Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - FAIRFIELD FUTURES FUND LP II | Financial_Report.xls |

| EX-32.1 - EX-32.1 - FAIRFIELD FUTURES FUND LP II | d450375dex321.htm |

| EX-31.1 - EX-31.1 - FAIRFIELD FUTURES FUND LP II | d450375dex311.htm |

| EX-32.2 - EX-32.2 - FAIRFIELD FUTURES FUND LP II | d450375dex322.htm |

| EX-31.2 - EX-31.2 - FAIRFIELD FUTURES FUND LP II | d450375dex312.htm |

| EX-10.4(A) - EX-10.4(A) - FAIRFIELD FUTURES FUND LP II | d450375dex104a.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(X) ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2012

OR ( ) TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission File Number 000-51282

FAIRFIELD FUTURES FUND L.P. II

(Exact name of registrant as specified in its charter)

| New York | 56-2421596 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

c/o Ceres Managed Futures LLC

522 Fifth Avenue — 14th Floor

New York, New York 10036

(Address and Zip Code of principal executive offices)

(855)-672-4468

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act: Redeemable Units of Limited Partnership Interest

(Title of Class)

Indicate by check mark if the registrant is a well known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes No X

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes No X

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes X No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes X No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this form 10-K [X]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | Accelerated filer | Non-accelerated filer X (Do not check if a smaller reporting company) |

Smaller reporting company |

Indicate by check mark if the registrant is a shell company (as defined in rule 2b-2 of the Exchange Act)

Yes No X

Limited Partnership Redeemable Units with an aggregate value of $14,566,340 were outstanding and held by non-affiliates as of the last business day of the registrant’s most recently completed second fiscal quarter.

As of February 28, 2013, 17,077.5231 Limited Partnership Redeemable Units were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

[None]

PART I

Item 1. Business.

(a) General Development of Business. Fairfield Futures Fund L.P. II (the “Partnership”) is a limited partnership organized on December 18, 2003 under the partnership laws of the State of New York to engage, directly or indirectly, in the speculative trading of a diversified portfolio of commodity interests including futures contracts, options, swaps and forward contracts. The sectors traded include currencies, energy, grains, indices, U.S. and non-U.S. interest rates, livestock, lumber, metals and softs. The Partnership commenced trading operations on March 15, 2004. The commodity interests that are traded by the Partnership, through its investment in the Master (as defined below) are volatile and involve a high degree of market risk.

Between January 12, 2004 (commencement of the offering period) and March 12, 2004, 28,601 redeemable units of limited partnership interest (“Redeemable Units”) and 285 General Partner unit equivalents were sold at $1,000 per unit. The proceeds of the initial offering were held in an escrow account until March 15, 2004 at which time they were remitted to the Partnership for trading. Effective January 31, 2012, the Partnership no longer offers Redeemable Units for sale. Subscriptions and redemptions of Redeemable Units and General Partner unit equivalents for the years ended December 31, 2012, 2011 and 2010 are reported in the Statements of Changes in Partners’ Capital on page 40 under “Item 8. Financial Statements and Supplementary Data.”

Ceres Managed Futures LLC, a Delaware limited liability company, acts as the general partner (the “General Partner”) and commodity pool operator of the Partnership. The General Partner is wholly owned by Morgan Stanley Smith Barney Holdings LLC (“MSSB Holdings”). Morgan Stanley, indirectly through various subsidiaries, owns a majority equity interest in MSSB Holdings. Citigroup Inc. indirectly owns a minority equity interest in MSSB Holdings. Citigroup Inc. also indirectly wholly owns Citigroup Global Markets Inc. (“CGM”), the commodity broker for the Partnership. Prior to July 31, 2009, the date as of which MSSB Holdings became its owner, the General Partner was wholly owned by Citigroup Financial Products Inc., a wholly owned subsidiary of Citigroup Global Markets Holdings Inc., the sole owner of which is Citigroup Inc. As of December 31, 2012, all trading decisions for the Partnership are made by the Advisor (defined below).

On June 1, 2006, the Partnership allocated substantially all of its capital to the CMF Graham Capital Master Fund L.P. (the “Master”), a limited partnership organized under the partnership laws of the State of New York. The Partnership purchased 74,569.3761 units of the Master with cash equal to $75,688,021. The Master was formed in order to permit accounts managed by Graham Capital Management, L.P. (“Graham” or the “Advisor”) using the K4D-15V Program, the Advisor’s proprietary, systematic trading program, to invest together in one trading vehicle. A description of the trading activities and focus of the Advisor is included on page 28 under “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.” The General Partner is also the general partner of the Master. The Master’s commodity broker is CGM. Individual and pooled accounts currently managed by the Advisor, including the Partnership, are permitted to be limited partners of the Master. The General Partner and the Advisor believe that trading through this master/feeder structure promotes efficiency and economy in the trading process. Expenses to investors as a result of the investment in the Master are approximately the same and redemption rights are not affected.

The financial statements of the Master, including the Condensed Schedule of Investments, are contained, elsewhere in this report and should be read together with the Partnership’s financial statements.

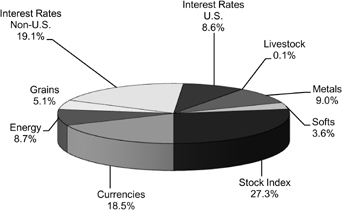

For the period January 1, 2012 through December 31, 2012, the approximate market sector distribution for the Partnership was as follows:

At December 31, 2012 and 2011, the Partnership owned approximately 15.0% and 15.4%, respectively of the Master. It is the Partnership’s intention to continue to invest substantially all of its assets in the Master. The performance of the Partnership is directly affected by the performance of the Master.

The Master’s trading of futures, forwards, swaps and options contracts, if applicable, on commodities is done primarily on U.S. commodity exchanges and foreign commodity exchanges. It engages in such trading through a commodity brokerage account maintained with CGM.

2

The Partnership will be liquidated upon the first of the following to occur: December 31, 2023; the net asset value per Redeemable Unit falls below $400 as of the close of any business day; a decline in net assets after trading commences to less than $1,000,000; or under certain circumstances as defined in the Limited Partnership Agreement of the Partnership (the “Limited Partnership Agreement”).

The General Partner administers the business and affairs of the Partnership including selecting one or more advisors to make trading decisions for the Partnership. The Partnership will pay the General Partner a monthly administrative fee in return for its services to the Partnership equal to 1/24 of 1% (0.5% per year) of month-end Net Assets of the Partnership. Month-end Net Assets, for the purpose of calculating administrative fees are Net Assets, as defined in the Limited Partnership Agreement, prior to the reduction of the current month’s management fee, the General Partner’s administrative fee, the profit share allocation accrual and any redemptions or distributions as of the end of such month. This fee may be increased or decreased at the discretion of the General Partner.

The General Partner, on behalf of the Partnership, has entered into a management agreement (the “Management Agreement”) with the Advisor, a registered commodity trading advisor. The Advisor is not affiliated with the General Partner or CGM and is not responsible for the organization or operation of the Partnership. The Partnership pays the Advisor a monthly management fee equal to 1/6 of 1% (2% per year) of month-end Net Assets allocated to the Advisor. Month-end Net Assets, for the purpose of calculating management fees are Net Assets, as defined in the Limited Partnership Agreement, prior to the reduction of the current month’s management fee, the General Partner’s administrative fee, the profit share allocation accrual and any redemptions or distributions as of the end of such month. The Management Agreement continues in effect until June 30 of each year and is renewable by the General Partner for additional one-year periods upon 30 days prior notice to the Advisor. The Management Agreement may be terminated upon notice by either party.

In addition, the Advisor is a special limited partner (the “Special Limited Partner”) of the Partnership and receives a quarterly profit share allocation to its capital account in the Partnership in the form of units of the Partnership, the value of which shall be equal to 20% of the New Trading Profits, as defined in the Management Agreement, earned by the Advisor on behalf of the Partnership during each calendar quarter and are issued as Special Limited Partner Units. The Advisor will not receive a profit share until the Advisor recovers the net loss incurred and earns additional New Trading Profits for the Partnership.

The Partnership has entered into a customer agreement (the “Customer Agreement”) with CGM which provides that the Partnership will pay CGM a monthly brokerage fee equal to 9/24 of 1% (4.5% per year) of month-end Net Assets, in lieu of brokerage fees on a per trade basis. Month-end Net Assets, for the purpose of calculating brokerage fees are Net Assets, as defined in the Limited Partnership Agreement, prior to the reduction of the current month’s brokerage fees, management fee, the General Partner’s administrative fee, profit share allocation accrual, other expenses and any redemptions or distributions as of the end of such month. The Master will pay for National Futures Association (“NFA”) fees as well as exchange, clearing, service, user, give-up and floor brokerage fees (collectively, the “clearing fees”). CGM will pay a portion of its brokerage fees to other properly registered selling agents and to financial advisors who have sold Redeemable Units. Prior to September 1, 2012 the General Partner paid (out of its own funds) a service fee to CGM. Effective September 1, 2012, the Partnership through its investment in the Master will pay CGM a service fee equal to $1 per round-turn futures transactions, an equivalent amount for swaps and $0.50 per side for options transactions. Brokerage fees will be paid for the life of the Partnership, although the rate at which such fees are paid may be changed. This fee may be increased or decreased at anytime at CGM’s discretion upon written notice to the Partnership. The Partnership’s assets not held in the Master’s account at CGM are held in the Partnership’s account at CGM. The Partnership’s cash is deposited by CGM in segregated bank accounts to the extent required by Commodity Futures Trading Commission (“CFTC”) regulations. CGM will pay the Partnership interest on its allocable share of 80% of the average daily equity maintained in cash in the Master’s brokerage account during each month at a 30-day U.S. Treasury bill rate determined weekly by CGM based on the average noncompetitive yield on 3-month U.S. Treasury bills maturing in 30 days from the date on which such weekly rate is determined. The Customer Agreement between the Partnership and CGM and the Master and CGM gives the Partnership and the Master, respectively, the legal right to net unrealized gains and losses on open futures and forward contracts. The Customer Agreement may be terminated upon notice by either party.

(b) Financial Information about Segments. The Partnership’s business consists of only one segment, speculative trading of commodity interests. The Partnership does not engage in sales of goods or services. The Partnership’s net income (loss) from operations for the years ended December 31, 2012, 2011, 2010, 2009 and 2008 is set forth under “Item 6. Selected Financial Data.” The Partnership’s Capital as of December 31, 2012 was $12,637,042.

(c) Narrative Description of Business.

See Paragraphs (a) and (b) above.

3

(i) through (xii) — Not applicable.

(xiii) — The Partnership has no employees.

(d) Financial Information About Geographic Areas. The Partnership does not engage in the sale of goods or services or own any long-lived assets, and therefore this item is not applicable.

(e) Available Information. The Partnership does not have an internet address. The Partnership will provide paper copies of its annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to these reports free of charge upon request.

(f) Reports to Security Holders. Not applicable.

(g) Enforceability of Civil Liabilities Against Foreign Persons. Not applicable.

(h) Smaller Reporting Companies. Not applicable.

Item 1A. Risk Factors.

As a result of leverage, small changes in the price of the Partnership’s positions may result in major losses.

The trading of commodity interests is speculative, volatile and involves a high degree of leverage. A small change in the market price of a commodity interest contract can produce major losses for the Partnership. Market prices can be influenced by, among other things, changing supply and demand relationships, governmental, agricultural, commercial and trade programs and policies, national and international political and economic events, weather and climate conditions, insects and plant disease, purchases and sales by foreign countries and changing interest rates.

An investor may lose all of its investment.

Due to the speculative nature of trading commodity interests, an investor could lose all of its investment in the Partnership.

The Partnership will pay substantial fees and expenses regardless of profitability.

Regardless of its trading performance, the Partnership will incur fees and expenses, including brokerage and management fees. Fees will be paid to the Advisor even if the Partnership experiences a net loss for the full year.

An investor’s ability to redeem or transfer units is limited.

An investor’s ability to redeem units is limited and no market exists for the units.

Conflicts of interest exist.

The Partnership is subject to numerous conflicts of interest including those that arise from the facts that:

1. The General Partner and the Partnership’s/Master’s commodity broker are affiliates;

2. The Advisor, the Partnership’s/Master’s commodity broker and their respective principals and affiliates may trade in commodity interests for their own accounts; and

3. An investor’s financial advisor will receive ongoing compensation for providing services to the investor’s account.

Investing in units might not provide the desired diversification of an investor’s overall portfolio.

4

One of the Partnership’s objectives is to add an element of diversification to a traditional stock and bond portfolio, but any benefit of portfolio diversification is dependent upon the Partnership achieving positive returns and such returns being independent of stock and bond market returns.

Past performance is no assurance of future results.

The Advisor’s trading strategies may not perform as they have performed in the past. The Advisor has from time to time incurred substantial losses in trading on behalf of clients.

An investor’s tax liability may exceed cash distributions.

Investors are taxed on their share of the Partnership’s income, even though the Partnership does not intend to make any distributions.

Regulatory changes could restrict the Partnership’s operations.

Regulatory changes could adversely affect the Partnership by restricting its markets or activities, limiting its trading and/or increasing the taxes to which investors are subject. Pursuant to the mandate of the Dodd-Frank Wall Street Reform and Consumer Protection Act, signed into law on July 21, 2010, the CFTC and the Securities and Exchange Commission (the “SEC”) have promulgated rules to regulate swaps dealers and to mandate additional reporting and disclosure requirements and continue to promulgate rules regarding capital and margin requirements, to require that swaps be traded on an exchange or swap execution facilities, to mandate additional reporting and disclosure requirements and to require that derivatives (such as those traded by the Partnership) be moved into central clearinghouses. These rules may negatively impact the manner in which swap contracts are traded and/or settled and limit trading by speculators (such as the Partnership) in futures and over-the-counter markets.

Speculative position and trading limits may reduce profitability.

The CFTC and/or U.S. exchanges have established speculative position limits on the maximum net long or net short positions which any person or group of persons may hold or control in particular futures, options on futures and swaps that perform significant price discovery function. Most exchanges also limit the amount of fluctuation in commodity futures contract prices on a single day. The Advisor believes that established speculative position and trading limits will not materially adversely affect trading for the Partnership. The trading instructions of an advisor may have to be modified, and positions held by the Partnership may have to be liquidated, in order to avoid exceeding these limits. Such modification or liquidation could adversely affect the operations and profitability of the Partnership by increasing transaction costs to liquidate positions and foregoing potential profits.

In October 2011, the CFTC adopted new rules governing position limits. In September 2012, these rules were vacated by the United States District Court for the District of Columbia and remanded to the CFTC for further consideration. It is possible, nevertheless, that these rules may take effect in some form via re-promulgation or a successful appeal by the CFTC of the District Court’s ruling. The vacated rules established position limits on certain futures contracts and any economically equivalent futures, options and swaps.

Item 2. Properties.

The Partnership does not own or lease any properties. The General Partner operates out of facilities provided by MSSB Holdings.

5

Item 3. Legal Proceedings.

This section describes the major pending legal proceedings, other than ordinary routine litigation incidental to the business, to which CGM or its subsidiaries is a party or to which any of their property is subject. There are no material legal proceedings pending against the Partnership or the General Partner.

CGM is a New York corporation with its principal place of business at 388 Greenwich St., New York, New York 10013. CGM is registered as a broker-dealer and futures commission merchant (“FCM”), and provides futures brokerage and clearing services for institutional and retail participants in the futures markets. CGM and its affiliates also provide investment banking and other financial services for clients worldwide.

Citigroup Inc., the ultimate parent company to CGM, files annual reports and quarterly reports with the SEC. These reports disclose information about various matters in which Citigroup Inc. and CGM may be parties, including information about any litigation or regulatory investigations. Such annual reports and quarterly reports are available on the website of the SEC (http://www.sec.gov/). Actions with respect to CGM’s futures commission merchant business are publicly available on the website of NFA (http://www.nfa.futures.org/).

There have been no material administrative, civil or criminal actions within the past five years against CGM (formerly known as Salomon Smith Barney) or any of its individual principals and no such actions are currently pending, except as follows.

Enron Corp.

Beginning in 2002, Citigroup, CGM and certain executive officers and current and former employees (along with, in many cases, other investment banks and certain Enron officers and directors, lawyers and/or accountants) were named as defendants in a series of individual and alleged class action lawsuits related to Enron.

On August 27, 2007, the District Court for the Southern District of New York in IN RE ENRON CORP. reversed the rulings of the federal bankruptcy court that certain bankruptcy claims held by Citigroup transferees could be equitably subordinated or disallowed solely because of the alleged misconduct of Citigroup, and remanded for further proceedings.

On April 4, 2008, Citigroup announced an agreement to settle actions filed by Enron in its Chapter 11 bankruptcy proceedings seeking to recover payments to Citigroup as alleged preferences or fraudulent conveyances, to disallow or equitably subordinate claims of Citigroup and Citigroup transferees on the basis of alleged fraud, and to recover damages from Citigroup for allegedly aiding and abetting breaches of fiduciary duty. Under the terms of the settlement, approved by the Bankruptcy Court for the Southern District of New York on April 24, 2008, Citigroup made a pretax payment of $1.66 billion to Enron, and waived certain claims against Enron’s estate. Enron also allowed specified Citigroup-related claims in the bankruptcy proceeding, including all of the bankruptcy claims of parties holding approximately $2.4 billion of Enron credit-linked notes (“CLNs”), and released all claims against Citigroup. Citigroup separately agreed to settle an action brought by certain trusts that issued the CLNs in question, by the related indenture trustee and by certain holders of those securities. The amounts paid to settle these actions were covered by existing Citigroup litigation reserves.

On February 14, 2008, Citigroup agreed to settle CONNECTICUT RESOURCES RECOVERY AUTHORITY v. LAY, ET AL., an action brought by the Attorney General of Connecticut in connection with an Enron-related transaction; subsequently, the District Court dismissed the case on March 5, 2008. The amount paid to settle this action was covered by existing Citigroup litigation reserves.

Over the first two quarters of 2008, Citigroup agreed to settle the following cases, brought by clients of a single law firm in connection with the purchase and holding of Enron securities, and naming Citigroup as a third-party defendant: (1) AHLICH v. ARTHUR ANDERSEN, L.L.P.; (2) DELGADO v. FASTOW; (3) PEARSON v. FASTOW; (4) ROSEN v. FASTOW; (5) BULLOCK v. ARTHUR ANDERSEN, L.L.P.; (6) CHOUCROUN v. ARTHUR ANDERSEN, L.L.P.; (7) GUY v. ARTHUR ANDERSEN, L.L.P. (8) ADAMS v. ARTHUR ANDERSEN, L.L.P.; (9) JOSE v. ARTHUR ANDERSEN, L.L.P.; and (10) ODAM, ET AL., v. ENRON CORP., ET AL. The amount paid to settle these actions was covered by existing Citigroup litigation reserves.

6

On May 23, 2008, Citigroup agreed to settle SILVERCREEK MANAGEMENT INC., ET AL. v. SALOMON SMITH BARNEY, INC. ET AL., and SILVERCREEK MANAGEMENT INC., ET AL. v. CITIGROUP INC., ET AL., two actions brought by investors in Enron debt securities. The amount paid to settle this action was covered by existing Citigroup litigation reserves. On May 30, 2008, the Southern District of Texas approved Citigroup’s settlement of WESTPAC BANKING CORP. v. CITIBANK, N.A., an action arising out of an Enron-related credit derivative transaction between Citibank and the plaintiff. The amount paid to settle this action was covered by existing Citigroup litigation reserves. On July 9, 2008, Citigroup agreed to settle PUBLIC UTILITY DISTRICT NO. 1 OF SNOHOMISH COUNTY, WASHINGTON v. CITIGROUP, ET AL., an action brought by a utility in connection with alleged electricity overcharges by Enron. The amount paid to settle this action was covered by existing Citigroup litigation reserves.

A number of other individual actions have been settled, including, on January 21, 2009, the parties settled VANGUARD BALANCED INDEX FUND, ET AL. v. CITIGROUP, ET AL., an action filed in 2003 in Pennsylvania state court by certain investment funds, and asserting claims under state securities and common law, arising out of plaintiffs’ purchase of certain Enron-related securities. The case had been coordinated with NEWBY, ET AL. v. ENRON CORP., ET AL., which was settled in 2006, until it was remanded to the United States District Court for the Eastern District of Pennsylvania in June 2008. Pursuant to the settlement, the case was voluntarily dismissed on February 4, 2009.

On May 14, 2009, a settlement agreement was executed among the parties in D K ACQUISITION PARTNERS, L.P., ET AL. v. J.P. MORGAN CHASE & CO., ET AL. and AVENUE CAPITAL MANAGEMENT II, L.P., ET AL. v. J.P. MORGAN CHASE & CO., ET AL. On June 3, 2009, a settlement agreement was executed among the parties in UNICREDITO ITALIANO, SpA, ET AL. v. J.P. MORGAN CHASE BANK, ET AL. The three actions, which were consolidated and pending trial in the United States District Court for the Southern District of New York, were brought against Citigroup and certain of its affiliates, and JPMorgan Chase and certain of its affiliates, in their capacity as co-agents on certain Enron revolving credit facilities. Pursuant to the settlements, the cases were dismissed with prejudice.

WorldCom, Inc.

Beginning in 2002, Citigroup, CGM and certain executive officers and current and former employees were named as defendants—along with twenty-two other investment banks, certain current and former WorldCom officers and directors, and WorldCom’s former auditors—in a consolidated class action (IN RE WORLDCOM, INC. SECURITIES LITIGATION) brought on behalf of individuals and entities who purchased or acquired publicly traded securities of WorldCom between April 29, 1999 and June 25, 2002. The class settlement became final in March 2006.

Following the resolution of all other individual actions by settlements and other resolutions, one individual action remains pending on appeal in the Second Circuit, HOLMES, et al. v. GRUBMAN, et al., which was brought by an individual and entities who opted out of the WorldCom securities class action settlement. On October 13, 2006, this action was dismissed with prejudice by the District Court for the Southern District of New York. On June 3, 2009, the Second Circuit certified certain state law questions to be resolved by the Georgia Supreme Court, which has issued an opinion answering those questions. The Second Circuit has not yet decided the appeal. On June 23, 2010, the Second Circuit affirmed the dismissal of the remaining claims in HOLMES v. GRUBMAN. Petitioners-plaintiffs submitted a petition for certiorari to the United States Supreme Court seeking review of the decision of the Second Circuit, affirming dismissal of the action.

Research

Customer Class Actions

In March 2004, an alleged research-related customer class action alleging various state law claims on behalf of Smith Barney customers arising out of the issuance of allegedly misleading research analyst reports, DISHER v. CITIGROUP GLOBAL MARKETS INC., was filed in Illinois state court. Citigroup removed this action to federal court, and in August 2005 the United States Court of Appeals for the Seventh Circuit reversed the District Court’s August 2004 order remanding the case to state court, and directed the District Court to dismiss plaintiffs’ claims as preempted. On June 26, 2006, the United States Supreme Court granted plaintiffs’ petition for a writ of certiorari, vacated the Seventh Circuit’s opinion and remanded the case to the Seventh Circuit for further

7

proceedings in light of the Supreme Court’s decision in Kircher v. Putnam Funds Trust. On January 22, 2007, the Seventh Circuit dismissed Citigroup’s appeal from the District Court’s removal order for lack of appellate jurisdiction. On February 1, 2007, plaintiffs secured an order reopening this case in Illinois state court, and on February 16, Citigroup removed the reopened action to federal court. On March 2, 2007, the District Court vacated its 2005 order dismissing the case and remanded the action to Illinois state court. On May 3, 2007, the District Court remanded the action to Illinois state court, and on June 13, 2007, Citigroup moved in state court to dismiss the action. On October 13, 2011, the court entered an order dismissing with prejudice all class action claims asserted in DISHER v. CITIGROUP GLOBAL MARKETS INC., holding that the claims were precluded under the Securities Litigation Uniform Standards Act of 1998. The court granted leave for lead plaintiff to file an amended complaint asserting only his individual state-law claims within 21 days. An amended complaint was not filed within the 21-day period. The alleged representative plaintiff has filed a notice of appeal from the court’s October 13, 2011 order. On February 3, 2012, the Illinois Appellate Court dismissed plaintiff’s appeal in DISHER v. CITIGROUP GLOBAL MARKETS INC. for lack of a final, appealable judgment, and the Circuit Court entered a final judgment dismissing the action on February 14, 2012. No appeal from that judgment has been filed.

Global Crossing, Ltd.

On or about January 28, 2003, lead plaintiff in a consolidated alleged class action in the United States District Court for the Southern District of New York (IN RE GLOBAL CROSSING, LTD. SECURITIES LITIGATION) filed a consolidated complaint on behalf of purchasers of the securities of Global Crossing and its subsidiaries, which named as defendants, among others, Citigroup, CGM and certain executive officers and current and former employees, asserting claims under the federal securities laws for allegedly issuing research reports without a reasonable basis in fact and for allegedly failing to disclose conflicts of interest with Global Crossing in connection with published investment research. On March 22, 2004, lead plaintiff amended its consolidated complaint to add claims on behalf of purchasers of the securities of Asia Global Crossing. The added claims asserted causes of action under the federal securities laws and common law in connection with CGM’s research reports about Global Crossing and Asia Global Crossing and for CGM’s roles as an investment banker for Global Crossing and as an underwriter in the Global Crossing and Asia Global Crossing offerings. The Citigroup-Related Defendants moved to dismiss all of the claims against them on July 2, 2004. The plaintiffs and the Citigroup-Related Defendants entered into a settlement agreement that was preliminarily approved by the Court on March 8, 2005, and was finally approved on June 30, 2005. The amount to be paid in settlement is covered by existing litigation reserves.

In addition, on or about January 27, 2004, the Global Crossing Estate Representative filed in the United States Bankruptcy Court for the Southern District of New York an adversary proceeding against Citigroup and several other financial institutions seeking to rescind the payment of a $1 billion loan made to a subsidiary of Global Crossing. The Citigroup-Related Defendants moved to dismiss the latter action on May 28, 2004, which motion remains pending. In addition, actions asserting claims against Citigroup and certain of its affiliates relating to CGM Global Crossing research reports are pending in numerous arbitrations around the country. On August 20, 2008, Plaintiff filed an amended complaint that narrowed the pending claims. Citigroup has yet to respond to the amended complaint.

Telecommunications Research Class Actions

Beginning in May 2002, Citigroup, CGM and certain executive officers and current and former employees were named as defendants in a series of alleged class action lawsuits and arbitration demands by purchasers of various securities, alleging violations of the federal securities laws, including Sections 10 and 20 of the Securities Exchange Act of 1934 for allegedly issuing research reports without a reasonable basis in fact and for allegedly failing to disclose conflicts of interest with companies in connection with published investment research. The Citigroup research analyst reports concerned seven issuers: AT&T Corp. (“AT&T”), Winstar Communications, Inc. (“Winstar”), Level 3 Communications, Inc. (“Level 3”), Metromedia Fiber Network, Inc. (“MFN”), XO Communications, Inc. (“XO”), Williams Communications Group Inc. (“Williams”), and Focal Communications, Inc. (“Focal”). These alleged class actions were assigned to a single judge in the United States District Court for the Southern District of New York for coordinated proceedings. The court consolidated these actions into seven separate proceedings corresponding to the seven issuers of securities involved.

8

On January 6, 2005, the District Court granted in part and denied in part Citigroup’s motion to dismiss the claims against it in the MFN action, In re SALOMON ANALYST METROMEDIA LITIGATION. On June 20, 2006, the District Court certified the plaintiff class in the M FN action. The District Court’s class certification decision is on appeal in the United States Court of Appeals for the Second Circuit, and oral argument was held in January 2008. On September 30, 2008, the District Court’s class certification decision was vacated on appeal by the United States Court of Appeals for the Second Circuit. On October 1, 2008, the parties reached a settlement pursuant to which Citigroup will pay $35 million to members of the settlement class that purchased or otherwise acquired MFN securities during the class period; the settlement was preliminarily approved by the District Court on November 19, 2008. On February 27, 2009, the District Court approved the class action settlement, and entered a final judgment dismissing the action with prejudice.

Credit-Crisis-Related Litigation and Other Matters

Citigroup and certain of its subsidiaries have been named as defendants in numerous legal actions and other proceedings asserting claims for damages and related relief for losses arising from the global financial credit and subprime-mortgage crisis that began in 2007. Such matters include, among other types of proceedings, claims asserted by: (i) individual investors and purported classes of investors in Citigroup’s common and preferred stock and debt, alleging violations of the federal securities laws, foreign laws, state securities and fraud law, and the Employee Retirement Income Security Act (“ERISA”); (ii) individual investors and purported classes of investors in, and issuers of, auction rate securities alleging violations of the federal securities and antitrust laws; (iii) counterparties to significant transactions adversely affected by developments in the credit and subprime markets; (iv) individual investors and purported classes of investors in securities and other investments underwritten, issued or marketed by Citigroup, including securities issued by other public companies, collateralized debt obligations (“CDOs”), mortgage-backed securities (“MBS”), auction-rate securities (“ARS”), investment funds, and other structured or leveraged instruments, which have suffered losses as a result of the credit crisis; (v) municipalities, related entities and individuals asserting public nuisance claims; and (vi) individual borrowers asserting claims related to their loans. These matters have been filed in state and federal courts across the U.S. and in foreign tribunals, as well as in arbitrations before Financial Industry Regulatory Authority (“FINRA”) and other arbitration associations.

In addition to these litigations and arbitrations, Citigroup continues to cooperate fully in response to subpoenas and requests for information from the SEC, FINRA, the Federal Housing Finance Agency (“FHFA”) , state attorneys general, the Department of Justice and subdivisions thereof, bank regulators, and other federal and state government agencies and authorities in connection with various formal and informal (and, in many instances, industry-wide) inquiries concerning Citigroup’s subprime and other mortgage-related conduct and business activities, as well as other business activities affected by the credit crisis. These business activities include, but are not limited to, Citigroup’s sponsorship, packaging, issuance, marketing, servicing, and underwriting of CDOs and MBS, and its origination, sale or other transfer, servicing, and foreclosure of residential mortgages.

Regulatory Actions: On October 19, 2011, in connection with its industry wide investigation concerning CDO-related business activities, the SEC filed a complaint in the United States District Court for the Southern District of New York regarding Citigroup’s structuring and sale of the Class V Funding III CDO transaction (“Class V”), which alleged that CGM negligently failed to disclose in the Class V offering documents that CGM played a role in the asset selection process for the transaction and retained a short position in certain of those assets. On the same day, the SEC and Citigroup announced a settlement of the SEC’s claims, subject to judicial approval, and the SEC filed a proposed final judgment pursuant to which Citigroup’s U.S. broker-dealer CGM agreed to disgorge $160 million and to pay $30 million in prejudgment interest and a $95 million penalty. On November 28, 2011, the district court issued an order refusing to approve the proposed settlement and ordering trial to begin on July 16, 2012. On December 15 and 19, 2011, respectively, the SEC and CGM filed notices of appeal from the district court’s November 28 order. On December 27, 2011, the United States Court of Appeals for the Second Circuit granted an emergency stay of further proceedings in the district court, pending the Second Circuit’s ruling on the SEC’s motion to stay the district court proceedings during the pendency of the appeals. On March 15, 2012, the United States Court of Appeals for the Second Circuit granted a stay of the district court proceedings pending resolution of the appeals in SEC v. CGM.

9

Federal and state regulators, including the SEC, also have served subpoenas or otherwise requested information related to Citigroup’s issuing, sponsoring, or underwriting of MBS. These inquiries include a subpoena from the Civil Division of the Department of Justice that Citigroup received on January 27, 2012.

Subprime Mortgage–Related Litigation and Other Matters

Beginning in November 2007, Citigroup and a number of current and former officers, directors, and employees have been named as defendants in a variety of class action and individual securities lawsuits brought by Citigroup shareholders, investors in Citigroup’s equity and debt securities, counterparties and others concerning Citigroup’s activities relating to subprime mortgages, including Citigroup’s disclosures regarding its exposure to CDOs, MBS, and structured investment vehicles (“SIVs”), Citigroup’s underwriting activity for subprime mortgage lenders, and Citigroup’s more general involvement in subprime- and credit-related activities.

Securities Actions:

On September 30 and October 28, 2008, Citigroup, certain Citigroup entities, certain current and former directors and officers of Citigroup and Citigroup Funding, Inc., and certain underwriters of Citigroup notes (including CGM) were named as defendants in two alleged class actions filed in New York state court but since removed to the United States District Court for the Southern District of New York. These actions allege violations of Sections 11, 12, and 15 of the Securities Act of 1933, as amended, arising out of forty-eight corporate debt securities, preferred stock, and interests in preferred stock issued by Citigroup and related issuers over a two-year period from 2006 to 2008. On December 10, 2008, these two actions were consolidated under the caption IN RE CITIGROUP INC. BOND LITIGATION, and lead plaintiff and counsel were appointed. On January 15, 2009, plaintiffs filed a consolidated class action complaint.

On March 13, 2009, defendants filed a motion to dismiss the complaint. On July 12, 2010, the court issued an opinion and order dismissing plaintiffs’ claims under Section 12 of the Securities Act of 1933, as amended, as amended, but denying defendants’ motion to dismiss certain claims under Section 11. On September 30, 2010, the district court entered a scheduling order in IN RE CITIGROUP INC. BOND LITIGATION. Fact discovery began in November 2010, and plaintiffs’ motion to certify a class is pending. Plaintiffs have not yet quantified the alleged class’ alleged damages. Because of the preliminary stage of the proceedings, Citigroup cannot at this time estimate the possible loss or range of loss, if any, for this action or predict the timing of its eventual resolution.

On March 13 and 16, 2009, two cases were filed in the United States District Court for the Southern District of New York alleging violations of the Securities Act of 1933, as amended -BUCKINGHAM v. CITIGROUP INC., ET AL. and CHEN v. CITIGROUP INC., ET AL. and were later designated as related to IN RE CITIGROUP INC. BOND LITIGATION. On May 7, 2009, BUCKINGHAM and CHEN were consolidated with IN RE CITIGROUP INC. BOND LITIGATION.

On April 9, 2009, another case asserting violations of the Securities Act of 1933, as amended -PELLEGRINI v. CITIGROUP INC., ET AL.-was filed in the United Stated District Court for the Southern District of New York and the parties have jointly requested that the PELLEGRIN I action be designated as related to IN RE CITIGROUP INC. SECURITIES LITIGATION and IN RE CITIGROUP INC. BOND LITIGATION. On May 11, 2009, an alleged class action ASHER, ET AL. v. CITIGROUP INC., ET AL. was filed in the United States District Court for the Southern District of New York alleging violations of the Securities Act of 1933, as amended in connection with plaintiffs’ investments in certain offerings of preferred stock issued by Citigroup. On May 15, 2009, plaintiffs in IN RE CITIGROUP INC. BOND LITIGATION requested that ASH ER and PELLEGRINI be consolidated with IN RE CITIGROU P INC. BOND LITIGATION. On August 31, 2009, ASH ER and PELLEGRINI were consolidated with IN RE CITIGROUP INC. BOND LITIGATION.

On March 23, 2009, a case was filed in the United States District Court for the Southern District of California alleging violations of both the Securities Act of 1933, as amended and the Securities Exchange Act of 1934- BRECHER v. CITIGROUP INC., ET AL. On April 16, 2009, Citigroup filed a motion before the Judicial Panel on Multidistrict Litigation for transfer of the BRECHER action to the Southern District of New York for coordinated pre-trial proceedings with IN RE CITIGROUP INC. SECURITIES LITIGATION and IN RE CITIGROUP INC. BOND LITIGATION. On August 7, 2009, the Judicial Panel on Multidistrict Litigation transferred BRECHER, ET AL. v. CITIGROUP INC., ET AL. to the Southern District of New York for coordination with IN RE CITIGROUP INC. SECURITIES LITIGATION.

10

On April 17, 2009, an alleged class action BRECHER, ET AL. v. CGM, ET AL. was filed in California state court asserting claims against Citigroup, CGM, and certain of the Citigroup’s current and former directors under California’s Business and Professions Code and Labor Code, as well as under California common law, relating to, among other things, losses incurred on common stock awarded to Smith Barney financial advisors in connection with the execution of their employment contracts. On May 19, 2009, an amended complaint was filed. On July 9, 2009, the Judicial Panel on Multidistrict Litigation was notified that BRECHER, ET AL. v. CGM, ET AL. is a potential tag-along action to IN RE CITIGROUP, INC. SECURITIES LITIGATION. On July 15, 2009, after having removed the case to the United States District Court for the Southern District of California, defendants filed motions to dismiss the complaint and to stay all further proceedings pending resolution of the tag-along petition. On July 22, 2009, plaintiffs in BRECHER, ET AL. v. CGM, ET AL. voluntarily dismissed the claims against the individual defendants and moved to remand the remaining action against Citigroup, CGM, and the Personnel and Compensation Committee to state court. On September 8, 2009, the United States District Court for the Southern District of California ordered that defendants show cause as to why there was federal jurisdiction over the case. On September 17, 2009, defendants responded to the district court’s order.

On August 19, 2009, KOCH, ET AL. v. CITIGROUP INC., ET AL., an alleged class action, was filed in the United States District Court for the Southern District of California on behalf of participants in Citigroup’s Voluntary FA Capital Accumulation Program (“FA CAP Program”) against various defendants, including Citigroup and CGM, asserting claims under the Securities Act of 1933, as amended, the Securities Exchange Act of 1934, and Minnesota state law in connection with plaintiffs’ acquisition of certain securities through the FA CAP Program. On September 30, 2009, the Judicial Panel on Multidistrict Litigation conditionally transferred KOCH to the United States District Court for the Southern District of New York as a potential tag-along to IN RE CITIGROUP INC. SECURITIES LITIGATION. On October 8, 2009, a consolidated amended complaint was filed in BRECHER, ET AL. v. CITIGROUP INC., ET AL. in the United States District Court for the Southern District of New York, asserting claims under the federal securities laws and Minnesota and California state law. The complaint purports to consolidate the similar claims asserted in KOCH.

In the consolidated action, lead plaintiffs assert claims on behalf of an alleged class of participants in Citigroup’s Voluntary Financial Advisor Capital Accumulation Plan from November 2006 through January 2009. On June 7, 2011, the district court granted defendants’ motion to dismiss the complaint and subsequently entered judgment. On November 14, 2011, the district court granted in part plaintiffs’ motion to alter or amend the judgment and granted plaintiffs leave to amend the complaint. On November 23, 2011, plaintiffs filed an amended complaint alleging violations of Section 12 of the Securities Act of 1933, as amended and Section 10(b) of the Securities Exchange Act of 1934. Defendants filed a motion to dismiss certain of plaintiffs’ claims on December 21, 2011.

Several institutions and sophisticated investors that purchased debt and equity securities issued by Citigroup and related issuers have also filed actions on their own behalf against Citigroup and certain of its subsidiaries in the Southern District of New York and the Court of Common Pleas for Philadelphia County. These actions assert claims similar to those asserted in the IN RE CITIGROUP INC. SECURITIES LITIGATION and IN RE CITIGROUP INC. BOND LITIGATION actions described above. Collectively, these investors seek damages exceeding $1 billion. On June 8, 2012, defendants filed an interlocutory appeal in the United States Court of Appeals for the Second Circuit from the district court’s decision in INTERNATIONAL FUND MANAGEMENT S.A., ET AL. v. CITIGROUP INC., ET AL., holding that the tolling doctrine set forth in American Pipe & Construction Co. v. Utah, 414 U.S. 538 (1974), applies to the statute of repose in the Securities Act of 1933, as amended.

Other Matters:

Underwriting Actions. In its capacity as a member of various underwriting syndicates, CGM also has been named as a defendant in several subprime-related actions asserted against various issuers of debt and other securities. Most of these actions involve claims asserted on behalf of alleged classes of purchasers of securities for alleged violations of Sections 11 and 12(a)(2) of the Securities Act of 1933, as amended.

11

AIG. Beginning in October 2008, four alleged class actions were filed in the United States District Court for the Southern District of New York by American International Group, Inc. (“AIG”) investors and shareholders. These actions allege violations of Sections 11, 12, and 15 of the Securities Act of 1933, as amended arising out of allegedly false and misleading statements contained in the registration statements and prospectuses issued in connection with offerings of AIG debt securities and common stock, some of which were underwritten by CGM. On March 20, 2009, the four alleged class actions were consolidated by the United States District Court for the Southern District of New York under the caption IN RE AMERICAN INTERNATIONAL GROUP, INC. 2008 SECURITIES LITIGATION. Plaintiffs filed a consolidated amended complaint on May 19, 2009, which includes two Citigroup affiliates among the underwriter defendants. On August 5, 2009, the underwriter defendants, including CGM and CGML, moved to dismiss the consolidated amended complaint.

Ambac Financial Group. On May 9, 2008, four alleged class actions brought by shareholders of Ambac Financial Group, Inc., pending in the United States District Court for the Southern District of New York, were consolidated under the caption IN RE AMBAC FINANCIAL GROUP, INC. SECURITIES LITIGATION. On August 22, 2008, plaintiffs filed a consolidated amended class action complaint alleging violations of Sections 11 and 12 of the Securities Act of 1933, as amended arising out of allegedly false and misleading statements contained in the registration statements and prospectuses issued in connection with offerings of Ambac securities, some of which were underwritten by CGM. Defendants filed a motion to dismiss the complaint on October 21, 2008. On December 3, 2010, plaintiffs and the underwriter defendants, including Citigroup, entered into a memorandum of understanding settling all claims against Citigroup subject to the entry of a final stipulation of settlement and court approval. On May 6, 2011, plaintiffs and the underwriter defendants, including Citigroup, in IN RE AMBAC FINANCIAL GROUP, INC. SECURITIES LITIGATION signed formal stipulations of settlement, which were submitted to the court for preliminary approval. On June 14, 2011, the court entered an order preliminarily approving the proposed settlement. On September 28, 2011, the district court approved the settlement between plaintiffs and defendants, including Citigroup, in IN RE AMBAC FINANCIAL GROUP INC. SECURITIES LITIGATION and judgment was entered. A member of the settlement class has appealed the judgment to the United States Court of Appeals for the Second Circuit. On December 22, 2011, the underwriter defendants moved to dismiss the appeal. On March 21, 2012, the United States Court of Appeals for the Second Circuit granted the underwriters, motion to dismiss an appeal seeking to challenge the district court’s approval of the underwriters, settlement of IN RE AMBAC FINANCIAL GROUP, INC. SECURITIES LITIGATION.

American Home Mortgage. On March 21, 2008, 19 alleged class actions brought by shareholders of American Home Mortgage Investment Corp., pending in the United States District Court for the Eastern District of New York, were consolidated under the caption IN RE AMERICAN HOME MORTGAGE SECURITIES LITIGATION. On June 3, 2008, plaintiffs filed a consolidated amended complaint, alleging violations of Sections 11 and 12 of the Securities Act of 1933, as amended arising out of allegedly false and misleading statements contained in the registration statements and prospectuses issued in connection with two offerings of American Home Mortgage securities underwritten by CGM, among others. Defendants, including Citigroup and CGM, filed a motion to dismiss the complaint on September 12, 2008. On July 7, 2009, lead plaintiffs filed a motion for preliminary approval of settlements reached with all defendants (including Citigroup and CGM). On July 31, 2009, the District Court entered an order preliminarily approving settlements reached with all defendants (including Citigroup and CGM).

On July 27, 2009, UTAH RETIREMENT SYSTEMS v. STRAUSS, ET AL. was filed in the United States District Court for the Eastern District of New York asserting, among other claims, claims under the Securities Act of 1933, as amended and Utah state law arising out of an offering of American Home Mortgage common stock underwritten by CGM. This matter has been settled.

Countrywide. Citigroup has been named in several alleged class actions lawsuits alleging violations of Section 11 and 12 of the Securities Act of 1933, as amended relating to its role as one of numerous underwriters of offerings of securities and mortgage pass-through certificates issued by Countrywide. The lawsuits include a consolidated action filed in the United States District Court for the Central District of California and two other lawsuits pending in the Superior Court of the California, Los Angeles County.

12

Lehman. Citigroup has been named in several alleged class action lawsuits alleging violations of Section 11 and 12 of the Securities Act of 1933, as amended relating to its role as one of numerous underwriters of offerings of securities issued by Lehman Brothers. The lawsuits are currently pending in the United States District Courts for the Southern District of New York, the Eastern District of New York and the Eastern and Western Districts of Arkansas. On May 2, 2012, the United States District Court for the Southern District of New York entered a judgment approving a stipulation of settlement with the underwriter defendants, including Citigroup, in IN RE LEHMAN BROTHERS EQUITY/DEBT SECURITIES LITIGATION.

Fannie Mae. Beginning in August 2008, CGM, along with a number of other financial institutions, was named as a defendant in eight complaints filed by shareholders of Federal National Mortgage Association (“Fannie Mae”) in connection with the underwriting of three offerings of Fannie Mae stock during 2007 and 2008. CGM, along with the other defendants, moved to dismiss three of the suits that alleged violations of Section 12(a)(2) of the Securities Act of 1933, as amended. The remaining actions allege violations of Section 10(b) of the Securities Exchange Act. On January 29, 2009, the U.S. Judicial Panel on Multidistrict Litigation heard oral argument on whether all lawsuits pending against CGM and several other lawsuits pending against other defendants should be consolidated.

Freddie Mac. CGM, along with a number of other financial institutions, has been named as a defendant in two lawsuits pending in the United States District Court for the Southern District of New York brought by Freddie Mac shareholders who purchased preferred shares traceable to a November 2007 offering of Z Preferred Shares. Plaintiffs allege violations of Section 12(a)(2) of the Securities Act of 1933, as amended and Section 10(b) of the Securities Exchange Act of 1934 because the offering materials failed to disclose Freddie Mac’s exposure to mortgage-related losses, poor underwriting procedures and risk management, and the resulting negative impact to Freddie’s capital.

Discrimination in Lending Actions. Two alleged class actions have been filed alleging claims of racial discrimination in mortgage lending under the Equal Credit Opportunity Act, the Fair Housing Act, and/or the Civil Rights Act. The first action, PUELLO, ET AL. v. CITIFINANCIAL SERVICES, INC., ET AL., was filed against Citigroup and its affiliates in the United States District Court for the District of Massachusetts. The second action, NAACP v. AMERIQUEST MORTGAGE CO., ET AL., was filed against one of Citigroup’s affiliates in the United States District Court for the Central District of California. In each action, defendants’ motions to dismiss have been denied. On September 21, 2009, the United States District Court for the Central District of California denied defendant CitiMortgage’s motion for summary judgment and granted its motion to strike the jury demand.

Counterparty and Investor Actions. Citigroup and certain of its subsidiaries have been named as defendants in actions brought by counterparties and investors that have suffered losses as a result of the credit crisis. Those actions include claims asserted by investors in CDO-related transactions, including Moneygram Payment Systems, Inc., which filed a lawsuit in Minnesota state court on October 26, 2011, alleging misstatements in connection with the sale of CDO securities.

Ambac: Counterparties to transactions involving CDOs, SIVs, credit default swaps (“CDS”), and other instruments related to investments in MBS have sued Citigroup on a variety of theories. On August 3, 2009, one such counterparty filed an action—AMBAC CREDIT PRODUCTS, LLC v. CITIGROUP INC., et al. —in New York Supreme Court, County of New York, alleging various claims including fraud and breach of fiduciary duty in connection with Citigroup’s purchase of CDS from Ambac as credit protection for a $1.95 billion super-senior tranche of a CDO structured by Citigroup, the underlying assets of which allegedly included subprime MBS. Ambac alleges, among other things, that Citigroup misrepresented the nature of the risks that were being transferred. On October 7, 2009, defendants filed a motion to dismiss the complaint. On June 7, 2010, in connection with a global settlement agreement between Ambac and Citigroup, the parties stipulated to a discontinuation with prejudice.

In August 2011, two Saudi nationals and related entities commenced a FINRA arbitration against CGM alleging $380 million in losses resulting from certain options trades referencing a portfolio of hedge funds and certain credit facilities collateralized by a private equity portfolio. CGM did not serve as the counterparty or credit facility provider in these transactions. In September 2011, CGM commenced an action in the United States District Court for the Southern District of New York seeking to enjoin the arbitration. Simultaneously with that filing, the Citigroup entities that served as the counterparty or credit facility provider to the transactions commenced actions in London and Switzerland for declaratory judgments of no liability.

13

RMBS Litigation and Other Matters

Beginning in July 2010, Citigroup and certain of its subsidiaries have been named as defendants in complaints filed by purchasers of MBS and CDOs sold or underwritten by Citigroup. The MBS-related complaints generally assert that the defendants made material misrepresentations and omissions about the credit quality of the mortgage loans underlying the securities, such as the underwriting standards to which the loans conformed, the loan-to-value ratio of the loans, and the extent to which the mortgaged properties were owner-occupied, and typically assert claims under Section 11 of the Securities Act of 1933, as amended, state blue sky laws, and/or common-law misrepresentation-based causes of action. The CDO-related complaints further allege that the defendants adversely selected or permitted the adverse selection of CDO collateral without full disclosure to investors. The plaintiffs in these actions generally seek rescission of their investments, recovery of their investment losses, or other damages. Other purchasers of MBS and CDOs sold or underwritten by Citigroup have threatened to file additional suits, for some of which Citigroup has agreed to toll (extend) the statute of limitations.

The filed actions generally are in the early stages of proceedings, and certain of the actions or threatened actions have been resolved through settlement or otherwise. The aggregate original purchase amount of the purchases at issue in the filed suits is approximately $10.8 billion, and the aggregate original purchase amount of the purchases covered by tolling agreements with investors threatening litigation is approximately $6.4 billion. The largest MBS investor claim against Citigroup and certain of its subsidiaries, as measured by the face value of purchases at issue, has been asserted by the FHFA, as conservator for Fannie Mae and Freddie Mac. This suit was filed on September 2, 2011, and has been coordinated in the United States District Court for the Southern District of New York with fifteen other related suits brought by the same plaintiff against various other financial institutions. Motions to dismiss in the coordinated suits have been denied in large part, and discovery is proceeding. An interlocutory appeal currently is pending in the United States Court of Appeals for the Second Circuit on issues common to all of the coordinated suits.

On July 14, 2011, plaintiff filed an amended complaint in FEDERAL HOME LOAN BANK OF INDIANAPOLIS v. BANC OF AMERICA MORTGAGE SECURITIES, INC., ET AL., which no longer names Citigroup or any of its affiliates as defendants.

On September 2, 2011, the FHFA filed four lawsuits against Citigroup and certain of its subsidiaries alleging actionable misstatements or omissions in connection with the issuance and/or underwriting of residential mortgage-backed securities. The FHFA has asserted similar claims against numerous other financial institutions. The FHFA seeks rescission of investments made by Fannie Mae and Freddie Mac, and/or other damages. On May 4, 2012, the district court in FEDERAL HOUSING FINANCE AGENCY v. UBS AMERICAS, INC., ET AL., a parallel case to FEDERAL HOUSING FINANCE AGENCY v. ALLY FINANCIAL INC., ET AL., FEDERAL HOUSING FINANCE AGENCY v. CITIGROUP INC., ET AL., and FEDERAL HOUSING FINANCE AGENCY v. JPMORGAN CHASE & CO., ET AL., denied defendants’ motion to dismiss plaintiff’s securities law claims and granted defendants’ motion to dismiss plaintiff’s negligent misrepresentation claims. On June 19, 2012, the district court granted defendants’ motion to certify an interlocutory appeal to the United States Court of Appeals for the Second Circuit from the court’s statutes of repose and limitations rulings. On August 14, 2012, a motions panel of the United States Court of Appeals for the Second Circuit granted defendants’ motion for leave to appeal from the district court’s denial of defendants’ motion to dismiss in FEDERAL HOUSING FINANCE AGENCY v. UBS AMERICAS, INC., ET AL., a parallel case to FEDERAL HOUSING FINANCE AGENCY v. ALLY FINANCIAL INC., ET AL., FEDERAL HOUSING FINANCE AGENCY v. CITIGROUP INC., ET AL., and FEDERAL HOUSING FINANCE AGENCY v. JPMORGAN CHASE & CO., ET AL.

On September 9, 2011, the Western & Southern Life Insurance Company and other entities filed an amended complaint against CGM, as well as other financial institutions, alleging actionable misstatements or omissions in connection with the sale of residential mortgage-backed securities. On June 6, 2012, the court granted in part and denied in part defendants’ motions to dismiss in WESTERN & SOUTHERN LIFE INS. CO., ET AL. v. RESIDENTIAL FUNDING CO., LLC, ET AL.

On January 27, 2012, in THE CHARLES SCHWAB CORP. v. BNP PARIBAS SECURITIES CORP., ET AL., the court overruled the demurrers as to all claims involving Citigroup. Plaintiff filed an amended complaint on April 5, 2012.

14

On May 15, 2012, Woori Bank filed a complaint in the United States District Court for the Southern District of New York against Citigroup and certain of its subsidiaries alleging actionable misstatements and omissions in connection with Woori Bank’s $95 million investment in five CDOs.

On May 18, 2012, the Federal Deposit Insurance Corporation filed complaints in the United States District Courts for the Southern District of New York and the Central District of California against various defendants, including CGM, Citicorp Mortgage Securities Inc., and CitiMortgage Inc., in connection with purchases of RMBS by two failed banks for which the FDIC is acting as receiver.

On June 26, 2012, the court overruled defendants’ demurrer to plaintiff’s amended complaint in FEDERAL HOME LOAN BANK OF CHICAGO v. BANC OF AMERICA SECURITIES, LLC, ET AL.

On July 27, 2012, John Hancock Life Insurance Co. and several affiliated entities filed a complaint in the United States District Court for the District of Minnesota against various defendants, including CGM, asserting disclosure claims arising out of purchases of RMBS.

On July 27, 2012, Royal Park Investments SA/NV filed a summons with notice in New York Supreme Court against various defendants, including Citigroup and certain of its subsidiaries, asserting disclosure claims arising out of purchases of RMBS.

On August 10, 2012, the FDIC filed complaints in the Alabama Circuit Court of Montgomery County and the United States District Courts for the Southern District of New York and the Central District of California against various defendants, including Citigroup and certain of its subsidiaries, asserting disclosure claims arising out of RMBS purchases by a failed bank for which the FDIC is acting as receiver.

On September 5, 2012, IKB International S.A. and IKB Deutsche Industriebank AG filed a summons with notice in New York Supreme Court against Citigroup and certain of its subsidiaries.

On September 19, 2012, the Illinois state court denied defendants’ motions to dismiss in FEDERAL HOME LOAN BANK OF CHICAGO v. BANC OF AMERICA FUNDING CORP., ET AL.

On September 28, 2012, the Massachusetts state court denied in part and granted in part defendants’ motion to dismiss in CAMBRIDGE PLACE INVESTMENT MANAGEMENT, INC. v. MORGAN STANLEY & CO., INC., ET AL.

On October 15, 2012, the United States District Court for the Southern District of New York granted lead plaintiffs’ amended motion for class certification in NEW JERSEY CARPENTERS HEALTH FUND V. RESIDENTIAL CAPITAL LLC, ET AL., having previously denied lead plaintiffs’ motion for class certification on January 18, 2011. Plaintiffs in this action allege violations of Sections 11, 12, and 15 of the Securities Act of 1933, as amended and assert disclosure claims on behalf of an alleged class of purchasers of mortgage-backed securities issued by Residential Accredited Loans, Inc. pursuant or traceable to prospectus materials filed on March 3, 2006 and April 3, 2007. CGM is one of the underwriter defendants.

Other purchasers of residential mortgage-backed securities sold or underwritten by affiliates of Citigroup affiliates have threatened to file lawsuits asserting similar claims, some of which Citigroup has agreed to toll pending further discussions with those investors.

In addition to these actions, various parties to MBS securitizations and other interested parties have asserted that certain affiliates of Citigroup breached representations and warranties made in connection with mortgage loans sold into securitization trusts (private-label securitizations). In connection with such assertions, Citigroup has received significant levels of inquiries and demands for loan files, as well as requests to toll (extend) the applicable statutes of limitation for, among others, representation and warranty claims relating to its private-label securitizations. These inquiries, demands and requests have come from trustees of securitization trusts and others.

15

Among these requests, in December 2011, Citigroup received a letter from the law firm Gibbs & Bruns LLP, which purports to represent a group of investment advisers and holders of MBS issued or underwritten by affiliates of Citigroup. Through that letter and subsequent discussions, Gibbs & Bruns LLP has asserted that its clients collectively hold certificates in 87 MBS trusts purportedly issued and/or underwritten by affiliates of Citigroup, and that affiliates of Citigroup have repurchase obligations for certain mortgages in these trusts. Given the continued and increased focus on mortgage-related matters, as well as the increasing level of litigation and regulatory activity relating to mortgage loans and mortgage-backed securities, the level of inquiries and assertions respecting securitizations may further increase. These inquiries and assertions could lead to actual claims for breaches of representations and warranties, or to litigation relating to such breaches or other matters.

Auction-rate Securities-Related Litigation and Other Matters

Beginning in March 2008, Citigroup and certain of its subsidiaries have been named as defendants in numerous actions and proceedings brought by Citigroup shareholders and purchasers or issuers of ARS, asserting claims under the federal securities laws, Section 1 of the Sherman Antitrust Act (the “Sherman Act”), and state law arising from the collapse of the ARS market in early 2008, which plaintiffs contend Citigroup and other ARS underwriters foresaw or should have foreseen but failed adequately to disclose. Most of these matters have been dismissed or settled.

Securities Actions: Beginning in March 2008, Citigroup, CGM and their affiliates and certain current and former officers, directors, and employees, have been named as defendants in several individual and alleged class action lawsuits related to ARS. These alleged securities class actions have been consolidated in the United States District Court for the Southern District of New York, as IN RE CITIGROUP AUCTION RATE SECURITIES LITIGATION. A consolidated amended complaint was filed on August 25, 2008, asserting claims for market manipulation under Sections 10 and 20 of the Securities Exchange Act of 1934, violations of the Investment Advisers Act and various state Deceptive Practices Acts, as well as claims for breach of fiduciary duty and injunctive relief. Defendants filed a motion to dismiss the complaint on October 24, 2008, which was fully briefed on January 23, 2009. On September 11, 2009, the court granted defendants’ motion to dismiss the consolidated amended complaint. On October 15, 2009, plaintiffs filed a further amended complaint, which defendants also have moved to dismiss. On March 1, 2011, the United States District Court for the Southern District of New York dismissed plaintiffs’ fourth consolidated amended complaint in IN RE CITIGROUP AUCTION RATE SECURITIES LITIGATION. Plaintiffs-appellants have appealed to the United States Court of Appeals for the Second Circuit from the order entered on March 1, 2011 by the United States District Court for the Southern District of New York in IN RE CITIGROUP AUCTION RATE SECURITIES LITIGATION dismissing their fourth consolidated amended complaint. Several individual ARS actions also have been filed in state and federal courts, asserting, among other things, violations of federal and state securities laws. Citigroup has moved the Judicial Panel on Multidistrict Litigation to transfer all of the individual ARS actions pending in federal court to the Southern District of New York for consolidation or coordination with IN RE CITIGROUP INC. AUCTION RATE SECURITIES LITIGATION.

On June 10, 2009, the Judicial Panel on Multidistrict Litigation granted CGM’s motion to transfer AMERICAN EAGLE OUTFITTERS, INC., ET AL. v. CITIGROUP GLOBAL MARKETS INC. from the United States District Court for the Western District of Pennsylvania to the United States District Court for the Southern District of New York, where it will be coordinated with IN RE CITIGROUP INC. AUCTION RATE SECURITIES LITIGATION and FINN v. SMITH BARNEY, ET AL. On June 17, 2009, the Judicial Panel on Multidistrict Litigation issued an order conditionally transferring three other individual auction rate securities actions pending against CGM in other federal courts to the United States District Court for the Southern District of New York. Plaintiffs in those actions have opposed their transfer.

On April 1, 2009, TEXAS INSTRUMENTS INC. v. CITIGROUP GLOBAL MARKETS INC., ET AL. was filed in Texas state court asserting violations of state securities law by CGM, B NY Capital Markets, Inc. and Morgan Stanley and Co., Inc. Defendants removed the case to the United States District Court for the Northern District of Texas, and plaintiff has moved to have it remanded to state court. On May 8, 2009, CGM filed a motion to sever the claims against it from the claims against its co-defendants. On May 17, 2011, the District Court of Dallas County, Texas, dismissed plaintiff’s complaint in TEXAS INSTRUMENTS INC. v. CITIGROUP GLOBAL MARKETS INC., ET AL, following the settlement of the matter.

16

On July 23, 2009, the Judicial Panel on Multidistrict Litigation issued an order transferring K-V PHARMACEUTICAL CO. v. CGM from the United States District Court for the Eastern District of Missouri to the United States District Court for the Southern District of New York for coordination with IN RE CITIGROUP AUCTION-RATE SECURITIES LITIGATION. On August 24, 2009, CGM moved to dismiss the complaint.

On October 2, 2009, the Judicial Panel on Multi-district Litigation transferred OCWEN FINANCIAL CORP., ET AL. v. CGM to the United States District Court for the Southern District of New York for coordination with IN RE CITIGROUP AUCTION RATE SECURITIES LITIGATION. On March 27, 2012, the United States Court of Appeals for the Second Circuit affirmed the district court’s dismissal of plaintiffs’ complaint in IN RE CITIGROUP AUCTION RATE SECURITIES LITIGATION.

Hansen Beverage Co. v. Citigroup Inc., et al.: On July 11, 2008, a complaint was filed against Citigroup, CGM and Smith Barney, alleging violations of Sections 10 and 20 of the Securities Exchange Act of 1934 and the Investment Advisers Act arising out of plaintiff’s investment in ARS. On September 22, 2008, the Citigroup defendants filed a motion to compel arbitration, which was granted on October 10, 2008. A motion to reconsider the District Court’s decision was denied on October 21, 2008. This action is currently stayed, pending arbitration.

Antitrust Actions: MAYOR & CITY COUNCIL OF BALTIMORE, MARYLAND v. CITIGROUP INC., ET AL. and RUSSELL MAYFIELD, ET AL. v. CITIGROUP INC., ET AL., are lawsuits filed in the Southern District of New York on behalf of a purported class of ARS issuers and investors, respectively, against Citigroup, CGM and various other financial institutions. In these actions, plaintiffs allege violations of Section 1 of the Sherman Act arising out of defendants’ alleged conspiracy to artificially restrain trade in the ARS market. On January 15, 2009, defendants filed motions to dismiss the complaints in these actions. On January 26, 2010, both actions were dismissed. The actions are now pending on appeal.

Governmental and Regulatory Matters. On August 7, 2008, Citigroup and certain of its affiliates reached a settlement with the New York Attorney General, the Securities and Exchange Commission, and other state regulatory agencies, pursuant to which Citigroup agreed to offer to purchase at par ARS that are not auctioning from all Citigroup individual investors, small institutions (as defined in by the terms of the settlement), and charities that purchased ARS from Citigroup prior to February 11, 2008. In addition, Citigroup agreed to pay a $50 million fine to the State of New York and a $50 million fine to the other state regulatory agencies. Citigroup and certain of its affiliates are also subject to formal and informal investigations, as well as subpoenas and/or requests for information, from various governmental and self-regulatory agencies relating to auction-rate securities. Citigroup and its affiliates are cooperating fully and are engaged in discussions on these matters.

Arbitrations. In addition to the various lawsuits discussed above, several arbitrations are pending against Citigroup and certain of its affiliates relating to A RS investments.

Falcon and ASTA/M AT–Related Litigation and Other Matters

Beginning in April 2008, Citigroup has been named as defendant in various complaints filed by investors in the Falcon and ASTA/MAT funds seeking recoupment of their alleged losses. Although most of these investor disputes have been resolved, some remain pending.