Attached files

| file | filename |

|---|---|

| EX-99.1 - PRESS RELEASE - DELTA AIR LINES, INC. | delta_8k-ex9901.htm |

| 8-K - CURRENT REPORT ON FORM 8-K - DELTA AIR LINES, INC. | delta_8k.htm |

Exhibit 99.2

Delta: A Balanced Approach to Capital Deployment May 8, 2013

This presentation contains various projections and other forward-looking statements which represent Delta’s estimates or expectations regarding future events. All forward-looking statements involve a number of assumptions, risks and uncertainties, many of which are beyond Delta’s control, that could cause the actual results to differ materially from the projected results. Factors which could cause such differences include, without limitation, business, economic, competitive, industry, regulatory, market and financial uncertainties and contingencies, as well as the “Risk Factors” discussed in Delta’s SEC filings. Caution should be taken not to place undue reliance on Delta’s forward-looking statements, which represent Delta’s views only as of the date of this presentation, and which Delta has no current intention to update. In this presentation, we will discuss certain non-GAAP financial measures. You can find the reconciliations of those measures to comparable GAAP measures on our website at delta.com. Safe Harbor 2

Balanced Approach To Capital Deployment Business Producing Strong Financial Results Disciplined Capital Investment Is Key To Success Balanced Approach To Capital Deployment 3 Delta’s financial foundation has strengthened considerably over the past five years with significant free cash flow used for balance sheet improvement; our five year plan shows growing cash flows and returns Taking a balanced approach to use of capital by allocating free cash flow among further debt reduction, shareholder returns, and opportunistically addressing longer-term pension funding obligations Maintaining disciplined approach to capital investment is key to sustained free cash flow generation and strong return on invested capital

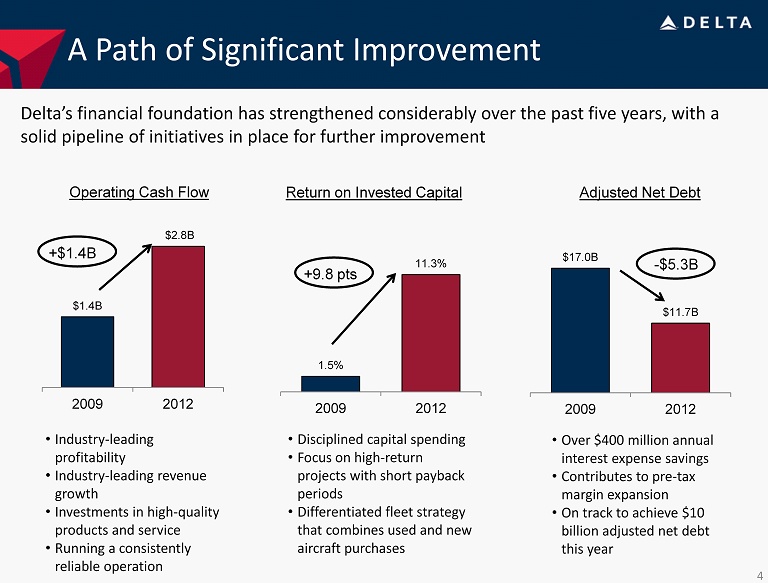

A Path of Significant Improvement Delta’s financial foundation has strengthened considerably over the past five years, with a solid pipeline of initiatives in place for further improvement $1.4B $2.8B 2009 2012 1.5% 11.3% 2009 2012 $17.0B $11.7B 2009 2012 Operating Cash Flow Return on Invested Capital Adjusted Net Debt +$1.4B +9.8 pts -$5.3B 4 •Industry-leading profitability •Industry-leading revenue growth •Investments in high-quality products and service •Running a consistently reliable operation •Disciplined capital spending •Focus on high-return projects with short payback periods •Differentiated fleet strategy that combines used and new aircraft purchases •Over $400 million annual interest expense savings •Contributes to pre-tax margin expansion •On track to achieve $10 billion adjusted net debt this year

A Detailed Five-Year Planning Process With initial post-merger financial goals nearly achieved, the Board of Directors evaluated Delta’s comprehensive financial plan for the next five years •Long-term goal is to achieve sustainable, high single-digit pre-tax margins •Hold capacity growth below expected GDP change •Plan capacity levels conservatively to improve profitability in a rising fuel environment •Fleet flexibility is key to cost-effectively adjusting capacity •Consistent but disciplined capital investment in the business to increase Delta’s revenue premium and improve cost efficiency •Further debt reduction beyond $10 billion adjusted net debt Using Our Guiding Principles and Goals… …To Produce A Solid Five-Year Plan •Steady pre-tax margin expansion over the next five years •Tightened correlation between fuel and revenue driven by structural changes in the industry •Harvests the benefits from existing investments, such as New York, Virgin Atlantic, and Trainer. •Capital plan provides for ongoing investment in the business, while also preserving flexibility •Achieves and maintains new $7 billion adjusted net debt target •Non-fuel unit cost growth maintained at or below forward inflation estimates •Unfunded pension liability steadily declines over the entire period assuming no change to funding levels or financial market conditions 5

Disciplined Capital Investment Is Key To Success 6 Capital plan provides for ongoing investment in the business, while maintaining flexibility to adjust annual spending levels 2013 2014 2015 2016 2017 Capital Spending of $2.0 -$2.5 Billion Annually Not committed Facilities, Technology and Product Aircraft –committed

Capital Discipline Drives Free Cash Flow Capital Spending and Operating Cash Flow ($ Billion) Note: Includes pre-merger NWA Delta’s business model produces both solid financial results and significant free cash flow 1998 –2000 Cumulative earnings: $6.5 billion Cumulative free cash flow: ($2.0 billion) 2010 –2012 Cumulative earnings: $4.1 billion Cumulative free cash flow: $3.9 billion 7 $2.6 $3.8 $4.1 $4.8 $4.1 $2.9 $1.8 $1.3 $1.2 $0.9 $2.1 $2.6 $1.2 $1.3 $1.3 $2.0 $2.4 ($2.0) ($1.0) $0.0 $1.0 $2.0 $3.0 $4.0 $5.0 $6.0 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 Capex Operating Cash Flow $2.0-$2.5

Plan For Free Cash Flow Deployment Delta’s plan expected to generate significant free cash flow, creating up to $5 billion of value for shareholders through a combination of further debt reduction, capital return to shareholders and opportunistic pension funding 8 Debt Reduction Return to Shareholders Pension Funding Further $5 billion debt reduction from 2012 levels allows company to achieve and maintain new adjusted net debt target of $7 billion Board has approved a plan that will return more than $1 billion to shareholders over the next three years At current funding levels, pension liability to decline over next decade to below $5 billion; opportunistic incremental contributions of up to $1 billion mitigate longer-term funding needs

Debt Reduction Remains A Priority •There is meaningful benefit to further debt reduction; new target is to achieve and maintain $7 billion of adjusted net debt •Additional debt reduction drives improvements to earnings and cash flow, while strengthening the balance sheet $17.0 $15.0 $12.9 $11.7 $10.0 $7.0 2009 2010 2011 2012 2013E Goal Adjusted Net Debt 9 Further deleveringcreates value by: •Reducing Delta’s cost of capital, lowering funding costs •Improving earnings through lower interest expense •Increasing stability through a healthier balance sheet •Providing more consistent access to the capital markets by reducing leverage and improving Delta’s credit metrics Interest expense $1.3B $0.5B $1.0B$1.1B $1.2B $0.9B

2012 2017 Targeting Improved Balance Sheet Metrics •Plan targets investment grade balance sheet metrics; these metrics became the basis for company’s new $7 billion adjusted net debt target •By deriskingthe business, Delta improves its investment profile for long-term investors 2012 2017 2012 2017 FFO/Debt EBITDA/Fixed Charges Debt/EBITDA 10 All metrics exclude unfunded pension liabilities; FFO is cash flow from operations, before changes in working capital, plus adjustments for depreciation associated with operating lease conversion to debt; EBITDA is earnings before interest, taxes, depreciation and amortization; Fixed charges include operating lease interest. Benchmarks Based on Three Year US Industrial Average Medians as of fiscal year end 2011, sourced from www.mycreditprofile.standardandpoors.com. 15.3% 35 -40% 2.8x 5.0 –5.5x 4.6x 2.5 –3.0x S&P Industrial Average Median BBB 34% BB 25% B 12% S&P Industrial Average Median BBB 8.2x BB 4.8x B 2.3x S&P Industrial Average Median BBB 2.3x BB 3.2x B 5.5x

Pension Liability Will Decline Over Time • Delta’s benefit pension plans are permanently frozen and closed to new participants. No additional benefits are accruing to existing plan participants. • Airline relief within the 2006 Pension Protection Act provides for both a favorable discount rate and longer funding period. • Over the next decade, minimum pension contributions combined with expected 9% asset returns should generate sufficient cash flows each year to pay current benefits and also modestly increase the pension asset base. Pension Unfunded Liability and Benefit Payments ($B) 11 Pension liability declines to less than $5 billion over next decade at current interest rates assuming only minimum funding $- $2.0 $4.0 $6.0 $8.0 $10.0 $12.0 $14.0 2013 2015 2017 2019 2021 2023 Expected Benefit Payments Unfunded liability at current 4% discount rate Unfunded liability at historical 7% discount rate

$- $500 $1,000 $1,500 $2,000 2014 2016 2018 2020 2022 2024 2026 2028 2030 Required funding 5-year plan average Average Pension Funding Levels Drop Beyond 2024 •Pension Protection Act relief smoothsfunding requirements through 2024 •Funding requirements beyond 2024 still average less than current $650M -$700M annual funding levels 12 Pension Funding ($M) PPA ERISA 5-yr plan avg. $680M 2024-31 average minimum funding: $520M Note: Assumes current 4% discount rate and 9% asset returns

$- $500 $1,000 2014 2016 2018 2020 2022 2024 2026 2028 2030 Required funding with addl. contributions 5-year plan average Incremental Pension Contributions Can Address Longer-Term Pension Funding •Incremental contributions of up to $1 billion over next five years would smooth remaining funding required from 2024-31 at current discount rates •Incremental contributions over next five years would produce funding levels significantly lower than current averages 13 Pension Funding ($M) PPA ERISA 5-yr plan avg. $680M 2024-31 average minimum funding: $225M Note: Assumes current 4% discount rate and 9% asset returns

$- $500 $1,000 2014 2016 2018 2020 2022 2024 2026 2028 2030 Required funding with addl. contributions 5-year plan average Incremental Pension Contributions Can Address Longer-Term Pension Funding •If discount rates rise to normal historical levels of 7% and incremental contributions are made, funding requirements beyond 2024 are minimal 14 Pension Funding ($M) PPA ERISA 5-yr plan avg. $680M 2024-31 average minimum funding: $25M Note: Assumes Towers Watson historical Bond-Link discount rate 7% and 9% asset returns

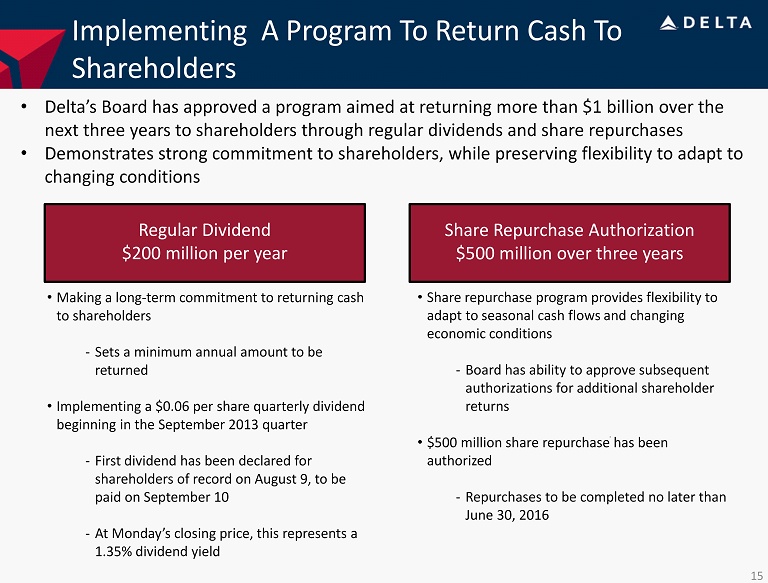

Implementing A Program To Return Cash To Shareholders • Delta’s Board has approved a program aimed at returning more than $1 billion over the next three years to shareholders through regular dividends and share repurchases • Demonstrates strong commitment to shareholders, while preserving flexibility to adapt to changing conditions Regular Dividend $200 million per year Share Repurchase Authorization $500 million over three years •Making a long-term commitment to returning cash to shareholders -Sets a minimum annual amount to be returned •Implementing a $0.06 per share quarterly dividend beginning in the September 2013 quarter -First dividend has been declared for shareholders of record on August 9, to be paid on September 10 -At Monday’s closing price, this represents a 1.35% dividend yield •Share repurchase program provides flexibility to adapt to seasonal cash flows and changing economic conditions -Board has ability to approve subsequent authorizations for additional shareholder returns •$500 million share repurchase has been authorized -Repurchases to be completed no later than June 30, 2016 15

Balanced Approach To Capital Deployment Business Producing Strong Financial Results Disciplined Capital Investment Is Key To Success Balanced Approach To Capital Deployment 16 Delta’s financial foundation has strengthened considerably over the past five years with significant free cash flow used for balance sheet improvement; our five year plan shows growing cash flows and returns Taking a balanced approach to use of capital by allocating free cash flow among further debt reduction, shareholder returns, and opportunistically addressing longer-term pension funding obligations Maintaining disciplined approach to capital investment is key to sustained free cash flow generation and strong return on invested capital

Non-GAAP Financial Measures

Delta sometimes uses information ("non-GAAP financial measures") that is derived from our Consolidated Financial Statements, but that is not presented in accordance with accounting principles generally accepted in the U.S. (“GAAP”). Under the U.S. Securities and Exchange Commission rules, non-GAAP financial measures may be considered in addition to results prepared in accordance with GAAP, but should not be considered a substitute for or superior to GAAP results. The tables below show reconciliations of non-GAAP financial measures to the most directly comparable GAAP financial measures.

Delta is unable to reconcile certain forward-looking projections to GAAP as the nature or amount of special items cannot be estimated at this time.

Delta excludes special items because management believes the exclusion of these items is helpful to investors to evaluate the company’s recurring core operational performance in the period shown.

Delta adjusts for mark-to-market (MTM) adjustments for fuel hedges recorded in periods other than the settlement period in order to evaluate the company's financial results in the period shown.

Delta uses adjusted total debt, including aircraft rent, in addition to long-term adjusted debt and capital leases, to present estimated financial obligations. Delta reduces adjusted total debt by cash, cash equivalents and short-term investments, resulting in adjusted net debt, to present the amount of additional assets needed to satisfy the debt.

Delta presents net cash provided by operating activities because management believes adjusting for certain items is helpful to investors to evaluate the company’s operating activities.

Delta presents combined capital spending because management believes adjusting for certain items is helpful to investors to evaluate the company’s investing activities.

Delta presents return on invested capital as management believes it is helpful to investors in assessing the company’s ability to generate returns using its invested capital.

Delta presents free cash flow because management believes this metric is helpful to investors to evaluate the company's ability to generate cash.

Delta presents Financial Metrics because management believes these metrics are helpful to investors to evaluate the company's financial performance.

| 17 |

| Operating Cash Flow | ||||||||

| Full Year | Full Year | |||||||

| (in billions) | 2012 | 2008 | ||||||

| Delta operating cash flow (GAAP) | $ | 2.5 | $ | (1.7 | ) | |||

| SkyMiles used pursuant to advance purchase under AMEX agreement | 0.3 | – | ||||||

| Northwest operating cash flow | – | 0.2 | ||||||

| Net cash provided by operations, adjusted | $ | 2.8 | $ | (1.5 | ) | |||

| Return on Invested Capital | ||||||||

| Full Year | Full Year | |||||||

| (in billions, except % return) | 2012 | 2009 | ||||||

| Adjusted Book Value of Equity | $ | 13.9 | $ | 12.9 | ||||

| Average Adjusted Net Debt | $ | 12.0 | $ | 16.8 | ||||

| Average Invested Capital | $ | 25.9 | $ | 29.7 | ||||

| Adjusted Total Operating Income | $ | 2.9 | $ | 0.5 | ||||

| Return on Invested Capital | 11.3% | 1.5% | ||||||

| Adjusted Net Debt | ||||||||||||||||||||||||||||||||

| December 31, | ||||||||||||||||||||||||||||||||

| (in billions) | 2012 | 2011 | 2010 | 2009 | ||||||||||||||||||||||||||||

| Debt and capital lease obligations | $ | 12.7 | $ | 13.8 | $ | 15.3 | $ | 17.2 | ||||||||||||||||||||||||

| Plus: unamortized discount, net from purchase accounting and fresh start reporting | 0.5 | 0.6 | 0.61 | 1.1 | ||||||||||||||||||||||||||||

| Adjusted debt and capital lease obligations | $ | 13.2 | $ | 14.4 | $ | 15.9 | $ | 18.3 | ||||||||||||||||||||||||

| Plus: 7x last twelve months' aircraft rent | 1.9 | 2.1 | 2.7 | 3.4 | ||||||||||||||||||||||||||||

| Adjusted total debt | 15.1 | 16.5 | 18.6 | 21.7 | ||||||||||||||||||||||||||||

| Less: cash, cash equivalents and short-term investments | (3.4 | ) | (3.6 | ) | (3.6 | ) | (4.7 | ) | ||||||||||||||||||||||||

| Adjusted net debt | $ | 11.7 | $ | 12.9 | $ | 15.0 | $ | 17.0 | ||||||||||||||||||||||||

| Capital Spending | ||||

| Full Year | ||||

| (in billions) | 2008 | |||

| Delta capital expenditures (GAAP) | $ | 1.5 | ||

| Northwest capital expenditures | 1.1 | |||

| Total combined capital spending | $ | 2.6 | ||

| 18 |

| Pre-Tax Income | ||||

| Three Years Ended | ||||

| (in billions) | December 31, 2012 | |||

| Pre-tax income | $ | 2.4 | ||

| Items excluded: | ||||

| Restructuring and other items | 1.1 | |||

| Loss on extinguishment of debt | 0.6 | |||

| Pre-tax income excluding special items | $ | 4.1 | ||

| Free Cash Flow | ||||

| Three Years Ended | ||||

| (in billions) | December 31, 2012 | |||

| Net cash provided by operating activities (GAAP) | $ | 8.1 | ||

| Net cash used in investing activities (GAAP) | (5.5 | ) | ||

| Adjustments: | ||||

| Proceeds from sale of property and investments and other | (0.8 | ) | ||

| Purchase of short-term investments | 1.8 | |||

| SkyMiles used pursuant to advance purchase under AMEX agreement | 0.3 | |||

| Total free cash flow | $ | 3.9 | ||

| Financial Metrics | ||||||||||

| Full Year | Full Year | |||||||||

| (in billions) | 2012 | (in billions) | 2012 | |||||||

| Net cash provided by operating activities (GAAP) | $ | 2.5 | Interest expense, net | $ | 0.8 | |||||

| Imputed operating lease depreciation and other | 1.0 | Amortization of debt discount, net | 0.2 | |||||||

| Adjusted funds from operations | $ | 3.5 | Imputed operating lease interest | 0.8 | ||||||

| Adjusted interest expense | $ | 1.8 | ||||||||

| Full Year | December 31, | |||||||||

| (in billions) | 2012 | (in billions) | 2012 | |||||||

| Operating income | $ | 2.2 | Total debt and capital lease obligations | $ | 12.7 | |||||

| Depreciation and amortization | 1.5 | Plus: Imputed amortized operating leases | 9.9 | |||||||

| Imputed operating lease interest | 0.8 | Adjusted debt, including imputed amortized operating leases |

$ | 22.6 | ||||||

| Restructuring and other items | 0.4 | |||||||||

| EBITDA, adjusted | $ | 4.9 | ||||||||

| FFO/Debt | 15.3 | % | ||||||||

| EBITDA/Fixed Charges | 2.8 | |||||||||

| Debt/EBITDA | 4.6 | |||||||||

| 19 |