Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Federal Home Loan Bank of Pittsburgh | d491304d8k.htm |

Member Audio/Web

Conference

February 26, 2013

Exhibit 99.1 |

Cautionary Statement Regarding Forward-

Looking Information and Adjusted Information

2

Data set forth in these slides includes unaudited data. This document contains

“forward-looking statements”- that is, statements related to future, not

past, events. In this context, forward-looking statements often address our expected future business and financial

performance, and often contain words such as “expect,” “anticipate,”

“intend,” “plan,” “believe,” “seek,” or “will.” The Bank cautions that,

by their nature, forward-looking statements involve risk or uncertainty and that actual results

could differ materially from those expressed or implied in these forward-looking statements

or could affect the extent to which a particular objective, projection, estimate, or prediction

is realized. These forward-looking statements involve risks and uncertainties including, but not limited to, the following:

economic and market conditions, including, but not limited to, real estate, credit and mortgage

markets; volatility of market prices, rates, and indices; political, legislative, regulatory,

litigation, or judicial events or actions; changes in assumptions used in the quarterly other-

than-temporary impairment (OTTI) process; changes in the assumptions used in the allowance for

credit loss; changes in the Bank’s capital structure; changes in the Bank’s

capital requirements; membership changes; changes in the demand by Bank members for Bank

advances; an increase in advances’ prepayments; competitive forces, including the availability of other sources of funding for

Bank members; changes in investor demand for consolidated obligations and/or the terms of interest

rate exchange agreements and similar agreements; changes in the FHLBank System’s debt

rating or the Bank’s rating; the ability of the Bank to introduce new products and

services to meet market demand and to manage successfully the risks associated with new products and services; the

ability of each of the other FHLBanks to repay the principal and interest on consolidated obligations

for which it is the primary obligor and with respect to which the Bank has joint and several

liability; applicable Bank policy requirements for retained earnings and the ratio of the

market value of equity to par value of capital stock; the Bank’s ability to maintain adequate capital levels (including meeting

applicable regulatory capital requirements); business and capital plan adjustments and amendments; and

timing and volume of market activity. This document also contains non-GAAP financial

information. Because of the nature of OTTI charges the Bank believes that adjusting net income

for this item and evaluating results as adjusted (which the Bank defines as “adjusted earnings") is important in

order to understand how the Bank is performing with respect to its primary business operations and to

provide meaningful comparisons to prior periods. Adjusted earnings are considered to be a

non-GAAP measurement. Management uses this information in its internal analysis of results

and believes that this information may be informative to investors in gauging the quality of our financial performance,

identifying trends in our results and providing meaningful period-to-period comparisons. |

Over/

2012

2011

(Under)

Net interest income

209.8

$

154.4

$

55.4

$

Provision for credit losses

0.4

10.0

(9.6)

Net OTTI credit losses

(11.4)

(45.1)

33.7

All other income

18.5

12.1

6.4

Other expenses

72.3

65.0

7.3

Income before assessments

144.2

46.4

97.8

AHP/REFCORP

14.5

8.4

6.1

GAAP net income

129.7

$

38.0

$

91.7

$

Net interest margin (bps)

37

30

7

Year Ended December 31,

Financial Highlights –

Statement of Income

(in millions)

3 |

Quarterly Adjusted Earnings

4Qtr 12

3Qtr 12

2Qtr 12

1Qtr 12

4Qtr 11

GAAP net income

51.7

$

33.0

$

23.2

$

21.8

$

10.9

$

Adjustments:

Net OTTI credit losses

(0.4)

(0.2)

(3.6)

(7.2)

(7.6)

AHP

-

-

0.4

0.7

0.7

Adjusted earnings

52.1

$

33.2

$

26.4

$

28.3

$

17.8

$

Net prepayment fees on

advances

17.5

$

2.2

$

7.4

$

4.7

$

5.0

$

Derivative and hedging activity

8.1

3.5

(4.8)

4.0

(0.5)

(in millions)

4 |

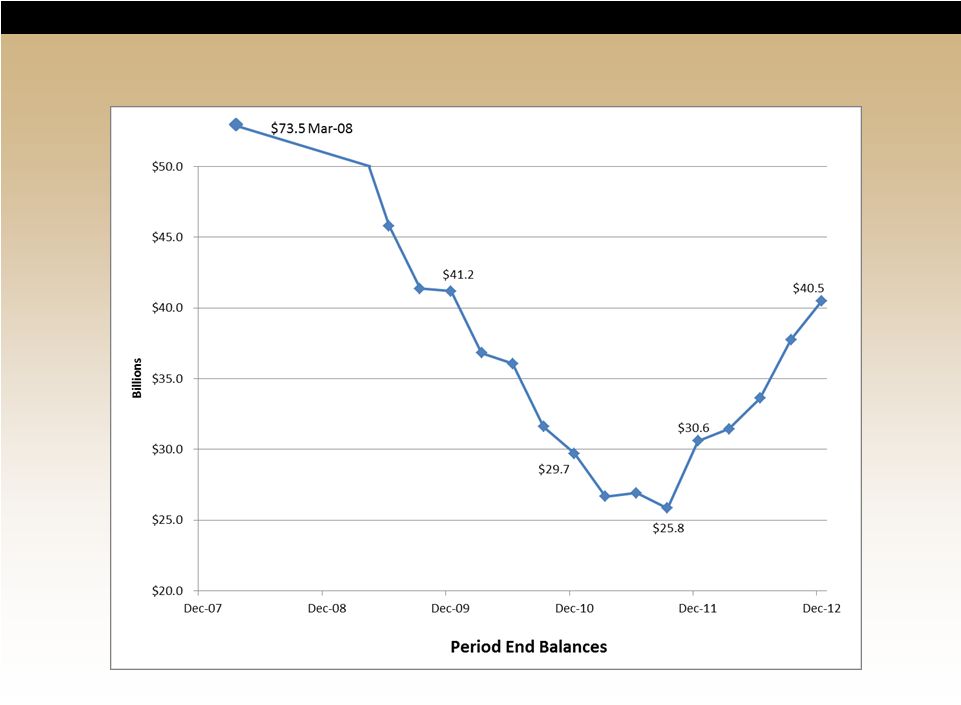

Quarterly Advance Trend

5 |

Financial Highlights –

Selected Balance Sheet

Year Ended December 31,

2012

2011

Amount

Average:

Total assets

57,516

$

51,784

$

5,732

$

11

%

Advances

33,488

27,105

6,383

24

Total investments

19,777

19,968

(191)

(1)

2012

2011

Amount

Spot:

Advances

40,498

$

30,605

$

9,893

$

32

%

PLMBS (par)

2,944

3,794

(850)

(22)

Retained earnings

559

435

124

29

Total AOCI

54

(162)

216

133

Percent

Over/(Under)

Over/(Under)

Percent

As of December 31,

(in millions)

(in millions)

6 |

Capital and Risk-Based Requirements

2012

2011

2010

Permanent capital

(1)

3,807

$

3,871

$

4,418

$

Risk-based capital requirement:

Credit risk capital

678

$

678

$

798

$

Market risk capital

114

139

448

Operations risk capital

238

245

374

Total risk-based capital requirement

1,030

$

1,062

$

1,620

$

Excess permanent capital

2,777

$

2,809

$

2,798

$

Percentage of requirement

370%

365%

273%

Capital ratio (4% minimum)

5.9%

7.4%

8.3%

Leverage ratio (5% minimum)

8.8%

11.2%

12.4%

Market value/capital stock (MV/CS)

115.1%

96.9%

93.3%

As of December 31,

(in millions)

(1)

Permanent

capital

includes

excess

capital

stock

of

$624,

$1,294,

and

$1,897

at

December

31,

2012, 2011 and 2010, respectively.

Third

quarter

2012

capital

classification

“adequately

capitalized.”

However,

our

regulator

has

maintained

concerns

regarding

our

level

of

retained

earnings

and

the

poor

quality

of

the

PLMBS

portfolio.

7 |

•

Dividend declared based on fourth quarter 2012 results

Equal to fourth quarter 2012 average three-month LIBOR (annual yield of

0.32%) Based on average stock outstanding for fourth quarter 2012

Payment date: February 22, 2013

•

Partial excess capital stock repurchase

Excess

capital

stock

repurchased

–

approximately

$300

million

Effective date: February 21, 2013

Payment date: February 22, 2013

•

No significant impact on:

Risk and capital adequacy measures

Members’

excess ownership percentage

•

Decisions for any future repurchases and/or dividend payments will be based on the

following:

Increased retained earnings

PLMBS AOCI levels

Adequate excess regulatory capital

MV/CS > 90%

Positive GAAP earnings which are sustainable for the foreseeable

future

Dividend Payment & Excess Stock Repurchase

8 |

Member Audio/Web

Conference

February 26, 2013 |