Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - VERINT SYSTEMS INC | d655350d8k.htm |

Verint Systems Inc.

Making

Big

Data

Actionable

TM

Presentation to Lenders

January 2014

THE

COMPANY

ACKNOWLEDGES

THAT

THE

RECIPIENT

OF

THIS

PRESENTATION

HAS

STATED

THAT

IT

DOES

NOT

WISH

TO

RECEIVE

MATERIAL NON-PUBLIC INFORMATION WITH RESPECT TO THE COMPANY OR ITS SECURITIES.

NEITHER THE COMPANY NOR THE ARRANGERS TAKE ANY RESPONSIBILITY FOR THE

RECIPIENT'S DECISION TO LIMIT THE SCOPE OF THE INFORMATION IT HAS OBTAINED IN

CONNECTION WITH ITS EVALUATION OF THE COMPANY AND THE FACILITIES.

Exhibit 99.1 |

1

Forward-Looking Statements

This document contains forward-looking statements, including statements

regarding expectations, predictions, views, opportunities, plans,

strategies, beliefs, and statements

of

similar

effect

relating

to

Verint

and

the

expected

benefits

of

the

KANA

acquisition. Forward-looking statements are often identified by future or

conditional words such as "will", "would", "plans",

"expects", "intends", "believes", "seeks",

"estimates", or "anticipates", or by variations of such words

or by similar

expressions. These forward-looking statements are not guarantees of future

performance and they are based on management’s expectations that

involve a number of risks, uncertainties, and assumptions, any of which

could cause actual results or events to differ materially from those

expressed in or implied by the forward-looking statements, including

risks associated with the KANA acquisition, such as uncertainties regarding

the closing of the KANA acquisition or the ability to realize the expected

benefits of the transaction, as well as risks associated with related system

integrations. For a detailed discussion of risk factors impacting Verint,

see Verint’s Annual Report on Form 10-K for the year ended January 31,

2013, its Quarterly Report on Form 10-Q for the quarter ended October 31, 2013,

and other filings Verint makes with the SEC. The forward-looking

statements contained in this document are made as of the date of this

document, and Verint assumes no obligation to revise or update any

forward-looking statement, except as otherwise required by law.

|

2

Management Presenters

Dan Bodner

President and Chief Executive Officer

Doug Robinson

Chief Financial Officer

Alan Roden

SVP, Corporate Development |

3

Table of Contents

Credit Suisse

Dan Bodner

Doug Robinson

Alan Roden

Credit Suisse

5.

Syndication Overview and Timing

4.

Key Credit Highlights

3.

Financial Overview

2.

Verint Overview

1.

Transaction Overview |

1.

Transaction Overview |

5

Transaction Overview

On

January

6,

2014,

Verint

Systems

Inc.

(“Verint”

or

the

“Company”)

signed

a

definitive

purchase

agreement

to

acquire

KANA Software (“KANA”

or the “Target”) from Accel-KKR for $514 million in cash (the

“Transaction”) KANA is a leader in customer service solutions

delivered both on-premises and in the cloud with ~900 customers The

Transaction is expected to be financed with: ~$100 million Verint cash from

balance sheet $300 million incremental term loan on the Company’s

existing senior secured term loan facility ~$126 million revolver draw

Pro forma LTM non-GAAP revenue of $1,020 million and non-GAAP EBITDA of

$258 million Pro forma LTM gross and net leverage of 4.2x and 3.1x,

respectively Verint expects to delever through a combination of EBITDA

growth, free cash flow generation and debt paydown Verint has a track record

of successfully delevering, having reduced net leverage from 5.7x to 2.0x within two years

after acquiring Witness in FY’08

The

Company

is

also

seeking

an

amendment

to

increase

its

incremental

debt

capacity

as

well

as

amend

the

conditionality

requirements

for

future

incremental

borrowings

in

connection

with

permitted

acquisitions

Existing

lenders

should

submit

signature

pages

for

the

amendment

to

LendAmend.

Instructions

will

be

posted

to

SyndTrak

Note:

LTM based on 10/31/13 results for Verint and the midpoint of 12/31/13E estimates for

KANA. KANA has not closed its financials for 12/31/13. Preliminary estimates

for LTM 12/31/13E are non-GAAP revenue of $135–$139 million and non-GAAP EBITDA of $35–$37 million. |

6

Sources & Uses and Pro Forma Capitalization

($ in millions)

Sources

Uses

Revolver Draw

$126

24.0%

Purchase Price

$514

Incremental Senior Secured Term Loan

300

57.0%

Estimated Transaction Expenses

12

Verint Cash from Balance Sheet

100

19.0%

Total Sources

$526

100.0%

Total Uses

$526

Note:

Based on current expectations regarding financing structure.

(1)

KANA non-GAAP EBITDA reflects the midpoint of estimated LTM 12/31/13E results of

$35–$37 million. Sources & Uses

Pro Forma Capitalization

($ in millions)

Existing

Pro Forma

10/31/2013

Adjustment

10/31/2013

Unrestricted Cash and Short-Term Investments

$376

($100)

$276

$200mm Revolving Credit Facility

–

126

126

Senior Secured Term Loan

645

300

945

Total Debt

$645

$426

$1,071

Financial summary:

$222

$36

$258

Credit statistics:

Total Debt / LTM 10/31/13 Non-GAAP EBITDA

2.9x

4.2x

Net Debt / LTM 10/31/13 Non-GAAP EBITDA

1.2x

3.1x

LTM

10/31/13

Non-GAAP

EBITDA

(1) |

2.

Verint Overview |

8

The Big Data Analytics Opportunity

Intelligent organizations are differentiating themselves and driving

competitive advantage through big data analytics |

9

Helping Customers Collect Big Data -

Examples

Enterprise Case Study

Enterprise Case Study

More than 50 million customer telephony

interactions per year

More than 300 million customer text

related interactions per year -

emails,

surveys and unstructured text

Security Case Study

Security Case Study

Tens of millions of communications per

day -

phone, email, chat, SMS, web

session, social media, etc.

Requires multiple Petabytes of storage

Objective: Extract intelligence from customer

interactions for customer-centric operations

Objective: Extract intelligence from

communications to fight crime and terrorism |

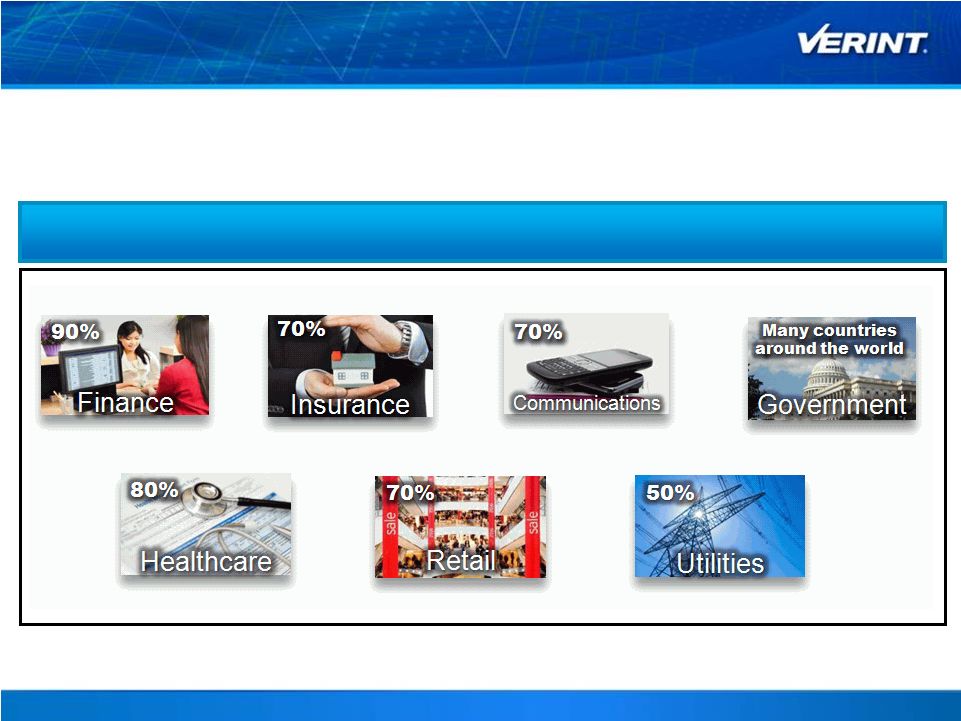

10

Large and Diversified Customer Base

Note:

%

represents

percentage

of

Global

Fortune

500

companies

that

are

Verint

customers.

Calculations based on 2012 data.

Large base of more than 10,000 customers provides Verint the opportunity to

deliver analytical applications across multiple markets

Strong Presence Across Global Fortune 500 Companies |

11

Enterprise Intelligence

Discover

Business

Trends

Optimize

the

Workforce

Our solutions enable customer service operations to enhance the customer

experience while increasing revenue and improving profitability

We are expanding from our strong position in the contact center into branch,

back-office and customer experience functions

Understand

Customer

Sentiment |

12

Security Intelligence

Optimize Public

Safety Call Centers

Improve Physical

Security Cost

Effectively

Generate

Intelligence

and Collect Evidence

Our

solutions

enable

security

organizations

to

leverage

big

data

from

a

Migration to IP networks creates new challenges and new opportunities

for law enforcement and security organizations

wide range of communications, video and data sources to enhance

security and prevent crime and terrorism |

13

Go-to-Market Strategy

Growing sales force and channel partners

Verticalized direct sales force with subject matter expertise

~800 professionals in sales and marketing

Partner strategy broadens market coverage

~50% of business through channel partners: OEMs, SIs and regional resellers

Flexible business models

Perpetual, software-as-a-service, managed services

Business models reflect customer preferences

Enterprise, typical software model

Security, prefer turnkey solutions |

14

Creating a New Leader for

Customer Engagement

To Empower Organizations to

Optimize and Transform Customer Engagements

Combination Helps Organizations Enhance Loyalty,

Mitigate Risk and Better Manage Operational Costs

The complementary solution set would enable

organizations worldwide to implement a single-vendor

solution

that helps optimize and align customer

engagement strategy |

15

Complementary Solutions

Case Management

NLP Knowledge Management

Agent Desktop

Web Self-Service & Secure Portal

Business Process Management

Inbound Routing and Queuing

Live Chat and Co-Browsing

Text Analytics

Email & Whitemail Management

Mobile and Social

WFO and WFM

Performance Management

Desktop and Process Analytics

Enterprise Feedback Management

Customer Feedback Management

Quality Monitoring

Recording

Speech Analytics

eLearning and Coaching

Video and Situation Intelligence |

3.

Financial Overview |

$139

$213

$200

$192

$205

$220–$223

21%

30%

28%

24%

24%

~24%

FY'09

FY'10

FY'11

FY'12

FY'13

FY'14E

Non-GAAP EBITDA

% Margin

17

Track Record of Strong Financial Performance

Outlook

Non-GAAP Revenue

Non-GAAP EBITDA and % Margin

FYE 1/31 ($ in millions)

FYE 1/31 ($ in millions)

$675

$704

$727

$796

$848

$903–$911

FY'09

FY'10

FY'11

FY'12

FY'13

FY'14E

Note:

Guidance relates to non-GAAP revenue, EPS and EBITDA.

FYE 2014

FYE 2015

FYE 2014

FYE 2015

Guidance

from

Q3

Conference

Call

Revenue Growth: 6.5% to 7.5% from the prior year

Diluted EPS: $2.75 to $2.80

Revenue to increase between 7.0% and 9.0% compared

to the year ending January 31, 2014

Update

from

1/6/14

Conference

Call

Verint reaffirmed prior guidance

Verint guidance expected to be updated after KANA

transaction closes

CY 2014E KANA Revenue: $140 to $150 million

CY 2014E KANA EBITDA: $40 to $45 million |

18

Pro Forma Financial Summary

LTM Non-GAAP EBITDA Contribution

LTM Non-GAAP Revenue Contribution

($ in millions)

($ in millions)

LTM Revenue by Segment Breakdown

Verint

KANA

Pro Forma

Note:

LTM financials based on 10/31/13 results for Verint and the midpoint of 12/31/13E

estimates for KANA. KANA has not closed its financials for 12/31/13.

Preliminary estimates for LTM 12/31/13E are non-GAAP revenue of $135–$139 million and non-GAAP EBITDA of $35–$37 million.

Enterprise

Intelligence

58%

Communications

Intelligence

29%

Video

Intelligence

13%

Enterprise

Intelligence

63%

Communications

Intelligence

25%

Video

Intelligence

12%

Enterprise

Intelligence

100%

$883

$137

$1,020

Verint

KANA

Pro Forma

$222

$36

$258

Verint

KANA

Pro Forma |

19

Track Record of De-levering and Ability to

Maintain Efficient Leverage Levels

($ in millions)

Net Debt

(1)

Key Highlights

Net Debt

(1)

/ Non-GAAP EBITDA

Verint generates good free cash flow and has

demonstrated an ability to de-lever

The Company has a number of positive cash flow

characteristics

–

Operating margins greater than 20%

–

Capex of less than 2%–3% of revenue

–

Minimal working capital needs

–

Low effective tax rate due to NOLs

(2)

(1)

Total debt less unrestricted cash and short-term investments.

(2)

Cash and debt balance as of 10/31/13. Unadjusted for current transaction.

(3)

Capital

expenditures

includes

cash

paid

for

capitalized

software

development

costs.

(2)

Low Capex Needs

($ in millions)

(3)

$527

$509

$437

$413

$447

$353

$268

FY'08

FY'09

FY'10

FY'11

FY'12

FY'13

LTM

10/31/13

5.7x

3.6x

2.0x

2.1x

2.3x

1.7x

1.2x

FY'08

FY'09

FY'10

FY'11

FY'12

FY'13

LTM

10/31/13

$16

$8

$11

$16

$20

$19

2%

1%

2%

2%

2%

2%

FY'09

FY'10

FY'11

FY'12

FY'13

LTM

10/31/13

Capex

% of Revenue |

4.

Key Credit Highlights |

21

Verint Key Credit Highlights

Highly Diversified Business

3

Significant Free Cash Flow Generation to Support Deleveraging

4

Experienced Management Team

5

Compelling Combination

2

Strong Financial Performance Underpinned by Attractive Industry Fundamentals

1 |

22

Strong Financial Performance Underpinned by

Attractive Industry Fundamentals

1

Enterprise Intelligence Growth Drivers

Integration of WFO applications

Greater insight through customer interaction analytics

to improve the performance of customer service

operations

Adoption of WFO across the enterprise

Migration to VoIP technologies

$139

$213

$200

$192

$205

$220–$223

21%

30%

28%

24%

24%

~24%

FY'09

FY'10

FY'11

FY'12

FY'13

FY'14E

Non-GAAP EBITDA

% Margin

Non-GAAP Revenue

Non-GAAP EBITDA and % Margin

($ in millions)

($ in millions)

$675

$704

$727

$796

$848

$903–$911

FY'09

FY'10

FY'11

FY'12

FY'13

FY'14E

Security Intelligence Growth Drivers

Growing demand for advanced intelligence and

investigative solutions

Terrorism, crime and other security threats around the

world are generating demand for advanced video

security solutions

Increasingly complex communications networks and

growing network traffic

Transition to IP networks and web and cyber security

Legal and regulatory compliance requirements |

23

Compelling Combination

Favorable Industry Reaction to the Transaction….

…And Industry Experts

…From Wall Street Analysts…

“

Kana enhances VRNT's SaaS capabilities and call center

technologies and deepens its reach into customer experience and

workforce optimization solutions.

”

“

We believe this acquisition is a significant enhancement for

Verint, as it augments the company's existing solution suite to include

significant online/e-business capabilities, such as response

management for e-mail, chat, and social media, as well as KANA's

agent desktop solution.

”

“

We like the transaction as it could accelerate the adoption of

customer engagement suites through the deployment of a solution set

from a single vendor and increase the company's importance as a

strategic

supplier.

KANA

Software

should

add

~800

employees

(200

in

R&D) and ~900 customers to Verint. We believe the move could be an

important part in helping the overall growth rate accelerate into the

double-digits.

”

“

We like this acquisition as it is expected to be accretive to FY

2015 earnings (FYE January) and see it expanding the Company’s

service

suite

in

its

fastest

growing

area

–

actionable

intelligence.

”

“

Big data and analytics meet customer experience. Verint expects

to expand its customer engagement optimization offering with the

acquisition of Kana. Verint's core capabilites, Vovici's voice of the

customer assets, and Kana's multichannel customer experience

solutions allow customers to move from data to information to insight to

action or decisions.

”

“

The acquisition provides greater gains than just complementary

product lines, and a venue for both companies to expand their current

footprints by cross-and upselling into their respective installed base.

The acquisition provides a vision for deeply personalized customer

service

interactions

which

are

delivered

with

maximum

efficiency

for

a

contact center.

”

“

By offering a ‘best of breed’

customer support suite, with pre-

integrated EFM capabilities, Verint should not only be able to sell the

entire stack, and have infinite upsell opportunities with existing

customers, but they also can better partner with companies to create a

vision for EFM, and then enable the entire vision from phone calls to

final analysis.

”

“

Kana enhances VRNT's SaaS capabilities and call center

technologies and deepens its reach into customer experience and

workforce optimization solutions.

” |

24

24

LTM Pro Forma Revenue by Segment

LTM Pro Forma Revenue by Type

(1)

More than 10,000 Customers in Over 150 Countries

Finance and Insurance

Communications

Government

Enterprise

Retail & Hospitality

Health Care

Utilities

Transportation

Note:

LTM pro forma revenue based on 10/31/13 results for Verint and the midpoint of

12/31/13E estimates for KANA. KANA has not closed its financials for 12/31/13.

Preliminary estimate for LTM 12/31/13E non-GAAP revenue of $135–$139 million.

(1)

KANA revenue by type estimates based on historical results; Product revenue includes

KANA License revenue; Service and Support revenue includes all other KANA revenue.

LTM Pro Forma Revenue by Region

Highly Diversified Business

3

Product Revenue

41%

Service and

Support

Revenue

59%

Americas

54%

EMEA

24%

APAC

22%

Enterprise

Intelligence

63%

Communications

Intelligence

25%

Video

Intelligence

12% |

25

Significant Free Cash Flow Generation to

Support Deleveraging

Net Debt

(1)

Net Debt

(1)

/ Non-GAAP EBITDA

Capital Structure Highlights

Favorable debt structure

No maturities until 2018

Efficient capital structure with ability to prepay all debt without

incurring prepayment penalties

Significant free cash flow generation to support deleveraging

The Company has a number of positive cash flow characteristics

–

Operating margins greater than 20%

–

Capex of less than 2%–3% of revenue

–

Minimal working capital needs

–

Low effective tax rate due to NOLs

Proven ability to delever following an acquisition

–

Acquired Witness in FY’08 and reduced net leverage to 2.0x

by the end of FY’10

Strong liquidity

10/31/13 pro forma unrestricted cash and short-term investments

balance of $276 million

Pro forma revolver availability of ~$75 million

(1)

Total debt less unrestricted cash and short-term investments.

(2)

Calculated as CFO less capex and cash paid for capitalized software development

costs. $527

$509

$437

$413

$447

$353

$268

FY'08

FY'09

FY'10

FY'11

FY'12

FY'13

LTM

10/31/13

5.7x

3.6x

2.0x

2.1x

2.3x

1.7x

1.2x

FY'08

FY'09

FY'10

FY'11

FY'12

FY'13

LTM

10/31/13

4

Free Cash Flow

(2)

NM

$38

$93

$59

$90

$103

$154

FY'08

FY'09

FY'10

FY'11

FY'12

FY'13

LTM

10/31/13

($ in millions)

($ in millions) |

26

Experienced Management Team

Years at Verint

Multi-

disciplinary

expertise

Significant

industry

background

Significant

M&A execution

and integration

track record

Strong

public

company

experience

Long

tenure

Professional

Experience

Dan Bodner

Chief Executive Officer and President

19

33

Doug Robinson

Chief Financial Officer

7

30

Elan Moriah

President of Verint Enterprise Intelligence Solutions and

Verint Video Intelligence Solutions

13

24

Hanan Gino

President, Communications and Cyber Intelligence

1

27

Meir Sperling

Chief Strategy Officer

13

38

Peter Fante

Chief Legal Officer and Chief Compliance Officer

11

20

Alan Roden

SVP, Corporate Development

11

20

Jane O’Donnell

SVP, Global Human Resources

12

33

5 |

5.

Syndication Overview and Timing |

28

Indicative Terms

Incremental Senior Secured Term Loan

(1)

Credit

agreement

terms

include

a

cap

on

cash

netting

of

$150mm.

Accordingly,

pro

forma

for

this

transaction,

the

1

lien

net

leverage

ratio

is

approximately

3.6x.

Borrower:

Verint Systems Inc.

Joint Lead Arrangers:

Credit Suisse Securities (USA) LLC, Deutsche Bank Securities Inc., RBC

Capital Markets, Barclays, HSBC Securities (USA) Inc.

Issue:

Maturity:

September 6, 2019 (same as existing TL-B)

LIBOR margin:

L + 300 bps (-25 bps step-down at BB-

/ Ba3)

LIBOR floor:

1.00%

Issue price:

99.75

Guarantors:

Same as existing, but will include all of KANA Software’s domestic

subsidiaries Amortization

:

1.00% per annum (adjusted to be fungible with existing term loans); payable

quarterly, with balance due at maturity

Incremental facility

:

Call protection:

Security:

Same as under existing facilities, with inclusion of assets of U.S.

subsidiaries of Kay Technology Holdings, Inc., including KANA Software, as

new guarantors Mandatory

prepayments:

Same as existing TL-B

Financial

covenants:

None

$200mm

plus

an

unlimited

amount

subject

to

3.5x

1st

lien

net

leverage

(1)

101 repricing protection through 3/6/2014 (same as existing TL-B)

st

$300

million

Incremental

Senior

Secured

Term

Loan

(fungible

with

existing

TL-B) |

29

Timetable

January 13

Lender conference call

January 17

Commitments due from lenders

February 3

Close and fund

S

M

T

W

T

F

S

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

January 2014

Holiday

Key date

Date

S

M

T

W

T

F

S

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

February 2014

Event

(1)

(1) Closing is subject to the expiration of applicable regulatory waiting periods

and the satisfaction or waiver of the other closing conditions. |

30

Transaction Contacts

Verint

Alan Roden

Senior Vice President, Corporate Development

(631) 962-9304

alan.roden@verint.com

Credit Suisse

Jeff Cohen

Managing Director,

Co-Head of US Syndicated Loan Capital Markets

(212) 325-7455

jeffrey.a.cohen@credit-suisse.com

Ryan Williams

Vice President,

Syndicated Loan Capital Markets

(212) 538-9568

ryan.williams@credit-suisse.com

Michael Speller

Managing Director,

Leveraged Finance Origination

(212) 538-8769

michael.speller@credit-suisse.com

Judy Smith

Managing Director,

Corporate Banking

(212) 538-2178

judy.smith@credit-suisse.com

Michael D’Onofrio

Associate,

Corporate Banking

(212) 325-6098

suisse.com

Raghu Velamati

Vice President,

Diversified Industrials and Services Investment Banking

(312) 750-3059

raghu.velamati@credit-suisse.com

Brett Kornblatt

Associate,

Diversified Industrials and Services Investment Banking

(312) 750-3043

brett.kornblatt@credit-suisse.com

Chris O’Keeffe

Analyst,

Diversified Industrials and Services Investment Banking

(312) 750-2921

christopher.okeeffe@credit-

suisse.com

michael.d’onofrio@credit-

Title

Phone

Email |

Appendix |

32

About Non-GAAP Financial Measures

The following tables include a reconciliation of certain financial measures

prepared in accordance with Generally Accepted Accounting Principles

(“GAAP”) to the most directly comparable financial measures not prepared

in accordance with GAAP (“non-GAAP”). Non-GAAP financial

measures should not be considered in isolation or as a substitute for comparable

GAAP financial measures. The non-GAAP financial measures we

present

in

the

following

tables

have

limitations

in

that

they

do

not

reflect

all

of

the

amounts

associated

with

our

results

of

operations

as

determined in accordance with GAAP, and these non-GAAP financial measures

should only be used to evaluate our results of operations in conjunction

with the corresponding GAAP financial measures. These non-GAAP financial measures do not represent discretionary cash available

to

us

to

invest

in

the

growth

of

our

business,

and

we

may

in

the

future

incur

expenses

similar

to

the

adjustments

made

in

these

non-GAAP

financial measures.

We believe that the non-GAAP financial measures we present in the following

tables provide meaningful supplemental information regarding our operating

results primarily because they exclude certain non-cash charges or items that we do not believe are reflective of our ongoing operating

results when budgeting, planning and forecasting, determining compensation and when

assessing the performance of our business with our individual operating

segments or our senior management. We believe that these non-GAAP financial measures also facilitate the comparison by

management and investors of results between periods and among our peer

companies. However, those companies may calculate similar non- GAAP

financial measures differently than we do, limiting their usefulness as comparative measures.

Our

non-GAAP

financial

measures

reflect

adjustments

to

the

corresponding

GAAP

financial

measure

based

on

the

items

set

forth

below.

The

purpose of these adjustments is to give an indication of our performance exclusive

of certain non-cash charges and other items that are considered

by

our

senior

management

to

be

outside

of

our

ongoing

operating

results.

The

non-GAAP

financial

measures

Verint

presents

have

limitations

in

that

they

do

not

reflect

all

of

the

amounts

associated

with

Verint’s

or

KANA’s results of operations as determined in accordance with GAAP, and these

non-GAAP financial measures should only be used to evaluate

Verint’s or KANA’s results of operations in conjunction with the

corresponding GAAP financial measures. These non-GAAP financial measures do

not represent discretionary cash available to Verint or KANA to invest in the

growth of its business, and Verint or KANA may in the future incur expenses

similar to or in addition to the adjustments made in these non-GAAP financial measures.

Because we do not predict special items that might occur in the future, and our

outlook is developed at a level of detail different than that used to

prepare GAAP financial measures, we are not providing a reconciliation to GAAP of

forward-looking financial measures for the fiscal years ending January

31, 2014 and January 31, 2015. Estimates for KANA’s non-GAAP

measures presented in this document were prepared in a manner similar to Verint’s non-GAAP measures.

KANA defines EBITDA as earnings (or loss) from continuing operations before

interest expense, income taxes, depreciation and amortization, and

amortization of non-cash stock-based compensation, non-recurring acquisition and restructuring expenses and the goodwill impairment

charges. |

33

About Non-GAAP Financial Measures |

34

Verint GAAP to Non-GAAP Reconciliation

($ in millions)

FY

FY

FY

FY

FY

FY

FY 2014

LTM

FYE 1/31

2008A

2009A

2010A

2011A

2012A

2013A

Q1A

Q2A

Q3A

10/31/2013

Revenue Reconciliation

GAAP revenue

$535

$670

$704

$727

$783

$840

$205

$222

$224

$881

Revenue Adjustments Related to Acquisitions

37

6

–

–

14

9

1

0

0

3

Non-GAAP revenue

$572

$675

$704

$727

$796

$848

$205

$223

$225

$883

EBIT Reconciliation

GAAP Operating Income

($115)

($15)

$66

$73

$86

$100

$14

$31

$38

$118

Revenue Adjustments Related to Acquisitions

37

6

–

–

14

9

1

0

0

3

Amortization and Impairment of Acquired Technology and Backlog

8

9

8

9

12

15

4

2

2

12

Amortization of Other Acquired Intangible Assets

20

25

22

21

23

24

6

6

6

24

Restructuring Costs

3

6

0

–

–

–

–

–

–

–

Stock-Based Compensation Expenses

31

36

44

47

28

25

6

9

10

32

M&A and Other Adjustments

–

–

1

5

12

17

6

2

0

17

Expenses Related to Restatement and Extended Filing Delay

41

29

55

29

1

–

–

–

–

–

Impairments of Goodwill and Other Acquired Intangible Assets

23

26

–

–

–

–

–

–

–

–

In-process Research and Development

7

–

–

–

–

–

–

–

–

–

Integration Costs

11

3

–

–

–

–

–

–

–

–

Other Legal Expenses (Recoveries)

9

(4)

–

–

–

–

–

–

–

–

Non-GAAP Operating Income

$75

$120

$196

$185

$177

$189

$37

$51

$56

$205

Non-GAAP Depreciation and Amortization

18

19

18

15

15

16

4

4

4

17

Non-GAAP EBITDA

$93

$139

$213

$200

$192

$205

$41

$55

$61

$222 |