Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Manitex International, Inc. | d775933d8k.htm |

Manitex

International, Inc. Corporate Presentation

(NASDAQ: MNTX)

Q2 2014

Exhibit 99.1 |

2

Forward Looking Statements & Non-GAAP Measures

Safe Harbor Statement under the U.S. Private Securities Litigation Reform Act of 1995: This

presentation contains statements that are forward-looking in nature which express

the beliefs and expectations of management including statements regarding the

Company’s expected results of operations or liquidity; statements concerning projections,

predictions, expectations, estimates or forecasts as to our business, financial and

operational results and future economic performance; and statements of

management’s goals and objectives and other similar expressions concerning matters

that are not historical facts. In some cases, you can identify forward-looking

statements by terminology such as “anticipate,”

“estimate,”

“plan,”

“project,”

“continuing,”

“ongoing,”

“expect,”

“we believe,”

“we intend,”

“may,”

“will,”

“should,”

“could,”

and similar expressions. Such statements are based on current plans, estimates and

expectations and involve a number of known and unknown risks, uncertainties and other

factors that could cause the Company's future results, performance or achievements to

differ significantly from the results, performance or achievements expressed or

implied

by

such

forward-looking

statements.

These

factors

and

additional

information

are

discussed

in

the

Company's

filings with the Securities and Exchange Commission and statements in this presentation should

be evaluated in light of these important factors. Although we believe that these

statements are based upon reasonable assumptions, we cannot guarantee future results.

Forward-looking statements speak only as of the date on which they are made, and the

Company undertakes no obligation to update publicly or revise any forward-looking

statement, whether as a result of new information, future developments or otherwise.

Non-GAAP

Measures:

Manitex

International

from

time

to

time

refers

to

various

non-GAAP

(generally

accepted

accounting

principles) financial measures in this presentation. Manitex believes that this

information is useful to understanding its operating results without the impact of

special items. See Manitex’s Q2 2014 earnings release on the Investor Relations

section of our website www.manitexinternational.com for a description and/or reconciliation of

these measures. Nasdaq: MNTX

8/15/2014 |

Company

Snapshot Manitex

International, Inc.

Niches

Served

Company

Origin

Energy exploration and

field development

(includes Canadian oil

sands and recent oil and

natural gas initiatives

throughout U.S.)

Power line construction

Military

Railroads

Ports

Government/agency

Launched as a private

company in 2003

Publicly traded on

NASDAQ: MNTX

Steady organic growth

Industry consolidator:

consistently adding

branded product lines

through M&A since

going public in 2006

3

8/15/2014

Nasdaq: MNTX

Global provider of highly

specialized and custom

configured cranes-

Straight-mast and

knucklebooms

Materials and container

handling equipment also

sold through

dealerships, globally |

•

Leading Italian

manufacturer of truck-

mounted hydraulic knuckle

boom cranes

•

Diverse product lines

ranging up to 108 ton

meters in lifting capacity;

sales in 50 countries

•

Engineered lifting equipment

•

Manitex boom trucks

•

SkyCrane aerial platforms

•

Sign cranes

•

RT forklifts

•

Special mission-oriented

vehicles

•

Carriers

•

Heavy material handling

•

Transporters & steel mill

equipment

•

Manufacturer of container

handling equipment for

the global port & inter-

modal sectors

•

Products: reach stackers,

laden and unladen

container forklifts &

straddle carriers

Product Overview

4

Nasdaq: MNTX

*

* PM transaction expected to close Q4 2014

8/15/2014 |

Competitive

Positioning 5

Core Competencies

Strong brand history

Acknowledged product

development record

International dealers enable us to

follow demand

Focused on specialized equipment

and niche end-markets

Products

Niche markets

Broad end-user base

Highly customized/specialized;

will configure-to-order

Parts and service an important

part of business model

Lower capital commitment for a boom truck vs.

competitors’

custom cranes of similar lifting capacity

Usually less or no special permitting vs. competitors’

custom cranes of similar lifting capacity

8/15/2014

Nasdaq: MNTX

Superior ROI |

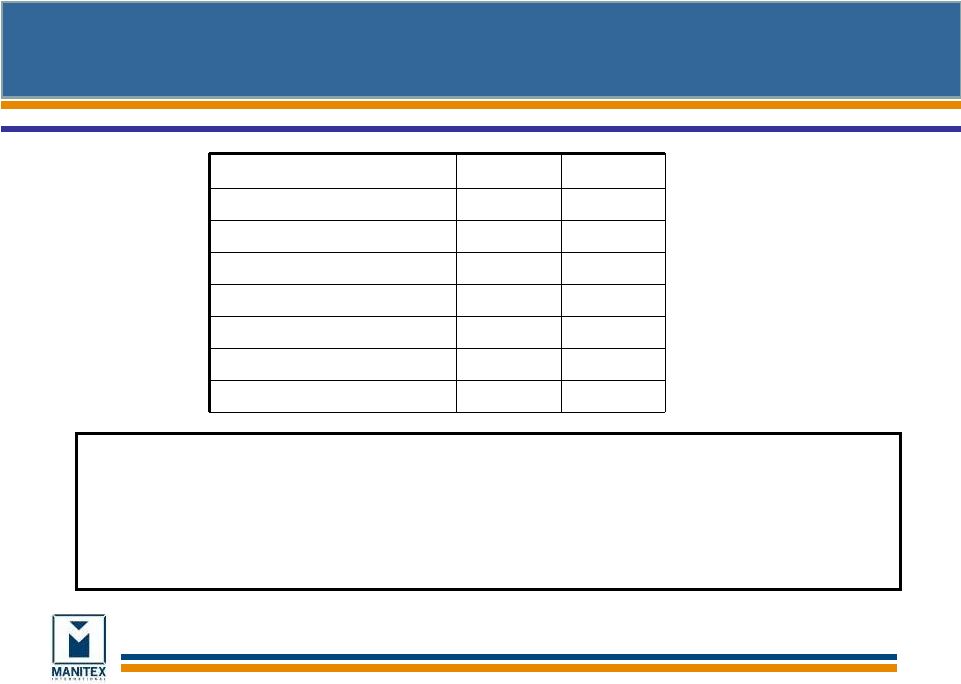

Financial Summary

$000, except %

2009

2010

2011

2012

2013

Revenues

$55,887

$95,875

$142,291

$205,249

245,072

Gross Margin (%)

20.0%

24.3%

20.6%

19.7%

19.0%

EBITDA

$1,982

$8,676

$11,120

$17,957

21,483

EBITDA Margin (%)

3.5%

9.0%

7.8%

8.7%

8.8%

Net income

$3,639

(1)

$2,109

$2,780

$8,077

$10,178

Backlog

$22,122

$39,905

$83,700

$130,352

$77,281

(1)

2009 GAAP Net Income includes gain on bargain purchase of $3,815

Key Statistics

Stock Price

(at 8/13/14)

$12.05/share

Market Cap (at

8/13/14) $166.6M

Total Ent. Value

(8/13/14)

$223.2M

2013 Revenue

$245.1M

2013 Net Income

$10.2M

2013 EBITDA

$21.5M

Ticker / Exchange

MNTX/NasdaqCM

Capitalization

Basic Shares O/S (at

6/30/14) 13.8M

Diluted Shares O/S

(at 6/30/14)

13.9M

Total Debt (at

6/30/14) $59.9M

6

8/15/2014

Nasdaq: MNTX |

Consistently Growing

Our Top- and Bottom-

Lines ($ Millions)

7

Historically

Consistent

EBITDA

Margin of

9.0%

2009-2012

CAGR was

45.3% (pre-

PM Group)

$M

Opportunity

2016E

2015E |

Pending

Acquisition-Agreement with PM-Group, July 2014

8

8/15/2014

Nasdaq: MNTX

•

Consideration of $107 million, subject to post-closing adjustments and

earnout provisions, is expected to consist of a combination of debt,

equity, and the assumption of $68 million in PM debt and liabilities.

(Final purchase price subject to adjustment based on market

conditions at close; assumed debt remains separate with recourse only to

PM.) •

The acquisition is expected to close in the fourth quarter of 2014,

subsequent to the pending Italian Court approval of a debt restructuring

plan.

•

PM-Group has trailing twelve months revenues of $106 million and adjusted

EBITDA margins of approximately 9% . |

Acquisition

Rationale: 9

Acquisition fits into Manitex International stated growth objectives to achieve

growth both organically and through acquisitions. PM-Group

represents our largest acquisition to date.

PM-Group is a strong strategic fit:

•

Adds product classes -

knuckle boom cranes and truck mounted aerial

platforms-

both are a highly desired product categories with strong demand.

•

Adds new manufacturing facilities/capacity

•

Adds new distributors, geographies and niche markets

Accelerates Manitex growth both within Europe and globally

Compelling synergies create value for shareholders

•

Accretion to EBITDA and Earnings expected in 2014

8/15/2014

Nasdaq: MNTX |

The Knuckleboom

Market- $2.3 Billion Globally

(Management Estimates)

10

8/15/2014

Nasdaq: MNTX

•

Large Market of $2.3 BN is roughly 2X the size of

the straight-mast boom truck market (global)

•

PM has a geographically diverse customer base with

70% of its business outside Europe

•

North American knuckleboom market is growing

•

Opportunity to increase PM Group’s No. American

market presence through Manitex’s distribution

network |

Lifting Equipment

Market Overview—Straight Mast

Principal products: boom truck cranes that vary in height

& tonnage capacity

Smaller tonnage cranes (<30 tons) more focused on

general construction markets; larger cranes (30+ tons)

focus on power line construction and energy

Larger tonnage cranes in higher demand since economic

downturn

Boom truck cranes typically less expensive than rough

terrain and all terrain cranes

Broader market: ~65% of cranes shipped in the smaller

tonnage range; ~75% of Manitex shipments have been in

larger tonnage

Focus on being a niche player allows specialization tailored

towards customers’

needs

Production distribution skewed toward larger tonnage

machines

First to launch 50-ton crane (May 2007)

Have developed a series of products around the demand

for larger tonnage cranes

11

Nasdaq: MNTX

Market Overview

Manitex Market Position

8/15/2014 |

Replacement

Parts & Service Consistent Recurring Revenue

12

•

Consistent recurring revenue stream throughout the cycle

•

Spares relate to swing drives, rotating components, and booms

among others, many of which are proprietary

–

Serve additional brands

–

Service team for crane equipment

–

Automated proprietary system implemented in principal operations

Nasdaq: MNTX

8/15/2014 |

Revenue Growth

Drivers 13

Nasdaq: MNTX

8/15/2014 |

Investment

Highlights 14

•

Niche markets with

solid demand

drivers for products

•

Steadying of

construction

environment and

energy markets

driving demand

•

Diverse end

markets result in

risk mitigation

•

Customer focused

design strategy

•

Diversified product

offering

•

Quickly adaptable

to changes in

demand

•

Commitment to

innovation,

research, &

product

development

•

Revenue and

earnings growth

have consistently

outpaced market

and industrial peers

since 2009

•

Backlog at $103M

as of 6/30/2014

•

Manitex dealer

network provides

footprint for on-

going North

American expansion

•

PM Group has little

penetration in US

and has excellent

non-US and non-

Europe customer

base

•

No Customer

represents over 10%

of annual revenues

•

Seasoned senior

management:

over 70 years of

collective industry

experience

•

Successfully

integrated

multiple

acquisitions

•

Significant

management

ownership

Growth in

End Markets

Flexible

Operating

Model

Broad Industry

& Geographic

Distribution

Growth in

Key Financial

Metrics

Experienced

Management

Nasdaq: MNTX

A

consolidator

in

the

lifting

and

hauling

industry,

Manitex

International

is

among

the

market

leaders

in

each

of

its

addressable

markets

with

an

estimated

$4

BN

in

annual

sales

8/15/2014 |

15

Financial Overview

Manitex International, Inc.

Q2 2014

Nasdaq: MNTX

8/15/2014 |

Key Figures

- Quarterly

$235M

16

$6,293

$5,513

$4,722

$2,986

$2,655

$1,877

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

$10,000

$0

$20,000

$40,000

$60,000

Q2-2014

Q2-2013

Q1-2014

Revenue

EBITDA

Net Income

USD thousands except as noted

Q2-2014

Q2-2013

Q1-2014

Net sales

$68,399

$62,554

$62,576

Gross profit

13,144

12,260

11,604

Gross margin %

19.2%

19.6%

18.5%

Operating expenses

7,966

7,656

7,993

Net Income

2,986

2,655

1,877

EBITDA

6,293

5,513

4,722

EBITDA % of Sales

9.2%

8.8%

7.5%

Backlog ($ million)

102.5

96.6

100.0

Nasdaq: MNTX

8/15/2014

$68,399

$62,554

$62,576 |

Summary Balance

Sheet 17

$000s

30-Jun-14

31-Dec-13

31-Dec-12

31-Dec-11

31-Dec-10

Current Assets

139,898

$122,037

$104,777

$71,209

$54,703

Fixed Assets

10,477

11,143

10,297

11,017

10,659

Other Long-Term Assets

48,340

49,550

36,430

39,365

40,155

Total Assets

198,715

$182,730

$151,504

$121,591

$105,517

Current Liabilities

55,506

$48,016

$43,351

$30,177

$23,011

Long-Term Liabilities

52,711

49,723

48,620

44,620

39,232

Total Liabilities

108,217

97,739

91,971

74,797

62,243

Shareholders’

Equity

90,498

84,991

59,533

46,794

43,274

Total Liabilities & Shareholders’

Equity

198,715

$182,730

$151,504

$121,591

$105,517

Nasdaq: MNTX

8/15/2014 |

18

Working Capital

“Focused

manufacturer of

engineered lifting

equipment”

$000

Q2-2014

Q4-2013

Working Capital

$84,392

$73,873

Days sales outstanding (DSO)

70

53

Days payable outstanding (DPO)

50

45

Inventory turns

2.8

2.9

Current ratio

2.5

2.5

Operating working capital

102,778

86,682

Operating working capital % of

annualized LQS

37.6%

33.1%

•Working capital increase Q2-2014 v Q4-2013, of $10.5m:

•Trade & Other Receivables $13.2m, Inventory $7.0m, partially offset

by reduced cash $2.9m, increased accounts payable $4.2m, short term

working capital borrowings $2.5m and accruals & other current liabilities $0.9m.

•Inventory increase includes governmental units shipped not recognized as

revenue in Q2 •Working capital ratios: DSO increase from a higher

proportion of international sales and timing of payments on

military |

19

“Focused

manufacturer of

engineered lifting

equipment”

$000

Q2-2014

Q4-2013

Total Cash

$3,189

$6,091

Total Debt

59,828

54,231

Total Equity

90,498

84,991

Net capitalization

147,137

133,131

Net debt / capitalization

38.5%

36.2%

Trailing 12 month EBITDA

$22,864

$21,483

Debt / EBITDA

x2.6

x2.5

•Increase in debt of $5.6 million from 12/31/13 principally reflects increase

in working capital facilities in N.A. ($4.1m) and Italy ($2.3m) funding

increased activity levels. •Other debt repayments in the quarter of $0.6

million •N. American revolver facilities, based on available collateral

at 6/30/14 was $50.8m. •N. American revolver availability at 6/30/14 of

$6.7m. •

Net capitalization is the sum of debt plus equity minus cash

•

Net debt is total debt less cash

Debt and Liquidity |

Experienced

Management Team 20

Name & Title

Experience

David Langevin

Chairman & CEO

20+ years principally with Terex

Andrew Rooke

President & COO

20+ years principally with Rolls Royce, GKN Sinter Metals,

Off-Highway & Auto Divisions

David Gransee

CFO & Treasurer

Formerly with Arthur Andersen, 15+ years with Eon Labs

(formerly listed)

Robert Litchev

President –

Manufacturing Operations

10+ years principally with Terex

Scott Rolston

SVP Strategic Planning

13+ years principally with Manitowoc

Bruce Peterson

SVP Sales and Marketing

20+ years principally with Manitowoc

Nasdaq: MNTX

8/15/2014 |

Company

Timeline 21

Nasdaq: MNTX

July 2013: Acquires

Sabre Manufacturing LLC

December 2009: Acquires

Load King Trailers

July 2009: Acquires

Badger Equipment Co.

November 2006:

Veri-Tek

Acquires LiftKing

July 2007: VCC

acquires Noble

forklift

May 2008: Name changed to Manitex International

and listed on Nasdaq (MNTX)

October 2008:

Crane &

Machinery and

Schaeff Forklift

acquired

July 2006: Manitex

merges into Veri-Tek,

Intl. (VCC)

July 2010: CVS

Operating Agreement

July 2011: Closes

Acquisition of CVS

January 2003:

Manitowoc

divests

Manitex

March 2002:

Manitowoc

(NYSE:MTW)

acquires Grove

November 2013:

Acquires Valla SpA

of Piacenza, Italy

July 2014: Agreement to

Acquire

PM Group SpA

8/15/2014 |

Operating

Companies 22

Brand

Products

End Markets

Drivers

•

Boom trucks and cranes

•

Sign cranes

•

Parts

•

Energy exploration

•

Power transmission

•

Industrial projects

•

Infrastructure development

•

Strong end market demand for specialized,

competitively differentiated products for oil, gas,

and energy sectors

•

Product development

•

Rough terrain cranes

•

Specialized construction

equipment

•

Parts

•

Railroad

•

Construction

•

Refineries

•

Municipality

•

Equipment replacement cycle in small tonnage

flexible cranes for refinery market

•

More efficient product offering across end

markets

•

Rough terrain forklifts

•

Special mission-oriented vehicles

•

Custom specialized carriers

•

Parts

•

Military

•

Utility

•

Ship building

•

Commercial

•

Steady, profitable growth from both commercial

and military application of products

•

Custom trailers

•

Hauling systems for heavy

equipment transport

•

Parts

•

Energy

•

Mining

•

Railroad

•

Commercial construction

•

U.S. energy exploration build-out

•

Oil and gas exploration

•

General infrastructure construction

•

Reach stackers

•

Container handling forklifts

•

Parts

•

Global container market

•

International container market and global trade

•

Re-establishing customer relationships and select

product categories

•

Specialized equipment for liquid

storage & containment

•

8,000-21,000 gallon capacities

•

Large client base in energy sector

•

Petrochemical

•

Waste management

•

Oil & gas drilling

•

Reputation for quality & innovation

•

Serves a market of over $1B annually

•

At acquisition, TTM (3/31/13) revenues ~ $39.1M,

adjusted EBITDA ~ $4.5M, EBIT ~ $4.2M

Nasdaq: MNTX

8/15/2014 |

Operating

Companies 23

Brand

Products

End Markets

Drivers

•

Precision pick & carry cranes

•

Automotive

•

Chemical / petrochemical

•

Industrial projects

•

Infrastructure development

•

Aerospace

•

Construction

•

Strong end market demand for specialized,

competitively differentiated products

•

Environmental (electric) or hazardous (spark free)

developments

•

Product development

Nasdaq: MNTX

•

Knuckleboom cranes

•

Aerial Platforms

•

Energy

•

Construction

•

Infrastructure

•

Utilities

•

Growing acceptance of knucklebooms in North

American markets

•

Oil and gas exploration creating demand

•

Product development

8/15/2014 |