Attached files

| file | filename |

|---|---|

| EX-99.1 - EXHIBIT 99.1 - LNB BANCORP INC | a50576010ex99_1.htm |

| 8-K - LNB BANCORP, INC. 8-K - LNB BANCORP INC | a50576010.htm |

Exhibit 99.2

Slide: 1 LNB Bancorp, Inc. NASDAQ: LNBB Investor Presentation February 2013

2 Forward Looking StatementsThis presentation contains forward-looking statements relating to the financial condition, results of operations and business of LNB Bancorp, Inc., including certain plans, expectations, goals and statements which are subject to numerous assumptions, risks and uncertainties. Actual results could differ materially from those indicated by such statements for a variety of reasons. Among the important factors that could cause actual results to differ materially from those indicated are movements in interest rates, changes in the mix of the Company’s business, competitive pressures, changes in general economic conditions, the nature, extent and timing of governmental actions and reforms and the risk factors detailed in the Company’s 2011 Annual Report on Form 10-K and subsequent current and periodic reports and registration statements filed with the Securities and Exchange Commission. All forward-looking statements included in this presentation are based on information available as of the date hereof. LNB Bancorp, Inc. undertakes no obligation to update these forward-looking statements to reflect events or circumstances after the date of this presentation.

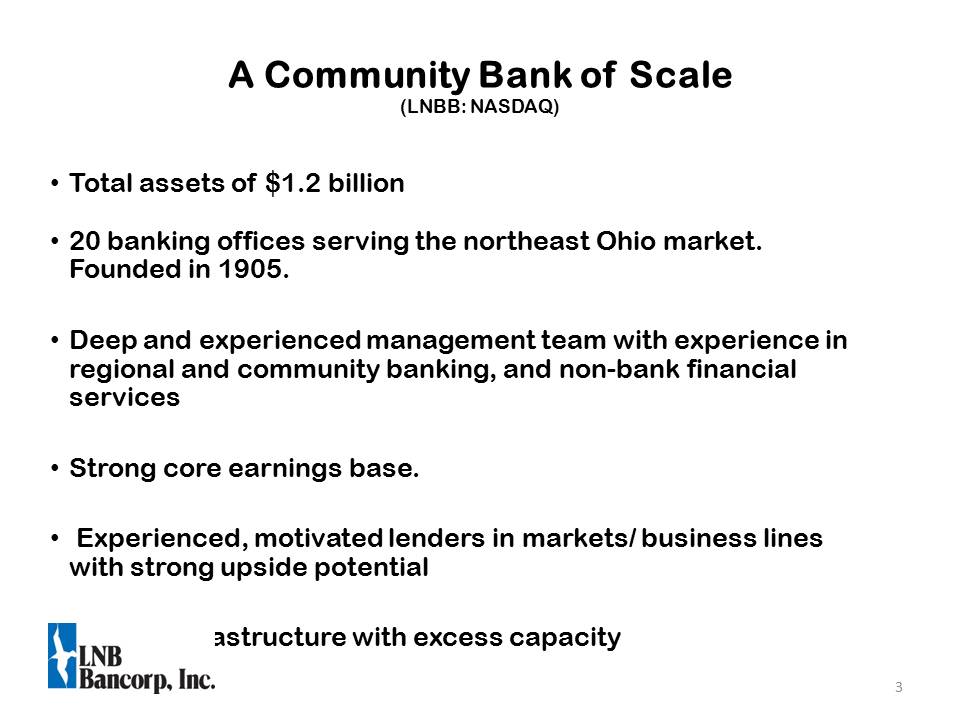

3 A Community Bank of Scale (LNBB: NASDAQ) Total assets of $1.2 billion 20 banking offices serving the northeast Ohio market. Founded in 1905. Deep and experienced management team with experience in regional and community banking, and non-bank financial services Strong core earnings base. Experienced, motivated lenders in markets/ business lines with strong upside potential Robust infrastructure with excess capacity

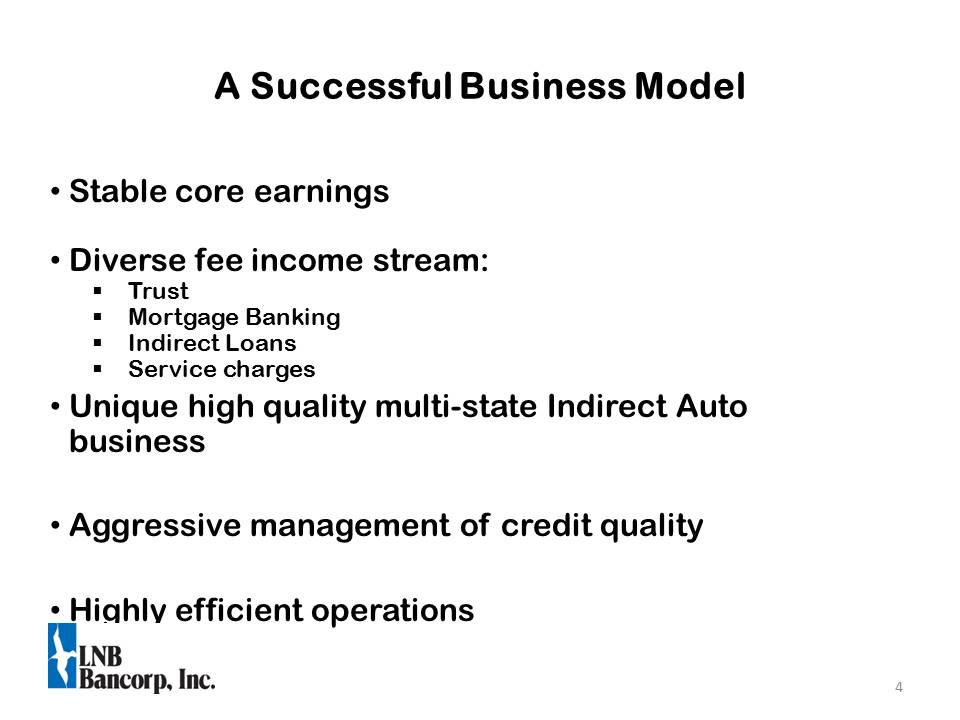

4 A Successful Business Model Stable core earnings Diverse fee income stream: Trust Mortgage Banking Indirect Loans Service charges Unique high quality multi-state Indirect Auto business Aggressive management of credit quality Highly efficient operations Other Placeholder

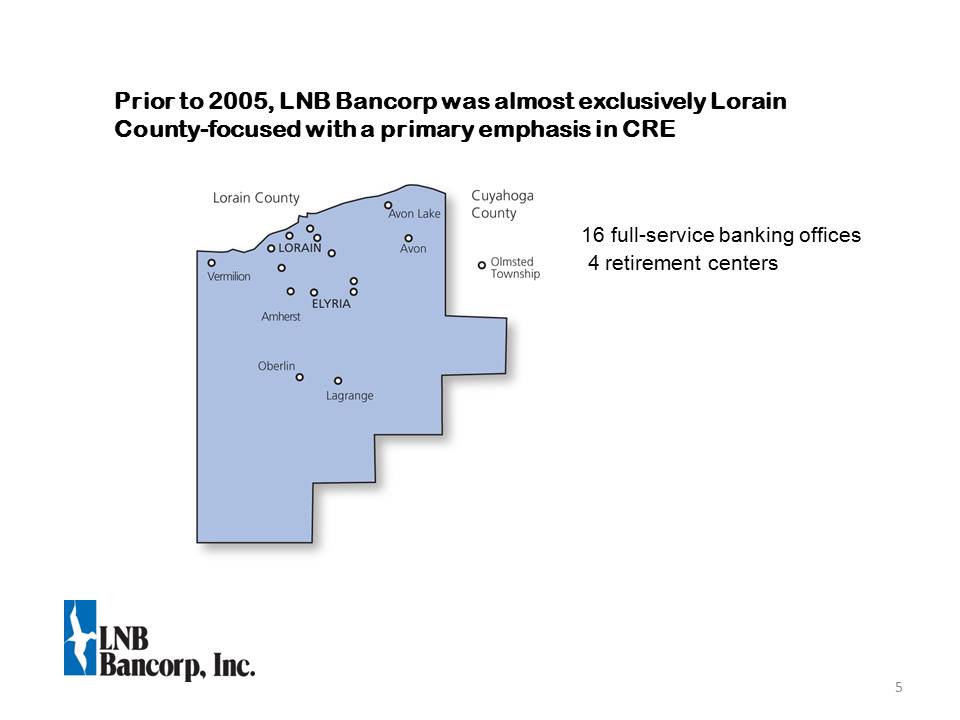

5 Prior to 2005, LNB Bancorp was almost exclusively Lorain County-focused with a primary emphasis in CRE 16 full-service banking offices 4 retirement centers

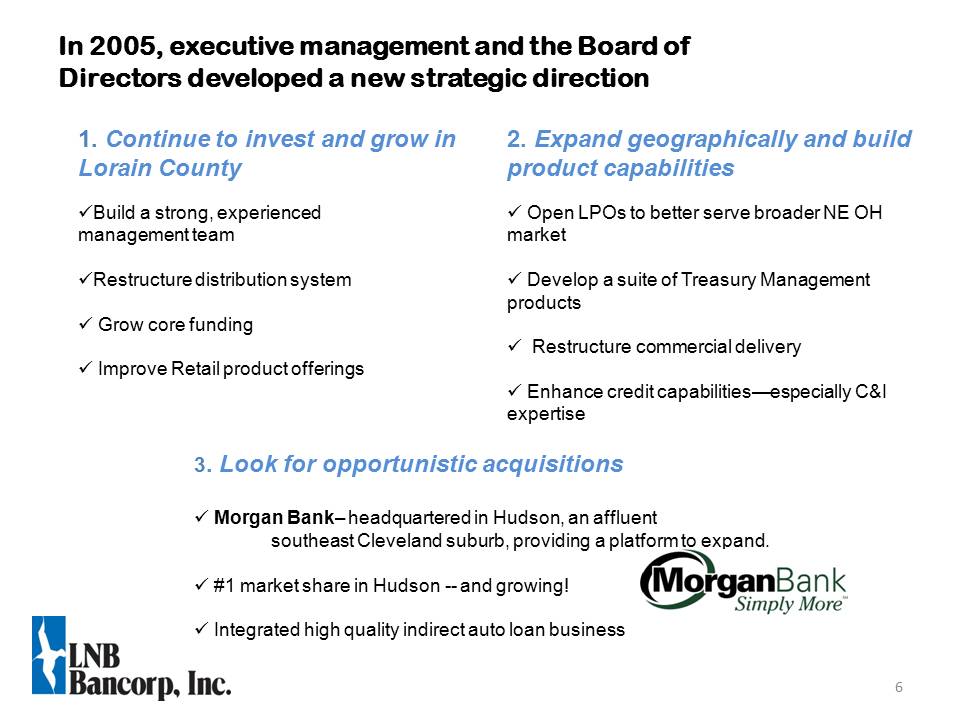

6 1. Continue to invest and grow in Lorain County Build a strong, experienced management team Restructure distribution system Grow core funding Improve Retail product offerings In 2005, executive management and the Board of Directors developed a new strategic direction 2. Expand geographically and build product capabilities Open LPOs to better serve broader NE OH market Develop a suite of Treasury Management products Restructure commercial delivery Enhance credit capabilities—especially C&I expertise 3. Look for opportunistic acquisitionsMorgan Bank– headquartered in Hudson, an affluent southeast Cleveland suburb, providing a platform to expand. #1 market share in Hudson -- and growing! Integrated high quality indirect auto loan business

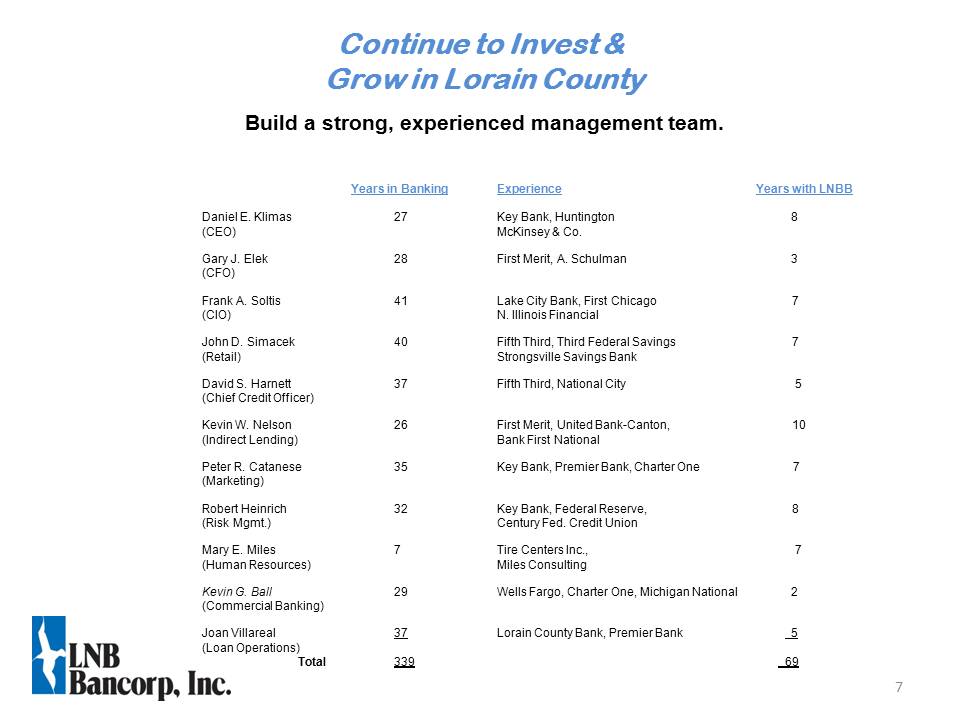

7 Build a strong, experienced management team. Continue to Invest & Grow in Lorain County Years in Banking Experience Years with LNBB Daniel E. Klimas 27 Key Bank, Huntington 8 (CEO) McKinsey & Co. Gary J. Elek 28 First Merit, A. Schulman 3 (CFO) Frank A. Soltis 41 Lake City Bank, First Chicago 7 (CIO) N. Illinois Financial John D. Simacek 40 Fifth Third, Third Federal Savings 7(Retail) Strongsville Savings BankDavid S. Harnett37 Fifth Third, National City 5 (Chief Credit Officer) Kevin W. Nelson 26 First Merit, United Bank-Canton, 10 (Indirect Lending) Bank First National Peter R. Catanese 35 Key Bank, Premier Bank, Charter One 7 (Marketing) Robert Heinrich 32 Key Bank, Federal Reserve, 8 (Risk Mgmt.) Century Fed. Credit Union Mary E. Miles 7 Tire Centers Inc., 7 (Human Resources) Miles Consulting Kevin G. Ball 29 Wells Fargo, Charter One, Michigan National 2 (Commercial Banking) Joan Villareal 37 Lorain County Bank, Premier Bank 5 (Loan Operations) Total 339 69

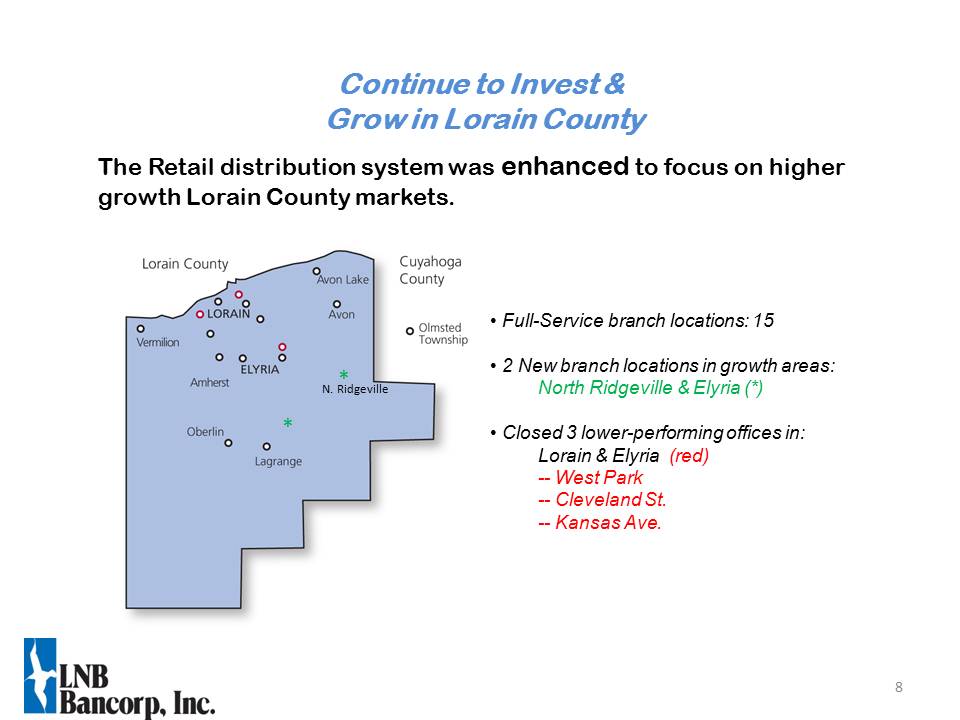

8 Full-Service branch locations: 15 2 New branch locations in growth areas:North Ridgeville & Elyria (*) Closed 3 lower-performing offices in:Lorain & Elyria (red)-- West Park-- Cleveland St.-- Kansas Ave. The Retail distribution system was enhanced to focus on higher growth Lorain County markets. N. Ridgeville Continue to Invest & Grow in Lorain County

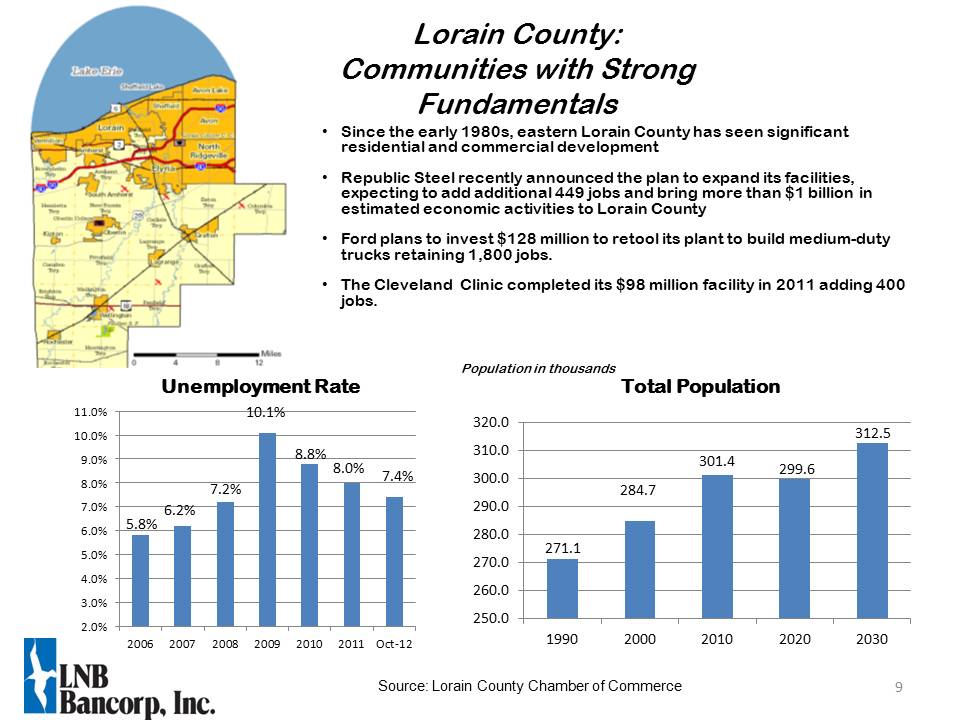

9 Lorain County:Communities with Strong Fundamentals Population in thousands Total Population Source: Lorain County Chamber of Commerce Since the early 1980s, eastern Lorain County has seen significant residential and commercial development Republic Steel recently announced the plan to expand its facilities, expecting to add additional 449 jobs and bring more than $1 billion in estimated economic activities to Lorain County Ford plans to invest $128 million to retool its plant to build medium-duty trucks retaining 1,800 jobs. The Cleveland Clinic completed its $98 million facility in 2011 adding 400 jobs. Unemployment Rate

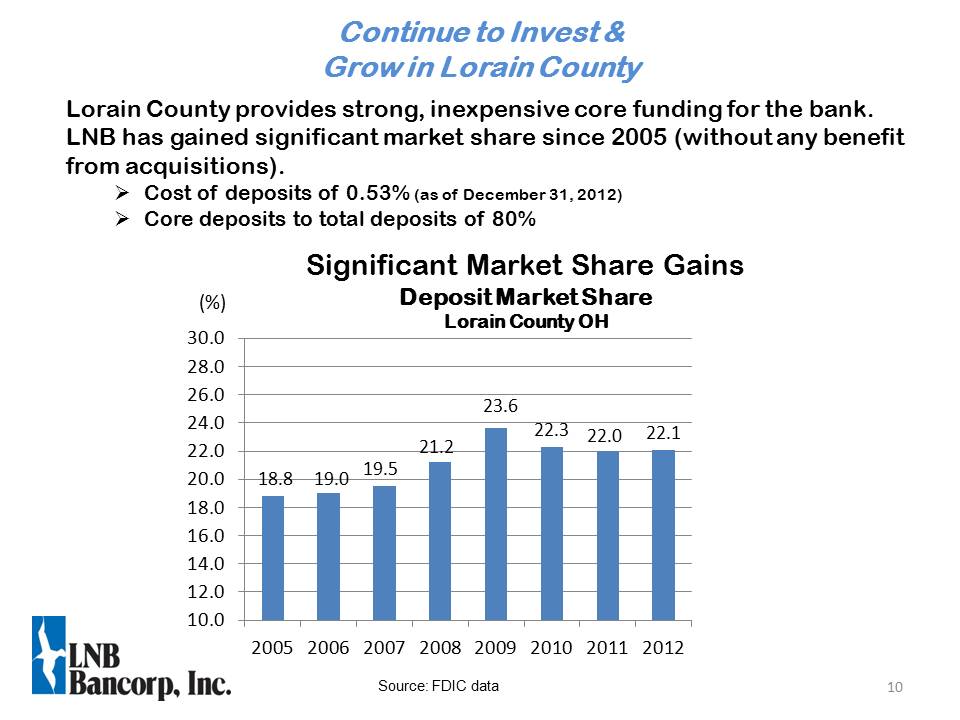

10 Significant Market Share Gains Deposit Market Share Lorain County OH Lorain County provides strong, inexpensive core funding for the bank. LNB has gained significant market share since 2005 (without any benefit from acquisitions). Cost of deposits of 0.53% (as of December 31, 2012) Core deposits to total deposits of 80% (%) Source: FDIC data Continue to Invest & Grow in Lorain County

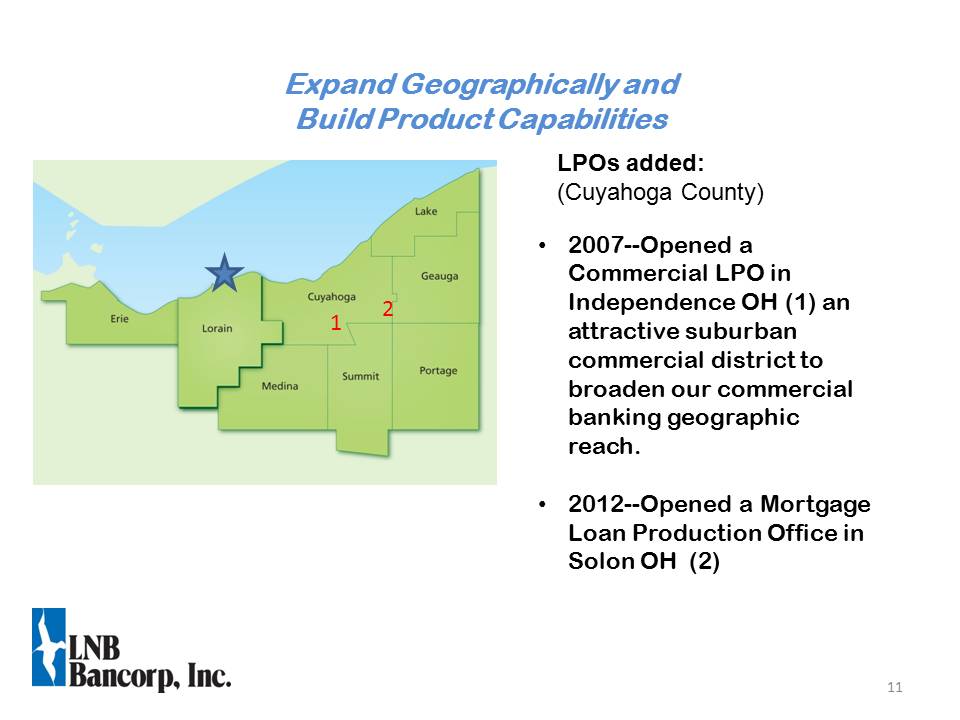

11 2007--Opened a Commercial LPO in Independence OH (1) an attractive suburban commercial district to broaden our commercial banking geographic reach. 2012--Opened a Mortgage Loan Production Office in Solon OH (2) LPOs added: (Cuyahoga County) 1 Expand Geographically and Build Product Capabilities 2

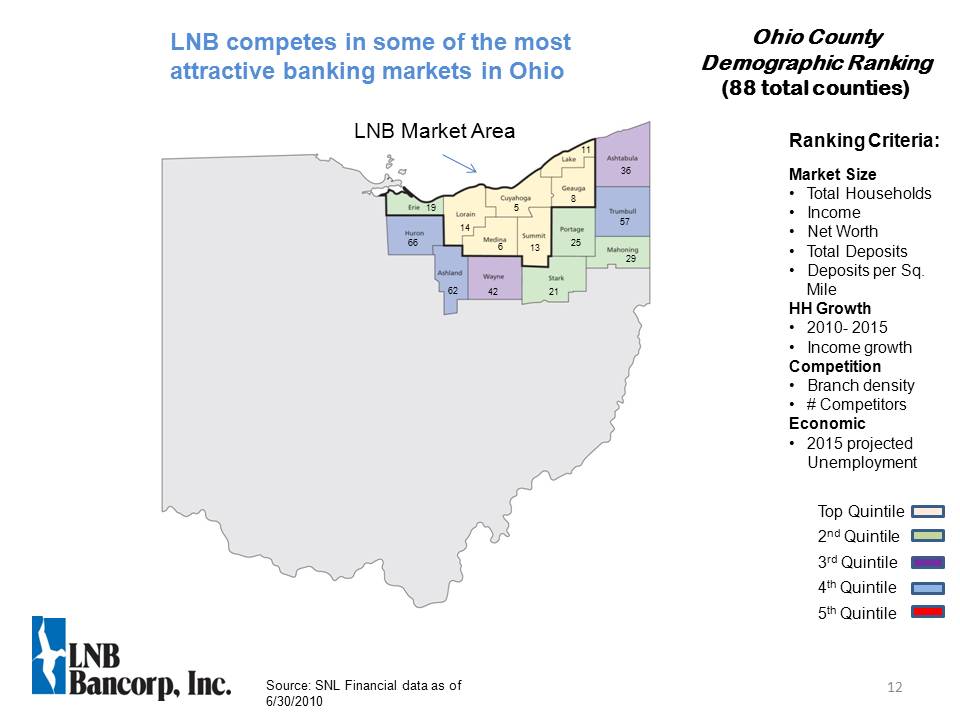

12 Ohio County Demographic Ranking (88 total counties) Source: SNL Financial data as of 6/30/2010 Top Quintile 2nd Quintile 3rd Quintile 4th Quintile 5th Quintile Ranking Criteria:Market Size Total Households Income Net Worth Total Deposits Deposits per Sq. Mile HH Growth 2010- 2015 Income growth Competition Branch density # Competitors Economic 2015 projected Unemployment LNB Market Area 36 57 29 21 25 8 5 13 6 14 42 62 66 19 11 LNB competes in some of the most attractive banking markets in Ohio

13 We significantly enhanced our commercial banking capabilities to support C&I lending and a broader geographic reach. Commercial Banking Improvements Treasury Management capabilities enhanced: Sweep product Remote check capture Lockbox Positive Pay CDARS network Developed Sales Executive & Portfolio Manager structure to enhance sales & credit capabilities. 70%+ of new commercial business now generated outside of Lorain County. Expand Geographically and Build Product Capabilities

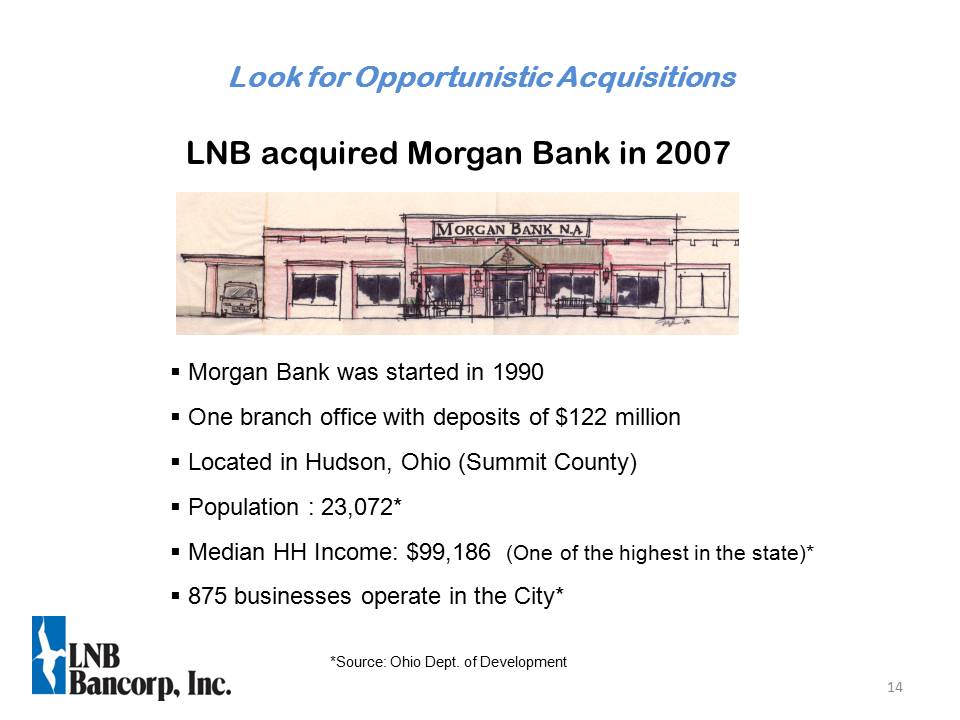

14 LNB acquired Morgan Bank in 2007 Morgan Bank was started in 1990 One branch office with deposits of $122 million Located in Hudson, Ohio (Summit County) Population : 23,072* Median HH Income: $99,186 (One of the highest in the state)* 875 businesses operate in the City* Look for Opportunistic Acquisitions *Source: Ohio Dept. of Development

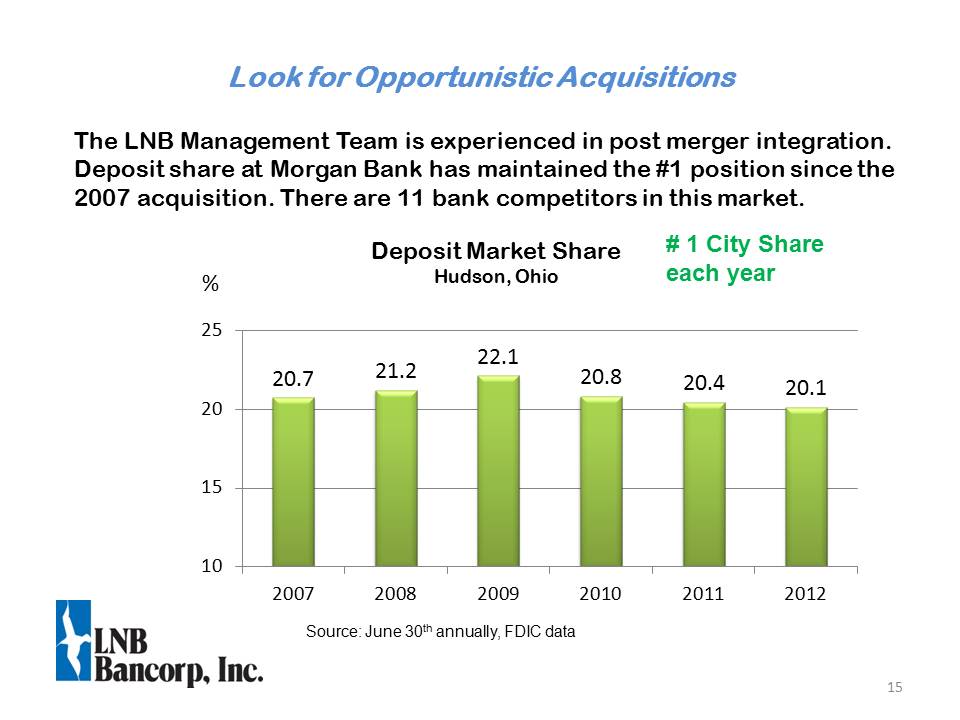

15 Deposit Market Share Hudson, Ohio # 1 City Share each year The LNB Management Team is experienced in post merger integration. Deposit share at Morgan Bank has maintained the #1 position since the 2007 acquisition. There are 11 bank competitors in this market. Source: June 30th annually, FDIC data % Look for Opportunistic Acquisitions

16 Indirect Auto Business 15 years of experience Originates loans through over 650 dealers in: Ohio, Kentucky, Tennessee, Georgia, Indiana, North Carolina and Pennsylvania Average credit score of 779 2013 Plan is to generate $160 million in assets The Indirect Auto business provides high quality assets to LNB’s balance sheet and generates recurring fee income through sales of these assets to other community banks. Look for Opportunistic Acquisitions

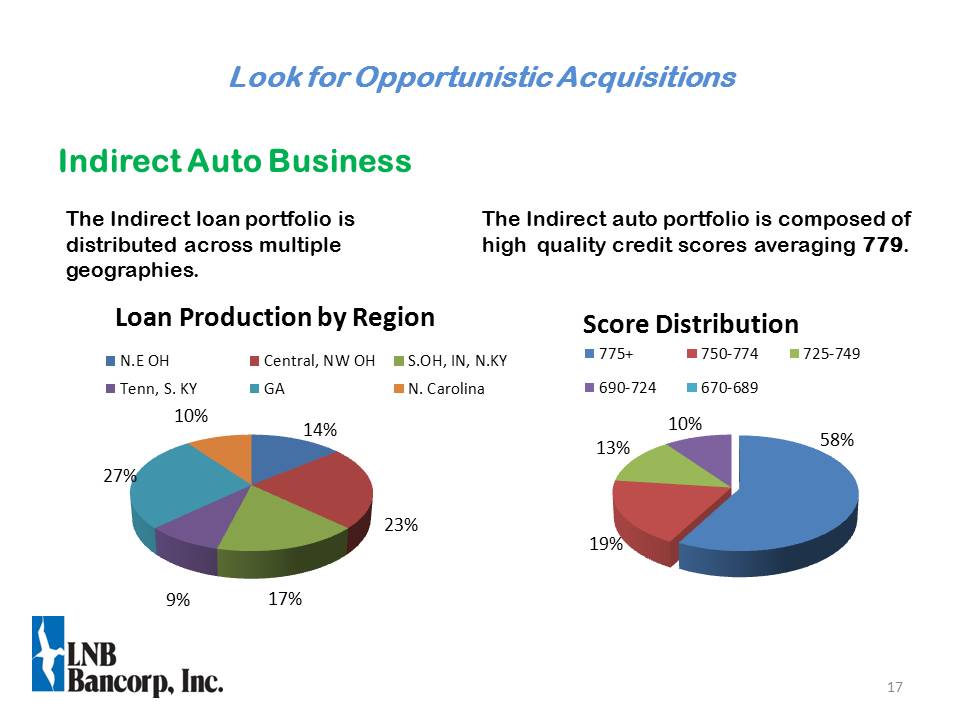

17 Indirect Auto Business The Indirect loan portfolio is distributed across multiple geographies. Look for Opportunistic Acquisitions The Indirect auto portfolio is composed of high quality credit scores averaging 779.

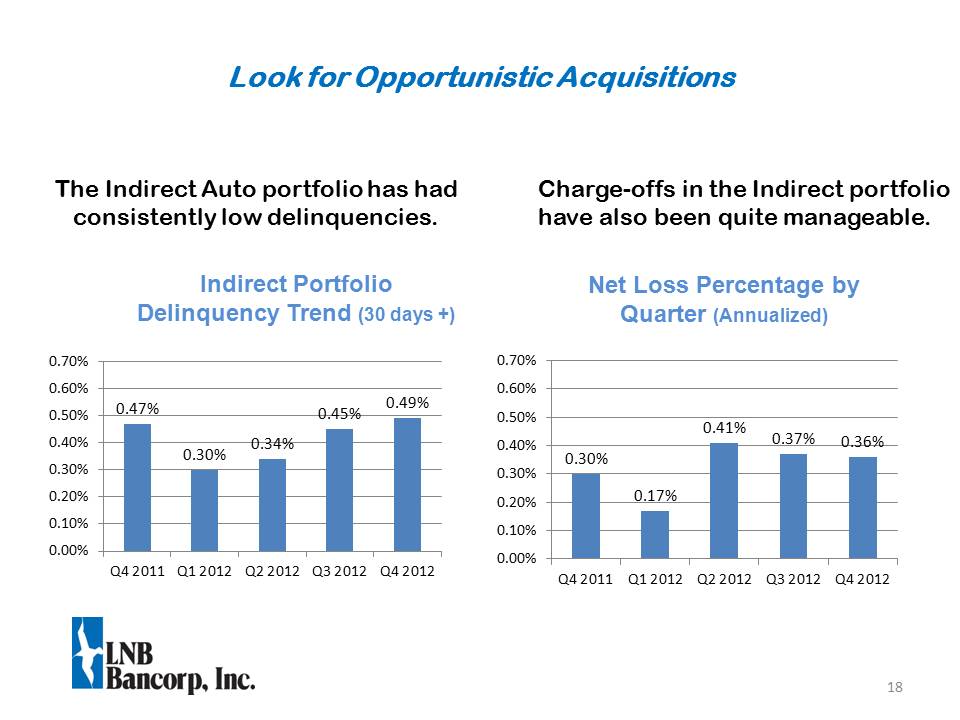

18 The Indirect Auto portfolio has had consistently low delinquencies. Look for Opportunistic Acquisitions Charge-offs in the Indirect portfolio have also been quite manageable. Indirect Portfolio Delinquency Trend (30 days +) Net Loss Percentage by Quarter (Annualized)

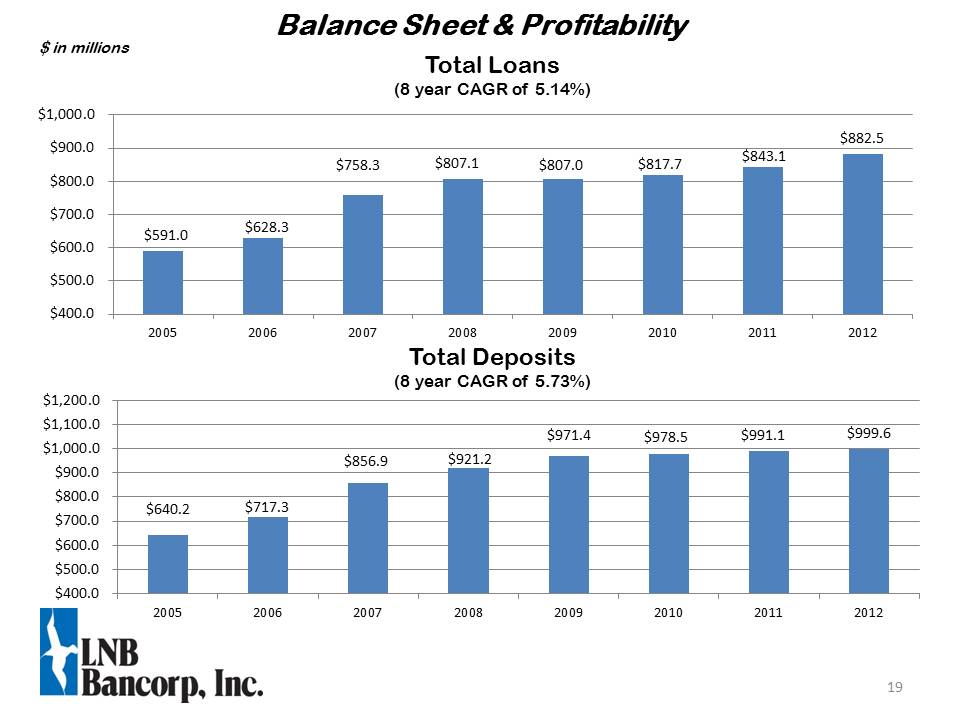

19 Balance Sheet & Profitability Total Deposits (8 year CAGR of 5.73%) $ in millions Total Loans (8 year CAGR of 5.14%)

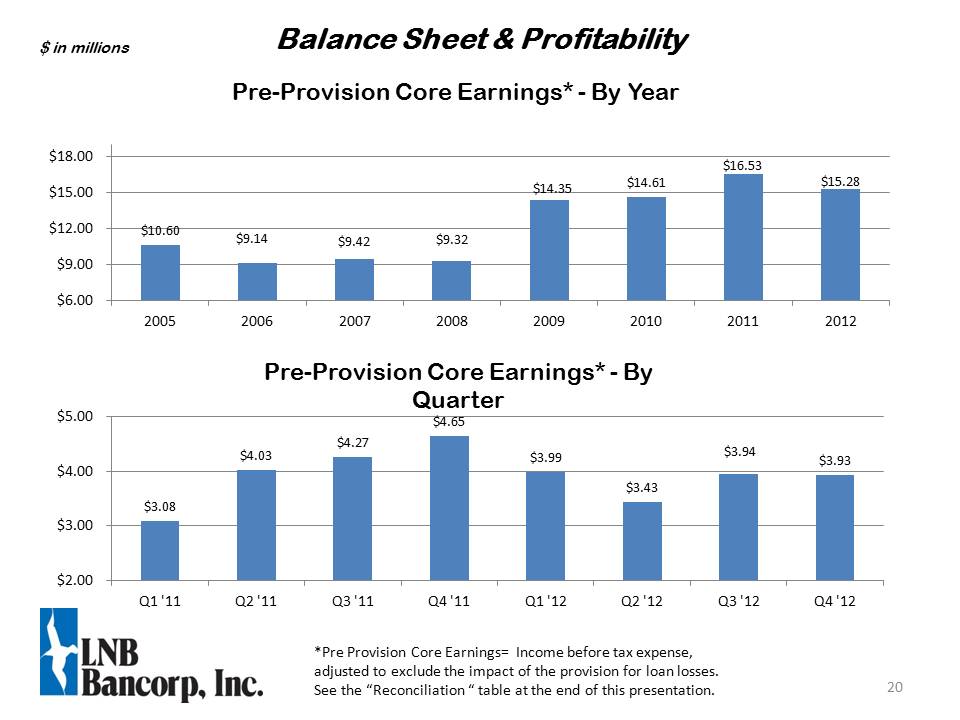

20 Balance Sheet & Profitability *Pre Provision Core Earnings= Income before tax expense, adjusted to exclude the impact of the provision for loan losses. See the “Reconciliation “ table at the end of this presentation. Pre-Provision Core Earnings* - By Year Pre-Provision Core Earnings* - By Quarter $ in millions

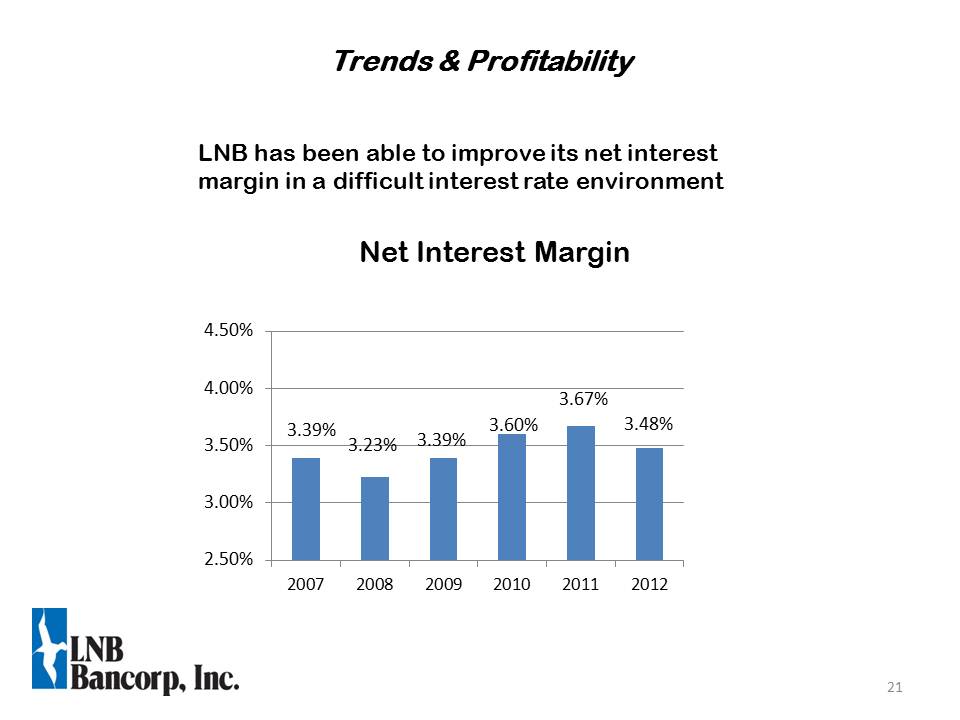

21 Net Interest Margin LNB has been able to improve its net interest margin in a difficult interest rate environment Trends & Profitability

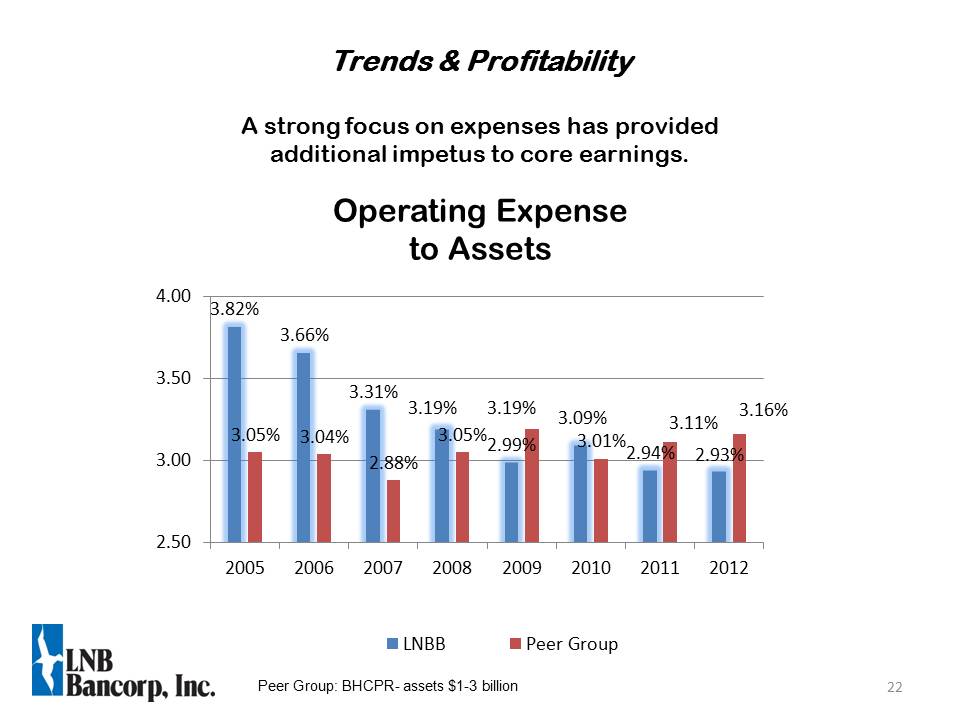

22 Operating Expenseto Assets A strong focus on expenses has provided additional impetus to core earnings. Peer Group: BHCPR- assets $1-3 billion Trends & Profitability

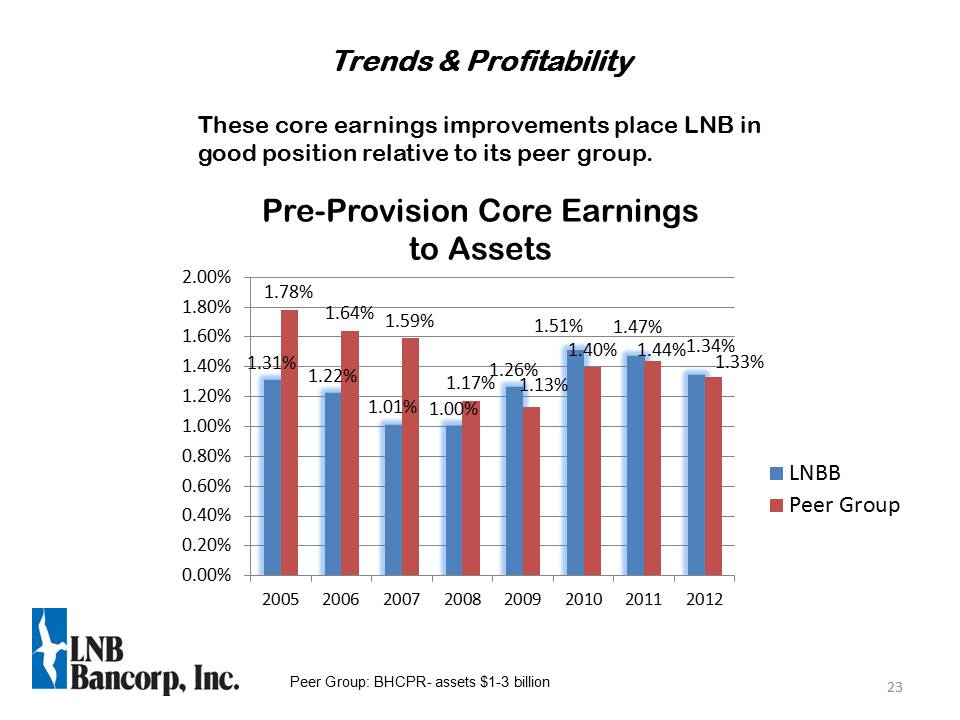

23 Pre-Provision Core Earningsto Assets These core earnings improvements place LNB in good position relative to its peer group. Trends & Profitability Peer Group: BHCPR- assets $1-3 billion

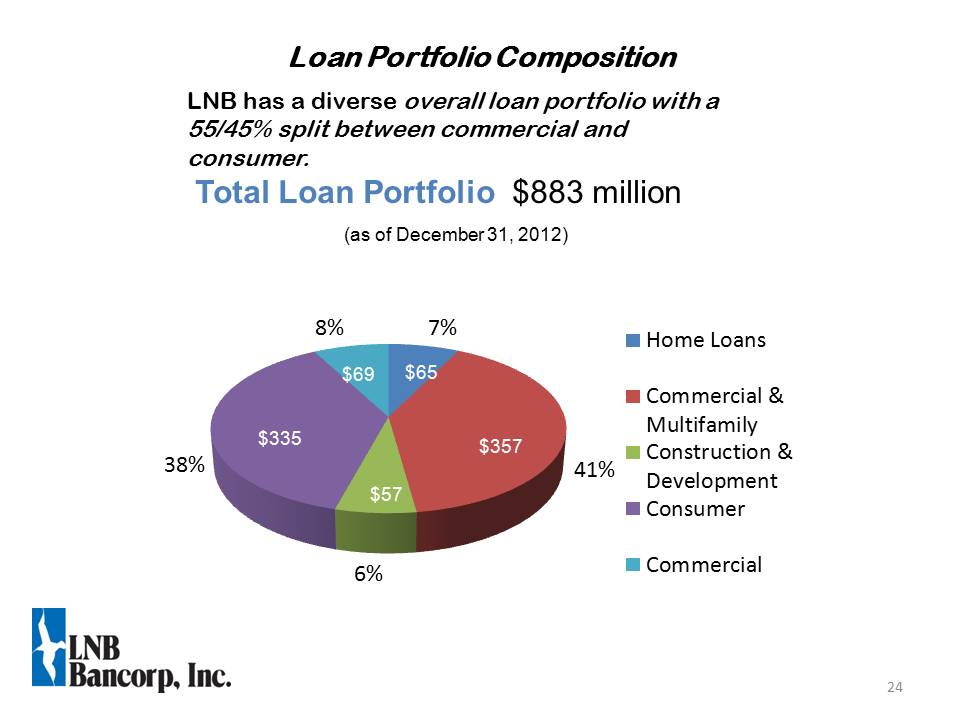

24 Total Loan Portfolio $883 million (as of December 31, 2012) LNB has a diverse overall loan portfolio with a 55/45% split between commercial and consumer. Loan Portfolio Composition

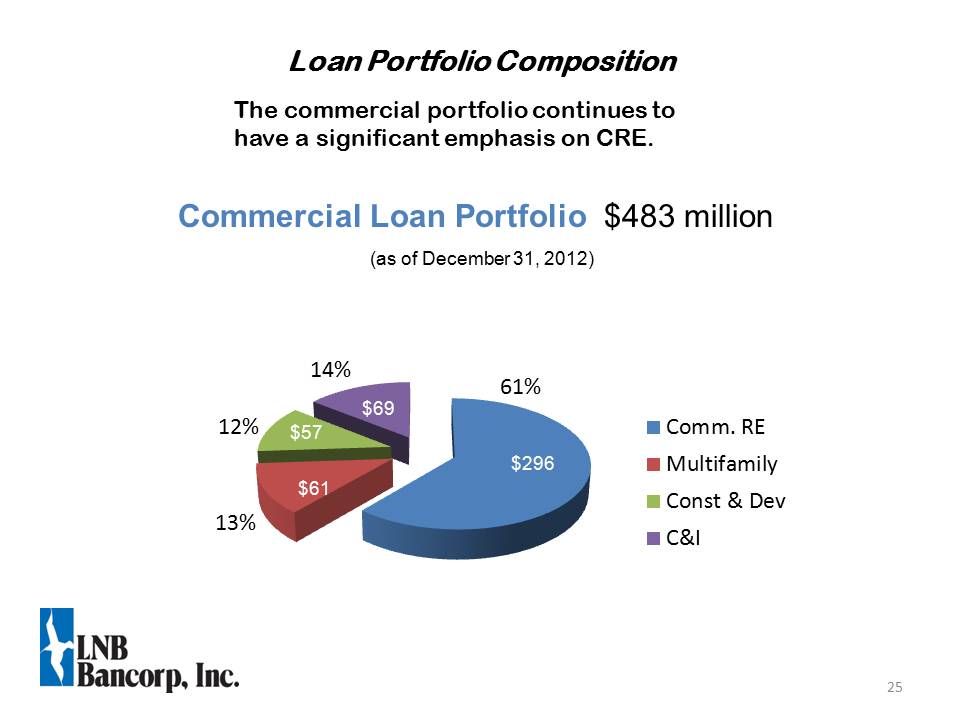

25 Commercial Loan Portfolio $483 million (as of December 31, 2012) The commercial portfolio continues to have a significant emphasis on CRE. Loan Portfolio Composition $296

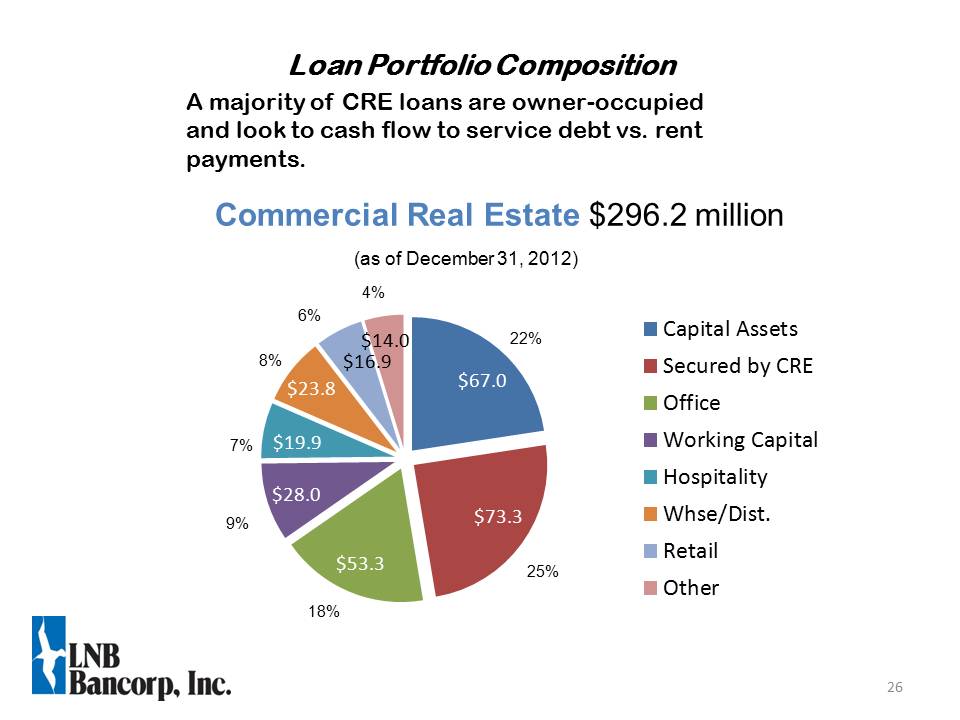

26 Commercial Real Estate $296.2 million (as of December 31, 2012) A majority of CRE loans are owner-occupied and look to cash flow to service debt vs. rent payments. Loan Portfolio Composition 7% 8%

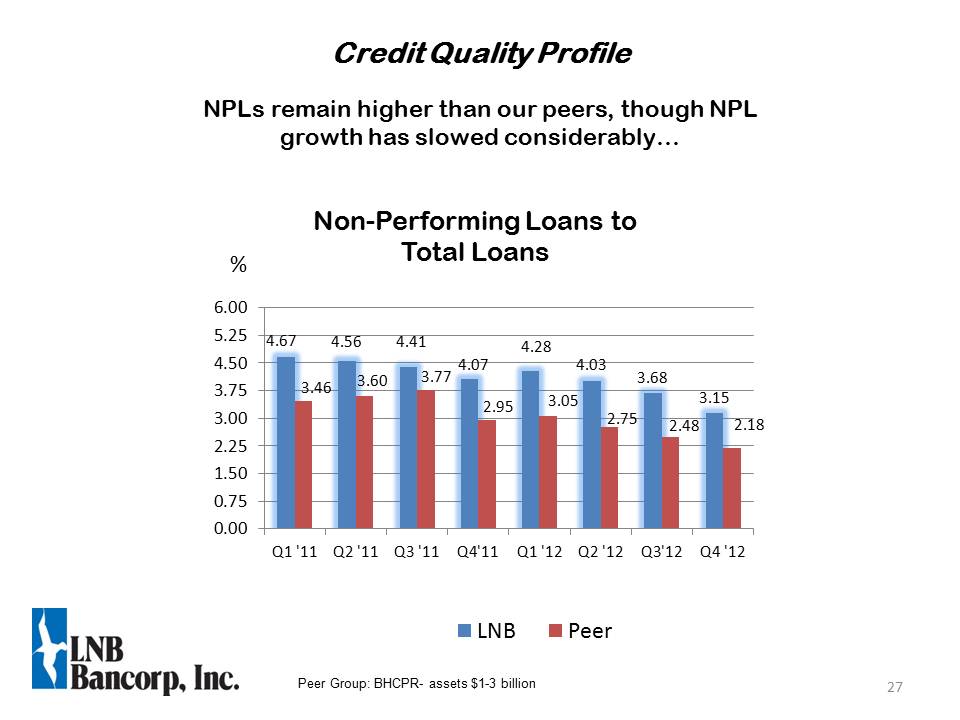

27 Non-Performing Loans to Total Loans NPLs remain higher than our peers, though NPL growth has slowed considerably… % Credit Quality Profile Peer Group: BHCPR- assets $1-3 billion

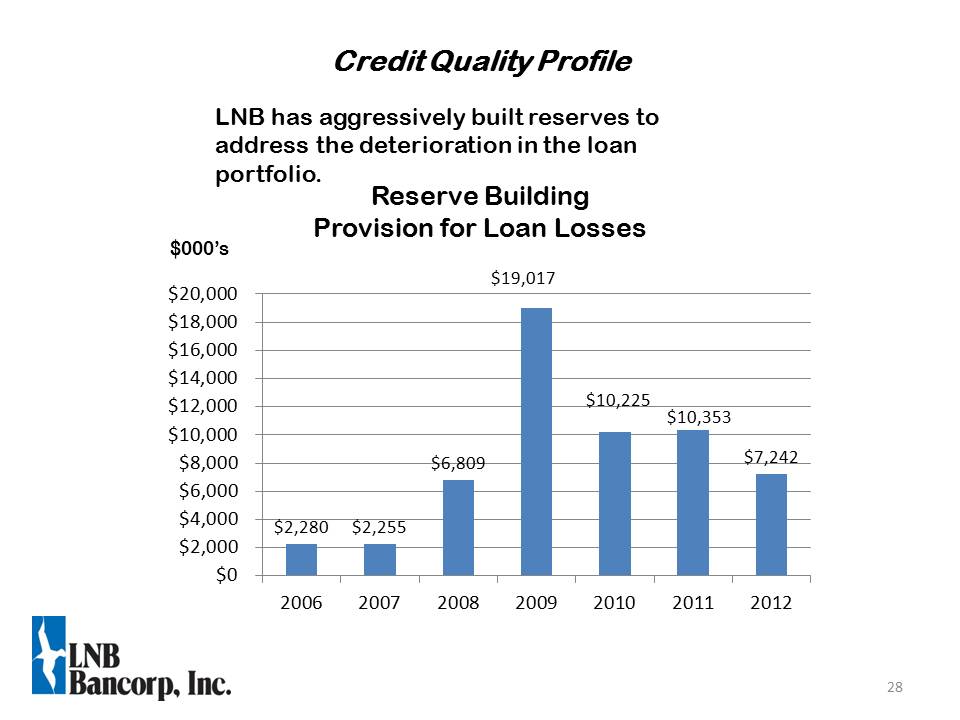

28 Reserve Building Provision for Loan Losses $000’s LNB has aggressively built reserves to address the deterioration in the loan portfolio. Credit Quality Profile

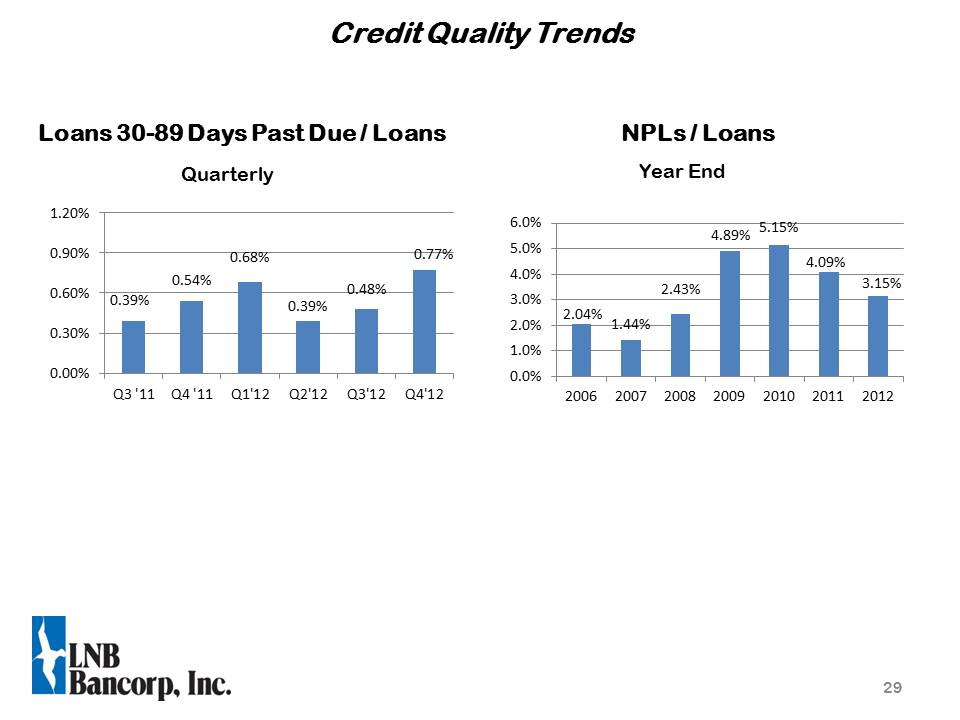

29 Credit Quality Trends Loans 30-89 Days Past Due / Loans NPLs / Loans Year End Quarterly

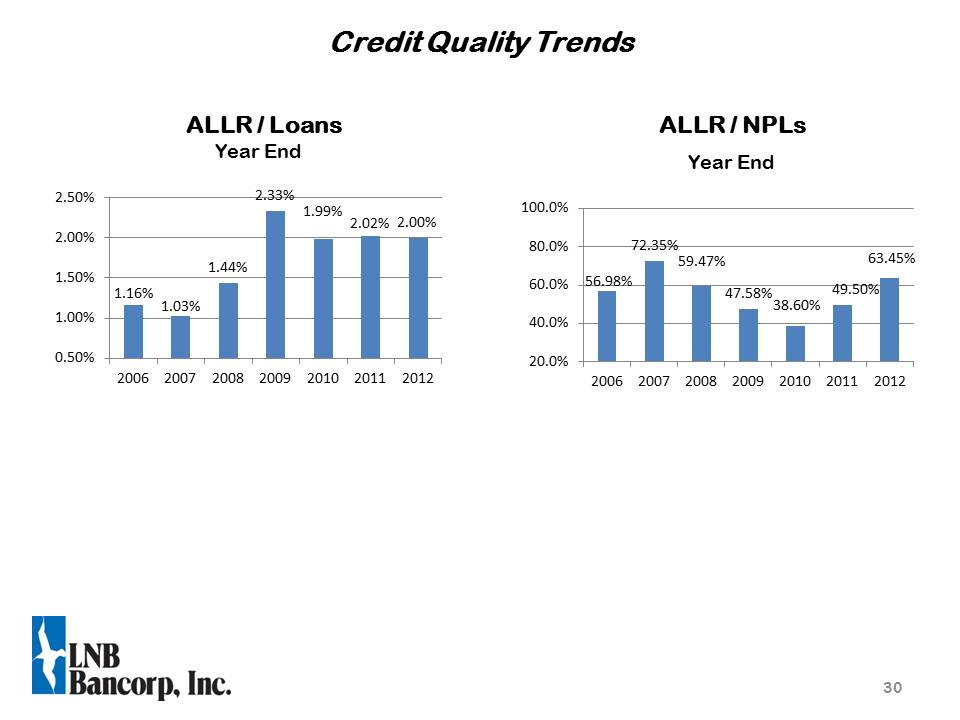

30 Credit Quality Trends ALLR / Loans ALLR / NPLs Year End Year End

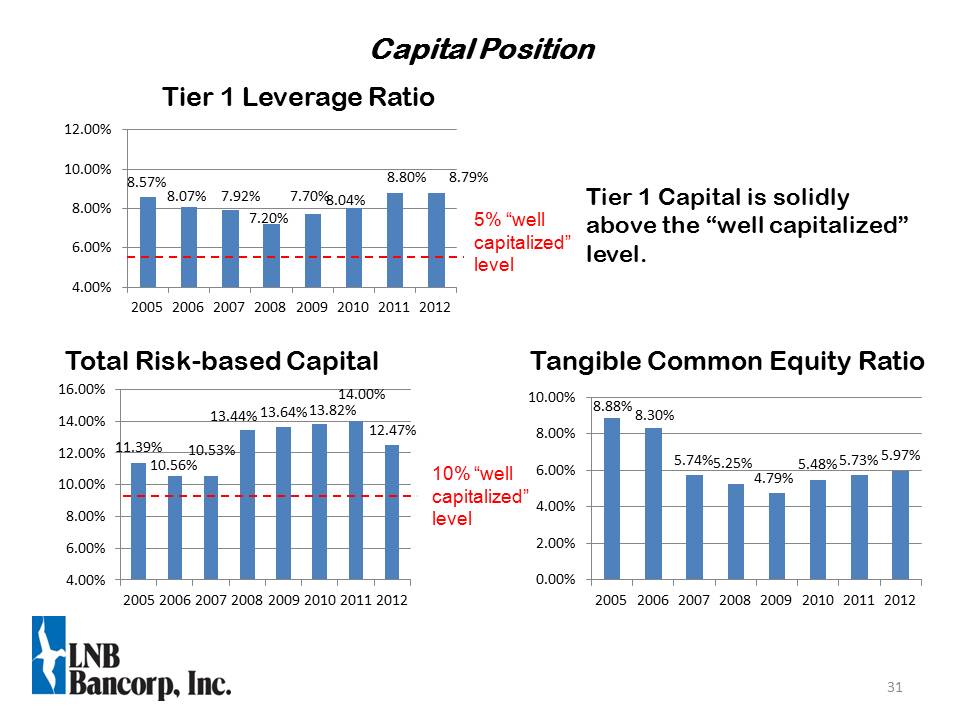

31 Tier 1 Leverage Ratio Tier 1 Capital is solidly above the “well capitalized” level. 5% “well capitalized” level Capital Position Total Risk-based Capital 10% “well capitalized” level Tangible Common Equity Ratio

Current Thoughts on TARP CPP $25.2 million of variable rate Series B cumulative perpetual preferred stock issued on December 12, 2008 Concurrently issued warrants to purchase 561,343 common shares at an exercise price of $6.74 per share Preferred stock sold by Treasury to private investors in June 2012. Company repurchased outstanding warrants from Treasury in July 2012. Company repurchased approximately 25% of outstanding preferred shares in December 2012 at a discount using funds generated from earnings. Continue to consider potential alternatives for eventually repurchasing remaining outstanding preferred shares, balancing the need to maintain a strong capital position with the objectives of building shareholder value and minimizing the impact of repurchase on current shareholders. Potential alternatives for funding repurchases include: Funding generated from earnings Common stock for preferred stock exchange Capital raise Line of credit As we stated in our March 23, 2012 shareholder letter: “no reason to rush into a transaction that could be detrimental in the long term to our institution and you, our shareholders. We are taking a measured and analytic approach to our review of alternatives”.

32 $25.2 million of variable rate Series B cumulative perpetual preferred stock issued on December 12, 2008Concurrently issued warrants to purchase 561,343 common shares at an exercise price of $6.74 per sharePreferred stock sold to private investors in June 2012. Company repurchased outstanding warrants.Company repurchased 25% of outstanding preferred shares at a discount using internal funds in December 2012.Continue to develop plans to repurchase remaining outstanding preferred shares, balancing the need to maintain a strong capital position with the objective of building shareholder value and minimizing the impact of repayment on current shareholders. Options include:Internal fundingCommon stock exchangeCapital raiseLine of creditAs we stated in our March 23, 2012 shareholder letter: “no reason to rush into a transaction that could be detrimental in the long term to our institution and you, our shareholders. We are taking a measured and analytic approach to our review of alternatives”. Current Thoughts on TARP CPP

32 $25.2 million of variable rate Series B cumulative perpetual preferred stock issued on December 12, 2008 Concurrently issued warrants to purchase 561,343 common shares at an exercise price of $6.74 per share Preferred stock sold to private investors in June 2012. Company repurchased outstanding warrants. Company repurchased 25% of outstanding preferred shares at a discount using internal funds in December 2012. Continue to develop plans to repurchase remaining outstanding preferred shares, balancing the need to maintain a strong capital position with the objective of building shareholder value and minimizing the impact of repayment on current shareholders. Options include: Internal funding Common stock exchange Capital raiseLine of credit As we stated in our March 23, 2012 shareholder letter: “no reason to rush into a transaction that could be detrimental in the long term to our institution and you, our shareholders. We are taking a measured and analytic approach to our review of alternatives”.

33 Strong Fundamentals with Attractive Valuation Improving asset quality trendsGrowing loan and deposit portfoliosGrowing revenuesManaged expensesStrong PTPP incomePositive operating leverageGrowing tangible book value per shareAttractive franchise

34 LNBB -- Long Term Potential Only “Community Bank of Scale” headquartered in Northeast Ohio Flexibility Responsiveness Speed Focus on core banking capabilities Strong Fee Income Service charges Trust Fees Mortgage Lending Unique high quality indirect auto business Expanding outside Ohio Strong core earnings base and growth trends