | 284,519 | |||||||||||||

|

Other operating |

20,324 | 18,910 | 18,719 | 19,918 | 73,938 | |||||||||||||

|

Total revenues |

339,267 | 284,385 | 294,117 | 313,978 | 1,191,840 | |||||||||||||

|

Operating Expenses |

||||||||||||||||||

|

Room |

57,568 | 53,842 | 54,513 | 57,064 | 218,198 | |||||||||||||

|

Food and beverage |

52,812 | 50,219 | 51,242 | 50,575 | 204,148 | |||||||||||||

|

Other expenses |

111,738 | 107,696 | 105,046 | 107,480 | 416,278 | |||||||||||||

|

Corporate overhead |

6,923 | 14,253 | 7,329 | 7,177 | 28,739 | |||||||||||||

|

Depreciation and amortization |

40,873 | 40,707 | 40,257 | 40,000 | 160,105 | |||||||||||||

|

Total operating expenses |

269,914 | 266,717 | 258,387 | 262,296 | 1,027,468 | |||||||||||||

|

Operating Income |

69,353 | 17,668 | 35,730 | 51,682 | 164,372 | |||||||||||||

|

Interest and other income |

1,828 | 946 | 891 | 981 | 3,479 | |||||||||||||

|

Interest expense |

(17,289) | (17,326) | (17,649) | (18,052) | (72,315) | |||||||||||||

|

Loss on extinguishment of debt |

(2) |

— |

(4,107) | (531) | (4,638) | |||||||||||||

|

Income before income taxes and discontinued operations |

53,890 | 1,288 | 14,865 | 34,080 | 90,898 | |||||||||||||

|

Income tax (provision) benefit |

(233) | (85) | (258) | 413 | (179) | |||||||||||||

|

Income from continuing operations |

53,657 | 1,203 | 14,607 | 34,493 | 90,719 | |||||||||||||

|

Loss from discontinued operations |

— |

— |

(350) |

— |

4,849 | |||||||||||||

|

Net Income |

$ |

53,657 |

$ |

1,203 |

$ |

14,257 |

$ |

34,493 |

$ |

95,568 | ||||||||

|

Adjusted EBITDA (2) |

$ |

110,368 |

$ |

65,709 |

$ |

77,838 |

$ |

92,270 |

$ |

324,973 | ||||||||

|

(1) |

Includes the Company's ownership results and prior ownership results for the 30 hotel comparable portfolio held for investment by the Company as of June 30, 2015. Includes the reduction of ground lease expense on the Fairmont Newport Beach due to the Company's land acquisition in June 2014, along with prior ownership results for the Wailea Beach Marriott Resort & Spa acquired July 17, 2014. The Company obtained prior ownership information from the Wailea Beach Marriott Resort & Spa's previous owner during the due diligence period before acquiring the hotel. The Company performed a limited review of the information as part of its analysis of the acquisition. Data for each 2014 period presented has been adjusted for changes stipulated by the industry's Uniform System of Accounts for the Lodging Industry, Eleventh Revised Edition, which became effective January 1, 2015. |

|

(2) |

The Adjusted EBITDA reconciliation for Q2 2015 can be found on page 13 of this supplemental package. The Adjusted EBITDA reconciliation for Q1 2015 can be found in the supplemental package furnished on Form 8-K to the SEC on May 4, 2015. The Adjusted EBITDA reconciliations for Q4 2014 and full year 2014 can be found in the supplemental package furnished on Form 8-K to the SEC on February 17, 2015. The Adjusted EBITDA reconciliation for Q3 2014 can be found in the supplemental package furnished on Form 8-K to the SEC on November 3, 2014. |

|

CORPORATE FINANCIAL INFORMATION |

|

|

Page 15 |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

Supplemental Financial Information |

|

EARNINGS GUIDANCE |

|

|

Page 16 |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

Supplemental Financial Information |

Earnings Guidance for Q3 and FY 2015

The Company is providing guidance at this time, but does not undertake to make updates for any unanticipated developments in its business or changes in the operating environment. Achievement of the anticipated results is subject to risks and uncertainties, including those disclosed in the Company’s filings with the Securities and Exchange Commission. The Company’s guidance does not take into account the impact of any unannounced hotel acquisitions, dispositions, re-brandings, management changes, transition costs, early lease termination costs, prior year property tax assessments and/or credits, debt repurchases or unannounced financings during 2015. The guidance presented takes into account various accounting changes as stipulated by the industry’s Uniform System of Accounts for the Lodging Industry, Eleventh Revised Edition (the “USALI Eleventh Revised Edition”), which became effective in January 2015. Guidance for 2015 Comparable Hotel RevPAR and Comparable Hotel Adjusted EBITDA Margins has been presented to reflect growth rates compared to prior year as if these 2014 statistics included the USALI Eleventh Revised Edition changes. Actual Comparable Hotel RevPAR and Comparable Hotel Adjusted EBITDA Margin change from prior year will differ slightly. The Company is presenting 2014 Comparable Hotel RevPAR and Comparable Hotel Adjusted EBITDA Margins on an as reported basis and on a pro forma basis, which will include the USALI Eleventh Revised Edition changes.

For the third quarter of 2015, the Company expects:

|

Metric |

Quarter Ended September 30, 2015 Guidance |

|

Comparable Hotel RevPAR Growth |

+ 3.0% - 4.0% |

|

Net Income ($ millions) |

$33 - $37 |

|

Adjusted EBITDA ($ millions) |

$90 - $94 |

|

Adjusted FFO Attributable to Common Stockholders ($ millions) |

$70 - $74 |

|

Adjusted FFO Attributable to Common Stockholders per Diluted Share |

$0.34 - $0.35 |

|

Diluted Weighted Average Shares Outstanding |

207,900,000 |

For the full year of 2015, the Company expects:

|

Metric |

Prior Full Year 2015 Guidance (1) |

Adjustments (2) |

Adjusted Prior Full Year 2015 Guidance |

Current Full Year 2015 Guidance |

Change in Full Year 2015 Guidance Midpoint |

|

Comparable Hotel RevPAR Growth |

+ 5.0% - 7.0% |

̶ |

+ 5.0% - 7.0% |

+ 5.0% - 6.5% |

-0.2% |

|

Net Income ($ millions) |

$109 - $123 |

-$3.2 |

$106 - $120 |

$110 - $121 |

+$2.5 |

|

Adjusted EBITDA ($ millions) |

$344 - $356 |

-$3.2 |

$341 - $353 |

$347 - $356 |

+$4.5 |

|

Adjusted FFO Attributable to Common Stockholders ($ millions) |

$262 - $274 |

-$3.2 |

$259 - $271 |

$265 - $274 |

+$4.5 |

|

Adjusted FFO Attributable to Common Stockholders per Diluted Share |

$1.26 - $1.32 |

-$0.02 |

$1.24 - $1.30 |

$1.28 - $1.32 |

+$0.03 |

|

Diluted Weighted Average Shares Outstanding |

207,700,000 |

̶ |

207,700,000 |

207,700,000 |

̶ |

|

(1) |

Reflects guidance presented on May 4, 2015. |

|

(2) |

Adjustments include the effects of the following: the sale of the Preferred Equity Investment in July 2015; the deferral of the $2 million Wailea Beach Marriott Resort & Spa guarantee payment from 2015 as this amount will now be paid in 2016, along with an additional $3 million. |

|

EARNINGS GUIDANCE |

|

|

Page 17 |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

Supplemental Financial Information |

Earnings Guidance for Q3 and FY 2015

Third quarter and full year 2015 guidance are based in part on the following assumptions:

|

· |

Full year Comparable Hotel Adjusted EBITDA Margin (as compared to 2014 adjusted for the USALI Eleventh Revised Edition) expansion of approximately 75 to 125 basis points, an increase of 25 basis points to the midpoint of the prior range. |

|

· |

Full year corporate overhead expense (excluding stock amortization and one-time expenses related to acquisition closing costs and severance charges) of approximately $21.5 million to $22.5 million, a reduction of $1.0 million to the midpoint of the prior range. |

|

· |

Deferral of $2 million of the Wailea Beach Marriott Resort & Spa guarantee income from Q4 2015 to 2016. |

|

· |

Full year interest expense of approximately $66 million to $67 million, including approximately $3 million in amortization of deferred financing fees, and excluding approximately $1.4 million of capital lease obligation interest. |

|

· |

Full year expense of approximately $0.7 million in one-time costs related to the Boston Park Plaza retail, meeting space and lobby relaunch, and $0.3 million in one-time costs related to an early lease termination at the Boston Park Plaza. |

|

· |

Full year hotel revenue disruption of $2.0 million to $3.0 million related to cancellations resulting from civil unrest in Baltimore, Maryland. The Company is pursuing a business interruption insurance claim for a portion of the disruption but may or may not receive any payments, and has not included any potential reimbursement in its current guidance. |

|

· |

Full year preferred dividends of $9.2 million for the Series D cumulative redeemable preferred stock. |

|

· |

Sale of the Preferred Equity Investment in July 2015, eliminating approximately $0.5 million and $0.7 million of interest income in Q3 2015 and Q4 2015, respectively, or $1.2 million for the second half of 2015. |

|

EARNINGS GUIDANCE |

|

|

Page 18 |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

Supplemental Financial Information |

Reconciliation of Net Income to Adjusted EBITDA and Adjusted FFO Attributable to Common Stockholders

Q3 and FY 2015

Reconciliation of Net Income to Adjusted EBITDA

|

Quarter Ended |

Year Ended |

|||||||||||

|

September 30, 2015 |

December 31, 2015 |

|||||||||||

|

(In thousands, except per share data) |

Low |

High |

Low |

High |

||||||||

|

Net income |

$ |

32,700 |

$ |

37,000 |

$ |

109,700 |

$ |

120,600 | ||||

|

Depreciation and amortization |

41,400 | 41,400 | 164,400 | 164,400 | ||||||||

|

Amortization of lease intangibles |

1,000 | 1,000 | 4,100 | 4,100 | ||||||||

|

Interest expense |

16,300 | 16,500 | 67,200 | 67,900 | ||||||||

|

Income tax provision |

400 | 400 | 1,000 | 1,000 | ||||||||

|

Non-controlling interests |

(3,100) | (3,500) | (11,800) | (14,400) | ||||||||

|

Amortization of deferred stock compensation |

1,200 | 1,200 | 7,100 | 7,100 | ||||||||

|

Non-cash straightline lease expense |

400 | 400 | 1,400 | 1,400 | ||||||||

|

Capital lease obligation interest - cash ground rent |

(400) | (400) | (1,400) | (1,400) | ||||||||

|

Gain on redemption of note receivable |

— |

— |

(900) | (900) | ||||||||

|

Prior year property tax adjustments, net |

— |

— |

(100) | (100) | ||||||||

|

Boston Park Plaza relaunch costs |

— |

— |

700 | 700 | ||||||||

|

Lease termination costs |

— |

— |

300 | 300 | ||||||||

|

Costs associated with CEO severance |

— |

— |

5,300 | 5,300 | ||||||||

|

Adjusted EBITDA |

$ |

89,900 |

$ |

94,000 |

$ |

347,000 |

$ |

356,000 | ||||

Reconciliation of Net Income to Adjusted FFO Attributable to Common Stockholders

|

Net income |

|

$ |

32,700 |

|

$ |

37,000 |

|

$ |

109,700 |

|

$ |

120,600 |

|

Preferred stock dividends |

|

|

(2,300) |

|

|

(2,300) |

|

|

(9,200) |

|

|

(9,200) |

|

Real estate depreciation and amortization |

|

|

40,800 |

|

|

40,800 |

|

|

162,400 |

|

|

162,400 |

|

Amortization of lease intangibles |

|

|

1,000 |

|

|

1,000 |

|

|

4,100 |

|

|

4,100 |

|

Non-controlling interests |

|

|

(2,800) |

|

|

(3,200) |

|

|

(10,400) |

|

|

(12,700) |

|

Write-off of deferred financing fees |

|

|

— |

|

|

— |

|

|

500 |

|

|

500 |

|

Non-cash straightline lease expense |

|

|

400 |

|

|

400 |

|

|

1,400 |

|

|

1,400 |

|

Gain on redemption of note receivable |

|

|

— |

|

|

— |

|

|

(900) |

|

|

(900) |

|

Prior year property tax adjustments, net |

|

|

— |

|

|

— |

|

|

(100) |

|

|

(100) |

|

Boston Park Plaza relaunch costs |

|

|

— |

|

|

— |

|

|

700 |

|

|

700 |

|

Lease termination costs |

|

|

— |

|

|

— |

|

|

300 |

|

|

300 |

|

Costs associated with CEO severance |

|

|

— |

|

|

— |

|

|

5,300 |

|

|

5,300 |

|

Amortization of deferred stock compensation associated with CEO severance |

|

|

— |

|

|

— |

|

|

1,600 |

|

|

1,600 |

|

Adjusted FFO attributable to common stockholders |

|

$ |

69,800 |

|

$ |

73,700 |

|

$ |

265,400 |

|

$ |

274,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Adjusted FFO attributable to common stockholders per diluted share |

|

$ |

0.34 |

|

$ |

0.35 |

|

$ |

1.28 |

|

$ |

1.32 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Diluted weighted average shares outstanding |

|

|

207,900 |

|

|

207,900 |

|

|

207,700 |

|

|

207,700 |

|

EARNINGS GUIDANCE |

|

|

Page 19 |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

Supplemental Financial Information |

|

CAPITALIZATION |

|

|

Page 20 |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

Supplemental Financial Information |

Comparative Capitalization

Q2 2015 – Q2 2014

|

|

|

|

June 30, |

|

|

March 31, |

|

|

Dec. 31, |

|

|

Sept. 30, |

|

|

June 30, |

|

|

(In thousands, except per share data) |

|

|

2015 |

|

|

2015 |

|

|

2014 |

|

|

2014 |

|

|

2014 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Common Share Price & Dividends |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

At the end of the quarter |

|

$ |

15.01 |

|

$ |

16.67 |

|

$ |

16.51 |

|

$ |

13.82 |

|

$ |

14.93 |

|

|

High during quarter ended |

|

$ |

17.08 |

|

$ |

17.98 |

|

$ |

17.17 |

|

$ |

15.17 |

|

$ |

15.25 |

|

|

Low during quarter ended |

|

$ |

14.63 |

|

$ |

16.18 |

|

$ |

13.42 |

|

$ |

13.71 |

|

$ |

13.22 |

|

|

Common dividends per share (1) |

|

$ |

0.05 |

|

$ |

0.05 |

|

$ |

0.36 |

|

$ |

0.05 |

|

$ |

0.05 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Common Shares & Units |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Common shares outstanding (2) |

|

|

208,697 |

|

|

208,686 |

|

|

206,650 |

|

|

205,397 |

|

|

205,432 |

|

|

Units outstanding |

|

|

— |

|

|

— |

|

|

— |

|

|

— |

|

|

— |

|

|

Total common shares and units outstanding |

|

|

208,697 |

|

|

208,686 |

|

|

206,650 |

|

|

205,397 |

|

|

205,432 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Capitalization |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Market value of common equity |

|

$ |

3,132,541 |

|

$ |

3,478,793 |

|

$ |

3,411,792 |

|

$ |

2,838,583 |

|

$ |

3,067,094 |

|

|

Liquidation value of preferred equity - Series D |

|

|

115,000 |

|

|

115,000 |

|

|

115,000 |

|

|

115,000 |

|

|

115,000 |

|

|

Consolidated debt (3) |

|

|

1,318,657 |

|

|

1,324,078 |

|

|

1,429,292 |

|

|

1,386,492 |

|

|

1,392,422 |

|

|

Consolidated total capitalization |

|

|

4,566,198 |

|

|

4,917,871 |

|

|

4,956,084 |

|

|

4,340,075 |

|

|

4,574,516 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Non-controlling interest in consolidated debt |

|

|

(56,718) |

|

|

(56,897) |

|

|

(57,074) |

|

|

(57,248) |

|

|

(57,435) |

|

|

Pro rata total capitalization |

|

$ |

4,509,480 |

|

$ |

4,860,974 |

|

$ |

4,899,010 |

|

$ |

4,282,827 |

|

$ |

4,517,081 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Consolidated debt to total capitalization |

|

|

28.9 |

% |

|

26.9 |

% |

|

28.8 |

% |

|

31.9 |

% |

|

30.4 |

% |

|

Pro rata debt to pro rata total capitalization |

|

|

28.0 |

% |

|

26.1 |

% |

|

28.0 |

% |

|

31.0 |

% |

|

29.6 |

% |

|

Consolidated debt and preferred equity to total capitalization |

|

|

31.4 |

% |

|

29.3 |

% |

|

31.2 |

% |

|

34.6 |

% |

|

33.0 |

% |

|

Pro rata debt and preferred equity to total capitalization |

|

|

30.5 |

% |

|

28.4 |

% |

|

30.4 |

% |

|

33.7 |

% |

|

32.1 |

% |

|

(1) |

Fourth quarter 2014 dividends were paid in a combination of cash and shares of the Company's common stock, pursuant to elections by individual stockholders. |

|

(2) |

Reflects shares outstanding at respective dates. Common shares outstanding at June 30, 2014 includes the effects of the Company's direct issuance of 4,034,970 shares to the seller of the Wailea Beach Marriott Resort & Spa in July 2014. |

|

(3) |

First quarter 2015 includes the effects of the Company's May 1, 2015 repayment of debt secured by four of its hotels: the Marriott Houston, the Marriott Park City, the Marriott Philadelphia and the Marriott Tysons Corner. |

|

CAPITALIZATION |

|

|

Page 21 |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

Supplemental Financial Information |

Consolidated Debt Summary Schedule

|

(In thousands) |

|

|

|

Interest Rate / |

|

Maturity |

|

|

June 30, 2015 |

|

|

Balance At |

|

Debt |

|

Collateral |

|

Spread |

|

Date |

|

|

Balance |

|

|

Maturity |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fixed Rate Debt |

|

|

|

|

|

|

|

|

|

|

|

|

|

Secured Mortgage Debt |

|

Renaissance Harborplace |

|

5.13% |

|

01/01/2016 |

|

$ |

87,081 |

|

$ |

85,227 |

|

Secured Mortgage Debt |

|

Hilton North Houston |

|

5.66% |

|

03/11/2016 |

|

|

30,965 |

|

|

30,579 |

|

Secured Mortgage Debt |

|

Renaissance Orlando at SeaWorld® |

|

5.52% |

|

07/01/2016 |

|

|

74,779 |

|

|

72,418 |

|

Secured Mortgage Debt |

|

Embassy Suites Chicago |

|

5.58% |

|

03/01/2017 |

|

|

68,666 |

|

|

65,756 |

|

Secured Mortgage Debt |

|

Marriott Boston Long Wharf |

|

5.58% |

|

04/11/2017 |

|

|

176,000 |

|

|

176,000 |

|

Secured Mortgage Debt |

|

Boston Park Plaza |

|

4.40% |

|

02/01/2018 |

|

|

115,416 |

|

|

109,813 |

|

Secured Mortgage Debt |

|

Hilton Times Square |

|

4.97% |

|

11/01/2020 |

|

|

85,931 |

|

|

76,145 |

|

Secured Mortgage Debt |

|

Renaissance Washington DC |

|

5.95% |

|

05/01/2021 |

|

|

123,100 |

|

|

106,855 |

|

Secured Mortgage Debt |

|

JW Marriott New Orleans |

|

4.15% |

|

12/11/2024 |

|

|

89,257 |

|

|

72,071 |

|

Secured Mortgage Debt |

|

Embassy Suites La Jolla |

|

4.12% |

|

01/06/2025 |

|

|

64,546 |

|

|

51,987 |

|

Total Fixed Rate Debt |

|

|

|

|

|

|

|

|

915,741 |

|

|

846,851 |

|

Secured Mortgage Debt |

|

Doubletree Guest Suites Times Square |

|

L + 3.25% |

|

10/07/2018 |

|

|

176,043 |

|

|

167,738 |

|

Secured Mortgage Debt |

|

Hilton San Diego Bayfront |

|

L + 2.25% |

|

08/08/2019 |

|

|

226,873 |

|

|

213,513 |

|

Credit Facility |

|

Unsecured |

|

L + 1.55% - 2.30% |

|

04/02/2019 |

|

|

— |

|

|

— |

|

Total Variable Rate Debt |

|

|

|

|

|

|

|

|

402,916 |

|

|

381,251 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TOTAL CONSOLIDATED DEBT |

|

|

|

|

|

|

|

$ |

1,318,657 |

|

$ |

1,228,102 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Preferred Stock |

|

|

|

|

|

|

|

|

|

|

|

|

|

Series D cumulative redeemable preferred |

|

|

|

8.00% |

|

perpetual |

|

$ |

115,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Debt Statistics |

|

|

|

|

|

|

|

|

|

|

|

|

|

% Fixed Rate Debt |

|

|

|

|

|

|

|

|

69.4 |

% |

|

|

|

% Floating Rate Debt |

|

|

|

|

|

|

|

|

30.6 |

% |

|

|

|

Average Interest Rate (1) |

|

|

|

|

|

|

|

|

4.4 |

% |

|

|

|

Weighted Average Maturity of Debt |

|

|

|

|

|

|

|

|

3.8 years |

|

|

|

|

(1) |

Average Interest Rate on variable-rate debt obligations is calculated based on the variable rates at June 30, 2015, and includes the effect of the Company's interest rate derivative agreements. |

|

CAPITALIZATION |

|

|

Page 22 |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

Supplemental Financial Information |

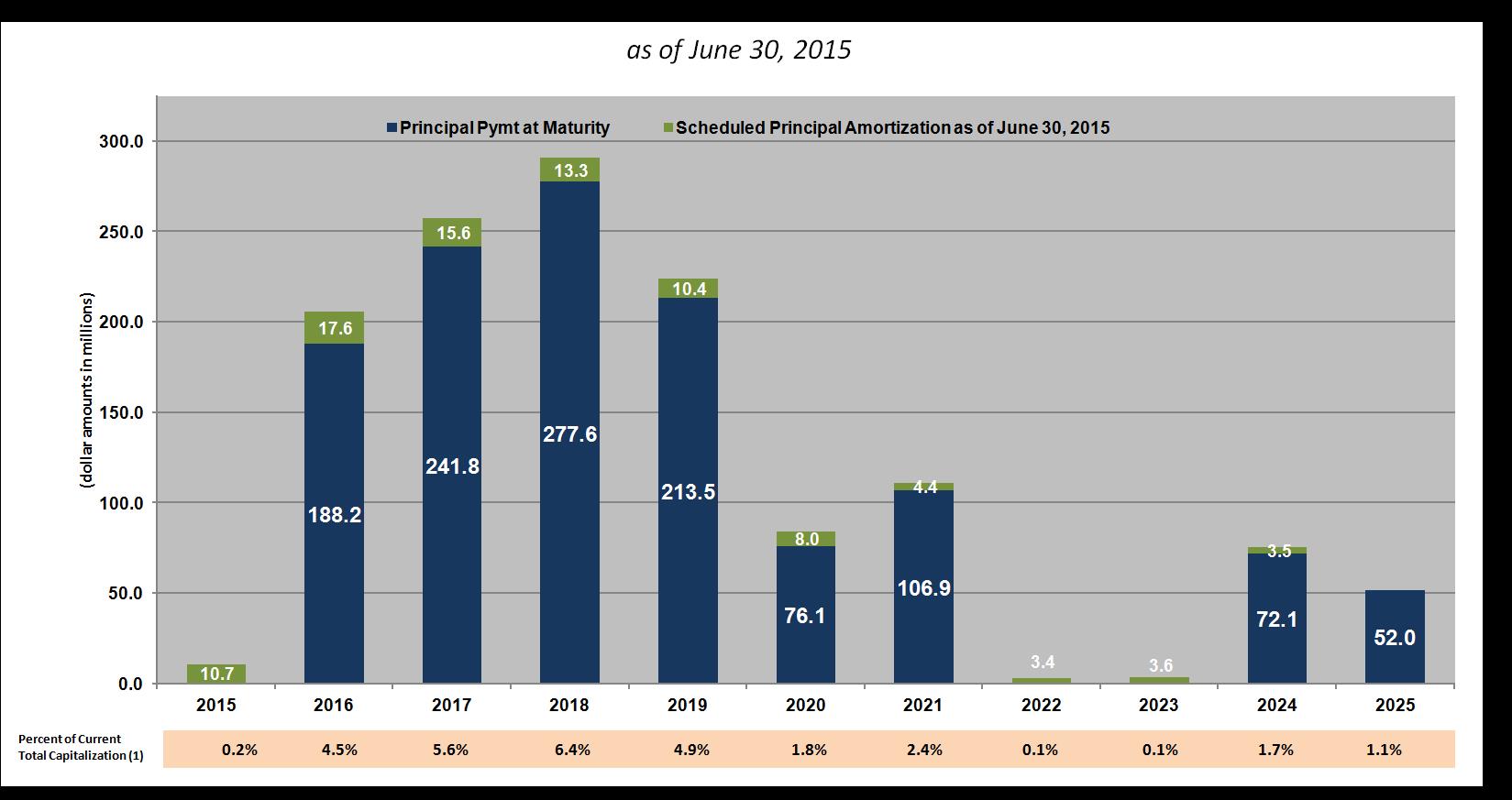

Consolidated Amortization and Debt Maturity Schedule

|

(1) |

Percent of Current Total Capitalization is calculated by dividing the sum of scheduled principal amortization and maturity payments by the June 30, 2015 consolidated total capitalization as presented on page 21. |

|

CAPITALIZATION |

|

|

Page 23 |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

Supplemental Financial Information |

|

PROPERTY LEVEL DATA |

|

|

Page 24 |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

Supplemental Financial Information |

Property-Level Data

|

Hotel |

|

Location |

|

Brand |

|

Number of |

|

% of Total |

|

Ownership |

|

Interest |

|

Leasehold |

|

Year Acquired |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

| 1 |

|

Hilton San Diego Bayfront |

|

California |

|

Hilton |

|

1,190 |

|

8.31% |

|

75% |

|

Leasehold |

|

2071 |

|

2011 |

||

| 2 |

|

Boston Park Plaza |

|

Massachusetts |

|

Independent |

|

1,054 |

|

7.36% |

|

100% |

|

Fee Simple |

|

|

|

2013 |

||

| 3 |

|

Renaissance Washington DC |

|

Washington DC |

|

Marriott |

|

807 |

|

5.64% |

|

100% |

|

Fee Simple |

|

|

|

2005 |

||

| 4 |

|

Hyatt Regency San Francisco |

|

California |

|

Hyatt |

|

804 |

|

5.62% |

|

100% |

|

Fee Simple |

|

|

|

2013 |

||

| 5 |

|

Renaissance Orlando at SeaWorld® (2) |

|

Florida |

|

Marriott |

|

781 |

|

5.46% |

|

100% |

|

Fee Simple |

|

|

|

2005 |

||

| 6 |

|

Renaissance Harborplace |

|

Maryland |

|

Marriott |

|

622 |

|

4.35% |

|

100% |

|

Leasehold |

|

2085 |

|

2005 |

||

| 7 |

|

Wailea Beach Marriott Resort & Spa |

|

|

Hawaii |

|

Marriott |

|

543 |

|

3.79% |

|

100% |

|

Fee Simple |

|

|

|

2014 |

|

| 8 |

|

Renaissance Los Angeles Airport |

|

California |

|

Marriott |

|

501 |

|

3.50% |

|

100% |

|

Fee Simple |

|

|

|

2007 |

||

| 9 |

|

JW Marriott New Orleans (3) |

|

Louisiana |

|

Marriott |

|

501 |

|

3.50% |

|

100% |

|

Leasehold |

|

2081 |

|

2011 |

||

| 10 |

|

Hilton North Houston |

|

Texas |

|

Hilton |

|

480 |

|

3.35% |

|

100% |

|

Fee Simple |

|

|

|

2002 |

||

| 11 |

|

Doubletree Guest Suites Times Square |

|

New York |

|

Hilton |

|

468 |

|

3.27% |

|

100% |

|

Leasehold |

|

2127 |

|

2011 |

||

| 12 |

|

Marriott Quincy |

|

Massachusetts |

|

Marriott |

|

464 |

|

3.24% |

|

100% |

|

Fee Simple |

|

|

|

2007 |

||

| 13 |

|

Hilton Times Square |

|

New York |

|

Hilton |

|

460 |

|

3.21% |

|

100% |

|

Leasehold |

|

2091 |

|

2006 |

||

| 14 |

|

Fairmont Newport Beach |

|

California |

|

Fairmont |

|

444 |

|

3.10% |

|

100% |

|

Fee Simple |

|

|

|

2005 |

||

| 15 |

|

Hyatt Chicago Magnificent Mile |

|

Illinois |

|

Hyatt |

|

419 |

|

2.93% |

|

100% |

|

Leasehold |

|

2097 |

|

2012 |

||

| 16 |

|

Marriott Boston Long Wharf |

|

Massachusetts |

|

Marriott |

|

412 |

|

2.88% |

|

100% |

|

Fee Simple |

|

|

|

2007 |

||

| 17 |

|

Hyatt Regency Newport Beach |

|

California |

|

Hyatt |

|

407 |

|

2.84% |

|

100% |

|

Leasehold |

|

2048 |

|

2002 |

||

| 18 |

|

Marriott Tysons Corner |

|

Virginia |

|

Marriott |

|

396 |

|

2.77% |

|

100% |

|

Fee Simple |

|

|

|

2002 |

||

| 19 |

|

Marriott Houston |

|

Texas |

|

Marriott |

|

390 |

|

2.72% |

|

100% |

|

Fee Simple |

|

|

|

2002 |

||

| 20 |

|

Renaissance Long Beach |

|

California |

|

Marriott |

|

374 |

|

2.61% |

|

100% |

|

Fee Simple |

|

|

|

2005 |