Attached files

| file | filename |

|---|---|

| EX-23.3 - CONSENT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM - ISHARES DIVERSIFIED ALTERNATIVES TRUST | d410618dex233.htm |

Table of Contents

As filed with the Securities and Exchange Commission on February 1, 2013

Registration No. 333-184143

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

Pre-Effective Amendment No. 2

to

Form S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

iSHARES® DIVERSIFIED ALTERNATIVES TRUST

SPONSORED BY iSHARES® DELAWARE TRUST SPONSOR LLC

(Exact name of Registrant as specified in its charter)

| Delaware | 6799 | 26-4632352 | ||

| (State or other Jurisdiction of Incorporation or Organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

c/o BlackRock Asset Management International Inc.

400 Howard Street

San Francisco, CA 94105

Attn: Product Management Team and Intermediary Investor and Exchange-Traded Products Department

(415) 670-2000

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

BlackRock Asset Management International Inc.

400 Howard Street

San Francisco, CA 94105

Attn: Product Management Team and Intermediary Investor and Exchange-Traded Products Department

(415) 670-2000

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| David Yeres, Esq. Clifford Chance US LLP 31 West 52nd Street New York, NY 10019 |

Deepa Damre, Esq. BlackRock Fund Advisors 400 Howard Street San Francisco, CA 94105 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. x

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act of 1933, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act of 1933, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act of 1933, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | x | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

CALCULATION OF REGISTRATION FEE

| Title of each class of securities to be registered | Amount to be registered |

Proposed maximum offering price per Share |

Proposed maximum aggregate offering price |

Amount of registration Fee(1) |

||||||||||||

| Shares |

16,900,000 | $0 | $0 | $0 | ||||||||||||

| (1) | This Registration Statement (the “replacement registration statement”) relates to 16,900,000 shares of the registrant that were previously registered pursuant to Registration Statement No. 333-153099 (the “expiring registration statement”) originally declared effective by the Securities and Exchange Commission on November 12th, 2009, and which remain unsold at the time of effectiveness of this replacement registration statement (such shares, the “unsold shares”). A filing fee of $47,151 was paid in respect of the unsold shares at the time of filing of the expiring registration statement. As provided in Rule 415(a)(6) under the Securities Act, the fee so paid will continue to be applied to the unsold shares and no additional filing fee is required. |

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said section 8(a), may determine.

Table of Contents

16,900,000 Shares

iShares® Diversified Alternatives Trust

The iShares® Diversified Alternatives Trust, or the Trust, is a Delaware statutory trust that issues Shares representing fractional undivided beneficial interests in its net assets. The Trust seeks to maximize its absolute returns by investing in long and/or short positions in foreign-currency forward contracts and exchange-traded futures contracts selected by BlackRock Fund Advisors, the Trust’s Advisor, following investment strategies that utilize quantitative methodologies to identify potentially profitable discrepancies in the relative values or market prices of one or more assets. See “Business of the Trust—Investment Objective; Strategies.” The objective of the Trust is to maximize absolute returns from investments with historically low correlation to traditional asset classes while seeking to control the risks and volatility inherent in futures and forward contracts by taking long and short positions in historically correlated assets.

The Shares are listed for trading on NYSE Arca under the symbol “ALT.” BlackRock Institutional Trust Company, N.A. is the Trustee of the Trust. The Trust is a commodity pool, as defined in the Commodity Exchange Act and the applicable regulations of the Commodity Futures Trading Commission, and is operated by its Sponsor, iShares® Delaware Trust Sponsor LLC, a commodity pool operator registered under the Commodity Exchange Act. The Trust is not an investment company registered under the Investment Company Act.

Investing in the Shares involves significant risk. See “Risk Factors” starting on page 15.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the securities offered in this prospectus, or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

THE COMMODITY FUTURES TRADING COMMISSION HAS NOT PASSED UPON THE MERITS OF PARTICIPATING IN THIS POOL NOR HAS THE COMMISSION PASSED ON THE ADEQUACY OR ACCURACY OF THIS DISCLOSURE DOCUMENT.

The Shares are not deposits or other obligations of BlackRock Institutional Trust Company, N.A. or any of their subsidiaries or affiliates or any other bank, are not guaranteed by BlackRock Institutional Trust Company, N.A. or any of their subsidiaries or affiliates or any other bank and are not insured by the Federal Deposit Insurance Corporation or any other governmental agency. An investment in the Shares is speculative and involves a high degree of risk.

The Trust intends to offer Shares on a continuous basis. The Trust issues and redeems Shares only in one or more blocks of 100,000 Shares called Baskets. These transactions take place only with certain broker-dealers with whom the Trust has entered into written arrangements regarding the issuance and redemption of Shares (we refer to these broker-dealers as Authorized Participants), in each case in exchange for a consideration per Share equal to the net asset value per Share announced by the Trust on the first Business Day (as defined herein) after the purchase or redemption order is received by the Trust. See “Business of the Trust—Computation of the Trust’s Net Asset Value.” Only institutions that enter into an agreement with the Trust to become Authorized Participants may purchase or redeem Baskets.

On January 31, 2013, the Shares closed on NYSE Arca at $50.93.

The Authorized Participants may offer to the public, from time to time, Shares from any Baskets they purchase from the Trust. Shares offered to the public by the Authorized Participants may be offered at a per-Share offering price that varies depending on, among other factors, the trading price of the Shares on NYSE Arca, the net asset value per Share and the supply of and demand for the Shares at the time of the offer. Shares initially comprising the same Basket but offered to the public at different times may have different offering prices. The Authorized Participants will not receive from the Trust, the Sponsor or any of their affiliates, any fee or other compensation in connection with their sale of Shares to the public; however, Authorized Participants may receive commissions or fees from investors who purchase Shares through their commission- or fee-based brokerage accounts.

The date of this prospectus is February 1, 2013.

Table of Contents

COMMODITY FUTURES TRADING COMMISSION

RISK DISCLOSURE STATEMENT

YOU SHOULD CAREFULLY CONSIDER WHETHER YOUR FINANCIAL CONDITION PERMITS YOU TO PARTICIPATE IN A COMMODITY POOL. IN SO DOING, YOU SHOULD BE AWARE THAT COMMODITY INTEREST TRADING CAN QUICKLY LEAD TO LARGE LOSSES, AS WELL AS GAINS. SUCH TRADING LOSSES CAN SHARPLY REDUCE THE NET ASSET VALUE OF THE POOL AND CONSEQUENTLY THE VALUE OF YOUR INTEREST IN THE POOL. IN ADDITION, RESTRICTIONS ON REDEMPTIONS MAY AFFECT YOUR ABILITY TO WITHDRAW YOUR PARTICIPATION IN THE POOL.

FURTHER, COMMODITY POOLS MAY BE SUBJECT TO SUBSTANTIAL CHARGES FOR MANAGEMENT, AND ADVISORY AND BROKERAGE FEES. IT MAY BE NECESSARY FOR THOSE POOLS THAT ARE SUBJECT TO THESE CHARGES TO MAKE SUBSTANTIAL TRADING PROFITS TO AVOID DEPLETION OR EXHAUSTION OF THEIR ASSETS. THIS DISCLOSURE DOCUMENT CONTAINS A COMPLETE DESCRIPTION OF EACH EXPENSE TO BE CHARGED THIS POOL AT PAGES 14 AND 45 AND A STATEMENT OF THE PERCENTAGE RETURN NECESSARY TO BREAK EVEN, THAT IS, TO RECOVER THE AMOUNT OF YOUR INITIAL INVESTMENT, AT PAGE 14.

THIS BRIEF STATEMENT CANNOT DISCLOSE ALL THE RISKS AND OTHER FACTORS NECESSARY TO EVALUATE YOUR PARTICIPATION IN THIS COMMODITY POOL. THEREFORE, BEFORE YOU DECIDE TO PARTICIPATE IN THIS COMMODITY POOL, YOU SHOULD CAREFULLY STUDY THIS DISCLOSURE DOCUMENT, INCLUDING A DESCRIPTION OF THE PRINCIPAL RISK FACTORS OF THIS INVESTMENT, AT PAGE 15.

YOU SHOULD ALSO BE AWARE THAT THIS COMMODITY POOL MAY TRADE FOREIGN FUTURES OR OPTIONS CONTRACTS. TRANSACTIONS ON MARKETS LOCATED OUTSIDE THE UNITED STATES, INCLUDING MARKETS FORMALLY LINKED TO A UNITED STATES MARKET, MAY BE SUBJECT TO REGULATIONS WHICH OFFER DIFFERENT OR DIMINISHED PROTECTION TO THE POOL AND ITS PARTICIPANTS. FURTHER, UNITED STATES REGULATORY AUTHORITIES MAY BE UNABLE TO COMPEL THE ENFORCEMENT OF THE RULES OF REGULATORY AUTHORITIES OR MARKETS IN NON-UNITED STATES JURISDICTIONS WHERE TRANSACTIONS FOR THE POOL MAY BE EFFECTED.

YOU SHOULD ALSO BE AWARE THAT THIS COMMODITY POOL MAY ENGAGE IN OFF-EXCHANGE FOREIGN CURRENCY TRADING. SUCH TRADING IS NOT CONDUCTED IN THE INTERBANK MARKET. THE FUNDS THAT THE POOL USES FOR OFF-EXCHANGE FOREIGN CURRENCY TRADING WILL NOT RECEIVE THE SAME PROTECTIONS AS FUNDS USED TO MARGIN OR GUARANTEE EXCHANGE-TRADED FUTURES AND OPTION CONTRACTS. IF THE POOL DEPOSITS SUCH FUNDS WITH A COUNTERPARTY AND THAT COUNTERPARTY BECOMES INSOLVENT, THE POOL’S CLAIM FOR AMOUNTS DEPOSITED OR PROFITS EARNED ON TRANSACTIONS WITH THE COUNTERPARTY MAY NOT BE TREATED AS A COMMODITY CUSTOMER CLAIM FOR PURPOSES OF SUBCHAPTER IV OF CHAPTER 7 OF THE BANKRUPTCY CODE AND THE REGULATIONS THEREUNDER. THE POOL MAY BE A GENERAL CREDITOR AND ITS CLAIM MAY BE PAID, ALONG WITH THE CLAIMS OF OTHER GENERAL CREDITORS, FROM ANY MONIES STILL AVAILABLE AFTER PRIORITY CLAIMS ARE PAID. EVEN POOL FUNDS THAT THE COUNTERPARTY KEEPS SEPARATE FROM ITS OWN FUNDS MAY NOT BE SAFE FROM THE CLAIMS OF PRIORITY AND OTHER GENERAL CREDITORS.

iSHARES® DIVERSIFIED ALTERNATIVES TRUST IS NOT A MUTUAL FUND OR ANY OTHER TYPE OF INVESTMENT COMPANY WITHIN THE MEANING OF THE INVESTMENT COMPANY ACT OF 1940, AS AMENDED, AND IS NOT SUBJECT TO REGULATION THEREUNDER.

i

Table of Contents

AUTHORIZED PARTICIPANTS MAY BE REQUIRED TO DELIVER A PROSPECTUS WHEN SELLING TO THE PUBLIC SHARES PURCHASED FROM THE TRUST. SEE “PLAN OF DISTRIBUTION.”

THE TRUST MAY CONSTITUTE A COLLECTIVE INVESTMENT SCHEME AS DEFINED IN THE FINANCIAL SERVICES AND MARKETS ACT 2000 (THE “FSMA”). THE TRUST IS NOT AUTHORIZED OR OTHERWISE RECOGNIZED IN THE UNITED KINGDOM AND THEREFORE WOULD BE CHARACTERIZED AS AN UNREGULATED COLLECTIVE INVESTMENT SCHEME FOR THE PURPOSES OF THE FSMA. AS SUCH, THE ISSUE AND DISTRIBUTION OF THIS PROSPECTUS IN THE UNITED KINGDOM IS RESTRICTED BY LAW. IN ADDITION, THIS PROSPECTUS HAS NOT BEEN APPROVED BY A PERSON AUTHORIZED TO CARRY ON INVESTMENT BUSINESS IN THE UNITED KINGDOM (AN “AUTHORIZED PERSON”) FOR THE PURPOSES OF SECTION 21(2)(B) OF THE FSMA. ACCORDINGLY, THIS PROSPECTUS CAN ONLY BE ISSUED OR DISTRIBUTED IN THE UNITED KINGDOM: (1) BY AN AUTHORIZED PERSON IN CIRCUMSTANCES PERMITTED BY SECTION 235 OF THE FSMA AND RULES MADE THEREUNDER AND THE PROVISIONS OF THE FSMA (FINANCIAL PROMOTION OF COLLECTIVE INVESTMENT SCHEMES) (EXEMPTIONS) ORDER 2001 (AS AMENDED), OR BY A PERSON WHO IS NOT AN AUTHORIZED PERSON, IN CIRCUMSTANCES PERMITTED BY THE FSMA (FINANCIAL PROMOTION) ORDER 2005 (AS AMENDED); AND (2) IN CIRCUMSTANCES WHERE THE ISSUANCE OR DISTRIBUTION OF THIS PROSPECTUS WOULD NOT CONSTITUTE OR OTHERWISE RESULT IN AN OFFER OF TRANSFERABLE SECURITIES TO THE PUBLIC IN THE UNITED KINGDOM WITHIN THE MEANING OF PART VI OF THE FSMA. ANY OTHER DISTRIBUTION OF THIS PROSPECTUS IN OR INTO THE UNITED KINGDOM IS UNAUTHORIZED. ANY PERSON ISSUING OR DISTRIBUTING THIS PROSPECTUS OR ANY PART OF IT MAY BE ACTING IN BREACH OF APPLICABLE LAW OR REGULATIONS AND ANY PERSONS RECEIVING THIS PROSPECTUS IN OR FROM THE UNITED KINGDOM IN CIRCUMSTANCES NOT FALLING WITHIN (1) OR (2) ABOVE MAY NOT RELY ON ITS CONTENTS. NO PART OF THIS PROSPECTUS SHOULD THEREFORE BE PUBLISHED, DISTRIBUTED OR OTHERWISE MADE AVAILABLE WITH UNRESTRICTED ACCESS IN ANY FORM IN THE UNITED KINGDOM.

THE TRUST HAS NOT BEEN APPROVED BY THE SWISS FINANCIAL MARKET SUPERVISORY AUTHORITY (THE “FINMA”) AS A FOREIGN COLLECTIVE INVESTMENT SCHEME PURSUANT TO ARTICLE 120 OF THE SWISS COLLECTIVE INVESTMENT SCHEME ACT OF JUNE 23, 2006 (THE “CISA”). ACCORDINGLY, THE SHARES MAY NOT BE PUBLICLY OFFERED IN OR FROM SWITZERLAND AND NEITHER THIS PROSPECTUS NOR ANY OTHER OFFERING MATERIALS RELATING TO THE TRUST AND/OR THE SHARES MAY BE MADE AVAILABLE THROUGH A PUBLIC OFFERING IN OR FROM SWITZERLAND. THE SHARES MAY ONLY BE OFFERED AND THIS PROSPECTUS MAY ONLY BE DISTRIBUTED IN OR FROM SWITZERLAND TO QUALIFIED INVESTORS (AS DEFINED IN THE CISA AND ITS IMPLEMENTING REGULATIONS).

OTHER INFORMATION

“iShares” is a registered trademark of BlackRock Fund Advisors or its affiliates.

ii

Table of Contents

| Page | ||||

| 1 | ||||

| 15 | ||||

| 38 | ||||

| 38 | ||||

| 39 | ||||

| 47 | ||||

| 48 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

51 | |||

| 64 | ||||

| THE SECURITIES DEPOSITORY; BOOK-ENTRY-ONLY SYSTEM; GLOBAL SECURITY |

70 | |||

| 71 | ||||

| 75 | ||||

| 75 | ||||

| 75 | ||||

| 78 | ||||

| 81 | ||||

| 82 | ||||

| 86 | ||||

| 89 | ||||

| 102 | ||||

| 103 | ||||

| 111 | ||||

| 111 | ||||

| 111 | ||||

| F-1 | ||||

You should rely only on the information contained in this prospectus. None of the Sponsor, the Trustee, the Delaware Trustee or the Trust has authorized any other person to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. None of the Sponsor, the Trustee, the Delaware Trustee or the Trust is making an offer to sell the Shares in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus is accurate only as of the date on the front cover of this prospectus.

Certain defined terms used in this prospectus are set forth in the “Glossary” in the Statement of Additional Information attached hereto.

iii

Table of Contents

This summary highlights some of the information contained in this prospectus. This summary does not contain all of the information you should consider before investing in the Shares. You should carefully read this entire prospectus, including “Risk Factors” beginning on page 15, before making a decision to invest in the Shares. Capitalized terms not defined in this section have the meaning set forth in the Glossary beginning on page 2-4 of Part 2 of this prospectus.

Structure of the Trust

The iShares® Diversified Alternatives Trust, or the Trust, is a Delaware statutory trust. The Trust intends to continuously issue and redeem Shares in transactions with Authorized Participants. Each Share represents a unit of fractional undivided beneficial interest in the net assets of the Trust. The assets of the Trust, called the Portfolio, consist of cash and financial instruments that are used, as needed, to secure the Trust’s trading obligations in respect of foreign-currency forward contracts and exchange-traded futures contracts selected by BlackRock Fund Advisors, the Trust’s Advisor, following investment strategies that utilize quantitative methodologies to identify potentially profitable discrepancies in the relative values or market prices of one or more assets and seek to control the risks and volatility inherent in these investments by taking long and short positions in historically correlated assets. See “—Investment Objective; Strategies.” The term of the Trust is perpetual, unless it is dissolved under the circumstances described under “Description of the Shares and the Trust Agreement—Amendment and Dissolution.” The principal offices of the Trust are located at 400 Howard Street, San Francisco, CA 94105, and the Trust’s telephone number is (415) 670-2000.

The Trust is a commodity pool as defined in the Commodity Exchange Act (the “CEA”) and the regulations of the Commodity Futures Trading Commission (the “CFTC”). The Trust is operated by its Sponsor, iShares® Delaware Trust Sponsor LLC, a limited liability company registered under the CEA as a commodity pool operator. The sole member and manager of the Sponsor is BlackRock Asset Management International Inc., a Delaware corporation. BlackRock Institutional Trust Company, N.A. is the Trustee of the Trust. The Advisor, BlackRock Fund Advisors, is the commodity trading advisor of the Trust and is registered under the CEA. The Trust is not an investment company registered under the Investment Company Act and is not required to register under that Act.

The material terms of the agreement governing the Trust are discussed in greater detail under “Description of the Shares and the Trust Agreement.”

Breakeven Point Per Unit of Initial Investment

The estimated amount of all fees and expenses which are anticipated to be incurred by a new investor during the first twelve months is 1.07% of the per Share price of $50.83 as of December 31, 2012 (or expressed as a dollar amount, $0.54 of the price of $50.83 per Share). Based on certain interest rate, expense and other assumptions, the estimated twelve-month breakeven point is 0.96% of the $50.83 per Share price as of December 31, 2012 (or expressed as a dollar amount, $0.48 of the price of $50.83 per Share). See “Breakeven Analysis”.

Creations and Redemptions

The Trust issues Shares only in one or more blocks of 100,000 Shares (each, a “Basket”) in exchange for cash in an amount equal to the Basket Amount announced by the Trust on the first Business Day after the purchase order is received by the Trust. The Trust redeems Shares only in Baskets in exchange for cash in an amount equal to the Basket Amount announced by the Trust on the first Business Day after the redemption order is received by the Trust. The Trust does not redeem individual Shares or Baskets held by

1

Table of Contents

parties who are not Authorized Participants. See “Risk Factors—Risk Relating to the Trust and Investment in the Shares—Creation and redemption of Baskets may be delayed when one or more of the exchanges where the Trust may need to trade, either to establish new positions or to liquidate existing ones, are scheduled to be closed, and may be subject to postponement, suspension or rejection under certain circumstances, all of which may reduce the liquidity of the Shares.”

The Sponsor

The Sponsor is iShares® Delaware Trust Sponsor LLC, a Delaware limited liability company. The Sponsor’s primary business function in connection with the Trust is to direct the actions of the Trustee in the management of the Trust and to act as commodity pool operator of the Trust.

The Sponsor has been registered under the CEA as a commodity pool operator and has been a member of the National Futures Association (the “NFA”) since June 2009.

The Sponsor arranged for the creation of the Trust, the registration of the Shares for their public offering and the listing of the Shares on NYSE Arca. The Sponsor is obligated under the Trust Agreement to pay the following administrative, operational and marketing expenses: (1) the fees of the Trustee, the Advisor, the Delaware Trustee, the Trust Administrator and the Processing Agent, (2) NYSE Arca listing fees, (3) printing and mailing costs, (4) audit fees, (5) fees for registration of the Shares with the SEC, (6) tax reporting costs and (7) legal expenses up to $100,000 annually. In recognition of its paying these expenses, the Sponsor is entitled to an allocation that accrues daily at an annualized rate equal to 0.95% of the Adjusted Net Asset Value of the Trust and is payable by the Trust monthly in arrears. That allocation to the Sponsor is referred to in this prospectus as the “Sponsor’s Fee.” For a description of how the net asset value of the Trust is calculated, see “Business of the Trust—Computation of the Trust’s Net Asset Value.”

The Sponsor may remove the Trustee and appoint a successor Trustee if the Trustee ceases to meet certain objective requirements, or if, having received written notice of a material breach of its obligations under the Trust Agreement, the Trustee has not cured the breach within 30 days. The Sponsor may also replace the Trustee during the 90 days following any merger, consolidation or conversion in which the Trustee is not the surviving entity or, in its discretion, at any time following the first anniversary of the creation of the Trust.

The principal office of the Sponsor is located at 400 Howard Street, San Francisco, CA 94105, and its telephone number is (415) 670-2000.

The Advisor

The Advisor is BlackRock Fund Advisors, a California corporation. The Advisor is the commodity trading advisor for the Trust and has discretionary authority to make all determinations with respect to the Portfolio, subject to specified limitations. The Advisor has been registered as a commodity trading advisor under the CEA since April 5, 1993 and is a member of the NFA.

The Advisor and the Trust may each terminate the Advisory Agreement at any time upon 30 days’ prior written notice.

The Trustee

The Trustee of the Trust is BlackRock Institutional Trust Company, N.A., a national banking association affiliated with the Sponsor. The Shares are not deposits or other obligations of BlackRock Institutional Trust

2

Table of Contents

Company, N.A. or any of its subsidiaries or affiliates or any other bank, are not guaranteed by BlackRock Institutional Trust Company, N.A. or any of its subsidiaries or affiliates or any other bank and are not insured by the Federal Deposit Insurance Corporation or any other governmental agency. An investment in the Shares is speculative and involves a high degree of risk.

The Delaware Trustee

Wilmington Trust Company, a Delaware corporation with trust powers, is the Delaware Trustee of the Trust. The Delaware Trustee is not entitled to exercise any of the powers, and does not have any of the duties or responsibilities, of the Trustee. The Delaware Trustee is a trustee of the Trust for the sole and limited purpose of fulfilling the requirements of the Delaware Statutory Trust Act.

The Trust Administrator and Certain Agents of the Trust

The Trust has delegated the processing of creation and redemption orders of Baskets to SEI Investments Distribution Co. (the “Processing Agent”). The Trust has also delegated the valuation of certain assets of the Trust for purposes of the daily calculation of the net asset value of the Trust and certain other administrative responsibilities to State Street Bank and Trust Company (the “Trust Administrator”). Neither the Processing Agent nor the Trust Administrator is affiliated with the Sponsor or the Trustee. The Trust has also retained PricewaterhouseCoopers LLP (the “Tax Administrator”) to provide tax accounting and tax reporting services for the Trust. The Trust may terminate the Processing Agent, the Trust Administrator or the Tax Administrator at any time or appoint different agents to act on its behalf.

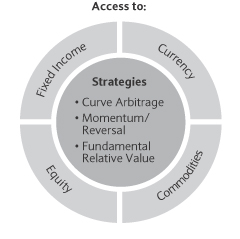

Investment Objective; Strategies

The investment objective of the Trust is to maximize absolute returns from a portfolio of foreign currency forward contracts and exchange-traded futures contracts that may involve commodities, currencies, interest rates and certain eligible stock or bond indices while seeking to control the risks and volatility inherent in those investments by taking long and short positions in historically correlated assets. The Trust also expects to earn interest on the assets used to collateralize its trading positions. The return on assets in the Portfolio, if any, is not intended to track the performance of any index or other benchmark. There is no assurance that the Trust will achieve its investment objectives.

Since the inception of the Trust, the Advisor set a range between 6% and 8% as its target for the annualized portfolio return volatility of the Trust. Seeking to improve Trust returns, shortly after the effectiveness of the registration statement that includes this prospectus the Advisor will increase the maximum portfolio return volatility to 10% per annum. This increase in volatility may result in higher losses.

Forward Contracts

A forward contract is an agreement between two parties, one of which undertakes to purchase from or sell to the other, on a specified future date, a specified quantity of a specified asset at a specified location in exchange for a specified purchase price. At the discretion of the Advisor, the Trust may enter into foreign currency forward contracts. See “Business of the Trust—Investment Objective; Strategies—Forward Contracts.”

Futures Contracts

Futures contracts are standardized forward contracts traded on an exchange. At the discretion of the Advisor, the Trust may engage in trading activities with respect to futures contracts that may involve commodities, currencies, interest rates and certain eligible stock or bond indices, as described elsewhere in this prospectus. See “Business of the Trust—Investment Objective; Strategies—Futures Contracts.”

Interest

Futures contracts are customarily bought and sold on margins that represent a very small percentage (ranging upward from less than 2% to 5%) of the purchase price of the asset underlying the futures contract

3

Table of Contents

being traded. Similarly the Trust may, from time to time, be required to satisfy collateral requirements set forth by its over-the-counter counterparties with respect to the Trust’s forward contracts trading obligations. Any interest paid on the Trust’s cash positions, together with any interest paid on collateral deposited as margin, net of expenses, is generally reinvested.

Strategies

The Advisor is the commodity trading advisor for the Trust. The Advisor invests cash proceeds from the sales of Baskets in short term United States government securities and other financial instruments that, in compliance with the rules of the futures exchanges and other markets where the Advisor trades on behalf of the Trust, are eligible to secure the Trust’s trading obligations in respect of a portfolio of foreign-currency forward contracts and exchange-traded futures contracts selected by the Advisor following strategies that utilize quantitative methodologies to identify potentially profitable discrepancies in the relative values or market prices of one or more assets and seek to control the risks and volatility of these investments by taking long and short positions in historically correlated assets. These strategies may include:

| • | Yield and Futures Curve Arbitrage Strategies which seek to take advantage of interest rate and futures contract price differentials by simultaneously entering into long and short positions in various bond futures contracts, interest rates futures contracts, commodity futures contracts and/or currency forward contracts that the Advisor determines to be mispriced relative to one another. The Advisor may enter into long positions in contracts whose underlying assets are deemed relatively inexpensive and may enter into short positions on contracts whose underlying assets are deemed relatively expensive. |

| • | Technical Strategies which, in general, seek to take advantage of a comparison between assets’ historical returns and their recent performance. Technical strategies are based on the theory that past price history may be predictive of asset value, and so technical strategies may be used to capture returns arising from price changes over time. For example, if recent performance of an asset exceeds historical performance, then a long “momentum” trade opportunity to buy may arise. If the historical performance of an asset exceeds recent performance, then a short “reversal” trade opportunity may arise. All technical strategies are quantitative in nature and financial modeling is used for determining long and/or short positions in various asset types. |

| • | Fundamental Relative Value Strategies which seek returns by attempting to identify instances where there are discrepancies between the market and fundamental values of an asset and trading long or short positions in that asset. |

See “Business of the Trust—Investment Objective; Strategies—Investment Strategies” and “—Portfolio Construction.”

Characteristics of an Investment in the Shares

The Shares are intended to constitute a relatively cost-effective means of achieving investment exposure to non-traditional asset classes. An investment in Shares is:

| • | Listed. Although there can be no assurance that an actively traded market in the Shares will exist at the time you wish to sell its Shares, the Shares are listed for trading on NYSE Arca under the symbol “ALT.” |

| • | Relatively cost efficient. Transactions in the asset classes that the Advisor, on behalf of the Trust, invests or trades in entail certain expenses. Nonetheless, because the expenses involved in the Portfolio are dispersed among all Shareholders, an investment in the Shares may represent a |

4

Table of Contents

| cost-efficient alternative to investment positions in the same asset classes for investors not otherwise in a position to participate directly in the markets for physical commodities, foreign currencies, interest rates, or futures, forwards or other over-the-counter derivative contracts involving those assets. See “Business of the Trust—Investment Objective; Strategies.” |

The Shares are eligible for margin accounts.

Risk Factors

An investment in the Shares is speculative and involves, among others, the following risks:

Risks Relating to Regulatory Requirements

| • | Changes to the regulatory regime applicable to futures contracts may have an adverse effect on the ability of the Trust to pursue its strategies and, therefore, result in a decreasing value of the Shares. |

| • | Regulatory and exchange position limits may restrict the creation of Baskets and the operation of the Trust. |

| • | Changes in the margin requirements set by the relevant futures exchanges and over-the-counter market participants may limit the Trust’s ability to meet its investment objectives. |

Risks Relating to Commodities Markets

| • | The price of the Shares fluctuates as a result of fluctuations in the prices of any commodities underlying the futures contracts owned by the Trust. Commodity prices may be volatile, thereby creating the potential for losses regardless of the length of time you intend to hold your Shares. |

| • | Historical performance of specific commodities or commodity indices is no guide to their future performance or to the performance of the Shares. |

| • | Commodity futures trading may be illiquid. In addition, suspensions or disruptions of market trading in the commodities markets and related derivatives markets may adversely affect the value of your Shares. |

5

Table of Contents

| • | During a period when commodity prices are fairly stationary, “backwardation” (a situation where the prices of futures contracts are higher for contracts with shorter-term expirations than for contracts with longer-term expirations) or “contango” (a situation where the prices of futures contracts with longer-term expirations are higher than the prices of futures contracts with shorter-term expirations) in the prices of the commodity-linked futures contracts held by the Trust may cause the price of your Shares to decrease. |

Risks Relating to Currency Markets

| • | As a multinational currency, the euro may experience greater price volatility due to the influence of multiple and uncoordinated political and fiscal regimes. |

| • | A country’s decision to abandon the euro zone could have adverse consequences for the value of the Shares. |

| • | The price of the Shares fluctuates as a result of fluctuations in the exchange rates of currencies underlying any currency-linked futures or forward contracts owned by the Trust. Exchange rates may be volatile, thereby creating the potential for losses regardless of the length of time you intend to hold your Shares. |

| • | Substantial transactions in a currency by any official sector market participant (such as central banks, other governmental agencies and/or other multi-lateral institutions that buy, sell or hold currencies) could adversely affect an investment in the Shares. |

| • | A country’s decision to abandon its current currency and adopt a new one could have adverse consequences for the value of any positions related to the old currency that the Trust may hold at the time. |

Risks Relating to U.S. Government and Sovereign Debt Markets

| • | Investing in debt obligations of the U.S. government creates exposure to credit and interest rate risk. |

| • | Investing in futures and/or forward contracts linked to sovereign debt instruments creates exposure to the direct or indirect consequences of political, social or economic changes in the countries in which the issuers are located and the creditworthiness of the sovereign. |

| • | Investing in futures and/or forward contracts linked to non-U.S. sovereign debt instruments creates exposure to the non-U.S. interest rate fluctuations. |

Risks Relating to Interest Rate Derivatives Markets

| • | Investing in interest rate futures contracts creates exposure to interest rate fluctuations in one country as well as relative interest rate movements between countries. |

Risks Relating to Security Index Futures Markets

| • | Investing in security index futures contracts creates exposure to the performance of the underlying index. |

Risks Relating to Derivative Contracts

| • | The Trust’s use of leverage and/or short positions involves certain risks, including potentially high volatility and magnified losses in the underlying assets, and should be considered to be speculative. |

6

Table of Contents

| • | The Trust is subject to credit risks and other risks associated with U.S. exchange-traded futures contracts. |

| • | Trading on futures exchanges outside the United States is not subject to U.S. regulation. |

| • | When entering into foreign currency forward contracts, the Trust assumes the risk that its counterparties may become unable or unwilling to pay any amounts owed to the Trust. |

| • | The Advisor, on behalf of the Trust, trades in forward contracts that are not traded on regulated exchanges and, therefore, offer different or lower levels of protections to investors. |

| • | Failure of the Clearing FCM to segregate assets or the insolvency of the Trust’s prime broker may increase losses. |

Risks Relating to the Advisor and its Trading Strategies

| • | The lack of experience of the Advisor and its principals in actively managing an entity like the Trust and applying quantitative investment strategies similar to those that are used in the selection of investments for the Trust may result in substantial trading losses for the Trust and, as a result, you could lose some or all of the value of your Shares. |

| • | The Advisor makes decisions regarding investments for the Trust relying on quantitative models that may be defective or not adequate to analyze market conditions at the time the investment decisions are made; as a result, the returns expected from those investments may not materialize. |

| • | The strategies used by the Advisor to identify investment opportunities for the Trust may fail to deliver the desired returns. |

| • | Relative value strategies used by the Advisor to identify investment opportunities for the Trust are subject to certain risks. |

| • | Various actual and potential conflicts of interest involving the Advisor may be detrimental to Shareholders. |

Risks Relating to the Trust and Investment in the Shares

| • | The Trust is subject to the risks associated with being a new type of investment vehicle. |

| • | The lack of an active trading market for the Shares may result in losses on your investment at the time of disposition of your Shares. |

| • | The Shares of the Trust are new securities products and their value could decrease if unanticipated operational or trading problems arise. |

| • | You may not rely on past performance in deciding whether to buy the Shares. |

| • | The Trust is subject to the costs and risks associated with being actively managed. These costs and risks may cause your investment in the Shares to result in losses that you might have avoided if you had invested in products not exposed to those costs and risks. |

| • | The price you receive upon the sale of your Shares may be less than their NAV. |

| • | The NAV may not always correspond to the market price of the Shares and, as a result, Baskets may be created or redeemed at a value that differs from the market price of the Shares. |

| • | None of the Sponsor, the Advisor or the Trustee can assure you that it will continue in its respective role. If any of them was no longer to act in those roles, the Trust and the value of the Shares may suffer. |

7

Table of Contents

| • | The Trust may incur additional transactional costs because the Portfolio is actively managed, and actively managed portfolios may have higher turnover rates. |

| • | Fees and expenses payable by the Trust are charged regardless of profitability and may result in a depletion of its assets. |

| • | It is not expected that the Trust will make any periodic distributions or dividend payments to Shareholders. |

| • | The Trust could be liquidated at a time when the disposition of its interests will result in losses to investors in the Shares. |

| • | The Sponsor has broad discretion to liquidate the Trust at any time. |

| • | The Shares may not provide anticipated benefits of diversification from other asset classes. |

| • | The liquidity of the Shares may be affected by the withdrawal from participation of Authorized Participants or by the suspension of issuance, transfers or redemptions of Shares by the Trust. |

| • | Creation and redemption of Baskets may be delayed when one or more of the exchanges where the Trust may need to trade, either to establish new positions or to liquidate existing ones, are scheduled to be closed, and may be subject to postponement, suspension or rejection under certain circumstances, all of which may reduce the liquidity of the Shares. |

| • | Competition from other commodities- and currencies-related investments could limit the market for, and reduce the liquidity of, the Shares. |

| • | As a Shareholder, you will not have the rights normally associated with ownership of common shares. |

| • | As a Shareholder, you will not have the protections normally associated with the ownership of shares in an investment company registered under the Investment Company Act. |

| • | Competing claims over ownership of relevant intellectual property rights could adversely affect the Trust or an investment in the Shares. |

| • | The value of the Shares will be adversely affected if the Trust is required to indemnify the Sponsor or the Advisor or if the Sponsor is required to indemnify the Trustee. |

| • | NYSE Arca may halt trading in the Shares, which would adversely impact your ability to sell your Shares. |

Risks Relating to Taxes

| • | The Trust’s classification as a publicly traded partnership not taxable as a corporation is not free from doubt, and if the Trust were to fail to qualify as a partnership for U.S. federal income tax purposes, the Trust’s income and items of deduction would not pass through to the Shareholders, the Trust would be required to pay tax at corporate rates on any portion of the Trust’s net income that does not constitute tax-exempt income, and distributions by the Trust to the Trust’s Shareholders would be taxable as dividends to the extent of the Trust’s earnings and profits. |

| • | Shareholders’ tax liability could exceed cash distributions on the Shares. |

| • | The IRS could adjust or reallocate items of income, gain, deduction, loss and credit with respect to the Shares if the IRS does not accept the assumptions or conventions utilized by the Trust. |

| • | Shareholders could become subject to U.S. withholding tax beginning in 2014. |

Conflicts of Interest

There may be conflicts of interest among the Shareholders and the Sponsor, the Trustee and the Advisor (or their affiliates). These conflicts may arise because of the affiliation between each of the

8

Table of Contents

Sponsor, the Advisor and the Trustee. Because of this affiliation, the Sponsor will have an incentive not to remove the Advisor or the Trustee. Conflicts may also result from the Sponsor’s authority to determine whether to make distributions to Shareholders. In addition, conflicts may arise in connection with trading activities for the proprietary accounts or customer accounts of the Sponsor, the Advisor or any of their affiliates or other accounts under management in regard to position limits, timing of the taking of positions or other similar conflicts. Conflicts may also arise in connection with research reports published by the Sponsor or its affiliates with respect to markets in which the Portfolio may participate. For more information regarding these potential conflicts of interest, see “Conflicts of Interest” beginning on page 82.

Certain U.S. Tax Consequences

The Trust has received an opinion of Clifford Chance US LLP to the effect that the Trust will not be treated as an association or a publicly traded partnership taxable as a corporation for U.S. federal income tax purposes. Accordingly, the Trust will not be a taxable entity for U.S. federal income tax purposes and will not incur U.S. federal income tax liability. Instead, you will be taxed as a beneficial owner of an interest in a partnership, which means that you generally will be required to take into account your allocable share of the Trust’s items of income, gain, loss, deduction, expense and credit in computing your U.S. federal income tax liability.

9

Table of Contents

The Offering

| Offering |

The Shares represent units of fractional undivided beneficial interests in the net assets of the Trust. |

| Use of Proceeds |

Proceeds received by the Trust from the issuance and sale of Baskets are invested by the Advisor in short-term United States government securities and other financial instruments that, in compliance with the rules of the futures exchanges and other markets where the Advisor trades on behalf of the Trust, are eligible to secure the Trust’s trading obligations in respect of a portfolio of foreign currency forward contracts and exchange-traded futures contracts that may involve commodities, currencies, interest rates and certain eligible stock or bond indices, selected by the Advisor. See “—Portfolio” below. |

| NYSE Arca Symbol |

ALT |

| CUSIP |

464294107 |

| Creation and Redemption |

The Trust intends to issue and redeem Baskets on a continuous basis. Baskets are issued and redeemed only in exchange for a consideration in cash equal to the Basket Amount announced by the Trust on the first Business Day after the purchase or redemption order is received by the Trust. Baskets may be created and redeemed only by Authorized Participants, who pay the Trustee a transaction fee of $800 per creation or redemption. See “—Net Asset Value” below and “Description of the Shares and the Trust Agreement—Creation of Baskets” and “—Redemption of Baskets.” |

| Authorized Participants |

Baskets may be created and redeemed only by Authorized Participants. Each Authorized Participant must (1) be a registered broker-dealer and, if required in connection with its activities, a registered futures commission merchant, (2) be a DTC Participant, and (3) have entered into an Authorized Participant Agreement with the Trust and the Sponsor. |

| Suspension of Issuance, Transfers and Redemptions |

The Trust may suspend the issuance of Baskets, registration of transfers of Shares and redemption of Baskets generally, or may refuse a particular purchase order, transfer or redemption order at any time, if the Trustee or the Sponsor determines that it is advisable to do so for any reason. See “Description of the Shares and the Trust Agreement—Requirements for Trustee Actions.” |

| Portfolio |

The Advisor selects for the Portfolio foreign currency forward contracts and exchange-traded futures contracts that may involve commodities, currencies, interest rates and certain eligible stock or bond indices with a view towards maximizing absolute returns |

10

Table of Contents

| while seeking to control the volatility inherent in these types of investments. While the Advisor may select investments for the Portfolio following a variety of strategies that utilize quantitative methodologies to identify potentially profitable discrepancies in the relative values or market prices of one or more assets, there are no mandatory holdings allocation requirements. Accordingly, at any given time, the Trust may be disproportionately exposed to one or more asset classes or contract counterparties, including over-the-counter counterparties and clearing organizations. See “Business of the Trust—Investment Objective; Strategies.” |

| The return on assets in the Portfolio, if any, is not intended to track the performance of any index or other benchmark. |

| While the Advisor has the authority to trade on behalf of the Trust at any time in its discretion, it is generally expected that such discretionary trading will not occur more than once a week. The Trust, however, may need to trade more frequently in order to invest proceeds from the issuance of Baskets of Shares or raise funds to honor redemption requests. The Trust will post the composition of the Portfolio daily on its website at www.ishares.com. |

| Margin Assets |

The Trust deposits, from time to time, with the Clearing FCM or other licensed financial or commodities market participant any required margin in the form of cash or other eligible assets (depending on the nature of the position being secured, customary practices in the relevant market and any applicable regulatory or counterparty requirements). Any interest paid on this collateral is part of the return on the Portfolio. |

| Net Asset Value |

On each Business Day, as soon as practicable after the close of regular trading of the Shares on NYSE Arca (normally 4:00 P.M., New York City time), the Trustee must determine the net asset value of the Trust, the net asset value per Share (the “NAV”) and the Basket Amount as of that date. |

| On each day on which the Trustee must determine the net asset value of the Trust, the NAV and the Basket Amount, the Trust Administrator values all futures and forward trading positions and other non-cash assets in the Portfolio and communicates that valuation to the Trustee for use by the Trustee in the determination of the Trust’s net asset value. The Trustee subtracts the Trust’s accrued fees (other than fees computed by reference to the value of the Trust or its assets), expenses and other liabilities on that day from the value of the Trust’s assets as of the close of trading on that day. The result is the Trust’s “Adjusted Net Asset Value.” Fees computed by reference to the value of the Trust or its assets (including the Sponsor’s Fee) are calculated on the Adjusted Net Asset Value. The Trustee subtracts |

11

Table of Contents

| the fees so calculated from the Adjusted Net Asset Value of the Trust to determine the Trust’s net asset value. |

| The Trustee determines the NAV by dividing the net asset value of the Trust on a given day by the number of Shares outstanding at the time the calculation is made. The Trustee then determines the Basket Amount corresponding to that date by multiplying the NAV by the number of Shares in a Basket (i.e., 100,000). |

| The NAV for each Business Day is expected to be distributed through major market data vendors and published online at www.ishares.com, or any successor thereto. It is expected that the Trust will update the NAV as soon as practicable after each subsequent NAV is calculated. See “Business of the Trust—Computation of the Trust’s Net Asset Value.” |

| You should note that while the NAV is updated on each Business Day, the NAV is calculated by reference to assets that trade on futures exchanges or other markets, including in non-U.S. jurisdictions. Accordingly, the NAV may not always reflect the same-day valuation of assets that trade on markets in non-U.S. jurisdictions if one or more of those jurisdictions are not open for business on any given Business Day. |

| Voting Rights |

Except in limited circumstances, owners of Shares have no voting rights. See “Description of the Shares and the Trust Agreement—Voting Rights.” |

| Distributions |

The Trust is not expected to make any distributions or pay any dividends to its Shareholders except (1) in connection with redemptions of Baskets, (2) as determined by the Sponsor in its absolute discretion, and (3) in connection with the liquidation of the Trust. |

| Limitation of Liabilities |

You cannot lose more than your investment in the Shares. Under Delaware law, Shareholders’ liability is limited to the same extent as the liability of stockholders of a for profit Delaware business corporation. |

| Dissolution Events |

The Trustee will dissolve the Trust if: |

| • | the Trustee is notified that the Shares are delisted from NYSE Arca and are not approved for listing on another national securities exchange within five Business Days of their delisting; |

| • | registered holders of at least 75% of the outstanding Shares notify the Trustee that they elect to dissolve the Trust; |

| • | sixty days have elapsed since the Trustee notified the Sponsor of the Trustee’s election to resign, and a successor trustee has not been appointed and accepted its appointment; |

12

Table of Contents

| • | the SEC (or its staff) or a court of competent jurisdiction determines that the Trust is an investment company under the Investment Company Act, and the Trustee has actual knowledge of that determination; |

| • | the Sponsor notifies the Trustee in writing that it has determined, in its discretion, that the dissolution of the Trust is advisable. The Sponsor may, for example (but is not obligated to), decide to liquidate the Trust if, among other reasons, (1) legal, regulatory or market changes result, in the opinion of the Sponsor, in a decrease of investment opportunities available to the Trust in compliance with its investment objective and strategies, (2) it becomes impossible or impractical to compute the net asset value of the Trust or to assess the accuracy of such valuations; or (3) the value of the Portfolio is below a level such that continued operation of the Trust is not cost-efficient; |

| • | the Trust is treated as an association taxable as a corporation for U.S. federal income tax purposes, and the Trustee receives notice from the Sponsor that the Sponsor has determined that the dissolution of the Trust is advisable; or |

| • | DTC is unable or unwilling to continue to perform its functions, and a comparable replacement is unavailable. |

| After dissolution of the Trust, the Trustee will deliver cash to the Shareholders upon surrender and cancellation of the Shares and, 90 days after dissolution, may sell any remaining Trust property and hold any remaining cash, uninvested and in a non-interest bearing account, for the pro rata benefit of the Shareholders who have not surrendered their Shares for cancellation. See “Description of the Shares and the Trust Agreement—Amendment and Dissolution.” |

| Clearance and Settlement |

The Shares are issued only in book-entry form. Transactions in Shares clear through the facilities of DTC. Investors may hold their Shares through DTC, if they are DTC Participants, or indirectly through entities that are DTC Participants. |

13

Table of Contents

Breakeven Analysis

The following table indicates the approximate dollar returns and percentages required for the value of an initial $50.83 investment in a Share to equal the amount originally invested twelve months after issuance.

The table, as presented, is only an approximation. The capitalization of the Trust does not directly affect the level of the charges as a percentage of its net asset values, other than the Sponsor’s Fee and brokerage commissions.

| Expense(1) | $ | % | ||||||

| Transaction Fee(2) |

0.02 | 0.04 | ||||||

| Sponsor’s Fee(3) |

0.48 | 0.95 | ||||||

| Syndication and Filing Expenses(3) |

— | 0.00 | ||||||

| Trust Operating Expenses(3) |

— | 0.00 | ||||||

| Commodity Trading Advisor Fee(3) |

— | 0.00 | ||||||

| Brokerage Commissions and Fees(4) |

0.04 | 0.08 | ||||||

| Interest Income(5) |

(0.06 | ) | (0.11 | ) | ||||

|

|

|

|

|

|||||

| 12-Month Break Even(6) |

0.48 | 0.96 | ||||||

|

|

|

|

|

|||||

| (1) | The foregoing breakeven analysis assumes that the Shares have a constant month-end net asset value. Calculations are based on $50.83 as the net asset value per Share, which was the net asset value as of the close of business on December 31, 2012. |

| (2) | Per share amounts assume the creation or redemption of one Basket (since the $800 fee is per transaction, creation or redemption in more than one-Basket increments will result in a lower per-Share transaction fee). |

| (3) | From the Sponsor’s Fee, the Sponsor is responsible for the ordinary and recurring expenses of the Trust, including the SEC registration fees, Trust operating expenses and the commodity trading advisor fee. |

| (4) | Brokerage commissions and fees are an estimate based on historical commission and fee rates from January 2012 to December 2012. Annual brokerage commissions and fees are estimated to be $41,000, based on net assets of $51,000,000. The actual amount of brokerage commissions and fees to be incurred will vary based upon the trading frequency of the Trust. |

| (5) | Interest income is currently estimated to be earned at an annual rate of 0.11%, which is based on the six-month U.S. Treasury rate as of December 31, 2012. |

| (6) | You may pay customary brokerage commissions in connection with purchases of Shares. Because brokerage commission rates will vary from investor to investor, we have not included brokerage commissions in the breakeven table. Investors should review the terms of their brokerage accounts for details on applicable charges. |

Summary Financial Condition

As of the close of business on December 31, 2012, the net asset value of the Trust was $50,827,436, and the NAV was $50.83.

14

Table of Contents

Investing in the Shares is speculative and involves a high degree of risk. You could lose all or a substantial portion of your investment in the Shares. Before making an investment decision, you should carefully consider the risks described below, as well as the other information included in this prospectus.

Risks Relating to Regulatory Requirements

Changes to the regulatory regime applicable to futures contracts may have an adverse effect on the ability of the Trust to pursue its strategies and, therefore, result in a decreasing value of the Shares.

The U.S. futures markets are subject to comprehensive regulation, not only by the CFTC but also by self-regulatory organizations, including the NFA and the exchanges on which the futures contracts are traded. As with any regulated activity, changes in the regulations may have unexpected results. For example, changes in the amount or quality of the collateral that traders in futures contracts are required to provide to secure their open positions, or in the limits on the number or size of positions that a trader may have open at a given time, may adversely affect the ability of the Trust to enter into certain transactions that could otherwise present lucrative opportunities.

Bills containing proposed legislative changes are from time to time introduced to the U.S. Congress in response to actual or perceived market inefficiencies or other problems. These bills often target perceived excessive speculation in commodities and commodity indices, including by institutional “index funds,” on regulated futures markets and in the over-the-counter derivatives markets. These bills include a broad range of measures intended to limit speculation, including possible increases in the margin levels required for regulated futures contracts; imposing, or tightening existing speculative position limits applicable to regulated futures and over-the-counter derivatives positions; providing the CFTC authority to establish or modify certain speculative position limits; imposing aggregate speculative position limits across regulated U.S. futures, over-the-counter positions and certain futures contracts traded on non-U.S. exchanges; eliminating or narrowing existing exemptions from speculative position limits; restricting the access of certain classes of investors to futures markets and over-the-counter derivatives markets; and imposing additional reporting requirements on market participants, such as the Trust.

While it is impossible to predict which measures will be adopted or precisely how they will affect the value of your shares, any such measures could increase the costs of the Trust, result in significant direct limitations on the maximum permitted size of the Trust’s futures positions and therefore on the size of the Trust or the number or type of strategies available to the Trust; and could also affect liquidity in the market for the Shares and the correlation between the price of the Shares and the net asset value of the Trust.

Regulatory and exchange position limits may restrict the creation of Baskets and the operation of the Trust.

Prior to the adoption of the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”), which was signed into law on July 21, 2010, position limits with respect to most U.S. futures contracts have been set by U.S. commodities exchanges and boards of trade. The Dodd-Frank Act required the CFTC to establish federal position limits on futures and options contracts in physical commodities (including energy) and on economically equivalent over-the-counter derivatives. As mandated by the Dodd-Frank Act, in October 2011 the CFTC finalized regulations that imposed federal position limits with respect to 28 physical delivery commodity futures and options contracts traded across various exchanges as well as to swaps that are economically equivalent to such contracts and directed the U.S. commodities exchanges and boards of trade to adopt corresponding position limits in futures, options and swaps not to exceed the limits adopted by the CFTC. The final rule significantly limited the availability of the bona fide hedging exemption to hedging of physical commodity positions or transactions and did not extend to financial hedging or risk management.

In September 2012, a federal district court in Washington D.C. vacated the new CFTC position rules and in November 2012 the CFTC decided to file an appeal against the court’s decision. As of the date of this prospectus it is not clear if the 2011 rules will eventually become effective.

15

Table of Contents

In addition to the federal position limits established by the CFTC, many U.S. and foreign futures exchanges impose “speculative position limits” or “accountability levels” on the maximum net long or short futures positions that any person may hold or control in contracts traded on such exchanges. Under the exchange rules and CFTC regulations, all accounts owned or managed by commodity trading advisors, such as the Advisor, their principals and their affiliates would be combined for position limit purposes.

Many U.S. futures exchanges and boards of trade also limit the amount of fluctuation permitted in futures contract prices during a single trading day by regulations referred to as “daily price fluctuation limits” or “daily limits.” Once the daily limit has been reached in a particular futures contract, no trades may be made that day at a price beyond that limit or trading may be suspended for specified periods during the trading day. Futures contract prices could move to the limit for several consecutive trading days with little or no trading, thereby preventing prompt liquidation of futures positions and potentially subjecting the Trust to substantial losses.

In order to comply with the position limits established by the CFTC and the relevant exchanges, the Advisor may in the future be required to reduce the size of outstanding positions, not enter into new positions that would otherwise be taken for the Trust or not trade certain markets on behalf of the Trust. Modification of trades made by the Trust, if required, could adversely affect the Trust’s operations and profitability and significantly limit the Trust’s ability to reinvest income in additional contracts, create additional Baskets, or add to existing positions in the desired amount.

In addition, a violation of position limits by the Advisor could lead to regulatory action resulting in mandatory liquidation of certain open positions held on behalf of the Advisor’s accounts in order to ensure compliance with the position limits. There can be no assurance that the Advisor will liquidate positions held on behalf of all the Advisor’s accounts, including any proprietary accounts, in a proportionate manner or at prices favorable to the Trust. In the event the Advisor chooses to liquidate a disproportionate number of positions held on behalf of any of the Trust at unfavorable prices, the Trust may incur substantial losses and the value of the Shares may be adversely affected.

Further, in October 2012 a new CFTC rule became effective which requires each registered futures commission merchant, such as the Clearing FCM, to establish risk-based limits on position and order size. As a result, the Trust’s Clearing FCM may be required to reduce its internal limits on the size of the positions it will execute or clear for the Trust, and the Trust may seek to use additional clearing FCMs, which may increase the costs of clearing for the Trust and adversely affect the value of the Shares.

The Trust may apply to the CFTC or to the relevant exchange for relief from certain position limits. If the Trust applies and is unable to obtain such relief, the Trust’s ability to issue new Baskets, or the Trust’s ability to reinvest income in additional futures contracts, may be limited to the extent these activities would cause the Trust to exceed applicable position limits. Limiting the size of the Trust may affect the correlation between the price of the Shares, as traded on the applicable U.S. futures exchange, and the net asset value of the Trust. Accordingly, the inability to create additional Baskets or add to existing positions in the desired amount could result in Shares trading at a premium or discount to NAV. See “Risks Relating to the Trust and Investment in the Shares—The NAV may not always correspond to the market price and, as a result, Baskets may be created or redeemed at a value that differs from the market price of the Shares.”

Changes in the margin requirements set by the relevant futures exchanges and over-the-counter market participants may limit the Trust’s ability to meet its investment objectives.

The Trust is required to deposit margin securing its exposure to one or more positions in the Portfolio. Futures contracts are customarily bought and sold on margins that represent a very small percentage (ranging upward from less than 2% to 5%) of the purchase price of the contract being traded. The exchanges or futures commission merchants, however, may raise the margin requirements at any time at

16

Table of Contents

their own discretion, particularly during the periods of perceived market volatility, and the Trust may be required to deposit additional funds in order to satisfy the additional margin requirements with respect to its open futures contract positions.

Commercial banks participating in trading over-the-counter derivative contracts often do not require margin deposits, but rely upon internal credit limitations and their judgments regarding the creditworthiness of their counterparties. In recent years, however, many over-the-counter market participants in foreign exchange trading have begun to require that their counterparties post margin. In addition, the Dodd-Frank Act subjects the Trust’s foreign exchange derivatives trading to a retail foreign exchange regime promulgated by a relevant regulator of the Trust’s counterparty. Upon effectiveness of the new retail foreign exchange regulations applicable to the Trust, the Trust would be required to post margin in the amount required under the regulations (between 2% and 5% depending on a currency pair).

If any of the relevant futures exchanges or over-the-counter market participants imposes substantially higher margin requirements or if margin requirements under the new retail foreign exchange regulations are substantially higher than those presently imposed by the Trust’s counterparties, the Trust may be unable to either realize expected returns or to fully implement its trading strategies as a result of substantially greater margin obligations.

Risk Relating to Commodities Markets

The price of the Shares fluctuates as a result of fluctuations in the prices of any commodities underlying the futures contracts owned by the Trust. Commodity prices may be volatile, thereby creating the potential for losses regardless of the length of time you intend to hold your Shares.

The price of the Shares depends on the value of the investments in the Portfolio. To the extent that the Portfolio includes long or short positions in futures contracts the value of which is linked to the price of an underlying commodity, the Trust, and therefore the Shares, are exposed to fluctuations in the price of one or more underlying commodities. The prices of certain physical commodities have been extremely volatile at times during the past several years. Depending on the level and type of fluctuation of these commodities, and whether the Portfolio includes long or short positions with respect to those assets, the value of commodity futures contracts that may be held by the Trust, and consequently the value of the Shares, may be adversely affected. Commodities prices are affected by, among other factors, the cost of producing, transporting and storing commodities, changes in consumer or commercial demand for commodities, the hedging and trading strategies of producers and consumers of commodities, speculative trading in commodities by commodity pools and other market participants, disruptions in commodity supply, weather, political and other global events, global macroeconomic factors, and government regulation of commodities or commodity futures markets. These factors cannot be controlled by the Trust, the Sponsor or the Advisor. Accordingly, the price of the Shares could change substantially and in a rapid and unpredictable manner. This exposes you to a potential loss if you need to sell your Shares when the value of the commodity futures contracts held by the Trust is lower than it was when you made your investment. These fluctuations can affect your investment regardless of the length of time you intend to hold your Shares.

The following events would generally result in a decline in the price of any underlying commodities represented in the Portfolio:

| • | A significant increase in hedging activity by producers of the underlying commodities. Should producers of the underlying commodities represented in the Portfolio increase their hedging of their future production through forward sales or other short positions, this increased selling pressure could depress the price of one or more of the underlying commodities, which could adversely affect the price of the Shares. |

17

Table of Contents

| • | A significant change in the attitude of speculators and investors toward the underlying commodities. Should the speculative or investment community take a negative view towards one or more of the underlying commodities, it could cause a decline in the value of commodity-linked derivative contracts held by the Trust, which could reduce the price of the Shares. |

Conversely, several factors may trigger a temporary increase in the price of the underlying commodities. The price of a commodity underlying a commodity-linked futures contract held by the Trust may be affected by several other factors, including:

| • | Large purchases or sales of physical commodities by the official sector. Governments and large institutions have large commodities holdings or may establish major commodities positions. For example, a significant portion of the aggregate world gold holdings is owned by governments, central banks and related institutions. Similarly, nations with centralized or nationalized oil production and organizations such as OPEC control large physical quantities of crude oil. If one or more of these or similar institutions decides to buy or sell any commodity in amounts large enough to cause a change in world prices, the value of any trading positions held by the Trust and the price of the Shares could be adversely affected. |

| • | Other political factors. In addition to the organized political and institutional trading-related activities described above, peaceful political activity such as imposition of regulations or entry into trade treaties, as well as political disruptions caused by societal breakdown, insurrection or war may greatly influence commodities prices. |

| • | Significant increases or decreases in the available supply of a physical commodity due to natural or technological factors. Natural factors would include depletion of known cost-effective sources for a commodity or the impact of severe weather on the ability to produce or distribute the commodity. Technological factors, such as increases in availability created by new or improved production, extraction, refining and processing equipment and methods or decreases caused by failure or unavailability of major production, refining and processing equipment (for example, shutting down or constructing oil refineries), also materially influence the supply of commodities. |

| • | Significant increases or decreases in the demand for a physical commodity due to natural or technological factors. Natural factors would include such events as unusual climate conditions impacting the demand for energy commodities. Technological factors may include such developments as substitutes for energy or other commodities. |

Prospective investors in the Shares should also keep in mind that the change in the price of the Shares that follows a change in the price of a commodity underlying futures contracts owned by the Trust will not always be in the same direction as the change in the price of that underlying commodity. Depending upon the nature of the Trust’s position with respect to the underlying commodity, it may be the case that a decrease in the price of the underlying commodity has a positive impact on the price of the Shares, or that an increase in the price of the underlying commodity has a negative impact on the price of the Shares. The Trust’s use of leverage has the potential to magnify the impact of fluctuations in the price of underlying commodities on the value of the Trust’s assets. See “Risks Relating to Derivative Contracts—The Trust’s use of leverage and/or short positions involves certain risks, including potentially high volatility and magnified losses in the underlying assets, and should be considered to be speculative.”

Historical performance of specific commodities or commodity indices is no guide to their future performance or to the performance of the Shares.

At any given time, the Trust may be exposed to changes in the prices of one or more commodities. Even at a time when the prices of some or most commodities are increasing, it is possible for the price of the Shares to decrease as a result of lack of exposure to such commodities, mistaken anticipation by the Advisor of the direction in which the price of the commodity would move or many other factors. Therefore, there are no external indicators of how the Shares will perform. Because the Trust does not track or seek

18

Table of Contents

to replicate any commodity index or other similar benchmark, the past performance of any commodity index is not necessarily indicative of the future performance of the Shares. You may lose some or all of your investment in the Shares even during times when commodities indices are showing positive returns.

Commodity futures trading may be illiquid. In addition, suspensions or disruptions of market trading in the commodities markets and related derivatives markets may adversely affect the value of your Shares.

The commodity, commodity futures and commodity derivatives markets are subject to temporary distortions or other disruptions due to various factors, including the lack of liquidity, congestion, disorderly markets, limitations on deliverable supplies, the participation of speculators, government regulation and intervention, technical and operational or system failures, nuclear accident, terrorism, riots and acts of God. In addition, forward contracts may entail breakage costs if terminated prior to their final maturity and futures positions cannot always be liquidated at the desired prices.

Further, U.S. futures exchanges and some foreign exchanges have regulations that limit position, size and/or the amount of fluctuation in futures contract prices that may occur during a single business day. These limits are generally referred to as “daily price fluctuation limits,” and the maximum or minimum price of a contract on any given day as a result of these limits is referred to as a “limit price.” Once the limit price has been reached in a particular contract, no trades may be made at a different price. It is not certain how long these price limits may remain in effect. Limit prices may have the effect of precluding trading in a particular contract or forcing the liquidation of contracts at disadvantageous times or prices, and possibly having a negative effect on the investment strategies of the Trust and/or the value of commodity-linked futures contracts held by the Trust. These circumstances could thereby adversely affect the price of your Shares. In addition, these circumstances could limit trading in commodity-linked futures contracts, which could affect the investment strategies of the Trust and/or the calculation of the NAV and the trading price of the Shares. Accordingly, these limits may result in an NAV that differs, and may differ significantly, from the NAV that would prevail in the absence of these limits. If Baskets are created or redeemed at a time when these price limits are in effect, the creation or redemption price will reflect the price limits as well.

Furthermore, exchanges may take steps, such as requiring liquidation of open positions, in the case of disorderly markets, market congestion and other market disruptions. These actions could require the Trust to limit or forego a desired investment strategy. This could adversely affect the NAV and the Trust’s performance.