Attached files

| file | filename |

|---|---|

| 8-K - 8-K - HANCOCK WHITNEY CORP | d664232d8k.htm |

Exhibit 99.1

For Immediate Release

January 23, 2014

For More Information

Trisha Voltz Carlson

SVP, Investor Relations Manager

504.299.5208

trisha.carlson@hancockbank.com

Hancock reports fourth quarter 2013 financial results

Higher core net interest income and lower operating expense largely offset declining purchased loan accretion

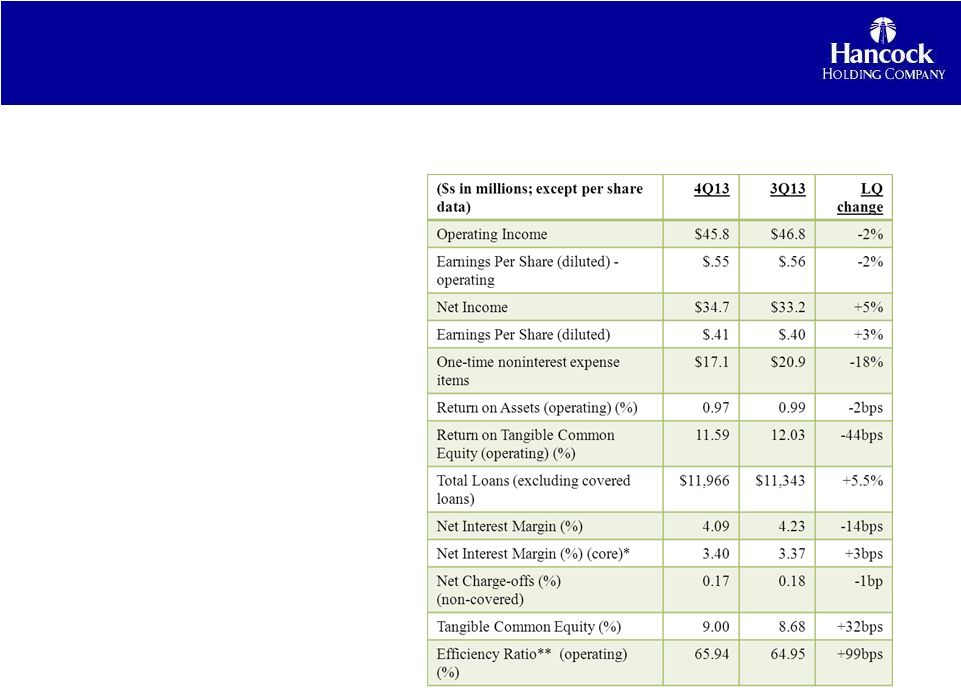

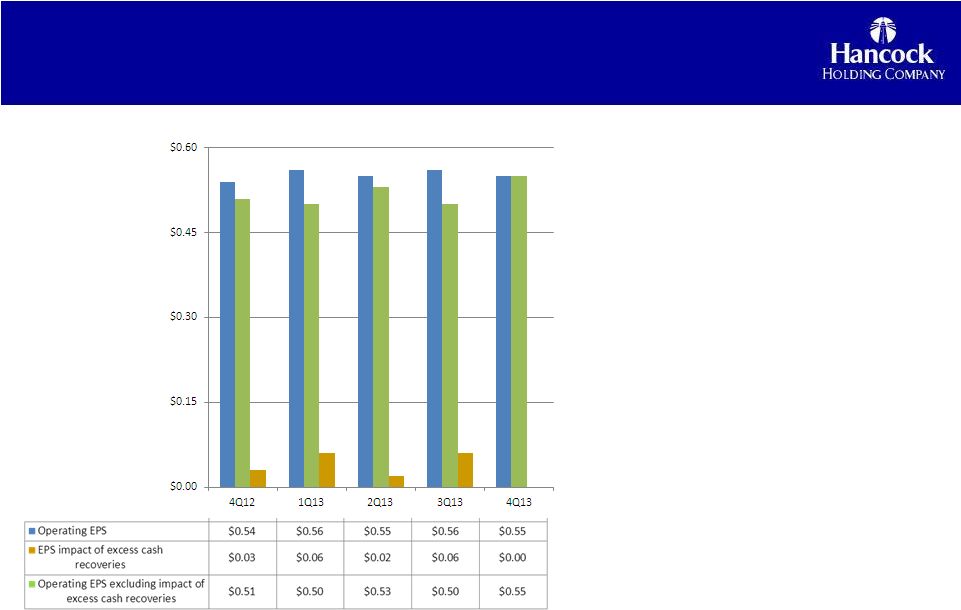

GULFPORT, Miss. (January 23, 2014) — Hancock Holding Company (Nasdaq: HBHC) today announced its financial results for the fourth quarter of 2013. Operating income for the fourth quarter of 2013 was $45.8 million or $.55 per diluted common share, compared to $46.8 million, or $.56 in the third quarter of 2013. Operating income was $46.6 million, or $.54, in the fourth quarter of 2012. We define our operating income as net income excluding tax-effected securities transactions gains or losses and one-time noninterest expense items. Management believes that operating income provides a useful measure of financial performance that helps investors compare the Company’s fundamental operations over time. The financial tables include a reconciliation of net income to operating income.

Highlights of the Company’s fourth quarter of 2013 results:

| • | Core net interest income (TE) increased approximately $1.5 million and core net interest margin (NIM) improved 3 basis points (bps) linked-quarter (we define our core results as reported results less the impact of net purchase accounting adjustments) |

| • | Operating expenses declined $4.2 million linked-quarter as the Company remains on track to meet its first quarter of 2014 expense target |

| • | Approximately $625 million linked-quarter net loan growth, or 22% annualized, and over $900 million, or 8%, year-over-year loan growth (each excluding the FDIC-covered portfolio) |

| • | Purchase accounting loan accretion declined approximately $8 million, or $.06 per diluted common share after tax |

| • | Continued improvement in overall asset quality metrics |

| • | Tax rate declined to 20%, mainly related to benefits from additional investments in New Market Tax Credit projects in the fourth quarter |

| • | Net income included one-time noninterest expense items of $17.1 million, or $11.1 million after tax ($.14 per diluted common share) |

Hancock’s return on average assets (ROA) (operating) was 0.97% for the fourth quarter of 2013, down slightly from 0.99% in the third quarter of 2013 and 0.98% in the fourth quarter a year ago.

- 1 -

Hancock reports fourth quarter 2013 financial results

January 23, 2014

“I have noted in previous quarters that our performance reflected an improvement in our core results, a trend we expected to build upon in the future,” said Hancock’s President and Chief Executive Officer Carl J. Chaney. “In the fourth quarter that trend accelerated and has now become more evident in our results. The results reflect the significant progress we are making in replacing the runoff in purchase accounting loan accretion with core operating income. Improvements were noted in many areas such as loan growth and mix, core net interest income and core net interest margin, and a reduction in operating expenses.”

Net income in the fourth quarter of 2013 was $34.7 million, or $.41 per diluted common share, compared to $33.2 million, or $.40, in the third quarter of 2013. Net income was $47.0 million, or $.54 per diluted common share, in the fourth quarter of 2012. Return on average assets (ROA) was 0.74% for the fourth quarter of 2013, compared to 0.70% in the third quarter of 2013 and 0.99% in the fourth quarter a year ago. Net income reflected the impact of certain one-time noninterest expenses of $17.1 million in the fourth quarter of 2013 and $20.9 million in the third quarter of 2013.

Loans

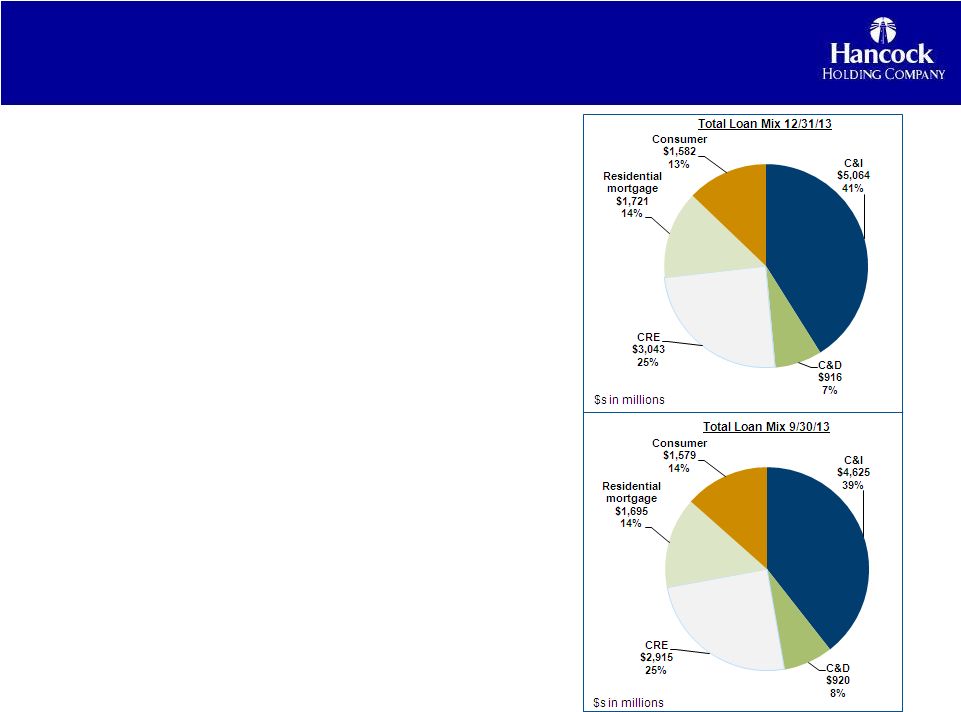

Total loans at December 31, 2013 were $12.3 billion, up $590 million from September 30, 2013. Excluding the FDIC-covered portfolio, which declined $33 million during the fourth quarter of 2013, total loans increased approximately $625 million, or 5.5% linked-quarter.

The largest component of linked-quarter net growth (excluding the FDIC-covered portfolio) was in the commercial and industrial (C&I) portfolio (+10%), followed by increases in the commercial real estate (CRE) (+5%) and residential mortgage (+3%) portfolios. Many of the markets across the Company’s footprint reported net loan growth during the quarter, with the majority of the growth in south Louisiana, Houston and Florida markets. The fourth quarter also included some net growth from seasonal borrowers, and loan paydowns and payoffs returned to a more normal level compared to the third quarter of 2013. For the full year of 2014 management expects period-end loan growth in the mid-single digit range.

A substantial portion of the fourth quarter’s net loan growth came toward the latter part of the period, and average loans were up $101 million, or 1%, from the third quarter of 2013.

Deposits

Total deposits at December 31, 2013 were $15.4 billion, up $306 million, or 2%, from September 30, 2013. Average deposits for the fourth quarter of 2013 were $14.9 billion, down $106 million, or 1%, from the third quarter of 2013.

Noninterest-bearing demand deposits (DDAs) totaled $5.5 billion at December 31, 2013, up $51 million, or 1%, compared to September 30, 2013. DDAs comprised 36% of total period-end deposits at December 31, 2013.

Interest bearing transaction and savings deposits totaled $6.2 billion at year-end 2013, up $155 million, or 3%, from September 30, 2013.

- 2 -

Hancock reports fourth quarter 2013 financial results

January 23, 2014

Time deposits (CDs) and interest-bearing public fund deposits totaled $3.7 billion at December 31, 2013, up $100 million, or 3%, from September 30, 2013. Public fund deposits typically reflect higher balances toward year-end with subsequent reductions beginning in the first quarter.

Asset Quality

Non-performing assets (NPAs) totaled $186 million at December 31, 2013, down $30 million from September 30, 2013. During the fourth quarter, total non-performing loans declined $21 million, and foreclosed and surplus real estate (ORE) and other foreclosed assets decreased $9 million. Non-performing assets as a percent of total loans, ORE and other foreclosed assets was 1.50% at December 31, 2013, down from 1.83% at September 30, 2013.

The Company’s total allowance for loan losses was $133.6 million at December 31, 2013, down from $138.2 million at September 30, 2013. The ratio of the allowance to period-end loans was 1.08%, compared to 1.18% at September 30, 2013. The decline in the allowance during the fourth quarter was primarily related to a $7.2 million reversal of a previous impairment on FDIC covered loans. The allowance maintained on the non-covered portion of the loan portfolio increased $2.6 million linked-quarter, totaling $80.5 million at December 31, 2013.

Net charge-offs from the non-covered loan portfolio were $5.2 million, or 0.17% of average total loans on an annualized basis in the fourth quarter of 2013, virtually unchanged from $5.4 million, or 0.18% of average total loans in the third quarter of 2013.

During the fourth quarter of 2013, Hancock recorded a total provision for loan losses of $7.3 million, down slightly from $7.6 million in the third quarter of 2013. The provision for non-covered loans was $7.9 million in the fourth quarter of 2013, compared to $6.5 million in the third quarter of 2013. The net provision from the covered portfolio was a credit of $0.5 million for the fourth quarter of 2013 compared to a provision of $1.0 million in the third quarter of 2013. This decline was driven by the reversal of impairment noted above.

Net Interest Income

Net interest income (TE) for the fourth quarter of 2013 was $168.5 million, down $5.6 million from the third quarter of 2013. Average earning assets were $16.4 billion, virtually unchanged from the third quarter of 2013. The reported net interest margin (TE) was 4.09% for the fourth quarter of 2013, down 14 basis points (bps) from the third quarter of 2013.

The linked-quarter decrease in both net interest income and net interest margin was primarily related to a decline of approximately $8 million in total purchase accounting loan accretion. As discussed in previous quarters, loan accretion can be volatile due in part to excess cash recoveries on acquired-impaired loan pools. During the fourth quarter of 2013, there were no excess cash recoveries above expected amounts included in the purchase accounting income total. The slide presentation referenced below includes detailed information on expected loan accretion and excess cash recoveries.

- 3 -

Hancock reports fourth quarter 2013 financial results

January 23, 2014

The core margin (reported net interest income (TE) excluding total net purchase accounting adjustments, annualized, as a percent of average earning assets) expanded 3 bps to 3.40% during the fourth quarter of 2013. A slight decline in the core loan yield (-3 bps) was offset by an improved earning asset mix, higher yields on investment securities (+19 bps) and a slight decline in the cost of funds (-1 bp).

Noninterest Income

Noninterest income totaled $59.0 million for the fourth quarter of 2013, down $4.1 million from the third quarter of 2013.

Service charges on deposits totaled $19.6 million for the fourth quarter of 2013, down $0.9 million, or 4%, from the third quarter of 2013. Bankcard and ATM fees totaled $11.3 million, down approximately $1.0 million, or 8%, from the third quarter of 2013.

Trust, investment and annuity, and insurance fees totaled $18.1 million, down $0.2 million, or 1%, from the third quarter of 2013. During the fourth quarter, an increase of $0.7 million, or 8%, in trust fees was offset by declines in investment and annuity, and insurance fees.

Fees from secondary mortgage operations totaled $1.6 million for the fourth quarter of 2013, down $0.9 million, or 37%, linked-quarter. The decline mainly reflects a continued slowdown in mortgage loan activity, reflecting mainly the impact of increased longer-term interest rates on originations. The fourth quarter’s activity also reflects a continued higher level of portfolio loan production compared to secondary market loan production.

Other noninterest income totaled $8.3 million for the fourth quarter of 2013, down $1.2 million, or 12%, linked-quarter. The decline mainly reflects a lower level of expected future losses on covered loans, which resulted in an increase of $1.1 million in the amortization of the indemnification asset.

Noninterest Expense & Taxes

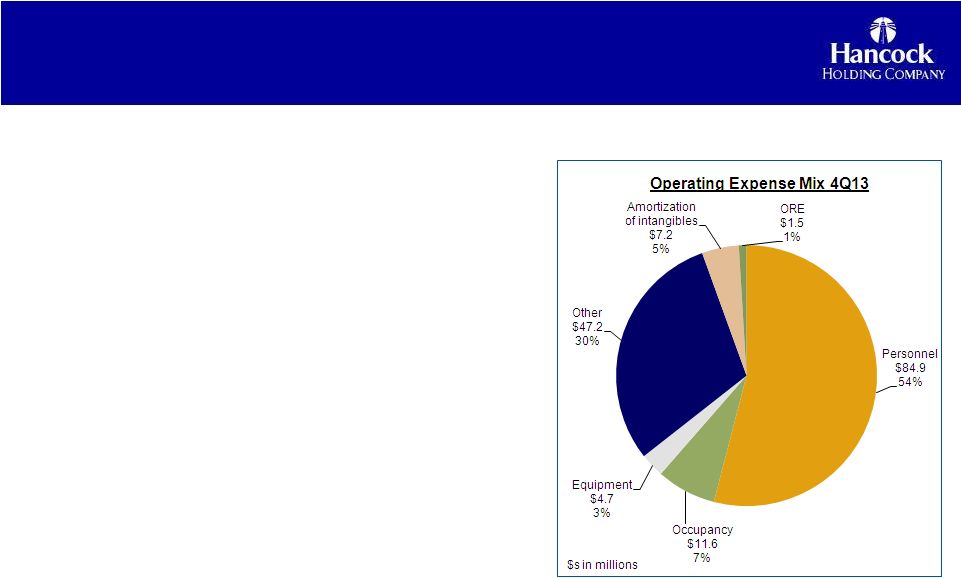

Noninterest expense for the fourth quarter of 2013 totaled $174.2 million, including $17.1 million of one-time costs related to the expense and efficiency initiative. Excluding these costs, noninterest expense (or operating expense) totaled $157.1 million, down $4.2 million, or 3%, from the comparable operating expense total for the third quarter of 2013.

Excluding one-time costs, total personnel expense, the largest component of the Company’s expense base, was $84.9 million in the fourth quarter of 2013, down $1.9 million, or 2%, from the third quarter of 2013. Occupancy and equipment expense totaled $16.3 million in the fourth quarter of 2013, down $1.2 million, or 7%, from the third quarter of 2013. The reduction in the personnel, occupancy and equipment expense categories reflect in part a full quarter’s impact from the closing of 26 branch locations across the Company’s five-state footprint in August 2013.

The sale of 7 Houston area branches was completed on November 8, 2013, and the sale of 3 Alexandria, Louisiana area branches was completed on January 10, 2014. Additionally, at year-end, the Company closed the remaining two branches that were part of the previously announced ongoing branch rationalization process.

- 4 -

Hancock reports fourth quarter 2013 financial results

January 23, 2014

ORE expense totaled $1.5 million in the fourth quarter of 2013, down $0.9 million from the third quarter, while other operating expense was essentially unchanged at $47.2 million.

The effective income tax rate for the fourth quarter of 2013 was 20%, down from 26% in the third quarter of 2013. The decline in the tax rate is primarily related to several additional New Market Tax Credit investments that were closed during the fourth quarter of 2013. Management expects the effective tax rate to approximate 25-27% in 2014. The effective income tax rate continues to be less than the statutory rate of 35% due primarily to tax-exempt income and tax credits.

Capital

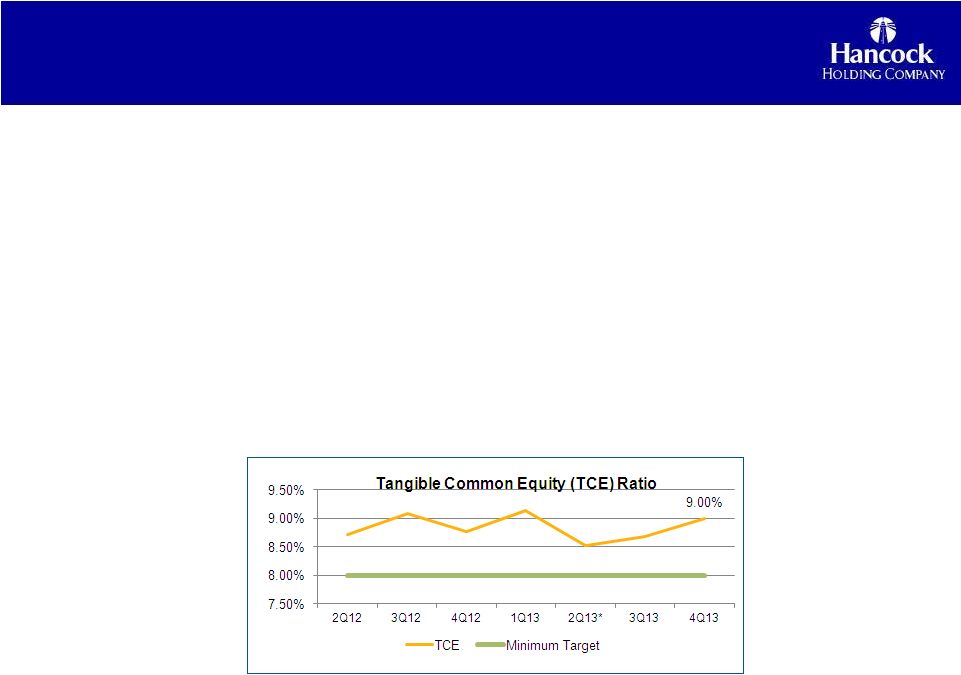

Common shareholders’ equity at year-end 2013 totaled $2.4 billion. The tangible common equity (TCE) ratio was 9.00% at December 31, 2013, up 32 bps from September 30, 2013. Management continues to review a full range of the strategic options presented by Hancock’s strong capital position, including additional stock buybacks, organic growth, acquisitions or increased dividends. Additional capital ratios are included in the financial tables.

Conference Call and Slide Presentation

Management will host a conference call for analysts and investors at 8:00 a.m. Central Time on Friday, January 24, 2014 to review the results. A live listen-only webcast of the call will be available under the Investor Relations section of Hancock’s website at www.hancockbank.com. A slide presentation related to fourth quarter results is also posted as part of the webcast link. To participate in the Q&A portion of the call, dial (877) 564-1219 or (973) 638-3429. An audio archive of the conference call will be available under the Investor Relations section of our website. A replay of the call will also be available through January 30, 2014 by dialing (855) 859-2056 or (404) 537-3406, passcode 30587330.

About Hancock Holding Company

Hancock Holding Company is the parent company of Hancock Bank and Whitney Bank. The Company operates as Hancock Bank in south Mississippi, southern and central Alabama, and the northern, central, and panhandle regions of Florida; and as Whitney Bank in south Louisiana and Houston, Texas. The Hancock Holding Company family of financial services companies also includes Hancock Investment Services, Inc.; Hancock Insurance Agency and Whitney Insurance Agency, Inc.; corporate trust offices in Gulfport and Jackson, Mississippi, New Orleans and Baton Rouge, Louisiana, and Orlando, Florida; and Harrison Finance Company. Additional information is available at www.hancockbank.com and www.whitneybank.com.

Forward-Looking Statements

This news release contains “forward-looking statements” within the meaning of section 27A of the Securities Act of 1933, as amended, and section 21E of the Securities Exchange Act of 1934, as amended, and we intend such forward-looking statements to be covered by the safe harbor provisions therein and are including this statement for purposes of invoking these safe-harbor provisions. Forward-looking statements provide projections of results of operations or of financial condition or state other forward-looking information, such as expectations about future conditions and descriptions of plans and strategies for the future.

- 5 -

Hancock reports fourth quarter 2013 financial results

January 23, 2014

Forward-looking statements that we may make include, but may not be limited to, comments with respect to future levels of economic activity in our markets, loan growth, deposit trends, credit quality trends, future sales of nonperforming assets, net interest margin trends, future expense levels and the ability to achieve reductions in non-interest expense or other cost savings, projected tax rates, future profitability, improvements in expense to revenue (efficiency) ratio, purchase accounting impacts such as accretion levels, the impact of the branch rationalization process, and the financial impact of regulatory requirements.

Hancock’s ability to accurately project results or predict the effects of future plans or strategies is inherently limited. Although Hancock believes that the expectations reflected in its forward-looking statements are based on reasonable assumptions, actual results and performance could differ materially from those set forth in the forward-looking statements. Factors that could cause actual results to differ from those expressed in Hancock’s forward-looking statements include, but are not limited to, those risk factors outlined in Hancock’s public filings with the Securities and Exchange Commission, which are available at the SEC’s internet site (http://www.sec.gov).

You are cautioned not to place undue reliance on these forward-looking statements. Hancock does not intend, and undertakes no obligation, to update or revise any forward-looking statements, whether as a result of differences in actual results, changes in assumptions or changes in other factors affecting such statements, except as required by law.

- 6 -

Hancock Holding Company

Financial Highlights

(amounts in thousands, except per share data and FTE headcount)

(unaudited)

| Three Months Ended | Twelve Months Ended | |||||||||||||||||||

| 12/31/2013 | 9/30/2013 | 12/31/2012 | 12/31/2013 | 12/31/2012 | ||||||||||||||||

| Common Share Data |

||||||||||||||||||||

| Earnings per share: |

||||||||||||||||||||

| Basic |

$ | 0.41 | $ | 0.40 | $ | 0.55 | $ | 1.93 | $ | 1.77 | ||||||||||

| Diluted |

$ | 0.41 | $ | 0.40 | $ | 0.54 | $ | 1.93 | $ | 1.75 | ||||||||||

| Operating earnings per share: (a) |

||||||||||||||||||||

| Basic |

$ | 0.55 | $ | 0.56 | $ | 0.54 | $ | 2.22 | $ | 2.15 | ||||||||||

| Diluted |

$ | 0.55 | $ | 0.56 | $ | 0.54 | $ | 2.22 | $ | 2.13 | ||||||||||

| Cash dividends per share |

$ | 0.24 | $ | 0.24 | $ | 0.24 | $ | 0.96 | $ | 0.96 | ||||||||||

| Book value per share (period-end) |

$ | 29.49 | $ | 28.70 | $ | 28.91 | $ | 29.49 | $ | 28.91 | ||||||||||

| Tangible book value per share (period-end) |

$ | 19.94 | $ | 19.04 | $ | 19.27 | $ | 19.94 | $ | 19.27 | ||||||||||

| Weighted average number of shares: |

||||||||||||||||||||

| Basic |

82,085 | 82,091 | 84,798 | 83,066 | 84,767 | |||||||||||||||

| Diluted |

82,220 | 82,205 | 85,777 | 83,167 | 85,588 | |||||||||||||||

| Period-end number of shares |

82,237 | 82,107 | 84,848 | 82,237 | 84,848 | |||||||||||||||

| Market data: |

||||||||||||||||||||

| High sales price |

$ | 37.12 | $ | 33.85 | $ | 32.50 | $ | 37.12 | $ | 36.73 | ||||||||||

| Low sales price |

$ | 30.09 | $ | 29.00 | $ | 29.47 | $ | 25.00 | $ | 27.96 | ||||||||||

| Period end closing price |

$ | 36.68 | $ | 31.38 | $ | 31.73 | $ | 36.68 | $ | 31.73 | ||||||||||

| Trading volume |

27,816 | 29,711 | 20,910 | 122,496 | 119,519 | |||||||||||||||

| Other Period-end Data |

||||||||||||||||||||

| FTE headcount |

3,978 | 4,068 | 4,235 | 3,978 | 4,235 | |||||||||||||||

| Tangible common equity |

$ | 1,639,524 | $ | 1,563,542 | $ | 1,634,833 | $ | 1,639,524 | $ | 1,634,833 | ||||||||||

| Tier I capital |

$ | 1,682,782 | $ | 1,656,497 | $ | 1,668,809 | $ | 1,682,782 | $ | 1,668,809 | ||||||||||

| Goodwill |

$ | 625,675 | $ | 625,675 | $ | 628,877 | $ | 625,675 | $ | 628,877 | ||||||||||

| Amortizing intangibles |

$ | 159,773 | $ | 167,116 | $ | 189,409 | $ | 159,773 | $ | 189,409 | ||||||||||

| Performance Ratios |

||||||||||||||||||||

| Return on average assets |

0.74 | % | 0.70 | % | 0.99 | % | 0.86 | % | 0.80 | % | ||||||||||

| Return on average assets (operating) (a) |

0.97 | % | 0.99 | % | 0.98 | % | 0.99 | % | 0.97 | % | ||||||||||

| Return on average common equity |

5.85 | % | 5.63 | % | 7.67 | % | 6.84 | % | 6.32 | % | ||||||||||

| Return on average common equity (operating) (a) |

7.71 | % | 7.93 | % | 7.60 | % | 7.88 | % | 7.66 | % | ||||||||||

| Return on average tangible common equity |

8.79 | % | 8.54 | % | 11.58 | % | 10.30 | % | 9.72 | % | ||||||||||

| Return on average tangible common equity (operating) (a) |

11.59 | % | 12.03 | % | 11.48 | % | 11.85 | % | 11.78 | % | ||||||||||

| Tangible common equity ratio |

9.00 | % | 8.68 | % | 8.77 | % | 9.00 | % | 8.77 | % | ||||||||||

| Earning asset yield (TE) |

4.32 | % | 4.47 | % | 4.76 | % | 4.45 | % | 4.80 | % | ||||||||||

| Total cost of funds |

0.23 | % | 0.24 | % | 0.28 | % | 0.25 | % | 0.32 | % | ||||||||||

| Net interest margin (TE) |

4.09 | % | 4.23 | % | 4.48 | % | 4.20 | % | 4.48 | % | ||||||||||

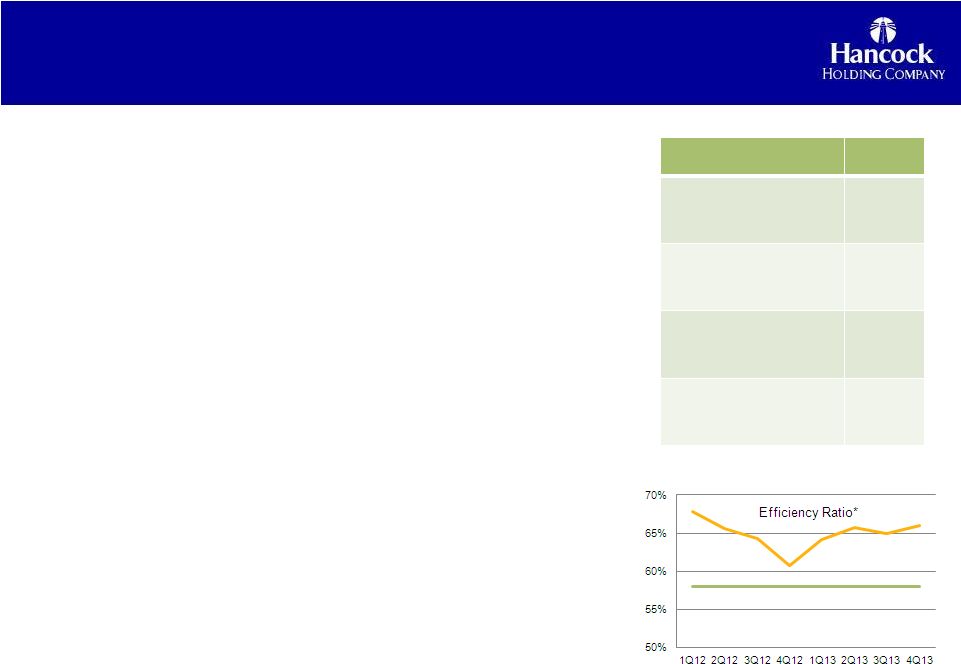

| Efficiency ratio (b) |

65.94 | % | 64.95 | % | 60.78 | % | 65.17 | % | 64.63 | % | ||||||||||

| Allowance for loan losses as a percent of period-end loans |

1.08 | % | 1.18 | % | 1.18 | % | 1.08 | % | 1.18 | % | ||||||||||

| Allowance for loan losses to non-performing loans + accruing loans 90 days past due |

111.97 | % | 94.69 | % | 81.40 | % | 111.97 | % | 81.40 | % | ||||||||||

| Average loan/deposit ratio |

79.93 | % | 78.70 | % | 76.29 | % | 77.56 | % | 74.68 | % | ||||||||||

| Noninterest income excluding securities transactions as a percent of total revenue (TE) |

25.90 | % | 26.59 | % | 26.02 | % | 26.25 | % | 25.88 | % | ||||||||||

| (a) | Excludes tax-effected securities transactions and one-time noninterest expense items. Management believes that operating income provides a useful measure of financial performance that helps investors compare the Company’s fundamental operations over time. |

| (b) | Efficiency ratio is defined as noninterest expense as a percent of total revenue (TE) before amortization of purchased intangibles, one-time noninterest expense items, and securities transactions. |

- 7 -

Hancock Holding Company

Financial Highlights

(amounts in thousands)

(unaudited)

| Three Months Ended | Twelve Months Ended | |||||||||||||||||||

| 12/31/2013 | 9/30/2013 | 12/31/2012 | 12/31/2013 | 12/31/2012 | ||||||||||||||||

| Income Statement |

||||||||||||||||||||

| Interest income |

$ | 175,650 | $ | 181,639 | $ | 191,140 | $ | 722,210 | $ | 762,549 | ||||||||||

| Interest income (TE) |

178,109 | 184,221 | 194,075 | 732,620 | 774,134 | |||||||||||||||

| Interest expense |

9,643 | 10,109 | 11,275 | 41,479 | 51,682 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net interest income (TE) |

168,466 | 174,112 | 182,800 | 691,141 | 722,452 | |||||||||||||||

| Provision for loan losses |

7,331 | 7,569 | 28,051 | 32,734 | 54,192 | |||||||||||||||

| Noninterest income excluding securities transactions |

58,894 | 63,057 | 64,308 | 246,038 | 252,195 | |||||||||||||||

| Securities transactions gains |

105 | — | 623 | 105 | 1,552 | |||||||||||||||

| Noninterest expense |

174,213 | 182,205 | 157,920 | 678,274 | 713,067 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income before income taxes |

43,462 | 44,813 | 58,825 | 215,866 | 197,355 | |||||||||||||||

| Income tax expense |

8,746 | 11,611 | 11,866 | 52,510 | 45,613 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income |

$ | 34,716 | $ | 33,202 | $ | 46,959 | $ | 163,356 | $ | 151,742 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Adjustments from net to operating income |

||||||||||||||||||||

| Securities transactions gains |

105 | — | 623 | 105 | 1,552 | |||||||||||||||

| One-time noninterest expense items |

||||||||||||||||||||

| Merger-related expenses |

— | — | — | — | 45,789 | |||||||||||||||

| Sub-debt early redemption costs |

— | — | — | — | 5,336 | |||||||||||||||

| Expense & efficiency initiative and other items |

17,116 | 20,887 | — | 38,003 | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total one-time noninterest expense items |

17,116 | 20,887 | — | 38,003 | 51,125 | |||||||||||||||

| Taxes on adjustments at 35% |

5,954 | 7,310 | (218 | ) | 13,264 | 17,350 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total adjustments (net of taxes) |

11,057 | 13,577 | (405 | ) | 24,634 | 32,223 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Operating income (c) |

$ | 45,773 | $ | 46,779 | $ | 46,554 | $ | 187,990 | $ | 183,965 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Noninterest Income and Noninterest Expense |

||||||||||||||||||||

| Service charges on deposit accounts |

$ | 19,605 | $ | 20,519 | $ | 20,232 | $ | 79,000 | $ | 78,246 | ||||||||||

| Trust fees |

10,214 | 9,477 | 8,273 | 38,186 | 32,736 | |||||||||||||||

| Bank card and ATM fees |

11,261 | 12,221 | 11,526 | 45,939 | 49,112 | |||||||||||||||

| Investment & annuity fees |

4,619 | 5,186 | 4,743 | 19,574 | 18,033 | |||||||||||||||

| Secondary mortgage market operations |

1,554 | 2,467 | 5,160 | 12,543 | 16,488 | |||||||||||||||

| Insurance fees |

3,304 | 3,661 | 3,588 | 15,804 | 15,692 | |||||||||||||||

| Other income |

8,337 | 9,526 | 10,786 | 34,992 | 41,888 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Noninterest income excluding securities transactions |

58,894 | 63,057 | 64,308 | 246,038 | 252,195 | |||||||||||||||

| Securities transactions gains |

105 | — | 623 | 105 | 1,552 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total noninterest income including securities transactions |

$ | 58,999 | $ | 63,057 | $ | 64,931 | $ | 246,143 | $ | 253,747 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Personnel expense |

$ | 84,912 | $ | 86,850 | $ | 87,358 | $ | 347,266 | $ | 356,734 | ||||||||||

| Occupancy expense (net) |

11,613 | 12,369 | 12,683 | 48,713 | 53,856 | |||||||||||||||

| Equipment expense |

4,679 | 5,120 | 5,051 | 20,019 | 21,862 | |||||||||||||||

| Other real estate owned expense (net) |

1,535 | 2,439 | 2,236 | 8,036 | 12,250 | |||||||||||||||

| Other operating expense |

47,180 | 47,234 | 42,862 | 186,767 | 185,173 | |||||||||||||||

| Amortization of intangibles |

7,178 | 7,306 | 7,730 | 29,470 | 32,067 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total operating expense |

157,097 | 161,318 | 157,920 | 640,271 | 661,942 | |||||||||||||||

| One-time noninterest expense items |

17,116 | 20,887 | — | 38,003 | 51,125 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total noninterest expense |

$ | 174,213 | $ | 182,205 | $ | 157,920 | $ | 678,274 | $ | 713,067 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Common Share Data |

||||||||||||||||||||

| Earnings per share: |

||||||||||||||||||||

| Basic |

$ | 0.41 | $ | 0.40 | $ | 0.55 | $ | 1.93 | $ | 1.77 | ||||||||||

| Diluted |

$ | 0.41 | $ | 0.40 | $ | 0.54 | $ | 1.93 | $ | 1.75 | ||||||||||

| Operating earnings per share: |

||||||||||||||||||||

| Basic |

$ | 0.55 | $ | 0.56 | $ | 0.54 | $ | 2.22 | $ | 2.15 | ||||||||||

| Diluted |

$ | 0.55 | $ | 0.56 | $ | 0.54 | $ | 2.22 | $ | 2.13 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Cash dividends per share |

$ | 0.24 | $ | 0.24 | $ | 0.24 | $ | 0.96 | $ | 0.96 | ||||||||||

| Book value per share (period-end) |

$ | 29.49 | $ | 28.70 | $ | 28.91 | $ | 29.49 | $ | 28.91 | ||||||||||

| Tangible book value per share (period-end) |

$ | 19.94 | $ | 19.04 | $ | 19.27 | $ | 19.94 | $ | 19.27 | ||||||||||

| Weighted average number of shares: |

||||||||||||||||||||

| Basic |

82,085 | 82,091 | 84,798 | 83,066 | 84,767 | |||||||||||||||

| Diluted |

82,220 | 82,205 | 85,777 | 83,167 | 85,588 | |||||||||||||||

| Period-end number of shares |

82,237 | 82,107 | 84,848 | 82,237 | 84,848 | |||||||||||||||

| Market data: |

||||||||||||||||||||

| High sales price |

$ | 37.12 | $ | 33.85 | $ | 32.50 | $ | 37.12 | $ | 36.73 | ||||||||||

| Low sales price |

$ | 30.09 | $ | 29.00 | $ | 29.47 | $ | 25.00 | $ | 27.96 | ||||||||||

| Period end closing price |

$ | 36.68 | $ | 31.38 | $ | 31.73 | $ | 36.68 | $ | 31.73 | ||||||||||

| Trading volume |

27,816 | 29,711 | 20,910 | 122,496 | 119,519 | |||||||||||||||

| (c) | Net income less tax-effected securities gains and one-time noninterest expense items. Management believes that operating income provides a useful measure of financial performance that helps investors compare the Company’s fundamental operations over time. |

- 8 -

Hancock Holding Company

Financial Highlights

(amounts in thousands)

(unaudited)

| Three Months Ended | ||||||||||||||||||||

| 12/31/2013 | 9/30/2013 | 6/30/2013 | 3/31/2013 | 12/31/2012 | ||||||||||||||||

| Period-end Balance Sheet |

||||||||||||||||||||

| Commercial non-real estate loans |

$ | 5,064,224 | $ | 4,625,315 | $ | 4,653,342 | $ | 4,425,286 | $ | 4,433,288 | ||||||||||

| Construction and land development loans |

915,541 | 920,408 | 966,499 | 992,820 | 989,306 | |||||||||||||||

| Commercial real estate loans |

3,042,841 | 2,914,969 | 2,872,254 | 2,873,403 | 2,923,094 | |||||||||||||||

| Residential mortgage loans |

1,720,614 | 1,695,197 | 1,616,093 | 1,587,519 | 1,577,944 | |||||||||||||||

| Consumer loans |

1,581,597 | 1,578,583 | 1,573,309 | 1,603,734 | 1,654,170 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total loans |

12,324,817 | 11,734,472 | 11,681,497 | 11,482,762 | 11,577,802 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Loans held for sale |

24,515 | 18,444 | 20,233 | 34,813 | 50,605 | |||||||||||||||

| Securities |

4,033,124 | 4,124,202 | 4,303,918 | 4,662,279 | 3,716,460 | |||||||||||||||

| Short-term investments |

268,839 | 462,313 | 442,917 | 475,677 | 1,500,188 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Earning assets |

16,651,295 | 16,339,431 | 16,448,565 | 16,655,531 | 16,845,055 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Allowance for loan losses |

(133,626 | ) | (138,223 | ) | (137,969 | ) | (137,777 | ) | (136,171 | ) | ||||||||||

| Other assets |

2,491,582 | 2,600,638 | 2,623,705 | 2,546,369 | 2,755,601 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total assets |

$ | 19,009,251 | $ | 18,801,846 | $ | 18,934,301 | $ | 19,064,123 | $ | 19,464,485 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Noninterest bearing deposits |

$ | 5,530,253 | $ | 5,479,696 | $ | 5,340,177 | $ | 5,418,463 | $ | 5,624,127 | ||||||||||

| Interest bearing transaction and savings deposits |

6,162,959 | 6,008,042 | 5,965,372 | 6,017,735 | 6,038,003 | |||||||||||||||

| Interest bearing public fund deposits |

1,571,532 | 1,240,336 | 1,410,866 | 1,528,790 | 1,580,260 | |||||||||||||||

| Time deposits |

2,095,772 | 2,326,797 | 2,439,523 | 2,288,363 | 2,501,798 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total interest bearing deposits |

9,830,263 | 9,575,175 | 9,815,761 | 9,834,888 | 10,120,061 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total deposits |

15,360,516 | 15,054,871 | 15,155,938 | 15,253,351 | 15,744,188 | |||||||||||||||

| Short-term borrowings |

657,960 | 782,779 | 828,107 | 722,537 | 639,133 | |||||||||||||||

| Long-term debt |

385,826 | 376,664 | 385,122 | 393,920 | 396,589 | |||||||||||||||

| Other liabilities |

179,880 | 231,090 | 219,794 | 217,215 | 231,297 | |||||||||||||||

| Common shareholders’ equity |

2,425,069 | 2,356,442 | 2,345,340 | 2,477,100 | 2,453,278 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total liabilities & shareholders’ equity |

$ | 19,009,251 | $ | 18,801,846 | $ | 18,934,301 | $ | 19,064,123 | $ | 19,464,485 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Capital Ratios |

||||||||||||||||||||

| Common shareholders’ equity |

$ | 2,425,069 | $ | 2,356,442 | $ | 2,345,340 | $ | 2,477,100 | $ | 2,453,278 | ||||||||||

| Tier 1 capital (d) |

1,682,782 | 1,656,497 | 1,632,874 | 1,700,115 | 1,668,809 | |||||||||||||||

| Tangible common equity ratio |

9.00 | % | 8.68 | % | 8.52 | % | 9.14 | % | 8.77 | % | ||||||||||

| Common equity (period-end) as a percent of total assets (period-end) |

12.76 | % | 12.53 | % | 12.39 | % | 12.99 | % | 12.60 | % | ||||||||||

| Leverage (Tier 1) ratio (d) |

9.36 | % | 9.10 | % | 8.96 | % | 9.28 | % | 9.11 | % | ||||||||||

| Tier 1 risk-based capital ratio (d) |

11.87 | % | 12.07 | % | 12.00 | % | 12.78 | % | 12.64 | % | ||||||||||

| Total risk-based capital ratio (d) |

13.23 | % | 13.52 | % | 13.45 | % | 14.41 | % | 14.28 | % | ||||||||||

| (d) | Estimated for most recent period-end. |

- 9 -

Hancock Holding Company

Financial Highlights

(amounts in thousands)

(unaudited)

| Three Months Ended | Twelve Months Ended | |||||||||||||||||||

| 12/31/2013 | 9/30/2013 | 12/31/2012 | 12/31/2013 | 12/31/2012 | ||||||||||||||||

| Average Balance Sheet |

||||||||||||||||||||

| Commercial non-real estate loans |

$ | 4,786,680 | $ | 4,720,608 | $ | 4,316,455 | $ | 4,615,973 | $ | 4,007,506 | ||||||||||

| Construction and land development loans |

931,214 | 970,411 | 1,035,401 | 965,237 | 1,157,064 | |||||||||||||||

| Commercial real estate loans |

2,915,323 | 2,891,830 | 2,910,880 | 2,899,317 | 2,897,317 | |||||||||||||||

| Residential mortgage loans |

1,715,716 | 1,668,201 | 1,613,919 | 1,659,324 | 1,571,465 | |||||||||||||||

| Consumer loans |

1,573,446 | 1,570,345 | 1,667,134 | 1,585,353 | 1,651,387 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total loans (e) |

11,922,379 | 11,821,395 | 11,543,789 | 11,725,204 | 11,284,739 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Securities (f) |

4,070,657 | 4,135,348 | 3,732,815 | 4,140,051 | 4,063,817 | |||||||||||||||

| Short-term investments |

383,551 | 427,892 | 969,037 | 578,613 | 771,523 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Earning assets |

16,376,587 | 16,384,635 | 16,245,641 | 16,443,868 | 16,120,079 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Allowance for loan losses |

(138,708 | ) | (137,936 | ) | (136,254 | ) | (137,897 | ) | (136,257 | ) | ||||||||||

| Other assets |

2,501,212 | 2,549,328 | 2,855,565 | 2,623,047 | 2,951,547 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total assets |

$ | 18,739,091 | $ | 18,796,027 | $ | 18,964,952 | $ | 18,929,018 | $ | 18,935,369 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Noninterest bearing deposits |

$ | 5,483,918 | $ | 5,415,303 | $ | 5,420,081 | $ | 5,393,955 | $ | 5,251,391 | ||||||||||

| Interest bearing transaction and savings deposits |

5,981,110 | 5,919,709 | 5,930,964 | 5,962,114 | 5,827,370 | |||||||||||||||

| Interest bearing public fund deposits |

1,253,199 | 1,302,425 | 1,332,163 | 1,410,679 | 1,451,459 | |||||||||||||||

| Time deposits |

2,197,450 | 2,384,248 | 2,448,694 | 2,350,488 | 2,579,963 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total interest bearing deposits |

9,431,759 | 9,606,382 | 9,711,821 | 9,723,281 | 9,858,792 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total deposits |

14,915,677 | 15,021,685 | 15,131,902 | 15,117,236 | 15,110,183 | |||||||||||||||

| Short-term borrowings |

848,934 | 820,500 | 847,058 | 806,082 | 843,798 | |||||||||||||||

| Long-term debt |

381,561 | 385,203 | 321,713 | 389,153 | 338,875 | |||||||||||||||

| Other liabilities |

237,151 | 229,694 | 229,100 | 229,983 | 241,710 | |||||||||||||||

| Common shareholders’ equity |

2,355,768 | 2,338,945 | 2,435,179 | 2,386,564 | 2,400,803 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total liabilities & shareholders’ equity |

$ | 18,739,091 | $ | 18,796,027 | $ | 18,964,952 | $ | 18,929,018 | $ | 18,935,369 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (e) | Includes loans held for sale. |

| (f) | Average securities does not include unrealized holding gains/losses on available for sale securities. |

- 10 -

Hancock Holding Company

Average Balance and Net Interest Margin Summary

(amounts in thousands)

(unaudited)

| Three Months Ended | ||||||||||||||||||||||||||||||||||||

| 12/31/2013 | 9/30/2013 | 12/31/2012 | ||||||||||||||||||||||||||||||||||

| Interest | Volume | Rate | Interest | Volume | Rate | Interest | Volume | Rate | ||||||||||||||||||||||||||||

| Average Earning Assets |

||||||||||||||||||||||||||||||||||||

| Commercial & real estate loans (TE) |

$ | 104,168 | $ | 8,633,217 | 4.79 | % | $ | 109,450 | $ | 8,582,849 | 5.06 | % | $ | 113,004 | $ | 8,262,736 | 5.44 | % | ||||||||||||||||||

| Residential mortgage loans |

23,612 | 1,715,716 | 5.50 | % | 24,968 | 1,668,201 | 5.99 | % | 27,998 | 1,613,919 | 6.94 | % | ||||||||||||||||||||||||

| Consumer loans |

24,382 | 1,573,446 | 6.15 | % | 25,740 | 1,570,345 | 6.51 | % | 28,593 | 1,667,134 | 6.82 | % | ||||||||||||||||||||||||

| Loan fees & late charges |

1,001 | — | 0.00 | % | 689 | — | 0.00 | % | 3,098 | — | 0.00 | % | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| Total loans (TE) |

153,163 | 11,922,379 | 5.10 | % | 160,847 | 11,821,395 | 5.41 | % | 172,693 | 11,543,789 | 5.95 | % | ||||||||||||||||||||||||

| US Treasury and government agency securities |

555 | 100,150 | 2.20 | % | 33 | 5,585 | 2.34 | % | 51 | 18,315 | 1.11 | % | ||||||||||||||||||||||||

| CMOs |

7,804 | 1,425,839 | 2.19 | % | 7,278 | 1,463,403 | 1.99 | % | 7,204 | 1,577,165 | 1.83 | % | ||||||||||||||||||||||||

| Mortgage backed securities |

13,866 | 2,299,544 | 2.41 | % | 13,042 | 2,410,763 | 2.16 | % | 10,475 | 1,891,704 | 2.22 | % | ||||||||||||||||||||||||

| Municipals (TE) |

2,443 | 235,778 | 4.14 | % | 2,715 | 247,140 | 4.39 | % | 2,942 | 238,733 | 4.93 | % | ||||||||||||||||||||||||

| Other securities |

58 | 9,346 | 2.49 | % | 53 | 8,457 | 2.51 | % | 94 | 6,898 | 5.43 | % | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| Total securities (TE) (g) |

24,726 | 4,070,657 | 2.43 | % | 23,121 | 4,135,348 | 2.24 | % | 20,766 | 3,732,815 | 2.21 | % | ||||||||||||||||||||||||

| Total short-term investments |

220 | 383,551 | 0.23 | % | 253 | 427,892 | 0.23 | % | 616 | 969,037 | 0.25 | % | ||||||||||||||||||||||||

| Average earning assets yield (TE) |

$ | 178,109 | $ | 16,376,587 | 4.32 | % | $ | 184,221 | $ | 16,384,635 | 4.47 | % | $ | 194,075 | $ | 16,245,641 | 4.76 | % | ||||||||||||||||||

| Interest-bearing Liabilities |

||||||||||||||||||||||||||||||||||||

| Interest-bearing transaction and savings deposits |

$ | 1,399 | $ | 5,981,110 | 0.09 | % | $ | 1,398 | $ | 5,919,709 | 0.09 | % | $ | 1,719 | $ | 5,930,964 | 0.12 | % | ||||||||||||||||||

| Time deposits |

3,328 | 2,197,450 | 0.60 | % | 3,687 | 2,384,248 | 0.61 | % | 4,507 | 2,448,694 | 0.73 | % | ||||||||||||||||||||||||

| Public funds |

663 | 1,253,199 | 0.21 | % | 766 | 1,302,425 | 0.23 | % | 861 | 1,332,163 | 0.26 | % | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| Total interest bearing deposits |

5,390 | 9,431,759 | 0.23 | % | 5,851 | 9,606,382 | 0.24 | % | 7,087 | 9,711,821 | 0.29 | % | ||||||||||||||||||||||||

| Short-term borrowings |

1,092 | 848,934 | 0.51 | % | 1,074 | 820,500 | 0.52 | % | 1,273 | 847,058 | 0.60 | % | ||||||||||||||||||||||||

| Long-term debt |

3,161 | 381,561 | 3.29 | % | 3,184 | 385,203 | 3.28 | % | 2,915 | 321,713 | 3.60 | % | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| Total borrowings |

4,253 | 1,230,495 | 1.37 | % | 4,258 | 1,205,703 | 1.40 | % | 4,188 | 1,168,771 | 1.43 | % | ||||||||||||||||||||||||

| Total interest bearing liabilities cost |

$ | 9,643 | $ | 10,662,254 | 0.36 | % | $ | 10,109 | $ | 10,812,085 | 0.37 | % | $ | 11,275 | $ | 10,880,592 | 0.41 | % | ||||||||||||||||||

| Net interest-free funding sources |

5,714,333 | 5,572,550 | 5,365,049 | |||||||||||||||||||||||||||||||||

| Total Cost of Funds |

$ | 9,643 | $ | 16,376,587 | 0.23 | % | $ | 10,109 | $ | 16,384,635 | 0.24 | % | $ | 11,275 | $ | 16,245,641 | 0.28 | % | ||||||||||||||||||

| Net Interest Spread (TE) |

$ | 168,466 | 3.96 | % | $ | 174,112 | 4.10 | % | $ | 182,800 | 4.35 | % | ||||||||||||||||||||||||

| Net Interest Margin (TE) |

$ | 168,466 | $ | 16,376,587 | 4.09 | % | $ | 174,112 | $ | 16,384,635 | 4.23 | % | $ | 182,800 | $ | 16,245,641 | 4.48 | % | ||||||||||||||||||

| (g) | Average securities does not include unrealized holding gains/losses on available for sale securities. |

- 11 -

Hancock Holding Company

Average Balance and Net Interest Margin Summary

(amounts in thousands)

(unaudited)

| Twelve Months Ended | ||||||||||||||||||||||||

| 12/31/2013 | 12/31/2012 | |||||||||||||||||||||||

| Interest | Volume | Rate | Interest | Volume | Rate | |||||||||||||||||||

| Average Earning Assets |

||||||||||||||||||||||||

| Commercial & real estate loans (TE) |

$ | 430,258 | $ | 8,480,527 | 5.07 | % | $ | 443,360 | $ | 8,061,887 | 5.50 | % | ||||||||||||

| Residential mortgage loans |

101,800 | 1,659,324 | 6.14 | % | 111,662 | 1,571,465 | 7.11 | % | ||||||||||||||||

| Consumer loans |

103,157 | 1,585,353 | 6.51 | % | 115,470 | 1,651,387 | 6.99 | % | ||||||||||||||||

| Loan fees & late charges |

3,494 | — | 0.00 | % | 6,335 | — | 0.00 | % | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total loans (TE) |

638,709 | 11,725,204 | 5.45 | % | 676,827 | 11,284,739 | 6.00 | % | ||||||||||||||||

| US Treasury and government agency securities |

606 | 28,063 | 2.16 | % | 2,104 | 99,136 | 2.12 | % | ||||||||||||||||

| CMOs |

29,627 | 1,502,867 | 1.97 | % | 29,790 | 1,545,531 | 1.93 | % | ||||||||||||||||

| Mortgage backed securities |

51,730 | 2,367,274 | 2.19 | % | 51,332 | 2,150,799 | 2.39 | % | ||||||||||||||||

| Municipals (TE) |

10,342 | 233,310 | 4.43 | % | 11,814 | 260,488 | 4.54 | % | ||||||||||||||||

| Other securities |

208 | 8,537 | 2.44 | % | 348 | 7,863 | 4.43 | % | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total securities (TE) (h) |

92,513 | 4,140,051 | 2.23 | % | 95,388 | 4,063,817 | 2.35 | % | ||||||||||||||||

| Total short-term investments |

1,398 | 578,613 | 0.24 | % | 1,919 | 771,523 | 0.25 | % | ||||||||||||||||

| Average earning assets yield (TE) |

$ | 732,620 | $ | 16,443,868 | 4.45 | % | $ | 774,134 | $ | 16,120,079 | 4.80 | % | ||||||||||||

| Interest-Bearing Liabilities |

||||||||||||||||||||||||

| Interest-bearing transaction deposits |

$ | 5,998 | $ | 5,962,114 | 0.10 | % | $ | 7,353 | $ | 5,827,370 | 0.13 | % | ||||||||||||

| Time deposits |

14,896 | 2,350,488 | 0.63 | % | 21,242 | 2,579,963 | 0.82 | % | ||||||||||||||||

| Public funds |

3,281 | 1,410,679 | 0.23 | % | 4,146 | 1,451,459 | 0.29 | % | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total interest bearing deposits |

24,175 | 9,723,281 | 0.25 | % | 32,741 | 9,858,792 | 0.33 | % | ||||||||||||||||

| Short-term borrowings |

4,542 | 806,082 | 0.56 | % | 6,065 | 843,798 | 0.72 | % | ||||||||||||||||

| Long-term debt |

12,762 | 389,153 | 3.28 | % | 12,876 | 338,875 | 3.80 | % | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total borrowings |

17,304 | 1,195,235 | 1.45 | % | 18,941 | 1,182,673 | 1.60 | % | ||||||||||||||||

| Total interest bearing liabilities cost |

$ | 41,479 | $ | 10,918,516 | 0.38 | % | $ | 51,682 | $ | 11,041,465 | 0.47 | % | ||||||||||||

| Net interest-free funding sources |

5,525,352 | 5,078,614 | ||||||||||||||||||||||

| Total Cost of Funds |

$ | 41,479 | $ | 16,443,868 | 0.25 | % | $ | 51,682 | $ | 16,120,079 | 0.32 | % | ||||||||||||

| Net Interest Spread (TE) |

$ | 691,141 | 4.07 | % | $ | 722,452 | 4.33 | % | ||||||||||||||||

| Net Interest Margin (TE) |

$ | 691,141 | $ | 16,443,868 | 4.20 | % | $ | 722,452 | $ | 16,120,079 | 4.48 | % | ||||||||||||

| (h) | Average securities does not include unrealized holding gains/losses on available for sale securities. |

- 12 -

Hancock Holding Company

Financial Highlights

(amounts in thousands)

(unaudited)

| Three Months Ended | Twelve Months Ended | |||||||||||||||||||

| 12/31/2013 | 9/30/2013 | 12/31/2012 | 12/31/2013 | 12/31/2012 | ||||||||||||||||

| Asset Quality Information |

||||||||||||||||||||

| Non-accrual loans (i) |

$ | 84,011 | $ | 100,649 | $ | 121,837 | $ | 84,011 | $ | 121,837 | ||||||||||

| Restructured loans (j) |

24,947 | 29,705 | 32,215 | 24,947 | 32,215 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total non-performing loans |

108,958 | 130,354 | 154,052 | 108,958 | 154,052 | |||||||||||||||

| ORE and foreclosed assets |

76,979 | 85,560 | 102,072 | 76,979 | 102,072 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total non-performing assets |

$ | 185,937 | $ | 215,914 | $ | 256,124 | $ | 185,937 | $ | 256,124 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Non-performing assets as a percent of loans, ORE and foreclosed assets |

1.50 | % | 1.83 | % | 2.19 | % | 1.50 | % | 2.19 | % | ||||||||||

| Accruing loans 90 days past due |

$ | 10,387 | $ | 15,620 | $ | 13,244 | $ | 10,387 | $ | 13,244 | ||||||||||

| Accruing loans 90 days past due as a percent of loans |

0.08 | % | 0.13 | % | 0.11 | % | 0.08 | % | 0.11 | % | ||||||||||

| Non-performing assets + accruing loans 90 days past due to loans, ORE and foreclosed assets |

1.58 | % | 1.96 | % | 2.31 | % | 1.58 | % | 2.31 | % | ||||||||||

| Net charge-offs - non-covered |

$ | 5,216 | $ | 5,430 | $ | 28,038 | $ | 24,309 | $ | 55,031 | ||||||||||

| Net charge-offs - covered |

(3,399 | ) | 506 | 3,230 | 2,355 | 26,069 | ||||||||||||||

| Net charge-offs - non-covered as a percent of average loans |

0.17 | % | 0.18 | % | 0.97 | % | 0.21 | % | 0.49 | % | ||||||||||

| Allowance for loan losses |

$ | 133,626 | $ | 138,233 | $ | 136,171 | $ | 133,626 | $ | 136,171 | ||||||||||

| Allowance for loan losses as a percent of period-end loans |

1.08 | % | 1.18 | % | 1.18 | % | 1.08 | % | 1.18 | % | ||||||||||

| Allowance for loan losses to non-performing loans + accruing loans 90 days past due |

111.97 | % | 94.69 | % | 81.40 | % | 111.97 | % | 81.40 | % | ||||||||||

| Provision for loan losses |

$ | 7,331 | $ | 7,569 | $ | 28,051 | $ | 32,734 | $ | 54,192 | ||||||||||

| Allowance for Loan Losses |

||||||||||||||||||||

| Beginning Balance |

$ | 138,223 | $ | 137,969 | $ | 135,591 | $ | 136,171 | $ | 124,881 | ||||||||||

| Net provision for loan losses - covered loans |

(532 | ) | 1,024 | 199 | 7,455 | 2,823 | ||||||||||||||

| Provision for loan losses - non-covered loans |

7,863 | 6,545 | 27,852 | 25,279 | 51,369 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net provision for loan losses |

7,331 | 7,569 | 28,051 | 32,734 | 54,192 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (Decrease) increase in FDIC loss share receivable |

(10,111 | ) | (1,379 | ) | 3,797 | (8,615 | ) | 38,198 | ||||||||||||

| Charge-offs - non-covered |

11,515 | 8,698 | 30,172 | 42,899 | 64,760 | |||||||||||||||

| Recoveries - non-covered |

(6,299 | ) | (3,268 | ) | (2,134 | ) | (18,590 | ) | (9,729 | ) | ||||||||||

| Net charge-offs - covered |

(3,399 | ) | 506 | 3,230 | 2,355 | 26,069 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net charge-offs |

1,817 | 5,936 | 31,268 | 26,664 | 81,100 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Ending Balance |

$ | 133,626 | $ | 138,223 | $ | 136,171 | $ | 133,626 | $ | 136,171 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net Charge-off Information |

||||||||||||||||||||

| Net charge-offs - non-covered: |

||||||||||||||||||||

| Commercial/real estate loans |

$ | 2,183 | $ | 1,267 | $ | 23,090 | $ | 11,684 | $ | 36,902 | ||||||||||

| Residential mortgage loans |

(197 | ) | 541 | 1,372 | 361 | 5,951 | ||||||||||||||

| Consumer loans |

3,230 | 3,622 | 3,576 | 12,264 | 12,178 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total net charge-offs - non-covered |

$ | 5,216 | $ | 5,430 | $ | 28,038 | $ | 24,309 | $ | 55,031 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Average loans: |

||||||||||||||||||||

| Commercial/real estate loans |

$ | 8,633,217 | $ | 8,582,849 | $ | 8,262,736 | $ | 8,480,527 | $ | 8,061,887 | ||||||||||

| Residential mortgage loans |

1,715,716 | 1,668,201 | 1,613,919 | 1,659,324 | 1,571,465 | |||||||||||||||

| Consumer loans |

1,573,446 | 1,570,345 | 1,667,134 | 1,585,353 | 1,651,387 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total average loans |

$ | 11,922,379 | $ | 11,821,395 | $ | 11,543,789 | $ | 11,725,204 | $ | 11,284,739 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net charge-offs - non-covered to average loans: |

||||||||||||||||||||

| Commercial/real estate loans |

0.10 | % | 0.06 | % | 1.11 | % | 0.14 | % | 0.46 | % | ||||||||||

| Residential mortgage loans |

(0.05 | )% | 0.13 | % | 0.34 | % | 0.02 | % | 0.38 | % | ||||||||||

| Consumer loans |

0.81 | % | 0.92 | % | 0.85 | % | 0.77 | % | 0.74 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total net charge-offs - non-covered to average loans |

0.17 | % | 0.18 | % | 0.97 | % | 0.21 | % | 0.49 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (i) | Non-accrual loans and accruing loans past due 90 days or more do not include non-accrual restructured loans and acquired credit-impaired loans which were written down to fair value upon acquisition and accrete interest income over the remaining life of the loan. |

| (j) | Included in restructured loans are $15.7 million, $19.1 million, and $15.8 million in non-accrual loans at 12/31/2013, 9/30/13, and 12/31/12, respectively. Total excludes acquired credit-impaired loans. |

- 13 -

Hancock Holding Company

Financial Highlights

(amounts in thousands)

(unaudited)

| Supplemental Asset Quality Information |

Originated Loans | Acquired Loans (k) | Covered Loans (l) | Total | ||||||||||||

| 12/31/2013 | ||||||||||||||||

| Non-accrual loans |

$ | 61,887 | $ | 18,580 | $ | 3,544 | $ | 84,011 | ||||||||

| Restructured loans |

21,222 | 3,725 | — | 24,947 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total non-performing loans |

83,109 | 22,305 | 3,544 | 108,958 | ||||||||||||

| ORE and foreclosed assets |

51,240 | — | 25,739 | 76,979 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total non-performing assets (m) |

$ | 134,349 | $ | 22,305 | $ | 29,283 | $ | 185,937 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Accruing loans 90 days past due |

$ | 3,298 | $ | 7,089 | — | $ | 10,387 | |||||||||

| Allowance for loan losses |

$ | 78,885 | $ | 1,647 | $ | 53,094 | $ | 133,626 | ||||||||

| 9/30/2013 | ||||||||||||||||

| Non-accrual loans |

$ | 75,663 | $ | 19,823 | $ | 5,163 | $ | 100,649 | ||||||||

| Restructured loans |

25,942 | 3,763 | — | 29,705 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total non-performing loans |

101,605 | 23,586 | 5,163 | 130,354 | ||||||||||||

| ORE and foreclosed assets |

60,187 | — | 25,373 | 85,560 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total non-performing assets |

$ | 161,792 | $ | 23,586 | $ | 30,536 | $ | 215,914 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Accruing loans 90 days past due |

$ | 12,512 | $ | 3,108 | — | $ | 15,620 | |||||||||

| Allowance for loan losses |

$ | 77,421 | $ | 463 | $ | 60,339 | $ | 138,223 | ||||||||

| Loans Outstanding |

Originated Loans | Acquired Loans (k) | Covered Loans (l) | Total | ||||||||||||

| 12/31/2013 | ||||||||||||||||

| Commercial non-real estate loans |

$ | 4,113,837 | $ | 926,997 | $ | 23,390 | $ | 5,064,224 | ||||||||

| Construction and land development loans |

752,381 | 142,931 | 20,229 | 915,541 | ||||||||||||

| Commercial real estate loans |

2,022,528 | 967,148 | 53,165 | 3,042,841 | ||||||||||||

| Residential mortgage loans |

1,196,256 | 315,340 | 209,018 | 1,720,614 | ||||||||||||

| Consumer loans |

1,409,130 | 119,603 | 52,864 | 1,581,597 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total loans |

$ | 9,494,132 | $ | 2,472,019 | $ | 358,666 | $ | 12,324,817 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Change in loan balance from previous quarter |

$ | 793,365 | ($ | 169,684 | ) | ($ | 33,336 | ) | $ | 590,345 | ||||||

|

|

|

|

|

|

|

|

|

|||||||||

| 9/30/2013 | ||||||||||||||||

| Commercial non-real estate loans |

$ | 3,633,490 | $ | 967,485 | $ | 24,340 | $ | 4,625,315 | ||||||||

| Construction and land development loans |

738,983 | 158,228 | 23,197 | 920,408 | ||||||||||||

| Commercial real estate loans |

1,816,402 | 1,038,287 | 60,280 | 2,914,969 | ||||||||||||

| Residential mortgage loans |

1,124,649 | 347,054 | 223,494 | 1,695,197 | ||||||||||||

| Consumer loans |

1,387,243 | 130,649 | 60,691 | 1,578,583 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total loans |

$ | 8,700,767 | $ | 2,641,703 | $ | 392,002 | $ | 11,734,472 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Change in loan balance from previous quarter |

$ | 447,012 | ($ | 355,328 | ) | ($ | 38,709 | ) | $ | 52,975 | ||||||

|

|

|

|

|

|

|

|

|

|||||||||

| (k) | Loans which have been acquired and no allowance brought forward in accordance with acquisition accounting. |

| (l) | Acquired loans which are covered by loss sharing agreements with the FDIC providing considerable protection against credit risk. |

| (m) | ORE received in settlement of acquired loans is no longer subject to purchase accounting guidance and has been included with ORE from originated loans. ORE received in settlement of covered loans remains covered under the FDIC loss share agreements. |

- 14 -

Fourth Quarter 2013

Financial Results

January

23, 2014

Fourth Quarter 2013

Financial Results

January

23, 2014 |

Forward-Looking

Statements

Forward-Looking

Statements

Certain of the statements or information included in this presentation

may constitute forward-looking statements.

Forward-looking statements include projections of revenue, costs, results of operations or

financial condition or statements regarding future market conditions or

our potential plans and strategies for the future.

Forward-looking statements that we may make include, but may not be limited to, comments

with respect to future levels of economic activity in our

markets, loan growth, deposit trends, credit quality

trends, future sales of nonperforming assets, net interest margin

trends, future expense levels and the ability to achieve

reductions in non-interest expense or other cost savings, projected tax rates, future

profitability, improvements in expense to revenue (efficiency) ratio,

purchase accounting impacts such as accretion levels, the impact

of the branch rationalization process, and the financial impact of regulatory

requirements. Hancock’s ability to accurately project

results or predict the effects of future plans or strategies is

inherently limited. We believe that the expectations

reflected or implied by any forward-looking statements are based on

reasonable assumptions, but actual results and performance could

differ materially from those set forth in

the forward-looking statements. Factors that could cause

actual results or outcomes to differ from those expressed in the

Company’s forward-looking statements include, but are not limited to, those outlined in

Hancock’s SEC filings, including the “Risk

Factors” section of the Company’s 10-K for the

year ended December 31, 2012 and most recent form

10-Q. Hancock undertakes no obligation to update or revise

any forward-looking statements, and you are cautioned not to

place undue reliance on such forward-looking statements. 2

|

Fourth Quarter Highlights:

Fourth Quarter Highlights:

Core Improvements Largely Offset Declining PAAs

Core Improvements Largely Offset Declining PAAs

3

Core net interest income (TE) increased approximately $1.5 million and

core net interest margin (NIM) improved 3 basis points (bps)

linked-quarter –

The Company defines its core results as reported results less the

impact of net purchase accounting adjustments (PAAs)

Operating expenses declined $4.2 million linked-quarter and the

Company remains on track to meet its first quarter of 2014

expense target Approximately $625 million linked-quarter net

loan growth, or 22% annualized, and over $900 million, or 8%,

year-over-year loan growth –

Each excluding the FDIC-covered loan portfolio

Purchase accounting loan accretion declined approximately $8 million,

or $.06 per diluted common share after tax

Continued improvement in overall asset quality metrics

Tax rate declined to 20%, mainly related to benefits from additional

investments in New Market Tax Credit projects in the fourth

quarter |

•

Net income (operating) $46 million or $.55 per diluted common share,

in line with Company guidance

•

ROA (operating) 0.97%

•

ROTCE (operating) 11.59%

•

Net income includes one-time

noninterest expense items of

$17.1 million ($11.1 million

after tax), or $.14 per diluted

common share

Fourth Quarter Highlights:

Fourth Quarter Highlights:

Core Improvements Largely Offset Declining PAAs

Core Improvements Largely Offset Declining PAAs

4

Operating income is defined as net income excluding tax-effected

securities transactions gains or losses and one-time

noninterest expense items. * Core is defined as

reported results less purchase accounting adjustments. See

table on slide 13. ** Noninterest expense as a percent of

total revenue (TE) before amortization of purchased intangibles,

one-time noninterest expense items and securities

transactions. |

Results In Line With Guidance

Results In Line With Guidance

Results In Line With Guidance

•

Volatility related to excess

cash recoveries (included in

loan accretion totals) has been

impacting quarterly operating

EPS results (additional data on

slide 13) •

Projections do not include

excess cash recoveries

•

Expected 4Q13 operating EPS

to be flat to slightly down

•

No excess cash recoveries

forecast for 2014

5 |

Strong Level of Originations Across The

Strong Level of Originations Across The

Footprint

Footprint

•

Excluding FDIC covered loans, total loans of $12.0

billion were up $625 million

–

The largest component of linked-quarter net growth was in

the commercial and industrial (C&I) portfolio (+10%),

followed by increases in the commercial real estate (CRE)

(+5%) and residential mortgage (+3%) portfolios

•

Many of the markets across the Company’s footprint

reported net loan growth during the quarter, with the

majority of the growth in south Louisiana, Houston

and Florida markets

•

For the full year of 2014, management expects

period-end loan growth in the mid-single digit range

Period-end balances. As of December 31, 2013

6 |

Whitney Portfolio Continues

Whitney Portfolio Continues

Solid Performance

Solid Performance

•

Loan mark on the acquired-performing portfolio accreted into

earnings over the life of the portfolio

•

Credit-impaired loan mark available for charge-offs; if not

needed for charge-offs then accreted into income

•

Quarterly reviews of accretion levels and portfolio performance will

impact reported margin 7

As of December 31, 2013

$s in millions

Credit-

Impaired

Performing

Total

Whitney loan mark at acquisition

(as adjusted in 4Q11)

$284

$187

$471

Acquired portfolio loan balances at acquisition

$818

$6,101

$6,919

Discount at acquisition

34.7%

3.1%

6.8%

Remaining Whitney loan mark at 12/31/13

$128

$30

$158

Remaining acquired portfolio loan balances at 12/31/13

$200

$2,431

$2,631

Acquired loan charge-offs from acquisition thru

12/31/13

$29

$10

$39

Discount at 12/31/13

64%

1.2%

6.0% |

Peoples First Loan Mark Used

Peoples First Loan Mark Used

For Charge-Offs

For Charge-Offs

•

FDIC covered loan portfolio

•

Entire loan mark available for charge-offs; if not needed for

charge-offs then accreted into income •

Quarterly reviews of accretion levels and portfolio performance will

impact reported margin •

FDIC loss share receivable totaled $114 million at December 31,

2013 Balance reflects the total amount expected to be collected

from the FDIC 8

$s in millions

Credit Impaired

Peoples First loan mark at acquisition (12/2009)

$509

Charge-offs from acquisition thru 12/31/13

$413

Accretion since acquisition date

$85

Remaining loan mark at 12/31/13

$50

Impairment reserve at 12/31/13

$53

Remaining covered portfolio loan balances at 12/31/13

$409

Discount & allowance at 12/31/13

25%

As of December 31, 2013 |

•

Nonperforming assets totaled $186 million, down $30

million compared to September 30, 2013

–

ORE and foreclosed assets declined $9 million linked-quarter

–

Nonperforming loans down $21 million, or 16%,

compared to 3Q13

•

The allowance for loan losses was $133.6 million (1.08%)

at year-end, down from $138.2 million (1.18%) linked-

quarter

–

The decline in the allowance was primarily related to a $7.2 million

reversal of a previous impairment on FDIC covered loans

–

The allowance maintained on the non-covered portion of the loan

portfolio increased $2.6 million linked-quarter, totaling

$80.5 million •

Provision for loan losses was $7.3 million, slightly down

from $7.6 million in 3Q13

–

4Q13 includes $7.9 million for the non-covered loan

portfolio, compared to $6.5 million in 3Q13

•

Non-covered net charge-offs totaled $5.2 million, or 0.17%,

compared to $5.4 million, or 0.18%, in 3Q13

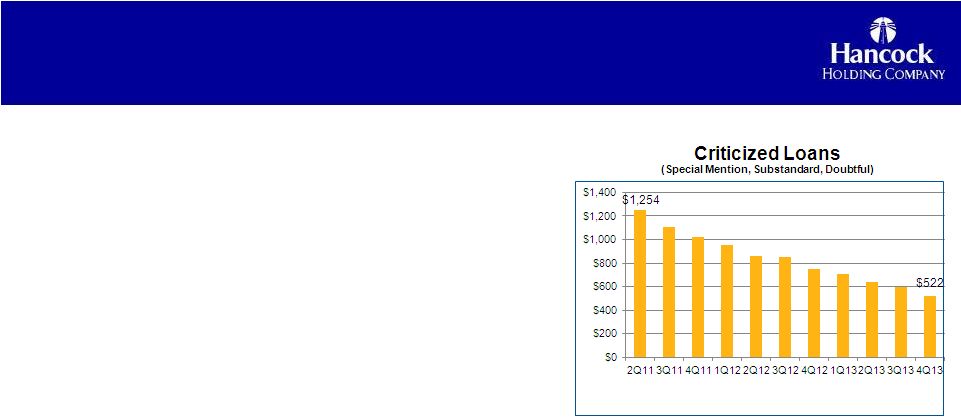

Continued Improvement In

Continued Improvement In

Asset Quality Metrics

Asset Quality Metrics

9

$s in millions

Excludes covered portfolio and gross of the Whitney loan mark

As of December 31, 2013 |

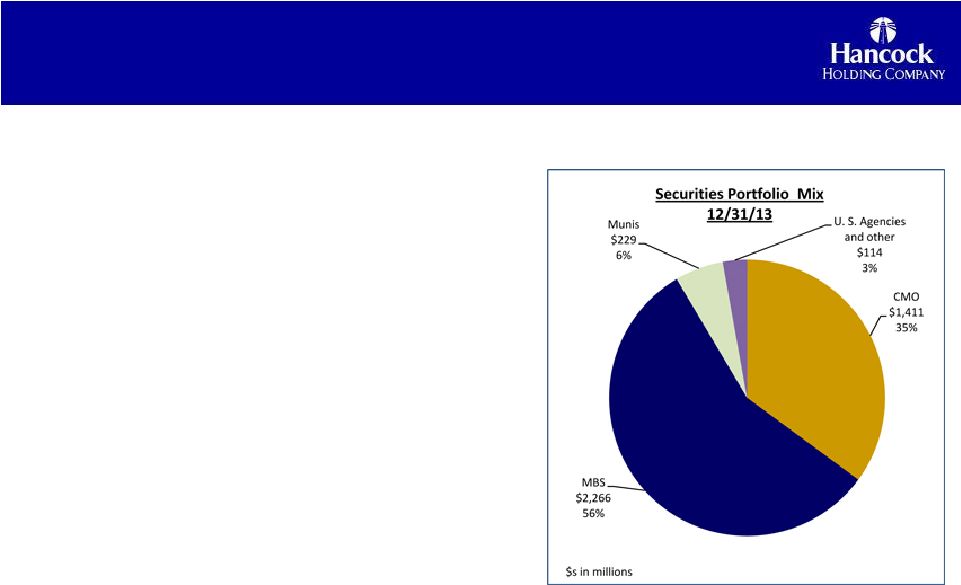

Securities Portfolio Continues To Fund

Loan Growth

Securities Portfolio Continues To Fund

Loan Growth

10

•

Portfolio totaled $4.0 billion, down $82 million

linked-quarter

•

Decline continues to fund loan growth

–

Better earning asset mix

•

Yield 2.43% for 4Q13, up 19 bps

•

Slowdowns in prepayments on mortgage-backed

securities continued to positively impact overall

portfolio yield during the quarter

•

Unrealized gain (net) of $13.0 million on AFS

•

65% HTM, 35% AFS

•

Duration 3.99, up from 3.84 at September 30, 2013

–

Extends to 4.2 in +100 bps shift in the yield curve

–

Extends to 4.5 in +200 bps shift in the yield curve

Period-end balances. As of December 31, 2013

|

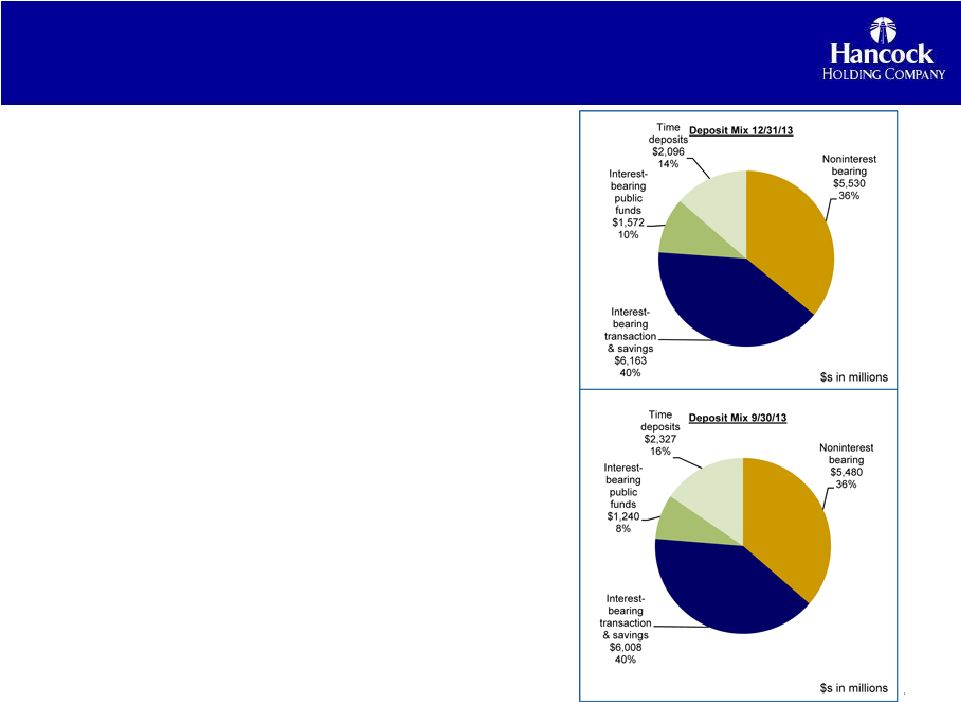

Strong Core Deposit

Strong Core Deposit

Funding

Funding

•

Total deposits $15.4 billion, up over $300

million linked-quarter

•

Linked-quarter growth related to increases in

interest bearing public fund deposits of $331

million

•

Time deposits declined $231 million, with the

remaining deposit categories up $206 million

•

Funding mix remained strong

–

Noninterest-bearing demand deposits (DDA)

comprised 36% of total period-end deposits

–

No and low cost deposits comprised 76% of total period-end

deposits

–

Cost of funds declined 1bp to 23 bps

11

Period-end balances. As of December 31, 2013

|

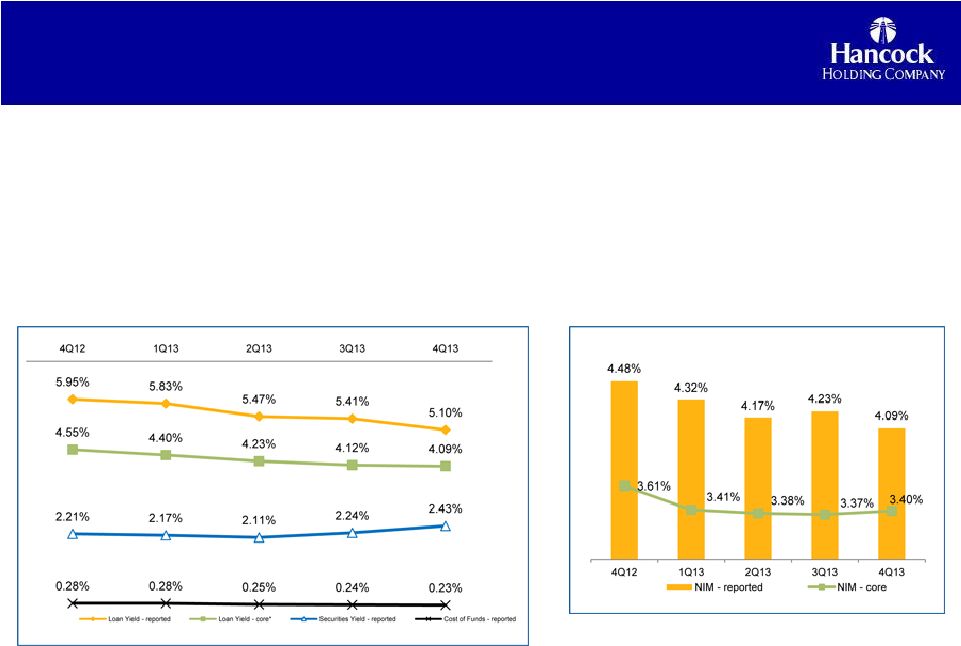

Core NIM Expansion; Reported NIM

Core NIM Expansion; Reported NIM

Impacted By Decline in PAAs

Impacted By Decline in PAAs

•

Reported net interest margin (NIM) 4.09%, down 14 bps

linked-quarter –

Approximately 17 bps of NIM compression related to the $7.1 million

decrease in net purchase accounting adjustments

linked-quarter •

Core NIM expanded 3 bps

–

Slight decline in core loan yield (3bps) offset by increased yield on

securities (+19bps) portfolio and a lower cost of funds

(1bp) –

Better earning asset mix and increased loan volume

12

Core NIM = reported net interest income (TE) excluding total net

purchase accounting adjustments, annualized, as a percent of

average earning assets. (See slide 12)

As of December 31, 2013 |

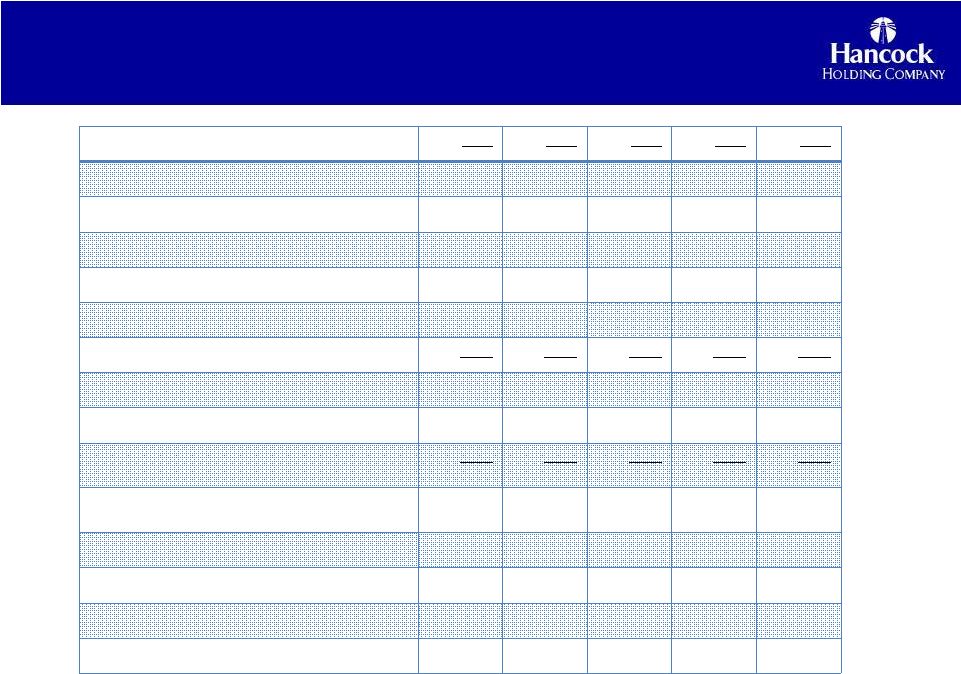

Purchase Accounting Adjustments

Core NII & NIM Reconciliation

Purchase Accounting Adjustments

Core NII & NIM Reconciliation

13

($s in millions)

4Q13

3Q13

2Q13

1Q13

4Q12

Net Interest Income (TE) –

reported (NII)

$168.5

$174.1

$171.8

$176.7

$182.8

Whitney expected loan accretion (performing)

9.3

10.4

12.8

13.7

17.6

Whitney expected loan accretion (credit impaired)

18.2

15.8

15.9

14.6

11.5

Peoples First expected loan accretion

2.8

4.3

4.1

4.5

7.4

Excess cash recoveries*

---

7.7

3.1

7.5

4.0

Total Loan Accretion

$30.3

$38.3

$35.9

$40.3

$40.5

Whitney premium bond amortization

(1.8)

(2.8)

(3.4)

(3.5)

(5.4)

Whitney and Peoples First CD accretion

.1

.1

.2

.3

.3

Total Net Purchase Accounting

Adjustments (PAAs) impacting NII

$28.5

$35.6

$32.7

$37.1

$35.5

Net Interest Income (TE) –

core

(Reported NII less net PAAs)

$140.0

$138.5

$139.0

$139.7

$147.3

Average Earning Assets

$16,377

$16,385

$16,500

$16,518

$16,246

Net Interest Margin –

reported

4.09%

4.23%

4.17%

4.32%

4.48%

Net Purchase Accounting Adjustments (%)

.69%

.86%

.79%

.91%

.87%

Net Interest Margin -

core

3.40%

3.37%

3.38%

3.41%

3.61%

* Excess cash recoveries include cash collected on certain zero

carrying value acquired loan pools above expected amounts. |

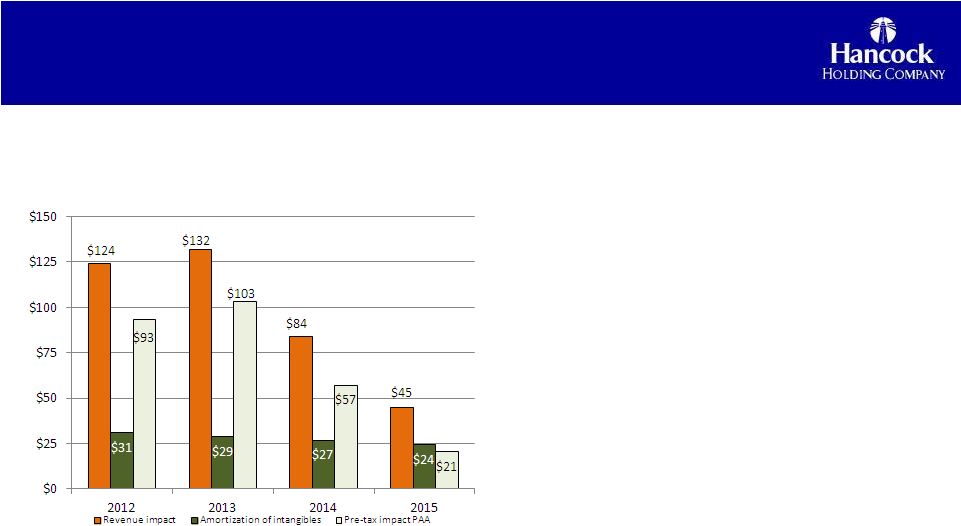

Purchased Loan Accretion Declining

Purchased Loan Accretion Declining

•

Net purchase accounting

adjustments will be part of

earnings through 2015

•

Revenue includes loan

accretion, securities

amortization, CD accretion

•

Amortization of intangibles

mainly related to the Whitney

acquisition

14

$s in millions

Impact of Purchase Accounting Adjustments 2012-2015

(2014-2015 projections will be updated quarterly; subject to

volatility) As of December 31, 2013

|

Noninterest Income Reflects Changes

Noninterest Income Reflects Changes

Related to Seasonality, Economy

Related to Seasonality, Economy

15

As of December 31, 2013

•

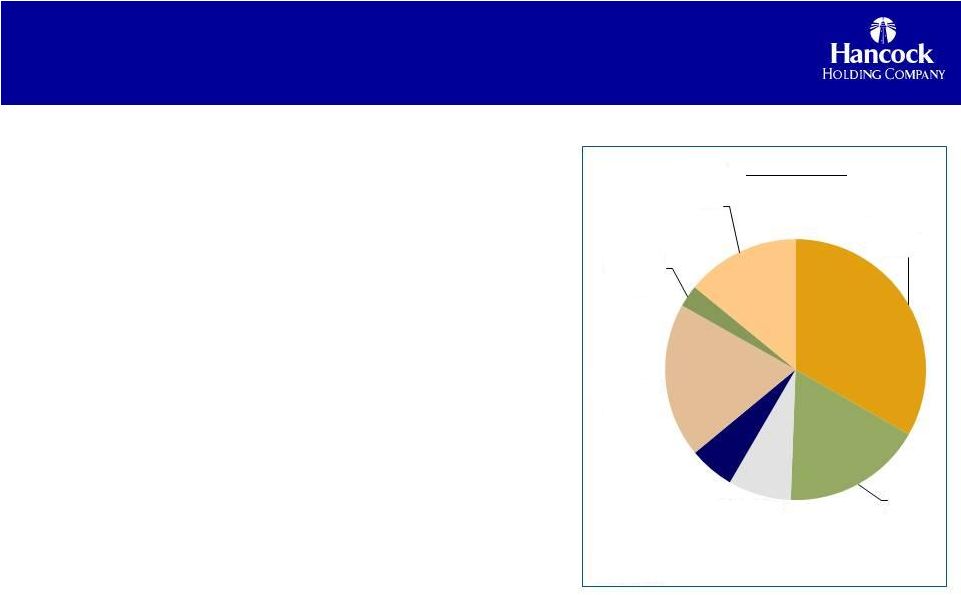

Noninterest income totaled $59.0 million, down $4.1 million

linked-quarter •

Service charges on deposits totaled $19.6 million, down $0.9 million

from 3Q13, due, in part, to fewer business days in the fourth

quarter •

Bankcard and ATM fees totaled $11.3 million, down approximately $1.0

million from 3Q13

–

Decline due, in part, to a one-time Visa-related incentive

recorded in 3Q13

•

Trust, investment and annuity, and insurance fees totaled $18.1

million, down $0.2 million from 3Q13

–

During the fourth quarter, an increase of $0.7 million, or 8%, in trust

fees was offset by declines in investment and annuity, and

insurance fees •

Other noninterest income totaled $8.3 million, down $1.2 million, or

12%, linked-quarter

–

The decline mainly reflects a lower level of expected future losses on

covered loans, which resulted in an increase of $1.1 million in

the amortization of the indemnification asset

•

Fees from secondary mortgage operations totaled $1.6 million, down $0.9

million linked-quarter

–

The decline mainly reflects a continued slowdown in mortgage loan

activity, reflecting mainly the impact of increased

longer-term interest rates on originations

–

The quarter’s activity also reflects a continued higher level of

portfolio production compared to secondary market

production $s in millions

Service

Charges on

Deposit

$19.6

33%

Trust

$10.2

17%

Investment &

annuity

$4.6

8%

Insurance

$3.3

6%

ATM

$11.3

19%

Secondary

mortgage

operations

$1.6

3%

Other

$8.3

14%

Bankcard and

Fee Mix 4Q13 |

Noninterest Expense Includes One-Time Items;

Noninterest Expense Includes One-Time Items;

Operating Expense Continues To Decline

Operating Expense Continues To Decline

•

Noninterest expense totaled $174.2 million in 4Q13

–

Includes $17.1 million of one-time costs mainly related

to the expense & efficiency initiative

•

Noninterest expense excluding one-time costs (or operating

expense) totaled $157.1 million, down $4.2 million from

3Q13

•

Personnel expense, the largest component of total

noninterest expense, totaled $84.9 million, a decrease

of $1.9 million linked-quarter

•

Occupancy and equipment totaled $16.3 million, down

$1.2 million linked-quarter

•

The reduction in personnel, occupancy and equipment

reflect a full quarter’s impact from the closing of 26