Attached files

| file | filename |

|---|---|

| 8-K - 8-K - US BANCORP \DE\ | d661409d8k.htm |

| EX-99.1 - EX-99.1 - US BANCORP \DE\ | d661409dex991.htm |

January 22, 2014

Richard K. Davis

Chairman, President and CEO

Andy Cecere

Vice Chairman and CFO

Exhibit 99.2

U.S. Bancorp

4Q13 Earnings

Conference Call

U.S. Bancorp

4Q13 Earnings

Conference Call |

2

Forward-looking Statements and Additional Information

The following information appears in accordance with the Private Securities Litigation Reform Act of

1995: This presentation contains forward-looking statements about U.S. Bancorp. Statements that

are not historical or current facts, including statements about beliefs and expectations, are

forward-looking statements and are based on the information available to, and assumptions and

estimates made by, management as of the date made. These forward-looking statements cover,

among other things, anticipated future revenue and expenses and the future plans and prospects

of U.S. Bancorp. Forward-looking statements involve inherent risks and uncertainties,

and important factors could cause actual results to differ materially from those anticipated. Global and domestic economies could

fail to recover from the recent economic downturn or could experience another severe contraction,

which could adversely affect U.S. Bancorp’s revenues and the values of its assets and

liabilities. Global financial markets could experience a recurrence of significant turbulence, which

could reduce the availability of funding to certain financial institutions and lead to a tightening of

credit, a reduction of business activity, and increased market volatility. Continued

stress in the commercial real estate markets, as well as a delay or failure of recovery in the residential

real estate markets, could cause additional credit losses and deterioration in asset values. In

addition, U.S. Bancorp’s business and financial performance is likely to be negatively

impacted by recently enacted and future legislation and regulation. U.S. Bancorp’s results could also be

adversely affected by deterioration in general business and economic conditions; changes in interest

rates; deterioration in the credit quality of its loan portfolios or in the value of the

collateral securing those loans; deterioration in the value of securities held in its investment securities

portfolio; legal and regulatory developments; increased competition from both banks and non-banks;

changes in customer behavior and preferences; effects of mergers and acquisitions and related

integration; effects of critical accounting policies and judgments; and management’s

ability to effectively manage credit risk, residual value risk, market risk, operational risk, interest rate risk and liquidity risk.

For discussion of these and other risks that may cause actual results to differ from

expectations, refer to U.S. Bancorp’s Annual Report on Form 10-K for the year

ended December 31, 2012, on file with the Securities and Exchange Commission, including the sections entitled “Risk

Factors” and “Corporate Risk Profile” contained in Exhibit 13, and all subsequent

filings with the Securities and Exchange Commission under Sections 13(a), 13(c), 14 or 15(d) of

the Securities Exchange Act of 1934. Forward-looking statements speak only as of the date they are made,

and U.S. Bancorp undertakes no obligation to update them in light of new information or future events.

This presentation includes non-GAAP financial measures to describe U.S. Bancorp’s

performance. The reconciliations of those measures to GAAP measures are provided within

or in the appendix of the presentation. These disclosures should not be viewed as a substitute for

operating results determined in accordance with GAAP, nor are they necessarily comparable to

non-GAAP performance measures that may be presented by other companies.

|

2013 Full Year Highlights

Record net income of $5.8 billion; $3.00 per diluted common share

Industry-leading profitability measures, including ROA of 1.65%, ROCE of 15.8%

and efficiency ratio of 52.4%

Average loan growth of 5.6% vs. 2012 and average deposit growth of 6.3%

vs. 2012

Net charge-offs declined 30.1% vs. 2012

Nonperforming assets declined 23.7% vs. 2012 (13.2% excluding covered assets)

Capital generation continues to reinforce capital position

•

Tier 1 common equity ratio of 9.4% vs. 9.0% in 2012

•

Repurchased 65 million shares of common stock during 2013

•

In

total,

returned

$4.0

billion,

or

71%,

of

our

earnings

in

2013

to

shareholders

3

4Q13 Earnings

Conference Call |

4

4Q13 Earnings

Conference Call

4Q13 Highlights

Net income of $1.5 billion; $0.76 per diluted common share

Average loan growth of 5.7% vs. 4Q12 and average loan growth of 1.5%

vs. 3Q13

Strong average deposit growth of 5.4% vs. 4Q12 and 1.8% vs. 3Q13

Net charge-offs declined 4.9% vs. 3Q13

Nonperforming assets declined 7.9% vs. 3Q13 (3.6% excluding covered assets)

Capital generation continues to reinforce capital position

•

Common equity tier 1 ratio of 8.8% estimated using final rules for the Basel III

standardized approach

•

Tier 1 common equity ratio of 9.4%; Tier 1 capital ratio of 11.2%

Returned 65% of earnings to shareholders in 4Q13

•

Repurchased 13 million shares of common stock during 4Q13

|

5

4Q13 Earnings

Conference Call

Performance Ratios

Return on Average Common Equity

and Return on Average Assets

Efficiency Ratio and

Net Interest Margin

Return on Avg Common Equity

Return on Avg Assets

Efficiency Ratio

Net Interest Margin

15.6%

16.0%

16.1%

15.8%

15.4%

1.62%

1.65%

1.70%

1.65%

1.62%

1.0%

1.5%

2.0%

2.5%

3.0%

8%

11%

14%

17%

20%

4Q12

1Q13

2Q13

3Q13

4Q13

52.6%

50.7%

51.7%

52.4%

54.9%

3.55%

3.48%

3.43%

3.43%

3.40%

2.0%

2.5%

3.0%

3.5%

4.0%

45%

50%

55%

60%

65%

4Q12

1Q13

2Q13

3Q13

4Q13

Efficiency ratio computed as noninterest expense divided by the sum of net interest income on a

taxable-equivalent

basis and noninterest income excluding securities gains (losses) net |

6

4Q13 Earnings

Conference Call

Taxable-equivalent basis

Revenue Growth

Year-Over-Year Growth

0.2%

(1.1%)

(2.4%)

(5.6%)

(4.4%)

$ in millions

$5,112

$4,874

$4,948

$4,891

$4,889

3,500

4,000

4,500

5,000

5,500

4Q12

1Q13

2Q13

3Q13

4Q13 |

Loan and Deposit Growth

Average Balances

Year-Over-Year Growth

$ in billions

5.7%

$229.4

5.7%

$232.8

6.4%

$220.3

5.8%

$222.4

5.2%

$225.2

5.5%

$252.4

5.4%

$256.9

9.2%

$243.8

7.3%

$245.0

7.0%

$247.4

260.0

240.0

220.0

200.0

180.0

4Q12

1Q13

2Q13

3Q13

4Q13

Loans

Deposits

7

4Q13 Earnings

Conference Call |

8

4Q13 Earnings

Conference Call

Credit Quality

* Excluding Covered Assets (assets subject to loss sharing agreements with

FDIC) Net Charge-offs

Nonperforming Assets*

$ in millions

Net Charge-offs (Left Scale)

NCOs to Avg Loans (Right Scale)

Nonperforming Assets (Left Scale)

NPAs to Loans plus ORE (Right Scale)

$468

$433

$392

$328

$312

0.85%

0.79%

0.70%

0.57%

0.53%

0.00%

0.75%

1.50%

2.25%

3.00%

0

200

400

600

800

4Q12

1Q13

2Q13

3Q13

4Q13

$2,088

$2,029

$1,921

$1,880

$1,813

0.98%

0.95%

0.88%

0.85%

0.80%

0.00%

0.75%

1.50%

2.25%

3.00%

0

800

1,600

2,400

3,200

4Q12

1Q13

2Q13

3Q13

4Q13 |

9

4Q13 Earnings

Conference Call

Earnings Summary

$ in millions, except per-share data

Taxable-equivalent basis

Full Year

Full Year

4Q13

3Q13

4Q12

vs 3Q13

vs 4Q12

2013

2012

% B/(W)

Net Interest Income

2,733

$

2,714

$

2,783

$

0.7

(1.8)

10,828

$

10,969

$

(1.3)

Noninterest Income

2,156

2,177

2,329

(1.0)

(7.4)

8,774

9,319

(5.8)

Total Revenue

4,889

4,891

5,112

(0.0)

(4.4)

19,602

20,288

(3.4)

Noninterest Expense

2,682

2,565

2,686

(4.6)

0.1

10,274

10,456

1.7

Operating Income

2,207

2,326

2,426

(5.1)

(9.0)

9,328

9,832

(5.1)

Net Charge-offs

312

328

468

4.9

33.3

1,465

2,097

30.1

Excess Provision

(35)

(30)

(25)

--

--

(125)

(215)

--

Income before Taxes

1,930

2,028

1,983

(4.8)

(2.7)

7,988

7,950

0.5

Applicable Income Taxes

459

598

608

23.2

24.5

2,256

2,460

8.3

Noncontrolling Interests

(15)

38

45

--

--

104

157

(33.8)

Net Income

1,456

1,468

1,420

(0.8)

2.5

5,836

5,647

3.3

Preferred Dividends/Other

67

68

71

1.5

5.6

284

264

(7.6)

NI to Common

1,389

$

1,400

$

1,349

$

(0.8)

3.0

5,552

$

5,383

$

3.1

Diluted EPS

0.76

$

0.76

$

0.72

$

-

5.6

3.00

$

2.84

$

5.6

Average Diluted Shares

1,832

1,843

1,880

0.6

2.6

1,849

1,896

2.5

% B/(W) |

10

4Q13 Earnings

Conference Call

4Q13 Results -

Key Drivers

vs. 4Q12

Net Revenue decline of 4.4%

•

Net interest income decline of 1.8%;

net interest margin of 3.40% vs. 3.55% in 4Q12

•

Noninterest income decline of 7.4%

Noninterest expense decline of 0.1%

Provision for credit losses lower by $166 million

•

Net charge-offs lower by $156 million

•

Provision lower than NCOs by $35 million vs. $25 million in 4Q12

vs. 3Q13

Net Revenue flat

•

Net

interest

income

growth

of

0.7%;

net

interest

margin

of

3.40%

vs.

3.43%

in

3Q13

•

Noninterest income decline of 1.0%

Noninterest expense increase of 4.6%

Provision for credit losses lower by $21 million

•

Net charge-offs lower by $16 million

•

Provision lower than NCOs by $35 million vs. $30 million in 3Q13

4Q13

4Q13

B/(W)

vs. 3Q13

vs. 4Q12

Noninterest

Expense -

Other

(31.0)

$

(53.0)

$

Income Taxes

84.0

106.0

Noncontrolling Interests

(53.0)

(53.0)

Total

0.0

$

0.0

$

Impact of Accounting Presentation Changes Related

to Investments in Tax-Advantaged Projects ($ in millions)

|

11

4Q13 Earnings

Conference Call

Capital Position

$ in billions

RWA = risk-weighted assets

4Q13

3Q13

2Q13

1Q13

4Q12

Shareholders' equity

41.1

$

40.1

$

39.7

$

39.5

$

39.0

$

Tier 1 capital

33.4

32.7

32.2

31.8

31.2

Total risk-based capital

39.3

38.9

38.4

38.1

37.8

Tier 1 common equity ratio

9.4%

9.3%

9.2%

9.1%

9.0%

Tier 1 capital ratio

11.2%

11.2%

11.1%

11.0%

10.8%

Total risk-based capital ratio

13.2%

13.3%

13.3%

13.2%

13.1%

Leverage ratio

9.6%

9.6%

9.5%

9.3%

9.2%

Tangible common equity ratio

7.7%

7.4%

7.5%

7.4%

7.2%

Tangible common equity as a % of RWA

9.1%

8.9%

8.9%

8.8%

8.6%

Basel

III

Common equity tier 1 to risk-weighted assets

estimated using final rules for the Basel III

standardized approach

8.8%

8.6%

8.6%

-

-

Common equity tier 1 to risk-weighted assets

approximated using proposed rules for the Basel III

standardized approach released June 2012

-

-

8.3%

8.2%

8.1% |

12

4Q13 Earnings

Conference Call

Mortgage Repurchase

Mortgages Repurchased and Make-whole Payments

Mortgage Representation and Warranties Reserve

$ in millions

4Q13

3Q13

2Q13

1Q13

4Q12

Beginning Reserve

$176

$190

$233

$240

$220

Net Realized Losses

(63)

(13)

(16)

(23)

(32)

Change in Reserve

(30)

(1)

(27)

16

52

Ending Reserve

$83

$176

$190

$233

$240

Mortgages

repurchased

and make-whole

payments

$32

$42

$41

$79

$57

Repurchase activity lower than

peers due to:

•

Conservative credit and

underwriting culture

•

Disciplined origination process -

primarily conforming

loans

(

95% sold to GSEs)

Do not participate in private

placement securitization market

Outstanding repurchase and

make-whole requests balance

= $89 million |

13

4Q13 Earnings

Conference Call |

14

4Q13 Earnings

Conference Call

Appendix |

Covered

Commercial

CRE

Res Mtg

Credit

Card

Retail

Average Loans

Average Loans

Key Points

$ in billions

vs. 4Q12

Average total loans grew by $12.5 billion, or 5.7%

Average total loans, excluding covered loans,

were higher by 7.3%

Average total commercial loans increased $5.0

billion, or 7.8%; average commercial real estate

loans increased $2.5 billion, or 6.7%; average

residential mortgage loans increased $7.6 billion,

or 17.6%

vs. 3Q13

Average total loans grew by $3.4 billion, or 1.5%

Average total loans, excluding covered loans,

were higher by 1.9%

Average total commercial loans increased $0.9

billion, or 1.3%; average commercial real estate

loans increased $0.8 billion, or 2.1%; average

residential mortgage loans increased $1.6 billion,

or 3.2%

Year-Over-Year Growth

6.4%

5.8%

5.2%

5.7%

5.7%

Covered

Commercial

CRE

Res Mtg

Retail

Credit Card

$220.3

$222.4

$225.2

$229.4

$232.8

15

4Q13 Earnings

Conference Call

(0.8%)

(1.4%)

(2.2%)

(2.1%)

(1.1%)

1.9%

(1.5%)

(1.7%)

2.3%

4.7%

19.0%

19.2%

19.7%

17.6%

2.9%

3.4%

3.7%

5.1%

6.7%

15.7%

14.3%

11.2%

9.4%

7.8%

4Q12

1Q13

2Q13

3Q13

4Q13

19.9%

280

210

140

70

0 |

16

4Q13 Earnings

Conference Call

8.8%

7.6%

(4.3%)

(5.7%)

(8.0%)

9.6%

15.6%

24.5%

17.8%

16.2%

4.7%

4.6%

6.4%

10.1%

9.2%

14.2%

4.4%

3.6%

0.2%

2.5%

0

80

160

240

320

4Q12

1Q13

2Q13

3Q13

4Q13

Time

Money

Market

Checking

& Savings

Noninterest

-bearing

Average Deposits

Average Deposits

Key Points

$ in billions

vs. 4Q12

Average total deposits increased by $13.1

billion, or 5.4%

Average low cost deposits (NIB, interest

checking, money market and savings)

increased by $16.8 billion, or 8.5%

vs. 3Q13

Average total deposits increased by $4.5

billion, or 1.8%

Average low cost deposits increased by $9.8

billion, or 4.8%

Year-Over-Year Growth

9.2%

7.3%

7.0%

5.5%

5.4%

Time

Money Market

Checking and Savings

Noninterest-bearing

$243.8

$245.0

$247.4

$252.4

$256.9 |

17

4Q13 Earnings

Conference Call

Net Interest Income

Net Interest Income

Key Points

$ in millions

Taxable-equivalent basis

vs. 4Q12

Average earning assets grew by $7.3 billion,

or 2.3%

Net interest margin lower by 15 bps (3.40%

vs. 3.55%) driven by:

•

Lower reinvestment rates on investment securities,

as well as growth in the portfolio, and lower rates

on loans

•

Partially offset by lower rates on deposits and a

reduction in higher cost long-term debt

vs. 3Q13

Average earning assets grew by $4.5 billion,

or 1.4%

Net interest margin lower by 3 bps (3.40% vs.

3.43%) driven by:

•

Growth in lower rate investment securities

•

Higher cash balances at the Federal Reserve

Year-Over-Year Growth

4.1%

0.7%

(1.5%)

(2.5%)

(1.8%)

$2,783

$2,709

$2,672

$2,714

$2,733

3.55%

3.48%

3.43%

3.43%

3.40%

0.0%

2.0%

4.0%

6.0%

8.0%

0

1,000

2,000

3,000

4,000

4Q12

1Q13

2Q13

3Q13

4Q13

Net Interest Income

Net Interest Margin |

18

4Q13 Earnings

Conference Call

Noninterest Income

Noninterest Income

Key Points

$ in millions

Payments = credit and debit card revenue, corporate payment products revenue and

merchant processing; Service charges = deposit service charges, treasury

management fees and ATM processing services vs. 4Q12

Noninterest income declined by $173 million, or

7.4%, driven by:

•

Mortgage banking revenue decline of $245 million

•

Higher credit and debit card revenue (8.7% increase) due to

higher transaction volumes including the impact of business

expansion; higher merchant processing (3.7% increase) due to

an increase in product fees and higher volumes

•

Higher trust and investment management fees (7.6% increase)

due to improved market conditions and business expansion;

higher investment product fees (15.4% increase) due to higher

sales volumes and fees

•

Higher commercial products revenue (7.5% increase), mainly

due to higher syndication fees on tax-advantaged projects

•

Lower corporate payments revenue (6.7% decline) due to lower

government-related transactions

vs. 3Q13

Noninterest income declined by $21 million, or

1.0%, driven by:

•

Mortgage banking revenue decline of $97 million

•

Lower corporate payments revenue (13.5% decrease) due to

seasonally higher 3Q13 government-related transaction volume

•

Higher commercial products revenue (17.4% increase) due to

higher syndication fees on tax-advantaged projects and

increases in commercial leasing and capital markets revenue

•

Higher credit and debit card revenue (7.8% increase) due to

seasonally higher sales volumes; higher trust and investment

management fees (6.1% increase) due to improved market

conditions and business expansion

•

Higher other income, mainly due to higher equity investment

and retail lease revenue

Year-Over-Year Growth

(4.2%)

(3.3%)

(3.4%)

(9.1%)

(7.4%)

$2,329

$2,165

$2,276

$2,177

$2,156

Trust and

Inv Mgmt

Service

Charges

All Other

Mortgage

Payments

All Other

Mortgage

Service Charges

Trust and Inv Mgmt

Payments

6.2%

(51.5%)

0.8%

7.6%

2.8%

0

700

1,400

2,100

2,800

4Q12

1Q13

2Q13

3Q13

4Q13 |

Noninterest Expense

Noninterest Expense

Key Points

$ in millions

vs. 4Q12

Noninterest expense was lower by $4 million, or

0.1%, driven by:

•

Lower professional services expense (28.9% decline) due to a

reduction in mortgage servicing review-related costs

•

Lower other expense, mainly due to a mortgage foreclosure-

related settlement accrual in 4Q12 and lower loan-related

expenses, including costs for other real estate owned, offset by

higher tax-advantaged project costs, including accounting

presentation changes in the current quarter

•

Higher employee benefits expense (19.0% increase), mainly due

to higher pension costs

•

Higher compensation expense (1.8% increase) due to growth in

staffing for business initiatives and the impact of merit increases,

partially offset by lower incentive and commission expense

vs. 3Q13

Noninterest expense was higher by $117 million, or

4.6%, driven by:

•

Higher professional services expense (25.5% increase) due to

seasonally higher costs; higher marketing and business

development expense (21.2% increase) due to timing of

marketing and business development projects

•

Higher compensation expense (1.4% increase) due to staffing

increases for business initiatives

•

Higher other expense, mainly due to higher costs related to

investments in tax-advantaged projects, reflecting higher volume

and the accounting presentation changes

Year-Over-Year Growth

(0.4%)

(3.5%)

(1.7%)

(1.7%)

(0.1%)

$2,686

$2,470

$2,557

$2,565

$2,682

Occupancy

and Equipment

Prof Services,

Marketing

and PPS

All Other

Tech and Comm

Compensation

and Benefits

All Other

Tech and Communications

Prof Svcs, Marketing and PPS

Occupancy and Equipment

Compensation and Benefits

4Q12

1Q13

2Q13

3Q13

4Q13

Mortgage servicing matters

80

$

-

$

-

$

-

$

-

$

Total

80

$

-

$

-

$

-

$

-

$

Notable Noninterest Expense Items

19

4Q13 Earnings

Conference Call

4.9%

2.6%

(13.3%)

(2.3%)

(4.0%)

3,200

2,400

1,600

800

0

4Q12

1Q13

2Q13

3Q13

4Q13 |

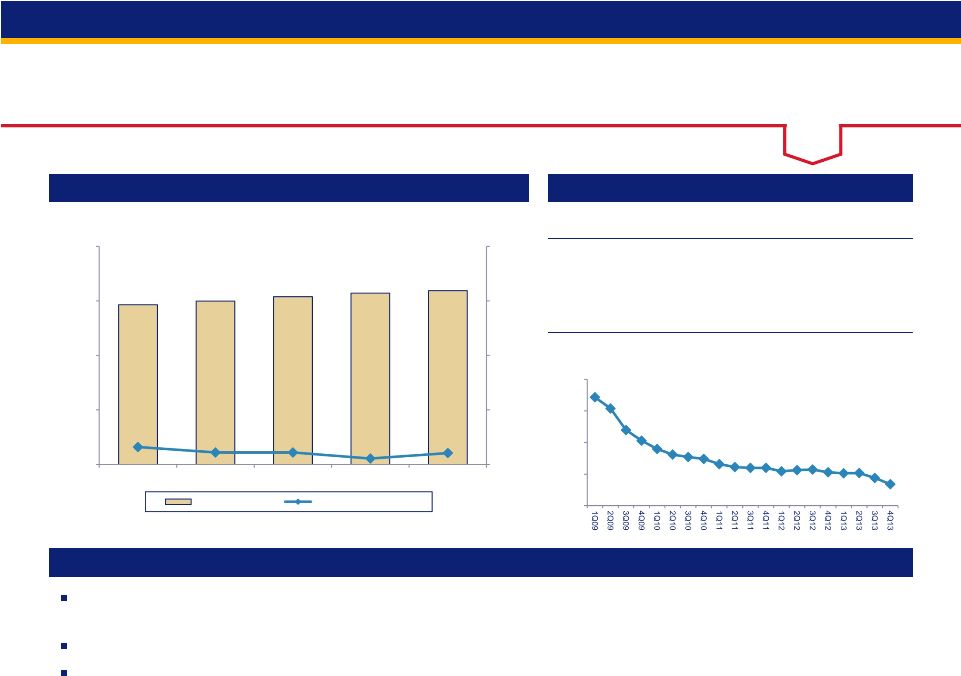

Credit Quality

-

Commercial Loans

Average Loans and Net Charge-offs Ratios

Key Statistics

Comments

Strong

lending

activity

with

1.4%

linked

quarter

loan

growth

and

8.8%

year-over-year

growth;

utilization rates continued at historically low levels

Net charge-offs continued to be modest; prior quarter included a few large

recoveries Nonperforming loans and delinquencies remained at low levels

4Q12

3Q13

4Q13

Average Loans

$58,552

$62,856

$63,714

30-89 Delinquencies

0.48%

0.28%

0.33%

90+ Delinquencies

0.10%

0.08%

0.08%

Nonperforming Loans

0.18%

0.16%

0.19%

$ in millions

20

4Q13 Earnings

Conference Call

80,000

60,000

40,000

20,000

0

4.0%

3.0%

2.0%

1.0%

0.0%

$58,552

$59,921

$61,507

$62,856

$63,714

0.32%

0.22%

0.22%

0.11%

0.21%

Average Loans

Net Charge-offs Ratio

40%

35%

30%

25%

20%

Revolving Line Utilization Trend

4Q12

1Q13

2Q13

3Q13

4Q13 |

21

4Q13 Earnings

Conference Call

Credit Quality

-

Commercial Leases

Average Loans and Net Charge-offs Ratios

Key Statistics

Comments

Net charge-offs remained at low levels and were essentially flat when adjusted

for a large recovery in 3Q13

Nonperforming loans and delinquencies continued at modest levels

4Q12

3Q13

4Q13

Average Loans

$5,377

$5,208

$5,210

30-89 Delinquencies

0.89%

0.76%

0.85%

90+ Delinquencies

0.00%

0.00%

0.00%

Nonperforming Loans

0.29%

0.23%

0.23%

$ in millions

Commercial Leases

Equipment

Finance

$2,089

Small Ticket

$3,121

9,000

6,000

3,000

0

$5,377

$5,378

$5,255

$5,208

$5,210

0.37%

0.23%

0.31%

0.23%

-0.53%

3.0%

2.0%

1.0%

0.0%

-1.0%

4Q12

1Q13

2Q13

3Q13

4Q13

Average Loans

Net Charge-offs Ratio |

22

4Q13 Earnings

Conference Call

Credit Quality

-

Commercial Real Estate

Average Loans and Net Charge-offs Ratios

Key Statistics

Comments

Average loans increased 2.1% on a linked quarter basis and 6.7%

year-over-year Net recovery ratio of 0.29%, marking the third

consecutive quarter of net recoveries Nonperforming loans of 0.76%,

continuing its downward trend 4Q12

3Q13

4Q13

Average Loans

$36,851

$38,501

$39,318

30-89 Delinquencies

0.43%

0.16%

0.24%

90+ Delinquencies

0.02%

0.02%

0.07%

Nonperforming Loans

1.48%

0.92%

0.76%

Performing TDRs*

$531

$365

$390

$ in millions

Investor

$20,698

Owner

Occupied

$11,082

Multi-family

$2,459

Retail

$532

Residential

Construction

$1,691

A&D

Construction

$553

Office

$719

Other

$1,584

* TDR = troubled debt restructuring

$36,851

$37,218

$37,884

$38,501

$39,318

0.18%

0.21%

-0.18%

-0.06%

-0.29%

-0.5%

0.0%

0.5%

1.0%

1.5%

0

20,000

40,000

60,000

4Q12

1Q13

2Q13

3Q13

4Q13

Average Loans

Net Charge-offs Ratio

CRE Mortgage

CRE Construction |

23

4Q13 Earnings

Conference Call

Credit Quality

-

Residential Mortgage

Average Loans and Net Charge-offs Ratios

Key Statistics

Comments

Strong growth in high quality originations (weighted average FICO 756, weighted

average LTV 70%), as average loans increased 3.2% over 3Q13

Over 77% of the balances have been originated since the beginning of 2009, the

origination quality metrics and performance to date have significantly

outperformed prior vintages with similar seasoning Net charge-offs

continued to decline as housing values improved 4Q12

3Q13

4Q13

Average Loans

$43,156

$49,139

$50,732

30-89 Delinquencies

0.79%

0.70%

0.70%

90+ Delinquencies

0.64%

0.53%

0.65%

Nonperforming Loans

1.50%

1.46%

1.51%

$ in millions

** Excludes GNMA loans, whose repayments are insured by the FHA or guaranteed by

the Department of VA ($2,607 million 4Q13) $43,156

$45,109

$46,873

$49,139

$50,732

0.88%

0.83%

0.63%

0.46%

0.38%

0.0%

1.0%

2.0%

3.0%

4.0%

0

15,000

30,000

45,000

60,000

4Q12

1Q13

2Q13

3Q13

4Q13

Average Loans

Net Charge-offs Ratio

$2,087

$2,035

$2,084

$2,030

$1,997

0

1,000

2,000

3,000

4,000

4Q12

1Q13

2Q13

3Q13

4Q13

Residential Mortgage Performing TDRs** |

24

4Q13 Earnings

Conference Call

4Q12

3Q13

4Q13

Average Loans

$16,588

$16,931

$17,366

30-89 Delinquencies

1.33%

1.25%

1.25%

90+ Delinquencies

1.27%

1.11%

1.17%

Nonperforming Loans

0.85%

0.55%

0.43%

Credit Quality -

Credit Card

Average Loans and Net Charge-offs Ratios

Key Statistics

Comments

Average loans increased 2.6% on a linked quarter basis

Net charge-offs ratio at lowest level since 4Q07 and delinquencies remain near

historically low levels Nonperforming loans have decreased for several

consecutive quarters $ in millions

$146

$127

$109

$94

$78

0.85%

0.78%

0.65%

0.55%

0.43%

0.0%

0.6%

1.2%

1.8%

2.4%

0

60

120

180

240

4Q12

1Q13

2Q13

3Q13

4Q13

Credit Card Nonperforming Loans

$16,588

$16,528

$16,416

$16,931

$17,366

3.86%

3.93%

4.23%

3.75%

3.72%

0.0%

2.5%

5.0%

7.5%

10.0%

0

5,000

10,000

15,000

20,000

4Q12

1Q13

2Q13

3Q13

4Q13

Average Loans

Net Charge-offs Ratio |

25

4Q13 Earnings

Conference Call

Credit Quality -

Home Equity

Average Loans and Net Charge-offs Ratios

Key Statistics

Comments

High-quality originations (weighted average FICO on commitments was 765,

weighted average CLTV

68%)

originated

primarily

through

the

retail

branch

network

to

existing

bank

customers

on

their primary residence

Net charge-off ratio declined on a linked quarter basis

4Q12

3Q13

4Q13

Average Loans

$16,950

$15,648

$15,488

30-89 Delinquencies

0.76%

0.65%

0.66%

90+ Delinquencies

0.30%

0.25%

0.32%

Nonperforming Loans

1.13%

1.15%

1.08%

Subprime: 2%

Wtd Avg LTV**: 91%

NCO: 3.98%

$ in millions

Prime: 95%

Wtd Avg LTV**: 72%

NCO: 0.89%

** LTV at origination

Other: 3%

Wtd Avg LTV**: 72%

NCO: 0.83%

24,000

18,000

12,000

6,000

0

4Q12

1Q13

2Q13

3Q13

4Q13

Average Loans

Net Charge-offs Ratio

$16,950

$16,434

$15,989

$15,648

$15,488

1.76%

1.80%

1.45%

0.95%

1.09%

6.0%

4.5%

3.0%

1.5%

0.0%

Home Equity |

26

4Q13 Earnings

Conference Call

Credit Quality -

Retail Leasing

Average Loans and Net Charge-offs Ratios

Key Statistics

Comments

Strong year-over-year growth (8.6%), driven by high-quality

originations (weighted average FICO 771) Delinquencies remained relatively

stable at very low levels Strong used auto values continued to contribute to

historically low net charge-offs 4Q12

3Q13

4Q13

Average Loans

$5,384

$5,664

$5,847

30-89 Delinquencies

0.22%

0.15%

0.18%

90+ Delinquencies

0.02%

0.02%

0.00%

Nonperforming Loans

0.02%

0.02%

0.02%

$ in millions

9,000

6,000

3,000

0

1.5%

1.0%

0.5%

0.0%

-0.5%

Average Loans

Net Charge-offs Ratio

$5,384

$5,448

$5,653

$5,664

$5,847

0.07%

0.07%

0.07%

0.00%

-0.07%

4Q12

1Q13

2Q13

3Q13

4Q13

Manheim Used Vehicle Index*

*

Manheim Used Vehicle Value Index source: www.manheimconsulting.com, January 1995 = 100, quarter value

= average monthly ending value |

Credit Quality -

Other Retail

Average Loans and Net Charge-offs Ratios

Key Statistics

Comments

Growth in auto loans continued to offset declines in student lending loan balances

(see slide 28 for auto loan detail)

Delinquencies

and

nonperforming

loans

remained

relatively

stable

and

at

very

low

levels

4Q12

3Q13

4Q13

Average Loans

$25,595

$25,682

$26,059

30-89 Delinquencies

0.59%

0.48%

0.50%

90+ Delinquencies

0.17%

0.14%

0.14%

Nonperforming Loans

0.11%

0.10%

0.09%

Installment

$5,738

Auto Loans

$13,409

Revolving

Credit

$3,283

Student

Lending

$3,629

$ in millions

27

4Q13 Earnings

Conference Call

40,000

30,000

20,000

10,000

0

4Q12

1Q13

2Q13

3Q13

4Q13

Average Loans

Net Charge-offs Ratio

$25,595

$25,364

$25,224

$25,682

$26,059

0.92%

0.83%

0.76%

0.83%

0.79%

Other Retail

4.0%

3.0%

2.0%

1.0%

0.0% |

28

4Q13 Earnings

Conference Call

Credit Quality -

Auto Loans

Average Loans and Net Charge-offs Ratios

Key Statistics

Comments

Continued growth in auto loans driven by high-quality originations in the

Indirect Channel (weighted average FICO 753)

Low net charge-offs and delinquencies continued as used vehicle values remain

strong 4Q12

3Q13

4Q13

Average Loans

$12,540

$12,946

$13,409

30-89 Delinquencies

0.41%

0.30%

0.34%

90+ Delinquencies

0.06%

0.03%

0.04%

Nonperforming Loans

0.02%

0.02%

0.02%

$ in millions

Auto Loans are included in Other Retail category

Direct: 8%

Wtd Avg FICO: 748

NCO: 0.10%

Indirect: 92%

Wtd Avg FICO: 766

NCO: 0.12%

$12,540

$12,519

$12,575

$12,946

$13,409

0.22%

0.16%

0.00%

0.09%

0.12%

0.0%

0.2%

0.4%

0.6%

0.8%

0

4,000

8,000

12,000

16,000

4Q12

1Q13

2Q13

3Q13

4Q13

Average Loans

Net Charge-offs Ratio

Indirect and Direct Channel |

Non-GAAP Financial Measures

$ in millions

4Q13

3Q13

2Q13

1Q13

4Q12

Total equity

41,807

$

41,552

$

41,050

$

40,847

$

40,267

$

Preferred stock

(4,756)

(4,756)

(4,756)

(4,769)

(4,769)

Noncontrolling interests

(694)

(1,420)

(1,367)

(1,316)

(1,269)

Goodwill (net of deferred tax liability)

(8,343)

(8,319)

(8,317)

(8,333)

(8,351)

Intangible assets, other than mortgage servicing rights

(849)

(878)

(910)

(963)

(1,006)

Tangible common equity (a)

27,165

26,179

25,700

25,466

24,872

Tier 1 capital, determined in accordance with prescribed

regulatory requirements using Basel I definition

33,386

32,707

32,219

31,774

31,203

Preferred stock

(4,756)

(4,756)

(4,756)

(4,769)

(4,769)

Noncontrolling interests, less preferred stock not eligible for Tier 1

capital (688)

(686)

(685)

(684)

(685)

Tier 1 common equity using Basel I definition (b)

27,942

27,265

26,778

26,321

25,749

Tangible common equity (as calculated above)

27,165

26,179

25,700

Adjustments

1

224

258

195

Common equity tier 1 estimated using final rules for the Basel III

standardized approach (c)

27,389

26,437

25,895

Tangible common equity (as calculated above)

25,700

25,466

24,872

Adjustments

2

(43)

81

126

Common equity tier 1 approximated using proposed rules for the

Basel III standardized approach released June 2012 (d)

25,657

25,547

24,998

1

Includes

net

losses

on

cash

flow

hedges

included

in

accumulated

other

comprehensive

income

and

unrealized

losses

on

securities

transferred

from

available-for-sale

to held-to-maturity included in accumulated other comprehensive income

2

Includes net losses on cash flow hedges included in accumulated other comprehensive income,

unrealized losses on securities transferred from available-for-sale to

held-to-maturity included in accumulated other comprehensive income and disallowed mortgage servicing rights

29

4Q13 Earnings

Conference Call |

30

4Q13 Earnings

Conference Call

Non-GAAP Financial Measures

$ in millions

4Q13

3Q13

2Q13

1Q13

4Q12

Total assets

364,021

$

360,681

$

353,415

$

355,447

$

353,855

$

Goodwill (net of deferred tax liability)

(8,343)

(8,319)

(8,317)

(8,333)

(8,351)

Intangible assets, other than mortgage servicing rights

(849)

(878)

(910)

(963)

(1,006)

Tangible assets (e)

354,829

351,484

344,188

346,151

344,498

Risk-weighted assets, determined in accordance with prescribed

regulatory requirements using Basel I definition (f)

297,919

293,155

289,613

Adjustments

13,712

13,473

12,476

Risk-weighted assets estimated using final rules for the Basel III

standardized approach (g)

311,631

306,628

302,089

Risk-weighted assets, determined in accordance with prescribed

regulatory requirements using Basel I definition (f)

289,613

289,672

287,611

Adjustments

4

20,866

21,021

21,233

Risk-weighted assets approximated using proposed rules for the

Basel III standardized approach released June 2012 (h)

310,479

310,693

308,844

Ratios

Tangible common equity to tangible assets (a)/(e)

7.7%

7.4%

7.5%

7.4%

7.2%

Tangible common equity to risk-weighted assets using Basel I definition

(a)/(f) 9.1%

8.9%

8.9%

8.8%

8.6%

Tier 1 common equity to risk-weighted assets using Basel I definition

(b)/(f) 9.4%

9.3%

9.2%

9.1%

9.0%

Common equity tier 1 to risk-weighted assets estimated using final rules

for the Basel III standardized approach (c)/(g)

8.8%

8.6%

8.6%

-

-

Common equity tier 1 to risk-weighted assets approximated using proposed

rules

for

the

Basel

III

standardized

approach

released

June

2012

(d)/(h)

-

-

8.3%

8.2%

8.1%

3

Includes higher risk-weighting for unfunded loan commitments, investment

securities and mortgage servicing rights, and other adjustments 4

Includes higher risk-weighting for residential mortgages, unfunded loan

commitments, investment securities and mortgage servicing rights, and other adjustments

3 |

January 22, 2014

U.S. Bancorp

4Q13 Earnings

Conference Call

U.S. Bancorp

4Q13 Earnings

Conference Call |