Attached files

| file | filename |

|---|---|

| EX-3.1(C) - EXHIBIT 3.1(C) - MAGNETEK, INC. | magdec201410kex31c.htm |

| EXCEL - IDEA: XBRL DOCUMENT - MAGNETEK, INC. | Financial_Report.xls |

| EX-31.1 - EXHIBIT 31.1 - MAGNETEK, INC. | magdec201410kex311.htm |

| EX-21.1 - EXHIBIT 21.1 - MAGNETEK, INC. | magdec201410kex211.htm |

| EX-32.1 - EXHIBIT 32.1 - MAGNETEK, INC. | magdec201410kex321.htm |

| EX-23.1 - EXHIBIT 23.1 - MAGNETEK, INC. | magdec201410kex231.htm |

| EX-31.2 - EXHIBIT 31.2 - MAGNETEK, INC. | magdec201410kex312.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One) | |

[ X ] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 28, 2014 | |

OR | |

[ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number 1-10233

MAGNETEK, INC.

(Exact name of Registrant as specified in its charter)

DELAWARE | 95-3917584 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

N49 W13650 Campbell Drive Menomonee Falls, Wisconsin | 53051 | |

(Address of Principal Executive Offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (262) 783-3500

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered |

Common Stock, $.01 par value | The NASDAQ Global Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well known seasoned issuer, as defined in Rule 405 of the Securities Act. | Yes [ ] | No [X] |

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. | Yes [ ] | No [X] |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. | Yes [X] | No [ ] |

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). | Yes [ X ] | No [ ] |

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. | [X] | |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer”, and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer [ ] | Accelerated filer [ ] | Non-accelerated filer [ ] | Smaller reporting company [ X ] | ||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). | Yes [ ] | No [X] | |||||

The aggregate market value of the voting stock held by non-affiliates of the registrant, based on the closing price of $23.65 per share as reported by the NASDAQ Stock Market, on June 27, 2014 (the last business day of the Company’s most recently completed second fiscal quarter), was $72,768,803. Shares of common stock held by each executive officer and director have been excluded since such persons may be deemed affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

The number of shares outstanding of the registrant’s Common Stock, as of February 20, 2015, was 3,534,875 shares.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Magnetek, Inc. definitive 2015 Proxy Statement, to be filed with the Securities and Exchange Commission within 120 days after the close of the fiscal year ended December 28, 2014, are incorporated by reference into Part II and Part III of this Form 10-K.

TABLE OF CONTENTS

Page | ||

PART I | ||

Business | ||

Risk Factors | ||

Unresolved Staff Comments | ||

Properties | ||

Legal Proceedings | ||

Mine Safety Disclosures | ||

PART II | ||

Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases | ||

of Equity Securities | ||

Selected Financial Data | ||

Management's Discussion and Analysis of Financial Condition and Results of Operations | ||

Quantitative and Qualitative Disclosures About Market Risk | ||

Financial Statements and Supplementary Data | ||

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | ||

Controls and Procedures | ||

Other Information | ||

PART III | ||

Directors, Executive Officers and Corporate Governance | ||

Executive Compensation | ||

Security Ownership of Certain Beneficial Owners and Management and | ||

Related Stockholder Matters | ||

Certain Relationships and Related Transactions and Director Independence | ||

Principal Accountant Fees and Services | ||

PART IV | ||

Exhibits and Financial Statement Schedules | ||

Signatures | ||

2

PART I

CAUTION REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K, including documents incorporated herein by reference, contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. The words “believe”, “expect”, “estimate”, “anticipate”, “intend”, “may”, “might”, “will”, “would”, “could”, “project”, "objective", and “predict”, or similar words and phrases generally identify forward-looking statements. Forward-looking statements contained or incorporated by reference in this document, including those set forth in Part II, Item 7 entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations" and in Item 1 of this Annual Report on Form 10-K entitled “Business” include, but are not limited to, statements regarding our plans, objectives, goals, strategies, future events, future sales or performance, projections of revenues, income or loss, capital expenditures, plans for future operations, products or services, legal issues, financing needs or expectations, and other information that is not historical information, as well as assumptions relating to the foregoing. All forward-looking statements are based upon our current expectations, beliefs, projections, and assumptions.

Our expectations, beliefs, projections and assumptions are expressed in good faith and we believe there is a reasonable basis for them. However, there can be no assurance that our financial condition or results of operations will meet the expectations set forth in our forward-looking statements. Forward-looking statements are inherently subject to risks and uncertainties which in many cases are beyond the control of the Company and which cannot be predicted or quantified. As a result, future events and actual results could differ materially from those set forth in, contemplated by, or underlying forward-looking statements. Such risks and uncertainties include, but are not limited to, economic conditions in general, sensitivity to industry conditions, competitive factors such as technology and pricing pressures, business conditions in electronics, industrial equipment and energy markets, international sales and operations, dependence on major customers, increased material costs, risks and costs associated with acquisitions, litigation and environmental matters, and the risk that the Company’s ultimate costs of doing business exceed present estimates. A discussion of these and other specific risks is included in Part I, Item 1A. “Risk Factors” of this Annual Report on Form 10-K. Forward-looking statements contained in this Annual Report speak only as of the date of this document or, in the case of any document incorporated by reference, the date of that document. The Company does not have an obligation to publicly update or revise any forward-looking statement contained or incorporated by reference in these documents to reflect changed assumptions, the occurrence of unanticipated events, or changes to future operating results over time.

ITEM 1. BUSINESS

General

Magnetek, Inc. (“Magnetek,” the “Company,” “we,” or “us” ) is a global provider of digital power control systems that are used to control motion and power primarily in material handling, elevator, and mining applications. Magnetek is listed on the NASDAQ Global Market (NASDAQ: MAG) and was founded in 1984 as a Delaware corporation. However, certain businesses we have acquired have a long history of technical innovation that predates the founding of Magnetek. Our digital power control systems serve the needs of selected niches of traditional and emerging markets that are becoming increasingly dependent on “smart” power. Over the past ten years, we have successfully transitioned the Company from a component supplier to a provider of systems solutions. Today, much of our focus is on developing and introducing innovative electronic drive solutions that both enhance our customers' operational efficiency and save energy. Our products are sold directly or through manufacturers' representatives to original equipment manufacturers (“OEMs”) for incorporation into their products, to system integrators and value-added resellers for assembly and incorporation into end-user systems, to distributors for resale to OEMs and contractors, and to end users for repair and replacement purposes. We operate in a single segment, Digital Power Control Systems. Revenue and profit information, additional financial data, and commentary on recent financial results, which are provided in Part II, Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and in Part II, Item 8. “Financial Statements and Supplementary Data” of this Annual Report Report on Form 10-K, should be read in conjunction with this section.

We believe we are North America's largest independent supplier of digital drives, radio controls, software, and accessories for industrial cranes and hoists, and we believe we are also the largest independent supplier of digital direct current (“DC”) motion control systems for elevators. Customers include most of the industrial crane and hoist companies in North America and the world's leading elevator builders. In addition, we have a growing range of motion control products for mining equipment applications. Our operations are located in North America, predominantly in Menomonee Falls, Wisconsin, the location of our headquarters.

3

One of our primary goals is to expand our position in markets offering long-term stability, excellent growth potential, and profitability. Our focus is on markets where we can apply both our industry expertise and our systems integration model to add value to our customers by improving their productivity, throughput, energy efficiency, or safety, while reducing labor costs, downtime, and maintenance costs.

Product Offerings

Magnetek is a leading provider of innovative power control and delivery systems and solutions for overhead material handling applications used in a number of diverse industries, including aerospace, automotive, steel, aluminum, paper, logging, mining, ship loading, nuclear power plants, and heavy movable structures. We are a major supplier in North America of power and motion control systems, which include alternating current (“AC”) and DC drive systems, radio remote controls, push button pendant stations, brakes, and collision avoidance and power delivery subsystems. While we sell primarily to OEMs of overhead cranes and hoists, we spend a great deal of effort understanding the needs of end users to gain specification. We can combine our products with engineered services to provide complete customer-specific systems solutions.

Magnetek also designs, builds, sells, and supports elevator application-specific drive products that efficiently deliver power used to control motion, primarily in high-rise, high-speed elevator applications. We are recognized as an industry leader for DC high-performance elevator drives, as well as for AC drives used with low- and high-performance traction elevators, due to our extensive application expertise and product reliability. Our elevator product offerings are comprised of highly integrated subsystems and drives, sold mainly to elevator OEMs. In addition, our product options include a number of regenerative controls for both new building installations and elevator modernization projects that help building owners save energy. We estimate over 90,000 Magnetek elevator drives have been installed worldwide.

We are also a leading independent supplier of AC and DC digital motion control systems for underground coal mining equipment. Our systems are used in coal hauling vehicles, shuttle cars, scoops, and other heavy mining equipment. We estimate that nearly 11,000 Magnetek drive systems have been installed in mining equipment throughout the world.

We intend to continue to build on our competitive strengths in established material handling, elevator, and mining markets and continue to invest in research and development to expand our product portfolio aimed at penetrating growing and emerging markets for digital power-based systems.

Growth Drivers in our Served Markets

We believe that future demand for our products will be aided by certain trends that we expect to drive growth in our served markets, including the following:

Focus on Increasing Efficiency and Productivity

In response to increasingly competitive economic conditions, many manufacturers seek to increase productivity and efficiency while controlling costs, and many of our product offerings enable our customers to achieve these goals. Our variable frequency AC drive products and DC digital controls are highly reliable, operate at high speeds, and improve production output, while reducing labor and maintenance costs. Technology advancements in control products and engineering enable us to convert manual processes and systems to automated systems, providing a wide range of benefits, including labor and space savings, improved productivity, efficient material flow, more accurate positioning, and safer operation. As a result, we can demonstrate many opportunities to improve our customers' operations and provide them with quantifiable, and in many cases, significant returns on invested capital.

Modernization and Upgrade of Existing Equipment

Overhead cranes, elevators, and mining equipment represent significant investments in capital which in most cases operate under severe duty and in some cases, in harsh environments. Many of the structural components of these systems are manufactured to withstand significant mechanical forces, and to have useful lives in excess of 30 years. For example, it is not uncommon to find cranes that are more than 50 years old still operating today, or elevators or mining equipment operating with aging and inefficient power control equipment. Rather than scrap structurally sound but outdated equipment, it is often more cost-effective to modernize the equipment to meet current operational needs by upgrading the power control systems. Our current drive technology along with our application expertise can provide reduced energy consumption, greater reliability, improved throughput, lower operational costs, enhanced features, and prolonged equipment life over older drive technology. We believe our large installed base of product combined with our industry expertise provides us with opportunities to expand our business through modernization projects.

Technological advancements have resulted in a shift away from electro-mechanical control to digital power control. For example, a number of years ago, cranes relied mainly on contactors, relays, and static controls for their operation, whereas today, AC and DC drives are the preferred method of control. Improvements in drive technology have also allowed for the downsizing of power platforms and the inclusion of many high-performance features valued by the marketplace. AC power control is generally used for new installations in overhead material handling systems, elevators, and mining equipment.

4

However, DC drive solutions are also a viable alternative for existing installations that wish to retain existing DC power sources. We believe this trend will benefit us in the future as our primary core competency is in digital power control.

Conversion to Wireless Applications

Many industries, including the overhead material handling, mobile hydraulic, construction, and mining markets, are rapidly adopting remote wireless control solutions. While wireless control has been available for a number of years, technology has improved significantly in recent years, enabling enhancements that have resulted in products that are safer, more reliable, ergonomically designed, versatile, and cost-effective. Over the past several years, through both acquisition and internal development, we have invested in expanding the breadth of our wireless control product offering, which we believe will help us to meet demand, increase market share, and enter new markets in this growing field.

Systems Solutions

In an effort to reduce costs and streamline operations, many customers are recognizing increased value in consolidating purchasing requirements with suppliers who can provide increasingly integrated solutions. We benefit from this trend as we can bundle a wide breadth of products together with engineered services to provide customer-specific solutions that will result in reduced installation costs as well as lower operating and maintenance costs for our customers. In many of our served markets, we can provide turnkey service, including project evaluation, project management, installation services, field start-up, operator training, and after-sales service and systems support.

Communication and Diagnostic Features

In many electrical applications today, electronic devices controlled by microprocessors are increasingly being networked together, resulting in smart devices with greater productivity and user benefits. The benefits of this trend on control systems for industrial applications include lower installation costs, better monitoring of performance, improved integration with supervisory systems, and improved uptime. We believe the power of embedded and connected microprocessors within our power electronic devices provide a tremendous benefit for users at all levels from maintenance to production to finance.

Growing Energy Needs and Focus on Energy Efficiency

Total global energy consumption is projected to increase 30% by the year 2040 according to the U.S. Energy Information Administration ("EIA"). The vast majority of energy consumed today comes from traditional energy sources such as coal, oil, and natural gas, and the EIA projects that fossil fuels will supply nearly 80% of world energy use through 2040. Approximately 40% of the electricity used in the U.S. today comes from coal, and coal is expected to remain the leading source of global electricity generation through 2040, per the EIA. We have a wide variety of product offerings across all of our major served markets which are engineered to efficiently use available power, or which convert energy to usable power in an energy efficient manner. We have been a leading supplier of AC and DC digital motion control systems to underground coal mining equipment manufacturers for nearly 30 years. In addition, our regenerative elevator drives can provide energy savings of 25% to 45% over other elevator solutions. We also recently introduced a new line of regenerative drives for the material handling market that, when coupled with our existing motor drive technology, have the ability to provide energy savings of over 40% compared to non-regenerative solutions in the market. We believe our energy efficient product offerings have us well positioned to benefit from the expected growing demand for energy and energy efficient solutions in the future.

Safer Workplace Environments

In an effort to comply with increasing workplace safety regulations and to reduce ongoing costs associated with health insurance, workplace accidents, and workers' compensation expenses, many employers are focused on providing safer workplace environments. We offer a vast number of optional features that can further enhance workplace safety and reduce the risk of accidents and personal injury, including collision avoidance software, programmable acceleration and deceleration, and other safeguards that prevent overheating, eliminate load swing, and prevent uneven lifting.

Competitive Strengths

We believe that we benefit from competitive advantages in the following areas:

Industry Expertise and Technological Capabilities

We emphasize and leverage our ability to provide customized solutions for power and motion control applications through digital power technology. We have a long history of technical innovation and a highly skilled and experienced technical staff. Our technical personnel possess substantial expertise in disciplines central to digital power systems and applications. These include analog-to-digital circuit design, thermal management technology, and the application of microprocessors, digital signal processors, and software algorithms in the development of smart power products. We are widely recognized for our expertise in our served markets, regularly hosting training and technology seminars for customers and end users. We believe we are at the forefront of innovation in the industries we have traditionally served, continuously developing new products to provide cost-effective, value-added solutions to meet the changing needs of our customers.

5

Customer and End-User Relationships

We have established long-term relationships with major manufacturers of cranes and hoists, elevators, and mining equipment, among others. We believe that these relationships have resulted from our reliability and responsiveness, readiness to meet special customer requirements based on innovative technology and application expertise, and the quality and performance of our products, all of which ultimately adds value to our customers by improving their operations and reducing their costs.

Product Breadth and Brand Name Recognition

We provide a wide variety of products in most of our major served markets, and we are among the leaders in the U.S. in many of our served markets. For material handling customers, we serve as a one-stop source, providing a full range of AC and DC crane controls as well as subsystems, including radio controls, push button stations, motors, brakes, and power delivery products. For elevator customers, we offer both AC and DC integrated digital motion control subsystems for mid- to high-rise buildings at varying speed and performance levels. Our elevator control systems can be found in many of the world's most recognizable buildings. Over the past several years, we've introduced a number of new innovative products to further broaden our product offerings, including severe duty AC traction drives for mining applications, regenerative AC and DC drives for elevator applications, and a new generation of lower-cost AC elevator drives for mid-rise applications.

Our brand names, including Telemotive, Electromotive Systems, OmniPulse, IMPULSE, Enrange, Mondel, M-FORCE, and Quattro, are among the most known and respected in the industries we serve. We believe our strong brand name recognition enables us to retain and leverage existing customer relationships while also providing opportunities to gain market share with new customers and grow our business by entering new markets.

Large Installed Base with Proven Technology

Our many years of experience combined with leading share positions in our served markets has resulted in a significant installed base of our products operating in material handling systems, elevators, and mining equipment around the world. We believe the large installed base of our quality products not only demonstrates our technical capability and expertise, but also serves as a potential source for future business from service, repair, retrofit, and modernization opportunities. As production requirements change and existing installed equipment ages, reliability may deteriorate, resulting in reduced productivity, increased downtime, unscheduled repair costs, and safety issues. In these situations, it is often prudent to replace and upgrade power control systems with state-of-the-art controls that can meet present operational needs, enhance performance, and prolong the life of the equipment.

Sales Channels

Our sales force is comprised of a combination of direct employees, sales representatives, and distributors. Although we sell our products to OEMs, our sales and marketing efforts are also aimed at gaining end-user specification. Our sales and marketing team is focused on targeted markets, and has extensive experience and a great deal of application expertise in those markets. We believe that our well established sales network constitutes a significant competitive advantage in the North American marketplace.

Aftermarket Service and Support

We have a highly trained team of experienced service technicians dedicated to aftermarket support to provide prompt service to end users of our products, 24 hours a day, every day of the year. We believe we are able to attract and retain customers in part due to our commitment to quality, service, and customer satisfaction.

Strategy

Invest in Innovation and New Product Development

We continue to invest in research and development (“R&D”) in an effort to grow our business and remain competitive, refreshing our product offerings and developing new products and services to address the changing needs of our customers. Developing and offering a broad range of products for each of our served markets is an integral part of our strategy. We make innovative modifications to existing products in an effort to add features and special application software that improve performance. We continue to expand our bundling opportunities in material handling with our radio drive serial interface (“RDSI”). An RDSI module allows a wireless radio to communicate directly with the crane control system, providing improved diagnostic and troubleshooting information.

We believe opportunities for growth exist in available elevator markets through the expansion of the breadth of available product offerings to include additional competitive products for AC applications. We also believe opportunities for growth exist in available material handling, elevator, and mining markets through the introduction of new energy-saving product offerings. Over the past several years, we've developed an AC version of our Quattro regenerative elevator drive, and a severe duty AC traction drive for mining equipment.

6

Gain Market Share in Served Markets

Our long-standing customer relationships, sales network, and end-user relationships provide us with insights into our served markets that help us to anticipate changes in market conditions and customer requirements. We believe we can leverage our close relationships with our channel partners to grow our business by further enhancing strategic partnerships with key customers. We also believe we can use our knowledge and application expertise to increase our share in our served markets by expanding our level of sales with existing customers and by providing value-added solutions to displace our competition.

Entry into New Markets

We continue to seek to grow our business by migrating our proven technology and application expertise into new markets. Over the past several years, we've strategically allocated R&D, sales, and marketing resources to markets such as automation and mobile hydraulic in material handling and non-coal applications in mining markets in an effort to understand the dynamics and requirements of those markets. We've had success in growing our business in those markets, and will continue to look for opportunities where we believe we can take advantage of our competitive strengths to enter into and gain share in new markets.

Expand Geographically

We have leading North American market positions and derive the majority of our revenue from North American, and more specifically, U.S. customers. We believe that certain non-U.S. markets may provide us with compelling growth opportunities for our products. We also believe that, with our commitment to technological innovation and our demonstrated ability to reduce our customers' costs and improve efficiency, our business model may transfer well to markets outside the U.S. where cost-effective, high quality, reliable power solutions are also valued. In addition, certain of our customers are increasing their global footprint, which could provide us with opportunities to partner with them and service those customers locally. We intend to evaluate these opportunities, and prudently allocate sales resources to those markets outside the U.S. where we think we have the best growth prospects relative to the level of investment required to enter the market.

Generate Sufficient Cash to Fund our Growth Initiatives and our Obligations

Our business has consistently generated positive cash flow from operating activities, prior to funding pension obligations, even during periods of economic downturns by focusing on controlling our costs and effectively managing our working capital. Since January 2007, our unrestricted cash balances have increased from $7 million to nearly $10 million at the end of December 2014. During that time, we've contributed cash of approximately $94 million to our defined benefit pension plan while also experiencing some of the worst economic conditions since the 1930s. In addition, we've continued to spend approximately $3 to $4 million annually on R&D activities aimed at growing our business through innovative new product introductions and entry into new markets. We intend to continue to focus on retaining discipline in our resource allocation, controlling our costs, and effectively managing our assets. At the same time, we intend to continue to prudently invest in our business to drive future growth, in an effort to maximize our profitability and cash flow, while we reduce our pension obligation over time through contributions.

In summary, we intend to continue to pursue internal growth opportunities in our core product lines, seeking to increase our market share, enter new markets, and expand our current business model geographically. We may also selectively pursue external growth through acquisitions in our served or related markets, adding products, technology, or capabilities that complement our existing business. Our focus over the next 12 months will be directed toward aligning our resources and investments with the best growth and profit opportunities, maximizing those opportunities through new product introductions and penetration of new markets. At the same time, we'll strive to effectively manage our cost structure and our assets to optimize cash flow and profitability.

Seasonality

Our power control systems for material handling applications represented nearly 74% of our revenue in fiscal year 2014. Sales of these products tend to follow capital budgeting and spending patterns of the customer base. As a result, our revenues are generally strongest in our June and December fiscal quarters, with relatively lower revenues in our March and September fiscal quarters.

Backlog

Our backlog as of the end of fiscal 2014 was $12.7 million, comparable to our backlog of $12.8 million at the end of fiscal 2013. While we use our backlog figure as an indicator of future sales activity, we have historically had a significant amount of revenue derived from orders that are booked and shipped within the same reporting period. We expect most of the orders in our backlog to be filled during fiscal 2015.

7

Competition

Our primary competitors include: Konecranes Inc., Power Electronics International, Inc., Cattron Group International (a division of Laird Technologies), Conductix-Wampfler (a division of Delachaux Group), Control Techniques (a division of Emerson Electric), OMRON Corporation, KEB GmbH, and Fujitec. Some of these companies have substantially greater financial, marketing, and other resources, larger product portfolios, and greater global reach than us.

Suppliers and Raw Materials

Virtually all materials and components that we purchase are available from multiple suppliers. During fiscal 2014, raw material purchases accounted for approximately 75% of our total cost of sales. Production of digital power control systems depends heavily on various electronic components as well as steel and aluminum enclosures and wire harnesses. We seek to obtain competitive pricing on these raw materials by utilizing multiple suppliers and leveraging our total purchasing requirements.

Research and Development

Our research and development activities, which are conducted primarily in Menomonee Falls, Wisconsin, are directed toward developing new products, improving existing products by, among other things, adding features or reducing costs, and customizing or modifying products to meet customers’ specific needs. Total research and development expenditures were approximately $3.2 million, $3.2 million, and $3.8 million for fiscal 2014, 2013 and 2012, respectively.

Intellectual Property

Magnetek holds numerous patents, trademarks, and copyrights, and we believe that we hold or license all of the patent, trademark, copyright, and other intellectual property rights necessary to conduct our business. We generally rely upon patents, copyrights, trademarks, and trade secret laws to establish and maintain our proprietary rights in our technology and products. There can be no assurance that any of our patents, trademarks or other intellectual property rights will not be challenged, invalidated, or circumvented, or that any rights granted thereunder will provide competitive advantages to us. In addition, there can be no assurance that patents will be issued from pending patent applications filed by us, or that claims allowed on any future patents will be sufficiently broad to protect Magnetek's technology. Further, the laws of some foreign countries may not permit the protection of our proprietary rights to the same extent as do the laws of the United States. Although we believe the protection afforded by our patents, patent applications, trademarks, and copyrights have value, Magnetek's future success will depend primarily on the innovative skills, technological expertise, research and development, and management capabilities of our employees rather than on patent, copyright, and trademark protection.

International Operations

International sales accounted for $11.8 million, or 11% of our net sales, while domestic sales were $97.9 million, or 89% of our net sales in fiscal year 2014. We define international sales as sales of products manufactured by our facilities outside the U.S. that are sold outside of the U.S., as well as sales of products manufactured in the U.S. sold to purchasers outside of the U.S. International sales accounted for $11.3 million, or 11% of our net sales, while domestic sales were $92.0 million, or 89% of our net sales, in fiscal 2013. International sales accounted for $13.9 million, or 12% of our net sales, while domestic sales were $100.4 million, or 88% of our net sales in fiscal year 2012. We hold assets in Canada and the United Kingdom totaling $6.5 million, of which $4.4 million are held in Canada and $2.1 million are in the United Kingdom.

Employee Relations

As of February 20, 2015, we had 130 salaried employees and 188 hourly employees, none of whom were covered by collective bargaining agreements with unions. We believe that our relationships with our employees are favorable.

Available Information

Our Internet website address is www.magnetek.com. Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and any amendments to these reports that are filed by the Company with the Securities and Exchange Commission (SEC) pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 are available free of charge at or through our website.

8

Environmental Matters

From time to time, Magnetek has taken action to bring certain facilities associated with previously owned businesses into compliance with applicable environmental laws and regulations. Upon the subsequent sale of certain businesses, we agreed to indemnify the buyers against environmental claims associated with the divested operations, subject to certain conditions and limitations. Remediation activities, including those related to our indemnification obligations, did not involve material expenditures during fiscal 2014, fiscal 2013, or in fiscal year 2012.

We have been identified by the United States Environmental Protection Agency and certain state agencies as a potentially responsible party for cleanup costs associated with alleged past waste disposal practices at several previously utilized, owned or leased facilities and offsite locations. Our remediation activities as a potentially responsible party were not material in fiscal 2014, fiscal 2013, or in fiscal year 2012. Although the materiality of future expenditures for environmental activities may be affected by the level and type of contamination, the extent and nature of cleanup activities required by governmental authorities, the nature of our alleged connection to the contaminated sites, the number and financial resources of other potentially responsible parties, the availability of indemnification rights against third parties and the identification of additional contaminated sites, our estimated share of liability, if any, for environmental remediation, including our indemnification obligations, is not expected to be material.

For a discussion of environmental-related litigation matters in which we are engaged, please refer to Item 3 - “Legal Proceedings” of this Annual Report on Form 10-K.

Supplemental Information-Executive Officers of the Company

The following table sets forth certain information regarding the current executive officers of the Company, each of whom serves a one-year term of office, as appointed by the Board of Directors.

Name | Age | Position | ||

Peter M. McCormick | 54 | Director, President and Chief Executive Officer | ||

Marty J. Schwenner | 54 | Vice President, Chief Financial Officer | ||

Scott S. Cramer | 62 | Vice President, General Counsel and Corporate Secretary | ||

Michael J. Stauber | 41 | Vice President, Corporate Controller | ||

Hungsun S. Hui | 52 | Vice President, Operations | ||

Peter McCormick has been President and Chief Executive Officer of Magnetek since October 2008. Prior to that, Mr. McCormick served as Chief Operating Officer of Magnetek since November 2006 and served as the Executive Vice President responsible for the Company's power control systems group since 2002. Prior to that, he served as the President of the Company’s industrial controls group from 1999 until 2002. Since joining the Company in 1993, Mr. McCormick has also served as the Vice President of Operations for the Company’s drives group from 1998 until 1999 and as Vice President of the custom products business group from 1996 until 1998.

Marty Schwenner has been Chief Financial Officer of Magnetek since November 2006. Mr. Schwenner has served as a Vice President of the Company since 2003 and was Controller of the Company from 2002 until November 2006. Mr. Schwenner was Vice President of Finance for the Company’s power electronics group from 1998 until 2002. Mr. Schwenner also served as the Chief Financial Officer of the Company's European operations from 1992 to 1998 and as Internal Audit Manager from 1991 until 1992. Mr. Schwenner joined Magnetek as an Internal Auditor in 1989. Mr. Schwenner is a Certified Public Accountant and a Certified Internal Auditor.

Scott Cramer has been Vice President, General Counsel and Corporate Secretary of Magnetek since March 2010. Prior to joining Magnetek, Mr. Cramer served as Senior Vice President and General Counsel with Bucyrus International, Inc. in South Milwaukee, WI from 2006 until 2010. From 2005 to 2006, Mr. Cramer was Senior Legal Counsel with Regal Beloit Corporation following private practice from 2004 to 2005. Mr. Cramer served as Vice President, General Counsel and Secretary from 1997 until 2004 with Superior Services, Inc. following his tenure with Browning-Ferris Industries in Houston, TX and Utrecht, The Netherlands, where he served respectively as Senior Counsel and EMEA General Counsel from 1984 to 1997.

9

Michael Stauber has been Vice President, Corporate Controller since February 2011. Prior to that, Mr. Stauber served as Operations Controller for the Company since November 2007 and prior thereto served as Finance Manager of the Company’s Power Control Division since joining the Company in December 2004. Prior to joining Magnetek, from August 1995 to December 2004, Mr. Stauber was with Rockwell Automation in a variety of financial roles of increasing responsibility.

Hungsun Hui has served as Vice President, Operations since February 2001. Mr. Hui previously held the positions of Magnetek’s Vice President, Engineering from June 1999 to January 2001, and Magnetek’s Director of Advance Manufacturing from March 1998 to June 1999. Prior to joining Magnetek, from June 1985 to February 1998, Mr. Hui was with Rockwell Automation in a variety of operational roles of increasing responsibility.

10

ITEM 1A. RISK FACTORS

Our future results of operations and the other forward-looking statements contained in this Annual Report on Form 10-K, including the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” under Item 7, involve a number of risks and uncertainties. In particular, the statements regarding future goals and strategies, opportunities for growth in certain markets, new product introductions, penetration of new markets, projections of sales revenues, manufacturing costs and operating costs, pricing of our products and raw materials required to manufacture our products, gross margin expectations, relocation and outsourcing of production capacity, capital spending, research and development expenses, the outcome of pending legal proceedings and environmental matters, tax rates, sufficiency of funds to meet our needs including contributions to our defined benefit pension plan, and our plans for future operations, as well as our assumptions relating to the foregoing, are all subject to risks and uncertainties.

A number of other factors could cause our actual results to differ materially from our expectations. We are subject to all of the business risks facing public companies, including business cycles and trends in the general economy, financial market conditions, demand variations and volatility, potential loss of key personnel, supply chain disruptions, government legislation and regulation, and natural causes. The following list of risk factors is not all-inclusive. Other factors and unanticipated events could adversely affect our financial position or results of operations. We believe that the most significant potential risk factors that could adversely impact us are the following:

Economic conditions, primarily in the U.S., may adversely affect our served markets, our business, demand for our products, and our results of operations and cash flows

Demand for our products, which impacts our revenue and gross profit, is affected by general business and economic conditions as well as by changes in customer order patterns. Adverse developments in business conditions, economic activity, or capital spending levels could result in reduced demand for our products and impair our ability to accurately forecast and plan future business activities. We cannot predict the timing, duration, or strength of any economic recovery or the timing, duration, or severity of a subsequent economic slowdown, worldwide, in the U.S., or in the specific end markets we serve. In the event of a future prolonged slowdown in economic activity, our business, financial condition, results of operations, and cash flows could be adversely and materially affected. Additionally, our stock price could decrease if investors have concerns that our business and financial condition will be negatively impacted by weakening economic conditions.

We operate in a highly competitive industry

We operate in a competitive industry characterized by periodic changes in technology, product demand, prices and lead times. Our future profitability depends on our ability to successfully identify and react to these changing trends. Specifically, achievement of our sales and profit goals is dependent in part upon our ability to successfully anticipate product demand, to introduce quality products to meet that demand in a timely manner at competitive prices, to gain acceptance of our products in the marketplace, to achieve cost reductions during the product life cycle, and to adapt our existing product platforms in the event of changes in technology. Failure to do so could result in low returns on investment in new products and technologies, a loss of competitive position relative to our peers, obsolete products and technologies, and an adverse impact on our operating results. In addition, price erosion in response to competition in our served markets could have a material impact on our financial position or results of operations.

Our future sales growth is partially dependent on the successful introduction of new products

Achievement of our Company objectives of sales growth of at least 5% on a year-over year basis and gross margins in excess of 35% are in part dependent upon the successful introduction of new products, acceptance of these new products by customers in those markets, and successful cost reduction efforts related to new products. Any delay in introduction of new products, customer acceptance of new products, or cost reduction actions could have an adverse impact on our financial position or results of operations.

Changes in technology could reduce demand for our products

We believe that our intellectual property is equal or superior to our competitors’ and we do not know of any new technologies that could cause a shift away from digital power electronic solutions in the end markets we serve. However, major advancements in digital power electronic technologies by competitors or the advent of technologies obviating digital power electronic solutions could have an adverse effect on our financial position or results of operations.

11

The loss of one or more major customers could adversely affect our results of operations or financial condition

We rely on several large customers for a significant portion of our sales. The loss of one or more of these customers or significant decreases in these customers' purchase levels could have an adverse effect on our business and on our results of operations.

Certain of our competitors have substantially greater resources and greater global reach than us

We compete with crane and hoist drive manufacturers and drive system integrators, radio control manufacturers, elevator drive manufacturers and control system integrators, and mining machinery drive builders. The total number of such enterprises with whom we compete directly is believed to be fewer than 100. However, certain of our competitors are significantly larger and have substantially greater resources than we do, and some are global in scope, whereas we currently compete primarily in the North American market.

We have pension liabilities and funding obligations which are subject to changes in interest rates, asset return rates, and mortality assumptions

Our defined benefit pension plan was underfunded as of December 28, 2014, due primarily to reductions in interest rates over the past decade, which impact the discount rate used to estimate the net present value of our pension obligations. Current actuarial estimates indicate that we will be required to make contributions of $25 million to our defined benefit pension plan to achieve fully funded status.

In addition, changes in interest rates, investment returns, mortality assumptions, and other factors could adversely affect the funded status of our pension plan in the future and require that we contribute additional cash to the pension plan over and above the amounts currently estimated. Such volatility could also increase pension expense in periods beyond fiscal 2014. As a result, we may be required to seek additional sources of cash to fund both our operations and our required pension contributions.

We may seek additional capital through private or public sales of equity, debt or convertible debt securities, which could have negative effects on our existing investors

We may seek to raise additional funding through equity or certain forms of debt financing in the future that could dilute the percentage ownership held by existing stockholders. In addition, new investors may demand rights or privileges that are preferable to, or senior to, those of our existing stockholders, such as interest payments, dividends or warrants, as a condition to completing a transaction that provides us with capital.

We may have limited access to additional financing

Macroeconomic conditions several years ago led to volatility in security prices, the failure of financial institutions, diminished liquidity and credit availability, and deflation in the valuation of investment vehicles across varied asset classes.

In the event capital and credit markets again become illiquid and the availability of funds becomes limited, we could incur increased costs associated with future equity or debt financing transactions. Our ability to access the capital and credit markets may be limited by these or other factors unique to our Company. Limited access to financing opportunities in the future could have a material adverse impact on our ability to fund our operations or meet our corporate obligations.

We are subject to credit risk

We are exposed to the credit risk of our customers, including risk of bankruptcy, and are subject to losses from uncollectable accounts receivable. If the financial condition of any of our customers deteriorates and impairs their ability to make payments, we could incur future write-offs of accounts receivable that could have a material impact on our financial position, results of operations, or cash flows.

We are reliant on suppliers

We purchase raw materials and subassemblies used in our products from third-party suppliers, and also purchase finished goods for resale to customers from third-party subcontractors. If our suppliers or subcontractors cannot meet their commitments to us in terms of price, delivery, or quality, it may negatively impact our ability to meet our commitments to our customers. This could result in disruption of production, delay in shipments to customers, higher material costs, quality issues

12

with our products and damage to customer relationships. In addition, increases in the cost of raw materials purchased from third-party suppliers could negatively impact our gross profit and results of operations.

We may face claims of infringement on the intellectual property of others, or others may infringe upon our intellectual property

Our future success depends in part on our ability to prevent others from infringing on our proprietary rights, as well as our ability to operate without infringing upon the proprietary rights of others. We may be required at times to take legal action to protect our proprietary rights and, despite our best efforts, we may be sued for infringing on the patent rights of others. Patent litigation is costly and, even if we prevail, the cost of such litigation could adversely affect our financial condition. In addition, we could be adversely affected financially should we be judged to have infringed upon the intellectual property of others.

We may suffer losses resulting from legal and environmental issues

Our results of operations could be adversely impacted by pending and future litigation, including claims related to, but not limited to, product liability, patent infringement, contracts, employment and labor issues, personal injury, and property damage, including damage to the environment.

In some cases, we have agreed to provide indemnification against legal and environmental liabilities and potential liabilities associated with operations that we have divested, including certain motor, generator, lighting ballast, transformer, drive and power supply manufacturing operations. If we are required to make payments under such indemnification obligations, such payments could have a material adverse impact on our financial position, results of operations, or cash flows. Further, we have been indemnified against potential legal and environmental liabilities and potential liabilities associated with operations that we have acquired, including lighting ballast, transformer, capacitor, and crane brake manufacturing operations that were subsequently divested. If not borne by the indemnifying party, such liabilities, if any, could be borne by us and have an adverse effect on our financial position or results of operations.

Our business, operations, and financial results could be adversely impacted in the event of a failure or security breach of our information technology systems

The efficient operation of our business is dependent on our information technology systems. We rely on those systems to manage the day-to-day operation of our business, manage relationships with our business partners, and maintain our financial and accounting records. The failure of our information technology systems, or any compromise of the integrity or security of the data we generate from our information technology systems, could disrupt our business and severely limit our ability to operate our business. In addition, our information technology systems are vulnerable to damage or interruption from natural disasters, theft, computer viruses and hackers, hardware or software failures, and power outages. Any interruption of our information technology systems could result in decreased revenue, increased expenses, increased capital expenditures, customer dissatisfaction, and potential legal actions, any of which could have a material adverse effect on our results of operations or financial condition.

Ordinary transfers of our common stock between shareholders could result in an ownership change as defined in Section 382 of the Internal Revenue Code, limiting our ability to fully utilize our net operating loss carryforwards for U.S. federal tax purposes

We had net operating loss (“NOL”) carryforwards for U.S. federal tax purposes of $242 million as of December 28, 2014. Our NOLs have a carryforward period of 20 years with expiration dates ranging from 2019 to 2034. We anticipate that no federal income tax liability, other than alternative minimum tax, would be recorded if and when we generate U.S. taxable income and such carryforwards are utilized.

We periodically evaluate whether ordinary transfers of our common stock between shareholders have resulted in an ownership change as defined in Section 382 of the Internal Revenue Code. Based on available information, we have determined that no such ownership change has occurred. If such ownership change had occurred, utilization of the Company’s NOLs would be subject to annual limitation provisions per the Internal Revenue Code and similar state laws. Such annual limitations could defer the utilization of NOL carryforwards and accelerate payment of federal income taxes, and could result in the expiration of a portion of the NOL carryforwards before utilization. An ownership change under Section 382 of the Internal Revenue Code would not have a material adverse effect on our results of operations or financial position, as we have provided a full valuation allowance against substantially all of our deferred tax assets. Ordinary transfers of our common stock between

13

shareholders in future periods could result in an ownership change in such periods and accordingly, at that time, limit the utilization of our NOLs as described above.

14

ITEM 1B. UNRESOLVED STAFF COMMENTS

Not applicable.

ITEM 2. PROPERTIES

Magnetek’s headquarters and each of our facilities for the continuing operations of the Company are listed below, each of which is leased.

Location | Lease Term | Approximate Size (Sq. Ft.) | Principal Use | ||||

Menomonee Falls, Wisconsin | 2020 | 143,700 | Power control systems manufacturing and corporate headquarters | ||||

Mississauga, Canada | 2016 | 11,180 | Sales and service | ||||

Pittsburgh, Pennsylvania | 2017 | 11,400 | Power control systems manufacturing | ||||

Bedford, England | 2023 | 7,000 | Sales and service | ||||

Bridgeville, Pennsylvania | 2017 | 6,800 | Engineering | ||||

We believe our facilities are in satisfactory condition and are adequate for our continuing operations.

ITEM 3. LEGAL PROCEEDINGS

We are involved from time to time in legal actions for product liability and other matters that arise in the ordinary course of our business. We are also involved in legal actions associated with our discontinued business operations, including product liability, asbestos-related liability, and environmental proceedings relating to cleanup costs associated with alleged past waste disposal practices at several previously utilized, owned or leased facilities and offsite locations. It is not possible to predict with certainty the outcome of any of these unresolved legal actions or proceedings or the range of possible loss or recovery. A discussion of these matters appears in Note 10 of the Notes to Consolidated Financial Statements under Item 8, including a discussion of whether or not these unresolved matters will have a material impact on our financial position or results of operations.

Litigation - Product Liability

We have been named, along with multiple other defendants, in asbestos-related lawsuits associated with business operations we previously acquired, but which are no longer owned. During our ownership, none of the businesses produced or sold asbestos-containing products. For such claims, we are either contractually indemnified against liability, or contractually obligated to defend and indemnify the purchaser of these former Magnetek business operations. With respect to these claims, we are uninsured, but we believe that we have no such liability and we aggressively seek dismissal from these proceedings. Management does not believe the asbestos proceedings, individually or in the aggregate, will have a material adverse effect on our financial position or results of operations. Given the nature of the above issues, uncertainty of the ultimate outcome, and the inability to estimate the potential loss, no amounts have been reserved for these matters.

Litigation - Patent Infringement and Related Proceedings

In August 2008, we filed a complaint in the Circuit Court of Cook County, Illinois, County Department, Law Division, against Kirkland & Ellis, LLP (“K&E”). The lawsuit involved a claim for breach of professional responsibility arising out of K&E’s representation of Magnetek in the patent infringement action, Ole K. Nilssen v. Magnetek, Inc. We alleged that, as a result of K&E’s negligent breach of professional duty in failing to discover or investigate the existence of prior art and prior misconduct which would have made Nilssen’s patent claim unenforceable or invalidated his patent, we suffered an arbitration award and judgment in the amount of $23.4 million, which judgment was ultimately settled by the payment to Nilssen of $18.75 million. Accordingly, we sought damages in the amount of $18.75 million. Following a December 2011 mediation, we entered into a settlement agreement with K&E. Under the terms of the settlement agreement all outstanding claims were settled and released with prejudice in consideration of K&E making a $5 million settlement payment to us, which we received in January 2012. The federal proceeding and the Illinois Supreme Court proceeding were subsequently dismissed, also in January 2012. We entered into the settlement agreement to eliminate the uncertainties, burden, and expense of further litigation. We recorded the settlement payment as a gain in discontinued operations in fiscal 2012.

15

Litigation - Other

In November 2007, a lawsuit was filed by Antonio Canova in Italy, in the Court of Arezzo, Labor Law Section, against us and Power-One Italy, S.p.A. Mr. Canova is a former Executive Vice President of Magnetek and was Deputy Chairman and Managing Director of our former Italian subsidiary, Magnetek, S.p.A. Mr. Canova asserted claims for damages in the amount of 3.5 million Euros (approximately US$4.3 million) allegedly incurred in connection with the termination of his employment at the time of the sale of our power electronics business to Power-One, Inc. ("Power One") in October 2006. The claims against us relate to a change of control agreement and restricted stock grant. In March 2012, the Court of Arezzo ruled in our favor, dismissing Mr. Canova's claims against us as invalid. Mr. Canova appealed the ruling in September 2012. On October 16, 2013, the Labor Court of Appeals issued its decision rejecting all claims of Mr. Canova against Magnetek, Inc. and ordered Mr. Canova to pay a nominal amount in favor of Magnetek, Inc. toward our legal expenses incurred in the appeal. Mr. Canova did not appeal the ruling to the Supreme Court on or before October 16, 2014, and thereby relinquished any right to appeal. Accordingly we consider this matter closed.

In October 2010, we received a request for indemnification from Power-One for an Italian tax matter arising out of the sale of our power electronics business to Power-One in October 2006. With a reservation of rights, we affirmed our obligation to indemnify Power-One for certain pre-closing taxes. The sale included an Italian company, Magnetek, S.p.A., and its wholly owned subsidiary, Magnetek Electronics (Shenzhen) Co. Ltd. (the “Power-One China Subsidiary”). The tax authority in Arezzo, Italy, issued a notice of audit report in September 2010 wherein it asserted that the Power-One China Subsidiary had its administrative headquarters in Italy with fiscal residence in Italy and, therefore, was subject to taxation in Italy. In November 2010, the tax authority issued a notice of tax assessment for the period of July 2003 to June 2004, alleging that taxes of approximately Euro 1.9 million (approximately US$2.3 million) were due in Italy on taxable income earned by the Power-One China Subsidiary during this period. In addition, the assessment alleged potential penalties calculated at 120% of the tax amount claimed together with interest in the amount of approximately Euro 2.6 million (or approximately US$3.2 million) for the alleged failure of the Power-One China Subsidiary to file its Italian tax return. A hearing before the Tax Court of Arezzo ("Tax Court") was held July 5, 2012, on the tax assessment for the period July 2003 to June 2004. In September 2012, the Tax Court ruled in favor of the Power-One China Subsidiary dismissing the tax assessment for the period of July 2003 to June 2004. In February 2013, the tax authority filed an appeal of the Tax Court's September 2012 ruling. The Regional Tax Commission of Florence heard the appeal of the tax assessment dismissal for the period of July 2003 to June 2004 and on October 6, 2014, issued its ruling finding in favor of the tax authority. We believe the commission's decision was based upon erroneous interpretation of the applicable law and we intend to to appeal the ruling to the Italian Supreme Court.

In August 2012, the tax authority in Arezzo, Italy issued additional notices of tax assessment for the periods July 2002 to June 2003 and July 2004 to December 2006, alleging that taxes of approximately Euro 9.5 million (approximately US$11.6 million) were due in Italy on taxable income earned by the Power-One China Subsidiary together with an allegation of potential penalties in the amount of approximately 2.8 million Euro (approximately US$3.4 million) for the alleged failure of the Power-One China Subsidiary to file its Italian tax returns for the reporting periods. The tax authority asserted that the Power-One China Subsidiary had its administrative headquarters in Italy with fiscal residence in Italy and, therefore, was subject to taxation in Italy. The Tax Court held a hearing on December 4, 2014 and thereafter scheduled another hearing for April 16, 2015. We believe the Italian tax claims are without merit and intend to vigorously defend against them.

Litigation - Environmental Matters

From time to time, we have taken action to bring certain facilities associated with previously owned businesses into compliance with applicable environmental laws and regulations. Upon the subsequent sale of certain businesses, we agreed to indemnify the buyers against environmental claims associated with the divested operations, subject to certain conditions and limitations. Remediation activities, including those related to our indemnification obligations, did not involve material expenditures during fiscal years 2014, 2013 or 2012.

We have also been identified by the United States Environmental Protection Agency and certain state agencies as a potentially responsible party for clean-up costs associated with alleged past waste disposal practices at several previously utilized, owned, or leased facilities and offsite locations. Our remediation activities as a potentially responsible party were not material in fiscal years 2014, 2013 or 2012. Although the materiality of future expenditures for environmental activities may be affected by the level and type of contamination, the extent and nature of clean-up activities required by governmental authorities, the nature of our alleged connection to the contaminated sites, the number and financial resources of other potentially responsible parties, the availability of indemnification rights against third parties and the identification of additional contaminated sites, our estimated share of liability, if any, for environmental remediation, including its indemnification obligations, is not expected to be material.

16

Bridgeport, Connecticut Facility

In 1986, we acquired the stock of Universal Manufacturing Company (“Universal”) from a predecessor of Fruit of the Loom (“FOL”), and the predecessor agreed to indemnify us against certain environmental liabilities arising from pre-acquisition activities at a facility in Bridgeport, Connecticut. Environmental liabilities covered by the indemnification agreement included completion of additional clean-up activities, if any, at the Bridgeport facility and defense and indemnification against liability for potential response costs related to offsite disposal locations. Our leasehold interest in the Bridgeport facility was assigned to the buyer in connection with the sale of our transformer business in June 2001. FOL, the successor to the indemnification obligation, filed a petition for Reorganization under Chapter 11 of the Bankruptcy Code in 1999 and we filed a proof of claim in the proceeding for obligations related to the environmental indemnification agreement. We believe that FOL had substantially completed the clean-up obligations required by the indemnification agreement prior to the bankruptcy filing. In November 2001, we entered into an agreement with FOL involving the allocation of certain potential tax benefits and we withdrew our claims in the bankruptcy proceeding. We further believe that FOL's obligation to the state of Connecticut was not discharged in the reorganization proceeding.

In January 2007, the Connecticut Department of Environmental Protection (“DEP”) requested parties, including us, to submit reports summarizing the investigations and remediation performed to date at the site and the proposed additional investigations and remediation necessary to complete those actions at the site. DEP requested additional information from us relating to site investigations and remediation. We retained an environmental consultant to review and prepare reports on historical operations and environmental activities at the Bridgeport facility. In November 2009, we submitted our site summary report and proposed work plan to the DEP and in October 2010 submitted a revised work plan to the DEP. We agreed to the scope of the work plan with the DEP in November 2010. We have recorded a liability of $0.4 million related to the Bridgeport facility, representing our best estimate of future site investigation costs and remediation costs which are expected to be incurred in the future. The liability is included in accrued liabilities in the consolidated balance sheet as of December 28, 2014.

FOL's inability to satisfy its remaining obligations to the state of Connecticut related to the Bridgeport facility and any offsite disposal locations or the discovery of additional environmental contamination at the Bridgeport facility could have a material adverse effect on our financial position, cash flows, or results of operations.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

17

PART II

ITEM 5. MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Our common stock trades on the NASDAQ Global Market under the symbol "MAG." As of February 20, 2015, there were 117 record holders of Magnetek’s common stock.

The following table sets forth the high and low sales prices of our common stock during each quarter of fiscal years 2014 and 2013:

Fiscal Year 2014 | High | Low | |||||

Fourth Quarter | $ | 45.71 | $ | 25.58 | |||

Third Quarter | 35.00 | 23.21 | |||||

Second Quarter | 23.71 | 19.00 | |||||

First Quarter | 25.75 | 18.68 | |||||

Fiscal Year 2013 | High | Low | |||||

Fourth Quarter | $ | 23.71 | $ | 17.08 | |||

Third Quarter | 18.33 | 16.22 | |||||

Second Quarter | 18.21 | 12.71 | |||||

First Quarter | 14.12 | 10.25 | |||||

We have not paid any cash dividends on our common stock and do not anticipate paying cash dividends in the near future. Our ability to pay dividends on our common stock is restricted by provisions in our 2007 revolving loan agreement, as amended, which provides that we may not declare or pay any dividend or make any distribution with respect to our capital stock.

There were no unregistered sales of equity securities during fiscal year 2014.

Securities Authorized for Issuance Under Equity Compensation Plans

The information required by this Item 5 is hereby incorporated by reference to the section of the Company's 2015 Proxy Statement entitled "Equity Compensation Plan Information Table."

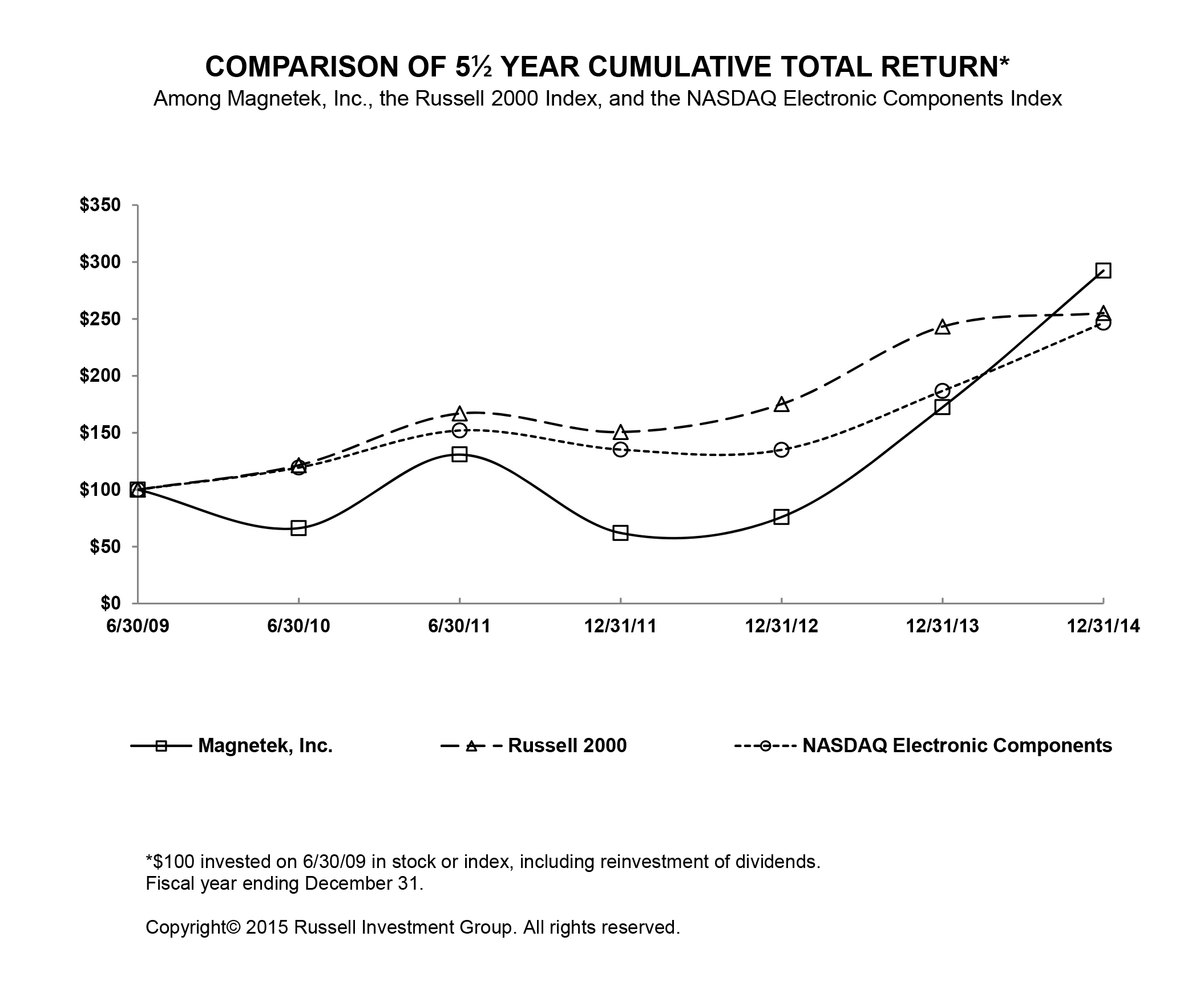

Stock Performance Graph – Return to Shareholders

The table and line graph shown below compare the cumulative total return for the last five years and six months to holders of Magnetek common stock with the cumulative total return of the Russell 2000 Index and the NASDAQ Electronics Components index.

The table and line graph below assume an investment of $100 in the Company’s common stock and in each of the comparison groups beginning June 28, 2009, and assumes the reinvestment of all dividends, through December 28, 2014. The stock price performance information shown below should not be considered indicative of potential future stock price performance.

Jun-09 | Jun-10 | Jun-11 | Dec-11 | Dec-12 | Dec-13 | Dec-14 | |||||||||||||||

Magnetek, Inc. | 100.00 | 66.19 | 130.94 | 61.94 | 75.97 | 172.45 | 292.45 | ||||||||||||||

Russell 2000 | 100.00 | 121.48 | 166.93 | 150.61 | 175.24 | 243.27 | 255.17 | ||||||||||||||

NASDAQ Electronic Components | 100.00 | 119.40 | 152.01 | 135.18 | 135.01 | 186.76 | 246.59 | ||||||||||||||

18

Issuer Purchases of Equity Securities

We did not purchase any shares of our common stock during the fourth quarter of fiscal year 2014.

19

ITEM 6. SELECTED FINANCIAL DATA

The following table sets forth selected historical financial data for Magnetek, Inc. for fiscal years 2014, 2013 and 2012, the six-month transition period ended January 1, 2012, and the previous two fiscal years. The financial data presented below is derived from our audited consolidated financial statements. For additional information, see our financial statements and the notes thereto included elsewhere in this Annual Report on Form 10-K. The following table should be read in conjunction with Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” below.

Statement of Operations Data | Fiscal Year Ended | Six Months Ended | Fiscal Year Ended | |||||||||||||||||||||

December 28, 2014 | December 29, 2013 | December 30, 2012 | January 1, 2012 | July 3, 2011 | June 27, 2010 | |||||||||||||||||||

(Amounts in thousands, except per share data) | ||||||||||||||||||||||||

Net sales | $ | 109,713 | $ | 103,316 | $ | 114,274 | $ | 58,721 | $ | 109,832 | $ | 80,571 | ||||||||||||

Gross profit | 39,951 | 35,325 | 39,844 | 20,333 | 35,157 | 24,128 | ||||||||||||||||||

Gross profit % | 36.4 | % | 34.2 | % | 34.9 | % | 34.6 | % | 32.0 | % | 29.9 | % | ||||||||||||

Income (loss) from operations | $ | (25,730 | ) | $ | 4,775 | $ | 8,022 | $ | 4,880 | $ | 5,446 | $ | (2,314 | ) | ||||||||||

Net income (loss): | ||||||||||||||||||||||||

Continuing operations | $ | (26,445 | ) | $ | 3,759 | $ | 6,926 | $ | 4,331 | $ | 4,817 | $ | (3,158 | ) | ||||||||||

Discontinued operations | (818 | ) | (627 | ) | 5,697 | (39 | ) | (1,154 | ) | (1,943 | ) | |||||||||||||

Net income (loss) | $ | (27,263 | ) | $ | 3,132 | $ | 12,623 | $ | 4,292 | $ | 3,663 | $ | (5,101 | ) | ||||||||||

Earnings (loss) per common share - basic | ||||||||||||||||||||||||

Continuing operations | $ | (7.89 | ) | $ | 1.16 | $ | 2.18 | $ | 1.38 | $ | 1.54 | $ | (1.02 | ) | ||||||||||

Discontinued operations | $ | (0.24 | ) | $ | (0.19 | ) | $ | 1.79 | $ | (0.01 | ) | $ | (0.37 | ) | $ | (0.62 | ) | |||||||

Net income (loss) | $ | (8.13 | ) | $ | 0.97 | $ | 3.97 | $ | 1.36 | $ | 1.17 | $ | (1.64 | ) | ||||||||||

Earnings (loss) per common share - diluted | ||||||||||||||||||||||||

Continuing operations | $ | (7.89 | ) | $ | 1.13 | $ | 2.14 | $ | 1.35 | $ | 1.51 | $ | (1.02 | ) | ||||||||||

Discontinued operations | $ | (0.24 | ) | $ | (0.19 | ) | $ | 1.76 | $ | (0.01 | ) | $ | (0.37 | ) | $ | (0.62 | ) | |||||||

Net income (loss) | $ | (8.13 | ) | $ | 0.94 | $ | 3.90 | $ | 1.34 | $ | 1.15 | $ | (1.64 | ) | ||||||||||

Balance Sheet Data | ||||||||||||||||||||||||

(Amounts in thousands) | December 28, 2014 | December 29, 2013 | December 30, 2012 | January 1, 2012 | July 3, 2011 | June 27, 2010 | ||||||||||||||||||

Total assets | $ | 78,700 | $ | 81,969 | $ | 98,815 | $ | 92,005 | $ | 85,433 | $ | 76,100 | ||||||||||||

Long-term debt, including current portion | — | — | — | — | — | 4 | ||||||||||||||||||

Other long term obligations | 845 | 911 | 1,095 | 1,517 | 1,318 | 1,461 | ||||||||||||||||||

Pension benefit obligations | 27,360 | 48,461 | 102,340 | 98,108 | 61,382 | 77,914 | ||||||||||||||||||

Stockholders' equity (deficit) | 23,619 | 8,236 | (30,875 | ) | (35,745 | ) | (4,462 | ) | (23,937 | ) | ||||||||||||||

20

ITEM 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Overview

We are a global provider of digital power control systems that are used to control motion and power primarily in material handling, elevator, and mining applications. Our digital power control systems serve the needs of selected niches of traditional and emerging markets that are becoming increasingly dependent on “smart” power. We believe we are North America's largest independent supplier of digital drives, radio controls, software, and accessories for industrial cranes and hoists, and believe we are also the largest independent supplier of digital DC motion control systems for elevators. Customers include most of the industrial crane and hoist companies in North America and the world's leading elevator builders. In addition, we have a growing range of products for motion control systems used in mining equipment. We are focused on providing our customers cost-effective power solutions that will improve efficiency, reduce costs, and save energy. Other trends in our served markets we believe we can capitalize on include the adoption of wireless control solutions, modernization and upgrading of installed equipment, and an increasing appreciation in our served markets for communication and diagnostic features, enhanced performance, and safer workplace environments. We believe that with our focus on innovation and our application expertise, combined with strong brand name recognition, broad product offerings and sales channel capabilities, we are well positioned to grow our business by gaining share in both our served markets as well as in new markets. Our operations are located in North America, predominantly in Menomonee Falls, Wisconsin, our Company headquarters.