Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - COCA-COLA EUROPEAN PARTNERS US, LLC | d27156d8k.htm |

| EX-99.2 - EXHIBIT 99.2 - COCA-COLA EUROPEAN PARTNERS US, LLC | d27156dex992.htm |

Presenting Coca-Cola European Partners August 6, 2015 Exhibit 99.1 |

2 Included in this presentation are forward-looking management comments and other statements that reflect management’s current outlook for future periods. Included in this presentation are forward-looking management comments and other statements that reflect management’s current outlook for future periods. As always, these expectations are based on currently available competitive, financial, and economic data along with our current operating plans and are subject to risks and uncertainties that could cause actual results to differ materially from the results contemplated by the forward- looking statements. The forward-looking statements in this presentation should be read in conjunction with the risks and uncertainties discussed in our filings with the Securities and Exchange Commission (“SEC”), including our most recent Form 10-K and other SEC filings. |

3 COCA-COLA EUROPEAN PARTNERS OVERVIEW COCA-COLA EUROPEAN PARTNERS OVERVIEW COCA-COLA EUROPEAN PARTNERS BACKGROUND COCA-COLA EUROPEAN PARTNERS BACKGROUND TRANSACTION HIGHLIGHTS TRANSACTION HIGHLIGHTS |

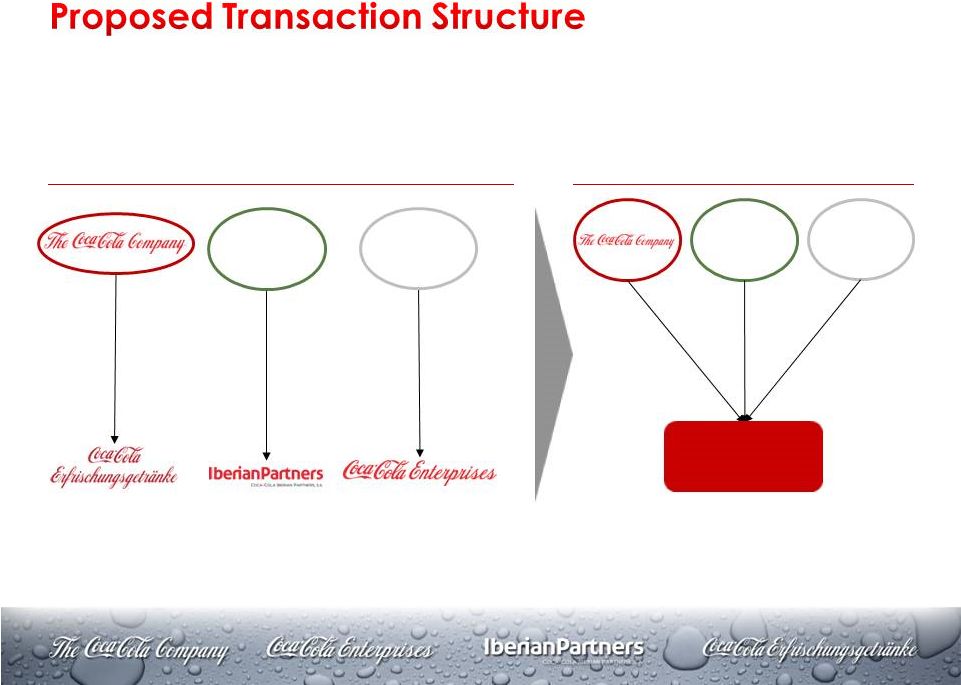

4 • Combines bottling operations of Coca-Cola Enterprises (CCE), Coca-Cola Iberian Partners (CCIP), and Coca-Cola Erfrischungsgetränke (CCEAG) into a new Western European bottler, Coca-Cola European Partners (CCEP), serving over 300 million consumers across 13 countries • Combined company pro forma 2015 expected annual net revenues of $12.6 billion and EBITDA of $2.1 billion (before synergies) • CCE shareowners to own 48%, CCIP shareowners to own 34%, and The Coca-Cola Company (TCCC) to own 18% of CCEP on a fully diluted basis • CCE shareowners to receive one share of CCEP and a cash payment of $14.50 per share of CCE • CCEP will be headquartered and incorporated in the United Kingdom and publicly traded on the Euronext Amsterdam, NYSE, and Madrid Stock Exchange * Owned by controlling shareowner of CCIP, expected to be contributed to CCIP prior to closing

Norway Sweden Netherlands Germany France Great Britain Iceland* Spain Portugal Andorra Luxembourg Monaco Belgium |

5 • Enhances alignment of the Coca-Cola system (TCCS) to compete more effectively across Western Europe with world-class production, sales, and

distribution platforms

• Strategically optimizes TCCS to drive growth in the Western European

Non-Alcoholic Ready-To-Drink (NARTD) market

• Improves service to customers and consumers through a more consistent strategy for product and brand development across Western Europe • Increases scale and flexibility with a broader geographic footprint • Expected to realize annual run-rate pre-tax savings of approximately $350 to

$375 million within 3 years of closing

• Leverages best practices and strong leadership from CCE, CCIP, and CCEAG |

6 • CCE shareowners to receive one share of CCEP and a cash payment of $14.50 per share of CCE • Participation in long-term upside from ownership in CCEP • Expected pre-tax, run-rate savings of approximately $350 to $375 million

within 3 years of closing

• Solid earnings growth and robust cash flow generation • Continued strong focus on driving shareowner value • CEO: John Brock, Chairman and CEO of CCE • COO: Damian Gammell, CEO of Anadolu Efes • CFO: Nik Jhangiani, CFO of CCE • CIO*: Victor Rufart, General Manager of CCIP Substantial Value Creation Proven Management Team * Chief Integration Officer |

7 • Committed to investment grade capital structure for long-term sustainability

• Transaction financed with ~$3.3 billion funded by the new company using newly issued debt • Expected to have 2015 pro forma net debt to EBITDA ratio of ~3.5x; given

anticipated cash flows, expect to de-lever to ~2.5x by year-end

2017 •

Intends to operate within a 2.5x to 3.0x net debt ratio longer term • CCEP to target attractive total return to shareowners • Expected dividend payout of 30% to 40% of net income over time • Potential for excess cash return to shareowners to resume once appropriate

net leverage reached

• Transaction expected to close during Q2 2016 • Closing subject to CCE shareowner, regulatory, and other approvals Capital Structure Capital Return Expected Timing |

8 COCA-COLA EUROPEAN PARTNERS OVERVIEW COCA-COLA EUROPEAN PARTNERS BACKGROUND TRANSACTION HIGHLIGHTS |

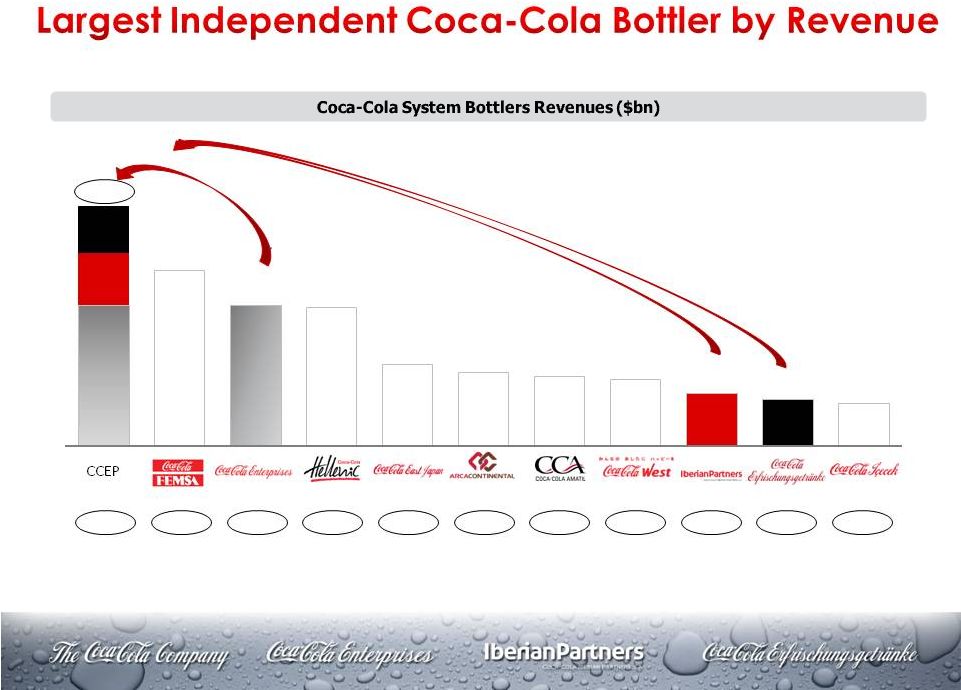

9 • Creates the largest independent Coca-Cola bottler based on net revenues • Combines bottling operations of CCE, CCIP, and CCEAG into a new Western European bottler, serving over 300 million consumers across 13 countries • Strategically positions CCEP to drive growth in the Western European NARTD market • Builds on each bottler’s capabilities to create more efficient and effective

operations in their respective markets

• Expected to realize annual run-rate pre-tax savings of approximately $350 to $375

million within 3 years of closing |

10 Today New Structure CCIP HoldCo Public 100% 100% 100% 18% 34% 48% + $14.50/share in cash (~$3.3bn) for CCE Shareowners Family shareholders CCE Shareholders Coca-Cola European Partners • CCE, CCIP, and CCEAG will merge their operations across Europe under a new UK company, CCEP

• CCE shareowners to own 48%, CCIP shareowners to own 34%, and TCCC to own 18% of CCEP on a fully

diluted basis Private Incorporated in Germany Private Incorporated in Spain NYSE: CCE Incorporated in the US Euronext Amsterdam

(ASX) New York Stock Exchange (NYSE) Madrid Stock Exchange Incorporated in the UK |

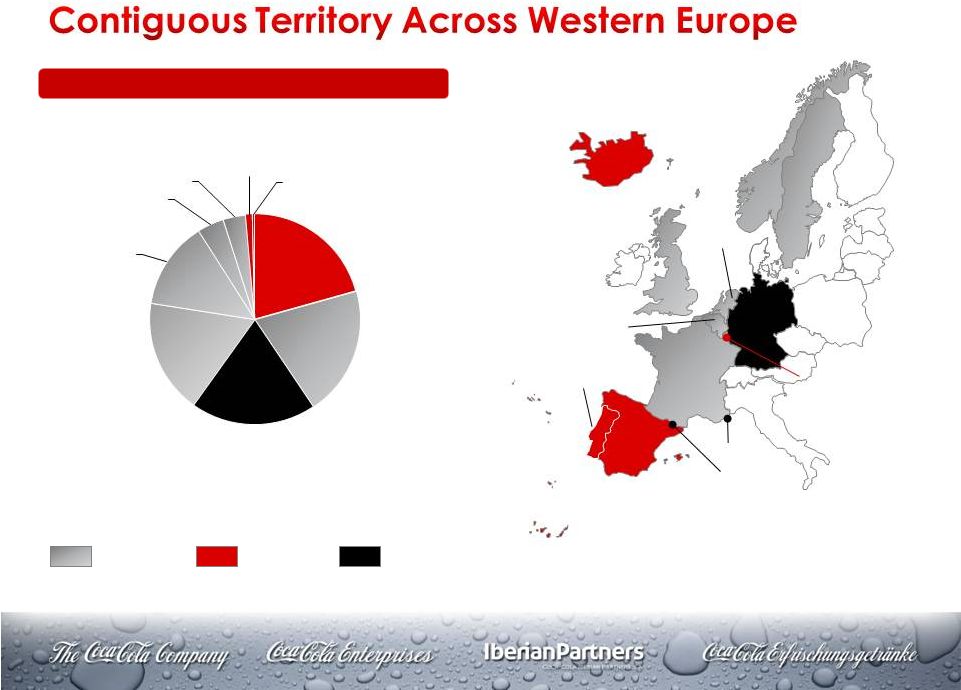

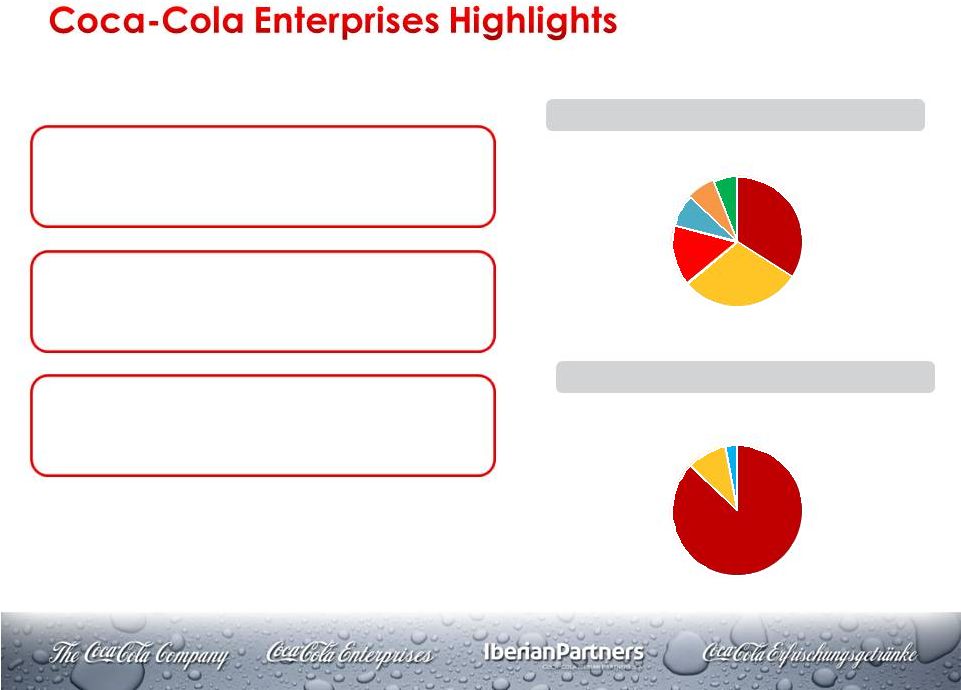

11 Pro Forma 2014 Net Revenue of $12.4B CCE CCEAG CCIP Norway Sweden Netherlands Germany France Great Britain Iceland Spain Portugal Andorra Luxembourg Monaco Belgium Note: Financials based on exchange rates of 1.12 $/€, 1.57 $/£, 0.14 $/NOK and 0.12 $/SEK

Great Britain 20% Germany 19% France 18% BeNeLux 13% Norway 4% Sweden 4% Portugal 1% Iceland <1% Spain 21% |

12 Volume (bn unit cases) 2.5 3.4 1.3 2.0 1.3 0.2 0.6 0.5 1.1 0.3 0.7 $12.4 Source: 2014 company filings, FactSet; numbers are rounded |

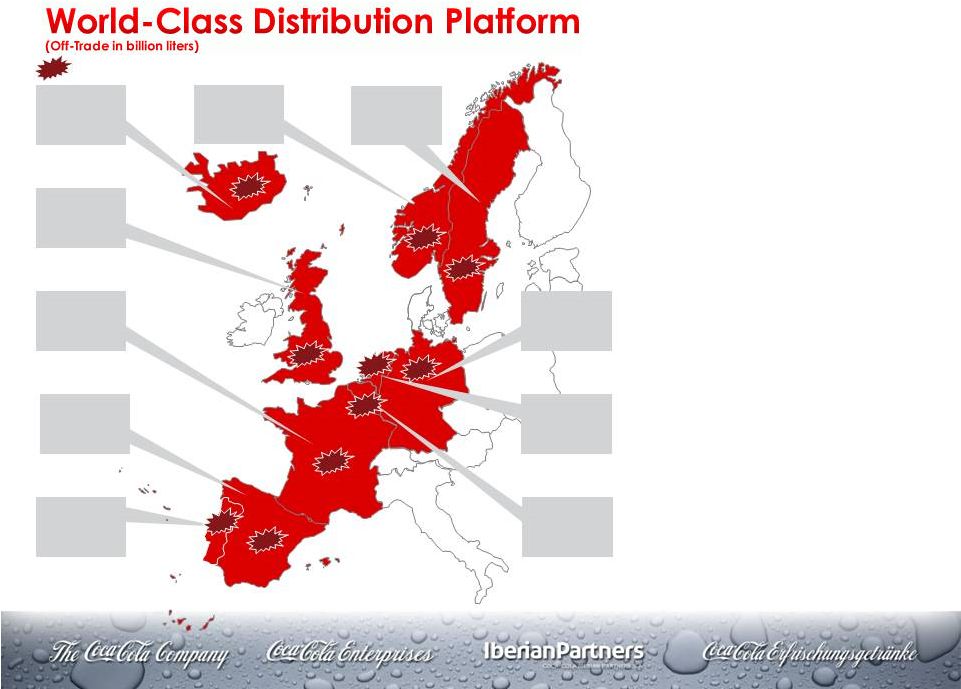

• Serves 13 countries in Western Europe • Consumer population base of over 300 million • Over 50 bottling plants and ~27,000 associates • Leading position in every country Source: Euromonitor (a) Does not include Luxembourg. Portugal Pop: 11m Soft Drinks: 1.4bn TCCC: 0.1bn Norway Pop: 5m Soft Drinks: 0.7bn TCCC: 0.2bn NARTD Market Position # #1 #1 Iceland Pop: 0.3m Sweden Pop: 10m Soft Drinks: 1.1bn TCCC: 0.3bn Great Britain Pop: 64m Soft Drinks: 8.7bn TCCC: 1.9bn France Pop: 65m Soft Drinks: 12.6bn TCCC: 1.4bn Spain Pop: 47m Soft Drinks: 9.4bn TCCC: 1.8bn #1 Germany Pop: 84m Soft Drinks: 20.0bn TCCC: 2.1bn The Netherlands Pop: 17m Soft Drinks: 2.3bn TCCC: 0.4bn Belgium/Lux. Pop: 12m Soft Drinks: 2.5bn (a) TCCC: 0.6bn #1 #1 #1 #1 #1 #1 #1 13 |

14 Leading Coca-Cola System Bottler Supply Chain Excellence World-Class Sales Team Large Store Expertise Excellence in Industrial Productivity Excellence in TCCC Partnership Model World-Class Segmentation of and Execution in Outlets Customer Engagement & Loyalty Winning Household Penetration Strategy Discounter Expertise |

15 Topline Growth Supply Chain Operating Expenditures Expected annual run-rate pre-tax savings of approximately $350 to $375 million within 3 years of closing • Shared vision between TCCC and CCEP to drive growth in Western Europe • Become a better commercial partner to pan- European, large, local, and independent customers • Scale and speed to win in new categories (e.g., stills) • Increase efficiency and effectiveness of manufacturing footprint and warehouse operations • Savings opportunities in procurement of direct and indirect categories • Opportunity to share core support functions across the new company • Reduce management team duplications • Adjust required headquarters facilities |

16 Key Pro Forma Metrics 2014 2015E Net Revenue EBITDA (before Synergies) Operating Income (before Synergies) Run-Rate Annual Pre-Tax Savings (a) 2015 Net Debt/EBITDA Effective Tax Rate $12.4bn $1.9bn $1.5bn $12.6bn $2.1bn $1.6bn ~$350 to $375m ~3.5x 26% - 28% Note: Financials based on exchange rates of 1.12 $/€, 1.57 $/£, 0.14 $/NOK and 0.12 $/SEK

(a) Implemented within 3 years of closing |

17 • John Brock, Chairman and CEO of CCE • 9 years of experience in the Coca-Cola System • 20+ years management experience with leading European beverage companies

— Former CEO of InBev (2003-2005) — COO of Cadbury Schweppes (1999-2002) — Served as Director of Campbell Soup Company and Interbrew/Inbrew • 40+ years experience in beverage and consumer products industries, particularly in Western Europe

• Damian Gammell, CEO of Anadolou Efes • 24 years experience in the Coca-Cola System with key leadership positions

— Former CEO of Coca-Cola Içecek, former CEO of CCEAG, former Commercial Director of Coca-Cola

Amatil, former CEO of Coca-Cola Hellenic Russia

• Named a Young Global Leader by the World Economic Forum in 2009 • Nik Jhangiani, CFO of CCE • 15+ years of experience in the Coca-Cola System and 20+ years as finance executive in global markets — Former VP of Finance of CCE, former Group CFO of Bharti Enterprises, former CFO of Coca-Cola

Hellenic Bottling Company (2004-2009)

• V íctor Rufart, General Manager of CCIP • 25 years of experience in the Coca-Cola System — Former General Manager of Cobega — Mr. Rufart successfuly led the integration of the 8 Spanish and Portuguese bottlers that formed CCIP

. |

18 CCEP Board of Directors Key Contract Provisions • Sol Daurella, Chairwoman of CCIP, to serve as Chairwoman of CCEP • John Brock, CEO of CCE, to serve as director • 17-member Board with majority (9) independent non-executive directors (INEDs) • 7 INEDs selected by CCE • 2 additional INEDs with EU experience • 5 directors selected by CCIP, including Chair • 2 directors selected by TCCC, and • CEO to serve as director • The Senior Independent Director to be selected by the Board • New 10 + 10 bottling agreement • Initial four-year incidence pricing agreement extending economic terms currently in place in each respective territory |

19 • File Form F-4 registration statement with the SEC • CCE shareowner vote to approve the transaction • Customary regulatory reviews • Closing expected in the second quarter of 2016 |

20 • Strengthens the Coca-Cola System in Western Europe • Strong strategic and economic rationale • Delivers significant value to shareowners • CCEP is an attractive long term total return investment opportunity |

21 COCA-COLA EUROPEAN PARTNERS OVERVIEW COCA-COLA EUROPEAN PARTNERS BACKGROUND TRANSACTION HIGHLIGHTS |

22 Strong track record of focusing on cash flow generation and delivering shareowner value Refreshing 170 million consumers annually with 1.3 billion unit cases manufactured and distributed from 17 production facilities by ~12k employees Diversified geographic footprint covering territories with stable economies, affluent consumers, and growing population Geographic Sales Mix Product Volume Mix* Source: CCE 2014 10-K * CSD = Carbonated Soft Drinks, NCB = Non-Carbonated Soft Drinks CSD 87% NCB 10% Water 3% Great Britain 34% France 30% Belgium 15% The Netherlands 8% Norway 7% Sweden 6% |

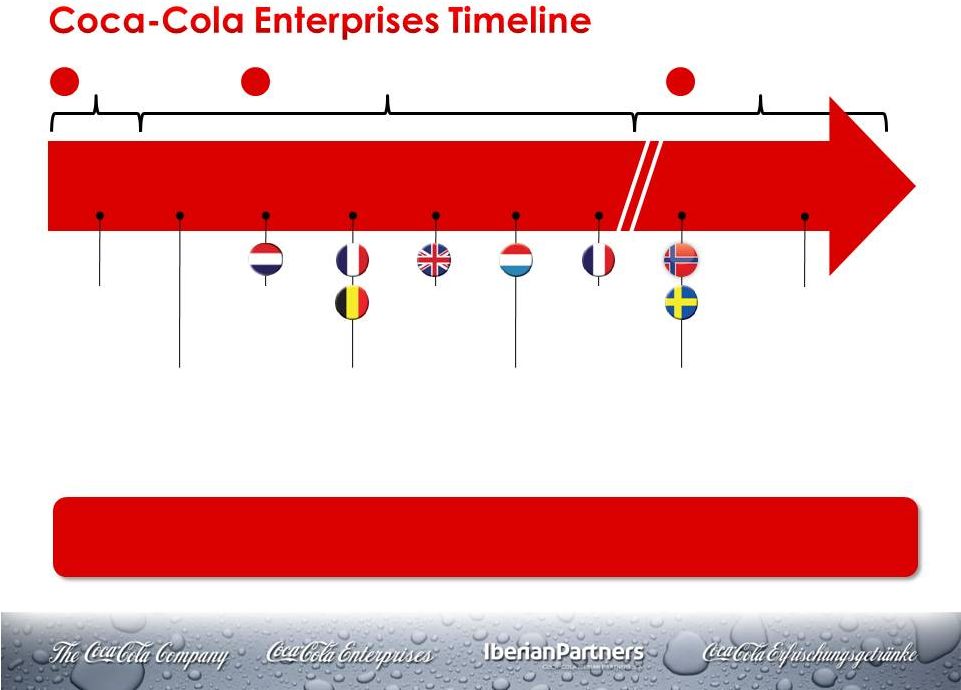

23 TCCC creates CCE; NYSE listing CCE Merges with Johnston Bottling Group 1986 1991 1993 1996 1997 1998 1999 2010 Current Netherlands acquisition Northern France & Belgium acquired Great Britain & Canada acquired Luxembourg acquired Southern France acquired North America sold; Norway & Sweden acquired Focus on maximizing FCF and return of cash to shareowners Evolution from a US bottler to a European bottler Creation NA and EU Expansion Transformation 1 2 3 |

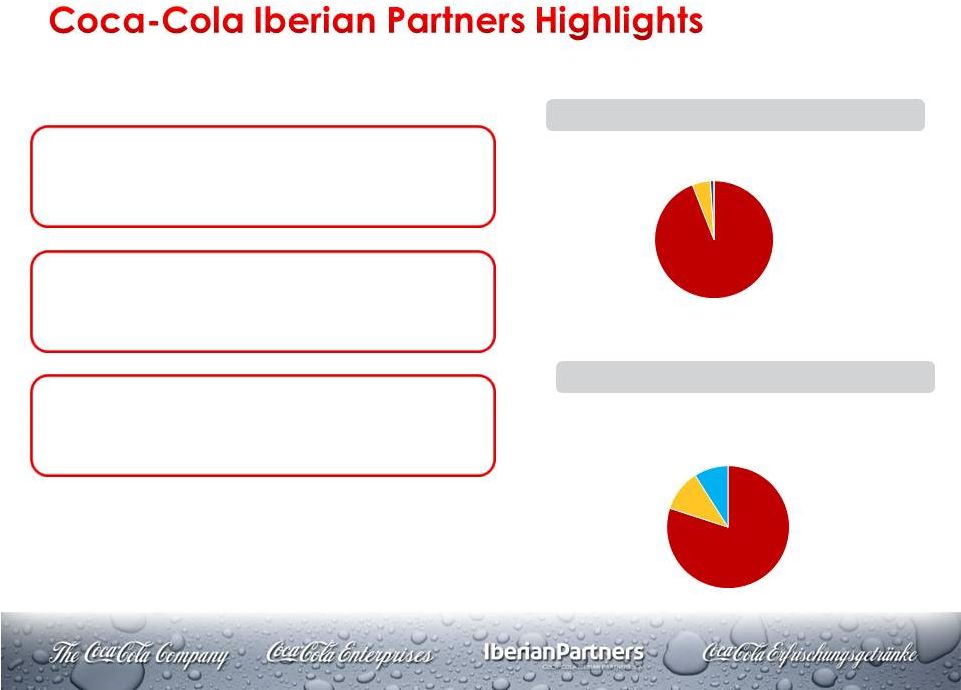

24 Exclusive bottler for Coca-Cola in Spain, Portugal, Iceland, and Andorra Refreshing 57 million consumers annually with 0.5 billion unit cases manufactured and distributed from 17 production facilities by ~5k employees Leading player in CSDs in Spain and Portugal and leading player in NCBs in Spain Geographic Sales Mix Product Volume Mix Source: Company internal reports CSD 80% NCB 11% Water 9% Spain 94% Portugal 5% Iceland 1% |

25 Formation of CCIP through the merger of 8 bottlers Feb 2013 Beginning of the integration process Jun 2013 End of the integration process Dec 2014 Ongoing Further margin improvement initiatives ~1950 60+ years of experience of success and value creation in the bottling business for TCCC CCIP was formed through the merger of 8 bottlers – successful integration process and further margin improvement initiatives underway |

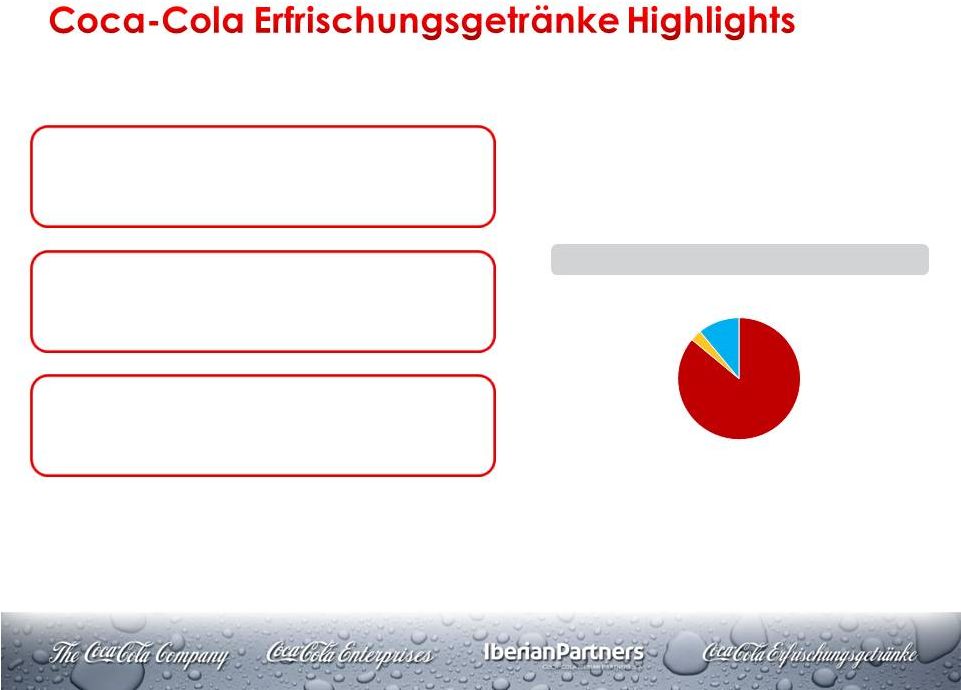

26 Continuous gain of CSD volume share since 2010 Refreshing 80 million consumers annually with 0.7 billion unit cases manufactured and distributed from 20 production facilities by ~10k employees Highest customer satisfaction score of NARTD manufacturers and top workplace in FMCG industry Product Volume Mix Source: Company internal reports CSD 86% NCB 3% Water 11% |

27 Coca-Cola has transformed its German bottling network from a fragmented

patchwork of individually owned local bottlers to a single bottler for the entire

German market

1946 2007 2008 2009 2010 … 2014 1974 1998 124 bottlers 1 bottler 116 bottlers 8 bottlers Bottler Integration: Financial, legal & organizational consolidation Restructuring: Production, Distribution and HC Scale / Coke One: Harmonization of processes & systems |

Presenting Coca-Cola European Partners August 6, 2015 |

29 Forward-Looking Statements This communication may contain statements, estimates or projections that constitute “forward-looking statements” as defined under U.S. federal securities laws. Generally, the words “believe,” “expect,” “intend,” “estimate,” “anticipate,” “project,” “plan,” “seek,” “may,” “could,” “would,” “should,” “might,” “will,” “forecast,” “outlook,” “guidance,” “possible,” “potential,” “predict” and similar expressions identify forward-looking statements, which generally are not historical in nature. Forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from The Coca-Cola Company’s (“KO”), Coca-Cola Enterprises, Inc.’s (“CCE”) or Spark Orange Limited’s (“CCEP”) historical experience and their respective present expectations or projections, including expectations or projections with respect to the transaction. These risks include, but are not limited to, obesity concerns; water scarcity and poor quality; evolving consumer

preferences; increased competition

and capabilities in the marketplace; product safety and quality concerns; perceived negative health consequences of certain ingredients, such as non-nutritive sweeteners and biotechnology-derived substances, and of other substances present in their beverage products or packaging materials; increased demand for food products and decreased agricultural productivity; changes in the retail landscape or the loss of key retail or foodservice customers; an inability to expand operations in emerging or developing markets; fluctuations in foreign currency exchange rates; interest rate increases; an inability to maintain good relationships with their partners; a deterioration in their partners’ financial condition; increases in income tax rates, changes in income tax laws or unfavorable resolution of tax matters; increased or new indirect taxes in the United States or in other tax jurisdictions; increased cost, disruption of supply or shortage of energy or fuels; increased cost, disruption of supply or shortage of ingredients, other raw materials or packaging materials; changes in laws and regulations relating to beverage containers and packaging; significant additional labeling or warning requirements or limitations on the availability of their respective products; an inability to protect their respective information systems against service interruption, misappropriation of data or breaches of security; unfavorable general economic or political conditions in the United States, Europe or elsewhere; litigation or legal proceedings; adverse weather conditions; climate change; damage to their respective brand images and corporate reputation from negative publicity, even if unwarranted, related to product safety or quality, human and workplace rights, obesity or other issues; changes in, or failure to comply with, the laws and regulations applicable to their respective products or business operations; changes in accounting standards; an inability to achieve their respective overall long-term growth objectives; deterioration of global credit market conditions; default by or failure of one or more of their respective counterparty financial institutions; an inability to timely implement their previously announced actions to reinvigorate growth, or to realize the economic benefits they anticipate from these actions; failure to realize a significant portion of the anticipated benefits of their respective strategic relationships, including (without limitation) KO’s relationship with Keurig Green Mountain, Inc. and Monster Beverage Corporation; an inability to renew collective bargaining agreements on satisfactory terms, or they or their respective partners experience strikes, work stoppages or labor unrest; future impairment charges; multi-employer plan withdrawal liabilities in the future; an inability to successfully manage the possible negative consequences of their respective productivity initiatives; global or regional catastrophic events; risks and uncertainties relating to the transaction, including the risk that the businesses will not be integrated successfully or such integration may be more difficult, time-consuming or costly than expected, which could result in additional demands on KO’s or CCEP’s resources, systems, procedures and controls, disruption of its ongoing business and diversion of management’s attention from other business concerns, the possibility that certain assumptions with respect to CCEP or the transaction could prove to be inaccurate, the failure to receive, delays in the receipt of, or unacceptable or burdensome conditions imposed in connection with, all required regulatory approvals and the satisfaction of the closing conditions to the transaction, the potential failure to retain key employees of CCE, Coca-Cola Iberian Partners, S.A.’s (“CCIP”) as a result of the proposed transaction or during integration of the businesses and disruptions resulting from the proposed transaction, making it more difficult to maintain business relationships; and other risks discussed in KO’s and CCE’s filings with the Securities and Exchange Commission (the “SEC”), including their respective Annual Reports on Form 10-K for the year ended December 31, 2014, subsequently filed Quarterly Reports on Form 10-Q and Current Reports on Form 8-K, which filings are available from the SEC. You should not place undue reliance on forward-looking statements, which speak only as of the date they are made. None of KO, CCE, CCIP or CCEP undertakes any obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise. None of KO, CCE, CCIP or CCEP assumes responsibility for the accuracy and completeness of any forward- looking statements. Any or all of the forward-looking statements contained in this filing and in any other of their respective public statements may prove to be incorrect. |

30 Important Additional Information and Where to Find It This communication does not constitute an offer to sell or the solicitation of an offer to buy any securities or a

solicitation of any vote or approval.

In connection with the proposed transaction, CCEP will file with the SEC a registration

statement on Form F-4 that will include

a preliminary proxy statement/prospectus regarding the proposed transaction. After the registration statement has been declared effective by the SEC, a definitive proxy statement/prospectus will be mailed to CCE’s stockholders in

connection with the proposed transaction. INVESTORS ARE URGED TO READ THE PROXY STATEMENT/PROSPECTUS (INCLUDING ALL AMENDMENTS AND SUPPLEMENTS THERETO) AND OTHER DOCUMENTS RELATING TO THE

TRANSACTION FILED WITH THE SEC WHEN THEY BECOME AVAILABLE, BECAUSE THEY WILL CONTAIN

IMPORTANT

INFORMATION ABOUT THE PROPOSED TRANSACTION. You may obtain a copy of the proxy statement/prospectus (when available) and other related documents filed by KO, CCE or CCEP with the SEC regarding the

proposed transaction as well as other filings containing information, free of charge,

through the website maintained by the SEC at

www.sec.gov, by directing a request to KO’s Investor Relations department at (404) 676-2121, or to CCE’s Investor Relations department at (678) 260-3110, Attn: Thor Erickson – Investor Relations. Copies of the proxy statement/prospectus and the filings with the SEC that will be incorporated by reference in the proxy statement/prospectus can also be obtained,

when available, without charge, from KO’s website at www.coca-colacompany.com under the heading “Investors” and CCE’s website at www.cokecce.com under the heading “Investors.” Participants in Solicitation KO, CCE and CCEP and their respective directors, executive officers and certain other members of management and

employees may be deemed to be participants in the solicitation of proxies in favor of the proposed merger. Information regarding the persons who may, under the rules of the SEC, be considered participants in the solicitation of proxies in favor of the proposed merger will be set forth in the proxy statement/prospectus when it is filed with the SEC. You can find information about KO’s and CCE’s directors and executive officers in their respective definitive proxy statements filed with the SEC on

March 12, 2015, and March 11, 2015, respectively. You can obtain free

copies of these documents from KO and CCE, respectively, using the

contact information above. Information regarding CCEP’s directors

and executive officers will be available in the proxy

statement/prospectus when it is filed with the SEC. |