Attached files

| file | filename |

|---|---|

| EX-31.1 - SECTION 302 CEO AND CFO CERTIFICATION - CHESAPEAKE GRANITE WASH TRUST | chkr-2012x1231x10kex311.htm |

| EX-32.1 - SECTION 906 CEO AND CFO CERTIFICATION - CHESAPEAKE GRANITE WASH TRUST | chkr-2012x1231x10kex321.htm |

| EX-99.1 - REPORT OF RYDER SCOTT COMPAN, L.P. - CHESAPEAKE GRANITE WASH TRUST | chkr-2012x1231x10kex991.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

[X] Annual Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the Fiscal Year Ended December 31, 2012

[ ] Transition Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the transition period from to .

Commission File No. 001-35343

Chesapeake Granite Wash Trust

(Exact name of registrant as specified in its charter)

Delaware | 45-6355635 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

The Bank of New York Mellon Trust Company, N.A., Trustee Global Corporate Trust | ||

919 Congress Avenue | ||

Austin, Texas | 78701 | |

(Address of principal executive offices) | (Zip Code) | |

(855) 802-1093

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: | |

Title of Each Class Common Units Representing Beneficial Interests | Name of Each Exchange on which Registered New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None | |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [ ] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant's knowledge, in definitive proxy

or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [X]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer [ ] | Accelerated filer [X] | Non-accelerated filer [ ] | Smaller reporting company [ ] |

(Do not check if a smaller reporting company) | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes [ ] No [X]

The aggregate market value of the 23,000,000 Common Units representing beneficial interests in Chesapeake Granite Wash Trust held by non-affiliates of the registrant, computed using the closing sale price of $19.69 on June 29, 2012, was approximately $453 million.

As of March 14, 2013, 35,062,500 Common Units and 11,687,500 Subordinated Units representing beneficial interests in Chesapeake Granite Wash Trust were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Listed below is the only document parts of which are incorporated herein by reference and the parts of this Annual Report into which the document is incorporated:

None

CHESAPEAKE GRANITE WASH TRUST

2012 ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

PART I | Page | |

Item 1. | Business | |

Item 1A. | Risk Factors | |

Item 1B. | Unresolved Staff Comments | |

Item 2. | Properties | |

Item 3. | Legal Proceedings | |

Item 4. | Mine Safety Disclosures | |

PART II | ||

Item 5. | Market for Units of the Trust, Related Unitholder Matters and Trust Purchases of Units | |

Item 6. | Selected Financial Data | |

Item 7. | Trustee's Discussion and Analysis of Financial Condition and Results of Operations | |

Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | |

Item 8. | Financial Statements and Supplementary Data | |

Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | |

Item 9A. | Controls and Procedures | |

Item 9B. | Other Information | |

PART III | ||

Item 10. | Directors, Executive Officers and Corporate Governance | |

Item 11. | Executive Compensation | |

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Unitholder Matters | |

Item 13. | Certain Relationships and Related Transactions and Director Independence | |

Item 14. | Principal Accountant Fees and Services | |

PART IV | ||

Item 15. | Exhibits, Financial Statement Schedules | |

All references to “we,” “us,” “our,” or the “Trust” refer to Chesapeake Granite Wash Trust. The royalty interests conveyed on November 16, 2011 by Chesapeake from its interests in certain properties in the Colony Granite Wash formation in Oklahoma and held by the Trust are referred to as the “Royalty Interests.” References to “Chesapeake” refer to Chesapeake Energy Corporation and, where the context requires, its subsidiaries.

DISCLOSURES REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K (“Annual Report”) includes “forward-looking statements” about the Trust and Chesapeake and other matters discussed herein that are subject to risks and uncertainties that are intended to qualify for the safe harbor from liability established by the Private Securities Litigation Reform Act of 1995, and Section 21E of the Securities Exchange Act of 1934, as amended. All statements other than statements of historical fact included in this document, including, without limitation, statements under “Trustee’s Discussion and Analysis of Financial Condition and Results of Operations” in Item 7 of Part II and “Risk Factors” in Item 1A of Part I and elsewhere herein regarding the proved oil, NGL and natural gas reserves associated with the properties underlying the Royalty Interests, the Trust’s or Chesapeake’s future financial position, business strategy, budgets, projected costs and plans and objectives for future operations, information regarding target distributions, statements pertaining to future development activities and costs, statements regarding the number of development wells to be completed in future periods and information regarding production and reserve growth, are forward-looking statements. Actual outcomes and results may differ materially from those projected. Our forward-looking statements are generally accompanied by words such as “estimate,” “project,” “predict,” “believe,” “expect,” “anticipate,” “potential,” “could,” “may,” “foresee,” “plan,” “goal,” “assume,” “target,” “should,” “intend” or other words that convey the uncertainty of future events or outcomes. These statements are based on certain assumptions made by the Trust, and by Chesapeake in light of its experience and perception of historical trends, current conditions and expected future developments, as well as other factors we believe are appropriate under the circumstances. However, whether actual results and developments will conform with such expectations and predictions is subject to a number of risks and uncertainties, including the risk factors discussed in Item 1A of Part I of this Annual Report, which could affect the future results of the energy industry in general, and the Trust and Chesapeake in particular, and could cause those results to differ materially from those expressed in such forward-looking statements. The actual results or developments anticipated may not be realized or, even if substantially realized, they may not have the expected consequences to or effects on Chesapeake's business and the Trust. Such statements are not guarantees of future performance and actual results or developments may differ materially from those projected in such forward-looking statements. The Trustee relies on Chesapeake for information regarding the Royalty Interests, the Underlying Properties and Chesapeake itself. The Trust undertakes no obligation to publicly update or revise any forward-looking statements.

GLOSSARY OF CERTAIN TERMS

In this Annual Report, the following terms have the meanings specified below. Other terms are defined in the text of this Annual Report.

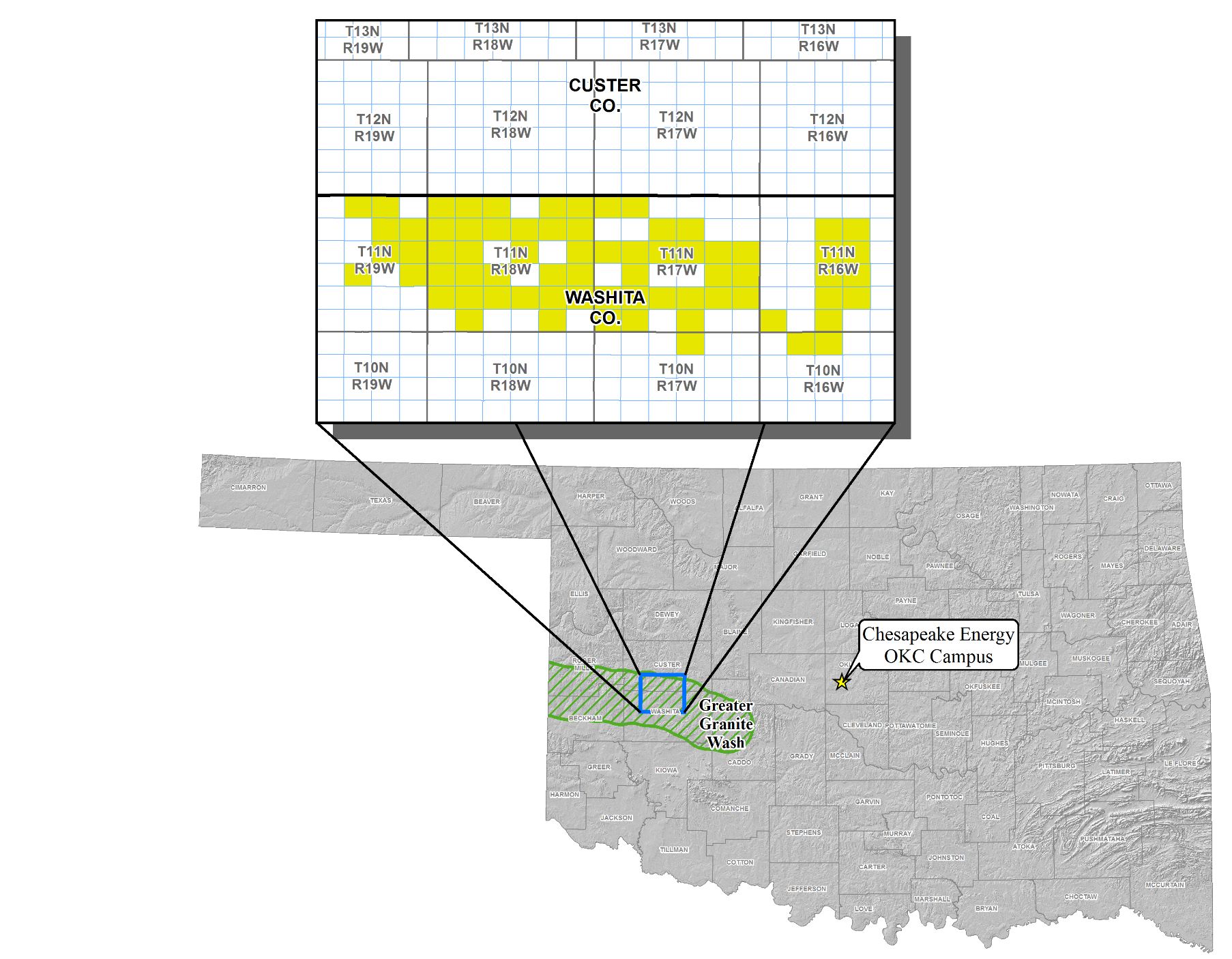

AMI. The area of mutual interest, or AMI, lies within Washita County in western Oklahoma and is limited to the Colony Granite Wash formation in the area identified below, consisting of approximately 45,400 gross acres (29,000 net acres) held by Chesapeake as of December 31, 2012.

Bbl. One stock tank barrel, or 42 U.S. gallons liquid volume, used herein in reference to crude oil or other liquid hydrocarbons.

Bcf. Billion cubic feet.

Boe. Barrel of oil equivalent, determined using the ratio of six mcf of natural gas to one bbl of oil, condensate or NGL, which approximates the relative energy content of oil, condensate and NGL as compared to natural gas. Despite holding the ratio constant at six mcf to one bbl, prices have historically often been higher for oil than natural gas on an energy equivalent basis, although there have been periods in which they have been lower.

Btu. British thermal unit, which is the quantity of heat required to raise the temperature of one pound of water one degree Fahrenheit.

Completion. The process of treating a drilled well followed by the installation of permanent equipment for the production of oil, NGL and natural gas, or in the case of a dry well, the reporting to the appropriate authority that the well has been abandoned.

Condensate. A mixture of hydrocarbons that exists in the gaseous phase at the original reservoir temperature and pressure, but that, when produced, is in the liquid phase at surface pressure and temperature.

Developed Acreage. The number of acres which are allocated or assignable to producing wells or wells capable of production.

Developed Reserves. Developed reserves are reserves of any category that can be expected to be recovered (i) through existing wells with existing equipment and operating methods or in which the cost of the required equipment is relatively minor compared to the cost of a new well and (ii) through installed extraction equipment and infrastructure operational at the time of the reserves estimate if the extraction is by means not involving a well.

Development Area. The sections adjacent to governmental sections in the AMI.

Development Costs. Costs incurred to obtain access to proved reserves and to provide facilities for extracting, treating, gathering and storing the oil and gas. More specifically, development costs, including depreciation and applicable operating costs of support equipment and facilities and other costs of development activities, are costs incurred to (i) gain access to and prepare well locations for drilling, including surveying well locations for the purpose of determining specific development drilling sites, clearing ground, draining, road building and relocating public roads, gas lines and power lines, to the extent necessary in developing the proved reserves, (ii) drill and equip Development Wells, development-type stratigraphic test wells and service wells, including the costs of platforms and of well equipment such as casing, tubing, pumping equipment, and the wellhead assembly, (iii) acquire, construct and install production facilities such as leases, flow lines, separators, treaters, heaters, manifolds, measuring devices and production storage tanks, natural gas cycling and processing plants, and central utility and waste disposal systems, and (iv) provide improved recovery systems.

Development Well. As defined by the SEC, a development well is a well that is drilled within the proved area of an oil or natural gas reservoir to the depth of a stratigraphic horizon known to be productive. For the purposes of the Trust and as used herein, references to “Development Wells” refer to the 118 horizontal development wells that, since July 1, 2011, have been or are to be drilled on properties held by Chesapeake in the AMI and in which the Trust has received or will receive an interest.

Dry Well. A well found to be incapable of producing either oil or natural gas in sufficient quantities to justify completion as a natural gas or oil well.

Economically Producible. The term economically producible, as it relates to a resource, means a resource which generates revenue that exceeds, or is reasonably expected to exceed, the costs of the operation. The value of the products that generate revenue is determined at the terminal point of oil and gas producing activities as defined in Rule 4-10(a)(16) of Regulation S-X under the Securities Act.

Estimated Future Net Revenues. Also referred to as “estimated future net cash flows.” The result of applying current prices of oil, natural gas and NGL to estimated future production from oil, natural gas and NGL proved reserves, reduced by estimated future expenditures, based on current costs to be incurred, in developing and producing the proved reserves, excluding overhead.

Field. An area consisting of a single reservoir or multiple reservoirs all grouped on or related to the same individual geological structural feature and/or stratigraphic condition. There may be two or more reservoirs in a field which are separated vertically by intervening impervious strata, or laterally by local geologic barriers, or both. Reservoirs that are associated by being in overlapping or adjacent fields may be treated as a single or common operational field. The geological terms "structural feature" and "stratigraphic condition" are intended to identify localized geological features as opposed to the broader terms of basins, trends, provinces, plays or areas of interest.

GAAP. Generally accepted accounting principles in the United States.

Gross Acres or Gross Wells. The total acres or wells, as the case may be, in which a working interest is owned.

Horizontal Wells. Wells which are drilled at angles greater than 70 degrees from vertical.

IRS. The Internal Revenue Service of the United States federal government.

Mbbl. One thousand barrels of crude oil or other liquid hydrocarbons.

Mboe. One thousand boe.

Mcf. One thousand cubic feet.

Mmbtu. One million btus.

Mmcf. One million cubic feet.

Net Acres or Net Wells. The sum of the fractional working interest owned in gross acres or gross wells.

Net Revenue Interest. A share of production after all burdens, such as royalty and overriding royalty interests, have been deducted from the working interest.

Natural Gas Liquids (NGL). Those hydrocarbons in natural gas that are separated from the gas as liquids through the process of absorption, condensation, adsorption or other methods in gas processing or cycling plants. Natural gas liquids primarily include ethane, propane, butane, isobutene, pentane, hexane and natural gasoline.

NYMEX. New York Mercantile Exchange.

Plugging and Abandoning. Refers to the sealing off of fluids in the strata penetrated by a well so that the fluids from one stratum will not escape into another or to the surface. Oklahoma regulations require plugging of abandoned wells.

Present Value of Future Net Revenues (“PV-10”). The present value of estimated future net revenue to be generated from the production of proved reserves, discounted using an annual discount rate of 10% (as required by the SEC), calculated without deducting future income taxes. PV-10 is a non-GAAP financial measure and generally differs from the standardized measure of discounted net cash flows, or Standardized Measure, the most directly comparable GAAP financial measure, because it does not include the effects of income taxes on future net revenues. Because the Trust will not bear federal income tax expense, the PV-10 and Standardized Measure attributable to the Royalty Interests are the same. Neither PV-10 nor Standardized Measure represents an estimate of the fair market value of the Underlying Properties or the Royalty Interests. The Trust, Chesapeake and others in the oil and gas industry use PV-10 as a measure to compare the relative size and value of proved reserves held by companies without regard to the specific tax characteristics of such entities. PV-10 for the Royalty Interests has been calculated without deduction for production and development costs, as the Trust will not bear those costs.

Price Differential. The difference in the price of natural gas or oil received at the sales point and the NYMEX price.

Producing Well. As defined by the SEC, a producing well is a well that is found to be capable of producing hydrocarbons in sufficient quantities such that proceeds from the sale of such production exceeds production expenses and taxes. For the purposes of the Trust and as used herein, references to “Producing Wells” refer to the 69 existing horizontal wells in which Chesapeake conveyed an interest to the Trust effective as of July 1, 2011.

Production Expenses.

(i) Costs incurred to operate and maintain wells and related equipment and facilities, including depreciation and applicable operating costs of support equipment and facilities and other costs of operating and maintaining those wells and related equipment and facilities. They become part of the cost of oil, NGL and natural gas produced. Examples of production expenses (sometimes called lifting expenses) are:

(A) | Costs of labor to operate the wells and related equipment and facilities. |

(B) | Repairs and maintenance. |

(C) | Materials, supplies, and fuel consumed and supplies utilized in operating the wells and related equipment and facilities. |

(D) | Property taxes and insurance applicable to proved properties and wells and related equipment and facilities. |

(E) Production taxes.

(ii) Some support equipment or facilities may serve two or more oil and natural gas producing activities and may also serve transportation, refining and marketing activities. To the extent that the support equipment and facilities are used in oil and gas producing activities, their depreciation and applicable operating costs become exploration, development or production expenses, as appropriate. Depreciation, depletion and amortization of capitalized acquisition, exploration, and development costs are not production expenses but also become part of the cost of oil and natural gas produced along with production (lifting) costs identified above.

Productive Well. A well that is not a dry well. Productive wells include producing wells and wells that are mechanically capable of production.

Prospectus. The Chesapeake Granite Wash Trust Prospectus dated November 10, 2011 and filed with the SEC on November 14, 2011 in connection with the initial public offering of the Trust's common units.

Proved Developed Reserves. Proved reserves that can be expected to be recovered through existing wells with existing equipment and operating methods or in which the cost of the required equipment is relatively minor compared to the cost of a new well.

Proved Reserves. Proved oil, NGL and natural gas reserves are those quantities of oil, NGL and natural gas, which, by analysis of geoscience and engineering data, can be estimated with reasonable certainty to be economically producible - from a given date forward, from known reservoirs, and under existing economic conditions, operating methods, and government regulations - prior to the time at which contracts providing the right to operate expire, unless evidence indicates that renewal is reasonably certain, regardless of whether deterministic or probabilistic methods are used for the estimation. The project to extract the hydrocarbons must have commenced or the operator must be reasonably certain that it will commence the project within a reasonable time. The area of a reservoir considered as proved includes (i) the area identified by drilling and limited by fluid contacts, if any, and (ii) adjacent undrilled portions of the reservoir that can, with reasonable certainty, be judged to be continuous with it and to contain economically producible natural gas or oil on the basis of available geoscience and engineering data. In the absence of information on fluid contacts, proved quantities in a reservoir are limited by the lowest known hydrocarbons as seen in a well penetration unless geoscience, engineering, or performance data and reliable technology establishes a lower contact with reasonable certainty. Where direct observation from well penetrations has defined a highest known oil elevation and the potential exists for an associated gas cap, proved oil reserves may be assigned in the structurally higher portions of the reservoir only if geoscience, engineering, or performance data and reliable technology establish the higher contact with reasonable certainty. Reserves that can be produced economically through application of improved recovery techniques (including, but not limited to, fluid injection) are included in the proved classification when (i) successful testing by a pilot project in an area of the reservoir with properties no more favorable than in the reservoir as a whole, the operation of an installed program in the reservoir or an analogous reservoir, or other evidence using reliable technology establishes the reasonable certainty of the engineering analysis on which the project or program was based and (ii) the project has been approved for development by all necessary parties and entities, including governmental entities. Existing economic conditions include prices and costs at which economic producibility from a reservoir is to be determined. The price is the average price during the 12-month period prior to the ending date of the period covered by the report, determined as an unweighted arithmetic average of the first-day-of-the-month price for each month within such period, unless prices are defined by contractual arrangements, excluding escalations based upon future conditions.

Proved Undeveloped Reserves. Proved reserves that are expected to be recovered from new wells on undrilled acreage, or from existing wells where a relatively major expenditure is required for recompletion. Reserves on undrilled acreage are limited to those directly offsetting development spacing areas that are reasonably certain of production when drilled, unless evidence using reliable technology exists that establishes reasonable certainty of economic producibility at greater distances. Undrilled locations can be classified as having proved undeveloped reserves only if a development plan has been adopted indicating that they are scheduled to be drilled within five years, unless the specific circumstances justify a longer time. Estimates for proved undeveloped reserves are not attributed to any acreage for which an application of fluid injection or other improved recovery technique is contemplated, unless such techniques have been proved effective by actual projects in the same reservoir or an analogous reservoir, or by other evidence using reliable technology establishing reasonable certainty.

PV-10. See “Present value of future net revenues.”

Reserves. Estimated remaining quantities of oil, NGL and natural gas and related substances anticipated to be economically producible as of a given date, by application of development projects to known accumulations. In addition,

there must exist, or there must be a reasonable expectation that there will exist, the legal right to produce or a revenue interest in the production, installed means of delivering oil and gas or related substances to market, and all permits and financing required to implement the project. Reserves should not be assigned to adjacent reservoirs isolated by major, potentially sealing, faults until those reservoirs are penetrated and evaluated as economically producible. Reserves should not be assigned to areas that are clearly separated from a known accumulation by a non-productive reservoir (i.e., absence of reservoir, structurally low reservoir, or negative test results). Such areas may contain prospective resources (i.e., potentially recoverable resources from undiscovered accumulations).

Reservoir. A porous and permeable underground formation containing a natural accumulation of producible oil and/or gas that is confined by impermeable rock or water barriers and is individual and separate from other reservoirs.

Standardized Measure of Discounted Future Net Cash Flows. The discounted future net cash flows relating to proved reserves based on the prices used in estimating the proved reserves, year-end costs and statutory tax rates (adjusted for permanent differences) and a 10% annual discount rate. Standardized measure differs from PV-10 because standardized measure includes the effect of future income taxes on future net revenues. Because the Trust does not bear income taxes, PV-10 and standardized measure with respect to the Royalty Interests are the same.

Undeveloped Acreage. Acreage on which wells have not been drilled or completed to a point that would permit the production of economic quantities of oil and natural gas regardless of whether such acreage contains proved reserves.

Working Interest. The operating interest which gives the owner the right to drill, produce and conduct operating activities on the property and a share of production.

PART I

ITEM 1. | Business |

Introduction

Chesapeake Granite Wash Trust is a statutory trust formed in June 2011 under the Delaware Statutory Trust Act pursuant to an initial trust agreement by and among Chesapeake, as Trustor, The Bank of New York Mellon Trust Company, N.A., as Trustee (the “Trustee”), and The Corporation Trust Company, as Delaware Trustee (the “Delaware Trustee”). The Trust maintains its offices at the office of the Trustee, which is located at 919 Congress Avenue, Suite 500, Austin, Texas 78701, the telephone number of the Trustee is (855) 802-1093.

The Trustee maintains a website for filings by the Trust with the Securities and Exchange Commission (the “SEC”). Electronic filings by the Trust with the SEC are available free of charge through the Trust's website at www.chkgranitewashtrust.com or through the SEC's website at www.sec.gov. The Trust will also provide electronic and paper copies of its recent filings free of charge upon request to the Trustee.

General

The Trust was created to own the Royalty Interests for the benefit of Trust unitholders pursuant to a trust agreement dated as of June 29, 2011 and subsequently amended and restated as of November 16, 2011 by and among Chesapeake, Chesapeake Exploration, L.L.C., a wholly owned subsidiary of Chesapeake, the Trustee and the Delaware Trustee (the “Trust Agreement”). The Royalty Interests are derived from Chesapeake's interests in specified oil and natural gas properties located in the Colony Granite Wash play in Washita County in the Anadarko Basin of western Oklahoma (the “Underlying Properties”). Chesapeake conveyed the Royalty Interests to the Trust from Chesapeake's interests in the Producing Wells and the Development Wells.

The business and affairs of the Trust are managed by the Trustee. The Trust Agreement limits the Trust's business activities generally to owning the Royalty Interests and any activity reasonably related to such ownership, including activities required or permitted by the terms of the conveyances related to the Royalty Interests and derivative contracts between the Trust and its counterparty. The royalty interest in the Producing Wells (the “PDP Royalty Interest”) entitles the Trust to receive 90% of the proceeds (exclusive of any production or development costs but after deducting certain post-production expenses and any applicable taxes) from the sales of oil, NGL and natural gas production attributable to Chesapeake's net revenue interest in the Producing Wells. The royalty interest in the Development Wells (the “Development Royalty Interest”) entitles the Trust to receive 50% of the proceeds (exclusive of any production or development costs but after deducting certain post-production expenses and any applicable taxes) from the sales of oil, NGL and natural gas production attributable to Chesapeake's net revenue interest in the Development Wells.

Through an initial public offering in November 2011, the Trust sold 23,000,000 of its common units representing beneficial interests in the Trust to the public for net proceeds, after payment of offering expenses, of approximately $409.7 million. The Trust delivered the net proceeds of the initial public offering, along with 12,062,500 common units and 11,687,500 subordinated units, to certain wholly owned subsidiaries of Chesapeake in exchange for the conveyance of the Royalty Interests to the Trust. Upon completion of these transactions and as of December 31, 2012, there were 46,750,000 Trust units issued and outstanding, consisting of 35,062,500 common units and 11,687,500 subordinated units. The common units and subordinated units have identical rights and privileges, except with respect to their voting rights and rights to receive distributions as described below under Target Distributions and Subordination and Incentive Thresholds.

Neither the Trust nor the Trustee is responsible for, or has any control over, any costs related to the drilling of the Development Wells or any other operating or capital costs of the Underlying Properties. The Trust's cash receipts with respect to the Royalty Interests in the Underlying Properties are determined after deducting certain post-production expenses and any applicable taxes associated with the Royalty Interests. Post-production expenses generally consist of costs incurred to gather, store, compress, transport, process, treat, dehydrate and market the oil, NGL and natural gas produced. However, the Trust is not responsible for costs of marketing services provided by affiliates of Chesapeake. Cash distributions to unitholders will be increased or decreased by the effect of the Trust's derivative contracts and reduced by the Trust's general and administrative expenses. See Derivative Contracts below.

1

The Trust will dissolve and begin to liquidate on June 30, 2031, or earlier upon certain events (the “Termination Date”), and will soon thereafter wind up its affairs and terminate. At the Termination Date, (a) 50% of the total Royalty Interests conveyed by Chesapeake (the “Term Royalties”) will revert automatically to Chesapeake and (b) 50% of the total Royalty Interests conveyed by Chesapeake (the “Perpetual Royalties”) will be retained by the Trust and thereafter sold. The net proceeds of the sale of the Perpetual Royalties, as well as any remaining Trust cash reserves, will be distributed to the unitholders on a pro rata basis. Chesapeake will have a right of first refusal to purchase the Perpetual Royalties retained by the Trust at the Termination Date.

Target Distributions and Subordination and Incentive Thresholds

The Trust will make quarterly cash distributions of substantially all of its quarterly cash receipts, after deducting the Trust's administrative expenses, on or about 60 days following the completion of each quarter through (and including) the quarter ending June 30, 2031. Quarterly distributions to Trust unitholders will generally include royalty income attributable to sales of oil, NGL and natural gas for three months, including the first two months of the quarter just ended and the last month of the quarter prior to that one. The first quarterly distribution was made on December 28, 2011 to record unitholders as of December 15, 2011.

In connection with the initial public offering of the Trust, Chesapeake established quarterly target levels of cash distributions to unitholders for the life of the Trust. These target distributions were used to calculate the subordination and incentive thresholds described in more detail below and do not represent estimates of the actual distributions that may be received by Trust unitholders. Actual cash distributions to the Trust unitholders will fluctuate quarterly based on the quantity of oil, NGL and natural gas sold from the Underlying Properties, the prices received for such sales, when Chesapeake receives payment for such sales, payments under the Trust's derivative contracts, the Trust's expenses and other factors. While target distributions initially increase as Chesapeake completes its drilling obligation and production increases, over time target distributions decline as a result of the depletion of the reserves in the Underlying Properties.

In order to provide support for cash distributions on the common units, Chesapeake agreed to subordinate 11,687,500 of the Trust units retained following the initial public offering of common units, which constitutes 25% of the outstanding Trust units. The subordinated units are entitled to receive pro rata distributions from the Trust each quarter if and to the extent there is sufficient cash to pay a cash distribution on the common units that is no less than the 80% of the target distribution for the corresponding quarter (the "subordination threshold"). If there is not sufficient cash to fund such a distribution on all of the common units, the distribution to be made with respect to the subordinated units will be reduced or eliminated for such quarter in order to make a distribution, to the extent possible, of up to the subordination threshold amount on all the common units, including the common units held by Chesapeake.

In exchange for agreeing to subordinate a portion of its Trust units, and in order to provide additional financial incentive to Chesapeake to satisfy its drilling obligation and perform operations on the Underlying Properties in an efficient and cost-effective manner, Chesapeake is entitled to receive incentive distributions equal to 50% of the amount by which the cash available for distribution on all of the Trust units in any quarter is 20% greater than the target distribution for such quarter (each, an “incentive threshold”). The remaining 50% of cash available for distribution in excess of the incentive thresholds will be paid to Trust unitholders, including Chesapeake, on a pro rata basis.

At the end of the fourth full calendar quarter following Chesapeake's satisfaction of its drilling obligation with respect to the Development Wells, the subordinated units will automatically convert into common units on a one-for- one basis and Chesapeake's right to receive incentive distributions for any subsequent quarter will terminate. With respect to distributions for quarters following the fourth full quarter after Chesapeake's satisfaction of its drilling obligation with respect to the Development Wells, the common units will no longer have the protection of the subordination threshold, and all Trust unitholders will share on a pro rata basis in the Trust's distributions. The period during which the subordinated units are outstanding is referred to as the "subordination period."

2

The following table sets forth the subordination threshold and the incentive threshold for each calendar quarter through the second quarter of 2017, as established in the Trust Agreement:

Period | Subordination Threshold(1) | Incentive Threshold(1) | |

($ per unit) | |||

2012: | |||

Fourth Quarter(2) | 0.67 | 1.01 | |

2013: | |||

First Quarter | 0.69 | 1.04 | |

Second Quarter | 0.69 | 1.04 | |

Third Quarter | 0.71 | 1.07 | |

Fourth Quarter | 0.69 | 1.04 | |

2014: | |||

First Quarter | 0.69 | 1.04 | |

Second Quarter | 0.68 | 1.02 | |

Third Quarter | 0.69 | 1.03 | |

Fourth Quarter | 0.66 | 0.99 | |

2015: | |||

First Quarter | 0.66 | 0.99 | |

Second Quarter | 0.68 | 1.02 | |

Third Quarter | 0.64 | 0.96 | |

Fourth Quarter | 0.56 | 0.84 | |

2016: | |||

First Quarter | 0.51 | 0.76 | |

Second Quarter | 0.47 | 0.70 | |

Third Quarter | 0.44 | 0.66 | |

Fourth Quarter | 0.41 | 0.62 | |

2017: | |||

First Quarter | 0.39 | 0.59 | |

Second Quarter | 0.37 | 0.56 | |

(1) For each quarter, the subordination threshold equals 80% of the target distribution and the incentive threshold equals 120% of the target distribution. The subordination and incentive thresholds terminate after the distribution is made for the fourth full calendar quarter following Chesapeake's completion of its drilling obligation.

(2) A distribution of $0.6700 per common unit and $0.3772 per subordinated unit was paid on March 1, 2013 to unitholders of record as of February 19, 2013.

The aggregate distributions paid in the twelve months ended December 31, 2012 were $2.6265 per common unit and $2.0892 per subordinated unit. The first two distributions, paid on March 1, 2012 and May 31, 2012, were above the subordination threshold and below the incentive threshold for the corresponding distribution period. However, the distributable income available for distribution to unitholders with respect to the distributions paid on August 30, 2012 and November 29, 2012 were below the applicable subordination thresholds, resulting in a payment of $0.6100 per common unit and $0.4819 per subordinated unit on August 30, 2012 and a payment of $0.6300 per common unit and $0.2208 per subordinated unit on November 29, 2012. As of March 14, 2013, Chesapeake owned 12,062,500 common units and all 11,687,500 subordinated units, which together represent 50.8% of the outstanding Trust units.

3

Derivative Contracts

The Trust uses derivative instruments to manage its exposure to variability in cash flow from changes in oil and NGL prices. On November 16, 2011, Chesapeake novated to the Trust, and the Trust became party to, derivative contracts covering approximately 50% of the expected oil and NGL production and approximately 37% of the expected revenue (based on NYMEX strip oil prices as of October 28, 2011) attributable to the Royalty Interests from October 1, 2011 through September 30, 2015. To the extent oil production falls below the hedged oil volume, the derivative contracts will also cover NGL production. To the extent oil and NGL prices are not correlated, the derivative contracts will not effectively mitigate the price risk of the Trust’s NGL production. The remaining estimated production of oil and NGL during that time, all production of natural gas during that time and all production after such time, will not be hedged, except in connection with the restructuring of an existing derivative contract. The derivative contracts are not qualified for hedge accounting treatment, and therefore all future mark-to-market fluctuations will be recorded to the Trust Corpus until cash settled. The value of the derivative contracts as of December 31, 2012, was a liability of $8.1 million.

These commodity derivative contracts consist of fixed-price oil swaps, in which the Trust receives a fixed price and pays a floating market price, based on NYMEX settlement prices, to the counterparty for the underlying commodity of the derivative. As a party to these contracts, the Trust will receive payments directly from its counterparty or be required to pay any amounts owed directly to its counterparty. All swaps are net settled based on the difference between the fixed-price payment and the floating-price payment. Settlements are due on a quarterly basis, including the first two months of the calendar quarter just ended and the last month of the calendar quarter prior to that one. Any payment due to or from such counterparty will be made by the 40th day following the end of the calendar quarter in which such payments become due. See Note 3 to the financial statements contained in Part II Item 8 of this Annual Report for further discussion of the derivative contracts.

Under the derivative contracts and separate from the drilling obligation under the development agreement, there is a requirement that Chesapeake drill and complete, or cause to be drilled and completed, a specified number of wells (inclusive of the Producing Wells as of the completion of the initial public offering and Development Wells) by the end of each six-month period ending June 30 and December 31 during the term of the derivative contracts. Specifically, from November 16, 2011 until June 30, 2016, the derivative contracts require that Chesapeake drill and complete, cause to be drilled and completed or participate as a non-operator in the drilling of the wells in accordance with the drilling plan set forth in the following table:

Reference Period End Date | Cumulative Minimum Well Requirement |

December 31, 2012 | 69 |

June 30, 2013 | 78 |

December 31, 2013 | 85 |

June 30, 2014 | 90 |

December 31, 2014 | 97 |

June 30, 2015 | 108 |

December 31, 2015 | 111 |

June 30, 2016 | 117 |

Chesapeake's drilling plan, which provides for the ratable drilling of the Development Wells during the development period, contemplates drilling more wells in each six-month period than the drilling obligation under the derivative contracts requires. As of December 31, 2012, Chesapeake has drilled and completed 120 gross wells that count towards the cumulative minimum well requirement under the derivative contracts.

In addition, with respect to each such six-month period, the Trust is required to deliver to the counterparty and the collateral agent under the derivative contracts (a) an independent reserve engineers' report that sets forth the total reserves estimated to be attributable to the Trust's interest in the Underlying Properties as of the end of such period and such other information as is typically included in, or required under SEC rules to be included in, summary reserve engineers reports and (b) a report that sets forth certain information regarding the Development Wells drilled and completed as of the end of such six-month period.

4

The Trust's obligations to the counterparty under the derivative contracts are secured by proved reserves attributable to the Trust's interest in the Underlying Properties. The counterparty's obligations under the hedging arrangement must be secured by cash or short-term U.S. Treasury instruments to the extent that any mark-to-market amounts owed to the Trust exceeds defined thresholds. Subject to any applicable notice and cure periods, if, among other things, the Trust or Chesapeake is in material default of the drilling, payment or reporting requirements under the derivative contracts, becomes subject to bankruptcy proceedings or the Trust becomes subject to certain change of control transactions, the hedging counterparty may foreclose on the lien on the Royalty Interests. Even if such foreclosure is solely a result of Chesapeake's action or omission, the Trust may have no remedy against Chesapeake. In addition, the derivative contracts contain a prohibition on the Trust granting additional liens on any of its properties, other than customary permitted liens and liens in favor of the Trustee or the Delaware Trustee. Under the Trust Agreement, the Trustee may create a cash reserve to pay for future expenses of the Trust.

Administrative Services Agreement

On November 16, 2011, the Trust entered into an administrative services agreement with Chesapeake, effective July 1, 2011, pursuant to which Chesapeake provides the Trust with certain accounting, tax preparation, bookkeeping and information services related to the Royalty Interests and the registration rights agreement. In return for the services provided by Chesapeake under the administrative services agreement, the Trust pays Chesapeake an annual fee of $200,000, which is paid in equal quarterly installments and remains fixed for the life of the Trust. Chesapeake will also be entitled to receive reimbursement for its actual out-of-pocket fees, costs and expenses incurred in connection with the provision of any of the services under the agreement.

Additionally, the administrative services agreement established Chesapeake as the Trust's hedge manager, pursuant to which Chesapeake has the authority, on behalf of the Trust, to administer the Trust's derivative contracts. As hedge manager, Chesapeake also has authority to terminate, restructure or otherwise modify all or any portion of the Trust's derivative contracts to the extent that Chesapeake reasonably determines, acting in good faith, that the volumes hedged under such contracts exceed, or are expected to exceed, the combined estimated production attributable to the Royalty Interests over the periods hedged. However, in fulfilling its role as hedge manager, Chesapeake is not acting as a fiduciary for the Trust and has no affirmative duty to modify any of the Trust's derivative contracts, except as required by the derivative contracts. Moreover, under the Trust Agreement, Chesapeake is indemnified by the Trust for any actions it takes in this regard.

The administrative services agreement will terminate upon the earliest to occur of (a) the date the Trust shall have been wound up in accordance with the Trust Agreement, (b) the date that all of the Royalty Interests have been terminated or are no longer held by the Trust, (c) with respect to services to be provided with respect to any Underlying Properties being transferred by Chesapeake, the date that either Chesapeake or the Trustee may designate by delivering 90-days prior written notice, provided that Chesapeake's drilling obligation has been completed and the transferee of such Underlying Properties assumes responsibility to perform the services in place of Chesapeake or (d) a date mutually agreed by Chesapeake and the Trustee.

Description of the Trust

Common Units and Subordinated Units. Each Trust unit is a unit of the beneficial interest in the Trust and is entitled to receive cash distributions from the Trust on a pro rata basis. The Trust has 46,750,000 Trust units issued and outstanding, consisting of 35,062,500 common units and 11,687,500 subordinated units. The common units and subordinated units have identical rights and privileges, except with respect to their voting rights and rights to receive distributions.

The subordinated units will automatically convert into common units on a one-for-one basis at the end of the fourth full calendar quarter following Chesapeake's satisfaction of its drilling obligation to the Trust with respect to the Development Wells.

Distributions and Income Computations. The Trust makes quarterly cash distributions to unitholders from its available funds for such calendar quarter. Royalty Interest payments due to the Trust with respect to any calendar quarter are based on actual sales volumes attributable to the Trust's interests in the Underlying Properties (as measured at Chesapeake's metering systems) for the first two months of the quarter just ended as well as the last month of the immediately preceding quarter and actual revenues received for such volumes. Chesapeake makes the Royalty Interest payments to the Trust within 35 days of the end of each calendar quarter. In addition, any payments due from or required to be made to the counterparty under the Trust's derivative contracts are paid within 40 days of the end of

5

such calendar quarter. Taking into account the receipt and disbursement of all such amounts, the Trustee determines for such calendar quarter the amount of funds available for distribution to the Trust unitholders. Available funds are the excess cash, if any, received by the Trust over the Trust's expenses for that quarter. Available funds are reduced by any cash the Trustee decides to hold as a reserve against future liabilities.

The Trustee distributes cash approximately 60 days (or the next succeeding business day following such day if such day is not a business day) following each calendar quarter to each person who is a Trust unitholder of record on the quarterly record date together with interest expected to be earned on the amount of such quarterly distribution from the date of receipt thereof by the Trustee to the payment date.

Unless otherwise advised by counsel or the IRS, the Trustee treats the income and expenses of the Trust for each quarter as belonging to the Trust unitholders of record on the quarterly record date that occurs in such quarter. Trust unitholders recognize income and expenses for tax purposes in the quarter the Trust receives or pays those amounts, rather than in the quarter the Trust distributes them. Minor variances may occur. For example, the Trustee could establish a reserve in one quarter that would not result in a tax deduction until a later quarter. The Trustee could also make a payment in one quarter that would be amortized for tax purposes over several months.

Transfer of Trust Units. Trust unitholders may transfer their Trust units in accordance with the Trust Agreement. The Trustee does not require either the transferor or transferee to pay a service charge for any transfer of a Trust unit. The Trustee may require payment of any tax or other governmental charge imposed for a transfer. The Trustee may treat the owner of any Trust unit as shown by its records as the owner of the Trust unit. The Trustee will not be considered to know about any claim or demand on a Trust unit by any party except the record owner. A person who acquires a Trust unit after any quarterly record date will not be entitled to the distribution relating to that quarterly record date. Delaware law will govern all matters affecting the title, ownership or transfer of Trust units.

Periodic Reports. The Trustee files all required Trust federal and state income tax and information returns. The Trustee prepares and mails to Trust unitholders a Schedule K-1 and also causes to be prepared and filed reports required to be filed under the Securities Exchange Act of 1934, as amended, and by the rules of the New York Stock Exchange.

Each Trust unitholder and his representatives have the right, at his own expense and during reasonable business hours upon reasonable prior notice, to examine and inspect the records of the Trust and the Trustee in reference thereto for any purpose reasonably related to the Trust unitholder's interest as a Trust unitholder.

Liability of Trust Unitholders. Under the Delaware Statutory Trust Act, Trust unitholders are entitled to the same limitation of personal liability extended to stockholders of private corporations for profit under the General Corporation Law of the State of Delaware. No assurance can be given, however, that the courts in jurisdictions outside of Delaware will give effect to such limitation.

Voting Rights of Trust Unitholders. The Trustee or Trust unitholders owning at least 10% of the outstanding Trust units may call meetings of Trust unitholders. The Trust does not intend to hold annual meetings of the Trust Unitholders. The Trust is responsible for all costs associated with calling a meeting of Trust unitholders unless such meeting is called by the Trust unitholders, in which case the Trust unitholders are responsible for all costs associated with calling such meeting of Trust unitholders. Meetings must be held in such location as is designated by the Trustee in the notice of such meeting. The Trustee must send written notice of the time and place of the meeting and the matters to be acted upon to all of the Trust unitholders at least 20 days and not more than 60 days before the meeting. Trust unitholders representing a majority of Trust units outstanding must be present or represented to have a quorum. Each Trust unitholder is entitled to one vote for each Trust unit owned. Abstentions and broker non-votes shall not be deemed to be a vote cast.

Unless otherwise required by the Trust Agreement, a matter may be approved or disapproved by the vote of a majority of the Trust units held by the Trust unitholders voting in person or by proxy at a meeting where there is a quorum. This is true, even if a majority of the total outstanding Trust units did not approve it.

6

Until such time as Chesapeake and its affiliates own less than 10% of the outstanding Trust units, the affirmative vote of the holders of a majority of common units (excluding common units owned by Chesapeake and its affiliates) and a majority of Trust units voting in person or by proxy at a meeting of such holders at which a quorum is present is required to:

• | dissolve the Trust (except in accordance with its terms); |

• | remove the Trustee or the Delaware Trustee; |

• | amend the Trust Agreement, the royalty conveyances, the administrative services agreement, the development agreement and the Drilling Support Lien (except with respect to certain matters that do not adversely affect the right of Trust unitholders in any material respect); |

• | merge, consolidate or convert the Trust with or into another entity; or |

• | approve the sale of all or any material part of the assets of the Trust. |

At any time when Chesapeake and its affiliates own less than 10% of the outstanding Trust units, the vote of the holders of a majority of Trust units, including units owned by Chesapeake, voting in person or by proxy at a meeting of such holders at which a quorum is present will be required to take the actions described above.

Certain amendments to the Trust Agreement may be made by the Trustee without approval of the Trust unitholders. The Trustee must consent before all or any part of the Trust assets can be sold except in connection with the dissolution of the Trust or limited sales directed by Chesapeake in conjunction with its sale of Underlying Properties.

Description of the Trust Agreement. The Trust was created under Delaware law as a separate legal entity to acquire and hold the Royalty Interests for the benefit of the Trust unitholders pursuant to the Trust Agreement among Chesapeake, the Trustee and the Delaware Trustee. The Royalty Interests are passive in nature and neither the Trust nor the Trustee has any control over, or responsibility for, costs relating to the operation of the Underlying Properties. Neither Chesapeake nor other operators of the Underlying Properties have any contractual commitments to the Trust to provide additional funding or to conduct further drilling on or to maintain their ownership interest in any of these properties other than the obligations of Chesapeake to drill the Development Wells.

The Trust Agreement provides that the Trust's business activities are generally limited to owning the Royalty Interests, being a party to the derivative contracts and any activities reasonably related thereto, including activities required or permitted by the terms of the conveyances related to the Royalty Interests. As a result, the Trust is not generally permitted to acquire other oil, NGL and natural gas properties or royalty interests. The Trust is not able to issue any additional Trust units.

Contractual Rights and Assets of the Trust. Contractual rights of the Trust include the development agreement, Drilling Support Lien and administrative services agreement. The assets of the Trust consist of the Royalty Interests, the derivative contracts and any cash and temporary investments being held for the payment of expenses and liabilities and for distribution to the Trust unitholders.

Duties and Powers of the Trustee. The duties and powers of the Trustee are specified in the Trust Agreement and by the laws of the State of Delaware, except as modified by the Trust Agreement. The Trust Agreement provides that the Trustee shall not have any duties or liabilities, including fiduciary duties, except as expressly set forth in the Trust Agreement and the duties and liabilities of the Trustee as set forth in the Trust Agreement replace any other duties and liabilities, including fiduciary duties, to which the Trustee might otherwise be subject.

7

The Trustee's principal duties consist of:

• | collecting cash proceeds attributable to the Royalty Interests; |

• | paying expenses, charges and obligations of the Trust from the Trust's assets; |

• | receiving and making payments under the derivative contracts; |

• | determining whether cash distributions exceed subordination or incentive thresholds, and making cash distributions to the unitholders and Chesapeake (with respect to incentive distributions) in accordance with the Trust Agreement; |

• | causing to be prepared and distributed a Schedule K-1 for each Trust unitholder and to prepare and file tax returns on behalf of the Trust; and |

• | causing to be prepared and filed reports required to be filed under the Securities Exchange Act of 1934, as amended, and by the rules of any securities exchange or quotation system on which the Trust units are listed or admitted to trading. |

Chesapeake will provide administrative and other services to the Trust in fulfillment of certain of the foregoing duties pursuant to the administrative services agreement.

The Trustee may create a cash reserve to pay for future expenses of the Trust. If the Trustee determines that the cash on hand and the cash to be received are insufficient to cover the Trust's expenses, the Trustee may cause the Trust to borrow funds required to pay the expenses. The Trust may borrow the funds from any person, including the Trustee or its affiliates or, as described below, Chesapeake. The terms of such indebtedness, if funds were loaned by the entity serving as Trustee or Delaware Trustee, must be similar to the terms which such entity would grant to a similarly situated, unaffiliated commercial customer, and such entity shall be entitled to enforce its rights with respect to any such indebtedness as if it were not then serving as Trustee or Delaware Trustee. If the Trust borrows funds, the Trust unitholders will not receive distributions until the borrowed funds are repaid (except in certain circumstances, where the Trust borrows funds from Chesapeake).

Each quarter, the Trustee will pay Trust obligations and expenses and distribute to the Trust unitholders the remaining proceeds received from the Royalty Interests and derivative contracts. The cash held by the Trustee as a reserve against future liabilities must be invested in:

• | interest-bearing obligations of the U.S. government; |

• | money market funds that invest only in U.S. government securities; |

• | repurchase agreements secured by interest-bearing obligations of the U.S. government; or |

• | bank certificates of deposit. |

Alternatively, cash held for distribution at the next distribution date may be held in a non-interest bearing account.

The Trustee withheld approximately $1.0 million from the first distribution to establish an initial cash reserve available for Trust expenses. If the Trustee uses its cash reserve (or any portion thereof) to pay or reimburse Trust liabilities or expenses, no further distributions will be made to unitholders (except in respect of any previously determined quarterly cash distribution amount) until the cash reserve is replenished. Additional cash reserves may also be established from time to time as determined by the Trustee to pay for future expenses of the Trust. This cash reserve will be part of the Trust estate and will bear interest at the same rate as other cash on hand in the Trust estate. Upon the dissolution of the Trust, after payment of Trust liabilities, the balance of the cash reserve (including accrued interest thereon) will be distributed to Trust unitholders on a pro rata basis.

The Trust may not acquire any asset except the Royalty Interests, the other assets described above under “Assets of the Trust”, interests acquired in connection with foreclosure under the Drilling Support Lien and cash and temporary cash investments, and it may not engage in any investment activity except investing cash on hand. Chesapeake, acting as hedge manager for the Trust, may cause the Trust to restructure existing derivative contracts in certain circumstances.

8

The Trust Agreement provides that the Trustee will not make business decisions affecting the assets of the Trust. However, the Trustee may:

• | prosecute or defend, and settle, claims of or against the Trust or its agents; |

• | foreclose on the Drilling Support Lien if Chesapeake does not satisfy its drilling obligation on or before June 30, 2016, and contract with a third-party operator to drill any remaining Development Wells, and transfer a portion of the Trust's assets in connection therewith; |

• | retain professionals and other third parties to provide services to the Trust; |

• | charge for its services as Trustee; |

• | retain funds to pay for future expenses and deposit them with one or more banks or financial institutions (which may include the Trustee to the extent permitted by law); |

• | lend funds at commercial rates to the Trust to pay the Trust's expenses; and |

• | seek reimbursement from the Trust for its out-of-pocket expenses. |

In discharging its duty to Trust unitholders, the Trustee may act in its discretion and will be liable to the Trust unitholders only for willful misconduct, bad faith or gross negligence, and certain taxes, fees and other charges based on fees, commissions or compensation received by the Trustee in connection with the transactions contemplated by the Trust Agreement. The Trustee is not liable for any act or omission of its agents or employees unless the Trustee acts with willful misconduct, bad faith or gross negligence in its selection and retention. The Trustee will be indemnified individually or as the Trustee for any liability or cost that it incurs in the administration of the Trust, except in cases of willful misconduct, bad faith or gross negligence. The Trustee has a lien on the assets of the Trust as security for this indemnification and its compensation earned as Trustee. Trust unitholders are not liable to the Trustee for any indemnification. The Trustee is obligated to ensure that all contractual liabilities of the Trust are limited to the assets of the Trust.

The Trust may merge or consolidate with or into, or convert into, one or more limited partnerships, general partnerships, corporations, business trusts, limited liability companies, or associations or unincorporated businesses if such transaction is agreed to by the Trustee and approved by the vote of the holders of a majority of the Trust units and a majority of the common units (excluding common units owned by Chesapeake and its affiliates) in each case voting in person or by proxy at a meeting of such holders at which a quorum is present and such transaction is permitted under the Delaware Statutory Trust Act and any other applicable law. At any time that Chesapeake and its affiliates collectively own less than 10% of the outstanding Trust units, however, the standard for approval will be the vote of a majority of the Trust units, including units owned by Chesapeake voting in person or by proxy at a meeting of such holders at which a quorum is present.

Trustee's Power to Sell Trust Assets. The Trustee may sell Trust assets, including the Royalty Interests, under any of the following circumstances:

• | the sale is requested by Chesapeake, following the satisfaction of its drilling obligation, in accordance with the provisions of the Trust Agreement; |

• | the sale is approved by the vote of holders representing a majority of the Trust units and a majority of the common units (excluding common units owned by Chesapeake and its affiliates) in each case voting in person or by proxy at a meeting of such holders at which a quorum is present; except that at any time that Chesapeake and its affiliates collectively own less than 10% of the outstanding Trust units, the standard for approval will be the vote of a majority of the Trust units, including units owned by Chesapeake voting in person or by proxy at a meeting of such holders at which a quorum is present; or |

• | in connection with a foreclosure on the Drilling Support Lien. |

Upon dissolution of the Trust the Trustee must sell the remaining Royalty Interests. No Trust unitholder approval is required in this event.

The Trustee will distribute the net proceeds from any sale of the Royalty Interests and other assets to the Trust unitholders after payment or reasonable provision for payment of the liabilities of the Trust.

9

Dispute Resolution. To the fullest extent permitted by law, any dispute, controversy or claim that may arise between Chesapeake and the Trustee relating to the Trust will be submitted to binding arbitration before a panel of three arbitrators.

Trust Fees and Expenses. The Trust is a party to derivative contracts and the Trust previously has had, and in the future could have, payment obligations under such arrangements. Otherwise, the Trust does not conduct an active business and the Trustee has little power to incur obligations. As a result, it is expected that the Trust will only incur liabilities for routine administrative expenses, such as legal, accounting, tax advisory, engineering, printing and other administrative and out-of-pocket fees and expenses incurred by or at the direction of the Trustee or the Delaware Trustee, including tax return and Schedule K-1 preparation and mailing costs; independent auditor fees; and registrar and transfer agent fees. The Trust is also responsible for paying costs associated with annual and quarterly reports to unitholders. Moreover, the Trustee's and the Delaware Trustee's compensation, and the fee payable to Chesapeake pursuant to the administrative services agreement, are paid out of the Trust's assets.

Chesapeake Obligation to Fund Trust Expenses in Certain Circumstances. Chesapeake has agreed that, if at any time the Trust's cash on hand (including available cash reserves) is not sufficient to pay the Trust's ordinary course expenses as they become due, Chesapeake will lend funds to the Trust necessary to pay such expenses. Any funds loaned by Chesapeake pursuant to this commitment will be limited to the payment of current accounts payable or other obligations to trade creditors in connection with obtaining goods or services or the payment of other accrued current liabilities arising in the ordinary course of the Trust's business, and may not be used to satisfy Trust indebtedness for borrowed money. If Chesapeake lends funds pursuant to this commitment, unless Chesapeake agrees otherwise, no further distributions will be made to unitholders (except in respect of any previously determined quarterly cash distribution amount) until such loan is repaid. Any such loan will be on an unsecured basis, and the terms of such loan will be substantially the same as those which would be obtained in an arms' length transaction between Chesapeake and an unaffiliated third party.

Duration of the Trust; Sale of Royalty Interests. The Trust will dissolve and begin to liquidate on June 30, 2031, or earlier upon certain events, and will soon thereafter wind up its affairs and terminate. At the Termination Date the Term Royalties will revert automatically to Chesapeake. Following the Termination Date, the Perpetual Royalties will be sold by the Trust and the net proceeds of the sale, as well as any remaining Trust cash reserves, will be distributed to the unitholders pro rata. Chesapeake will have a right of first refusal to purchase the Perpetual Royalties from the Trust following the Termination Date.

The Trust will not dissolve until the Termination Date, which is June 30, 2031, unless:

• | the Trust sells all of the Royalty Interests; |

• | cash available for distribution is less than $1.0 million for any four consecutive quarters; |

• | the holders of a majority of the Trust units and a majority of the common units (excluding common units owned by Chesapeake and its affiliates) in each case voting in person or by proxy at a meeting of such holders at which a quorum is present vote in favor of dissolution; except that at any time that Chesapeake and its affiliates collectively own less than 10% of the outstanding Trust units, the standard for approval will be a majority of the Trust units, including units owned by Chesapeake voting in person or by proxy at a meeting of such holders at which a quorum is present; or |

• | the Trust is judicially dissolved. |

In the case of any of the foregoing, the Trustee would sell all of the Trust's assets, either by private sale or public auction, and distribute the net proceeds of the sale to the Trust unitholders after payment, or reasonable provision for payment, of all Trust liabilities.

Federal Income Tax Considerations

The Trust's federal income tax reporting position is that it is classified as a partnership for federal and applicable state income tax purposes. This position relies on the opinion of Bracewell & Giuliani L.L.P., counsel to Chesapeake and the Trust rendered in connection with the initial public offering of the Trust units, in which counsel opined that at least 90% of the Trust's gross income is qualifying income within the meaning of Section 7704 of the Internal Revenue Code of 1986, as amended. The Trust's federal income tax reporting positions are consistent with the Federal Income Tax Considerations section in the prospectus filed by the Trust on November 14, 2011 in connection with the offering of its common units to the public (the “Federal Income Tax Considerations Section in the Prospectus”). However, as

10

discussed in detail below under Item 1A. Risk Factors - Tax Risks Related to the Trust's Common Units, the Trust has not requested a ruling from the IRS regarding its United States federal income tax reporting positions and its positions may not be sustained by a court or if contested by the IRS.

The material federal income tax considerations that may be relevant to certain Trust unitholders were discussed in the Federal Income Tax Considerations Section in the Prospectus. Unitholders and prospective unitholders should review the Federal Income Tax Considerations Section in the Prospectus.

Competition and Markets

The oil and gas industry is highly competitive. Chesapeake competes with both major integrated and other independent oil and gas companies in acquiring desirable leasehold acreage, producing properties and the equipment and expertise necessary to explore, develop and operate its properties and market its production. Some of Chesapeake's competitors may have larger financial and other resources than Chesapeake. The oil and gas industry also faces competition from alternative fuel sources, including other fossil fuels such as coal and imported liquefied natural gas. Competitive conditions may be affected by future legislation and regulations as the U.S. develops new energy and climate-related policies. In addition, some of Chesapeake's larger competitors may have a competitive advantage when responding to factors that affect demand for oil, NGL and natural gas production, such as changing prices, domestic and foreign policy conditions, weather conditions, the price and availability of alternative fuels, the proximity and capacity of pipelines and other transportation facilities, and overall economic conditions. Chesapeake believes that its technological expertise, its exploration, land drilling and production capabilities and the experience of its management generally enable it to compete effectively.

Future price fluctuations of oil, NGL and natural gas will directly impact Trust distributions, estimates of reserves attributable to the Trust's interest, and estimated and actual future net revenues to the Trust. In view of the many uncertainties that affect the supply and demand for oil, NGL and natural gas, neither the Trust nor Chesapeake can make reliable predictions of future supply and demand for oil, NGL and natural gas, future oil, NGL and natural gas prices or the effect of future oil, NGL and natural gas prices on the Trust.

Environmental Matters and Regulation

General. All of Chesapeake's operations are conducted onshore in the United States. The U.S. oil, NGL and natural gas industry is regulated at the federal, state and local levels, and some of the laws, rules and regulations that govern its operations carry substantial penalties for noncompliance. These regulatory burdens increase Chesapeake's cost of doing business and, consequently, affect its profitability.

Regulation of Oil and Natural Gas Operations. The laws and regulations applicable to Chesapeake's exploration and production operations include requirements for permits to drill and to conduct other operations and for provision of financial assurances (such as bonds) covering drilling and well operations. Other activities subject to regulations include, but are not limited to:

• | the location of wells; |

• | the method of drilling and completing wells; |

• | the surface use and restoration of properties upon which wells are drilled; |

• | water withdrawal; |

• | the plugging and abandoning of wells; |

• | the disposal of fluids used or other wastes generated in connection with operations; |

• | the marketing, transportation and reporting of production; and |

• | the valuation and payment of royalties. |

Chesapeake's operations are also subject to various conservation regulations. These include the regulation of the size of drilling and spacing units (regarding the density of wells that may be drilled in a particular area) and the unitization or pooling of oil and natural gas properties. In this regard, some states, including Oklahoma, allow the forced pooling or integration of tracts to facilitate exploration, while other states, such as Texas and Pennsylvania, rely on voluntary pooling of lands and leases. In areas where pooling is voluntary, it may be more difficult to form units and

11

therefore, more difficult to fully develop a project if the operator owns less than 100% of the leasehold. In addition, state conservation laws establish maximum rates of production from oil and natural gas wells, generally prohibit the venting or flaring of natural gas and impose certain requirements regarding the ratability of production. The effect of these regulations is to limit the amount of oil, NGL and natural gas Chesapeake can produce and to limit the number of wells and the locations at which it can drill.

Chesapeake operates a number of natural gas gathering systems. The U.S. Department of Transportation and certain state agencies regulate the safety and operating aspects of the transportation and storage activities of these facilities. There is currently no price regulation of the company's sales of oil, NGL and natural gas, although governmental agencies may elect in the future to regulate certain sales.

Chesapeake does not anticipate that compliance with existing laws and regulations governing exploration, production and natural gas gathering will have a material adverse effect upon its capital expenditures, earnings or competitive position.

Environmental, Health and Safety Regulation. The business operations of Chesapeake and its ownership and operation of oil, NGL and natural gas interests are subject to various federal, state and local environmental, health and safety laws and regulations pertaining to the release, emission or discharge of materials into the environment, the generation, storage, transportation, handling and disposal of materials (including solid and hazardous wastes), the safety of employees, or otherwise relating to pollution, preservation, remediation or protection of human health and safety, natural resources, wildlife or the environment. Chesapeake must take into account the cost of complying with environmental regulations in planning, designing, constructing, drilling, operating and abandoning wells and related surface facilities. In most instances, the regulatory frameworks relate to the handling of drilling and production materials, the disposal of drilling and production wastes, and the protection of water and air. In addition, Chesapeake's operations may require it to obtain permits for, among other things,

• | air emissions; |

• | the construction and operation of underground injection wells to dispose of produced saltwater and other non-hazardous oilfield wastes; and |

• | the construction and operation of surface pits to contain drilling muds and other non-hazardous fluids associated with drilling operations. |

Delays in obtaining permits, an inability to obtain new permits or revocation of Chesapeake's current permits due to noncompliance could result in the imposition of fines and could inhibit Chesapeake's ability to drill the remaining Development Wells or continue production from the Producing Wells and completed Development Wells.