Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - IDEX CORP /DE/ | d482077d8k.htm |

| EX-99.2 - TRANSCRIPT OF IDEX CORPORATIONS EARNINGS CONFERENCE CALL - IDEX CORP /DE/ | d482077dex992.htm |

Fourth Quarter 2012 Earnings Release

February 5, 2013

Exhibit 99.1 |

Agenda

2

•

IDEX Outlook

•

2012 Financial Performance

•

2012 Segment Performance

Fluid & Metering

Health & Science

Fire & Safety / Diversified

•

2013 Guidance

•

Q&A |

IDEX Proprietary & Confidential

Replay Information

Dial toll–free: 855.859.2056

International: 404.537.3406

Conference ID: #86510532

Log on to: www.idexcorp.com

3 |

IDEX Proprietary & Confidential

Cautionary Statement Under the Private Securities

Litigation Reform Act

This presentation and discussion will include forward-looking statements.

Our actual performance may differ materially from that indicated

or suggested

by any such statements. There are a number of factors that could cause those

differences, including those presented in our most recent annual

report and

other company filings with the SEC.

4 |

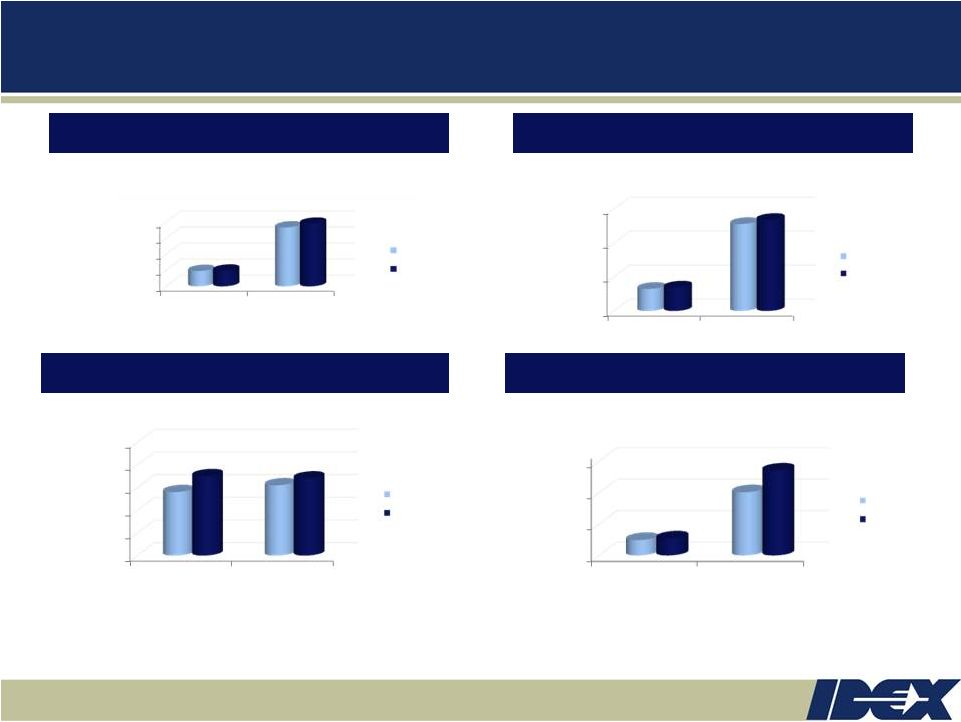

IDEX Proprietary & Confidential

Total Revenue

Operating Margin*

Free Cash Flow**

EPS*

IDEX 2012 Financial Performance

Continued growth, margin expansion and strong cash flow in a volatile

market 5

* 2012 EPS / Op Margin data adjusted for impairment charge ($198M for Q4 and YTD) and

restructuring expenses ($18M in Q4 and $32M YTD) while 2011 EPS / Op Margin data

adjusted for restructuring expenses ($9M in Q4 and $12M YTD) and CVI inventory step-up expense ($16M YTD)

** 2011 Q4 and YTD Free Cash Flow adjusted for the forward starting interest rate swap

settlement ($39M) Org: 3%

30 bps expansion

30% growth

Org: Flat

5% growth

6% growth

70 bps expansion

8% growth

$0

$500

$1,000

$1,500

$2,000

Q4

Year

$481

$1,838

$491

$1,954

2011

2012

$0.00

$1.00

$2.00

$3.00

Q4

Year

$0.65

$2.56

$0.69

$2.68

2011

2012

$25

$125

$225

$325

Q4

Year

$74

$226

$79

$295

2011

2012

15%

16%

17%

18%

19%

20%

Q4

Year

17.8%

18.1%

18.5%

18.4%

2011

2012 |

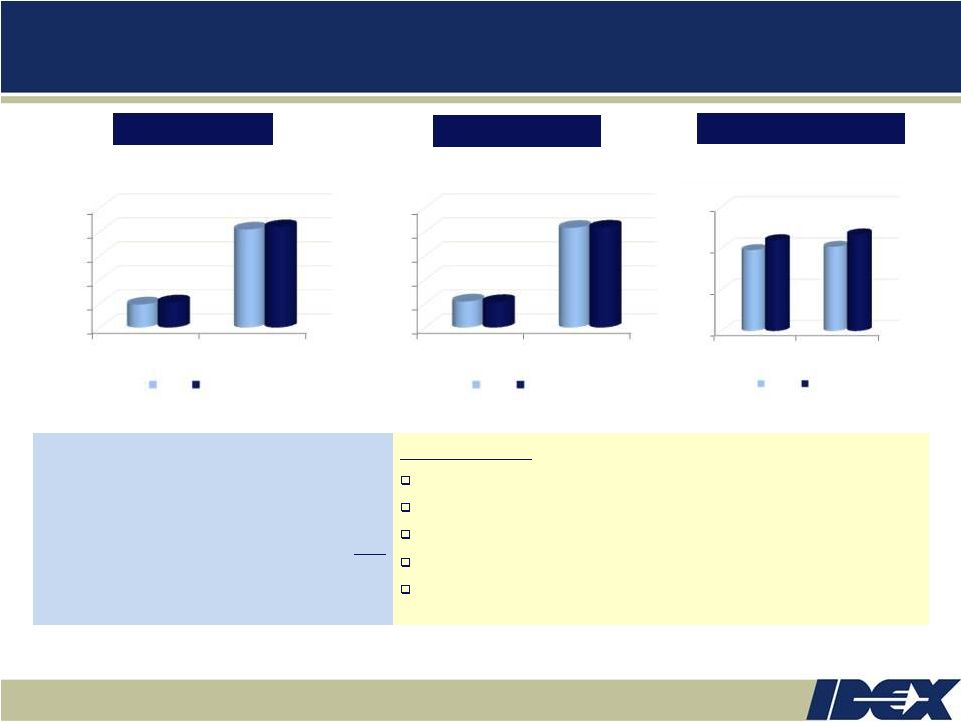

IDEX Proprietary & Confidential

Fluid & Metering

Productivity and strong execution generated margin expansion of 150 bps

in 2012 6

Q4 Sales Mix:

Organic

-1%

Acquisition

0%

Fx

-1%

Total

-2%

Q4

Summary:

Energy and Ag markets remain robust

Chemical project activity has rebounded

Municipal water services remain soft

Excellent operational execution and productivity

Improved general market environment

Total Orders

Total Revenue

Operating Margin*

Org: 2% growth

150 bps expansion

Org: 4% growth

* Op Margin data adjusted for impairment charge (2012) and restructuring expense (2012 and

2011) Org: 10% growth

Org: 1% decline

120 bps expansion

$0

$200

$400

$600

$800

$1,000

Q4

Year

$192

$817

$209

$836

2011

2012

$0

$200

$400

$600

$800

$1,000

Q4

Year

$217

$831

$212

$833

2011

2012

10%

15%

20%

25%

Q4

Year

19.8%

20.2%

21.0%

21.7%

2011

2012 |

IDEX Proprietary & Confidential

Health & Science

Q4 Operating Margins of 18.4% up 110 bps sequentially

7

Q4 Sales Mix:

Organic

-3%

Acquisition

+9%

Fx

0%

Total

+6%

Q4

Summary:

Scientific Fluidics experienced sequential growth and favorable

outlook in Asia

Synergies being realized between Matcon and the remainder of MPT

Optics & Photonics long term prospects remain solid

Industrial-exposed businesses off to a good start in January 2013

* Op Margin data adjusted for impairment charge (2012), restructuring

expense (2012 and 2011) and CVI inventory step-up expense (2011)

Total Orders

Total Revenue

Operating Margin*

Org: 1% decline

280 bps contraction

Org: 2% decline

Org: 4% decline

Org: 3% decline

100 bps contraction

$0

$200

$400

$600

$800

Q4

Year

$163

$597

$170

$674

2011

2012

$0

$200

$400

$600

$800

Q4

Year

$165

$608

$175

$695

2011

2012

10%

15%

20%

25%

Q4

Year

19.4%

20.4%

18.4%

17.6%

2011

2012 |

IDEX Proprietary & Confidential

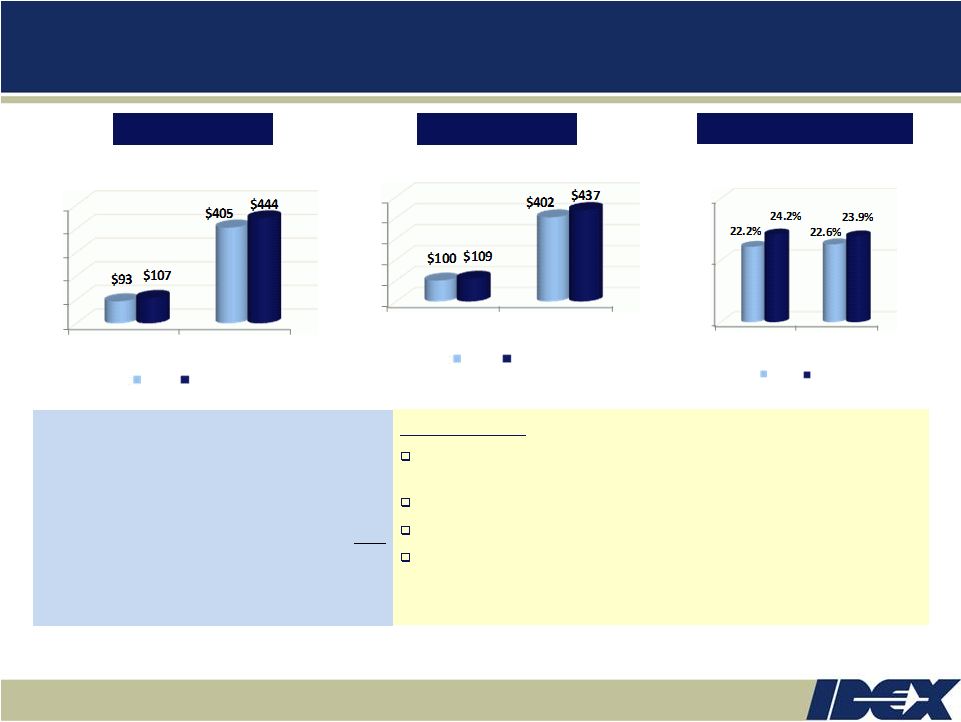

$0

$100

$200

$300

$400

$500

Q4

Year

2011

2012

$0

$100

$200

$300

$400

$500

Q4

Year

2011

2012

10%

20%

30%

Q4

Year

2011

2012

Fire & Safety/Diversified

Tremendous performance across all of the diversified businesses

8

Q4 Sales Mix:

Organic

+10%

Acquisition

0%

Fx

-1%

Total

+9%

Q4

Summary:

North American Fire markets were steady in Q4 and completed restructuring

activities will generate benefit in FY13

Rescue experiencing strong North American and Middle Eastern markets

Dispensing domestic markets remain strong

Op margins are up 200 bps driven by structural cost actions, productivity and

volume leverage

* Op Margin data adjusted for restructuring expense (2012 and

2011) Total Orders

Total Revenue

Operating Margin*

Org: 11% growth

130 bps expansion

Org: 12% growth

Org: 14% growth

Org: 10% growth

200 bps expansion |

IDEX Proprietary & Confidential

2013 Guidance Detail

9

Completed structural cost actions driving earnings growth

2013 Growth Expectations

Low to mid single digit organic revenue growth

Future acquisitions not contemplated in the growth below

* EPS adjusted to exclude impairment and restructuring charges

** Wage, fringe and material inflation, net of productivity and sourcing savings

Sales

EPS

(in M's)

FY 2012 Actuals*

$

1,954 $ 2.68

Organic Growth

40 -

75

0.10 -

0.20

FX

0.01

Full Year Acquisitions

30

0.03

Structural Cost Benefits

0.24

Growth Investments

(0.14)

Net Inflation**

(0.07)

FY 2013 Forecast

$2.0 -

$2.1B

$2.85 -

$2.95

10 |

IDEX Proprietary & Confidential

Outlook: 2013 Guidance Summary

Q1 2013

EPS

estimate

range:

$0.70

–

$0.72

Flat organic revenue growth

Positive acquisition impact ~ 3%

Operating margin ~ 18.5%

FY 2013

EPS

estimate

range:

$2.85

–

$2.95

Low-to-mid single digit organic revenue growth

Positive acquisition impact ~ 1.5%

Operating margin ~ 19%

Positive Fx impact ~ 1% to sales

Other modeling items

Tax

rate

~

29

-

30%

Cap

Ex

~

$40

-

$42M

Free Cash Flow will significantly exceed net income

Continued opportunistic share repurchases

EPS estimate excludes future acquisitions

10 |

IDEX Proprietary & Confidential

Q&A

11 |