Attached files

| file | filename |

|---|---|

| EX-31.1 - CERTIFICATION PURSUANT TO RULE 13A-14(A)/15D-14(A) - YELP INC | exhibit31-1.htm |

| EX-21.1 - SUBSIDIARIES OF YELP INC. - YELP INC | exhibit21-1.htm |

| EX-31.2 - CERTIFICATION PURSUANT TO RULE 13A-14(A)/15D-14(A) - YELP INC | exhibit31-2.htm |

| EX-23.1 - CONSENT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM - YELP INC | exhibit23-1.htm |

| EXCEL - IDEA: XBRL DOCUMENT - YELP INC | Financial_Report.xls |

| EX-32.1 - CERTIFICATIONS OF CHIEF EXECUTIVE OFFICER AND CHIEF FINANCIAL OFFICER - YELP INC | exhibit32-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

|

Form 10-K |

| ☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

|

For the Fiscal Year Ended December 31, 2014 |

OR

| ☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||

| For the Transition period from | to | ||

Commission file number: 001-35444

|

YELP

INC. |

| Delaware | 20-1854266 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

140 New Montgomery

Street, 9th Floor

San Francisco,

California 94105

(Address

of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: (415) 908-3801

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Name of Each Exchange on Which Registered | |

| Class A Common Stock, par value $0.000001 per share | New York Stock Exchange LLC |

Securities registered

pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ☒ NO ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES ☐ NO ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES ☒ NO ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES ☒ NO ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☒ | Accelerated filer ☐ |

| Non-accelerated filer (Do not check if a smaller reporting company) ☐ | Smaller reporting company ☐ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). YES ☐ NO ☒

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant was approximately $4,716,654,432 as of June 30, 2014, the last day of the registrant’s most recently completed second fiscal quarter, based upon the closing sale price of the registrant's Class A common stock on the New York Stock Exchange LLC reported for June 30, 2014. Excludes an aggregate of 195,660 shares of the registrant’s Class A common stock and an aggregate of 10,288,701 shares of the registrant’s Class B common stock held by officers, directors, affiliated stockholders and The Yelp Foundation. For purposes of determining whether a stockholder was an affiliate of the registrant at June 30, 2014, the registrant assumed that a stockholder was an affiliate of the registrant if such stockholder (i) beneficially owned 10% or more of the registrant’s capital stock, as determined based on public filings, and/or (ii) was an executive officer or director, or was affiliated with an executive officer or director, of the registrant at June 30, 2014. Exclusion of such shares should not be construed to indicate that any such person possesses the power, direct or indirect, to direct or cause the direction of the management or policies of the registrant or that such person is controlled by or under common control with the registrant.

As of February 20, 2015, there were 64,890,244 shares of registrant’s Class A Common Stock, par value $0.000001 per share, issued and outstanding and 9,592,748 shares of registrant’s Class B Common Stock, par value $0.000001 per share, issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive Proxy Statement for the 2015 Annual Meeting of Stockholders to be filed with the U.S. Securities and Exchange Commission pursuant to Regulation 14A not later than 120 days after the end of the fiscal year covered by this Annual Report on Form 10-K are incorporated by reference in Part III, Items 10-14 of this Annual Report on Form 10-K.

2014 ANNUAL REPORT ON FORM 10-K

____________________

Unless the context suggests otherwise, references in this Annual Report on Form 10-K, or Annual Report, to “Yelp,” the “Company,” “we,” “us,” and “our” refer to Yelp Inc. and, where appropriate, its subsidiaries.

Yelp, Yelp Inc., the Yelp logo, Eat24, SeatMe and other trade names, trademarks or service marks of Yelp appearing in this Annual Report are the property of Yelp. Trade names, trademarks and service marks of other companies appearing in this Annual Report are the property of their respective holders.

Unless the content otherwise indicates, where we refer in this Annual Report to our “mobile application” or “mobile app,” we refer to all of our applications for mobile-enabled devices; references to our “mobile platform” refer to both our mobile app and the versions of our website dedicated to mobile-based browsers. Similarly, references to our “website” refer to both the U.S. and international versions of our website, as well as the versions of our website dedicated to mobile-based browsers.

i

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report contains forward-looking statements that involve risks and uncertainties, as well as assumptions that, if they never materialize or prove incorrect, could cause our results to differ materially from those expressed or implied by such forward-looking statements. The statements contained in this Annual Report that are not purely historical are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act. Forward-looking statements are often identified by the use of words such as, but not limited to, “anticipate,” “believe,” “can,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “might,” “plan,” “project,” “seek,” “should,” “target,” “will,” “would” and similar expressions or variations intended to identify forward-looking statements. These statements are based on the beliefs and assumptions of our management based on information currently available to management. Such forward-looking statements are subject to risks, uncertainties and other important factors that could cause actual results and the timing of certain events to differ materially from future results expressed or implied by such forward-looking statements. Factors that could cause or contribute to such differences include, but are not limited to, those discussed in the section titled “Risk Factors” included under Part I, Item 1A below. Furthermore, such forward-looking statements speak only as of the date of this report. Except as required by law, we undertake no obligation to update any forward-looking statements to reflect events or circumstances after the date of such statements.

ii

PART I

Company Overview

Yelp connects people with great local businesses by bringing “word of mouth” online and providing a platform for businesses and consumers to engage and transact. With a total of approximately 71.2 million cumulative reviews of almost every type of local business in 29 countries as of December 31, 2014, we are one of the world’s leading local business review sites.

Our platform provides value to consumers and businesses alike by connecting consumers with great local businesses at the critical moment when they are deciding where to spend their money. The key strengths of our platform include:

At the heart of our business are the vibrant communities of contributors across the world that contribute the content on our platform. These contributors provide rich, firsthand information about local businesses in the form of reviews and ratings, tips, photos and videos. Each review, tip, photo and video expands the breadth and depth of the content on our platform, which drives a powerful network effect: the expanded content draws in more consumers and more prospective contributors. This increase in content and consumer traffic in turn improves our value proposition to local businesses as they seek easy-to-use and effective advertising solutions. For this reason, we foster and support communities of contributors and make the consumer experience our highest priority.

Of the approximately 71.2 million cumulative reviews our contributors had submitted through December 31, 2014, approximately 50.0 million were recommended and available on business profile pages; approximately 16.3 million were not recommended and available on secondary pages; and approximately 4.9 million had been removed from our platform. Although they do not factor into a business’s overall star rating, we provide access to reviews that are not recommended because they provide additional perspectives and information on reviewed businesses, as well as transparency of the efficacy of our automated recommendation software.

1

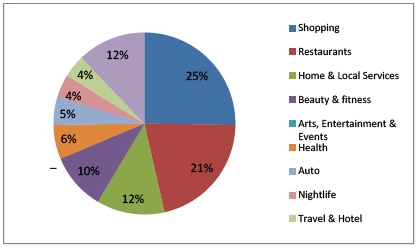

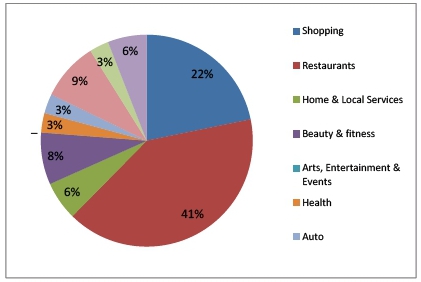

The reviews contributed to our platform cover a wide set of local business categories, including restaurants, shopping, beauty and fitness, arts, entertainment and events, home and local services, health, nightlife, travel and hotel, auto and other categories. We highlight below the breakdown by industry of local businesses that have received reviews on our platform and the breakdown by industry of reviews contributed to our platform through December 31, 2014.

|

Reviewed Businesses*

Reviews*

|

| * | The charts above include information based upon all contributed reviews and include some businesses that have only received reviews that are not recommended or have been removed. |

We believe that the concentration of reviews in the restaurant and shopping categories in particular is primarily due to the frequency with which individuals visit specific businesses or engage in certain activities versus others. For example, an individual may eat at a restaurant three times in one week or go shopping once a week, but the same individual is unlikely to visit a mechanic, get a haircut or use a home or local service with the same frequency.The top five industry categories accounted for an aggregate of 76% of our local advertising revenue for the quarter ended December 31, 2014, broken down as follows: Home & Local Services, 26%; Restaurants, 15%; Beauty & Fitness, 13%; Health, 11%; and Shopping, 11%.

2

Our Products

Local Advertising

We provide both free and paid business listing products to businesses of all sizes. In addition, we enable businesses to deliver targeted search advertising to large local audiences through our website and mobile app. We recognize revenue from these products as local advertising revenue.

|

Free Online Business Account |

We enable businesses to create a free online business account and claim the page for each of their business locations. With their free business accounts, businesses can view trends (e.g. statistics and charts of the performance of their pages on our platform), use the Revenue Estimator tool (e.g. to quantify the revenue opportunity Yelp provides), message customers (e.g. to reply to reviews either publicly or privately), update information (e.g. address, hours of operation) and offer Yelp Deals and Gift Certificates (as described below). | |

|

Enhanced Profile |

Our enhanced profile solution eliminates search advertising from a business’s profile page and allows the business to incorporate a video clip or photo slide show on the page. Businesses can also promote a desired transaction of their choosing — such as scheduling an appointment or printing a coupon — directly on their business listing pages with our Call to Action feature. This feature takes consumers directly from a business’s listing page to the business’s own website to complete the action. | |

Branded Profile |

For businesses with ten or more locations, our branded profile solution offers the ability to incorporate a video clip or photo slide show, as well as a Call to Action Button, on each location’s business listing page. | |

|

Search and Other Ads |

We allow businesses to promote themselves as a sponsored search result on our platform and on the listing pages of related businesses. We sell ads on either a per-impression or per-click basis. | |

|

Online Reservations |

We provide restaurants, nightlife and certain other venues with the ability to offer online reservations directly from their Yelp business listing pages through our SeatMe feature, which also offers front-of-house management tools. We also offer Yelp Reservations, a free tool with basic reservation functionality for businesses in the restaurant and nightlife categories. |

Brand Advertising

We offer advertising solutions for national brands that want to improve their local presence in the form of display advertisements and brand sponsorships. Our national advertisers include leading brands in the food and restaurant, automobile, financial services, logistics, consumer goods and health and fitness industries. We recognize revenue from these products as brand advertising revenue.

|

Traditional Display Advertising |

We offer both graphic and text display advertisements on our website and mobile app. We typically sell these ads on a per-impression basis. We offer businesses display advertising opportunities on our mobile app through display ads that are optimized for the mobile experience, on our home page and on individual web pages. |

3

|

Brand Sponsorships |

Our fixed-price brand sponsorships provide businesses with exclusivity over a section or advertisement placement on Yelp for a fixed period of time. Brand sponsorships are generally associated with a particular platform — desktop, mobile web or mobile app — and are short in duration. |

Other Services

In addition to our business listing and advertising products, we also offer several features and consumer-interactive tools to facilitate transactions between consumers and the local businesses they find on Yelp. We recognize revenue from these sources as other services revenue.

|

Yelp Platform |

The Yelp Platform allows consumers to transact directly on Yelp. Through partnerships with companies including Eat24 (which we acquired in February 2015), Booker, Hipmunk and CellarPass, consumers are currently able to complete food delivery transactions, book spa and salon appointments, and make hotel bookings and winery reservations, all without leaving Yelp. | |

|

Yelp Deals |

Our Yelp Deals product allows local business owners to create promotional discounted deals for their products and services, which are marketed to consumers through our platform. Yelp Deals typically have a fee structure based solely on transaction volume with no upfront costs, and we typically earn a fee based on the discounted price of each deal sold. We process all customer payments and remit to the business the revenue share of any Yelp Deal purchased. | |

|

Gift Certificates |

Our Gift Certificates product allows local business owners to sell full-price gift certificates directly to customers through their business profile pages. The business chooses the price point to offer (from $10 to $500), and the buyer may purchase Gift Certificates denominated in such amounts. We earn a fee based on the amount of the Gift Card sold. We process all consumer payments and remit to the business the revenue share of any Gift Certificate purchased. |

The following table provides a breakdown of our revenue by product for the years indicated:

| Year Ended December 31, | |||||||||

| 2014 | 2013 | 2012 | |||||||

| Percentage of total net revenue by product: | |||||||||

| Local advertising | 85 | % | 83 | % | 79 | % | |||

| Brand advertising | 9 | 12 | 15 | ||||||

| Other services | 6 | 5 | 6 | ||||||

| Total | 100 | % | 100 | % | 100 | % | |||

Our Strategy

Our mission is to connect people with great local businesses. We focus on the following key strategies to grow our business, audience of consumers and advertiser base:

4

Accelerate Network Effect

| ● |

Expand Content. We believe that as the amount of content on

our platform grows, our platform will become more widely known and

relevant to broader audiences, thus attracting new consumers to use our

service. Accordingly, we will continue to explore ways to expand our

content and further enable contributors to share their local experiences

through detailed reviews, photos, tips and other forms of content

contribution across our platform. For example, in the fourth quarter of

2014, we acquired Restaurant Kritik, a German review website, and Cityvox,

a French review website. We plan to migrate the content from those sites

to the Yelp platform in 2015, thereby increasing the depth and breadth of

our European content. In 2014, we also entered into a strategic

partnership with YP – the company formerly

known as Yellow Pages – pursuant to which YP business

owner profile data will appear on our platform. |

| ● |

Increase

Traffic. As we continue to grow our contributor and consumer footprint within Yelp communities,

we expect to benefit from accelerating network effect dynamics, further driving the growth of reviews,

consumers and local business activity. In the first quarter of 2014, we entered into a partnership with

Yahoo! to use Yelp content to power Yahoo Search in the United States, which we believe will increase our

brand recognition and enable us to reach a larger audience. In addition, we expect to redirect traffic from

the Restaurant Kritik and Cityvox websites following our planned migration of the content from those sites

in 2015. We also plan to continue to invest in the development of our mobile platform to take advantage of

the growing number of consumers accessing Yelp through their mobile devices. |

| ● |

Increase Engagement. By continuing to expand our community engagement efforts and providing a more feature-rich experience, we believe we can increase the number of visits and searches per user. In 2014, we added a number of new features aimed at increasing user engagement, including mobile review translations, our “Message the Business” feature, which allows consumers to contact local businesses directly, and the ability for consumers to upload short videos. In 2014, we also introduced Community Ambassadors — a part-time position similar to Community Managers — to foster and support contributors in certain of our smaller communities. |

Enhance Monetization

| ● |

Attract More Businesses. As of December 31, 2014, we were

recognizing revenue from approximately 93.7 thousand local businesses

accounts; with approximately 62.4 million local businesses on our platform

as of that date, we believe there is significant opportunity to increase

the number of local businesses advertising on Yelp. In particular, we

believe that the continued expansion of the Yelp Platform, new business

owner products and comprehensive tools to measure the effectiveness of our

products will encourage businesses to advertise on our platform. For

example, in 2014, we launched a Yelp for Business Owners app, designed to make it easier for

business owners to engage consumers, and Yelp Reservations, a free tool

that allows businesses in the restaurant and nightlife categories to start

taking online reservations. |

| ● |

Expand Our Sales

Efforts. We plan to continue to grow our sales force and explore sales partnerships so

we can reach more businesses. During 2014, we continued to invest aggressively in sales resources. We

believe this ongoing investment in our sales force will drive an increase in local businesses advertising on

Yelp. In addition, we will continue to explore partnerships, such as our YP partnership, for the sale of our

products. |

| ● |

Expand Our

Portfolio of Revenue-Generating Products. We plan to continue to grow and develop

advertising and e-commerce products and partner arrangements that provide incremental value to our

advertisers and business partners to encourage them to increase their advertising budgets allocated towards

our platform. In 2014, we continued to expand the Yelp Platform to provide consumers with a continuous

experience from discovery to completion of transactions across new verticals. For example, we added the

ability for consumers to book spa and salon appointments through Booker, make hotel bookings through Hipmunk and make winery reservations through CellarPass. However, as we explore opportunities to

monetize our products, we remain dedicated to adhering to high standards of user experience. We will not

incorporate advertising or other products or solutions that we believe may excessively degrade the user

experience and potentially alienate users, even if they might result in increased short-term monetization. |

| ● |

Expand Our Reach. We also plan to continue to innovate and introduce our content and solutions on new platforms and distribution channels such as automobile navigation systems, web-enabled televisions and voice-enabled mobile devices. For example, in 2014, we brought Yelp content to wearable devices, such as Intel’s MICA intelligent bracelet. In addition, we continue to have relationships with several companies such as Microsoft Corporation and Apple Inc., under which we make our content and solutions available on their website and consumer devices, respectively. |

5

Marketing

Community Management

We have a team of Community Managers and Community Ambassadors based across the United States and in 28 countries internationally, whose primary goals are to support and grow their local communities of contributors, raise brand awareness and engage with their surrounding communities through:

| ● |

planning and

executing fun and engaging events for the community, such as parties,

outings and activities at restaurants, museums, hotels and other local

places of interest; |

| ● |

getting to know

community members and helping them get to know one another as a way to

foster an offline community experience that can be transferred

online; |

| ● |

promoting Yelp,

including guest appearances on local television and radio, and at local

events such as concerts and street fairs; and |

| ● |

writing weekly e-mail newsletters to share information with the community about local businesses, events and activities. |

Through these activities, we believe our community management team helps us increase awareness of our platform and grow avid communities who are willing to contribute content to our platform. These active contributors to our platform may be invited to attend sponsored social events, but do not receive compensation for their contributions. This community growth drives the network effect whereby contributed reviews expand the breadth and depth of our content base. This expansion draws an increasing number of consumers to access the content on our platform, thus inspiring new and existing contributors to create additional reviews that can be shared with this growing audience.

There are currently active Yelp communities in Argentina, Australia, Austria, Belgium, Brazil, Canada, Chile, the Czech Republic, Denmark, Finland, France, Germany, Hong Kong, Ireland, Italy, Japan, Mexico, The Netherlands, New Zealand, Norway, Poland, Portugal, Singapore, Spain, Sweden, Switzerland, Turkey, the United Kingdom and the United States.

Community Development

The Yelp communities that we have established to date have generally followed a similar development path: a pre-launch content development phase, followed by the hiring of a Community Manager, leading to review growth and consumer activity, which, at scale, supports our sales efforts to local businesses.

We select new locations based on a number of different location-specific criteria, including, but not limited to, population size, local gross domestic product, pre-existing base of reviews on our platform, Internet and wireless penetration, proximity to existing markets, number of local businesses and local ad market growth.

Before launching in any country, we license business listing information from third-party data providers and create individual pages for each business location in the entire country. During this pre-launch preparation phase, we sometimes hire temporary local employees, called “scouts,” to provide additional rich content, such as reviews, photos and hours of operation. To bolster the integrity of the content they provide, we closely monitor their contributions to the platform, prohibit them from reviewing businesses with which they have a conflict of interest and identify them in their public profiles as paid contributors. At launch, consumers can read and write reviews about any business on our platform and contribute information about businesses that are not already listed.

6

After launch, we focus on attracting a community of contributors, consumers and local businesses to our platform by hiring a Community Manager to raise brand awareness and foster local engagement as described above. At scale, our platform reaches a critical mass of reviews, consumers and claimed local business accounts, and we begin an active sales effort with local businesses. Thereafter, our largest expense is related to sales efforts to attract local business advertising customers. In Yelp communities that have attained this level of development, we expect to achieve economies of scale and operating cost leverage.

To further illustrate the development of Yelp communities as they scale, we highlight below our review and revenue metrics for three cohorts of Yelp communities in the United States: the Yelp communities that we launched in 2005-2006; the Yelp communities that we launched in 2007-2008; and the Yelp communities that we launched in 2009-2010.

| U.S. Market Cohort | Number of Yelp Communities(1) |

Average Cumulative Reviews as of December 31, 2014(2) |

Year-Over- Year Growth in Average Cumulative Reviews(3) |

Average Local Advertising Revenue in Q4 2014(4) |

Year-Over- Year Growth in Average Local Advertising Revenue(5) | ||||||||

| 2005 – 2006 Cohort | 6 | 4,728 | 31 | % | $ | 6,532 | 52 | % | |||||

| 2007 – 2008 Cohort | 14 | 1,026 | 34 | % | $ | 1,802 | 63 | % | |||||

| 2009 – 2010 Cohort | 18 | 344 | 43 | % | $ | 470 | 78 | % | |||||

| (1) | A Yelp community, which we previously referred to as a Yelp market, is defined as a city or region in which we have hired a Community Manager. | |

| (2) | Average cumulative reviews is defined as the total cumulative reviews of the cohort as of December 31, 2014 (in thousands), including the reviews that were not recommended or had been removed from our platform, divided by the number of Yelp communities in the cohort. | |

| (3) | Year-over-year growth in average cumulative reviews compares the average cumulative reviews as of December 31, 2014 with the average cumulative reviews as of December 31, 2013. | |

| (4) | Average local advertising revenue is defined as the total local advertising revenue from businesses in the cohort for the quarter ended December 31, 2014 (in thousands), divided by the number of Yelp communities in the cohort. | |

| (5) | Year-over-year growth in average local advertising revenue compares local advertising revenue for the quarter ended December 31, 2014 with local advertising revenue for the quarter ended December 31, 2013. | |

In general, the Yelp communities in our earlier U.S. community cohorts are more populous than those in later cohorts, and we have already entered many of the largest cities in the United States. For these and other reasons, launching additional communities in the United States may not yield results similar to those of our existing U.S. communities.

Advertising

We have not historically spent significantly on marketing programs, but have focused instead on organic and viral growth driven by our community development efforts as described above. However, we believe there may be significant opportunity to increase our traffic and brand awareness through targeted advertising programs and we began selectively testing advertising to consumers through various online and offline channels in the second half of 2014. We plan to continue our selective advertising efforts in 2015. Our marketing expenses may increase if we significantly expand these efforts to attract additional consumers.

7

Sales

We sell our products directly through our sales force, indirectly through partners and online through our website. Our sales force consisted of 1,547 employees as of December 31, 2014 and is located in San Francisco, California; Scottsdale, Arizona; New York, New York; Dublin, Ireland; and Hamburg, Germany. A new sales office in Chicago, Illinois is expected to open in the first quarter of 2015.

Direct Sales. A large majority of our sales force is dedicated to selling our local advertising products. A smaller component of our sales force is responsible for selling display advertisements and brand sponsorships to national advertisers. Local sales representatives are primarily responsible for generating qualified sales leads by identifying and contacting local businesses through direct engagement, direct marketing campaigns and weekly e-mails to claimed local businesses. Although we see opportunity to deepen our relationships with existing customers, to date our sales force has focused on increasing revenue by adding new local advertising accounts. Sales representatives are typically compensated on the basis of revenue booked over a given period.

Sales Partnerships. In 2014, we entered into a partnership with YP under which YP sells certain of our local advertising products as part of a package with its own advertising products to its advertiser base. The products covered by this arrangement include our enhanced profile and Call to Action products. We continue to explore additional partnerships for the sale or bundling of our products.

Self-Service Ads. Our online, or self-service, sales channel allows businesses to purchase local advertising solutions directly from our website. Businesses can purchase performance-based cost-per-click sponsored search advertising directly through this channel.

Technology

Product development and innovation are core pillars of our strategy. We aim to delight our users and business partners with our products. We provide our web-based and mobile services using a combination of in-house and third-party technology solutions and products.

| ● |

Search and Ranking

Technology. We leverage the

data stored on our platform and our proprietary indexing and ranking

techniques to provide our users with contextual, relevant and up-to-date

results to their search queries. For example, a consumer desiring

environmentally friendly carpet cleaners does not have to call individual

cleaners to inquire about their use of chemical-based cleaning solutions.

Instead, the consumer can

search for “environmentally-friendly carpet

cleaners” on Yelp and discover cleaners with the best service and “green”

cleaning products that serve a specific neighborhood. |

| ● |

Recommendation

Software. We employ our

proprietary automated recommendation software to analyze and screen all

reviews submitted to our platform. We believe our recommendation

technology is one of the key contributors to the quality and integrity of

the reviews on our platform and the success of our service. See “—Consumer

Protection Efforts” below

for additional details regarding our recommendation

software. |

| ● |

Mobile Solutions. As mobile device usage has grown over the past several years, we have invested significant resources into the development of a comprehensive mobile platform for consumers supporting the major smartphone operating systems available today, including iOS, Android and Windows Mobile. Over time, we have enhanced the functionality of our mobile platform, such that it provides similar and, in some areas, greater functionality than our website. Some of the innovations we introduced through our mobile platform include “check-ins,” “tips,” “comments,” “Nearby” and “Monocle,” our augmented reality feature. Mobile devices accounted for approximately 65% of all searches on our platform in the quarter ended December 31, 2014, and approximately 43% of our unique visitors in the quarter ended December 31, 2014 were to our mobile website. In December 2014, we also launched a mobile app for business owners, designed to make it easier for them to engage with their customers and manage their Yelp profiles. The Yelp for Business Owners app is currently available for iOS and Android. |

8

| ● |

Advertising Technologies. We use proprietary ad targeting and delivery technologies designed to provide

relevant local advertisements. Our proprietary ad delivery system leverages our unique repository of data

to provide useful ads to users and high value leads to advertisers. |

| ● |

Infrastructure. Our web and mobile platforms are currently hosted from multiple locations. The primary

and secondary locations are within shared data center environments in California and Virginia. We also

host parts of our infrastructure through Amazon Web Services, as well as with third-party leased server

providers. Our web and mobile platforms are designed to have high availability, from the Internet

connectivity providers we choose, to the servers, databases and networking hardware that we deploy. We

design our systems such that the failure of any individual component is not expected to affect the overall

availability of our platform. We also leverage other third-party Internet-based (cloud) services such as

rich-content storage, map-related services, ad serving and bulk processing. |

| ● |

Network Security. Computer viruses, malware, phishing attacks, denial-of-service and other attacks and similar disruptions from unauthorized use of computer systems have become more prevalent in our industry, have occurred on our systems in the past, and we expect them to occur periodically on our systems in the future. For this reason, our platform includes a host of encryption, antivirus, firewall and patch-management technologies designed to help protect and maintain the systems located at data centers as well as other systems and computers across our business. |

Consumer Protection Efforts

Our success depends on our ability to maintain consumer trust in our solutions and in the quality and integrity of the user content and other information found on our platform. We dedicate significant resources to the goal of maintaining and enhancing the quality, authenticity and integrity of the reviews on our platform, primarily through the following methods:

Automated Recommendation Software. We use proprietary software to analyze the reliability and utility of each review submitted to our platform. The software applies the same objective standards to each review based on a wide range of data associated with each review and reviewer — regardless of the business being reviewed. The results of this analysis can change over time as the software factors in new information, which may result in reviews that were previously recommended becoming not recommended, and reviews that were previously not recommended being restored to recommended status. Reviews that the software deems to be the most useful and reliable are published directly on business listing pages, though neither we nor the software purport to establish whether or not any individual review is authentic. As of December 31, 2014, our software was recommending approximately 70% of the reviews submitted to our platform. Reviews that are not recommended are published on secondary pages and do not factor into a business’s overall star rating. As of December 31, 2014, 23% of the reviews submitted to our platform were not recommended but still accessible on our platform.

Sting Operations. We routinely conduct sting operations to identify businesses and individuals who offer or receive cash, discounts or other benefits in exchange for reviews. For example, we may respond to advertisements offering to pay for reviews that are posted on Craigslist, Facebook and other platforms. We also receive and investigate tips from our users about potential paid reviews. If we identify or confirm any such issues through our investigations and operations, we typically pursue one or more of the courses of action described below (each of which we may also employ on a stand-alone basis).

Consumer Alerts Program. We issue consumer alert warnings on business listing pages from time to time when we encounter suspicious activity that we believe is indicative of attempts to deceive or mislead consumers. For example, we may issue a consumer alert if we encounter a business attempting to purchase favorable reviews or a large number of favorable reviews submitted from the same Internet Protocol address. Consumer alerts generally remain in effect for 90 days, or longer if the deceptive practices continue.

9

Coordination with Law Enforcement. We regularly cooperate with law enforcement and consumer protection agencies to investigate and identify businesses and individuals who may be engaged in false advertising or deceptive business practices relating to reviews. For example, in 2013, we assisted the New York Attorney General with “Operation Clean Turf,” an undercover investigation targeting review manipulation that resulted in 19 companies agreeing to pay more than $350,000 in fines to the State of New York.

Legal Action. Our terms of service prohibit the buying and selling of reviews, as well as writing fake reviews. In egregious cases, we take legal action against businesses we believe to be engaged in deceptive practices based on these prohibitions.

Removal of Reviews. We regularly remove reviews from our platform that we believe violate our terms of service, including, without limitation: fake or defamatory reviews; content that has been bought, sold or traded; threatening, harassing or lewd content, as well as hate speech and other displays of bigotry; and content that violates the rights of any third party or any applicable law. Users can access information about reviews that we have removed for a particular business by clicking on a link on the business’s listing page. As of December 31, 2014, 7% of the reviews submitted to our platform had been removed.

Intellectual Property

We rely on federal, state, common law and international rights, as well as contractual restrictions, to protect our intellectual property. We control access to our proprietary technology and algorithms by entering into confidentiality and invention assignment agreements with our employees and contractors, as well as confidentiality agreements with third parties.

In addition to these contractual arrangements, we also rely on a combination of trade secrets, copyrights, trademarks, service marks and domain names to protect our intellectual property. We pursue the registration of our copyrights, trademarks, service marks and domain names in the United States and in certain locations internationally. Our registration efforts have focused on gaining protection of our trademarks for Yelp and the Yelp burst logo, among others. These marks are material to our business and essential to our brand identity as they enable others to easily identify us as the source of the services offered under these marks.

Circumstances outside our control could pose a threat to our intellectual property rights. For example, effective intellectual property protection may not be available in the United States or other countries in which we operate. Also, the efforts we have taken to protect our proprietary rights may not be sufficient or effective. Any significant impairment of our intellectual property rights could harm our business or our ability to compete. Protecting our intellectual property rights is also costly and time-consuming. Any unauthorized disclosure or use of our intellectual property could make it more expensive to do business and harm our operating results.

Companies in the Internet, technology and media industries own large numbers of patents and other intellectual property rights, and frequently request license agreements, or threaten or enter into litigation based on allegations of infringement or other violations of such rights. We do not own any patents and, therefore, may be unable to deter competitors or others from pursuing patent or other intellectual property infringement claims against us. From time to time, we receive notice letters from patent holders alleging that certain of our products and services infringe their patent rights. We are also currently subject to, and expect to face in the future, allegations that we have infringed the trademarks, copyrights, patents and other intellectual property rights of third parties, including our competitors and non-practicing entities. As we face increasing competition and as our business grows, we will likely face more claims of infringement.

10

Competition

The market for information regarding local businesses and advertising is intensely competitive and rapidly changing. We compete for consumer traffic with traditional, offline local business guides and directories as well as other online providers of local and web search. We also compete for a share of local businesses’ overall advertising budgets with traditional, offline media companies and other Internet marketing providers. Our competitors include the following types of businesses:

| ● |

Offline. Competitors include offline media companies

and service providers, many of which have existing relationships with

local businesses. Services provided by competitors range from yellow pages

listings to direct mail campaigns to advertising and listing services in

local newspapers, magazines, television and

radio. |

| ● |

Online. Competitors also include Internet search engines, such as Google, Yahoo! and Bing, review and social media websites as well as various other online service providers. These include regional websites that may have strong positions in particular markets. |

Our competitors may enjoy competitive advantages, such as greater name recognition, longer operating histories, substantially greater market share, established marketing relationships with, and access to, large existing user bases and substantially greater financial, technical and other resources. These companies may use these advantages to offer products similar to ours at a lower price, develop different products to compete with our current solutions and respond more quickly and effectively than we do to new or changing opportunities, technologies, standards or client requirements. Certain competitors could also use strong or dominant positions in one or more markets to gain competitive advantage against us in markets in which we operate.

We compete on the basis of a number of factors. We compete for consumer traffic on the basis of factors including: the reliability of our content; the breadth, depth and timeliness of information; and the strength and recognition of our brand. We compete for local businesses’ advertising budgets on the basis of factors including: the size of our consumer audience; the effectiveness of our advertising solutions; our pricing structure; and recognition of our brand.

Government Regulation

As a company conducting business on the Internet, we are subject to a variety of laws in the United States and abroad that involve matters central to our business, including laws regarding privacy and data retention, distribution of user-generated content, consumer protection and data protection, among others. For example:

| ● |

Privacy. Because we receive, store and process

personal information and other user data, including credit card

information in certain cases, we are subject to numerous federal, state

and local laws around the world regarding privacy and the storing,

sharing, use, processing, disclosure and protection of personal

information and other user data. |

| ● |

Liability for Third-Party Action.

We rely on laws limiting

the liability of providers of online services for activities of their

users and other third parties. |

| ● |

Advertising. We are subject to a variety of laws,

regulations and guidelines that regulate the way we distinguish paid

search results and other types of advertising from unpaid search

results. |

| ● |

Information Security and Data Protection. The laws in several states require companies to implement specific information security controls to protect certain types of information. Likewise, all but a few states have laws in place requiring companies to notify users if there is a security breach that compromises certain categories of their information. |

11

Many of these laws and regulations are still evolving and could be interpreted in ways that harm our business. The application and interpretation of these laws and regulations are often uncertain, particularly in the new and rapidly evolving industry in which we operate. They may be interpreted and applied inconsistently from country to country and inconsistently with our current policies and practices. For example, regulatory frameworks for privacy issues are currently in flux worldwide, and are likely to remain so for the foreseeable future. Similarly, laws providing immunity to websites that publish user-generated content are currently being tested by a number of claims, including actions based on invasion of privacy and other torts, unfair competition, copyright and trademark infringement and other theories based on the nature and content of the materials searched, the ads posted or the content provided by users. Changes in existing laws or regulations or their interpretations, as well as new legislation or regulations, could increase our administrative costs and make it more difficult for consumers to use our platform, resulting in less traffic and revenue. Such changes could also make it more difficult for us to provide effective advertising tools to businesses on our platform, resulting in fewer advertisers and less revenue.

As our business grows and evolves and our solutions are used in a greater number of countries, we will also become subject to laws and regulations in additional jurisdictions. Foreign data protection, privacy and other laws and regulations can be more restrictive than those in the United States. Any failure on our part to comply with these laws may subject us to significant liabilities.

Our Culture and Employees

We take great pride in our company culture and consider it to be one of our competitive strengths. Our culture is at the foundation of our success, and it continues to help drive our business forward as a pivotal part of our everyday operations. It allows us to attract and retain a talented group of employees, create an energetic work environment and continue to innovate in a highly competitive market. As of December 31, 2014, we had 2,711 full-time employees globally.

Our culture extends beyond our offices and into the local communities in which people use Yelp. Our community management team’s responsibilities include supporting the sharing of experiences by consumers in the local markets that they serve and increasing brand awareness. We organize events several times a year to recognize our most important contributors, facilitating face-to-face interactions, building the Yelp brand and fostering the sense of true community in which we believe so strongly. We also engage with small businesses. For example, in 2010, we created the Yelp Small Business Advisory Council as a way to interact with and get feedback from our core community of local business owners. We have also worked with the U.S. Small Business Administration and other partners to educate small business owners across the United States on best practices for online marketing.

In addition, The Yelp Foundation, a non-profit organization established by our board of directors in November 2011, or the Foundation, directly supports consumers and local businesses in the communities in which we operate. In the quarter ended December 31, 2011, our board of directors approved the contribution and issuance to the Foundation of 520,000 shares of our common stock, of which the Foundation had sold 100,000 shares as of December 31, 2014. The Foundation uses the proceeds from the sale of its shares of our common stock to make grants to local non-profit organizations that are actively engaged in supporting community and small business growth. At December 31, 2014, the foundation held 420,000 shares of Class B common stock, representing less than 1% of our outstanding capital stock.

Information About Segment and Geographic Revenue

Information about segment and geographic revenue is set forth in Note 16 of the Notes to Consolidated Financial Statements included elsewhere in this Annual Report.

Seasonality

Our business is affected both by cyclicality in business activity and by seasonal fluctuations in Internet usage and advertising spending. We believe our rapid growth has masked most of the cyclicality and seasonality of our business. As our revenue growth rate slows, we expect that the cyclicality and seasonality in our business may become more pronounced, causing our operating results to fluctuate. In particular, we expect traffic numbers to be weakest in the fourth quarter of the year.

12

Corporate and Available Information

We were incorporated in Delaware on September 3, 2004 under the name Yelp, Inc. We changed our name to Yelp! Inc. in late September 2004 and to Yelp Inc. in February 2012. Our principal executive offices are located at 140 New Montgomery Street, San Francisco, California 94105, and our telephone number is (415) 908-3801. Our website is located at www.yelp.com, and our investor relations website is located at www.yelp-ir.com.

We file or furnish electronically with the U.S. Securities and Exchange Commission, or SEC, our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act. We make copies of these reports available free of charge through our investor relations website as soon as reasonably practicable after we file or furnish them with the SEC.

We webcast our earnings calls and certain events we participate in or host with members of the investment community on our investor relations website. Additionally, we provide notifications of news or announcements regarding our financial performance, including filings with the SEC, investor events, press and earnings releases, and blogs as part of our investor relations website. Investors and others can receive notifications of new information posted on our investor relations website in real time by signing up for email alerts and RSS feeds.

Information contained on or accessible through our websites is not incorporated into, and does not form part of, this Annual Report or any other report or document we file with the SEC, and any references to our websites are intended to be inactive textual references only.

Our operations and financial results are subject to various risks and uncertainties, including those described below, which could adversely affect our business, financial condition, results of operations, cash flows and the trading price of our Class A common stock. You should carefully consider the risks and uncertainties described below before making an investment decision. Additional risks not presently known to us or that we currently believe are immaterial may also significantly impair our business operations.

Risks Related to Our Business and Industry

If we are unable to increase traffic to our website and mobile app, or user engagement on our platform declines, our revenue, business and operating results may be harmed.

We derive substantially all of our revenue from the sale of advertising, primarily through impression- and click-based advertising. Because traffic to our platform determines the number of ads we are able to show, affects the value of those ads to businesses and influences the content creation that drives further traffic, slower growth rates may harm our business and financial results. As a result, our ability to grow our business depends on our ability to increase traffic to and user engagement on our platform. Our traffic could be adversely affected by factors including:

| ● | Reliance on Internet Search Engines. As discussed in greater detail below, we rely on Internet search engines to drive traffic to our platform. However, the display, including rankings, of unpaid search results can be affected by a number of factors, many of which are not in our direct control, and may change frequently. For example, a search engine may change its ranking algorithms, methodologies or design layouts. As a result, links to our website may not be prominent enough to drive traffic to our website, and we may not be in a position to influence the results. Although Internet search engine results have allowed us to attract a large audience with minimal organic traffic acquisition costs to date, if they fail to drive sufficient traffic to our platform in the future, we may need to increase our marketing expenses, which could harm our operating results. |

| ● | Increasing Competition. The market for information regarding local businesses is intensely competitive and rapidly changing. If the popularity, usefulness, ease of use, performance and reliability of our products and services do not compare favorably to those of our competitors, traffic may decline. |

| ● | Review Concentration. Our restaurant and shopping categories together accounted for approximately 42% of the businesses that had been reviewed on our platform and approximately 58% of the cumulative reviews through December 31, 2014. If the high concentration of reviews in these categories generates a perception that our platform is primarily limited to these categories, traffic may not increase or may decline. |

13

| ● |

Our Recommendation

Software. If our automated

software does not recommend helpful content or recommends unhelpful

content, consumers may reduce or stop their use of our platform. While we

have designed our technology to avoid recommending content that we believe

to be unreliable or otherwise unhelpful, we cannot guarantee that our

efforts will be successful. |

| ● |

Content Scraping. From time to time, other companies copy

information from our platform, through website scraping, robots or other

means, and publish or aggregate it with other information for their own

benefit. This may make them more competitive and may decrease the likelihood

that consumers will visit our platform to find the local businesses and information they seek. Though we strive to detect and prevent

this third-party conduct, we may not be able to detect it in a timely manner

and, even if we could, may not be able to prevent it. In some cases,

particularly in the case of websites operating outside of the United

States, our available remedies may be inadequate to protect us against

such conduct. |

| ● |

Internet Access. The adoption of any laws or regulations that

adversely affect the growth, popularity or use of the Internet, including

laws impacting Internet neutrality, could decrease the demand for our

services. Similarly, any

actions by companies that provide Internet access that degrade, disrupt or

increase the cost of user access to our platform could

undermine our operations and result in the loss of

users. |

| ● |

Macroeconomic Conditions. Consumer purchases of discretionary items generally decline during recessions and other periods in which disposable income is adversely affected. As a result, adverse economic conditions may impact consumer spending, particularly with respect to local businesses, which in turn could adversely impact the number of consumers visiting our platform. |

We also anticipate that our traffic growth rate will continue to slow over time, and potentially decrease in certain periods, as our business matures and we achieve higher penetration rates. In particular, the number of major geographic markets, especially within the United States, we have not yet entered is declining; further expansion in smaller markets may not yield similar results or sustain our growth. That our traffic growth has slowed in recent quarters even as we have expanded our international presence is a reflection of this trend. As our traffic growth rate slows, our success will become increasingly dependent on our ability to increase levels of user engagement on our platform. This dependence may increase as the portion of our revenue derived from performance-based advertising increases. A number of factors may negatively affect our user engagement, including if:

| ● |

users engage with

other products, services or activities as an alternative to our

platform; |

| ● |

there is a decrease

in the perceived quality of the content contributed by our

users; |

| ● |

we fail to introduce

new and improved products or features, or we introduce new products or

features that do not effectively address consumer needs or otherwise alienate consumers; |

| ● |

technical or other

problems negatively impact the availability and reliability of our

platform or otherwise affect the user

experience; |

| ● |

users have difficulty

installing, updating or otherwise accessing our platform as a result of

actions by us or third parties that we rely on to distribute our

products; |

| ● |

users believe that

their experience is diminished as a result of the decisions we make with

respect to the frequency, relevance and prominence of the advertising we

display; and |

| ● |

we do not maintain our brand image or our reputation is damaged. |

14

We rely on Internet search engines and application marketplaces to drive traffic to our platform, certain providers of which offer products and services that compete directly with our solutions. If links to our website and applications are not displayed prominently, traffic to our platform could decline and our business would be adversely affected.

Our success depends in part on our ability to attract users through unpaid Internet search results on search engines like Google and Bing. The number of users we attract from search engines to our website (including our mobile website) is due in large part to how and where information from and links to our website are displayed on search engine result pages. The display, including rankings, of unpaid search results can be affected by a number of factors, many of which are not in our direct control, and may change frequently. For example, a search engine may change its ranking algorithms, methodologies or design layouts. As a result, links to our website may not be prominent enough to drive traffic to our website, and we may not know how or otherwise be in a position to influence the results. Beginning in the second quarter of 2014, for example, Google made changes to its algorithms and methodologies that may be contributing to the recent slowing of our traffic growth rate and decline in traffic in the fourth quarter of 2014. We cannot predict the long-term impact of these changes. Although traffic to our mobile app is less reliant on search results than traffic to our website, growth in mobile device usage may not decrease our overall reliance on search results if mobile users use our mobile website rather than our mobile app. In fact, growth in mobile device usage may exacerbate the risks associated with how and where our website is displayed in search results because mobile device screens are smaller than personal computer screens and therefore display fewer search results.

We also rely on application marketplaces, such as Apple’s App Store and Google’s Play, to drive downloads of our applications. In the future, Apple, Google or other marketplace operators may make changes to their marketplaces that make access to our products more difficult. For example, our applications may receive unfavorable treatment compared to the promotion and placement of competing applications, such as the order in which they appear within marketplaces. Similarly, if problems arise in our relationships with providers of application marketplaces, our user growth could be harmed.

In some instances, search engine companies and application marketplaces may change their displays or rankings in order to promote their own competing products or services or the products or services of one or more of our competitors. For example, Google has integrated its local product offering, Google + Local, with certain of its products, including search. The resulting promotion of Google’s own competing products in its web search results has negatively impacted the search ranking of our website. Because Google in particular is the most significant source of traffic to our website, accounting for more than half of the visits to our website from Internet searches during the three months ended December 31, 2014, our success depends on our ability to maintain a prominent presence in search results for queries regarding local businesses on Google. As a result, Google’s promotion of its own competing products or similar actions by Google in the future that have the effect of reducing our prominence or ranking on its search results could have a substantial negative effect on our business and results of operations.

Consumers are increasingly using mobile devices to access online services. If our mobile platform and mobile advertising products are not compelling, or if we are unable to operate effectively on mobile devices, our business could be adversely affected.

The number of people who access information about local businesses through mobile devices, including smartphones, tablets and handheld computers, has increased dramatically over the past few years and is expected to continue to increase. Although many consumers access our platform both on their mobile devices and through personal computers, we have seen substantial growth in mobile usage as we have developed our mobile solutions. We anticipate that growth in use of our mobile platform will be the driver of our growth for the foreseeable future and that usage through personal computers may continue to decline worldwide. As a result, we must continue to drive adoption of and user engagement on our mobile platform, and our mobile app in particular. If we are unable to drive continued adoption of and engagement on our mobile app, our business may be harmed and we may be unable to decrease our reliance on traffic from Google and other search engines.

In order to attract and retain engaged users of our mobile platform, the mobile products and services we introduce must be compelling. However, the ways in which users engage with our platform and consume content has changed over time, and we expect it will continue to do so as users increasingly engage via mobile. This may make it more difficult to develop mobile products that consumers find useful or provide them with the information they seek, and may also negatively affect our content if users do not continue to contribute high quality content on their mobile devices. In addition, building an engaged base of mobile users may also be complicated by the frequency with which users change or upgrade their mobile services. In the event users choose mobile devices that do not already include or support our mobile app or do not install our mobile app when they change or upgrade their devices, our traffic and user engagement may be harmed.

15

Our success is also dependent on the interoperability of our mobile products with a range of mobile technologies, systems, networks and standards that we do not control, such as mobile operating systems like Android and iOS. We may not be successful in developing products that operate effectively with these technologies, systems, networks and standards or in creating, maintaining and developing relationships with key participants in the mobile industry, some of which may be our competitors. Any changes that degrade the functionality of our mobile products, give preferential treatment to competitive products or prevent us from delivering advertising could adversely affect mobile usage and monetization. As new mobile devices and platforms are released, it is difficult to predict the problems we may encounter in developing products for these alternative devices and platforms, and we may need to devote significant resources to the creation, support and maintenance of such products. If we experience difficulties in the future integrating our mobile app into mobile devices, or we face increased costs to distribute our mobile app, our user growth and operating results could be harmed.

In addition, if our mobile advertising products prove ineffective, our advertisers may stop or reduce their advertising with us. Although we currently deliver advertising on our mobile app and mobile website, the mobile advertising market remains a new and evolving market; as new devices and platforms are released, users may begin consuming content in a manner that is more difficult to monetize. Given our limited experience in monetizing our mobile products, we may not be able to generate meaningful revenue from our mobile products despite the expected growth in mobile usage. For example, we may be unable to attract new advertisers if our mobile advertising products are not compelling or we fail to continue to innovate and introduce enhanced mobile solutions. Similarly, if we incur excessive expenses in these efforts or our products are insufficiently profitable, our ability to grow revenue would be negatively affected. However, if our mobile solutions alienate our user base our business may also suffer. Accordingly, we must also balance these considerations against our commitment to prioritizing the quality of user experience over short-term monetization, which we may not do effectively.

If our users fail to contribute high quality content or their contributions are not valuable to other users, our traffic and revenue could be negatively affected.

Our success in attracting users depends on our ability to provide consumers with the information they seek, which in turn depends on the quantity and quality of the content contributed by our users. We believe that as the depth and breadth of the content on our platform grow, our platform will become more widely known and relevant to broader audiences, thereby attracting new consumers to our service. However, if we are unable to provide consumers with the information they seek, they may stop or reduce their use of our platform, and traffic to our website and on our mobile app will decline. If our user traffic declines, our advertisers may stop or reduce the amount of advertising on our platform and our business could be harmed. Our ability to provide consumers with valuable content may be harmed:

| ● | if our users do not contribute content that is helpful or reliable; |

| ● | if our users remove content they previously submitted; |

| ● | as a result of user concerns that they may be harassed or sued by the businesses they review, instances of which have occurred in the past and may occur again in the future; and |

| ● | as users increasingly contribute content through our mobile platform, because content contributed through mobile devices tends to be shorter than desktop contributions. |

Similarly, if our platform does not provide current information about local businesses or users do not perceive reviews on our platform as relevant, our brand and business could be harmed. For example, we do not phase out or remove dated reviews, and consumers may view older reviews as less relevant, helpful or reliable than more recent reviews.

16

If we fail to maintain and expand our base of advertisers, our revenue and our business will be harmed.

Our ability to grow our business depends on our ability to maintain and expand our advertiser base. To do so, we must convince existing and prospective advertisers alike that our advertising products offer a material benefit and can generate a competitive return relative to other alternatives. Our ability to do so depends on factors including:

| ● | Acceptance of Online Advertising. We believe that the continued growth and acceptance of our online advertising products will depend on the perceived effectiveness and the acceptance of online advertising models generally, which is outside of our control. Many advertisers still have limited experience with online advertising and, as a result, may continue to devote significant portions of their advertising budgets to traditional, offline advertising media, such as newspapers or print yellow pages directories. |

| ● | Competitiveness of Our Products. We must deliver ads in an effective manner and provide accurate analytics and measurement solutions that demonstrate the value of our advertising products compared to those of our competitors. Similarly, if the pricing of our advertising products does not compare favorably to those of our competitors, advertisers may reduce their advertising with us or choose not to advertise with us at all. |

| ● | Traffic Quality. The success of our advertising program depends on delivering positive results to our advertising customers. Low-quality or invalid traffic, such as robots, spiders and the mechanical automation of clicking, may be detrimental to our relationships with advertisers and could adversely affect our advertising pricing and revenue. If we fail to detect and prevent click fraud or other invalid clicks on ads, the affected advertisers may experience or perceive a reduced return on their investments, which could lead to dissatisfaction with our products, refusals to pay, refund demands or withdrawal of future business. |

| ● | Perception of Our Platform. Our ability to compete effectively for advertiser budgets depends on our reputation and perceptions regarding our platform. For example, we may face challenges expanding our advertiser base in businesses outside the restaurant and shopping categories if businesses believe that consumers perceive the utility of our platform to be limited to finding businesses in these categories. The ratings and reviews that businesses receive from our users may also affect their advertising decisions. Favorable ratings and reviews, on the one hand, could be perceived as obviating the need to advertise. Unfavorable ratings and reviews, on the other, could discourage businesses from advertising to an audience that they perceive as hostile or cause them to form a negative opinion of our products and user base. |

| ● | Macroeconomic Conditions. Adverse macroeconomic conditions can have a negative impact on the demand for advertising, particularly with respect to online advertising products. We rely heavily on small and medium-sized businesses, which often have limited advertising budgets and may be disproportionately affected by economic downturns. In addition, such business may view online advertising as lower priority than offline advertising. |

As is typical in our industry, our advertisers generally do not have long-term obligations to purchase our products. Their decisions to renew depend on the degree of satisfaction with our products as well as a number of factors that are outside of our control, including their ability to continue their operations and spending levels. Small and medium-sized local businesses in particular have historically experienced high failure rates. As a result, we may experience attrition in our advertisers in the ordinary course of business resulting from several factors, including losses to competitors, declining advertising budgets, closures and bankruptcies. To grow our business, we must continually add new advertisers to replace advertisers who choose not to renew their advertising, or who go out of business or otherwise fail to fulfill their advertising contracts with us, which we may not be able to do.

If we fail to expand our operations effectively, including in international markets where we have limited operating experience and may be subject to increased risks, our revenue and business will be harmed.

We intend to expand our operations into new markets, both domestically and abroad. Our expansion into new markets places us in competitive environments with which we are unfamiliar and involves various challenges, such as expanding our sales force and community management personnel to reach those new markets, and encountering different and potentially lower levels of user engagement or advertiser demand in some or all of these markets. Our current and future expansion plans will require significant resources and management attention, and the returns on such investments may not be achieved for several years, or at all.

17

Because we have already entered many of the largest markets in the United States and further expansion in smaller markets may not yield similar results, our continued growth depends on our ability to expand effectively in international markets. We have a limited operating history in international markets, which makes it difficult to evaluate our future prospects and may increase the risk that we will not be successful. If the markets we have targeted for international expansion do not develop as we expect, or if we fail to address the needs of those markets, our business will be harmed. Expanding internationally may also subject us to risks that we have not faced before or that increase our exposure to risks that we currently face, including risks associated with:

| ● | operating a rapidly growing business in an environment of multiple languages, cultures, customs, legal systems, regulatory systems and commercial infrastructures; |

| ● | recruiting and retaining qualified, multi-lingual employees, including sales personnel; |

| ● | increased competition from local websites and guides, and potential preferences by local populations for local providers; |

| ● | our ability to achieve prominent display of our content in unpaid search results, which may be more difficult in newer markets where we may have less content and more competitors than in more established markets; |

| ● | providing solutions in different languages for different cultures, which may require that we modify our solutions and features to ensure that they are culturally relevant in different countries; |

| ● | compliance with applicable foreign laws and regulations, including different privacy, censorship and liability standards; |

| ● | the enforceability of our intellectual property rights; |

| ● | credit risk and higher levels of payment fraud; |

| ● | currency exchange rate fluctuations; |

| ● | compliance with anti-bribery laws, including but not limited to the Foreign Corrupt Practices Act and the U.K. Bribery Act; |

| ● | foreign exchange controls that might prevent us from repatriating cash earned outside the United States; |

| ● | political and economic instability in some countries; |

| ● | double taxation of our international earnings and potential adverse tax consequences due to changes in the tax laws of the United States or foreign jurisdictions in which we operate; and |

| ● | higher costs of doing business internationally. |

We may acquire other companies or technologies, which could divert our management’s attention, result in additional dilution to our stockholders and otherwise disrupt our operations and harm our operating results. We may also be unable to realize the expected benefits and synergies of any acquisitions.