Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

[x] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2019

or

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission File Number: 000-51395

FEDERAL HOME LOAN BANK OF PITTSBURGH

(Exact name of registrant as specified in its charter)

Federally Chartered Corporation | 25-6001324 | |

(State or other jurisdiction of incorporation or organization) | (IRS Employer Identification No.) | |

601 Grant Street Pittsburgh, PA (Address of principal executive offices) | 15219 (Zip Code) | |

(412) 288-3400

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

— | — | — |

Securities registered pursuant to Section 12(g) of the Act: | ||

Capital Stock, putable, par value $100 | ||

(Title of Class) | ||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. []Yes [x]No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. []Yes [x]No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. [x]Yes []No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). [x] Yes [] No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

o Large accelerated filer | o Accelerated filer | o Emerging growth company |

x Non-accelerated filer | o Smaller reporting company | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. []

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). [] Yes [x] No

Registrant’s stock is not publicly traded and is only issued to members of the registrant. Such stock is issued and redeemed at par value, $100 per share, subject to certain regulatory and statutory limits. At June 30, 2019, the aggregate par value of the stock held by current and former members of the registrant was approximately $3,987.0 million. There were 29,985,999 shares of common stock outstanding at February 28, 2020.

FEDERAL HOME LOAN BANK OF PITTSBURGH

TABLE OF CONTENTS

PART I | ||

Item 1: Business | ||

Item 1A: Risk Factors | ||

Item 1B: Unresolved Staff Comments | ||

Item 2: Properties | ||

Item 3: Legal Proceedings | ||

Item 4: Mine Safety Disclosures | ||

PART II | ||

Item 5: Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | ||

Item 6: Selected Financial Data | ||

Item 7: Management’s Discussion and Analysis of Financial Condition and Results of Operations | ||

Risk Management | ||

Item 7A: Quantitative and Qualitative Disclosures about Market Risk | ||

Item 8: Financial Statements and Supplementary Financial Data | ||

Financial Statements for the Years 2019, 2018, and 2017 | ||

Notes to Financial Statements | ||

Item 9: Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | ||

Item 9A: Controls and Procedures | ||

Item 9B: Other Information | ||

PART III | ||

Item 10: Directors, Executive Officers and Corporate Governance | ||

Item 11: Executive Compensation | ||

Item 12: Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | ||

Item 13: Certain Relationships and Related Transactions, and Director Independence | ||

Item 14: Principal Accountant Fees and Services | ||

PART IV | ||

Item 15: Exhibits and Financial Statement Schedules | ||

Item 16: Form 10-K Summary | ||

Glossary | ||

Signatures | ||

i.

PART I

Forward-Looking Information

Statements contained in this Form 10-K, including statements describing the objectives, projections, estimates, or predictions of the future of the Federal Home Loan Bank of Pittsburgh (the Bank), may be “forward-looking statements.” These statements may use forward-looking terms, such as “anticipates,” “believes,” “could,” “estimates,” “may,” “should,” “will,” or their negatives or other variations on these terms. The Bank cautions that, by their nature, forward-looking statements involve risk or uncertainty and that actual results could differ materially from those expressed or implied in these forward-looking statements or could affect the extent to which a particular objective, projection, estimate, or prediction is realized. These forward-looking statements involve risks and uncertainties including, but not limited to, the following: economic and market conditions, including, but not limited to, real estate, credit and mortgage markets; volatility of market prices, rates, and indices related to financial instruments; including but not limited to, the possible discontinuance of the London Interbank Offered Rate (LIBOR) and the related effect on the Bank's LIBOR-based financial products, investments and contracts; the occurrence of man-made or natural disasters, global pandemics, conflicts or terrorist attacks or other geopolitical events; political, legislative, regulatory, litigation, or judicial events or actions; risks related to mortgage-backed securities (MBS); changes in the assumptions used to estimate credit losses; changes in the Bank’s capital structure; changes in the Bank’s capital requirements; changes in expectations regarding the Bank’s payment of dividends; membership changes; changes in the demand by Bank members for Bank advances; an increase in advance prepayments; competitive forces, including the availability of other sources of funding for Bank members; changes in investor demand for consolidated obligations and/or the terms of interest rate exchange agreements and similar agreements; changes in the Federal Home Loan Bank (FHLBank) System’s debt rating or the Bank’s rating; the ability of the Bank to introduce new products and services to meet market demand and to manage successfully the risks associated with new products and services; the ability of each of the other FHLBanks to repay the principal and interest on consolidated obligations for which it is the primary obligor and with respect to which the Bank has joint and several liability; applicable Bank policy requirements for retained earnings and the ratio of the market value of equity to par value of capital stock; the Bank’s ability to maintain adequate capital levels (including meeting applicable regulatory capital requirements); business and capital plan adjustments and amendments; technology and cyber-security risks; and timing and volume of market activity.

Item 1: Business

The Bank’s mission is to provide its members with readily available liquidity, including serving as a low-cost source of funds for housing and community development. The Bank strives to enhance the availability of credit for residential mortgages and targeted community development. The Bank manages its own liquidity so that funds are available to meet members’ demand for advances (loans to members and eligible nonmember housing associates). By providing needed liquidity and enhancing competition in the mortgage market, the Bank’s lending programs benefit homebuyers and communities. For additional information regarding the Bank’s financial condition and financial statements, refer to Item 7. Management’s Discussion and Analysis and Item 8. Financial Statements and Supplementary Financial Data in this Form 10-K. For additional information regarding the Bank’s business risks, refer to Item 1A. Risk Factors in this Form 10-K.

General

History. The Bank is one of 11 FHLBanks. The FHLBanks operate as separate entities with their own management, employees and board of directors. The 11 FHLBanks, along with the Office of Finance (OF - the FHLBanks’ fiscal agent) comprise the FHLBank System. The FHLBanks were organized under the authority of the Federal Home Loan Bank Act of 1932, as amended (the Act). The FHLBanks are commonly referred to as government-sponsored enterprises (GSEs), which generally means they are a combination of private capital and public sponsorship. The public sponsorship attributes include:

• | being exempt from federal, state and local taxation, except real estate taxes; |

• | being exempt from registration under the Securities Act of 1933 (the 1933 Act), although the FHLBanks are required by Federal Housing Finance Agency (FHFA or Finance Agency) regulation and the Housing and Economic Recovery Act of 2008 (the Housing Act or HERA) to register a class of their equity securities under the Securities Exchange Act of 1934 (the 1934 Act); and |

• | having a line of credit with the U.S. Treasury. This line represents the U.S. Treasury’s authority to purchase consolidated obligations in an amount up to $4 billion. |

1

Cooperative. The Bank is a cooperative institution, owned by member financial institutions that are also its primary customers. Any building and loan association, savings and loan association, commercial bank, homestead association, insurance company, savings bank, credit union, community development financial institution (CDFI), or insured depository institution that maintains its principal place of business in Delaware, Pennsylvania or West Virginia and that meets varying requirements can apply for membership in the Bank. All members are required to purchase capital stock in the Bank as a condition of membership. The capital stock of the Bank can be purchased only by members.

Mission. The Bank’s primary mission is to assure the flow of credit to its members to support housing finance and community lending and to provide related services that enhance their businesses and vitalize their communities. The Bank provides credit for housing and community development through two primary programs. First, it provides members with advances secured by residential mortgages and other types of high-quality collateral. Second, the Bank purchases residential mortgage loans originated by or through eligible member institutions. The Bank also offers other credit and noncredit products and services to member institutions. These include letters of credit, affordable housing grants, securities safekeeping, and deposit products and services. The Bank issues debt to the public (consolidated obligation bonds and discount notes) in the capital markets through the OF and uses these funds to provide its member financial institutions with a reliable source of liquidity. The U.S. government does not guarantee the debt securities or other obligations of the Bank or the FHLBank System.

Overview. As a GSE, the Bank is able to raise funds in the capital markets at narrow spreads to the U.S. Treasury yield curve. This fundamental competitive advantage, coupled with the joint and several liability on FHLBank System debt, enables the Bank to provide attractively priced funding to members. Though chartered by Congress, the Bank is privately capitalized by its member institutions, which are voluntary participants in its cooperative structure. The characterization of the Bank as a voluntary cooperative with the status of a federal instrumentality differentiates the Bank from a traditional banking institution in three principal ways:

• | Financial institutions choose membership in the Bank principally for access to liquidity, the value of the products offered, and the potential to receive dividends. |

• | Because the Bank’s customers and shareholders are predominantly the same institutions, normally there is a need to balance the pricing expectations of customers with the dividend expectations of shareholders. By charging wider spreads on loans to customers, the Bank could potentially generate higher earnings and dividends for shareholders. Yet these same shareholders are also customers who would generally prefer narrower loan spreads. The Bank strives to achieve a balance between the goals of providing liquidity and other services to members at advantageous prices and potentially generating an attractive dividend. The Bank typically does not strive to maximize the dividend yield on the stock, but to produce a dividend that compares favorably to short-term interest rates, thus compensating members for the cost of the capital they have invested in the Bank. |

• | The Bank’s GSE charter is based on a public policy purpose to assure liquidity for its members and to enhance the availability of affordable housing for lower-income households. In upholding its public policy mission, the Bank offers products that consume a portion of its earnings. The cooperative GSE character of this voluntary membership organization leads management to optimize the primary purpose of membership, access to liquidity, as well as the overall value of Bank membership. |

Nonmember Borrowers. In addition to member institutions, the Bank is permitted under the Act to make advances to nonmember housing associates that are approved mortgagees under Title II of the National Housing Act. These eligible housing associates must be chartered under law, be subject to inspection and supervision by a governmental agency, and lend their own funds as their principal activity in the mortgage field. The Bank must approve each applicant. Housing associates are not subject to certain provisions of the Act that are applicable to members, such as the capital stock purchase requirements. However, they are generally subject to more restrictive lending and collateral requirements than those applicable to members. As of December 31, 2019, the Bank maintains relationships with three approved state housing finance agencies (HFAs). Each is currently eligible to borrow from the Bank and one of the housing associates had an advance balance of $14.9 million as of December 31, 2019.

2

Regulatory Oversight, Audits and Examinations

Supervision and Regulation. The Bank and OF are supervised and regulated by the Finance Agency, which is an independent agency in the executive branch of the United States government. The Finance Agency ensures that the Bank carries out its housing finance mission, remains adequately capitalized and operates in a safe and sound manner. The Finance Agency establishes regulations, issues advisory bulletins (ABs), and otherwise supervises Bank operations primarily via periodic examinations. The Government Corporation Control Act provides that, before a government corporation issues and offers obligations to the public, the Secretary of the U.S. Treasury has the authority to prescribe the form, denomination, maturity, interest rate, and conditions of the obligations; the way and time issued; and the selling price. The U.S. Treasury receives the Finance Agency’s annual report to Congress and other reports on operations. The Bank is also subject to regulation by the Securities and Exchange Commission (SEC).

Examination. At a minimum, the Finance Agency conducts annual onsite examinations of the operations of the Bank. In addition, the Comptroller General has authority under the Act to audit or examine the Finance Agency and the Bank and to decide the extent to which they fairly and effectively fulfill the purposes of the Act. Furthermore, the Government Corporation Control Act provides that the Comptroller General may review any audit of the financial statements conducted by an independent registered public accounting firm. If the Comptroller General conducts such a review, then he or she must report the results and provide his or her recommendations to Congress, the Office of Management and Budget (OMB), and the FHLBank in question. The Comptroller General may also conduct his or her own audit of the financial statements of the Bank.

Audit. The Bank has an internal audit department that reports directly to the Audit Committee of the Bank’s Board of Directors (Board). In addition, an independent Registered Public Accounting Firm (RPAF) audits the annual financial statements and internal controls over financial reporting of the Bank. The independent RPAF conducts these audits following the Standards of the Public Company Accounting Oversight Board (PCAOB) of the United States of America and Government Auditing Standards issued by the Comptroller General. The Bank, the Finance Agency, and Congress all receive the independent RPAF audit reports.

3

Advances

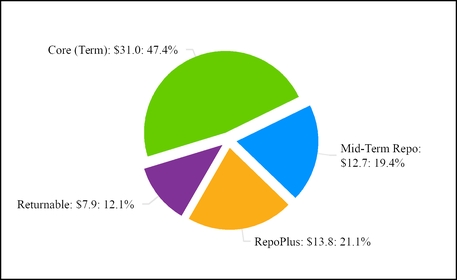

Advance Products. The Bank makes advances on the security of pledged mortgage loans and other eligible types of collateral. The following table summarizes the advance products offered by the Bank as of December 31, 2019.

Product | Description | Maturity | Key Features |

RepoPlus | Short-term, fixed-rate advances; principal and interest paid at maturity | 1 day to 89 days | The RepoPlus advance products serve member short-term liquidity needs. RepoPlus is typically a short-term, fixed-rate product while the Open RepoPlus is a revolving line of credit which allows members to borrow, repay and re-borrow based on the terms of the line of credit. These balances tend to be extremely volatile as members borrow and repay frequently. |

Mid-Term Repo | Mid-term, fixed-rate and adjustable-rate advances(1); principal paid at maturity; interest paid monthly or quarterly | 3 months to 3 years (2) | The Mid-Term Repo product assists members with managing intermediate-term interest rate risk. To assist members with managing basis risk, or the risk of a change in the spread relationship between two indices, the Bank offers adjustable-rate Mid-Term Repo advances. The Bank also offers Mid-Term fixed-rate advances. These balances tend to be somewhat unpredictable as these advances are not always replaced as they mature. |

Core (Term) | Long-term, fixed-rate and adjustable-rate advances(1); principal paid at maturity; interest paid monthly or quarterly (Note: amortizing loans principal and interest paid monthly) | 1 year to 30 years (2) | For managing longer-term interest rate risk and to assist with asset/liability management, the Bank offers long-term fixed-rate and adjustable-rate advances. Amortizing long-term fixed-rate advances can be fully amortized on a monthly basis over the term of the loan or amortized balloon-style, based on an amortization term longer than the maturity of the loan. |

Returnable | Short-term and long-term, fixed-rate and adjustable-rate advances with return options owned by member; principal paid at maturity; interest paid monthly or quarterly | 2 months to 30 years | These advances permit the member to prepay an advance on certain pre-determined date(s) without a fee. |

Notes:

(1) May include loans made under the Community Lending Program (CLP).

(2) Terms dependent upon market conditions.

4

The following chart shows the percentage of advances at par by product type and dollar amount (in billions) as of December 31, 2019.

Letters of Credit. Standby letters of credit are issued by the Bank for a fee on behalf of its members and housing associates to support certain obligations to third-party beneficiaries and are backed by an irrevocable, independent obligation from the Bank. These are subject to the same collateralization and borrowing limits that apply to advances. Standby letters of credit can be valuable tools to support community lending activities, including arranging financing to support bond issuances for community and economic development as well as affordable housing projects. The letters of credit offer customizable terms available to meet unique and evolving needs. If the Bank is required to make payment for a beneficiary’s draw, these amounts are withdrawn from the member/housing associates’ demand deposit account (DDA). Any remaining amounts not covered by the DDA withdrawal are converted into a collateralized overnight advance.

Collateral

The Bank protects against credit risk by fully collateralizing all member and nonmember housing associate advances and other credit products. The Act requires the Bank to obtain and maintain a security interest in eligible collateral at the time it originates or renews an advance.

Collateral Agreements. All members must enter into either the Advances, Collateral Pledge and Security Agreement or the Advances, Specific Collateral Pledge and Security Agreement with the Bank (both hereafter referred to as Master Agreement) in order to obtain advances or other credit products. In both cases, the Bank perfects its security interest under Article 9 of the Uniform Commercial Code (UCC) by filing a financing statement. The Specific Collateral Pledge and Security Agreement covers only those assets or categories of assets identified; the Bank therefore relies on a specific subset of the member’s total eligible collateral as security for the member’s obligations to the Bank. The Bank requires CDFIs, housing finance agencies (HFAs) and insurance companies to sign a specific collateral pledge agreement. See the Credit and Counterparty Risk - TCE and Collateral discussion in Risk Management in Item 7. Management’s Discussion and Analysis in this Form 10-K for a description of blanket and specific agreements.

Collateral Status. The Master Agreement identifies three types of collateral status: undelivered, undelivered detailed listing or specific pledge, and delivered status. All securities pledged must be delivered. A member is assigned a collateral status based on the member’s business needs and on the Bank’s determination of the member’s current financial condition and credit product usage, as well as other available information.

Undelivered Collateral Status. The Bank monitors eligible loan collateral using the Qualifying Collateral Report (QCR), derived from regulatory financial reports which are submitted quarterly (or monthly) to the Bank by the member. For members that submit a QCR on a quarterly basis, lending value is determined based on a percentage of the unpaid principal balance of qualifying collateral (commonly referred to as the collateral weight). Qualifying collateral is determined by deducting ineligible loans from the gross call report amount for each asset category. In addition, members are required to complete an Annual Collateral Certification Report (ACCR).

5

Undelivered Collateral Status: Detailed Listing or Specific Pledge. The Bank may require a member to provide a detailed listing of eligible collateral being pledged if the member is under a specific agreement, or if participating in the Bank’s market-value based pricing program, or as determined based on its credit condition. The member typically retains physical possession of collateral pledged to the Bank but provides a listing of assets pledged. In some cases, the member may benefit by choosing to list collateral, in lieu of non-listed status, since it may result in a higher collateral weighting being applied to the collateral. The Bank benefits from detailed listing collateral status because it provides more loan information to calculate a more precise valuation of the collateral.

Delivered Collateral Status. In this case, the Bank requires the member to deliver physical possession, or grant control of, eligible collateral in an amount sufficient to fully secure its total credit exposure (TCE) to the Bank. Typically, the Bank takes physical possession/control of collateral if the financial condition of the member is deteriorating. Delivery of collateral also may be required if there is action taken against the member by its regulator. Collateral delivery status is often required for members borrowing under specific pledge agreements as a practical means for maintaining specifically listed collateral. Securities collateral qualifies on a delivered basis only (i.e., held in a Bank restricted account or at an approved third-party custodian and subject to a control agreement in favor of the Bank). The Bank also requires delivery of collateral from de novo members at least until two consecutive quarters of profitability are achieved and for any other new member where a pre-existing blanket lien is in force with another creditor unless an effective subordination agreement is executed with such other creditor.

With respect to certain specific collateral pledge agreement borrowers (typically CDFIs, HFAs, and insurance companies), the Bank takes control of all collateral pledged at the time the loan is made through the delivery of securities or, where applicable, mortgage loans to the Bank or its custodian. See the Credit and Counterparty Risk - TCE and Collateral discussion in Risk Management in Item 7. Management’s Discussion and Analysis in this Form 10-K for further details on collateral status and types.

All eligible collateral securing advances is discounted to protect the Bank from loss in the event of default, including under adverse conditions. These discounts, also referred to as lending value or “haircuts”, vary by collateral type and the value of the collateral. The Bank’s collateral discounted values are presented in the table titled “Lending Value Assigned to the Collateral as a Percentage of Value” at the end of this subsection. The discounts typically include margins for estimated costs to sell or liquidate the collateral and the risk of a decline in the collateral value due to market or credit volatility. The Bank reviews the collateral weightings periodically and may adjust them, as well as the members’ reporting requirements to the Bank, for individual borrowers on a case-by-case basis.

The Bank determines the type and amount of collateral each member has available to pledge as security for a member’s obligations to the Bank by reviewing, on a quarterly basis, call reports the members file with their primary regulators. The resulting total value of collateral available to be pledged to the Bank after any collateral weighting is referred to as a member’s maximum borrowing capacity (MBC). Depending on a member’s credit product usage and current financial condition, that member may also be required to file a QCR on a quarterly or monthly basis. At a minimum, all members whose TCE exceeds 20% of their MBC and all members who are not community financial institutions (CFIs) as defined below must file a QCR quarterly.

The Bank also performs periodic on-site collateral reviews of its borrowing members to confirm the amounts and quality of the eligible collateral pledged for the members’ obligations to the Bank. For certain pledged residential and commercial mortgage loan collateral, as well as delivered and Bank-controlled securities, the Bank employs outside service providers to assist in determining market values. In addition, the Bank has developed and maintains an Internal Credit Rating (ICR) system that assigns each member a numerical credit rating on a scale of one to ten, with one being the best rating. Credit availability and term guidelines are based on a member’s ICR and MBC usage. The Bank reserves the right, at its discretion, to refuse certain collateral or to adjust collateral weightings. In addition, the Bank can require additional or substitute collateral while any obligations of a member to the Bank remain outstanding to protect the Bank’s security interest and ensure that it remains fully secured at all times.

See the Credit and Counterparty Risk - TCE and Collateral discussion in Risk Management in Item 7. Management’s Discussion and Analysis in this Form 10-K for further information on collateral policies and practices and details of eligible collateral, including amounts and percentages of eligible collateral securing members’ obligations to the Bank as of December 31, 2019.

As additional security for each member’s obligations to the Bank, the Bank has a statutory lien on the member’s capital stock in the Bank. In the event of deterioration in the financial condition of a member, the Bank will take possession or control

6

of sufficient eligible collateral to further perfect its security interest in collateral pledged to secure the member’s obligations to the Bank. Members with deteriorating creditworthiness are required to deliver collateral to the Bank or the Bank’s custodian to secure the members’ obligations with the Bank. Furthermore, the Bank requires specific approval of each of such members’ new or renewed advances.

Priority. The Act affords any security interest granted to the Bank by any member, or any affiliate of a member, priority over the claims and rights of any third party, including any receiver, conservator, trustee or similar party having rights of a lien creditor. The only two exceptions are: (1) claims and rights that would be entitled to priority under otherwise applicable law and are held by actual bona fide purchasers for value; and (2) parties that are secured by actual perfected security interests ahead of the Bank’s security interest. The Bank has detailed liquidation plans in place to promptly exercise the Bank’s rights regarding securities, loan collateral, and other collateral upon the failure of a member. Management believes that adequate policies and procedures are in place to effectively manage the Bank’s credit risk associated with lending to members and nonmember housing associates.

Types of Collateral. Single-family, residential mortgage loans may be used to secure members’ obligations to the Bank. The Bank contracts with a leading provider of comprehensive mortgage analytical pricing to provide market valuations of some listed and delivered residential mortgage loan collateral. In determining borrowing capacity for members with non-listed and non-delivered collateral, the Bank utilizes book value as reported on each member's regulatory call report. Loans that do not have a paper-based promissory note with a “wet ink” signature are ineligible for collateral purposes.

The Bank also may accept other real estate related collateral (ORERC) as eligible collateral if it has a readily ascertainable value and the Bank is able to perfect its security interest in such collateral. Types of eligible ORERC include commercial mortgage loans, multi-family residential mortgage loans, and second-mortgage installment loans. The Bank uses a leading provider of multi-family and commercial mortgage analytical pricing to provide more precise valuations of listed and delivered multi-family and commercial mortgage loan collateral.

A third category of eligible collateral is high quality investment securities as included in the table below. See the Credit and Counterparty Risk - TCE and Collateral discussion in Risk Management in Item 7. Management’s Discussion and Analysis in this Form 10-K for a definition of these securities. Members have the option to deliver such high quality investment securities to the Bank to obtain or increase their MBC. Upon delivery, these securities are valued daily and all non-government or agency securities are subject to weekly ratings reviews.

The Bank also accepts FHLBank cash deposits as eligible collateral. In addition, member CFIs may pledge a broader array of collateral to the Bank, including secured small business, small farm, small agri-business and community development loans. The Housing Act defines member CFIs as Federal Deposit Insurance Corporation (FDIC)-insured institutions with no more than $1.2 billion (the limit during 2019) in average assets over the past three years. This limit may be adjusted by the Finance Agency based on changes in the Consumer Price Index. The determination to accept such collateral is at the discretion of the Bank and is made on a case-by-case basis. Advances to CFIs are also collateralized by sufficient levels of non-CFI collateral. See the Credit and Counterparty Risk - TCE and Collateral discussion in Risk Management in Item 7. Management’s Discussion and Analysis in this Form 10-K for the percentage of each type of collateral held by the Bank at December 31, 2019.

The Bank does not accept subprime residential mortgage loans (defined as FICO® score of 660 or below. FICO is a registered trademark of Fair Isaac Corporation) as qualifying collateral unless certain mitigating factors are met. The Bank requires members to identify the amount of subprime and nontraditional mortgage collateral in their QCRs.

Nontraditional residential mortgage loans are defined by the Bank’s Collateral Policy as mortgage loans that allow borrowers to defer payment of principal or interest. These loans exhibit characteristics that may result in increased risk relative to traditional residential mortgage loan products. They may pose even greater risk when granted to borrowers with undocumented or undemonstrated repayment capacity, for example, low or no documentation loans or credit characteristics that would be characterized as subprime. The potential for increased risk is particularly true if the nontraditional residential mortgage loans are not underwritten to the fully indexed rate.

Regarding nontraditional mortgage collateral for the QCR, the Bank requires filing members to stratify their holdings of first lien residential mortgage loans into traditional, qualifying low FICO, and qualifying unknown FICO categories. Under limited circumstances, the Bank allows nontraditional residential mortgage loans that are consistent with Federal Financial Institutions Examination Council (FFIEC) guidance to be pledged as collateral and used to determine a member’s MBC.

7

Management believes that the Bank has limited collateral exposure to subprime and nontraditional loans due to its conservative policies pertaining to collateral and low credit risk due to the design of its mortgage loan purchase programs. See the Credit and Counterparty Risk - TCE and Collateral discussion in Risk Management in Item 7. Management’s Discussion and Analysis in this Form 10-K for specific requirements regarding subprime and nontraditional loan collateral.

The various types of eligible collateral and related lending values as of December 31, 2019 are summarized below. The weightings are analyzed on at least a semi-annual basis and adjusted as necessary. At the discretion of the Bank, on a case-by-case basis, the collateral weighting on loan categories may be increased (up to a maximum of 85%) upon completion of specific market valuation of such collateral and authorization from the Bank’s Membership and Credit Committee.

Securities Collateral | Lending Values as a Percentage of Fair Value for All Members |

Deposits held by the Bank and pledged to, and under the sole control of, the Bank | 100% |

U.S. Treasury securities; U.S. Agency securities, including securities of FNMA, FHLMC, FFCB, NCUA, SBA, USDA and FDIC notes; FHLBank consolidated obligations; REFCORP Bonds (1) | 97% |

MBS, including collateralized mortgage obligations (CMOs) issued or guaranteed by GNMA, FHLMC, and FNMA | 95% |

U.S. Treasury STRIPs | 90% |

Non-agency residential MBS, including CMOs, representing a whole interest in such mortgages. | AAA 85% |

AA 75% | |

A 70% | |

Commercial mortgage-backed securities (CMBS) | AAA 85% |

AA 75% | |

A 70% | |

Securities issued by a state or local government or its agencies, or authorities or instrumentalities in the United States (municipals) with a real estate nexus. | AAA 92% |

AA 90% | |

A 88% | |

Loan Collateral | Lending Values | ||

% of Unpaid Principal Balance | % of Fair Value | ||

QCR Filer or Full Collateral Delivery Policy Reasons | Full Collateral Credit Reasons | Market Valuation Program | |

Federal Housing Administration (FHA), Department of Veterans Affairs (VA) and Conventional whole, fully disbursed, first mortgage loans secured by 1-to-4 family residences (Note: Includes first lien HELOCs for listing members only) | 80% | 70% | 85% |

Nontraditional mortgage loans and loans with unknown FICO (2) scores | 70% | 60% | 80% |

Conventional and FHA whole, fully-disbursed mortgage loans secured by multifamily properties | 75% | 65% | 85% |

Farmland loans | 70% | 60% | n/a |

Commercial real estate loans (owner & non-owner occupied) | 70% | 60% | 80% |

Low FICO score loans with mitigating factors as defined by the Bank | 60% | 50% | 75% |

Conventional, fully disbursed, second-mortgage loans secured by 1-to-4 family residences. Both term loans and HELOCs | 60% | 50% | |

CFI Collateral | 60% | 50% | n/a |

Notes:

(1) Defined as Federal National Mortgage Association (Fannie Mae or FNMA), Federal Home Loan Mortgage Corporation (Freddie Mac or FHLMC), Federal Farm Credit Bank (FFCB), Government National Mortgage Association (Ginnie Mae or GNMA), Home Equity Line of Credit (HELOC), National Credit Union Administration (NCUA), Resolution Funding Corporation (REFCORP), Small Business Administration (SBA), and U.S. Department of Agriculture (USDA).

(2) Nontraditional mortgage loan portfolios may be required to be independently identified for collateral review and valuation for inclusion in a member’s MBC. This may include a request for loan-level listing on a periodic basis.

During 2019, the Bank implemented some changes to its collateral policies and practices. See the Credit and Counterparty Risk - TCE and Collateral discussion in Risk Management in Item 7. Management’s Discussion and Analysis in this Form 10-K for details regarding these changes.

8

Investments

Overview. The Bank maintains a portfolio of investments for two main purposes: liquidity and additional earnings. The Bank invests in short term instruments for operating liquidity, including interest-bearing deposits, Federal funds, securities purchased under agreements to resell, as well as U.S. Treasury and GSE obligations that are classified as trading. The Bank also maintains a contingency liquidity investment portfolio which consists of certificate of deposits and unencumbered repurchase-eligible assets within its available-for-sale (AFS) and held-to-maturity (HTM) securities portfolio. These securities may also be pledged as collateral for derivative transactions on occasion.

The Bank further enhances income by acquiring securities issued by GSEs and state and local government agencies as well as Agency MBS. The Bank's private label MBS portfolio continues to run-off; no private label MBS have been purchased since late 2007. Securities currently in the portfolio were required to carry one of the top two ratings from Moody’s Investors Service, Inc. (Moody’s), Standard & Poor’s Ratings Services (S&P) or Fitch Ratings (Fitch) at the time of purchase.

The long-term investment portfolio is intended to provide the Bank with higher returns than those available in the short-term money markets. See the Credit and Counterparty Risk – Investments discussion in Risk Management in Item 7. Management’s Discussion and Analysis in this Form 10-K for discussion of the credit risk of the investment portfolio and further information on these securities’ current ratings.

Prohibitions. Under Finance Agency regulations, the Bank is prohibited from purchasing certain types of securities, including:

• | instruments, such as common stock, that represent an ownership interest in an entity, other than stock in small business investment companies or certain investments targeted to low-income persons or communities; |

• | instruments issued by non-U.S. entities, other than those issued by United States branches and agency offices of foreign commercial banks; |

• | non-investment-grade debt instruments, other than certain investments targeted to low-income persons or communities and instruments that were downgraded after purchase by the Bank; |

• | whole mortgages or other whole loans, other than: (1) those acquired under the Bank’s mortgage purchase program; (2) certain investments targeted to low-income persons or communities; (3) certain marketable direct obligations of state, local or tribal government units or agencies that are of investment quality; (4) MBS or asset-backed securities (ABS) backed by manufactured housing loans or home equity loans (HELOCs); and (5) certain foreign housing loans authorized under Section 12(b) of the Act; and |

• | non-U.S. dollar denominated securities. |

The provisions of Finance Agency regulation further limit the Bank’s investment in MBS and ABS. These provisions require that the total book value of MBS owned by the Bank not exceed 300% of the Bank’s previous month-end regulatory capital on the day of purchase of additional MBS. In addition, the Bank is prohibited from purchasing:

• | interest-only or principal-only strips of MBS; |

• | residual-interest or interest-accrual classes of collateralized mortgage obligations and real estate mortgage investment conduits; and |

• | fixed-rate or floating-rate MBS that on the trade date are at rates equal to their contractual cap and that have average lives that vary by more than six years under an assumed instantaneous interest rate change of 300 basis points. |

The FHLBanks are prohibited from purchasing an FHLBank consolidated obligation as part of the consolidated obligation’s initial issuance. The Bank’s investment policy is even more restrictive, as it prohibits it from investing in FHLBank consolidated obligations for which another FHLBank is the primary obligor. The Federal Reserve Board (Federal Reserve) requires Federal Reserve Banks (FRBs) to release interest and principal payments on the FHLBank System consolidated obligations only when there are sufficient funds in the FHLBanks’ account to cover these payments. The prohibitions on purchasing FHLBank consolidated obligations noted above will be temporarily waived if the Bank is obligated to accept the direct placement of consolidated obligation discount notes to assist in the management of any daily funding shortfall of another FHLBank.

The Bank does not consolidate any off-balance sheet special-purpose entities or other conduits.

9

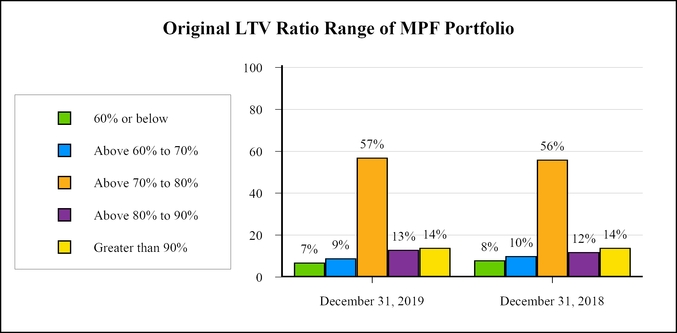

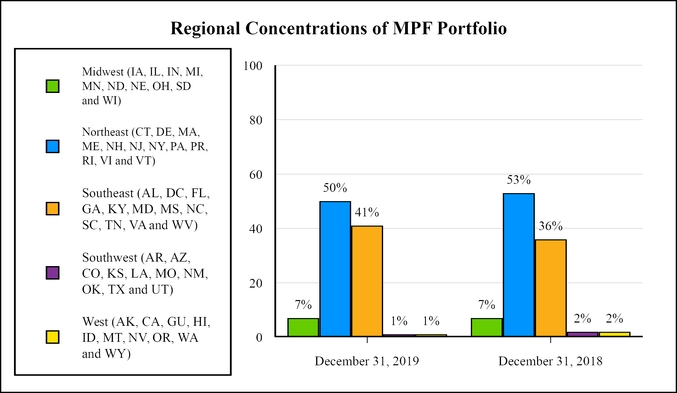

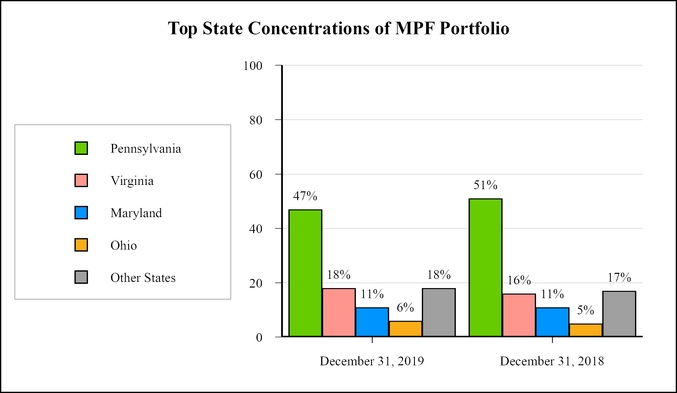

Mortgage Partnership Finance® (MPF®) Program

Under the MPF Program, the Bank purchases qualifying 5- to 30-year conventional conforming and government-insured fixed-rate mortgage loans secured by one-to-four family residential properties. The MPF Program provides participating members and eligible housing associates a secondary market alternative that allows for increased balance sheet liquidity and provides a method for removal of assets that carry interest rate and prepayment risks from their balance sheets. In addition, the MPF Program provides a greater degree of competition among mortgage purchasers and allows small and mid-sized community-based financial institutions to participate more effectively in the secondary mortgage market.

The Bank currently offers five products under the MPF Program to Participating Financial Institutions (PFIs): MPF Original, MPF 35, MPF Government, MPF Direct and MPF Xtra. The MPF Direct and MPF Xtra products are described below. Further details regarding the credit risk structure for each of the other MPF products, as well as additional information regarding the MPF Program and the products offered by the Bank, is provided in the Financial Condition section and the Credit and Counterparty Risk - Mortgage Loans discussion in Risk Management, both in Item 7. Management’s Discussion and Analysis in this Form 10-K.

PFI. Members and eligible housing associates must specifically apply to become a PFI. The Bank reviews their eligibility including servicing qualifications and ability to supply documents, data and reports required to be delivered under the MPF Program. The Bank added one new PFI in 2019, and as of December 31, 2019, 128 members were approved participants in the MPF Program.

Under the MPF Program, PFIs generally market, originate and service qualifying residential mortgages for sale to the Bank. Member banks have direct knowledge of their mortgage markets and have developed expertise in underwriting and servicing residential mortgage loans. By allowing PFIs to originate mortgage loans, whether through retail or wholesale operations, and to retain or sell servicing of mortgage loans, the MPF Program gives control of the mortgage process to PFIs. PFIs also may earn servicing income if they choose to retain loan servicing or receive a servicing released premium, if they chose to sell servicing rights to a third-party.

During the life of the loan, PFIs are paid a credit enhancement (CE) fee for retaining and managing a portion of the credit risk in the conventional mortgage loan portfolios sold to the Bank under the MPF Original and MPF 35 Programs. The CE structure motivates PFIs to minimize loan losses on mortgage loans sold to the Bank. The Bank is responsible for managing the interest rate risk, prepayment risk, liquidity risk and a portion of the credit risk associated with the mortgage loans.

Mortgage Loan Purchases. The Bank and the PFI enter into a Master Commitment which provides the general terms under which the PFI will deliver mortgage loans, including a maximum loan delivery amount, maximum CE amount and expiration date. Mortgage loans are purchased by the Bank directly from a PFI pursuant to a delivery commitment, a binding agreement between the PFI and the Bank.

Mortgage Loan Participations. The Bank may sell participation interests in purchased mortgage loans to other FHLBanks, institutional third party investors approved in writing by the FHLBank of Chicago, the member that provided the CE, and other members of the FHLBank System. The Bank also may purchase mortgage loans from other FHLBanks.

Mortgage Loan Servicing. Under the MPF Program, PFIs may retain or sell servicing to third parties. The Bank does not service loans or own any servicing rights. The FHLBank of Chicago acts as the master servicer for the Bank and has contracted with Wells Fargo Bank, N.A. to fulfill the master servicing duties. The Bank pays the PFI or third-party servicer a servicing fee to perform these duties. The servicing fee is 25 basis points for conventional loans and 44 basis points for government loans.

MPF Xtra. MPF Xtra allows PFIs to sell residential, conforming, fixed-rate mortgages to FHLBank of Chicago, which concurrently sells them to Fannie Mae on a nonrecourse basis. MPF Xtra does not have the CE structure of the traditional MPF Program. Additionally, because these loans are sold from the PFI to FHLBank of Chicago to Fannie Mae, they are not reported on the Bank’s Statement of Condition. With the MPF Xtra product, there is no credit obligation assumed by the PFI or the Bank and no CE fees are paid. PFIs which have completed all required documentation and training are eligible to offer the product. As of December 31, 2019, 39 PFIs were eligible to offer the product. The Bank receives a nominal fee for facilitating these MPF Xtra transactions.

MPF Direct. This is operationally similar to MPF Xtra and allows PFIs to sell residential, jumbo, fixed-rate mortgages to FHLBank Chicago, which concurrently sells them to a third party on a nonrecourse basis. PFIs which have completed all required documentation and training are eligible to offer the product. MPF Direct does not have the credit structure of the traditional MPF Program, and there is no CE obligation assumed by the PFI or the Bank and no CE fees are paid. The Bank

10

receives a nominal fee for facilitating MPF Direct transactions. Given the arrangement, these loans are not reported on the Bank's Statement of Condition.

The FHLBank of Chicago, in its role as MPF Provider, provides the programmatic and operational support for the MPF Program and is responsible for the development and maintenance of the origination, underwriting and servicing guides.

“Mortgage Partnership Finance”, “MPF”, “MPF Xtra”, “MPF Direct” and “MPF 35” are registered trademarks of the FHLBank of Chicago.

Specialized Programs

For additional information on Affordable Housing Program (AHP) and other similar programs, refer to the Community Investment Products section in Item 7. Management’s Discussion and Analysis in this Form 10-K.

Deposits

The Act allows the Bank to accept deposits from its members, from any institution for which it is providing correspondent services, from other FHLBanks, or from other Federal instrumentalities. Deposit programs are low-cost funding resources for the Bank, which also provide members a low-risk earning asset that is used in meeting their regulatory liquidity requirements. The Bank offers several types of deposit programs to its members including demand, overnight and term deposits.

Debt Financing — Consolidated Obligations

The primary source of funds for the Bank is the issuance of debt securities, known as consolidated obligations, which are then sold by dealers to investors. These consolidated obligations are issued as both bonds and discount notes, depending on maturity. Consolidated obligations are the joint and several obligations of the 11 FHLBanks. Consolidated obligations are not obligations of the U.S. government, and the U.S. government does not guarantee them. Moody’s has rated consolidated obligations Aaa with stable outlook/P-1, and S&P has rated them AA+ with stable outlook/A-1+. The following table presents the total par value of the consolidated obligations of the Bank and the FHLBank System at December 31, 2019 and 2018.

(in millions) | December 31, 2019 | December 31, 2018 | ||||

Consolidated obligation bonds | $ | 66,704.2 | $ | 64,368.4 | ||

Consolidated obligation discount notes | 23,211.5 | 36,985.0 | ||||

Total Bank consolidated obligations | 89,915.7 | 101,353.4 | ||||

Total FHLBank System combined consolidated obligations | $ | 1,025,894.7 | $ | 1,031,617.5 | ||

OF. The OF has responsibility for facilitating the issuance and servicing of consolidated obligations on behalf of the FHLBanks. The OF also serves as a source of information for the Bank on capital market developments, markets the FHLBank System’s consolidations obligations on behalf of the FHLBanks, selects and evaluates underwriters, prepares combined financial statements, and manages the Banks’ relationship with the rating agencies and the U.S. Treasury with respect to the consolidated obligations.

Consolidated Obligation Bonds. On behalf of the Bank, the OF issues bonds that the Bank uses to fund advances, the MPF Program and its investment portfolio. Generally, the maturity of these bonds ranges from one year to ten years, although the maturity is not subject to any statutory or regulatory limit. Bonds can be issued and distributed through negotiated or competitively bid transactions with approved underwriters or selling group members. In some instances, the Bank swaps its term fixed-rate debt issuance to floating rates through the use of interest rate swaps. Bonds can be issued through:

• | a daily auction for both bullet (non-callable and non-amortizing) and American-style (callable daily after lockout period expires) callable bonds |

• | a selling group, which typically has multiple lead investment banks on each issue |

• | a negotiated transaction with one or more dealers |

The process for issuing bonds under the three methods above can vary depending on whether the bonds are non-callable or callable. For example, the Bank can request funding through the TAP auction program (quarterly debt issuances that reopen or “tap” into the same CUSIP number) for fixed-rate non-callable (bullet) bonds. This program uses specific maturities that may be reopened daily during a three-month period through competitive auctions. The goal of the TAP program is to aggregate frequent smaller issues into a larger bond issue that may have greater market liquidity.

11

Consolidated Obligation Discount Notes. The OF also issues discount notes to provide short-term funds for advances for seasonal and cyclical fluctuations in deposit flows, mortgage financing, short-term investments and other funding needs. Discount notes are sold at a discount and mature at par. These securities have maturities of up to 365 days. There are three methods for issuing discount notes:

• | The OF auctions one-, two-, three- and six-month discount notes twice per week and any FHLBank can request an amount to be issued. The market sets the price for these securities. |

• | Via the OF’s window program, through which any FHLBank can offer a specified amount of discount notes at a maximum rate and a specified term up to 365 days. These securities are offered daily through a consolidated discount note selling group of broker-dealers. |

• | Via reverse inquiry, wherein a dealer requests a specified amount of discount notes be issued for a specific date and price. The OF presents reverse inquiries to the FHLBanks, which may or may not choose to issue those particular discount notes. |

See the Liquidity and Funding Risk discussion in the Risk Management section in Item 7. Management’s Discussion and Analysis in this Form 10-K for further information regarding consolidated obligations and related liquidity risk.

Capital Resources

Capital Plan. The Bank currently has two subclasses of capital stock: B1 membership and B2 activity. The Capital Plan generally sets the calculation of the annual Membership Asset Value (MAV) stock purchase requirement based on the member’s assets as set forth in its prior December 31 call report data. Membership assets include, but are not limited to, the following: U.S. Treasury securities; U.S. Agency securities; U.S. Agency MBS; non-Agency MBS; 1-4 family residential first mortgage loans; multi-family mortgage loans; 1-4 family residential second mortgage loans; home equity lines of credit; and commercial real estate loans. A factor is applied to each membership asset category and the resulting MAV is determined by summing the products of the membership asset categories and the respective factor. Adjustments to the amount of membership and activity stock that each member must hold can be made periodically by the Bank's Board in accordance with the terms of the Capital Plan. Ranges have been built into the Capital Plan to allow the Bank to adjust the stock purchase requirement to meet its regulatory capital requirements, if necessary. Currently, these are the stock purchase requirements for each class of stock.

Each member is required to purchase and maintain membership stock equal to the following:

Range of membership stock requirement according to the Capital Plan | |||

Minimum | Maximum | Current requirement | |

% of membership assets | 0.05% | 1.0% | 0.1% |

Membership stock cap | $5 million | $100 million | $45 million |

Membership stock floor | $10 thousand | ||

Each member is required to purchase and maintain activity stock equal to the percentage of the book value of the following transactions as shown in the table below:

Range of activity stock requirement according to the Capital Plan | |||

Minimum | Maximum | Current requirement | |

Outstanding advances | 2.0% | 6.0% | 4.0% |

Acquired member assets (AMA) | 0.0% | 6.0% | 4.0% |

Letters of credit | 0.0% | 4.0% | 0.75% |

Outstanding advance commitments (settling more than 30 days after trade date) | 0.0% | 6.0% | 0.0% |

Bank capital stock is not publicly traded; it may be issued, redeemed and repurchased at its stated par value of $100 per share. Under the Capital Plan, capital stock is redeemed upon five years’ notice, subject to certain conditions. In addition, the Bank has the discretion to repurchase excess stock from members. The Bank's current practice is to repurchase all excess capital stock on a weekly basis.

12

Dividends and Retained Earnings. As prescribed in the Capital Plan, the Bank may pay dividends on its capital stock only out of unrestricted retained earnings or current net income, subject to certain limitations and conditions. The Bank’s Board may declare and pay dividends in either cash or capital stock. The Bank’s practice has been to pay only a cash dividend. The amount of dividends the Board determines to pay out is affected by, among other factors, the level of retained earnings recommended under the Bank’s retained earnings policy. In addition, as set forth in the Capital Plan, the dividends paid on subclass B2 activity stock will be equal to or higher than the dividends being paid on subclass B1 membership stock at that time. For further information on dividends, see Note 15 - Capital in the Notes to Financial Statements in Item 8. of this Form 10-K.

As of December 31, 2019, the balance in retained earnings was $1,326.0 million, of which $415.3 million was deemed restricted. Refer to the Capital Resources section and the Risk Governance discussion in Risk Management, both in Item 7. Management’s Discussion and Analysis in this Form 10-K for additional discussion of the Bank’s capital-related metrics, retained earnings, dividend payments, capital levels and regulatory capital requirements.

Derivatives and Hedging Activities

The Bank may enter into interest rate swaps, swaptions, to-be-announced (TBAs), and interest rate cap and floor agreements (collectively, derivatives) to manage its exposure to changes in interest rates and prepayment risk. The Bank uses these derivatives to adjust the effective maturity, repricing frequency, or option characteristics of financial instruments to achieve its risk management objectives. The Bank may use derivative financial instruments in the following ways: (1) by designating them as a fair value hedge of an underlying financial instrument or a firm commitment; or (2) in asset/liability management (i.e., an economic hedge).

The Finance Agency regulates the Bank’s use of derivatives. The regulations prohibit the trading in or speculative use of these instruments and limit credit risk arising from these instruments. All derivatives are recorded in the Statement of Condition at fair value. See Note 11- Derivatives and Hedging Activities to the audited financial statements in Item 8. Financial Statements and Supplementary Financial Data in this Form 10-K for additional information.

Competition

Advances. The Bank competes with other suppliers of wholesale funding, both secured and unsecured, including the FRBs, commercial banks, investment banking divisions of commercial banks, and brokered deposits, largely on the basis of interest rates as well as types and weightings of collateral. Competition is often more significant when originating advances to larger members, which have greater access to the capital markets. Competition within the FHLBank System is somewhat limited; however, there may be some members of the Bank that have affiliates that are members of other FHLBanks. The Bank's ability to compete successfully with other suppliers of wholesale funding for business depends primarily on pricing, dividends, capital stock requirements, credit and collateral terms, and products offered.

Purchase of Mortgage Loans. Members have several alternative outlets for their mortgage loan production including Fannie Mae, Freddie Mac, and other secondary market conduits. The MPF Program competes with these alternatives on the basis of price and product attributes. Additionally, a member may elect to hold all or a portion of its mortgage loan production in portfolio, potentially funded by an advance from the Bank.

Issuance of Consolidated Obligations. The Bank competes with the U.S. Treasury, Fannie Mae, Freddie Mac and other GSEs as well as corporate, sovereign and supranational entities for funds raised through the issuance of unsecured debt in the national and global debt markets. Increases in the supply of competing debt products may, in the absence of increases in demand, result in higher debt cost. The Bank’s status as a GSE affords certain preferential treatment for its debt obligations under the current regulatory scheme for depository institutions operating in the U.S. as well as preferential tax treatment in a number of state and municipal jurisdictions. Any change in these regulatory conditions as they affect the holders of Bank debt obligations would likely alter the relative competitive position of such debt issuance and result in potentially higher costs to the Bank.

Major Customers

Ally Bank, JP Morgan Chase Bank, N.A., PNC Bank, N.A. and Santander Bank, each had advance balances in excess of 10% of the Bank’s total portfolio as of December 31, 2019. See further discussion in Item 1A. Risk Factors and the Credit and Counterparty Risk - TCE and Collateral discussion in the Risk Management section in Item 7. Management’s Discussion and Analysis, both in this Form 10-K.

13

Personnel

As of December 31, 2019, the Bank had 224 full-time employee positions and four part-time employee positions, for a total of 226 full-time equivalents. The employees are not represented by a collective bargaining unit and the Bank considers its relationship with its employees to be good.

Taxation

The Bank is exempt from all Federal, state and local taxation with the exception of real estate property taxes and certain employer payroll taxes.

AHP

The FHLBanks must set aside for the AHP annually, on a combined basis, the greater of $100 million or 10% of current year’s net income (GAAP net income before interest expense related to mandatorily redeemable capital stock and the assessment for AHP). If the Bank experienced a full year net loss, as defined in Note 14 - Affordable Housing Program (AHP) to the audited financial statements in Item 8. Financial Statements and Supplementary Financial Data in this Form 10-K, the Bank would have no obligation to the AHP for the year except in the following circumstance: if the result of the combined 10% calculation described above is less than $100 million for all 11 FHLBanks, then the Act requires that each FHLBank contribute such prorated sums as may be required to assure that the aggregate contributions of the FHLBanks equal $100 million. The proration would be made on the basis of an FHLBank’s net income in relation to the income of all FHLBanks for the previous year. Each FHLBank’s required annual AHP contribution is limited to its annual net income. If an FHLBank finds that its required contributions are negatively impacting the financial stability of that FHLBank, it may apply to the Finance Agency for a temporary suspension of its contributions. As allowed by AHP regulations, an FHLBank can elect to allot fundings based on future periods’ required AHP contributions to be awarded during a year (referred to as Accelerated AHP). Accelerated AHP allows an FHLBank to commit and disburse AHP funds to meet the FHLBank’s mission when it would otherwise be unable to do so, based on its normal funding mechanism.

For additional details regarding the AHP assessment, please see the Earnings Performance discussion in Item 7. Management’s Discussion and Analysis and Note 14 - Affordable Housing Program (AHP) in Item 8. Financial Statements and Supplementary Financial Data in this Form 10-K.

SEC Reports and Corporate Governance Information

The Bank is subject to the informational requirements of the 1934 Act and, in accordance with the 1934 Act, files annual, quarterly and current reports with the SEC. The Bank’s SEC File Number is 000-51395. The SEC maintains an internet site that contains reports, proxy and information statements and other information regarding registrants that file electronically with the SEC, including the Bank’s filings. The Bank’s financial information is also filed in eXtensible Business Reporting Language (XBRL) as required by the SEC. The SEC’s website address is www.sec.gov.

The Bank also makes the Annual Reports filed on Form 10-K, Quarterly Reports filed on Form 10-Q, certain Current Reports filed on Form 8-K, and amendments to those reports filed with or furnished to the SEC pursuant to Section 13(a) or 15(d) of the 1934 Act available free of charge on or through its internet website as soon as reasonably practicable after such material is filed with or furnished to the SEC. The Bank’s internet website address is www.fhlb-pgh.com. The Bank filed the certifications of the President and Chief Executive Officer, Chief Operating Officer (principal financial officer), and the Chief Accounting Officer pursuant to Sections 302 and 906 of the Sarbanes-Oxley Act of 2002 with respect to the Bank’s 2019 Annual Report on Form 10-K as exhibits to this Report.

Information about the Bank’s Board and its committees and corporate governance, as well as the Bank’s Code of Conduct, is available in the corporate governance section of the “About Us” dropdown on the Bank’s website at www.fhlb-pgh.com. Printed copies of this information may be requested without charge by written request to the Bank’s Legal Department.

Item 1A: Risk Factors

There are many factors - including those beyond the Bank's control - that could cause financial results to differ significantly from the Bank's expectations. The following discussion summarizes some of the more important factors that should be considered carefully in evaluating the Bank's business. This discussion is not exhaustive and there may be other factors not described or factors, such as business, credit, market/liquidity and operational risks, which are described elsewhere in this report (see the Risk Management discussion in Item 7. Management's Discussion and Analysis in this Form 10-K),

14

which could cause results to differ materially from the Bank's expectations. However, management believes that these risks represent the material risks relevant to the Bank, its business and industry. Any factor described in this report could by itself, or together with one or more other factors, adversely affect the Bank's business operations, future results of operations, financial condition or cash flows.

BUSINESS RISK

The Bank is subject to legislative and regulatory actions, including a complex body of Finance Agency regulations, which may be amended in a manner that may affect the Bank's business, operations and financial condition and members' investment in the Bank. Additionally, legislation and regulations applicable to Bank members may affect the Bank’s business as well.

The FHLBanks' business operations, funding costs, rights, obligations, and the environment in which FHLBanks carry out their liquidity mission continue to be impacted by the evolving regulations impacting the finance industry. The Housing Act or HERA was intended to, among other things, expand the Finance Agency's authority and address GSE reform issues. Over the last few years, there have been several legislative efforts and policy proposals regarding reform of the Housing Enterprises, Fannie Mae and Freddie Mac, and the federal government’s ongoing role in the mortgage market. Congress continues to consider GSE reform legislation. Depending on the terms of any such legislation, it could have a material effect on the Bank including debt issuance, financial condition and results of operations. In addition, future legislative changes to the Act or HERA may affect the Bank's business, risk profile, results of operations and financial condition. Recently, there have been legislative efforts and discussions regarding allowing non-banks such as captive insurers, mortgage banks, fintech companies and other financial companies to become members of the FHLBank System. Such entities are subject to different regulatory requirements and may have different risk appetites than the Bank’s current members and, if such entities were to become members of the Bank, it could materially impact the Bank’s risk profile and results of financial condition.

The FHLBanks are also governed by regulations as adopted by the Finance Agency pursuant to their authority under federal laws. The Finance Agency's extensive statutory and regulatory authority over the FHLBanks includes, without limitation, the authority to liquidate, merge or consolidate FHLBanks, redistrict or adjust equities among the FHLBanks. The Bank cannot predict if or how the Finance Agency could exercise such authority in regard to any FHLBank or the potential impact of such action on members' investment in the Bank. The Finance Agency also has authority over the scope of permissible FHLBank products and activities, including the authority to impose limits on those products and activities. The Finance Agency supervises the Bank and establishes the regulations governing the Bank. Changes in Finance Agency leadership may also impact the nature and extent of any new or revised regulations on the Bank.

The Bank cannot predict new guidance or the effect of any new regulations on the Bank's operations. Regulatory requirements on the Bank’s members may affect their capacity and demand for Bank products, and as a result, impact the Bank’s operations and financial condition. Changes in Finance Agency regulations and other Finance Agency regulatory actions could result in, among other things, changes in the Bank's capital composition, an increase in the Banks' cost of funding, a change in permissible business activities, a decrease in the size, scope, or nature of the Banks' lending, investment or mortgage purchase program activities, or a decrease in demand for the Bank's products and services, which could negatively affect its financial condition and results of operations and members' investment in the Bank.

Regulatory changes drive updates to the Bank's computer information systems to support these requirements. Heightened regulatory focus on technology operations including cyber-security, cloud computing and vendor oversight influence the Bank’s operations. Legislation and regulation regarding enhanced cyber-security standards and requirements necessitates additional work to appropriately mitigate the risks and align with requirements. The Finance Agency has issued guidance for the FHLBanks regarding information security and cyber risk management, business resiliency, vendor risk management and cloud. These are all areas of operational risk that are expected to have an ongoing area of regulatory focus. See the Legislative and Regulatory Developments section of Item 7. Management’s Discussion and Analysis in this Form 10-K regarding recent Finance Agency guidance in these areas.

The intention of the United Kingdom’s Financial Conduct Authority (FCA) is to cease sustaining LIBOR after 2021. The introduction of alternative interest rates could adversely affect the Bank’s business, financial condition, and results of operations and increase operational risk.

In July 2017, the Chief Executive of the FCA announced the FCA’s intention to cease sustaining LIBOR after 2021. The Federal Reserve convened the Alternative Reference Rates Committee (ARRC) to identify a set of alternative reference interest rates for possible use as market benchmarks. The ARRC identified the Secured Overnight Financing Rate (SOFR) as such an alternative rate, and the FRB of New York began publishing SOFR rates in the second quarter of 2018.

15

The Bank is not able to predict with certainty that LIBOR will cease to be available after 2021. While the Bank is planning for LIBOR to cease to exist, the market’s transition from LIBOR to alternative rates (e.g., SOFR) is expected to be complicated. Risks relating to the market demand for the Bank’s products, changes in legacy contractual terms on the Bank’s financial assets, liabilities and derivatives, and critical vendors being able to adjust systems to properly process and account for alternative rates are examples of the risks. Additionally, the introduction of alternative rates also may create additional basis risk and increased volatility for market participants including the Bank, as alternative indices are utilized along with LIBOR. Alternative rates and other market changes related to the replacement of LIBOR, including the introduction of financial products and changes in market practices, may lead to risk modeling and valuation challenges. For further details regarding LIBOR/SOFR transition, refer to the Operational and Business Risks section in Item 7: Management’s Discussion and Analysis in this Form 10-K.

The Bank's business is dependent upon its computer information systems. An inability to process or physically secure information or implement technological changes, or an interruption in the Bank's systems, may result in lost business or increased operational risk. The Bank's dependence on computer systems and technologies to engage in business transactions and to communicate with its stakeholders has increased the Bank's exposure to cyber-security risks.

Cyber threats include computer viruses, malicious or destructive code, phishing attacks, brute force attacks, ransomware attacks, denial of service or information or other security breaches. They could result in the unauthorized release, gathering, monitoring, misuse, loss or destruction of confidential, proprietary and other information of the Bank, its employees, its members or other third parties, or otherwise materially disrupt the Bank’s or its members’ or other third parties’ network access, business operations or ability to provide services. For example, the Bank provides on-line banking transactional capability to enable its members to execute borrowing and other transactions with the Bank. The Bank like many financial institutions and others businesses faces cyber attack attempts routinely, for example, from phishing campaigns and denial of service attempts. Although the Bank has both information and physical security measures in place and devotes significant resources to secure the Bank's computer systems and networks, it might not be able to anticipate or implement effective preventive measures against all security breaches, particularly given that such attacks have significantly evolved in scale and maliciousness during the past few years. Additionally, cyber vulnerabilities and/or attacks could go undetected for a period of time. During such time, the Bank may not necessarily know the extent of the harm and certain actions could be compounded before they are discovered and remediated, any or all of which could further increase the consequences of a cyber attack.

As cyber threats continue to evolve, the Bank may be required to expend significant additional resources to continue to modify or enhance its layers of defense or to investigate and remediate any information security vulnerabilities. Previously, the Bank had experienced a limited number of successful desktop (e.g., malware) security incidents. However, these incidents were limited and did not involve any breaches of data such as those that trigger notice requirements under applicable law. Each of these incidents was responded to appropriately which prevented material impact on the Bank’s operations. The Bank’s technology control environment, along with security policies and standards, incident response procedures, security controls testing and dedicated information security resources, have protected the Bank against material cyber-security attacks. In addition, the Bank completes periodic independent assessments that leverage industry recognized frameworks in order to continually improve the Bank’s control environment against cyber-security attacks. If a successful penetration were to occur, it might result in unauthorized access to digital systems for purposes of misappropriating assets (including loss of funds), or sensitive information (including confidential information of the Bank, members, counterparties or mortgage loan borrowers), corrupt data or cause operational disruption. This may result in financial loss or a violation of privacy or other laws. The Bank could incur substantial costs and suffer other negative consequences as a result, including but not limited to remediation costs, increased security costs, litigation, penalties, and reputational damage.

In addition, the Bank's business is dependent upon its ability to effectively exchange and process information using its computer information systems. The Bank's products and services require a complex and sophisticated computing environment, which includes licensed or purchased, custom-developed software, and software-as-a-service (SaaS). Maintaining the effectiveness and efficiency of the Bank's operations is dependent upon the continued timely implementation of technology solutions and systems, which may require ongoing expenditures, as well as the ability to sustain ongoing operations during technology solution implementations or upgrades. If the Bank were unable to sustain its technological capabilities, it may not be able to remain competitive, and its business, financial condition and profitability may be significantly compromised. To advance its disaster recovery and continuous operations, the Bank continues to take steps to review and improve its recovery facilities and processes through its Business Continuity Plan and testing those plans annually. Nonetheless, the Bank cannot guarantee the effectiveness of its Business Continuity Plan or other related policies, procedures and systems to protect the Bank in any particular future situation.

16

Global financial market disruptions could result in uncertainty and unpredictability for the Bank in managing its business. Geopolitical conditions, widespread health emergencies or a natural disaster, especially those affecting the Bank or the Bank's district, customers or counterparties, could also adversely affect the Bank's business, results of operations or financial condition.