Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - KEYCORP /NEW/ | d625225d8k.htm |

| KeyCorp

Bank of America Merrill Lynch 2013 Banking and

Financial Services Conference

Chris Gorman

President, Key Corporate Bank

Don Kimble

Chief Financial Officer

EXHIBIT 99.1 |

| FORWARD-LOOKING STATEMENTS AND ADDITIONAL

INFORMATION DISCLOSURE

This presentation contains forward-looking statements, including statements

about our financial condition, results of operations, asset quality trends,

capital

levels

and

profitability.

Forward-looking

statements

can

often

be

identified

by

words

such

as

“outlook,”

“goal,”

“objective,”

“plan,”

“expect,”

“anticipate,”

“intend,”

“project,”

“believe,”

or “estimate.”

Forward-looking statements represent management’s current expectations

and forecasts regarding future events. If underlying assumptions prove to be

inaccurate or unknown risks or uncertainties arise, actual results could vary

materially from these projections or expectations. Risks and uncertainties

include but are not limited to: (1) continued strain on the global financial markets; (2) the slow progress of the U.S. economic

recovery; changes in trade, monetary and fiscal policies; (3) our ability to

anticipate interest rate changes correctly and manage interest rate risk; (4)

changes

in

local,

regional

and

international

business,

economic

or

political

conditions;

(5)

regulatory

initiatives

in

the

U.S.,

including

the

Dodd-Frank

Act, subjecting us to new and more stringent regulatory requirements; (6) the

increase in unemployment or deterioration in real estate asset values or

their failure to recover for an extended period of time; (7) adverse changes in

credit quality trends; (8) our ability to determine accurate values of

certain assets and liabilities; (9) adverse behaviors in securities, public debt,

and capital markets ; (10) unanticipated changes in our liquidity position,

including but not limited to, changes in the cost of liquidity, our ability to

enter the financial markets and to secure alternative funding sources; (11) the

soundness

of

other

financial

institutions;

(12)

our

ability

to

satisfy

new

capital

and

liquidity

standards

such

as

those

imposed

by

the

Dodd-Frank

Act

and

those

adopted

by

the

Basel

Committee;

(13)

our

ability

to

receive

dividends

from

our

subsidiary,

KeyBank;

(14)

downgrades

in

our

credit

ratings

and the credit ratings of KeyBank; (15) our ability to timely and effectively

implement our strategic initiatives; (16) operational or risk management

failures; breaches of security or failures of our technology systems due to

technological or other factors and cybersecurity threats; (17) the occurrence

of natural or man-made disasters or conflicts or terrorist attacks; (18) the

adequacy of our risk management programs; (19) adverse judicial

proceedings;

(20)

increased

competitive

pressure

due

to

industry

consolidation;

(21)

our

ability

to

attract

and

retain

talented

executives

and

employees, to effectively sell additional products or services to new or existing

customers, and to manage our reputational risks; and (22) unanticipated

adverse effects of acquisitions and dispositions of assets or businesses. We

provide greater detail regarding these factors in our 2012 Form 10-K and subsequent filings, which are available online at www.key.com/ir and

www.sec.gov. Forward looking statements speak only as of the date they are made and

Key does not undertake any obligation to update the forward- looking

statements to reflect new information or future events. This

presentation

also

includes

certain

Non-GAAP

financial

measures

related

to

“tangible

common

equity,”

“Tier

1

common

equity,”

“pre-provision

net

revenue,”

“cash

efficiency

ratio,”

and

“adjusted

cash

efficiency

ratio.”

Management

believes

these

ratios

may

assist

investors,

analysts

and

regulators

in analyzing Key’s financials. Although Key has procedures in place to ensure

that these measures are calculated using the appropriate GAAP or

regulatory

components,

they

have

limitations

as

analytical

tools

and

should

not

be

considered

in

isolation,

or

as

a

substitute

for

analysis

of

results

under GAAP. For more information on these calculations and to view the

reconciliations to the most comparable GAAP measures, please refer to the

Appendix to this presentation or our most recent earnings press release, which is

accessible at www.key.com/ir. 2 |

Key

is a strong company that is well-positioned to leverage its distinctive

capabilities Key –

Who We Are

Revenue

Ranking based on asset size

Loans and deposit balances: 3Q13 YTD average; revenue and noninterest income: YTD

as of 9/30/13 Loans

•

15

th

largest U.S. bank-based financial

services company

•

Two primary lines of business:

Key Community Bank

Key Corporate Bank

•

Business diversity across the franchise

•

Relationship-based strategy and value

proposition

•

Local presence with industry expertise

Key Corporate Bank

Key Community Bank

Other

Noninterest Income

3 |

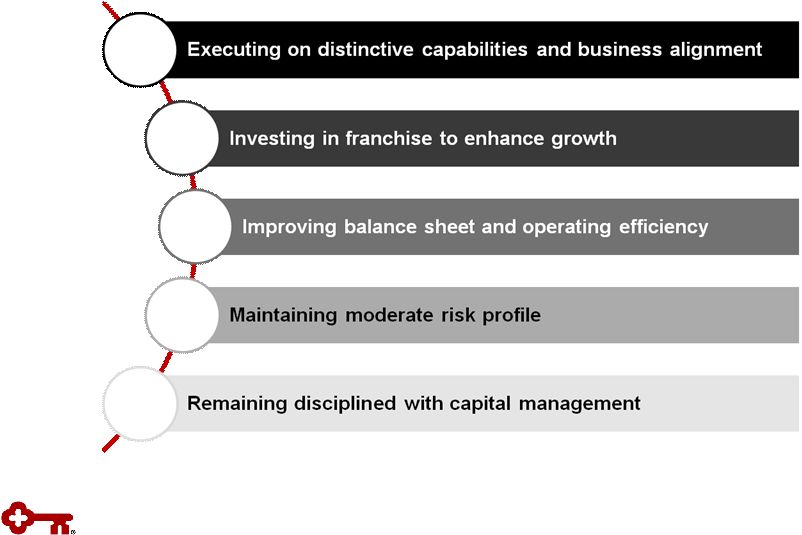

Execution of strategic priorities position Key to best deliver for its clients

Positioned to Win

Executing on distinct capabilities

and business alignment

Investing in franchise

Improving productivity

Maintaining moderate risk profile

Remaining disciplined with

capital management

Solutions that meet clients’

needs

Broad capabilities, including on-balance sheet and capital markets

alternatives

Competitive businesses, positioned to grow

Winning market share and investing for growth

More efficient and productive with improved client focus

Cash efficiency ratio

(a)

down to 64% in 3Q13 from 69% at the

launch of the efficiency initiative (2Q12)

Strong credit culture and risk management process

Net charge-offs down 66% from 3Q12

Delivering shareholder value and returning capital

Total payout of 79% YTD

(b)

Benefit to Key and Clients

Strategic Priorities

(a)

Excludes efficiency initiative charges

(b)

Includes dividends and share repurchases through 9/30/13

4 |

Business Model: Aligned and Targeted

Traditional Bank Products

Capital Markets Capabilities

Deposits & payments

Loans

Wealth management &

private banking

Equipment

finance

Commercial mortgage

banking

Derivatives & foreign

exchange

Equity capital markets

Equity research

M&A /

financial sponsors /

leveraged finance

Investment grade & high-

yield debt

Loan syndications

Public finance

Key’s Competitive Advantage

Commercial Client Revenue Size ($MM)

Local delivery of broad product set and industry expertise

Community Bank

Corporate Bank

Targeted Industries

5 |

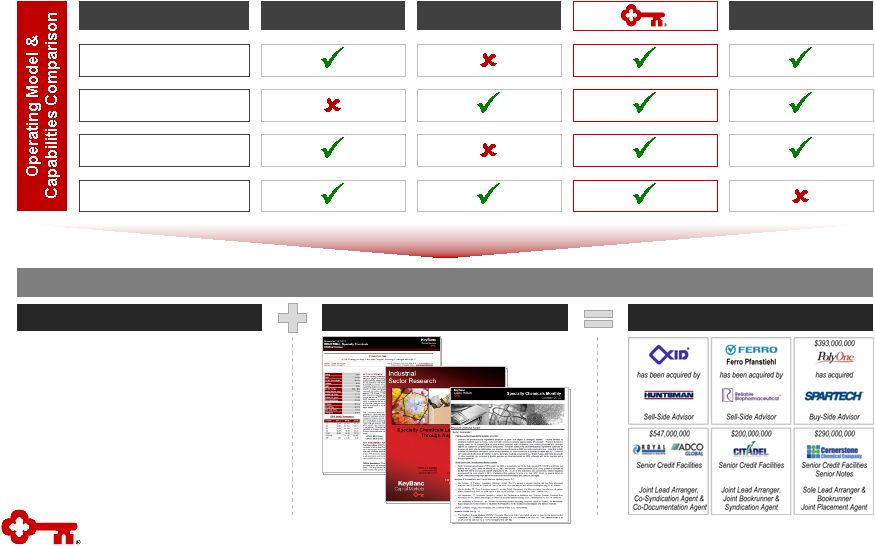

6

Key Corporate Bank

Our middle market focus, industry-driven operating model and broad corporate

& investment banking capability set are unique…and drive results

Regional Banks

Universal Banks

Capability / Model

Middle Market Focus

Industry-driven Model

Investment Banking

Focused Franchise

Deep Industry Knowledge

Results (FY13)

Case Study: Industrial (Specialty Chemicals Practice)

•

Four dedicated chemicals coverage

bankers with aligned M&A, syndications

and capital markets professionals

•

Leading M&A advisory practice

•

Strong presence across industry events

•

Top-rated equity research franchise (two

analysts covering 36 companies)

•

$1B in capital committed to sector

•

> 50 clients and 200 prospects

Commercial Banking

Boutiques

Note:

Operating

model

and

capabilities

comparison

data

are

illustrative

and

represent

a

typical

firm

within

each

category;

some

exceptions

will

apply. |

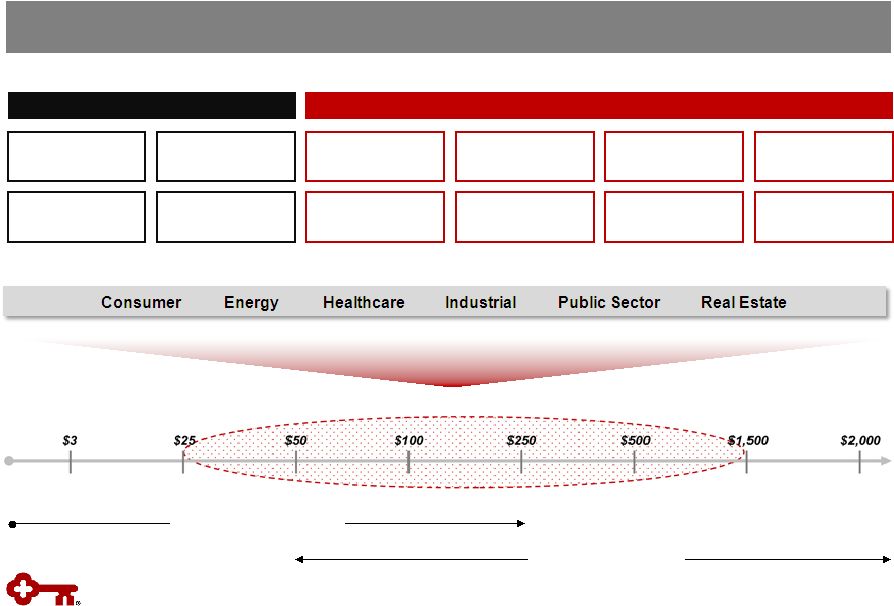

7

Delivering the Distinctive Platform

Key can lead transactions across markets --

this breadth and access allow

us to match client needs and market conditions to deliver the best execution

for our clients

•

In the twelve months ended 3Q13, Key Corporate Bank raised $57B in capital in >

800 transactions, less than 15% of which went to our balance sheet

Healthcare

Energy

Consumer

Industrial

Public Sector

Real Estate

Key’s Balance

Sheet

Equity Capital

Markets

Syndicated Loans

Real Estate Capital

Markets

Debt Capital Markets

(IG/HY/Public Fin.)

Private Capital

Industry Verticals

Capital Placement ($B)

Key’s Capital Solutions

Credit facility (bank or institutional)

Bridge loan

Direct placement (debt or equity)

Equity offerings (IPOs / FOs / converts)

Commercial mortgage

Investment grade & high-yield debt

Mezzanine capital placement

Tax-exempt securities

Note:

Capital

placement

$

are

LTM

3Q13

and

include:

in

transactions

where

Key

served

as

bookrunner

(or

equivalent)

--

100%

of

capital

raised;

in

transactions

where

Key

served

as

co-manager

--

the

proportion

of

capital

corresponding

to

Key’s

transaction

economics

(e.g.,

$20MM

if

Key

were

a

10%

co-manager

on

a

$200MM

equity

offering).

Balance

sheet

figures

represent

loan

commitments.

Data

exclude

equipment

finance

and

syndicated

loan

participations.

$8

$36

$5

$5

$1

$2

Additional value is created as Key delivers non-capital solutions (e.g.,

payments, derivatives, foreign exchange, financial advisory) to

clients |

Growing

Our Franchise We have taken purposeful steps to enhance our ability to

acquire and expand

targeted client relationships within our industry verticals

the result is

greater transaction activity and enhanced roles for Key

•

Key Corporate Bank has raised $46B of capital for our clients during the first nine

months of FY13 --

more than any previous full-year period

Capital Placement ($B)

Note:

Capital

placement

$

include:

in

transactions

where

Key

served

as

bookrunner

(or

equivalent)

--

100%

of

capital

raised;

in

transactions

where

Key

served

as

co-

manager

--

the

proportion

of

capital

corresponding

to

Key’s

transaction

economics

(e.g.,

$20MM

if

Key

were

a

10%

co-manager

on

a

$200MM

equity

offering).

Data

include

loan

commitments

and

exclude

equipment

finance

and

syndicated

loan

participations.

8

$23

$31

$37

$46

$0

$15

$30

$45

$60

$75

FY10

FY11

FY12

YTD 3Q13 |

$29.4

$28.4

$25.5

$22.9

$21.5

$19.9

$18.7

$18.0

$17.2

$16.6

$17.3

$18.5

$18.5

$18.4

$19.2

$19.9

$20.1

$20.2

$20.9

$177

$149

$149

$153

$154

$155

$193

$208

$243

$258

$227

$224

$222

$235

$272

$320

$339

$352

$355

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

2Q13

3Q13

Achieving Results

Note:

Chart depicts period-end loan balances for Key Corporate Bank only. LTM

denotes the twelve month period ended 3Q13. We continue to make solid progress

in growing both loans and investment banking & debt placement fees

-- demonstrating the power of our model

•

Since 1Q09, investment banking and debt placement fees have doubled while we

focused our balance sheet strategically on a more targeted client base

•

Loan balances up $4.3B (+26%) vs. 2Q11 trough

Loan Balances ($B) & LTM Investment Banking & Debt Placement Fees

($MM) Corporate Bank Loan Balances ($B)

LTM Investment Banking & Debt Placement Fees ($MM)

9 |

External Benchmarking

Our results compare favorably to external benchmarks

we are gaining C&I

loan share and getting paid for the risks we take

Loan Growth

Source:

Federal

Reserve

H8

report

dated

October

25,

2013;

peer

SEC

filings

and

earnings

releases.

Peer

data

are

for

Corporate

Bank

equivalent

segments

of

peer

financial

institutions

(e.g.,

PNC

Corporate

&

Institutional

Banking

segment).

Peer

banks

include

BAC,

CMA,

FITB,

JPM,

PNC,

STI,

USB,

WFC.

Revenue

/

assets

calculation

is

calculated

based

on

LTM

3Q13

revenue

divided

by

3Q13

average

assets

for

Key

and

peers.

Asset Productivity

Since our portfolio troughed in 2Q11, Key Corporate Bank has taken

C&I loan share…

…while our broad product capabilities generate peer leading asset

productivity

10 |

Note:

Middle

Market

denotes:

Public

companies

with

market

capitalization

between

$50MM

and

$1.5B

+

private

companies

and

public

sector

entities

with

revenue between $50MM and $1.5B. Key clients include Key Corporate Bank +

Commercial Banking business units. Source:

Capital IQ; Dun & Bradstreet; U.S. Census.

We have a substantial opportunity to expand our client base --

targeting

middle market companies $50MM to $1.5B within our focus industry

verticals

•

~5,000 prospects headquartered within Key’s Community Bank franchise that

align with the Corporate Bank’s focus industry verticals

•

On a YTD basis, Key’s new corporate & investment banking clients generate

average revenue ~$300k

Sizing the Opportunity

U.S. Middle Market Universe

(all industries and geographies)

Focus Verticals

(all geographies)

Focus Verticals + In-Footprint

~40,000 companies & institutions

~25,000 companies & institutions

~6,000 companies & institutions

Key clients

Non-clients

11 |

A

clear, focused strategy executed with rigor and discipline over the cycle is

the core of our risk management strategy

•

Net charge-offs of $21MM (10bps) over the last twelve months

•

Portfolio credit quality is strongest since pre-crisis across all

metrics Effective Risk Management

•

Industry expertise

& specialization

–

Lend to sectors we

know well

–

Better discern risk/return

trade-offs

–

Ability to distribute risk via

syndications and capital

markets solutions

•

Client selection

–

Long-term approach to client

relationships and franchise building

–

Target clients within Key’s risk

appetite

•

Risk culture & awareness

–

Strong partnership

between sales and risk

teams

•

Core principles

•

Willing to exit relationships

–

Exited > 2,000 client relationships

post-crisis for risk-related reasons

–

Reduced construction lending by

more than 75% ($2B) since crisis

•

Clearly defined “good

business”

parameters

–

Strong hurdles & tracking

for new opportunities

–

Disciplined hold limits

–

Structural rigor

–

Client-level ROE thresholds

–

Lead with ideas and

solutions, vs. balance sheet

12 |

| Financial Review

13

*

*

*

*

*

*

*

*

* |

Progress on Targets for Success

Focus areas

Metrics

(a)

KEY

FY11

KEY

FY12

KEY

3Q13 YTD

Targets

Improving balance

sheet efficiency

Loan to deposit ratio

(b)

87%

86%

84%

90-100%

Maintaining

moderate risk profile

NCOs to average loans

1.11%

.69%

.33%

40-60 bps

Provision to average loans

(.12)%

.45%

.28%

Growing high

quality, diverse

revenue streams

Net interest margin

3.16%

3.21%

3.16%

>3.50%

Noninterest income

to total revenue

44%

46%

43%

>40%

Generating positive

operating leverage

Adj. cash efficiency ratio

(ex. efficiency initiative

charges)

(c)

68%

67%

65%

60-65%

Strengthening

returns with

disciplined capital

management

Return on average assets

1.17%

1.05%

1.02%

1.00-1.25%

(a)

Continuing operations, unless otherwise noted

(b)

Represents period-end consolidated total loans and loans held for sale

(excluding education loans in the securitization trusts) divided by

period-end consolidated total deposits (excluding deposits in foreign office)

(c)

Excludes intangible asset amortization; non-GAAP measure: see Appendix for

reconciliation 14 |

Operating Leverage: Driving Productivity and Efficiency

(a)

Efficiency initiative charges include pension settlement in 3Q13

(b)

Non-GAAP measures: see Appendix for reconciliation

(c)

Excludes one-time gains of $54 million related to the redemption of trust

preferred securities Achieved cost savings target; focused on further

efficiency improvement Driving productivity enhancements: improving annualized

revenue per FTE 15 |

Strong Capital Position is a Competitive Strength Over Time

Disciplined Capital Management

Executing on Capital Priorities

(a)

Peer group data source: SNL; 9/30/13 ratios are estimated

1. Organic Growth

4. Opportunistic Growth

2. Dividends

3. Share Repurchases

16 |

Focused Forward

Key is well-positioned to grow and improve returns

17 |

| Appendix

18

*

*

*

*

*

*

*

*

*

* |

Outlook

and Expectations Loans

•

Mid-single digit average balance growth

NIM

•

Relatively stable to the 3Q13 level over the next few quarters

•

Potential downward pressure, dependent upon level of liquidity

Revenue

•

Net interest income relatively stable in 2H13

•

Continued strength in fee income businesses

Expense

•

$680 -

$700 million for 4Q13, including one-time charges

Efficiency

•

60% -

65% cash efficiency

NCOs / Provision

•

Within

or

below

targeted

range

of

40

–

60

bps

of

average

loans

•

Provision near the level of net charge-offs

Capital

•

Remaining share repurchase authority of $187 million over the next

two quarters

Guidance provided during 3Q13 earnings call

19 |

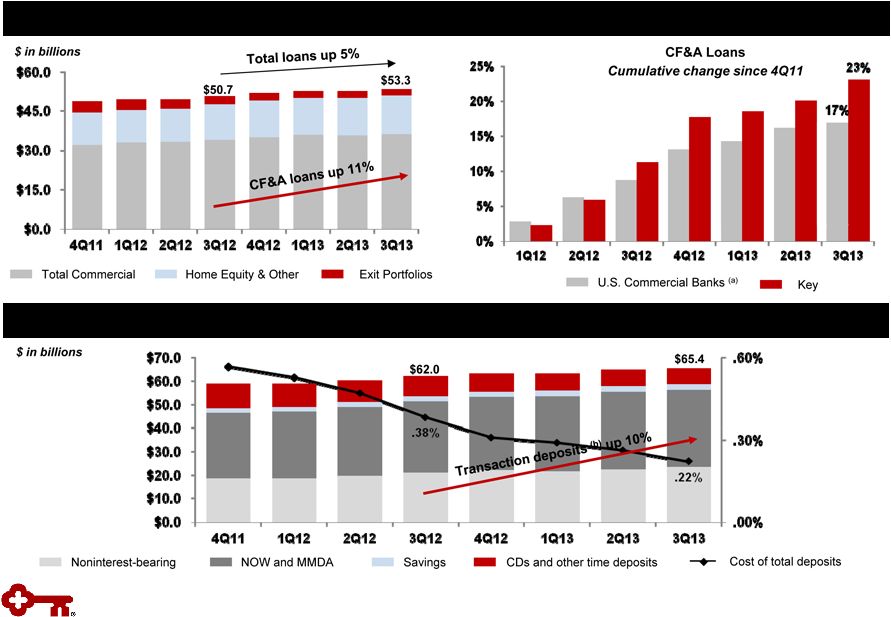

Efficient Balance Sheet: Improving Balance Sheet Mix

Average Loans Continue to Increase, Driven by Commercial, Financial &

Agricultural (CF&A) Growth in Non-time Deposits with Improved Funding

Cost 20

Note: Loan and deposit figures represent average balances; deposits exclude

deposits in foreign office (a) Source: Federal Reserve H8;

industry data are not seasonally adjusted (b) Transaction

deposits include noninterest-bearing, NOW, and MMDA |

Average Total Investment Securities

Highlights

High Quality Investment Portfolio

Portfolio composed of Agency or GSE backed

CMOs: Fannie, Freddie & GNMA

–

No private label MBS or financial paper

Average portfolio life at 9/30/13 of 3.8 years

compared to 3.2 years at 6/30/13

Unrealized net gain of $3 million on available-for-

sale securities portfolio at 9/30/13

Securities cash flows of $1.3 billion in 3Q13

and $1.5 billion in 2Q13

Yields on purchases were 67 bps lower than

3Q13 maturities

Securities to Total Assets

(b)

(a) Yield is calculated on the basis of amortized cost

(b) Includes end of period held-to-maturity and

available-for-sale securities 21 |

High

Quality Revenue: Diverse Streams TE = Taxable equivalent

(a) Excludes gains from the redemption of trust preferred securities

and leveraged lease terminations Noninterest income diversity provides

strength; growth in core businesses (a)

Net Interest Income & Net Interest Margin (TE) Trend

Noninterest Income

22

Continuing Operations |

Significant Improvement in Credit Quality Trends

Moderate Risk Profile: Strong Credit Quality

Maintaining Moderate Risk Profile

(a)

Peer group data source: SNL

23 |

Asset

Quality Trends Quarterly Change in Criticized Outstandings

(a)

Delinquencies to Period-end Total Loans

(a)

Loan and lease outstandings

(b)

From continuing operations

Metric

(b)

3Q13

2Q13

1Q13

4Q12

3Q12

Delinquencies to EOP total loans: 30-89 days

.54

%

.47

%

.70

%

.80

%

.69

%

Delinquencies to EOP total loans: 90+ days

.17

.15

.16

.15

.17

NPLs to EOP portfolio loans

1.01

1.23

1.24

1.28

1.27

NPAs to EOP portfolio loans + OREO + Other NPAs

1.08

1.30

1.34

1.39

1.39

Allowance for loan losses to period-end loans

1.62

1.65

1.70

1.68

1.73

Allowance for loan losses to NPLs

160.4

134.4

137.4

131.8

136.0

24 |

Period-

end

loans

Average

loans

Net loan

charge-offs

Net loan

charge-offs

(b)

/

average loans

(%)

Nonperforming

loans

(c)

Ending

allowance

Allowance /

period-end

loans

(d)

(%)

Allowance /

NPLs

(%)

9/30/13

3Q13

3Q13

2Q13

3Q13

2Q13

9/30/13

6/30/13

9/30/13

9/30/13

9/30/13

Commercial, financial and agricultural

(a)

$24,317

$23,864

$ 4

$ 8

.07

.14

$ 102

$ 146

$

370 1.52

362.75

Commercial real estate:

Commercial Mortgage

7,544

7,575

(8)

(2)

(.42)

(.11)

58

106

172

2.28

296.55

Construction

1,058

1,073

(6)

1

(2.22)

.38

17

26

36

3.40

211.76

Commercial lease financing

4,550

4,633

15

(2)

1.28

(.17)

22

14

64

1.41

290.91

Real estate –

residential mortgage

2,198

2,193

2

4

.36

.74

98

94

35

1.59

35.71

Home equity:

Key Community Bank

10,285

10,247

12

14

.46

.56

198

205

82

.80

41.41

Other

353

364

2

5

2.18

5.16

13

16

14

3.97

107.69

Consumer other –

Key Community Bank

1,440

1,435

7

5

1.94

1.44

2

3

27

1.88

N/M

Credit cards

698

700

8

6

4.53

3.45

4

11

34

4.87

850.00

Consumer other:

Marine

1,083

1,120

1

5

.35

1.66

25

30

31

2.86

124.00

Other

71

67

-

1

-

5.42

2

1

3

4.23

150.00

Continuing total

(e)

$53,597

$53,271

$ 37

$ 45

.28

.34

$ 541

$ 652

$

868 1.62

160.44

Discontinued operations

4,738

4,905

9

7

1.36

1.04

23

19

38

.80

165.22

Consolidated total

$58,335

$58,176

$46

$ 52

.33

.38

$ 564

$ 671

$

906 1.55

160.64

Credit Quality by Portfolio

Credit Quality

(a) 9-30-13 ending loan balances include $96 million of

commercial credit card balances; 9-30-13 average loan balances

include $96 million of assets from commercial credit cards

(b)

Net loan charge-off amounts are annualized in calculation. NCO ratios for

discontinued operations and consolidated Key exclude education loans in the

securitization trusts since valued at fair-market value (c)

9-30-13 and 6-30-13 NPL amounts exclude $18 million and $19

million respectively of purchased credit impaired loans acquired in July 2012.

(d) Allowance/period loans ratios for discontinued operations and

consolidated Key exclude education loans in the securitization trusts since valued at

fair-market value

(e) 9-30-13 ending loan balances include purchased loans of $176

million of which $18 million were purchased credit impaired $ in millions

N/M = Not Meaningful

25 |

Vintage (% of Loans)

Loan

Balances

Average Loan

Size ($)

Average

FICO

Average

LTV

(a)

% of Loans

LTV>90%

2012 and

later

2011

2010

2009

2008 and

prior

Home equity loans and lines

First lien

$

16 $ 23,209

744

35

%

.4

%

-

-

1%

1%

98

%

Second lien

337

23,003

729

82

32.5

-

-

-

-

100

Total home equity loans and lines

$ 353

23,013

729

80

31.0

-

-

-

-

100

Nonaccrual loans

First lien

$

1 $

24,247 729

33

%

-

-

-

-

-

100

%

Second lien

12

24,712

702

82

35.1

%

-

-

-

-

100

Total home equity nonaccrual loans

$

13 24,685

703

80

33.0

-

-

-

-

100

Exit Portfolio -

Home Equity

Third quarter net charge-offs

$

2 -

-

-

-

100

%

Net loan charge-offs to average loans

2.18

%

Vintage (% of Loans)

Loan

Balances

Average Loan

Size ($)

Average

FICO

Average

LTV

(a)

% of Loans

LTV>90%

2012 and

later

2011

2010

2009

2008 and

prior

Home equity loans and lines

First lien

$

5,932 $

67,691 765

67

%

.6

%

40

%

6%

4

%

4

%

46%

Second lien

4,353

47,569

760

76

3.2

25

6

4

4

61

Total home equity loans and lines

$ 10,285

57,525

763

71

1.8

33

6

4

4

53

Nonaccrual loans

First lien

$

108 $

58,708 713

73

%

.4%

2

%

3%

3

%

5

%

87%

Second lien

90

48,922

711

78

2.0

-

2

2

4

92

Total home equity nonaccrual loans

$

198 53,794

712

75

1.1

1

2

3

5

89

Community Bank -

Home Equity

Third quarter net charge-offs

$

12 -

3%

-

4

%

93%

Net loan charge-offs to average loans

.46

%

(a)

Average LTVs are at origination. Current average LTVs for Community Bank total

home equity loans and lines is approximately 74%, which compares to 75% at

the end of the second quarter 2013. Community Bank –

Home Equity

Exit Portfolio –

Home Equity

$ in millions, except average loan size

Home Equity Loans –

9/30/13

$ in millions, except average loan size

26 |

Balance Outstanding

Change

Net Loan Charge-offs

Balance on

Nonperforming Status

9-30-13

6-30-13

9-30-13

vs.

6-30-13

3Q13

(c)

2Q13

(c)

9-30-13

6-30-13

Residential properties –

homebuilder

$ 26

$ 26

-

-

$ 1

$ 8

$ 8

Marine and RV floor plan

25

28

$ (3)

-

-

6

7

Commercial lease financing

(a)

796

931

(135)

$ (2)

(2)

1

1

Total commercial loans

847

985

(138)

(2)

(1)

15

16

Home equity –

Other

353

375

(22)

2

5

14

16

Marine

1,083

1,160

(77)

1

5

25

31

RV and other consumer

71

69

2

-

1

2

-

Total consumer loans

1,507

1,604

(97)

3

11

41

47

Total exit loans in loan portfolio

$ 2,354

$ 2,589

$ (235)

$ 1

$ 10

$ 56

$ 63

Discontinued operations –

education lending

business (not included in exit loans above)

(b)

$ 4,738

$ 4,992

$ (254)

$ 9

$ 7

$ 23

$ 19

(a)

Includes (1) the business aviation, commercial vehicle, office products,

construction and industrial leases; (2) Canadian lease financing portfolios;

and (3) all remaining balances related to lease in, lease out; sale in, lease out;

service contract leases; and qualified technological equipment leases (b)

Includes loans in Key’s consolidated education loan securitization

trusts (c)

Credit amounts indicate recoveries exceeded charge-offs

$ in millions

Exit Loan Portfolio

Exit Loan Portfolio

27 |

Three months ended

9-30-13

6-30-13

9-30-12

Tangible common equity to tangible assets at period end

Key shareholders’

equity (GAAP)

$

10,206

$

10,229

$

10,251

Less:

Intangible assets

(a)

1,017

1,021

1,031

Preferred Stock, Series A

(b)

282

282

291

Tangible common equity (non-GAAP)

$

8,907

$

8,926

$

8,929

Total assets (GAAP)

$

90,708

$

90,639

$

86,950

Less:

Intangible assets

(a)

1,017

1,021

1,031

Tangible assets (non-GAAP)

$

89,691

$

89,618

$

85,919

Tangible common equity to tangible assets ratio (non-GAAP)

9.93

%

9.96

%

10.39

%

Tier 1 common equity at period end

Key shareholders' equity (GAAP)

$

10,206

$

10,229

$

10,251

Qualifying capital securities

340

339

339

Less:

Goodwill

979

979

979

Accumulated

other

comprehensive

income

(loss)

(c)

(409)

(359)

(109)

Other assets

(d)

96

101

121

Total Tier 1 capital (regulatory)

9,880

9,847

9,599

Less:

Qualifying capital securities

340

339

339

Preferred Stock, Series A

(b)

282

282

291

Total Tier 1 common equity (non-GAAP)

$

9,258

$

9,226

$

8,969

Net

risk-weighted

assets

(regulatory)

(d)

$

82,913

$

82,528

$

79,363

Tier 1 common equity ratio (non-GAAP)

11.17

%

11.18

%

11.30

%

Pre-provision net revenue

Net interest income (GAAP)

$

578

$

581

$

572

Plus:

Taxable-equivalent adjustment

6

5

6

Noninterest income (GAAP)

459

429

518

Less:

Noninterest expense (GAAP)

716

711

712

Pre-provision net revenue from continuing operations (non-GAAP)

$

327

$

304

$

384

GAAP to Non-GAAP Reconciliation

$ in millions

(a)

Three months ended September 30, 2013, June 30, 2013, and September 30, 2012

exclude $99 million, $107 million, and $130 million, respectively, of

period end purchased credit card receivable intangible assets (b)

Net of capital surplus for the three months ended September 30, 2013 and June 30,

2013 (c)

Includes net unrealized gains or losses on securities available for sale (except

for net unrealized losses on marketable equity securities), net gains or

losses on cash flow hedges, and amounts resulting from the application of the applicable accounting guidance for defined benefit and other

postretirement plans

(d)

Other assets deducted from Tier 1 capital and net risk-weighted assets consist

of disallowed intangible assets (excluding goodwill) and deductible

portions of nonfinancial equity investments. There were no disallowed

deferred tax assets at 9-30-13, 6-30-13, and 9-30-12

28 |

GAAP

to Non-GAAP Reconciliation (continued) $ in millions

(a)

Three months ended September 30, 2013, June 30, 2013, and September 30, 2012

exclude $103 million, $110 million and $86 million, respectively, of

average ending purchased credit card receivable intangible assets

Three months ended

9-30-13

6-30-13

9-30-12

Average tangible common equity

Average Key shareholders' equity (GAAP)

$

10,237

$

10,314

$

10,222

Less:

Intangible assets (average)

(a)

1,019

1,023

1,026

Preferred Stock, Series A (average)

291

291

291

Average tangible common equity (non-GAAP)

$

8,927

$

9,000

$

8,905

Return on average tangible common equity from continuing operations

Net

income

(loss)

from

continuing

operations

attributable

to

Key

common

shareholders

(GAAP)

$

229

$

193

$

211

Average tangible common equity (non-GAAP)

8,927

9,000

8,905

Return on average tangible common equity from continuing operations

(non-GAAP) 10.18

%

8.60

%

9.43

%

Return on average tangible common equity consolidated

Net income (loss) attributable to Key common shareholders (GAAP)

$

266

$

198

$

214

Average tangible common equity (non-GAAP)

8,927

9,000

8,905

Return on average tangible common equity consolidated (non-GAAP)

11.82

%

8.82

%

9.56

%

Cash efficiency ratio

Noninterest expense (GAAP)

$

716

$

711

$

712

Less:

Intangible asset amortization on credit cards (GAAP)

8

7

6

Other intangible asset amortization (GAAP)

4

3

3

Adjusted noninterest expense (non-GAAP)

$

704

$

701

$

703

Net interest income (GAAP)

$

578

$

581

$

572

Plus:

Taxable-equivalent adjustment

6

5

6

Noninterest income (GAAP)

459

429

518

Total taxable-equivalent revenue (non-GAAP)

$

1,043

$

1,015

$

1,096

Cash efficiency ratio (non-GAAP)

67.5

%

69.1

%

64.1

%

Adjusted cash efficiency ratio

Adjusted noninterest expense (non-GAAP)

$

704

$

701

$

703

Less:

Efficiency initiative and pension settlement charges (non-GAAP)

41

37

9

Net adjusted noninterest expense (non-GAAP)

$

663

$

664

$

694

Total taxable-equivalent revenue (non-GAAP)

$

1,043

$

1,015

$

1,096

Adjusted cash efficiency ratio (non-GAAP)

63.6

%

65.4

%

63.3

%

29 |

Tier 1

Common Equity Under the Regulatory Capital Rules, Incorporating Basel III

Guidance (estimated) (a)

KeyCorp & Subsidiaries

$ in billions

Quarter ended

Sept. 30, 2013

Tier 1 common equity under current regulatory rules

$

9.3 Adjustments from current regulatory rules

to the Regulatory Capital Rules: Deferred tax assets and other

(b)

(.1)

Tier 1 common equity anticipated under the Regulatory Capital Rules

(c)

$

9.1 Total risk-weighted

assets under current regulatory rules

$

82.9 Adjustments from current regulatory rules to the

Regulatory Capital Rules: Loan commitments <1 year

.5

Past Due Loans

.2

Mortgage servicing assets

(d)

.6

Deferred tax assets

(d)

.2

Other

1.5

Total risk-weighted assets anticipated under the Regulatory Capital

Rules

$

85.9 Tier 1 common equity ratio under the Regulatory Capital

Rules 10.6

%

(a)

Tier

1

common

equity

is

a

non-generally

accepted

accounting

principle

(GAAP)

financial

measure

that

is

used

by

investors,

analysis

and

bank

regulatory agencies to assess the capital position of financial services

companies; management reviews Tier 1 common equity along with other

measures of capital as part of its financial analyses

(b)

Includes the deferred tax asset subject to future taxable income

for realization, primarily tax credit carryforwards

(c)

The

anticipated

amount

of

regulatory

capital

and

risk-weighted

assets

is

based

upon

the

federal

banking

agencies’

Regulatory

Capital

Rules

(as

fully phased-in on January 1, 2019); Key is subject to the Regulatory

Capital Rules under the “standardized approach”

(d)

Item is included in the 10%/15% exceptions bucket calculation and is

risk-weighted at 250% Table may not foot due to rounding

30 |