Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - LyondellBasell Industries N.V. | d477435d8k.htm |

| EX-99.1 - PRESS RELEASE DATED FEBRUARY 1, 2013 - LyondellBasell Industries N.V. | d477435dex991.htm |

Jim

Gallogly, Chief Executive Officer Karyn Ovelmen, Chief Financial Officer

Doug Pike, VP -

Investor Relations

February 1, 2013

Fourth-Quarter 2012 Earnings

Exhibit 99.2

Sergey Vasnetsov, SVP - Strategic Planning and Transactions

|

lyondellbasell.com

Cautionary Statement

2

The information in this presentation includes forward-looking statements. These

statements relate to future events, such as anticipated

revenues, earnings, business strategies, competitive position or other aspects of our

operations or operating results. Actual outcomes and results may differ materially from

what is expressed or forecast in such forward-looking statements. These statements are

not guarantees of future performance and involve certain

risks, uncertainties and assumptions that are difficult to predict. Factors

that could cause actual results to differ from forward-looking statements include, but are not

limited to, availability, cost and price volatility of raw materials and utilities;

supply/demand balances; industry production capacities and operating rates;

uncertainties associated with worldwide economies; legal, tax and environmental

proceedings; cyclical nature of the chemical and refining industries;

operating interruptions; current and potential governmental regulatory actions; terrorist

acts; international political unrest; competitive products and pricing; technological

developments; the ability to comply with the terms of our credit

facilities and other financing arrangements; the ability to implement business

strategies; and other factors affecting our business generally as set forth in the

“Risk Factors” section of our Form 10-K for the year ended

December 31, 2011, which can be found at www.lyondellbasell.com on the Investor

Relations page and on the Securities and Exchange Commission’s website at www.sec.gov.

This presentation contains time sensitive information that is accurate only as of the date

hereof. Information contained in this presentation is unaudited and

is subject to change. We undertake no obligation to update the information

presented herein except as required by law. |

Information Related to Financial Measures

3

We have included EBITDA in this presentation, which is a non-GAAP measure, as we believe

that EBITDA is a measure commonly used by investors. However, EBITDA, as presented

herein, may not be comparable to a similarly titled measure reported by other

companies due to differences in the way the measure is calculated. For purposes of

this presentation, EBITDA means net income before net interest expense, income taxes,

depreciation and amortization, reorganization items, income from equity investments,

income(loss) attributable to non-controlling interests, net income (loss) from discontinued

operations, plus joint venture dividends, as adjusted for other items management does not

believe are indicative of the Company’s underlying results of operations such as

impairment charges, asset retirement obligations and the effect of

mark-to-market accounting on our warrants. The specific items for which

EBITDA is adjusted in each applicable reporting period may only be relevant in certain periods and

are disclosed in the reconciliation of non-GAAP financial measures. EBITDA should not be

considered an alternative to profit or operating profit for any period as an

indicator of our performance, or as an alternative to operating cash flows as a

measure of our liquidity. See Table 9 of our accompanying earnings release for

reconciliations of EBITDA to net income. While we also believe that free cash flow (FCF) measure is commonly used by investors, free

cash flow, as presented herein, may not be comparable to similarly titled

measures reported by other companies due to differences in the way

the measure is calculated. For purposes of this presentation, free cash flow means

net cash provided by operating activities minus capital expenditures. lyondellbasell.com |

lyondellbasell.com

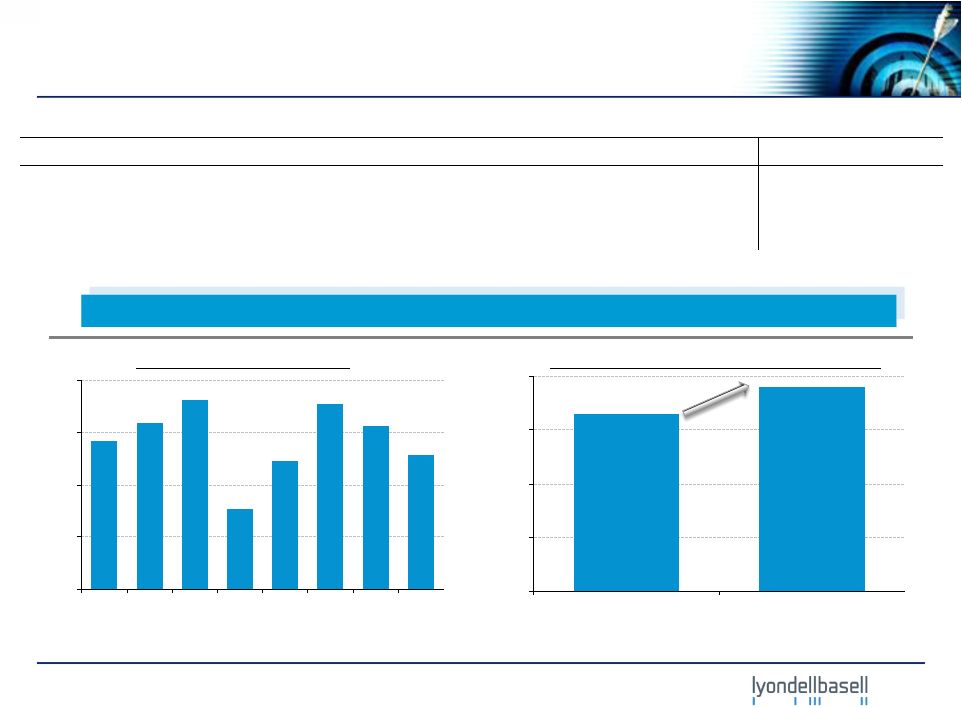

Highlights

EBITDA

(1)

1Q’11

–

4Q’12

FY

2012

Record

Earnings

–

16%

growth

in

Income

from

Continuing

Operations

vs.

2011

($ in millions)

4

500

1,000

1,500

$2,000

1Q'11

2Q'11

3Q'11

4Q'11

1Q'12

2Q'12

3Q'12

4Q'12

Income from Continuing Operations

750

1,500

2,250

$3,000

2011

2012

16%

($ in millions, except per share data)

4Q'12

3Q'12

4Q'11

FY 2012

FY 2011

EBITDA

(1)

$1,289

$1,565

$766

$5,856

$5,585

Income from Continuing Operations

$645

$851

$27

$2,858

$2,472

Diluted Earnings ($ / share) from Continuing Operations

$1.13

$1.47

$0.05

$4.96

$4.32

(1)

(1)

1)

The third quarter 2012 includes a $71 million market price recovery that offset second quarter 2012

lower of cost or market adjustment (LCM). |

lyondellbasell.com

Record Health, Safety and Environmental Performance

1) Includes employees and contractors.

Injuries per 200,000 Hours

Worked

(1)

Indexed Environmental Incidents

Indexed Process Incidents

5

0.00

0.15

0.30

0.45

0.60

2009

2010

2011

2012

0%

25%

50%

75%

100%

2009

2010

2011

2012

0%

25%

50%

75%

100%

2009

2010

2011

2012 |

lyondellbasell.com

Finance

•

Generated $4.8 billion cash

from operations

•

Paid $2.4 billion in

dividends, equivalent to ~

7% dividend yield

(2)

•

Increased quarterly interim

dividend to $0.40 per share

•

Reduced net annual interest

expense by $367 million

•

Received $147 million in JV

dividends

•

S&P 500 index inclusion

2012 Accomplishments

Manufacturing

•

Increased NGL cracking by

10% to 85% of North

American ethylene

production

•

Second half of the year,

North American ethylene

production exceeded

nameplate capacity

•

Completed two key

maintenance turnarounds at

two of our largest sites

•

Manufacturing achieved

multiple production records

Commercial

•

All major expansion

projects on schedule

•

Defined next phase of

ethylene expansions

•

Advanced European

restructuring and

optimization

•

Signed China Propylene

Oxide joint venture MOU

Record Results, continued progress made across the company

($ in millions)

Overall

•

Record earnings

•

89%

total

return

vs.

13%

for

S&P 500

(1)

•

Outstanding HSE

performance

•

Normalized fixed costs

managed flat since 2009

•

Ceased operations at the

Berre refinery

1)

Based

on

CapIQ

dividend

adjusted

beginning

and

closing

prices

for

2012.

2)

Dividend Yield data means the total 2012 dividends divided by the company market

capitalization. The market cap is calculated based on December 31, 2012 closing stock price and approximately 577 million outstanding shares.

6

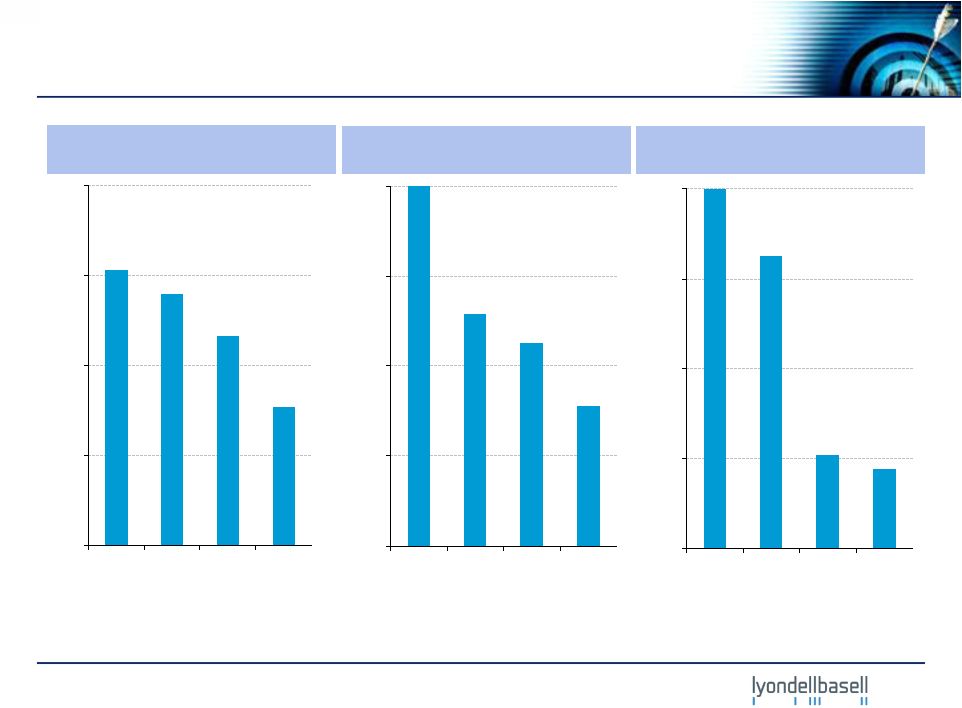

Segment EBITDA

2011 EBITDA

2012 EBITDA

Y-o-Y Change

Y-o-Y Change, %

Olefins & Polyolefins - Americas

$2,140

$2,963

$823

38%

Olefins & Polyolefins - EAI

894

561

(333)

-37%

Intermediates & Derivatives

1,392

1,653

261

19%

Refining

977

481

(496)

-51%

Technology

214

197

(17)

-8%

Total

$5,585

$5,856

$271

5% |

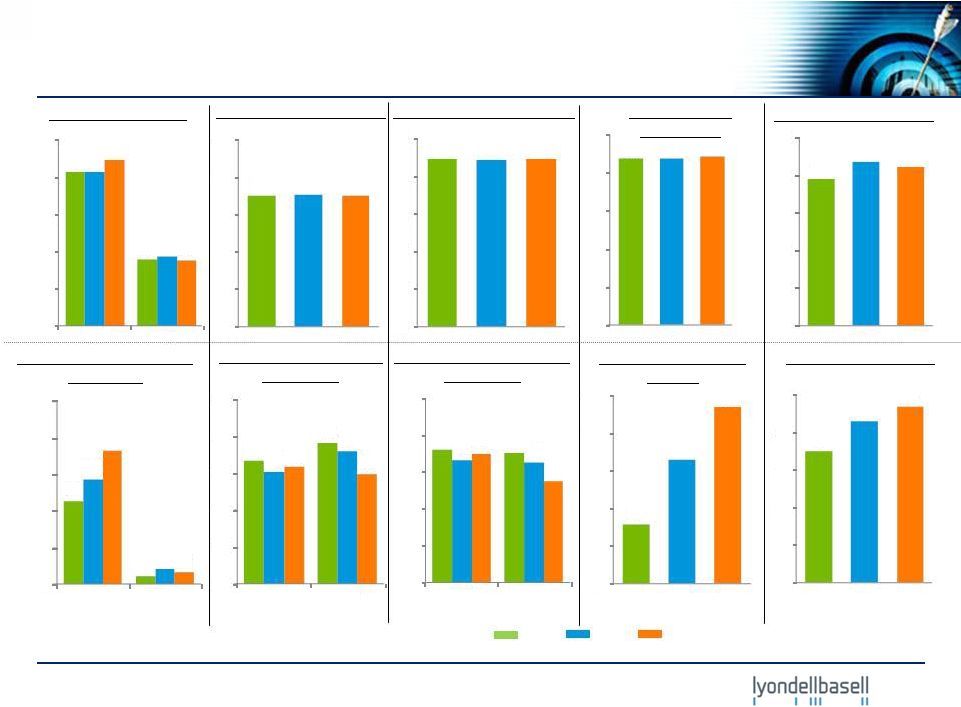

lyondellbasell.com

Key

Volumes

and

Margins:

2010

-

2012

HRO Crude Oil Rates

Polyethylene Volumes

Polypropylene Volumes

Maya 2-1-1 Spreads

Indexed Polyethylene

Spreads

(3)

Indexed Polypropylene

Spreads

(3)

Ethylene Volumes

Indexed Ethylene Cash

Margins

(2)

2010

2011

I&D Chemical

Volumes

(1)

MTBE Raw Material

Margin

MBPD

($/bbl)

billion lbs

billion lbs

billion lbs

billion lbs

(Cents/gal)

7

2012

1) I&D volumes exclude oxyfuels

2) EU ethylene cash margins normalized to 2009 US margins. 2009 indexed margin is

equal to 1.0 3) Polyethylene and Polypropylene spreads indexed to 2009;

2009 indexed margins are equal to 1.0 10.6

10.5

10.7

0

2

5

7

10

12

236

263

255

0

60

120

180

240

300

9.0

8.9

9.0

0

2

4

6

8

10

10.5

10.6

10.6

0

3

6

9

12

15

8.4

3.6

8.4

3.7

9.0

3.5

0

2

4

6

8

10

US

EU

2.3

0.2

2.9

0.5

3.7

0.3

0

1

2

3

4

5

US

EU

1.0

1.2

0.9

1.1

1.0

0.9

0.0

0.3

0.6

0.9

1.2

1.5

US

EU

1.1

1.1

1.0

1.0

1.1

0.8

0.0

0.3

0.6

0.9

1.2

1.5

US

EU

40

83

118

0

25

50

75

100

125

18

22

24

0

5

10

15

20

25 |

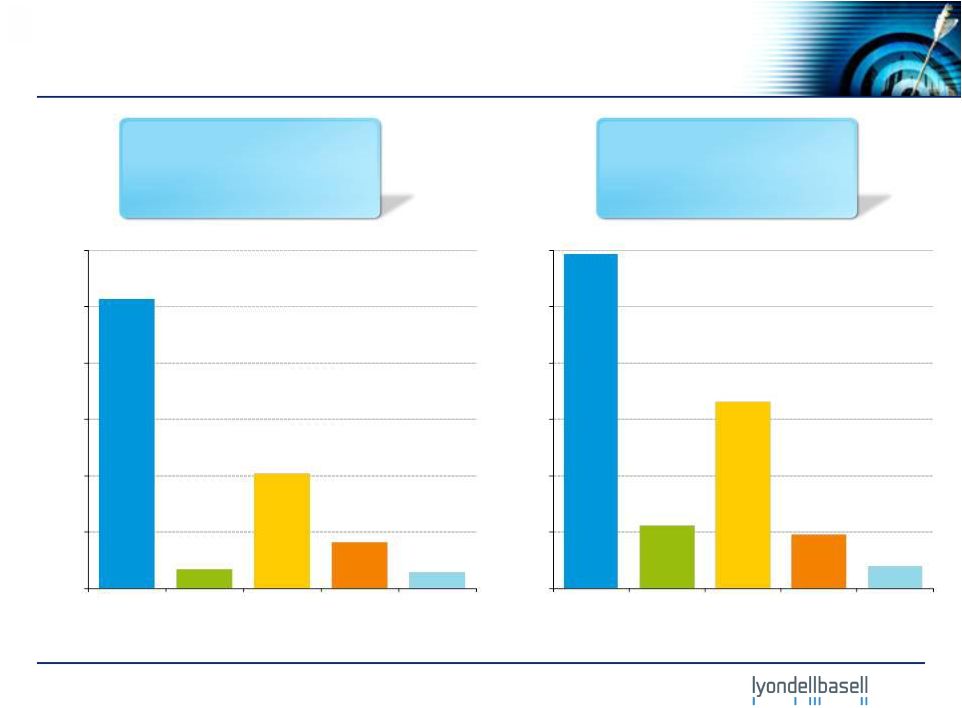

lyondellbasell.com

FY 2012 EBITDA

Fourth-Quarter 2012 and FY 2012 Segment EBITDA

Fourth-Quarter 2012 EBITDA

($ in millions)

($ in millions)

8

Q4’12 EBITDA

$1,289 million

Q4’12 Operating Income

$959 million

FY 2012 EBITDA

$5,856 million

FY 2012 Operating Income

$4,676 million

150

300

450

600

750

$900

Olefins &

Polyolefins -

Americas

Olefins &

Polyolefins -

EAI

Intermediates

& Derivatives

Refining

Technology

500

1,000

1,500

2,000

2,500

$3,000

Olefins &

Polyolefins -

Americas

Olefins &

Polyolefins -

EAI

Intermediates

& Derivatives

Refining

Technology |

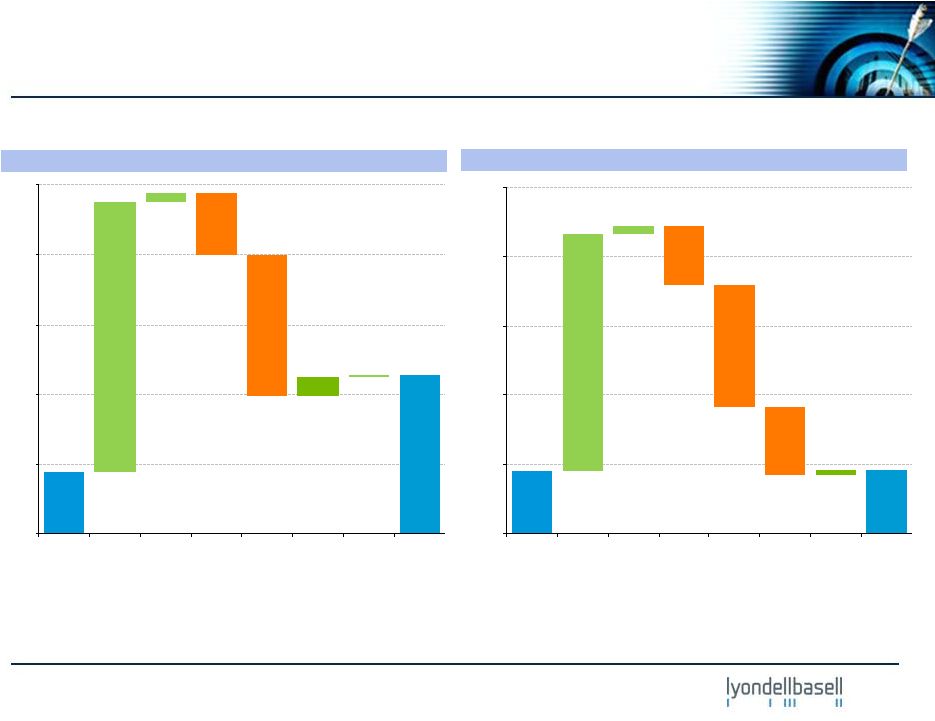

lyondellbasell.com

$2,711

$2,732

0

3,000

6,000

9,000

12,000

$15,000

May 2010

Begin.

Cash

Balance

CF from

Operations

excl.

Working

Capital

Working

Capital

Changes

Capex

Dividends

Net Debt

Repayment

Other

2012

Ending

Cash

Balance

$1,065

$2,732

0

1,200

2,400

3,600

4,800

$6,000

2012

Beginning

Cash

Balance

CF from

Operations

excl.

Working

Capital

Working

Capital

Changes

Capex

Dividends

Net Debt

Repayment

Other

2012

Ending

Cash

Balance

1) Beginning and ending cash balance includes cash and cash equivalents; 2)

Includes inventories, accounts payable and accounts receivable; 3) Includes capital and maintenance

turnaround spending.

(3)

(2)

(1)

($ in millions)

(2)

(1)

FY 2012

May 2010 –

December 2012

(3)

(1)

9

(1)

Cash Flow |

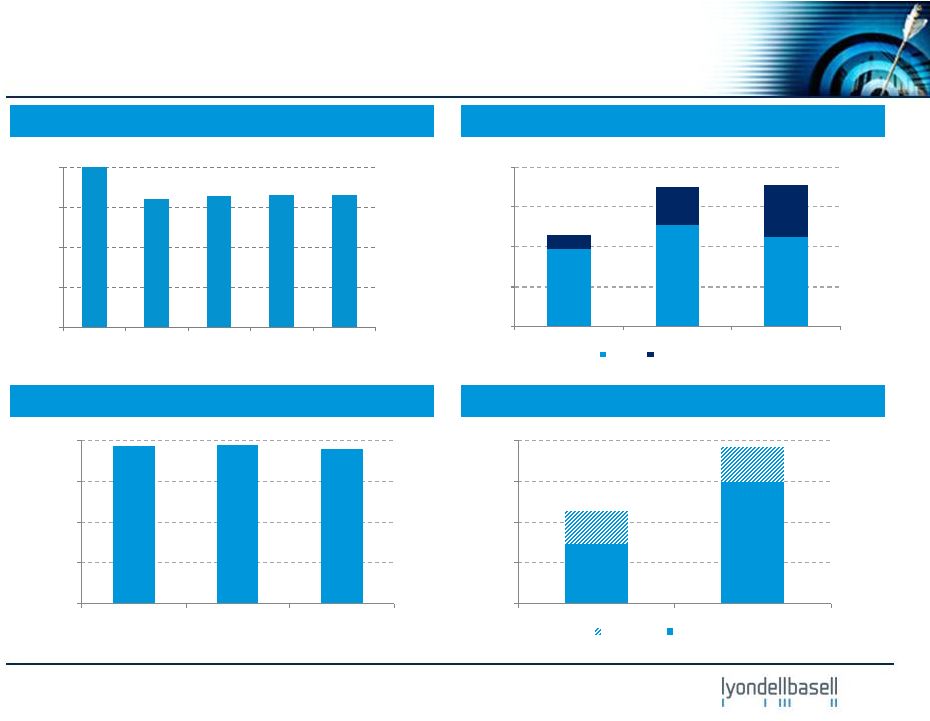

lyondellbasell.com

0

300

600

900

$1,200

2010

2011

2012

Base

Growth

10

Indexed

Cash

Fixed

Cost

(1)

Working

Capital

(2)

Capital Expenditures

Free

Cash

Flow

(3)

Working Capital and Key Financial Statistics

0

1,500

3,000

4,500

$6,000

2010

2011

2012

($ in millions)

($ in millions)

($ in millions)

0

1,250

2,500

3,750

$5,000

2011

2012

Capex

Free Cash Flow

1) Cash fixed costs include costs related to compensation, travel, insurance, third

party services, maintenance, marketing, selling, and administration; 2) Figures depicted represent

end

of

year

balances;

3)

Free

Cash

Flow

=

net

cash

provided

by

operating

activities

–

capex

0%

25%

50%

75%

100%

2008

2009

2010

2011

2012

(2008 index = 100%) |

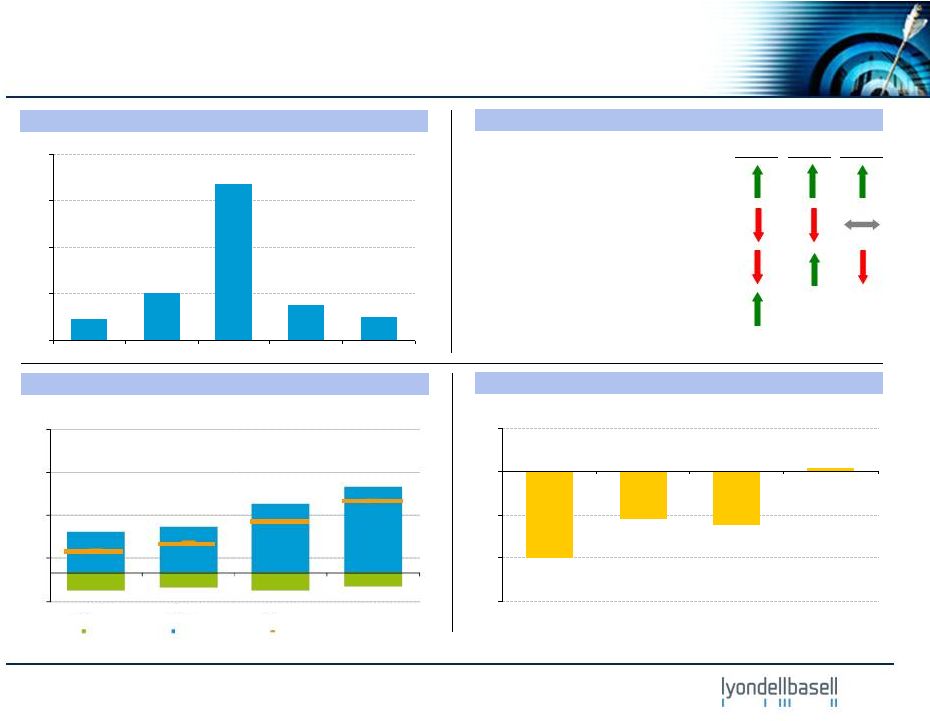

lyondellbasell.com

Olefins & Polyolefins -

Americas

Highlights and Business Drivers -

4Q’12

U.S. Olefins

•

100% capacity utilization

•

Margin up driven by higher ethylene

price

Polyethylene

•

Volumes relatively steady

•

Spread down 1¢/lb

Polypropylene (includes Catalloy)

•

Volumes down ~ 6%

•

Spread down 1¢/lb

Ethylene Chain Margins (per IHS)

EBITDA

(1)

Performance vs. 3Q’12

Polypropylene Margins (per IHS)

EBITDA

Margin

Volume

($ in millions)

(cents / lb)

(cents / lb)

11

1) Q3’12 EBITDA includes a $71 million non-cash LCM reversal of Q2’12

LCM inventory valuation adjustment. Q2’12 results include $29 million proceeds from hurricane

insurance settlement. Q1’12 and Q3’12 include $10 million each in

dividends from Indelpro joint venture. (1)

0

1

2

3

4

4Q'11

3Q'12

4Q'12

Jan'13

0

200

400

600

800

$1,000

4Q'11

1Q'12

2Q'12

3Q'12

4Q'12

(10)

5

20

35

50

4Q’11

3Q’12

4Q’12

Jan’13

Ethane Margin

Naphtha Margin

HDPE Margin

Ethylene/HDPE Chain |

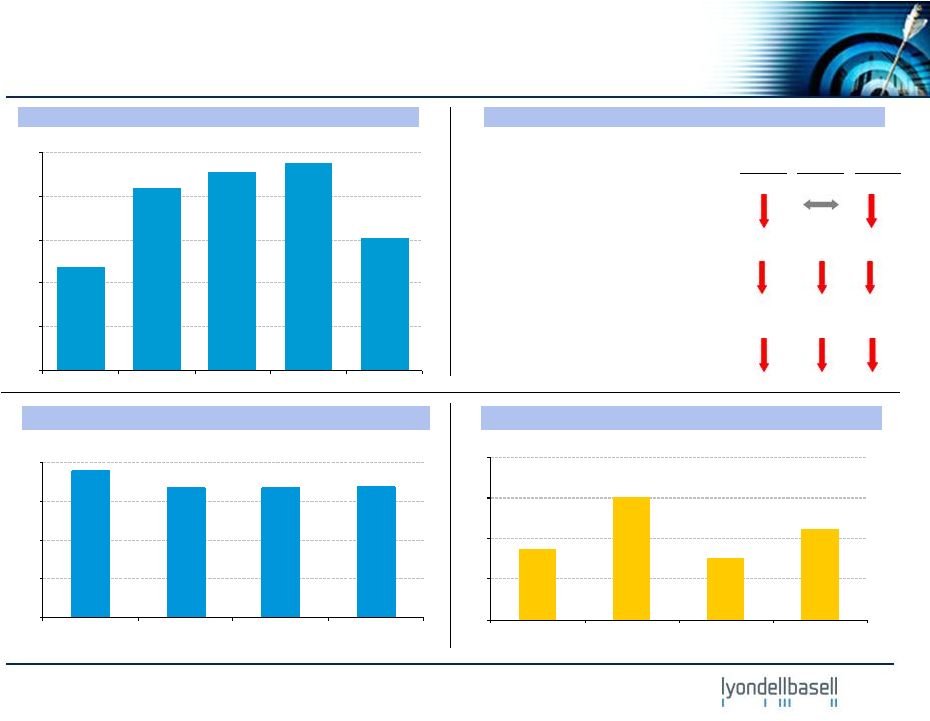

lyondellbasell.com

EBITDA

Margin

Volume

100

200

300

$400

4Q'11

1Q'12

2Q'12

3Q'12

4Q'12

Olefins & Polyolefins -

Europe, Asia, International

Highlights and Business Drivers -

4Q’12

EU Olefins

•

Margin near breakeven

•

Completed Wesseling turnaround

Polyethylene

•

Volumes relatively unchanged

Polypropylene (includes Catalloy)

•

Volumes down ~ 4%

JV dividends

•

Equity income relatively unchanged

•

$50 million in dividends received

European Ethylene Chain Margins (per IHS)

EBITDA

Performance vs. 3Q’12

European Polypropylene Margins (per IHS)

($ in millions)

(cents / lb)

(cents / lb)

12

(6)

(4)

(2)

0

2

4Q'11

3Q'12

4Q'12

Jan'13

(10)

5

20

35

50

4Q'11

3Q'12

4Q'12

Jan'13

HDPE Margin

Naphtha Margin

Ethylene/HDPE Chain |

lyondellbasell.com

0

11

22

33

44

4Q11

3Q12

4Q12

1Q13 E

Intermediates & Derivatives

Highlights and Business Drivers -

4Q’12

EBITDA

Propylene Oxide and Derivatives

•

Seasonal impact on volumes

•

Slow aircraft deicer sales

Intermediates

•

Seasonal impact on volumes and C4

chemical margins

Oxyfuels

EBITDA

Margin

Volume

Performance vs. 3Q’12

($ in millions)

13

EU MTBE Raw Material Margins (per Platts)

(cents / gallon)

P-Glycol Raw Material Margins (per Chemdata)

(cents / lb)

0

50

100

150

200

4Q'11

3Q'12

4Q'12

Jan'13

100

200

300

400

$500

4Q'11

1Q'12

2Q'12

3Q'12

4Q'12

•

Seasonal impact on volumes and

gasoline to butane spread |

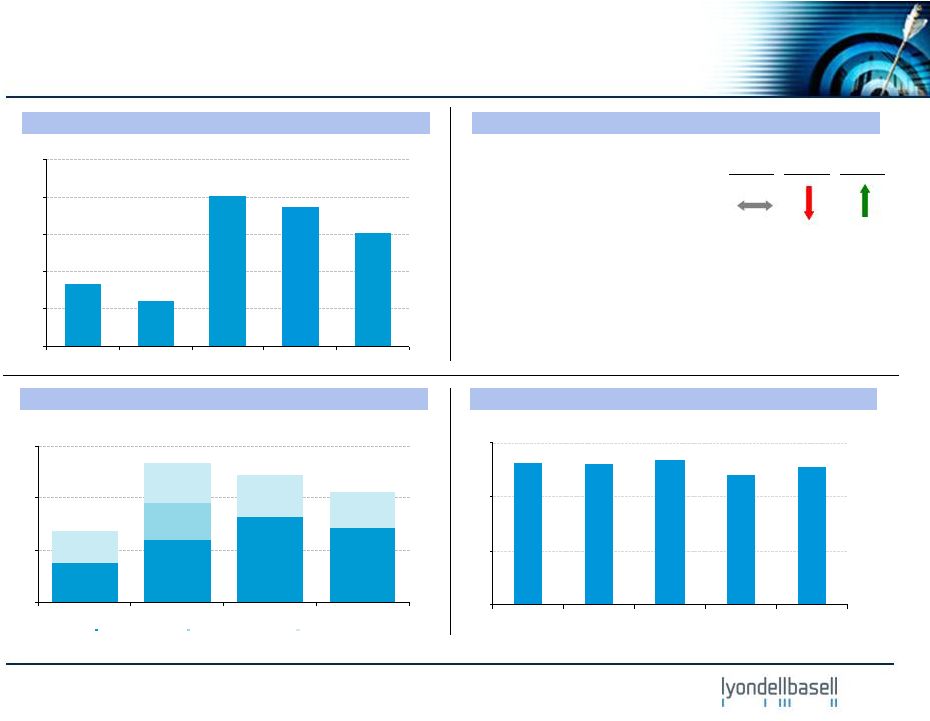

lyondellbasell.com

0

100

200

300

4Q'11

1Q'12

2Q'12

3Q'12

4Q'12

0

10

20

30

4Q'11

3Q'12

4Q'12

Jan'13

Lt-Hvy

Lt-Gasoline

Lt-Heating Oil

40

80

120

160

$200

4Q'11

1Q'12

2Q'12

3Q'12

4Q'12

Refining Highlights and Business Drivers -

4Q’12

Houston Refinery

•

Underlying EBITDA is relatively

unchanged

•

Q4 crude throughput: 255 MBPD;

refinery operational limitations

•

Maya 2-1-1: $24.36 per bbl

Refining Spreads (per Platts)

(2)

EBITDA

(1)

Performance vs. 3Q’12

EBITDA

Margin

Volume

($ in millions)

($ / bbl)

1) Q3’12 includes $24 million of restitution while Q2’12 includes

$53 million of hurricane insurance settlement; Underlying EBITDA is relatively unchanged exclusive of these items.

2) Light Louisiana Sweet (LLS) is the referenced light crude.

14

HRO Operating Rate

(MBPD)

(1) |

lyondellbasell.com

–

Benefitting from low ethane and propane

costs, increasing co-product values

–

Positive momentum building in:

•

U.S. ethylene, propylene, and polyethylene

–

European olefins chain remains weak

–

Houston refinery and I&D turnarounds in

the first quarter

–

Growth projects remain on schedule

15

Fourth-Quarter Summary and Outlook

–

Strong U.S. Olefins results

•

Continued U.S. NGL advantage

–

Business declines driven by seasonal

effects such as:

•

Lower oxyfuels margins

•

Lower polyolefin and I&D volumes

–

Minimal EBITDA generated in:

•

European olefins and commodity

polyolefins

–

Dividends

•

Paid $2.75 per share special dividend in

addition to interim dividend of $0.40 per

share

Fourth-Quarter Summary

Near-term Outlook |

lyondellbasell.com

Save the Date

16

Save the Date!

We cordially invite you to attend LyondellBasell's Investor Day on March 13,

2013, in New York. At this half-day session, you will have an

opportunity to interact with members of our leadership team and get an

update on current results, near-term outlook and long-term plans

for profitable growth. We hope you can join us to learn more about how we

are seizing the moment to secure our future success.

LOCATION

New York Marriott Marquis

Astor Ballroom

1535 Broadway,

New York, NY

10036

Invitation and additional information to follow. |