Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - Net Element, Inc. | Financial_Report.xls |

| EX-23.1 - EXHIBIT 23.1 - Net Element, Inc. | v404714_ex23-1.htm |

| EX-32.1 - EXHIBIT 32.1 - Net Element, Inc. | v404714_ex32-1.htm |

| EX-31.2 - EXHIBIT 31.2 - Net Element, Inc. | v404714_ex31-2.htm |

| EX-23.2 - EXHIBIT 23.2 - Net Element, Inc. | v404714_ex23-2.htm |

| EX-21.1 - EXHIBIT 21.1 - Net Element, Inc. | v404714_ex21-1.htm |

| EX-10.35 - EXHIBIT 10.35 - Net Element, Inc. | v404714_ex10-35.htm |

| EX-10.34 - EXHIBIT 10.34 - Net Element, Inc. | v404714_ex10-34.htm |

| EX-10.33 - EXHIBIT 10.33 - Net Element, Inc. | v404714_ex10-33.htm |

| EX-31.1 - EXHIBIT 31.1 - Net Element, Inc. | v404714_ex31-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2014

OR

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from __________ to __________

Commission file number: 001-34887

Net Element, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 90-1025599 | |

|

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

|

3363 NE 163 rd Street, Suite 705 North Miami Beach, FL |

33160 | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (305) 507-8808

Securities registered under Section 12(b) of the Exchange Act:

| Title of each class | Name of each exchange on which registered | |

| Common Stock, par value $0.0001 per share | NASDAQ Capital Market |

Securities registered under Section 12(g) of the Exchange Act:

| Warrants, each exercisable for one share of Common Stock |

| (Title of class) |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ¨ YES x NO

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ¨ YES x NO

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x YES ¨ NO

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). x YES ¨ NO

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | Accelerated filer ¨ |

| Non-accelerated filer ¨ (Do not check if a smaller reporting company) | Smaller reporting company x |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). ¨ YES x NO

The aggregate market value of the registrant’s common equity, other than shares held by persons who may be deemed affiliates of the registrant, as of June 30, 2014 was approximately $15,876,969 (based upon the reported closing price of $1.91 per share on June 30, 2014).

The registrant had 47,460,032 shares of common stock outstanding as of March 30, 2015.

DOCUMENTS INCORPORATED BY REFERENCE: NONE

Defined Terms; Share Amounts and Consideration for Shares

Net Element, Inc. (formerly known as Net Element International, Inc.) is a corporation organized under the laws of the State of Delaware. As used in this Annual Report on Form 10-K (this “Report”), unless the context otherwise requires, the terms “Company,” “we,” “us,” and “our” refer to Net Element, Inc. and, as applicable, its majority-owned and consolidated subsidiaries.

Forward-Looking Statements

This Report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Any statements contained in this Report that are not statements of historical fact may be deemed forward-looking statements. Forward-looking statements generally are identified by the words “expects,” “anticipates,” “believes,” “intends,” “estimates,” “aims,” “plans,” “may,” “will,” “continue,” “seeks,” “should,” “believe,” “potential” or the negative of such terms and similar expressions. Forward-looking statements are based on current plans, estimates and projections, and therefore you should not place too much reliance on them. Forward-looking statements speak only as of the date they are made, and the Company undertakes no obligation to update any forward-looking statement in light of new information or future events, except as expressly required by law. Forward-looking statements involve inherent risks and uncertainties, most of which are difficult to predict and are generally beyond the Company’s control. The Company cautions you that a number of important factors could cause actual results or outcomes to differ materially from those expressed in, or implied by, the forward-looking statements. These factors include, among other factors:

| ■ | the impact of any new or changes made to laws, regulations, card network rules or other industry standards affecting our business; |

| ■ | the impact of any significant chargeback liability and liability for merchant or customer fraud, which we may not be able to accurately anticipate and/or collect; |

| ■ | our ability to secure or successfully migrate merchant portfolios to new bank sponsors if current sponsorships are terminated; |

| ■ | our and our bank sponsors’ ability to adhere to the standards of the Visa and MasterCard payment card associations; |

| ■ | our reliance on third-party processors and service providers; |

| ■ | our dependence on independent sales groups (“ISGs”) that do not serve us exclusively to introduce us to new merchant accounts; |

| ■ | our ability to pass along increases in interchange costs and other costs to our merchants; |

| ■ | our ability to protect against unauthorized disclosure of merchant and cardholder data, whether through breach of our computer systems or otherwise; |

| ■ | the effect of the loss of key personnel on our relationships with ISGs, card associations, bank sponsors and our other service providers; |

| ■ | the effects of increased competition, which could adversely impact our financial performance; |

| ■ | the impact of any increase in attrition due to an increase in closed merchant accounts and/or a decrease in merchant charge volume that we cannot anticipate or offset with new accounts; |

| ■ | the effect of adverse business conditions on our merchants; |

| ■ | our ability to adopt technology to meet changing industry and customer needs or trends; |

| ■ | the impact of any decline in the use of credit cards as a payment mechanism for consumers or adverse developments with respect to the credit card industry in general; |

| ■ | the impact of any adverse conditions in industries in which we obtain a substantial amount of our bankcard processing volume; |

| ■ | the impact of seasonality on our operating results; |

| ■ | the impact of any failure in our systems due to factors beyond our control; |

| ■ | the impact of any material breaches in the security of third-party processing systems we use; |

| ■ | the impact of any new and potential governmental regulations designed to protect or limit access to consumer information; |

| ■ | the impact on our profitability if we are required to pay federal, state or local taxes on transaction processing; |

| ■ | the impact on our growth and profitability if the markets for the services that we offer fail to expand or if such markets contract; |

| ■ | our ability (or inability) to continue as a going concern; |

| ■ | the impact of sanctions against Russia on our operating results; |

| ■ | the Company’s ability (or inability) to obtain additional financing in sufficient amounts or on acceptable terms when needed; |

| ■ | the impact on our operating results as a result of impairment of our goodwill and intangible assets; |

| ■ | our material weaknesses in internal control over financial reporting and our ability to maintain effective controls over financial reporting in the future; and |

| ■ | the other factors identified in the section of this Report entitled “Risk Factors.” |

If these or other risks and uncertainties (including those described in Part I, Item 1A of this Report and the Company’s subsequent filings with the U.S. Securities and Exchange Commission (the “Commission”)) materialize, or if the assumptions underlying any of these statements prove incorrect, the Company’s actual results may be materially different from those expressed or implied by such statements. We undertake no obligation to publicly revise any forward-looking statement to reflect circumstances or events after the date of this Report to reflect the occurrence of unanticipated events. You should, however, review the factors and risks described in the reports we file from time-to-time with the Commission after the date of this Report.

World Wide Web addresses contained in this Report are for explanatory purposes only and they (and the content contained therein) do not form a part of, and are not incorporated by reference into, this Report.

TABLE OF CONTENTS

PART I

Company Overview

Net Element, Inc. (“Net Element,” the “Company,” “we,” “us,” and “our”) is a global payments-as-a-service, technology group specializing in mobile payments and value-added transactional services in the United States and emerging countries. The Company operates in a single operating segment as a provider of transactional services and mobile payment solutions. Through its U.S. based subsidiaries, the Company generates revenues from transactional services, valued-added payment technologies and proprietary cloud-based point of sale payments platform for small and medium-sized businesses (“SME”). Through several international subsidiaries, the Company operates its international business with a focus on transactional services, mobile payments transactions and value-added payment technologies in emerging countries including Russian Federation and the Commonwealth of Independent States (“CIS”), where our subsidiary TOT Money holds a leadership position in mobile payments.

General Business Developments

In 2014, we completed a number of transactions and other changes in pursuit of our strategy of enhancing financial results, creating a strong operational foundation and competitive advantage. We believe the following transactions and actions have focused and strengthened our company and improved our capital structure and cash flow.

Our primary actions during 2014 were as follows:

| · | On November 24, 2014, TOT Money entered into a financing agreement with Bank Otkritie Financial Corp. (“Bank Otkritie”), one of Russia’s largest private listed banks. This financing is complementary to our Alfa-Bank factoring facility, and provides additional flexibility and capacity to expand our presence in Russia’s transactional services market. In conjunction with the Alfa-Bank factoring agreement, TOT Money will have approximately $15 million of available credit to help fund its growth. Per the three-year Agreement, TOT Money will assign to Bank Otkritie its accounts receivable as security for financing in an aggregate amount of up to 200 million Russian rubles (approximately USD $4.2 million based on the currency exchange rate as of the close of business November 17, 2014). Included in this Agreement, Moscow-based Bank Otkritie will track the status of TOT Money’s account receivables, monitor timeliness of payment of such accounts receivable, and provide related servicing. Oleg Firer, our Chief Executive Officer, has personally guaranteed our agreement with Bank Otkritie. This financing is a factoring facility in which TOT Money could assign to the bank certain (but not all) of its accounts receivable suitable to the lender under such facility as security for financing. Accordingly, the amounts of our draws under such facility from time to time will depend on the amounts of the accounts receivable suitable for such assignment as of the time we choose to draw under such facility. We have not drawn any funds under such credit facility. |

| · | On October 17, 2014, we filed a $50 million universal shelf registration statement on Form S-3 with the Securities and Exchange Commission. The registration statement is intended to provide the Company with increased financial flexibility to execute on its business strategy and invest in opportunities in mobile payments and value-added transactional services. |

| · | On September 23, 2014, Alfa-Bank, Russia’s largest private bank, renewed and increased Net Element’s Russian subsidiary OOO TOT Money (“TOT Money”) credit facility from 300 million Russian rubles to 415 million Russian rubles (approximately USD $11 million at the time of the agreement). This financing facility will support our next stage of growth and operations in Russia and the Commonwealth of Independent States. This financing is a factoring facility in which TOT Money could assign to the bank certain (but not all) of its accounts receivable suitable to the lender under such facility as security for financing. Accordingly, the amounts of our draws under such facility from time to time will depend on the amounts of the accounts receivable suitable for such assignment as of the time we choose to draw under such facility. We have not drawn any funds under such credit facility. TOT Money’s previous financing agreement with Alfa-Bank, secured in September, 2012, for the amount of 300 million Russian rubles (approximately USD $9.8 million, at the time of the agreement), expired May 20, 2014 and was fully repaid, using TOT Money’s working capital, in accordance with the terms of the agreement. |

| · | On September 17, 2014, we announced the integration of Apple® services into our point-of-sale payment acceptance hardware and software. This enabled our merchants the ability to accept Apple Pay from customers. This new service will create a unique experience for customers who want to pay at the point-of-sale using their Apple® iPhone 6, Apple® iPhone 6 Plus and Apple® Watch devices. |

| · | On September 15, 2014, we entered into a debt exchange agreement with Crede CG III, Ltd. (“Crede”), a wholly owned subsidiary of Crede Capital Group, LLC. Under the agreement, we effectively eliminated $15,876,860 of indebtedness in exchange for 5,802,945 shares of the Company’s common stock. In addition to saving on the financing expenses associated with holding high-interest rate loans, we freed up a significant amount of cash flow and strengthened our balance sheet by replacing debt with equity. |

| · | On July 2, 2014, we closed on a $10 million credit facility from RBL Capital Group, LLC (“RBL Capital”). The $10 million credit facility extended to us by RBL Capital, triggered the conversion provisions of the first round convertible debt financing provided by Cayman Invest, S.A. (“CI”), converting its debenture to common shares of our Company. The effect of the new $10 million credit facility and the CI debt conversion was to significantly reduce our total outstanding indebtedness. The Company utilized $3 million of the $10 million credit facility to pay in full its loan obligations to MBF Merchant Capital, LLC. |

| · | On June 30, 2014, we appointed William Healy to our board of directors. Mr. Healy is an accomplished financial services industry veteran with more than 24 years of merchant financing and electronic payments industry experience. Mr. Healy is currently the President of Funds4Growth, a leading investment firm focused on financing of payment service providers in the United States. Since launching Funds4Growth, Mr. Healy has successfully structured and financed in excess of $100 million in merchant base loans. Prior to his tenure at Funds4Growth, Mr. Healy founded MBF Leasing, LLC in November of 2003, where he was responsible for strategic planning along with the financial and operational management. Prior to that, Mr. Healy spent 13 years with the CIT Group, Inc., where he was the President of CIT’s Lease Finance Group. |

| · | On May 21, 2014, we appointed Drew Freeman to our Board of Directors. Mr. Freeman is an accomplished industry veteran with more than 30 years of electronic payments and merchant services industry experience. His experience includes extensive work with agent banks, referral banks, direct sales, software integration, internet sales, dining programs, American Express, Diners Club, Discover Card, JCB and ISO/MSP programs. |

| 4 |

| · | On April 21, 2014, we entered into a Secured Convertible Senior Promissory Note (the “Note”) with Cayman Invest, S.A. (“CI”). Pursuant to the Note, CI agreed to loan to the Company $11,200,000.00. No interest will accrue under the Note; provided, however, that upon a default under the Note, the Note will accrue simple interest, at 12% per annum. Prior to March 31, 2015, effective upon a first financing closing after the date of the Note, in which the Company receives financing of at least $10 million from a third party (the “Qualified Financing”), the entire principal amount of the Note will be automatically converted into common shares of the Company equal to 15% of the then outstanding shares of the Company. Effective upon an equity financing after the date of the Note in which the Company issues stock, (other than a Qualified Financing) or at any time before or after March 31, 2015, at the option of CI, the entire principal amount of the Note may be converted into common shares of the Company equal to 15% of the then outstanding shares of the Company. Unless converted, the outstanding amount under the Note will be due and payable on the earlier of March 31, 2015 and the closing of a sale of a majority of the ownership of the Company or any voluntary or involuntary liquidation, dissolution or winding up of the Company. Under the Note, the Company agreed to take all actions to have the obligations under the Note positioned as a senior security interest secured by all assets of the Company and by those payment processing portfolios owned by the Company as of the date of the Note. During 2014, we recorded a gain on the change in fair value on the beneficial conversion derivative in the amount of $5,569,158 as a result of the conversion of the Cayman Invest loan to common stock. This was offset by a loss on debt payoff of the Cayman Invest loan in the amount of ($3,962,406) primarily due to the write-off of the remaining debt discount on the loan |

| · | On February 11, 2014, we agreed to transfer to T1T Group all of the Company’s minority interest in T1T Lab, LLC primarily in consideration for our release from our obligation to make future capital contributions to T1T Lab, LLC. This transaction completed the full divesture of our interests in entertainment assets (websites). |

Following the end of our 2014 fiscal year, on March 16, 2015, TOT Group Europe, Ltd. (“TOT Group Europe”), one of our subsidiaries, entered into a Binding Offer Letter (the "Offer") with Maglenta Enterprises Inc. and Champfremont Holding Ltd. to acquire all of the issued and outstanding equity interests of the PayOnline group of companies (collectively, “PayOnline”) to be named in the course of preparation of a legally binding acquisition agreement. PayOnline’s business includes the operation of a protected payment processing system to accept bank card payments for goods and services.

The consideration for all of the equity interests of PayOnline will be a combination of cash and restricted shares, payable in five installments. The Offer sets forth the determination of the value of such shares based on the closing sales price on the date before each applicable payment date and provides certain additional restrictions on trading of the Company's common stock. The first installment will be payable upon closing of the PayOnline acquisition and will consist of $3.6 million in cash and the restricted shares of the Company's common stock with a value of $3.6 million. The other four installments will be payable after the end of each applicable quarter for which the installment is calculated, and will consist of a combination of cash and the restricted shares of the Company's common stock, in each case equal to the earn-out. The earn out will be calculated based on PayOnline EBITDA for certain post-closing periods, multiplied by 1.35. Pursuant to the Offer, the aggregate valuation of PayOnline on a debt-free basis will be $8,482,000, and the purchase price will not exceed such amount.

At the end of the 12-month period following the issuance of restricted shares of the Company's common stock to the Sellers (“Guarantee Period”), TOT Group Europe will guaranty that the value of such stock then not sold by the sellers of PayOnline equity interests (the “Sellers”) will not be less than the value of such at the date of the issuance of such stock. Subject to certain conditions, if at the end of the Guarantee Period the value of the any such remaining stock is less than the value of such stock at the date of the issuance of such stock, TOT Group Europe will pay a cash amount equaling the difference between such values. If any party terminates the Offer, it will be subject to $400,000 penalty.

Our Corporate Organization

Our Company was formed in 2010 and incorporated as a Cayman Islands exempted company with limited liability under the name Cazador Acquisition Corporation Ltd. (“Cazador”). Cazador was a blank check company incorporated for the purpose of effecting a merger; share capital exchange; asset acquisition; share purchase; reorganization or similar business combination with one or more operating businesses or assets. In 2012, Cazador completed a merger (the “Merger”) with Net Element, Inc., a Delaware corporation (“Net Element”), which was a company with businesses in the online media and mobile commerce payment processing markets. Immediately prior to the effectiveness of the Merger, the Company (then known as Cazador Acquisition Corporation Ltd.) changed its jurisdiction of incorporation by discontinuing as an exempted company in the Cayman Islands and continuing and domesticating as a corporation incorporated under the laws of the State of Delaware. Effective upon consummation of the Merger, (i) Net Element was merged with and into the Company, resulting in Net Element ceasing to exist and the Company continuing as the surviving company in the Merger, and (ii) the Company changed its name to Net Element International, Inc. In 2013, the Company divested its non-core entertainment assets. In December 2013, the Company changed its name to Net Element, Inc. We entered the mobile payments business through the launch of TOT Money in Russia in 2012. We entered the financial technology and value-added transactional service business through the acquisitions of Unified Payments in April 2013 and Aptito in June 2013. Our principal office is located at 3363 NE 163rd Street, Suite 705, North Miami Beach, Florida 33160, and our main telephone number is (305) 507-8808.

Our Industry Segment

We manage one segment, consisting of payment-as-a-service offering, which includes: transactional processing, mobile payment solutions, value-added transactional offerings and proprietary cloud-based point of sale payments platform.

| · | TOT Payments, our transactional processing group for the SME business, provides technology and services that businesses require to accept cashless transactions. TOT Payments processes cashless transactions for card-present (or “swipe”) or card-not-present transactions, including point-of-sale (“POS”), mobile POS (“mPOS”), EMV, near field communication (“NFC”), Apple Pay®, Internet businesses, service-oriented businesses, and mail order / telephone order (“MOTO”) merchants. TOT Payments also processes other cashless transactions including checks and direct debits. TOT Payments services include merchant performance analytics and merchant back office reporting. TOT Payments services are distributed in most part through ISGs, value-added resellers, system integrators and affinity partners. TOT Payments markets its services in the United States under the brand Unified Payments (www.unifiedpayments.com ). |

| · | Aptito is our cloud based Software-as-a-Service (“SaaS”) restaurant management solution, which provides integrated POS, mPOS, Kiosk, Digital Menus functionality to drive consumer engagement via Apple® iPad®-based POS, kiosk and all other cloud-connected devices. Aptito’s proprietary, customer engaged, patent-pending, cloud-based platform provides hospitality merchants with tools to increase sales, productivity and customer loyalty. Utilizing its disruptive platform, Aptito provides merchants a feature-rich, innovative and socially driven, all-in-one digital software solution for the food-service industry. Aptito’s Restaurant mPOS solution provides restaurants with tools to increase sales, productivity, and customer loyalty. Aptito’s suite of integrated tools enables inventory management, complete payroll, staff scheduling, patron reservations and digital menus. More capable and less costly than a traditional POS system, Aptito doesn’t have the steep learning curve associated with typical POS products (www.aptito.com ) |

| 5 |

| · | TOT Money is our proprietary, state-of-the-art mobile payments and commerce platform, which provides carrier-integrated mobile payments solutions, mobile campaign management and distribution. TOT Money mobile platform is positioned in the center of the mobile commerce for digital goods with carrier billing checkout and offers various mobile payment solutions for web services and mobile applications. We provide mobile payment solutions to help digital merchants, such as: social networks, games, online magazines and digital media monetize its mobile clients and the subscription base. We provide users with a simple, secure and fast way to pay for purchases via mobile without a credit card or a bank account. Our mobile campaign tools allow for the delivery of scalable mobile campaigns on behalf of our content partners. TOT Money’s relationships and integration with mobile operators gives us substantial geographic coverage, a strong capacity for innovation in mobile payments and messaging, and the ability to offer its clients In-App payments, Wireless Access Protocol (“WAP”) click, premium Short Message Services (“P-SMS”), Online and Carrier Billing. This deep integration with carriers and expertise in mobile direct billing enables our partners to experience the next generation of mobile payments in just one click. |

The Company has 18 Software Engineers located in our offices in Miami, Moscow and Yekaterinburg, providing all of our software development and support requirements.

Our Services

Payments Acceptance. We provide merchants with turnkey payment acceptance solutions, which include the necessary hardware and software, as well as the necessary technology, to integrate into their existing POS systems, applications and websites. We also provide transaction processing, training, on-going customer, and technical support, risk management to help detect and prevent fraudulent transactions, real-time online reporting, analytics and administrative tools. For these services, we charge our merchants a discount fee, or “Merchant Discount”, which is based primarily on a percentage of the dollar amount of each transaction we process. The Merchant Discount may vary based on several factors, including the type of merchant, the type of payment method used and whether the transaction process is a swipe card-based transaction, mobile transaction or a card-not-present transaction.

| · | Card-based Transactions. A transaction is initiated when a consumer purchases a product or service at a merchant using his or her card. At the point of sale, the consumer’s credit card information is submitted to our processing vendor, which then communicates with the card-issuing bank through the proper association network (such as Visa or MasterCard) to authorize the transaction. After authorization, we instruct our processing vendor to route funds from the card-issuing bank to our sponsoring bank. Our sponsoring bank, which sponsors us for membership in the Visa, MasterCard or other card association, settles the transaction with the merchant. We pay interchange fees and assessment fees to the card-issuing bank and the credit card association, respectively, which are typically passed through in the Merchant Discount. We outsource certain services to third parties, including the receipt and settlement of funds and after-hours customer and technical support. We believe this structure allows us to maintain an efficient operating structure and enables us to expand our operations without significantly increasing our fixed costs or capital expenditures. |

| · | Mobile Transactions. A mobile transaction is initiated when a consumer purchases digital goods or subscribes to digital content using its mobile phone number as a form of payment. Allowing merchants to have the charge added to a customer’s phone bill, or more commonly in markets where pre-paid dominates have it deducted from the user’s balance, bypasses the traditional card-based ecosystem. We use our proprietary mobile payments platform to integrate with mobile operators and facilitate mobile transaction in real-time or on subscription basis. We share revenues with mobile operators and charge our merchants a Merchant Discount fee for processing of such transactions. |

| - | Mobile One Click Payments. Mobile one click payment service provides users with an easy and intuitive way of paying for their goods and services via the browser on their mobile device. Mobile one click payment service allows users browsing websites on their mobile device to purchase digital goods and services directly through their mobile browser. Mobile one click payment service automatically recognizes the user’s mobile number and charges the purchase to their mobile bill or deducts it from their pre-paid credit in just one click. We use an encrypted identification process to immediately recognize the user’s phone number, which provides a secure and automatic authentication, so that the payment process only takes one click. There’s no need for passwords and PIN numbers. |

| - | In-App Payment. In-App Payment allows application users to purchase goods and services from inside the native application in just one click. In-App payment technology recognizes the user’s phone number and charges the purchase to their mobile bill or deducts it from their pre-paid credit. This service has been optimized to work both for users connected to the Mobile Operator’s network (for e.g. 3G, EDGE, GPRS) and also for users connected via WiFi. In-App Payment is available for both One-time and Subscription payment models. |

| - | Web & Desktop Payments. Web Payment allows users browsing merchant’s website on a desktop PC to purchase digital goods and services and charge it directly to their mobile phone bill or deduct the amount from their pre-paid credit. The user’s purchase is authenticated through a secure pin code, which is sent to their mobile. |

| - | Subscription Payments. Subscription Payments option allows merchants to automatically charge users’ mobile bill on a periodic, weekly or monthly basis. By introducing this option merchants will be able to offer users that subscribe access to premium features. Examples of purchases that may benefit from Subscription Payments include online content site subscriptions and credit top ups. |

| - | P-SMS Billing. Purchases are made by means of Premium SMS sent or received where the payment is charged to the user’s mobile monthly bill or deducted from his or her prepaid credit. |

All-in-one Digital POS Platform. Utilizing its disruptive platform, Aptito provides merchants a feature-rich, innovative and socially driven, all-in-one digital software solution for the food-service industry. Aptito’s Restaurant mPOS solution provides restaurants with tools to increase sales, productivity, and customer loyalty. Aptito’s suite of integrated tools enables inventory management, complete payroll, staff scheduling, patron reservations and digital menus. More capable and less costly than a traditional POS system, Aptito doesn’t have the steep learning curve associated with typical POS products.

Business Analytics. Our information, analytics and reporting solutions empower merchants to utilize payment data and analytics to manage and grow their business. The Unified Payments Insight solution uses transactional data, online reputation management and social media to help identify sales trends and seize opportunities for growth.

Merchant Management Portal – Sales Central is our cloud-based solution providing an integrated toolkit to both Independent Sales Organizations and merchants to effectively manage a variety of sales, operations, reporting and accounting functions. Sales Central for ISGs is our comprehensive back office solution for Independent Sales Organization. Our merchant underwriting and boarding process is seamless and paperless. Merchant Library allows ISO to safely store and retrieve any agreement, form or contract, related to ISG’s merchants. Our ISGs are equipped with merchant pricing, residuals calculation and risk management modules, which take care of most of their day-to-day operations. Our ISGs can manage customers’ profit by using multi-level, single-click, drill-down navigation to pricing, detail, summary and statement information.

| 6 |

Relationships with Mobile Operators, Sponsors and Processors

Mobile Operators. In order for us to provide payment and SMS messaging services to mobile subscribers and debit their accounts for payments, we need to have contractual agreements with mobile operators, which allow us to bill its subscribers. We have direct and indirect agreements with mobile operators and mobile operator aggregators in over 40 countries. The three largest mobile operators through which we process the majority of our transactions are: Mobile TeleSystems OJSC (“MTS”), MegaFon OJSC (“MegaFon”) and OJSC VimpelCom (“VimpelCom”). These contracts with mobile operators, allow us to facilitate payments using SMS, Multimedia Messaging Services (“MMS”) and WAP for their mobile phone subscribers. From time to time, we may enter into agreements with additional mobile operators and mobile operator aggregators. In addition, we also have contracts and our platform is integrated with various mobile operator aggregators, which give us access to mobile operator networks in approximately 50 countries.

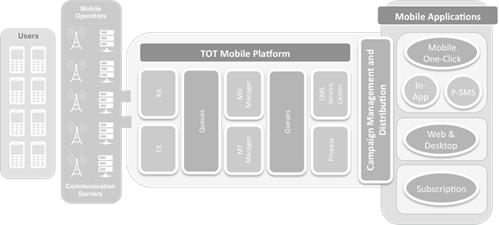

As an example of processing a mobile transaction, the below diagram illustrates the participants involved in a mobile payment transaction. There are four main participants, the user, the mobile operator, transaction processor (TOT Mobile Platform) and the mobile applications (Merchants). Merchants are primarily content or digital goods providers such as: social networks, games and online magazines.

In order to provide transaction-processing services for Visa and MasterCard transactions, a financial institution that is a principal member of the Visa and MasterCard card association must sponsor us. Additionally, we must be registered with Visa and MasterCard as a member service provider.

Sponsoring Banks. Because we are not a member bank as defined by Visa and MasterCard rules and regulations, in order to authorize and settle bankcard transactions for our merchants, we must be sponsored by a financial institution that holds a member bank status. We have agreements with several banks that sponsor us for membership in the Visa and MasterCard card associations and settle card transactions for our merchants. The principal sponsoring bank through which we process the majority of our transaction in the United States is BMO Harris Bank. From time to time, we may enter into agreements with additional banks. See “Risk Factors – Risk Factors Relating to Our Business – We rely on bank sponsors, which have substantial discretion with respect to certain elements of our business practices, in order to process bankcard transactions. If these sponsorships are terminated and we are not able to secure or successfully migrate merchant portfolios to new bank sponsors, we will not be able to conduct our business.”

Processing Vendors. We have agreements with several processing vendors to provide us with, on a non-exclusive basis transaction processing and transmittal, transaction authorization and data capture, and access to various reporting tools. Our primary processing vendor in the United States is Cynergy Data, LLC (“Cynergy”), which provides us with the processing conduit to Total System Services, Inc. (“TSYS”) authorization and settlement network. We have entered into several service agreements with Cynergy. Each of the Cynergy service agreements may be terminated by Cynergy if, among other things, (i) certain insolvency events occur with respect to us or (ii) we fail to maintain our good standing in the Visa or MasterCard associations. We may terminate each of the agreements if, among other things, (i) certain insolvency events occur with respect to Cynergy, (ii) Cynergy materially breaches any of the terms, covenants or conditions of the agreements and fails to cure such breach within 30 days following receipt of written notice thereof, or (iii) under certain circumstances, Cynergy is unable to perform services described in the agreement.

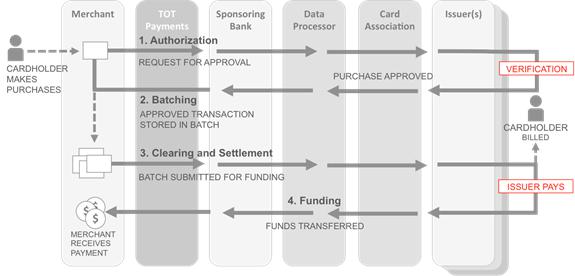

As an example of processing an electronic payment, the below diagram illustrates the participants involved in a credit card transaction. There are four main participants, the merchant, the service provider (TOT payments), the sponsoring bank and the data processor. Merchants are primarily business owners that accept credit card payment in exchange for their merchandise and services.

| 7 |

Our Client Base

In Russia, we enable mobile payment processing services for more than 390 million mobile users in Russia through strategic direct agreements and integrations with Top 3 mobile operators such as Mobile TeleSystem, MegaFon and VimpelCom, Ltd. In January 2015, we have reached a crucial company milestone by exceeding 1 million recurring mobile payment subscribers. As of December 31, 2014, our mobile payments subscriber base consisted of 941,668 recurring mobile payments subscribers.

In the United States, we have developed significant expertise in industries that we believe present relatively low risks as the customers are generally present and the products or services are generally delivered at the time the transaction is processed. These include:

| ■ | Professional service providers |

| ■ | Restaurants |

| ■ | Brick and mortar retailers |

| ■ | Educational service providers |

| ■ | Food stores |

| ■ | Automotive sales and repair shops |

| ■ | Hotel and lodging establishments |

Merchants we serve typically process on average $11,223 each month in credit card transactions and have an average transaction value of $54.35 per transaction. Larger payment processors have traditionally underserved these merchants. As a result, these merchants have historically paid higher transaction fees than larger merchants and have not been provided with tailored solutions and on-going services that larger merchants typically receive from larger payment processing providers.

As of December 31, 2014, approximately 44% of our SME merchants were eating places and restaurants and 18% were schools and educational services. No other merchant class has exceeded 3% concentration. High concentration in eating places and restaurants reflects the efforts of our sales team, actively targeting our Aptito product line. The following table reflects the percentage concentration of our merchant base by class:

| SIC/MCC | Description | % of Total | ||||

| 5812 | EATING PLACES, RESTAURANTS | 44.34 | % | |||

| 8299 | SCHOOLS & EDUCATIONAL SVCS | 17.59 | % | |||

| 5814 | FAST FOOD RESTAURANTS | 2.10 | % | |||

| 5399 | MISCELLANEOUS GENERAL MERCHANDISE | 2.07 | % | |||

| 5712 | FURNITURE & HOME FURNISHINGS | 1.62 | % | |||

| 7011 | HOTELS, MOTELS & RESORTS | 1.54 | % | |||

| 7538 | AUTOMOTIVE REPAIR SHOPS-NON-DEALER | 1.46 | % | |||

| 7298 | HEALTH & BEAUTY SPAS | 1.44 | % | |||

| 5411 | GROCERY STORES & SUPERMARKETS | 1.41 | % | |||

| 8043 | OPTICIANS, OPTICAL GOODS & EYE GLASSES | 1.36 | % | |||

| 7230 | BEAUTY SHOPS & BARBER SHOPS | 1.36 | % | |||

| 5499 | MISCELLANEOUS FOOD STORES-SPECIALTY | 1.24 | % | |||

The following table reflects the percentage concentration of our merchant base by state:

| State | Trans Volume |  |

| NY | 29.84% | |

| NJ | 10.25% | |

| NC | 9.13% | |

| CA | 7.21% | |

| FL | 6.72% | |

| TX | 5.14% | |

| IL | 4.37% | |

| CT | 3.08% | |

| PA | 3.13% | |

| WA | 2.19% | |

| MA | 2.13% | |

| VA | 2.23% | |

| CO | 1.36% | |

| AZ | 1.32% | |

| OH | 1.67% | |

| SC | 1.36% |

Merchant and Transaction Risk Management

In the United States, we focus our sales efforts on low-risk bankcard merchants and have developed systems and procedures designed to minimize our exposure to potential merchant losses.

Effective risk management helps us minimize merchant losses for the mutual benefit of our merchants, Independent Sales Organization (ISO) and ourselves. Our Underwriting and Risk Management Policy and procedures help to protect us from fraud perpetrated by our merchants. We believe our knowledge and experience in dealing with attempted fraud has resulted in our development and implementation of effective risk management and fraud prevention systems and procedures. In 2014, we experienced losses of .008% of our SME card processing volume.

| 8 |

We employ the following systems and procedures to minimize our exposure to merchant and transaction fraud:

| ■ | Application Evaluation Underwriting. There are varying degrees of risk associated with different merchant types based on their industry, the nature of the merchant’s business, processing volumes and average transaction size. As such, varying levels of scrutiny are needed to evaluate a merchant application and to underwrite a prospective merchant account. These range from basic due diligence for merchants with low risk profiles to more comprehensive review for higher risk merchants. The results of this assessment serves as the basis for decisions regarding acceptance of the merchant account, criteria for establishing reserve requirements, processing limits, average transaction amounts and pricing. Once aggregated, these factors also assist TOT Payments in monitoring transactions for those accounts when pre-determined criteria have been exceeded. |

| ■ | Merchant Monitoring. We employ several levels of merchant account monitoring to help us identify suspicious transactions and trends. Daily merchant activity is sorted into a number of customized reports by our systems. Our risk management team reviews any unusual activity highlighted by these reports, such as larger than normal transactions or credits, and monitors other parameters that are helpful in identifying suspicious activity. We have daily windows to decide if any transactions should be held for further review, which provides us time to interview a merchant or issuing bank to determine the validity of suspicious transactions. We also place merchants who require special monitoring on alert status and have engaged a third-party web crawling solution that scans all merchant websites for content and integrity. |

| ■ | Investigation and Loss Prevention. If a merchant exceeds any parameters established by our underwriting and/or risk management staff or violates regulations established by the applicable bankcard network or the terms of our merchant agreement, one of our investigators will identify the incident and take appropriate action to reduce our exposure to loss and the exposure of our merchant. This action may include requesting additional transaction information, withholding or diverting funds, verifying delivery of merchandise or even deactivating the merchant account. Additionally, Relationship Managers may be instructed to retrieve equipment owned by us. In addition, to protect ourselves from unexpected losses, we maintain a reserve account with our sponsoring bank, which can be used to offset any losses incurred at a given time. As of December 31, 2014, our reserve balance was $151,306, our reserve is capped at $250,000 at any given time and replenished by funding 0.03% of bankcard processing volume in the event we need to use it to fund an unexpected loss. This reserve is accounted for on our balance sheet under the caption “other assets”. |

| ■ | Reserves. Some of our merchants are required to post reserves (cash deposits) that are used to offset chargebacks incurred. Our sponsoring banks hold such reserves related to our merchant accounts as long as we are exposed to loss resulting from a merchant’s processing activity. In the event that a small company finds it difficult to post a cash reserve upon opening an account with us, we may build the reserve by retaining a percentage of each transaction the merchant performs until the reserve is established. This solution permits the merchant to fund our reserve requirements gradually as its business develops. As of December 31, 2014, our total reserve deposits were approximately $35,000. We have no legal title to the cash accounts maintained at the sponsor bank in order to cover potential chargeback and related losses under the applicable merchant agreements. We also have no legal obligation to these merchants with respect to these reserve accounts. Accordingly, we do not include these accounts and the corresponding obligation to the merchants in our consolidated financial statements. |

In Russia, we are responsible for content compliance and merchant underwriting and are subject to chargebacks for the full value of the transaction. If any such chargebacks arise we pass these chargebacks to our merchants, in the event we are unsuccessful in passing these charges to the merchant we are responsible for these chargebacks. In 2014, we had no losses from our mobile payments processing volume, as all chargebacks were collected from our aggregators.

Market Overview

The financial technology and transaction processing industry is an integral part of today’s worldwide financial structure. The industry is continually evolving, driven in large part by technological advances. The benefits of card-based payments allow merchants to access a broader universe of consumers, enjoy faster settlement times and reduce transaction errors. By using credit or debit cards, consumers are able to make purchases more conveniently, whether in person, over the Internet, or by mail, fax or telephone, while gaining the benefit of loyalty programs, such as frequent flyer miles or cash back, which are increasingly being offered by credit or debit card issuers.

Consumers are also beginning to use card-based and other electronic payment methods for purchases at an earlier age in life, and increasingly for small dollar amount purchases. Given these advantages of card-based payment systems to merchants and consumers, favorable demographic trends, and the resulting proliferation of credit and debit card usage, we believe businesses will increasingly seek to accept card-based payment systems in order to remain competitive.

Our management believes that cash transactions are becoming progressively obsolete. The proliferation of bankcards has made the acceptance of bankcard payments a virtual necessity for many businesses, regardless of size, in order to remain competitive. In addition, the advent and growth of e-commerce have marked a significant new trend in the way business is being conducted. E-commerce is dependent upon credit and debit cards, as well as other cashless payment processing methods.

The payment processing industry continues to evolve rapidly, based on the application of new technology and changing customer needs. We intend to continue to evolve with the market to provide the necessary technological advances to meet the ever-changing needs of our market place. Traditional players in the industry must quickly adapt to the changing environment or be left behind in the competitive landscape.

| 9 |

Competition

The payment processing industry is highly competitive. We compete with other providers of payment processing services on the basis of the following factors:

| ■ | quality and reliability of service; |

| ■ | ability to evaluate, undertake and manage risk; |

| ■ | ability to attract and retain independent sales organizations; |

| ■ | ability to offer differentiating products and services; |

| ■ | speed in approving merchant applications and deploying equipment; and |

| ■ | cost to the customer. |

We are committed not only to servicing clients’ current processing needs, but also to being amongst the first to make available new technologies that may improve our merchants’ respective competitive positions. We are committed to gaining the expertise and relationships to adopt and implement new technologies that we believe may differentiate our service offerings.

Many large and small companies compete with us in providing payment processing services and related services to a wide range of merchants. Many of our current and prospective competitors have substantially greater financial, technical and marketing resources, larger customer bases, longer operating histories, more developed infrastructures, greater name recognition and/or more established relationships in the industry than we have. Because of this our competitors may be able to adopt more aggressive pricing policies than we can, develop and expand their service offerings more rapidly, adapt to new or emerging technologies and changes in customer requirements more quickly, take advantage of acquisitions and other opportunities more readily, achieve greater economies of scale, and devote greater resources to the marketing and sale of their services. There are also many smaller transaction processors that provide various services to small and medium sized merchants. See “Risk Factors - Risk Factors Related to Our Business Generally - The markets in which we operate are very competitive, and many of our competitors and potential competitors are larger, more established and better capitalized than we are.”

We believe that our specific focus on smaller merchants, in addition to our understanding of the needs and risks associated with providing payment processing services to small merchants and ISGs, gives us a competitive advantage over larger competitors, which have a broader market perspective and priorities. We also believe that we have a competitive advantage over competitors of a similar or smaller size that may lack our extensive experience, value-added product offering and resources.

Our Business Strategy

To continue to grow our business, our strategy is to focus on providing merchants with the ability to process a variety of electronic transactions, including card-based swipe transaction, mobile transaction or a card-not-present transaction.

Key elements of our business strategy include:

| ■ | continuing to strive to enhance our risk management capabilities and solutions for our merchants; |

| ■ | expanding our merchant customer base in our transaction processing for the SME business segment; |

| ■ | expanding into high growth segments and verticals; |

| ■ | broaden and deepen our distribution channels; and |

| ■ | expanding the geographical availability of our payment-as-a-service, mobile payments value-added product offering into new territories. |

With our existing infrastructure and supplier relationships, we believe that we can accommodate expected industry growth. We believe that our available capacity and infrastructure will allow us to take advantage of operational efficiencies as we grow our processing volume and expand to other geographical territories.

Sales and Marketing

We market and sell our services to merchants throughout the United States primarily through a network of ISGs, which are non-employee, external sales organizations with which we have contractual relationships, partnerships with various associations, value-added resellers and technology integrators, through the use of electronic media, telemarketing and other programs utilizing partnerships with other companies that market products and services to small businesses. Our relationships with ISGs are typically mutually non-exclusive, permitting us to establish relationships with multiple ISGs and permitting our groups to enter into relationships with other providers of transaction processing services. We believe that this sales approach provides us with access to an experienced sales force to market our services with limited investment in sales infrastructure and management time. We believe our focus on the unique needs of small and medium size merchants allows us to develop compelling offerings for our sales channels to bring to prospective merchants and provides us with a competitive advantage in our target market. Among the services and capabilities we provide are rapid application response time, merchant application acceptance by fax or on-line submission, superior customer service, merchant reporting and robust analytics. In addition, by controlling the underwriting process we believe we offer the ISGs more rapid and consistent review of merchant applications than may be available from other service providers. Additionally, in certain circumstances, we offer our sales organizations tailored compensation programs and unique technology applications to assist them in the sales process. We keep an open dialogue with our sales partners to address their concerns as quickly as possible and work with them in investigating chargebacks or potentially suspicious activity with the aim of ensuring our merchants do not unduly suffer downtime or the unnecessary withholding of funds.

As compensation for their referral of merchant accounts, we pay our ISGs an agreed-upon residual, or percentage of the income we derive from the transactions we process from the merchants they refer to us. The amount of the residuals we pay to our ISGs varies on a case-by-case basis and depends on several factors, including but not limited to the number and type of merchants each group refers to us. We provide additional incentives to our ISGs, including, from time to time, advances and merchant acquisition bonuses that are secured by income earned from the referred merchant and repayable from future compensation that may be earned by the groups in respect to the merchant they have referred to us. For the year ended December 31, 2014, we had provided merchant acquisition incentives to ISGs in an aggregate amount of $0.34 million. Our organic growth plan calls for future incentives to be funded to our ISGs for referred merchants.

| 10 |

Value-Added Technology and Services

Our Services

Aptito – Aptito is a new generation of proprietary, smart, customer engaged, patent-pending restaurant management system, comprising Point-of-Sale (POS), mPOS, self-ordering Kiosk, digital menus, based on Apple® iPad® and iPhone®, integrated with credit card readers, cash drawers, receipt and kitchen printers. Through its cloud-based, off-line capable payments platform, Aptito offers merchants an innovative, socially driven, all-in-one digital software solution that offers a complete package of features for the food-service industry. Aptito’s Restaurant mPOS solution provides restaurants with tools to increase sales, productivity, and customer loyalty. Aptito’s suite of fully integrated modules enables inventory management, payroll and tips, staff scheduling, patron reservations and digital menus.

We believe the Aptito all-in-one digital solution is the next evolutionary step for restaurants that are seeking to increase customer awareness and loyalty, offer their valued customers a modern and interactive way to order food, and receive personalized and interactive service. Aptito’s all-in-one social solution will drive traffic to restaurants via deals, specials, promotions, and rewards. We expect our social media integration to propel Aptito above platforms that lack social integration and position Aptito to achieve a substantial market share.

Sales Central - is our cloud-based solution providing an integrated toolkit to both Independent Sales Organizations and merchants to effectively manage a variety of sales, operations, reporting and accounting functions.

Sales Central for ISOs is our comprehensive back office solution for Independent Sales Organization. Our merchant underwriting and boarding process is seamless and paperless. Merchant Library allows ISO to safely store and retrieve any agreement, form or contract, related to ISO’s merchants. Our ISOs are equipped with merchant pricing, residuals calculation and risk management modules, which take care of most of their day-to-day operations. Our ISOs can manage customers’ profit by using multi-level, single-click, drill-down navigation to pricing, detail, summary and statement information.

Sales Central for Merchants is our complimentary reporting, accounting and analytics back office solution for small and medium size merchants. Sales Central for Merchants offers a variety of reporting tools along with easy to read and understand charts enables merchants to analyze their sales and improve performance. Bank account reconciliation has never been easier with our ACH transaction, Deposit, Retrieval, Chargebacks reports.

Unified Payments Insights - is an online business dashboard that gives merchants a 360 degree view of their business. With Unified Payments Merchant Insights, merchants are able to compare current revenue, online reputation, and social media activity to their past performance and similar businesses in their area. They can also see what their customers are saying about their business across Yelp, TripAdvisor, Foursquare, OpenTable, Facebook, Twitter and many more all in one simple, easy to use dashboard.

TOT Money – Our omni-channel transactional platform and mobile payments billing system makes payment solutions possible across multiple channels. TOT Money provides the latest mobile payment solutions including premium Short Message Service (“SMS”) billing, mobile subscriptions, direct carrier-billing and WAP billing to allow users to easily and securely pay for web or mobile content. Leveraging our extensive mobile operator relationships and market expertise, our transactional platform and mobile billing system offers customers a variety of mobile payment solutions through an extensive network of mobile operator networks and any device type. TOT Money is currently utilized in our international business division.

Research and Development

We recognize the importance of having access to leading technology in order to develop advanced products for our customers, independent sales agents and for our own internal use. To this end, IT development of our products is conducted in-house. We are maintaining three teams of development engineers, quality assurance professionals, programming code writers, UX and UI designers, dedicated to financial services and value-added technology business.

Our representative office in Yekaterinburg, Russia employs four IT specialists engaged in Sales Central development, seven software engineers engaged in Aptito development and an IT Systems Administrator.

Our subsidiary office in Moscow employs three specialists primarily engaged in system development and support for TOT Money’s billing system.

Our head office in North Miami Beach employs a Chief Technology Officer, (supervising all IT teams), IT Systems Administrator and an Aptito Testing & Development Engineer.

| 11 |

Intellectual Property

We have several trademarks and service marks which are important to our business. The following trademarks and service marks are the subject of trademark registrations and are used in our financial services business:

| 1. | Unified Payments |

| 2. | Unified Payments – experience, confidence, growth |

| 3. | TOT |

We regard our software as proprietary and attempt to protect it, where applicable, with copyrights, trade secret measures and non-disclosure agreements. Despite these protections, it may be possible for competition or users to copy aspects of our intellectual property or to obtain information that we regard as trade secrets. Existing copyright laws afford only limited practical protection for computer software. The laws of foreign countries generally do not protect our proprietary rights in our products to the same extent as the laws of the United States. In addition, we may experience more difficulty in enforcing our proprietary rights in certain foreign jurisdictions. Patent Application number 13/471,717 was filed with United States Patent and Trademark Office on May 15, 2012 for “Restaurant Communication System and Method Utilizing Digital Menus.” This application for patent was assigned to Aptito, LLC on June 26, 2013.

Integrated Mobile Payments and Transaction Services

Our Services

The following services are provided outside the United States: value-added mobile payments; mobile billing; SMS messaging and integrated mobile payments. TOT Money is a provider of mobile messaging and mobile billing solutions in emerging markets. We offer targeted billing solutions via P-SMS, direct carrier billing, in-app purchases, WAP payments and mobile commerce. Instead of using traditional credit cards, TOT Money uses mobile devices as payment methods and allows third-party content or services providers to charge its customers for goods and services using customers pre-paid or post-paid mobile credit.

Relationships with Mobile Operators, Sponsors and Processors

Mobile Operators. In order for us to provide payment and SMS messaging services to mobile subscribers and debit their accounts for payments, we need to have contractual agreements with mobile operators, which allow us to bill its subscribers. We have direct and indirect agreements with mobile operators and mobile operator aggregators in over 40 countries. The three largest mobile operators through which we process the majority of our transactions are: Mobile TeleSystems OJSC (“MTS”), MegaFon OJSC (“MegaFon”) and OJSC VimpelCom (“VimpelCom”). These contracts with mobile operators allow us to facilitate payments using SMS, Multimedia Messaging Services (“MMS”) and WAP for their mobile phone subscribers. From time to time, we may enter into agreements with additional mobile operators and mobile operator aggregators.

Processing Vendors. We had agreements with several service processing vendors to provide us with, on a non-exclusive basis mobile gateway, carrier billing, transaction processing and transmittal, transaction authorization and data capture, and access to various reporting tools. Our primary processing vendors for the year ending December 31, 2014 for the TOT Money business was SDSP Group, which provided us with a mobile billing and support platform in the Russian Federation. During 2014, we acquired our own proprietary billing system and ceased using services provided by SDSP Group. In order for us to be able to process to bankcard transactions internationally, we entered into a partnership agreement with PAYON AG (“PAYON”). PAYON’s multi-channel payment infrastructure system allowed us to directly connect to the banks that we had sponsorship agreements with, and to provide transactional services to the merchants in these regions. This agreement was cancelled during 2014 as the Company launched TOT Platform, its own proprietary platform.

Customers

Everything we do is to ensure that our customers experience first-rate services. TOT Money’s current customers span across variety of industries and operate across different markets. Our clients include mobile operators, merchants, content and service providers.

We believe there are many ways to use TOT Money’s services, including the following:

| ■ | Mobile Operators – Mobile operators partner with us to generate revenues for incoming traffic. Mobile operators increase revenues via additional subscription and transactional services used by its subscribers. |

| ■ | Broadcast Media – SMS billing is becoming an increasingly popular communication tool on both radio & TV. It provides interactivity for the viewer/listener through voting/polls/competitions, and can generate revenues for the stations/production companies. |

| ■ | Portals/Content providers – SMS billing adds a further dimension to the offering of portals and content providers. It enables information alerts, ringtones and logos, SMS sending facility for end-users, all of which can generate revenues for the Company. |

| ■ | Marketing/Sales Promotion – SMS billing is being used as a new marketing channel. Its immediacy; directness and 2-way communication lends itself to effective measurable marketing and promotion. Integration with existing media adds a new dimension to marketing campaigns (e.g. outdoor, press, on-pack, and direct mail). |

Other industries using mobile messaging and mobile billing solutions include banking, retailing, brokering, tourism, transportation, gaming, and education.

| 12 |

Competition

TOT Money primarily competes with other companies operating in the mobile payment processing market in Russia, which market is primarily controlled by four companies, i-CUBE, Incore Media, iFree and TOT Money. Certain of TOT Money’s competitors have been in business longer than TOT Money and have significantly greater financial and other resources than TOT Money. In order to successfully increase our business in that market, we must convince content providers to use TOT Money’s services over competitive platforms that may already be in use. TOT Money must also retain good relations with the mobile operators providing service. We believe that TOT Money will be able to effectively compete in the mobile payment processing market in Russia based primarily upon services offered, functionality and ease of use of features offered. Failure to successfully continue developing TOT Money’s payment processing operations, maintain TOT Money’s existing contracts with mobile phone carriers and content providers and enter into additional contracts with content providers to use TOT Money’s services may harm our revenue and business prospects.

Employees

Our total number of employees at March 15, 2015 was 65 and 2 full time contractors. The staff in the United States is 24 full time employees and 2 full time consultants. Additionally, in Russia we have 39 employees consisting of 18 employees at TOT Money (mobile payments), and 9 employees at Net Element Russia (Executives/Accounting) and 12 employees in Yekaterinburg (System Development).

Regulation

Various aspects of our business are subject to U.S. and non-U.S. federal, state and local regulation. The operations of our subsidiary, TOT Money, are subject to regulation in Russia and may become subject to the laws and regulations of additional foreign jurisdictions as and when its business expands into additional markets. Many domestic and foreign laws and regulations that affect companies conducting business on the Internet and companies transmitting user information and payments via text message or other electronic means are still evolving and the interpretation of such laws and regulations are often uncertain. Failure to comply with applicable laws and regulations may result in the suspension or revocation of licenses or registrations, the limitation, suspension or termination of services and/or the imposition of civil and criminal penalties and/or fines. The services of TOT Money to mobile phone carriers also are subject to certain of the rules and policies of such carriers and ongoing contractual covenants with such carriers, the violation of which may result in penalties and/or fines and possible termination of TOT Money’s services. Certain of our services are also subject to rules set by various payment networks, such as Visa and MasterCard, as more fully described below under Association and Network Rules.

Laws and Rules of the Russian Federation

The relationships between TOT Money and telecommunications carriers in Russia are governed by the general rules of civil law for the provision of services (Chapter 39 of the Civil Code of the Russian Federation). In addition, because the “information and entertainment services” (content services) provided by TOT Money are inextricably linked with the networks of telecommunications carriers, these services are subject to the requirements of the Rules of Mobile Communications Services Provision, approved by the Decree of the Russian Federation Government dated May 25, 2005 No. 328. These Rules govern the relationship between a customer using mobile communication services and a telecommunications carrier in respect of mobile radio communications services, mobile radiotelephone services and/or mobile satellite radio services in the public network. Although TOT Money is not a telecommunications carrier, many requirements of such Rules are present in TOT Money’s contracts with telecommunications carriers, and such contracts impose responsibility and liability on TOT Money for violations.

TOT Money has a license for the provision of telematics services in Russia. TOT Money is considered an operator of telematic services in Russia because it has a direct connection to equipment of telecommunications carriers and it effects electronic communications (i.e., receiving, processing and/or transmitting electronic messages). Operators of telematics services in Russia are regulated by the Federal Law “On Communication” dated July 2, 2003 No. 126-FZ. This Federal Law provides the legal basis for activity in the field of communications in the Russian Federation and territories under the Russian Federation jurisdiction, defines the powers of public authorities in the field of communications, as well as the rights and responsibilities of persons involved in such activities or using communication services. TOT Money also is subject to the Rules of Telematics Services Provision approved by the Decree of the Russian Federation Government dated September 10, 2007 No. 575. These Rules govern the relationship between a customer or a user, on the one hand, and a telecommunications carrier providing telematic communication services, on the other hand, in the provision of telematic communication services.

The activity of TOT Money to some extent is regulated by the Federal Law “On Operational and Investigative Activities” dated August 12, 1995 No. 144-FZ. This Federal Law determines the content of the operational and investigative activities in the Russian Federation, and provides for a system of guarantees in the process of operational and investigative operations. Operational and investigative activities include activities carried out openly and secretly by operational branches of certain government bodies in order to protect life, health, rights and freedoms of the person and the citizen, property, security of the society and the state from criminal attacks.

In carrying out activities on the Internet in Russia, TOT Money is subject to the Federal Law “On Advertising” dated March 13, 2006 No. 38-FZ. The objectives of this Federal Law are the development of markets for goods and services based on the principles of fair competition, ensuring the common economic space in the Russian Federation, the realization of the rights of consumers to receive fair and accurate advertising, creating favorable conditions for the production and distribution of public service announcements, preventions of violations of the Russian Federation on advertising, as well as the suppression of improper advertising. TOT Money’s activities on the Internet in Russia also are subject to the Federal Law “On Protection of Children from Information Harmful to Health” dated December 29, 2010 No. 436-FZ. This Federal Law provides regulations protecting children from information harmful to their health and/or development.

| 13 |

Rules and Policies of and Contractual Covenants with Mobile Phone Carriers

While not governmental regulation, TOT Money is subject to certain of the rules and policies of mobile phone carriers to which TOT Money provides payment processing services and ongoing contractual covenants with such mobile phone carriers. The mobile phone carriers may from time to time update or otherwise modify or supplement their rules and policies. TOT Money periodically is subject to the imposition of fines or penalties as a result of failure to comply with such rules, policies and/or contractual covenants. TOT Money’s failure to comply with the mobile phone carriers’ respective requirements or to pay the fines or penalties they impose could result in the termination of TOT Money’s services.

Other Laws and Regulations

Since TOT Money collects certain information from members and users on its platform, it will be subject to current and future government regulations regarding the collection, use and safeguarding of consumer information over the Internet and mobile communication devices. These regulations and laws may involve taxation, tariffs, user privacy, rights of publicity, data protection, content, intellectual property, distribution, electronic contracts and other communications, consumer protection and electronic payment services. In many cases, it may be unclear how existing laws governing issues such as property ownership, sales and other taxes, libel and personal privacy apply to the Internet or mobile communication services as the vast majority of these laws were adopted prior to the advent of these technologies and do not contemplate or address the unique issues raised by the Internet and e-commerce.

There are a number of legislative proposals that are anticipated or pending before the U.S. Congress, various state legislative bodies, and foreign governments concerning data protection which could affect us. Many states, for example, have already passed laws requiring notification to subscribers when there is a security breach of personal data. It is possible that these laws may be interpreted and applied in a manner that is inconsistent with our data practices. If so, in addition to the possibility of fines, this could result in an order requiring that we change our data practices, which could have an adverse effect on our business.

Legislation could be passed that limits our ability to use or store information about our users. The Federal Trade Commission (the “FTC”) and various states have established regulatory guidelines issued under the Federal Trade Commission Act and various state acts, respectively, that govern the collection, use and storage of consumer information, establishing principles relating to notice, consent, access and data integrity and security. Our practices are designed to comply with these guidelines. For example, we disclose that we collect a range of information about our users, such as their names, email addresses, search histories and activity on our platform. We also use and store such information primarily to personalize the experience on our platforms, provide customer support and display relevant advertising. While we do not sell or share personally identifiable information with third parties for direct marketing purposes, we do have relationships with third parties that may allow them access to user information for other purposes.

We believe our policies and practices comply with the FTC privacy guidelines and other applicable laws and regulations. However, if our belief proves incorrect, or if these guidelines, laws or regulations or their interpretations change or new legislation or regulations are enacted, we may be compelled to provide additional disclosures to our users, obtain additional consents from our users before collecting or using their information or implement new safeguards to help our users manage our (or others’) use of their information, among other changes.

Dodd-Frank Act

In July 2010, the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 was signed into law in the United States. The Dodd-Frank Act has resulted in significant structural and other changes to the regulation of the financial services industry. Among other things, the Dodd-Frank Act established the Consumer Financial Protection Bureau, or CFPB, to regulate consumer financial services, including many offered by our clients.