Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - United States Oil Fund, LP | Financial_Report.xls |

| EX-31.2 - SECTION 302 PFO CERTIFICATION - United States Oil Fund, LP | d399234dex312.htm |

| EX-31.1 - SECTION 302 PEO CERTIFICATION - United States Oil Fund, LP | d399234dex311.htm |

| EX-32.1 - SECTION 906 PEO CERTIFICATION - United States Oil Fund, LP | d399234dex321.htm |

| EX-32.2 - SECTION 906 PFO CERTIFICATION - United States Oil Fund, LP | d399234dex322.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

| x | Quarterly report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the quarterly period ended September 30, 2012. |

OR

| ¨ | Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the transition period from to . |

Commission File Number: 001-32834

United States Oil Fund, LP

(Exact name of registrant as specified in its charter)

| Delaware | 20-2830691 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

1999 Harrison Street, Suite 1530

Oakland, California 94612

(Address of principal executive offices) (Zip code)

(510) 522-9600

(Registrant’s telephone number, including area code)

N/A

(Former name, former address and former fiscal year, if changed since last report)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). x Yes ¨ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer |

x |

Accelerated filer |

¨ | |||

| Non-accelerated filer |

¨ (Do not check if a smaller reporting company) |

Smaller reporting company |

¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ¨ Yes x No

Table of Contents

Table of Contents

Table of Contents

| Item 1. | Condensed Financial Statements. |

Index to Condensed Financial Statements

1

Table of Contents

Condensed Statements of Financial Condition

At September 30, 2012 (Unaudited) and December 31, 2011

| September 30, 2012 | December 31, 2011 | |||||||

| Assets |

||||||||

| Cash and cash equivalents (Note 5) |

$ | 846,272,968 | $ | 838,608,739 | ||||

| Equity in UBS Securities LLC trading accounts: |

||||||||

| Cash and cash equivalents |

291,628,169 | 303,665,981 | ||||||

| Unrealized loss on open commodity futures contracts |

(50,051,830 | ) | (6,472,310 | ) | ||||

| Receivable for units sold |

44,430,906 | 38,074,230 | ||||||

| Dividend receivable |

16,299 | 10,659 | ||||||

| Interest receivable |

167 | 202 | ||||||

| Other assets |

476,258 | 506,897 | ||||||

|

|

|

|

|

|||||

| Total assets |

$ | 1,132,772,937 | $ | 1,174,394,398 | ||||

|

|

|

|

|

|||||

| Liabilities and Partners’ Capital |

||||||||

| Investment payable |

$ | — | $ | 553 | ||||

| Payable for units redeemed |

— | 64,726,191 | ||||||

| Professional fees payable |

923,258 | 1,137,607 | ||||||

| General Partner management fees payable (Note 3) |

433,616 | 445,715 | ||||||

| Brokerage commissions payable |

43,911 | 32,186 | ||||||

| Other liabilities |

91,433 | 93,264 | ||||||

|

|

|

|

|

|||||

| Total liabilities |

1,492,218 | 66,435,516 | ||||||

|

|

|

|

|

|||||

| Commitments and Contingencies (Notes 3, 4 and 5) |

||||||||

| Partners’ Capital |

||||||||

| General Partner |

— | — | ||||||

| Limited Partners |

1,131,280,719 | 1,107,958,882 | ||||||

|

|

|

|

|

|||||

| Total Partners’ Capital |

1,131,280,719 | 1,107,958,882 | ||||||

|

|

|

|

|

|||||

| Total liabilities and partners’ capital |

$ | 1,132,772,937 | $ | 1,174,394,398 | ||||

|

|

|

|

|

|||||

| Limited Partners’ units outstanding |

33,100,000 | 29,100,000 | ||||||

|

|

|

|

|

|||||

| Net asset value per unit |

$ | 34.18 | $ | 38.07 | ||||

|

|

|

|

|

|||||

| Market value per unit |

$ | 34.12 | $ | 38.11 | ||||

|

|

|

|

|

|||||

See accompanying notes to condensed financial statements.

2

Table of Contents

Condensed Schedule of Investments (Unaudited)

At September 30, 2012

| Number of Contracts |

Unrealized Loss on Open Commodity Contracts |

% of Partners’ Capital |

||||||||||

| Open Futures Contracts - Long |

||||||||||||

| Foreign Contracts |

||||||||||||

| ICE WTI Crude Oil Futures November 2012 contracts, expiring October 2012 |

2,000 | $ | (9,110,000 | ) | (0.80 | ) | ||||||

|

|

|

|

|

|

|

|||||||

| United States Contracts |

||||||||||||

| NYMEX Crude Oil Futures CL November 2012 contracts, expiring October 2012 |

10,272 | (40,941,830 | ) | (3.62 | ) | |||||||

|

|

|

|

|

|

|

|||||||

| Total Open Futures Contracts |

12,272 | $ | (50,051,830 | ) | (4.42 | ) | ||||||

|

|

|

|

|

|

|

|||||||

| Principal Amount |

Market Value | |||||||||||

| Cash Equivalents |

||||||||||||

| United States Treasury Obligation |

||||||||||||

| U.S. Treasury Bill, 0.09%, 10/11/2012 |

$ | 150,390,000 | $ | 150,386,274 | 13.29 | |||||||

|

|

|

|

|

|||||||||

| United States - Money Market Funds |

||||||||||||

| Fidelity Institutional Government Portfolio - Class I |

137,050,191 | 137,050,191 | 12.11 | |||||||||

| Goldman Sachs Financial Square Funds - Government Fund - Class SL |

207,770,011 | 207,770,011 | 18.37 | |||||||||

| Morgan Stanley Institutional Liquidity Fund - Government Portfolio |

201,032,462 | 201,032,462 | 17.77 | |||||||||

| Wells Fargo Advantage Government Money Market Fund - Class I |

200,003,946 | 200,003,946 | 17.68 | |||||||||

|

|

|

|

|

|||||||||

| Total Money Market Funds |

745,856,610 | 65.93 | ||||||||||

|

|

|

|

|

|||||||||

| Total Cash Equivalents |

$ | 896,242,884 | 79.22 | |||||||||

|

|

|

|

|

|||||||||

See accompanying notes to condensed financial statements.

3

Table of Contents

Condensed Statements of Operations (Unaudited)

For the three and nine months ended September 30, 2012 and 2011

| Three months ended September 30, 2012 |

Three months ended September 30, 2011 |

Nine

months ended September 30, 2012 |

Nine

months ended September 30, 2011 |

|||||||||||||

| Income |

||||||||||||||||

| Gain (loss) on trading of commodity futures contracts: |

||||||||||||||||

| Realized gain (loss) on closed positions |

$ | 146,631,510 | $ | (149,599,580 | ) | $ | (62,348,970 | ) | $ | 39,659,420 | ||||||

| Change in unrealized loss on open positions |

(65,971,870 | ) | (62,291,620 | ) | (43,579,520 | ) | (165,561,060 | ) | ||||||||

| Dividend income |

50,326 | 18,394 | 159,647 | 166,750 | ||||||||||||

| Interest income |

45,771 | 26,544 | 116,306 | 47,332 | ||||||||||||

| Other income |

62,000 | 59,000 | 153,000 | 209,000 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total income (loss) |

80,817,737 | (211,787,262 | ) | (105,499,537 | ) | (125,478,558 | ) | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Expenses |

||||||||||||||||

| General Partner management fees (Note 3) |

1,391,015 | 1,493,839 | 4,281,910 | 5,412,280 | ||||||||||||

| Professional fees |

360,568 | 44,298 | 1,015,104 | 696,430 | ||||||||||||

| Brokerage commissions |

329,550 | 353,831 | 960,506 | 1,197,026 | ||||||||||||

| Other expenses |

142,695 | 152,952 | 382,408 | 518,223 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total expenses |

2,223,828 | 2,044,920 | 6,639,928 | 7,823,959 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income (loss) |

$ | 78,593,909 | $ | (213,832,182 | ) | $ | (112,139,465 | ) | $ | (133,302,517 | ) | |||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income (loss) per limited partnership unit |

$ | 2.29 | $ | (6.77 | ) | $ | (3.89 | ) | $ | (8.31 | ) | |||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income (loss) per weighted average limited partnership unit |

$ | 2.19 | $ | (5.66 | ) | $ | (3.20 | ) | $ | (3.17 | ) | |||||

|

|

|

|

|

|

|

|

|

|||||||||

| Weighted average limited partnership units outstanding |

35,838,043 | 37,797,826 | 35,012,044 | 42,026,007 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

See accompanying notes to condensed financial statements.

4

Table of Contents

Condensed Statement of Changes in Partners’ Capital (Unaudited)

For the nine months ended September 30, 2012

| General Partner | Limited Partners | Total | ||||||||||

| Balances, at December 31, 2011 |

$ | — | $ | 1,107,958,882 | $ | 1,107,958,882 | ||||||

| Addition of 80,500,000 partnership units |

— | 2,870,602,104 | 2,870,602,104 | |||||||||

| Redemption of 76,500,000 partnership units |

— | (2,735,140,802 | ) | (2,735,140,802 | ) | |||||||

| Net loss |

— | (112,139,465 | ) | (112,139,465 | ) | |||||||

|

|

|

|

|

|

|

|||||||

| Balances, at September 30, 2012 |

$ | — | $ | 1,131,280,719 | $ | 1,131,280,719 | ||||||

|

|

|

|

|

|

|

|||||||

| Net Asset Value Per Unit: |

||||||||||||

| At December 31, 2011 |

$ | 38.07 | ||||||||||

|

|

|

|||||||||||

| At September 30, 2012 |

$ | 34.18 | ||||||||||

|

|

|

|||||||||||

See accompanying notes to condensed financial statements.

5

Table of Contents

Condensed Statements of Cash Flows (Unaudited)

For the nine months ended September 30, 2012 and 2011

| Nine

months ended September 30, 2012 |

Nine

months ended September 30, 2011 |

|||||||

| Cash Flows from Operating Activities: |

||||||||

| Net loss |

$ | (112,139,465 | ) | $ | (133,302,517 | ) | ||

| Adjustments to reconcile net loss to net cash used in operating activities: |

||||||||

| (Increase) decrease in commodity futures trading account - cash and cash equivalents |

12,037,812 | (61,451,394 | ) | |||||

| Unrealized loss on open futures contracts |

43,579,520 | 165,561,060 | ||||||

| (Increase) decrease in dividend receivable |

(5,640 | ) | 44,774 | |||||

| Decrease in interest receivable |

35 | — | ||||||

| Decrease in other assets |

30,639 | 31,992 | ||||||

| Decrease investment payable |

(553 | ) | — | |||||

| Decrease in professional fees payable |

(214,349 | ) | (373,311 | ) | ||||

| Decrease in General Partner management fees payable |

(12,099 | ) | (236,999 | ) | ||||

| Increase (decrease) in brokerage commissions payable |

11,725 | (11,000 | ) | |||||

| Decrease in other liabilities |

(1,831 | ) | (22,977 | ) | ||||

|

|

|

|

|

|||||

| Net cash used in operating activities |

(56,714,206 | ) | (29,760,372 | ) | ||||

|

|

|

|

|

|||||

| Cash Flows from Financing Activities: |

||||||||

| Addition of partnership units |

2,864,245,428 | 3,795,167,029 | ||||||

| Redemption of partnership units |

(2,799,866,993 | ) | (4,312,704,770 | ) | ||||

|

|

|

|

|

|||||

| Net cash provided by (used in) financing activities |

64,378,435 | (517,537,741 | ) | |||||

|

|

|

|

|

|||||

| Net Increase (Decrease) in Cash and Cash Equivalents |

7,664,229 | (547,298,113 | ) | |||||

| Cash and Cash Equivalents, beginning of period |

838,608,739 | 1,522,955,092 | ||||||

|

|

|

|

|

|||||

| Cash and Cash Equivalents, end of period |

$ | 846,272,968 | $ | 975,656,979 | ||||

|

|

|

|

|

|||||

See accompanying notes to condensed financial statements.

6

Table of Contents

Notes to Condensed Financial Statements

For the period ended September 30, 2012 (Unaudited)

NOTE 1 — ORGANIZATION AND BUSINESS

The United States Oil Fund, LP (“USOF”) was organized as a limited partnership under the laws of the state of Delaware on May 12, 2005. USOF is a commodity pool that issues limited partnership units (“units”) that may be purchased and sold on the NYSE Arca, Inc. (the “NYSE Arca”). Prior to November 25, 2008, USOF’s units traded on the American Stock Exchange (the “AMEX”). USOF will continue in perpetuity, unless terminated sooner upon the occurrence of one or more events as described in its Fifth Amended and Restated Agreement of Limited Partnership dated as of October 13, 2008 (the “LP Agreement”). The investment objective of USOF is for the daily changes in percentage terms of its units’ per unit net asset value (“NAV”) to reflect the daily changes in percentage terms of the spot price of light, sweet crude oil delivered to Cushing, Oklahoma, as measured by the daily changes in the price of the futures contract for light, sweet crude oil traded on the New York Mercantile Exchange (the “NYMEX”) that is the near month contract to expire, except when the near month contract is within two weeks of expiration, in which case the futures contract will be the next month contract to expire (the “Benchmark Oil Futures Contract”), less USOF’s expenses. It is not the intent of USOF to be operated in a fashion such that the per unit NAV will equal, in dollar terms, the spot price of light, sweet crude oil or any particular futures contract based on light, sweet crude oil. It is not the intent of USOF to be operated in a fashion such that its per unit NAV will reflect the percentage change of the price of any particular futures contract as measured over a time period greater than one day. United States Commodity Funds LLC (“USCF”), the general partner of USOF, believes that it is not practical to manage the portfolio to achieve such an investment goal when investing in Oil Futures Contracts (as defined below) and Other Oil-Related Investments (as defined below). USOF accomplishes its objective through investments in futures contracts for light, sweet crude oil and other types of crude oil, heating oil, gasoline, natural gas and other petroleum-based fuels that are traded on the NYMEX, ICE Futures or other U.S. and foreign exchanges (collectively, “Oil Futures Contracts”) and other oil-related investments such as cash-settled options on Oil Futures Contracts, forward contracts for oil, cleared swap contracts and over-the-counter transactions that are based on the price of crude oil, heating oil, gasoline, natural gas and other petroleum-based fuels, Oil Futures Contracts and indices based on the foregoing (collectively, “Other Oil-Related Investments”). As of September 30, 2012, USOF held 10,272 Oil Futures Contracts for light, sweet crude oil traded on the NYMEX and 2,000 Oil Futures Contracts for light, sweet crude oil traded on the ICE Futures.

USOF commenced investment operations on April 10, 2006 and has a fiscal year ending on December 31. USCF is responsible for the management of USOF. USCF is a member of the National Futures Association (the “NFA”) and became a commodity pool operator registered with the Commodity Futures Trading Commission (the “CFTC”) effective December 1, 2005. USCF is also the general partner of the United States Natural Gas Fund, LP (“USNG”), the United States 12 Month Oil Fund, LP (“US12OF”), the United States Gasoline Fund, LP (“UGA”) and the United States Diesel-Heating Oil Fund, LP (formerly, the United States Heating Oil Fund, LP) (“USDHO”), which listed their limited partnership units on the AMEX under the ticker symbols “UNG” on April 18, 2007, “USL” on December 6, 2007, “UGA” on February 26, 2008 and “UHN” on April 9, 2008, respectively. As a result of the acquisition of the AMEX by NYSE Euronext, each of USNG’s, US12OF’s, UGA’s and USDHO’s units commenced trading on the NYSE Arca on November 25, 2008. USCF is also the general partner of the United States Short Oil Fund, LP (“USSO”), the United States 12 Month Natural Gas Fund, LP (“US12NG”) and the United States Brent Oil Fund, LP (“USBO”), which listed their limited partnership units on the NYSE Arca under the ticker symbols “DNO” on September 24, 2009, “UNL” on November 18, 2009 and “BNO” on June 2, 2010, respectively. USCF is also the sponsor of the United States Commodity Index Fund (“USCI”), the United States Copper Index Fund (“CPER”), the United States Agriculture Index Fund (“USAG”) and the United States Metals Index Fund (“USMI”), each a series of the United States Commodity Index Funds Trust. USCI, CPER, USAG and USMI listed their units on the NYSE Arca under the ticker symbol “USCI” on August 10, 2010, “CPER” on November 15, 2011, “USAG” on April 13, 2012 and “USMI” on June 19, 2012, respectively. All funds listed previously are referred to collectively herein as the “Related Public Funds.” USCF has also filed registration statements to register units of the United States Sugar Fund (“USSF”), the United States Natural Gas Double Inverse Fund (“UNGD”), the United States Gasoil Fund (“USGO”) and the United States Asian Commodities Basket Fund (“UAC”), each a series of the United States Commodity Funds Trust I, and the US Golden Currency Fund (“HARD”), a series of the United States Currency Funds Trust.

7

Table of Contents

USOF issues units to certain authorized purchasers (“Authorized Purchasers”) by offering baskets consisting of 100,000 units (“Creation Baskets”) through ALPS Distributors, Inc., as the marketing agent (the “Marketing Agent”). The purchase price for a Creation Basket is based upon the NAV of a unit calculated shortly after the close of the core trading session on the NYSE Arca on the day the order to create the basket is properly received.

In addition, Authorized Purchasers pay USOF a $1,000 fee for each order placed to create one or more Creation Baskets or to redeem one or more baskets (“Redemption Baskets”), consisting of 100,000 units. Units may be purchased or sold on a nationally recognized securities exchange in smaller increments than a Creation Basket or Redemption Basket. Units purchased or sold on a nationally recognized securities exchange are not purchased or sold at the per unit NAV of USOF but rather at market prices quoted on such exchange.

In April 2006, USOF initially registered 17,000,000 units on Form S-1 with the U.S. Securities and Exchange Commission (the “SEC”). On April 10, 2006, USOF listed its units on the AMEX under the ticker symbol “USO”. On that day, USOF established its initial per unit NAV by setting the price at $67.39 and issued 200,000 units in exchange for $13,479,000. USOF also commenced investment operations on April 10, 2006, by purchasing Oil Futures Contracts traded on the NYMEX based on light, sweet crude oil. As of September 30, 2012, USOF had registered a total of 1,627,000,000 units.

The accompanying unaudited condensed financial statements have been prepared in accordance with Rule 10-01 of Regulation S-X promulgated by the SEC and, therefore, do not include all information and footnote disclosure required under generally accepted accounting principles (“GAAP”) in the United States of America. The financial information included herein is unaudited; however, such financial information reflects all adjustments, consisting only of normal recurring adjustments, which are, in the opinion of USCF, necessary for the fair presentation of the condensed financial statements for the interim period.

NOTE 2 — SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Revenue Recognition

Commodity futures contracts, forward contracts, physical commodities and related options are recorded on the trade date. All such transactions are recorded on the identified cost basis and marked to market daily. Unrealized gains or losses on open contracts are reflected in the condensed statements of financial condition and represent the difference between the original contract amount and the market value (as determined by exchange settlement prices for futures contracts and related options and cash dealer prices at a predetermined time for forward contracts, physical commodities, and their related options) as of the last business day of the year or as of the last date of the condensed financial statements. Changes in the unrealized gains or losses between periods are reflected in the condensed statements of operations. USOF earns interest on its assets denominated in U.S. dollars on deposit with the futures commission merchant at the overnight Federal Funds Rate less 32 basis points. In addition, USOF earns income on funds held at the custodian or futures commission merchant at prevailing market rates earned on such investments.

Brokerage Commissions

Brokerage commissions on all open commodity futures contracts are accrued on a full-turn basis.

Income Taxes

USOF is not subject to federal income taxes; each partner reports his/her allocable share of income, gain, loss deductions or credits on his/her own income tax return.

In accordance with GAAP, USOF is required to determine whether a tax position is more likely than not to be sustained upon examination by the applicable taxing authority, including resolution of any tax related appeals or litigation processes, based on the technical merits of the position. USOF files an income tax return in the U.S. federal jurisdiction, and may file income tax returns in various U.S. states. USOF is not subject to income tax return examinations by major taxing authorities for years before 2008. The tax benefit recognized is measured as the largest amount of benefit that has a greater than fifty percent likelihood of being realized upon ultimate settlement. De-recognition of a tax benefit previously recognized results in USOF recording a tax liability that reduces net assets. However, USOF’s conclusions regarding this policy may be subject to review and adjustment at a later date based on factors including, but not limited to, on-going analysis of and changes to tax laws, regulations and interpretations thereof. USOF recognizes interest accrued related to unrecognized tax benefits and penalties related to unrecognized tax benefits in income tax fees payable, if assessed. No interest expense or penalties have been recognized as of and for the period ended September 30, 2012.

8

Table of Contents

Creations and Redemptions

Authorized Purchasers may purchase Creation Baskets or redeem Redemption Baskets only in blocks of 100,000 units at a price equal to the NAV of the units calculated shortly after the close of the core trading session on the NYSE Arca on the day the order is placed.

USOF receives or pays the proceeds from units sold or redeemed within three business days after the trade date of the purchase or redemption. The amounts due from Authorized Purchasers are reflected in USOF’s condensed statements of financial condition as receivable for units sold, and amounts payable to Authorized Purchasers upon redemption are reflected as payable for units redeemed.

Partnership Capital and Allocation of Partnership Income and Losses

Profit or loss shall be allocated among the partners of USOF in proportion to the number of units each partner holds as of the close of each month. USCF may revise, alter or otherwise modify this method of allocation as described in the LP Agreement.

Calculation of Per Unit Net Asset Value

USOF’s per unit NAV is calculated on each NYSE Arca trading day by taking the current market value of its total assets, subtracting any liabilities and dividing that amount by the total number of units outstanding. USOF uses the closing price for the contracts on the relevant exchange on that day to determine the value of contracts held on such exchange.

Net Income (Loss) Per Unit

Net income (loss) per unit is the difference between the per unit NAV at the beginning of each period and at the end of each period. The weighted average number of units outstanding was computed for purposes of disclosing net income (loss) per weighted average unit. The weighted average units are equal to the number of units outstanding at the end of the period, adjusted proportionately for units added and redeemed based on the amount of time the units were outstanding during such period. There were no units held by USCF at September 30, 2012.

Offering Costs

Offering costs incurred in connection with the registration of additional units after the initial registration of units are borne by USOF. These costs include registration fees paid to regulatory agencies and all legal, accounting, printing and other expenses associated with such offerings. These costs are accounted for as a deferred charge and thereafter amortized to expense over twelve months on a straight-line basis or a shorter period if warranted.

Cash Equivalents

Cash equivalents include money market funds and overnight deposits or time deposits with original maturity dates of six months or less.

Reclassification

Certain amounts in the accompanying condensed financial statements were reclassified to conform to the current presentation.

Use of Estimates

The preparation of condensed financial statements in conformity with GAAP requires USCF to make estimates and assumptions that affect the reported amount of assets and liabilities and disclosure of contingent assets and liabilities at the date of the condensed financial statements, and the reported amounts of the revenue and expenses during the reporting period. Actual results may differ from those estimates and assumptions.

9

Table of Contents

NOTE 3 — FEES PAID BY THE FUND AND RELATED PARTY TRANSACTIONS

USCF Management Fee

Under the LP Agreement, USCF is responsible for investing the assets of USOF in accordance with the objectives and policies of USOF. In addition, USCF has arranged for one or more third parties to provide administrative, custody, accounting, transfer agency and other necessary services to USOF. For these services, USOF is contractually obligated to pay USCF a fee, which is paid monthly, equal to 0.45% per annum of average daily total net assets.

Ongoing Registration Fees and Other Offering Expenses

USOF pays all costs and expenses associated with the ongoing registration of its units subsequent to the initial offering. These costs include registration or other fees paid to regulatory agencies in connection with the offer and sale of units, and all legal, accounting, printing and other expenses associated with such offer and sale. For the nine months ended September 30, 2012 and 2011, USOF incurred $61,498 and $35,490, respectively, in registration fees and other offering expenses.

Directors’ Fees and Expenses

USOF is responsible for paying its portion of the directors’ and officers’ liability insurance for USOF and the Related Public Funds and the fees and expenses of the independent directors who also serve as audit committee members of USOF and the Related Public Funds organized as limited partnerships and, as of July 8, 2011, the Related Public Funds organized as a series of a Delaware statutory trust. USOF shares the fees and expenses on a pro rata basis with each Related Public Fund, as described above, based on the relative assets of each fund computed on a daily basis. These fees and expenses for the year ending December 31, 2012 are estimated to be a total of $540,000 for USOF and the Related Public Funds.

Licensing Fees

As discussed in Note 4 below, USOF entered into a licensing agreement with the NYMEX on April 10, 2006, as amended on October 20, 2011. Pursuant to the agreement, through October 19, 2011, USOF and the Related Public Funds, other than USBO, USCI, CPER, USAG and USMI, paid a licensing fee that was equal to 0.04% for the first $1,000,000,000 of combined net assets of the funds and 0.02% for combined net assets above $1,000,000,000. On and after October 20, 2011, USOF and the Related Public Funds, other than USBO, USCI, CPER, USAG and USMI, pay a licensing fee that is equal to 0.015% on all net assets. During the nine months ended September 30, 2012 and 2011, USOF incurred $142,730 and $300,458, respectively, under this arrangement.

Investor Tax Reporting Cost

The fees and expenses associated with USOF’s audit expenses and tax accounting and reporting requirements are paid by USOF. These costs are estimated to be $1,200,000 for the year ending December 31, 2012.

Other Expenses and Fees

In addition to the fees described above, USOF pays all brokerage fees and other expenses in connection with the operation of USOF, excluding costs and expenses paid by USCF as outlined in Note 4 below.

NOTE 4 — CONTRACTS AND AGREEMENTS

USOF is party to a marketing agent agreement, dated as of March 13, 2006, as amended from time to time, with the Marketing Agent and USCF, whereby the Marketing Agent provides certain marketing services for USOF as outlined in the agreement. The fees of the Marketing Agent, which are borne by USCF, include a marketing fee of $425,000 per annum plus the following incentive fee: 0.00% on USOF’s assets from $0 – $500 million; 0.04% on USOF’s assets from $500 million – $4 billion; and 0.03% on USOF’s assets in excess of $4 billion.

The above fees do not include the following expenses, which are also borne by USCF: the cost of placing advertisements in various periodicals; web construction and development; or the printing and production of various marketing materials.

10

Table of Contents

USOF is also party to a custodian agreement, dated March 13, 2006, as amended from time to time, with Brown Brothers Harriman & Co. (“BBH&Co.”) and USCF, whereby BBH&Co. holds investments on behalf of USOF. USCF pays the fees of the custodian, which are determined by the parties from time to time. In addition, USOF is party to an administrative agency agreement, dated March 13, 2006, as amended from time to time, with USCF and BBH&Co., whereby BBH&Co. acts as the administrative agent, transfer agent and registrar for USOF. USCF also pays the fees of BBH&Co. for its services under such agreement and such fees are determined by the parties from time to time.

Currently, USCF pays BBH&Co. for its services, in the foregoing capacities, a minimum amount of $75,000 annually for its custody, fund accounting and fund administration services rendered to USOF and each of the Related Public Funds, as well as a $20,000 annual fee for its transfer agency services. In addition, USCF pays BBH&Co. an asset-based charge of (a) 0.06% for the first $500 million of USOF’s, USNG’s, US12OF’s, UGA’s, USDHO’s, USSO’s, US12NG’s, USBO’s, USCI’s, CPER’s, USAG’s and USMI’s combined net assets, (b) 0.0465% for USOF’s, USNG’s, US12OF’s, UGA’s, USDHO’s, USSO’s, US12NG’s, USBO’s, USCI’s, CPER’s, USAG’s and USMI’s combined net assets greater than $500 million but less than $1 billion, and (c) 0.035% once USOF’s, USNG’s, US12OF’s, UGA’s, USDHO’s, USSO’s, US12NG’s, USBO’s, USCI’s, CPER’s, USAG’s and USMI’s combined net assets exceed $1 billion. The annual minimum amount will not apply if the asset-based charge for all accounts in the aggregate exceeds $75,000. USCF also pays transaction fees ranging from $7 to $15 per transaction.

USOF has entered into a brokerage agreement with UBS Securities LLC (“UBS Securities”). The agreement requires UBS Securities to provide services to USOF in connection with the purchase and sale of Oil Futures Contracts and Other Oil-Related Investments that may be purchased and sold by or through UBS Securities for USOF’s account. In accordance with the agreement, UBS Securities charges USOF commissions of approximately $7 to $15 per round-turn trade, including applicable exchange and NFA fees for Oil Futures Contracts and options on Oil Futures Contracts. Such fees include those incurred when purchasing Oil Futures Contracts and options on Oil Futures Contracts when USOF issues units as a result of a Creation Basket, as well as fees incurred when selling Oil Futures Contracts and options on Oil Futures Contracts when USOF redeems units as a result of a Redemption Basket. Such fees are also incurred when Oil Futures Contracts and options on Oil Futures Contracts are purchased or redeemed for the purpose of rebalancing the portfolio. USOF also incurs commissions to brokers for the purchase and sale of Oil Futures Contracts, Other Oil-Related Investments or Treasuries. During the nine months ended September 30, 2012, total commissions accrued to brokers amounted to $960,506. Of this amount, approximately $786,899 was a result of rebalancing costs and approximately $173,607 was the result of trades necessitated by creation and redemption activity. By comparison, during the nine months ended September 30, 2011, total commissions accrued to brokers amounted to $1,197,026. Of this amount, approximately $920,879 was a result of rebalancing costs and approximately $276,147 was the result of trades necessitated by creation and redemption activity. The decrease in the total commissions accrued to brokers for the nine months ended September 30, 2012, as compared to the nine months ended September 30, 2011, was primarily a result of the decrease in USOF’s average total net assets during the nine months ended September 30, 2012, as compared to the nine months ended September 30, 2011. As an annualized percentage of average daily total net assets, the figure for the nine months ended September 30, 2012 represents approximately 0.10% of average daily total net assets. By comparison, the figure for the nine months ended September 30, 2011 represented approximately 0.10% of average daily total net assets. However, there can be no assurance that commission costs and portfolio turnover will not cause commission expenses to rise in future quarters.

USOF and the NYMEX entered into a licensing agreement on April 10, 2006, as amended on October 20, 2011, whereby USOF was granted a non-exclusive license to use certain of the NYMEX’s settlement prices and service marks. Under the licensing agreement, USOF and the Related Public Funds, other than USBO, USCI, CPER, USAG and USMI, pay the NYMEX an asset-based fee for the license, the terms of which are described in Note 3. USOF expressly disclaims any association with the NYMEX or endorsement of USOF by the NYMEX and acknowledges that “NYMEX” and “New York Mercantile Exchange” are registered trademarks of the NYMEX.

NOTE 5 — FINANCIAL INSTRUMENTS, OFF-BALANCE SHEET RISKS AND CONTINGENCIES

USOF engages in the trading of futures contracts, options on futures contracts and cleared swaps (collectively, “derivatives”). USOF is exposed to both market risk, which is the risk arising from changes in the market value of the contracts, and credit risk, which is the risk of failure by another party to perform according to the terms of a contract.

11

Table of Contents

USOF may enter into futures contracts, options on futures contracts and cleared swaps to gain exposure to changes in the value of an underlying commodity. A futures contract obligates the seller to deliver (and the purchaser to accept) the future delivery of a specified quantity and type of a commodity at a specified time and place. Some futures contracts may call for physical delivery of the asset, while others are settled in cash. The contractual obligations of a buyer or seller may generally be satisfied by taking or making physical delivery of the underlying commodity or by making an offsetting sale or purchase of an identical futures contract on the same or linked exchange before the designated date of delivery.

The purchase and sale of futures contracts, options on futures contracts and cleared swaps require margin deposits with a futures commission merchant. Additional deposits may be necessary for any loss on contract value. The Commodity Exchange Act requires a futures commission merchant to segregate all customer transactions and assets from the futures commission merchant’s proprietary activities.

Futures contracts and cleared swaps involve, to varying degrees, elements of market risk (specifically commodity price risk) and exposure to loss in excess of the amount of variation margin. The face or contract amounts reflect the extent of the total exposure USOF has in the particular classes of instruments. Additional risks associated with the use of futures contracts are an imperfect correlation between movements in the price of the futures contracts and the market value of the underlying securities and the possibility of an illiquid market for a futures contract.

All of the futures contracts held by USOF were exchange-traded through September 30, 2012. The risks associated with exchange-traded contracts are generally perceived to be less than those associated with over-the-counter transactions since, in over-the-counter transactions, a party must rely solely on the credit of its respective individual counterparties. However, in the future, if USOF were to enter into non-exchange traded contracts, it would be subject to the credit risk associated with counterparty non-performance. The credit risk from counterparty non-performance associated with such instruments is the net unrealized gain, if any, on the transaction. USOF has credit risk under its futures contracts since the sole counterparty to all domestic and foreign futures contracts is the clearinghouse for the exchange on which the relevant contracts are traded. In addition, USOF bears the risk of financial failure by the clearing broker.

USOF’s cash and other property, such as short-term obligations of the United States of two years or less (“Treasuries”), deposited with a futures commission merchant are considered commingled with all other customer funds, subject to the futures commission merchant’s segregation requirements. In the event of a futures commission merchant’s insolvency, recovery may be limited to a pro rata share of segregated funds available. It is possible that the recovered amount could be less than the total of cash and other property deposited. The insolvency of a futures commission merchant could result in the complete loss of USOF’s assets posted with that futures commission merchant; however, the majority of USOF’s assets are held in cash and/or cash equivalents with USOF’s custodian and would not be impacted by the insolvency of a futures commission merchant. The failure or insolvency of USOF’s custodian, however, could result in a substantial loss of USOF’s assets.

USCF invests a portion of USOF’s cash in money market funds that seek to maintain a stable per unit NAV. USOF is exposed to any risk of loss associated with an investment in such money market funds. As of September 30, 2012 and December 31, 2011, USOF held investments in money market funds in the amounts of $745,856,610 and $595,703,156, respectively. USOF also holds cash deposits with its custodian. Pursuant to a written agreement with BBH&Co., uninvested overnight cash balances are swept to offshore branches of U.S. regulated and domiciled banks located in Toronto, Canada, London, United Kingdom, Grand Cayman, Cayman Islands and Nassau, Bahamas, which are subject to U.S. regulation and regulatory oversight. As of September 30, 2012 and December 31, 2011, USOF held cash deposits and investments in Treasuries in the amounts of $392,044,527 and $546,571,564, respectively, with the custodian and futures commission merchant. Some or all of these amounts may be subject to loss should USOF’s custodian and/or futures commission merchant cease operations.

For derivatives, risks arise from changes in the market value of the contracts. Theoretically, USOF is exposed to market risk equal to the value of futures contracts purchased and unlimited liability on such contracts sold short. As both a buyer and a seller of options, USOF pays or receives a premium at the outset and then bears the risk of unfavorable changes in the price of the contract underlying the option.

12

Table of Contents

USOF’s policy is to continuously monitor its exposure to market and counterparty risk through the use of a variety of financial, position and credit exposure reporting controls and procedures. In addition, USOF has a policy of requiring review of the credit standing of each broker or counterparty with which it conducts business.

The financial instruments held by USOF are reported in its condensed statements of financial condition at market or fair value, or at carrying amounts that approximate fair value, because of their highly liquid nature and short-term maturity.

NOTE 6 — FINANCIAL HIGHLIGHTS

The following table presents per unit performance data and other supplemental financial data for the nine months ended September 30, 2012 and 2011 for the unitholders. This information has been derived from information presented in the condensed financial statements.

| For the nine months ended September 30, 2012 (Unaudited) |

For the nine months ended September 30, 2011 (Unaudited) |

|||||||

| Per Unit Operating Performance: |

||||||||

| Net asset value, beginning of period |

$ | 38.07 | $ | 38.97 | ||||

| Total income (loss) |

(3.70 | ) | (8.12 | ) | ||||

| Total expenses |

(0.19 | ) | (0.19 | ) | ||||

|

|

|

|

|

|||||

| Net decrease in net asset value |

(3.89 | ) | (8.31 | ) | ||||

|

|

|

|

|

|||||

| Net asset value, end of period |

$ | 34.18 | $ | 30.66 | ||||

|

|

|

|

|

|||||

| Total Return |

(10.22 | )% | (21.32 | )% | ||||

|

|

|

|

|

|||||

| Ratios to Average Net Assets |

||||||||

| Total income (loss) |

(8.30 | )% | (7.80 | )% | ||||

|

|

|

|

|

|||||

| Expenses excluding management fees* |

0.25 | % | 0.20 | % | ||||

|

|

|

|

|

|||||

| Management fees* |

0.45 | % | 0.45 | % | ||||

|

|

|

|

|

|||||

| Net income (loss) |

(8.82 | )% | (8.29 | )% | ||||

|

|

|

|

|

|||||

| * | Annualized |

Total returns are calculated based on the change in value during the period. An individual unitholder’s total return and ratio may vary from the above total returns and ratios based on the timing of contributions to and withdrawals from USOF.

NOTE 7 — FAIR VALUE OF FINANCIAL INSTRUMENTS

USOF values its investments in accordance with Accounting Standards Codification 820 – Fair Value Measurements and Disclosures (“ASC 820”). ASC 820 defines fair value, establishes a framework for measuring fair value in generally accepted accounting principles, and expands disclosures about fair value measurement. The changes to past practice resulting from the application of ASC 820 relate to the definition of fair value, the methods used to measure fair value, and the expanded disclosures about fair value measurement. ASC 820 establishes a fair value hierarchy that distinguishes between: (1) market participant assumptions developed based on market data obtained from sources independent of USOF (observable inputs) and (2) USOF’s own assumptions about market participant assumptions developed based on the best information available under the circumstances (unobservable inputs). The three levels defined by the ASC 820 hierarchy are as follows:

Level I – Quoted prices (unadjusted) in active markets for identical assets or liabilities that the reporting entity has the ability to access at the measurement date.

13

Table of Contents

Level II – Inputs other than quoted prices included within Level I that are observable for the asset or liability, either directly or indirectly. Level II assets include the following: quoted prices for similar assets or liabilities in active markets, quoted prices for identical or similar assets or liabilities in markets that are not active, inputs other than quoted prices that are observable for the asset or liability, and inputs that are derived principally from or corroborated by observable market data by correlation or other means (market-corroborated inputs).

Level III – Unobservable pricing input at the measurement date for the asset or liability. Unobservable inputs shall be used to measure fair value to the extent that observable inputs are not available.

In some instances, the inputs used to measure fair value might fall within different levels of the fair value hierarchy. The level in the fair value hierarchy within which the fair value measurement in its entirety falls shall be determined based on the lowest input level that is significant to the fair value measurement in its entirety.

The following table summarizes the valuation of USOF’s securities at September 30, 2012 using the fair value hierarchy:

| At September 30, 2012 | Total | Level I | Level II | Level III | ||||||||||||

| Short-Term Investments |

$ | 896,242,884 | $ | 896,242,884 | $ | — | $ | — | ||||||||

| Exchange-Traded Futures Contracts |

||||||||||||||||

| Foreign Contracts |

(9,110,000 | ) | (9,110,000 | ) | — | — | ||||||||||

| United States Contracts |

(40,941,830 | ) | (40,491,830 | ) | — | — | ||||||||||

| During the nine months ended September 30, 2012, there were no transfers between Level I and Level II. | ||||||||||||||||

| The following table summarizes the valuation of USOF’s securities at December 31, 2011 using the fair value hierarchy: |

||||||||||||||||

| At December 31, 2011 | Total | Level I | Level II | Level III | ||||||||||||

| Short-Term Investments |

$ | 746,071,600 | $ | 746,071,600 | $ | — | $ | — | ||||||||

| Exchange-Traded Futures Contracts |

||||||||||||||||

| Foreign Contracts |

(2,475,000 | ) | (2,475,000 | ) | — | — | ||||||||||

| United States Contracts |

(3,997,310 | ) | (3,997,310 | ) | — | — | ||||||||||

During the year ended December 31, 2011, there were no transfers between Level I and Level II.

Effective January 1, 2009, USOF adopted the provisions of Accounting Standards Codification 815 – Derivatives and Hedging, which require presentation of qualitative disclosures about objectives and strategies for using derivatives, quantitative disclosures about fair value amounts and gains and losses on derivatives.

Fair Value of Derivative Instruments

| Derivatives not Accounted for as Hedging Instruments |

Condensed Statements of Financial Condition Location |

Fair

Value At September 30, 2012 |

Fair

Value At December 31, 2011 |

|||||||

| Futures - Commodity Contracts |

Assets | $ | (50,051,830 | ) | $ | (6,472,310 | ) | |||

14

Table of Contents

The Effect of Derivative Instruments on the Condensed Statements of Operations

| For the nine months ended September 30, 2012 |

For the nine months ended September 30, 2011 |

|||||||||||||||||

| Derivatives not Accounted for as Hedging Instruments |

Location of Gain or (Loss) on Derivatives Recognized in Income |

Realized Gain or (Loss) on Derivatives Recognized in Income |

Change in Unrealized Gain or (Loss) on Derivatives Recognized in Income |

Realized Gain or (Loss) on Derivatives Recognized in Income |

Change in Unrealized Gain or (Loss) on Derivatives Recognized in Income |

|||||||||||||

| Futures - Commodity Contracts |

Realized gain (loss) on closed positions | $ | (62,348,970 | ) | $ | 39,659,420 | ||||||||||||

| Change in unrealized loss on open positions | $ | (43,579,520 | ) | $ | (165,561,060 | ) | ||||||||||||

NOTE 8 — RECENT ACCOUNTING PRONOUNCEMENTS

In December 2011, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) No. 2011-11, “Balance Sheet (Topic 210): Disclosures about Offsetting Assets and Liabilities.” The amendments in ASU No. 2011-11 require an entity to disclose information about offsetting and related arrangements to enable users of its financial statements to understand the effect of those arrangements on its financial position. ASU No. 2011-11 is effective for annual reporting periods beginning on or after January 1, 2013, and interim periods within those annual periods. The guidance requires retrospective application for all comparative periods presented. USCF is currently evaluating the impact ASU No. 2011-11 will have on USOF’s financial statements.

NOTE 9 — SUBSEQUENT EVENTS

USOF has performed an evaluation of subsequent events through the date the financial statements were issued. This evaluation did not result in any subsequent events that necessitated disclosures and/or adjustments.

15

Table of Contents

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations. |

The following discussion should be read in conjunction with the condensed financial statements and the notes thereto of the United States Oil Fund, LP (“USOF”) included elsewhere in this quarterly report on Form 10-Q.

Forward-Looking Information

This quarterly report on Form 10-Q, including this “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” contains forward-looking statements regarding the plans and objectives of management for future operations. This information may involve known and unknown risks, uncertainties and other factors that may cause USOF’s actual results, performance or achievements to be materially different from future results, performance or achievements expressed or implied by any forward-looking statements. Forward-looking statements, which involve assumptions and describe USOF’s future plans, strategies and expectations, are generally identifiable by use of the words “may,” “will,” “should,” “expect,” “anticipate,” “estimate,” “believe,” “intend” or “project,” the negative of these words, other variations on these words or comparable terminology. These forward-looking statements are based on assumptions that may be incorrect, and USOF cannot assure investors that the projections included in these forward-looking statements will come to pass. USOF’s actual results could differ materially from those expressed or implied by the forward-looking statements as a result of various factors.

USOF has based the forward-looking statements included in this quarterly report on Form 10-Q on information available to it on the date of this quarterly report on Form 10-Q, and USOF assumes no obligation to update any such forward-looking statements. Although USOF undertakes no obligation to revise or update any forward-looking statements, whether as a result of new information, future events or otherwise, investors are advised to consult any additional disclosures that USOF may make directly to them or through reports that USOF in the future files with the U.S. Securities and Exchange Commission (the “SEC”), including annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K.

Introduction

USOF, a Delaware limited partnership, is a commodity pool that issues units that may be purchased and sold on the NYSE Arca, Inc. (the “NYSE Arca”). The investment objective of USOF is for the daily changes in percentage terms of its units’ per unit net asset value (“NAV”) to reflect the daily changes in percentage terms of the spot price of light, sweet crude oil delivered to Cushing, Oklahoma, as measured by the daily changes in the price of the futures contract for light, sweet crude oil traded on the New York Mercantile Exchange (the “NYMEX”) that is the near month contract to expire, except when the near month contract is within two weeks of expiration, in which case it will be measured by the futures contract that is the next month contract to expire (the “Benchmark Oil Futures Contract”), less USOF’s expenses. “Near month contract” means the next contract traded on the NYMEX due to expire. “Next month contract” means the first contract traded on the NYMEX due to expire after the near month contract. It is not the intent of USOF to be operated in a fashion such that the per unit NAV will equal, in dollar terms, the spot price of light, sweet crude oil or any particular futures contract based on light, sweet crude oil. It is not the intent of USOF to be operated in a fashion such that its per unit NAV will reflect the percentage change of the price of any particular futures contract as measured over a time period greater than one day. The general partner of USOF, United States Commodity Funds LLC (“USCF”), believes that it is not practical to manage the portfolio to achieve such an investment goal when investing in Oil Futures Contracts (as defined below) and Other Oil-Related Investments (as defined below).

USOF invests in futures contracts for light, sweet crude oil, other types of crude oil, heating oil, gasoline, natural gas and other petroleum-based fuels that are traded on the NYMEX, ICE Futures or other U.S. and foreign exchanges (collectively, “Oil Futures Contracts”) and other oil interests such as cash-settled options on Oil Futures Contracts, forward contracts for oil, cleared swap contracts and over-the-counter transactions that are based on the price of crude oil, other petroleum-based fuels, Oil Futures Contracts and indices based on the foregoing (collectively, “Other Oil-Related Investments”). For convenience and unless otherwise specified, Oil Futures Contracts and Other Oil-Related Investments collectively are referred to as “Oil Interests” in this quarterly report on Form 10-Q.

USOF seeks to achieve its investment objective by investing in a combination of Oil Futures Contracts and Other Oil-Related Investments such that daily changes in its per unit NAV, measured in percentage terms, will closely track the daily changes in the price of the Benchmark Oil Futures Contract, also measured in percentage terms. USCF believes the daily changes in the price of the Benchmark Oil Futures Contract have historically exhibited a close correlation with the daily changes in the spot price of light, sweet crude oil. It is not the intent of USOF to be operated in a fashion such that the per unit NAV will equal, in dollar terms, the spot price of light, sweet crude oil or any particular futures contract based on light, sweet crude oil. It is not the intent of USOF to be operated in a fashion such that its per unit NAV will reflect the percentage change of the price of any particular futures contract as measured over a time period greater than one day. USCF believes that it is not practical to manage the portfolio to achieve such an investment goal when investing in Oil Futures Contracts and Other Oil-Related Investments.

16

Table of Contents

Regulatory Disclosure

Impact of Accountability Levels, Position Limits and Price Fluctuation Limits. Futures contracts include typical and significant characteristics. Most significantly, the Commodity Futures Trading Commission (the “CFTC”) and U.S. designated contract markets such as the NYMEX have established accountability levels and position limits on the maximum net long or net short futures contracts in commodity interests that any person or group of persons under common trading control (other than as a hedge, which an investment in USOF is not) may hold, own or control. The net position is the difference between an individual’s or firm’s open long contracts and open short contracts in any one commodity. In addition, most U.S.-based futures exchanges, such as the NYMEX, limit the daily price fluctuation for futures contracts. Currently, the ICE Futures imposes position and accountability limits that are similar to those imposed by U.S.-based futures exchanges and also limits the maximum daily price fluctuation, while some other non-U.S. futures exchanges have not adopted such limits.

The accountability levels for the Benchmark Oil Futures Contract and other Oil Futures Contracts traded on U.S.-based futures exchanges, such as the NYMEX, are not a fixed ceiling, but rather a threshold above which the NYMEX may exercise greater scrutiny and control over an investor’s positions. The current accountability level for investments for any one month in the Benchmark Oil Futures Contract is 10,000 contracts. In addition, the NYMEX imposes an accountability level for all months of 20,000 net futures contracts for light, sweet crude oil. In addition, the ICE Futures maintains the same accountability levels, position limits and monitoring authority for its light, sweet crude oil contract as the NYMEX. If USOF and the Related Public Funds (as defined below) exceed these accountability levels for investments in the futures contracts for light, sweet crude oil, the NYMEX and ICE Futures will monitor such exposure and may ask for further information on their activities including the total size of all positions, investment and trading strategy, and the extent of liquidity resources of USOF and the Related Public Funds. If deemed necessary by the NYMEX and/or ICE Futures, USOF could be ordered to reduce its aggregate position back to the accountability level. As of September 30, 2012, USOF held 10,272 futures contracts for light, sweet crude oil traded on the NYMEX and 2,000 Oil Futures Contracts traded on the ICE Futures. USOF exceeded accountability levels of the NYMEX during the nine months ended September 30, 2012, when it held a maximum of 13,918 Crude Oil Futures CL contracts, exceeding the “any” month limit. No action was taken by the NYMEX and USOF did not reduce the number of Futures Contracts held as a result. USOF did not exceed any accountability levels imposed by ICE Futures for the nine months ended September 30, 2012.

Position limits differ from accountability levels in that they represent fixed limits on the maximum number of future contracts that any person may hold and cannot allow such limits to be exceeded without express CFTC authority to do so. In addition to accountability levels and position limits that may apply at any time, the NYMEX and ICE Futures impose position limits on contracts held in the last few days of trading in the near month contract to expire. It is unlikely that USOF will run up against such position limits because USOF’s investment strategy is to close out its positions and “roll” from the near month contract to expire to the next month contract during a four-day period beginning two weeks from expiration of the contract. For the nine months ended September 30, 2012, USOF did not exceed any position limits imposed by the NYMEX and ICE Futures.

The regulation of commodity interests in the United States is subject to ongoing modification by governmental and judicial action. On July 21, 2010, a broad financial regulatory reform bill, the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”), was signed into law. All of the Dodd-Frank Act’s provisions became effective on July 16, 2011, but the actual implementation of some of the provisions is subject to continuing uncertainty because implementing rules and regulations have not been completely finalized and have been challenged in court. Pending final resolution of all applicable regulatory requirements, some specific examples of how the new Dodd-Frank Act provisions and rules adopted thereunder could impact USOF are discussed below.

17

Table of Contents

Futures Contracts and Position Limits

Provisions in the Dodd-Frank Act include the requirement that position limits be established on a wide range of commodity interests including energy-based and other commodity futures contracts, certain cleared commodity swaps and certain over-the-counter commodity contracts; new registration, recordkeeping, capital and margin requirements for “swap dealers” and “major swap participants” as determined by the new law and applicable regulations; and the forced use of clearinghouse mechanisms for many swap transactions that are currently entered into in the over-the-counter market. The new law and the rules thereunder may negatively impact USOF’s ability to meet its investment objective either through limits or requirements imposed on it or upon its counterparties. Further, increased regulation of, and the imposition of additional costs on, swap transactions under the new legislation and implementing regulations could cause a reduction in the swap market and the overall derivatives markets, which could restrict liquidity and adversely affect USOF. In particular, new position limits imposed on USOF or its counterparties may impact USOF’s ability to invest in a manner that most efficiently meets its investment objective, and new requirements, including capital and mandatory clearing, may increase the cost of USOF’s investments and doing business, which could adversely impact the ability of USOF to achieve its investment objective.

In late 2011, the CFTC adopted regulations implementing position limits and limit formulas for 28 core physical commodity futures contracts, including the Oil Futures Contracts and options on Oil Futures Contracts executed pursuant to the rules of designated contract markets (i.e., certain regulated exchanges) and commodity swaps that are economically equivalent to such futures and options contracts (collectively, “Referenced Contracts”). These regulations would have required, among other things, aggregation of position limits that would apply across different trading venues to contracts based on the same underlying commodity. However, the regulations would have required aggregation of Referenced Contracts held by separate Related Public Funds (as defined below) only if such Related Public Funds had “identical trading strategies.” USCF does not believe any of the Related Public Funds should be viewed as having identical trading strategies for purposes of the CFTC’s aggregation rules.

The position limit rules were to be implemented in two phases, the first of which was to be effective October 12, 2012. However, on September 28, 2012, the U.S. District Court for the District of Columbia issued a memorandum opinion and order vacating the final regulations. The court issued that ruling in response to a lawsuit filed by two industry organizations challenging certain aspects of the regulations. There is no way of knowing whether the CFTC will ultimately be successful in adopting position limit rules, how those rules might differ from existing position limits imposed by applicable designated contract markets, and, accordingly, whether any such rules would negatively impact the ability of USOF to achieve its objectives.

“Swap” Transactions

The Dodd-Frank Act imposes new regulatory requirements on certain “swap” transactions that USOF is authorized to engage in that may ultimately impact the ability of USOF to meet its investment objective. On August 13, 2012, the CFTC and the SEC published joint final rules defining the terms “swap” and “security-based swaps.” The term “swap” is broadly defined to include various types of over-the-counter derivatives, including swaps and options. The effective date of these final rules was October 12, 2012.

The Dodd-Frank Act requires that certain transactions ultimately falling within the definition of “swap” be executed on organized exchanges or “swap execution facilities” and cleared through regulated clearing organizations (which are referred to in the Dodd-Frank Act as “derivative clearing organizations” (“DCOs”)), if the CFTC mandates the central clearing of a particular contract. However, the CFTC has not issued any mandatory clearing determinations and, therefore, it is currently unknown which swaps will be subject to such trading and clearing requirements. If a swap is required to be cleared, the initial margin will be set by the clearing organization, subject to certain regulatory requirements and guidelines. Initial and variation margin requirements for swap dealers and major swap participants who enter into uncleared swaps and capital requirements for swap dealers and major swap participants who enter into both cleared and uncleared trades will be set by the CFTC, the SEC or the applicable “Prudential Regulator.” On May 23, 2012, the CFTC published final regulations, which became effective as of July 23, 2012, to determine which entities will be regulated as “swap dealers” and “major swap participants” and thus have to comply with these capital and margin requirements (as well as a multitude of other requirements under the Dodd-Frank Act). Most of the requirements became effective on October 12, 2012 when additional final rules defining the terms “swap,” “security-based swap” and “mixed swap” became effective. However, on October 11, 2012 and October 12, 2012, the CFTC issued several no-action letters and interpretative guidance which delayed much of the implementation of these requirements from October 12, 2012 until December 31, 2012. Increased regulation of, and the imposition of additional costs on, swap transactions could have an adverse effect on USOF by, for example, reducing the size of and therefore liquidity in the derivatives market, increasing transaction costs and decreasing the ability to customize derivative transactions.

18

Table of Contents

The majority of the Dodd-Frank Act regulations affecting the swap market will not become effective until later in calendar year 2012 or the beginning of 2013 at the earliest.

On February 7, 2012, the CFTC published a rule requiring each futures commission merchant (“FCM”) and DCO to segregate cleared swaps and related collateral posted by a customer of the FCM from the assets of the FCM or DCO, although such property can be commingled with the property of other cleared swaps customers of the FCM or DCO. This rule addresses losses incurred by a DCO in a so-called “double default” scenario in which a customer of an FCM defaults in its obligations to the FCM and the FCM, in turn, defaults in its obligations to the DCO. Under this scenario, the DCO can only access the collateral attributable to other customers of the DCO whose cleared swap positions are in a loss position following the primary customer’s default. This rule is scheduled to become effective on November 8, 2012. Some market participants have expressed concern that the requirements of this segregation rule may result in higher initial margins or higher fees. USOF does not anticipate any impact to its operations in order to meet the requirements of the new rule.

Additionally, the CFTC published rules on February 17, 2012 and April 3, 2012 that require “swap dealers” and “major swap participants” to: 1) adhere to business conduct standards, 2) implement policies and procedures to ensure compliance with the Commodity Exchange Act and 3) maintain records of such compliance. These new requirements may impact the documentation requirements for both cleared and non-cleared swaps and cause swap dealers and major swap participants to face increased compliance costs that, in turn, may be passed along to counterparties (such as USOF) in the form of higher fees and expenses that related to trading swaps.

On February 24, 2012, the CFTC amended certain disclosure obligations to require that the operator of a commodity pool that invests in swaps include standardized swap risk disclosures in the pool’s disclosure documents by December 31, 2012.

The CFTC issued a final rule on May 23, 2012 interpreting the definition of “eligible contract participant,” as amended by the Dodd-Frank Act, in such a manner that USOF may be limited as to the counterparties with which it may enter into forward contracts. Additionally, USOF may under certain circumstances related to the amount of assets under management no longer qualify as an eligible contract participant. USOF’s ability to maintain a certain minimum level of assets and to qualify as an eligible contract participant allows USOF to enter into swaps on swap execution facilities as well as on a bilateral, off-exchange basis. The loss of status as an eligible contract participant and the resulting loss of eligible counterparties and investment options could impact USOF’s ability to achieve its investment objective.

The effect of the future regulatory change on USOF is impossible to predict, but it could be substantial and adverse.

USCF, which is registered as a commodity pool operator (“CPO”) with the CFTC, is authorized by the Fifth Amended and Restated Agreement of Limited Partnership of USOF (the “LP Agreement”) to manage USOF. USCF is authorized by USOF in its sole judgment to employ and establish the terms of employment for, and termination of, commodity trading advisors or FCMs.

Price Movements

Crude oil futures prices were volatile during the nine months ended September 30, 2012 and exhibited moderate daily swings along with an uneven downward trend during the period. The price of the Benchmark Oil Futures Contract started the period at $98.83 per barrel. The low of the period was on June 28, 2012 when the price dropped to $77.69 per barrel. The high of the period was on February 24, 2012 when the price reached $109.77 per barrel. The period ended with the Benchmark Oil Futures Contract at $92.19 per barrel, down approximately 6.72% over the period. USOF’s per unit NAV began the period at $38.07 and ended the period at $34.18 on September 30, 2012, a decrease of approximately 10.22% over the period. USOF’s per unit NAV reached its high for the period on February 24, 2012 at $42.00 and reached its low for the period on June 28, 2012 at $29.17. The Benchmark Oil Futures Contract prices listed above began with the February 2012 contracts and ended with the November 2012 contracts. The decrease of approximately 6.72% on the Benchmark Oil Futures Contract listed above is a hypothetical return only and could not actually be achieved by an investor holding Oil Futures Contracts. An investment in Oil Futures Contracts would need to be rolled forward during the time period described in order to simulate such a result. Furthermore, the change in the nominal price of these differing crude Oil Futures Contracts, measured from the start of the period to the end of the period, does not represent the actual benchmark results that USOF seeks to track, which are more fully described below in the section titled “Tracking USOF’s Benchmark.”

19

Table of Contents

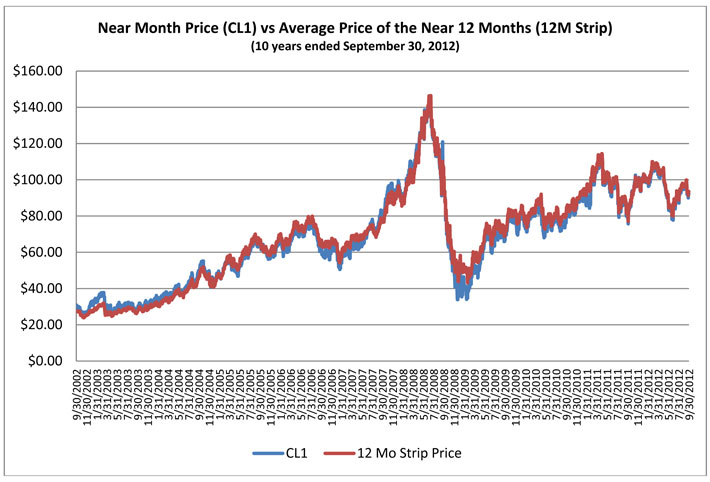

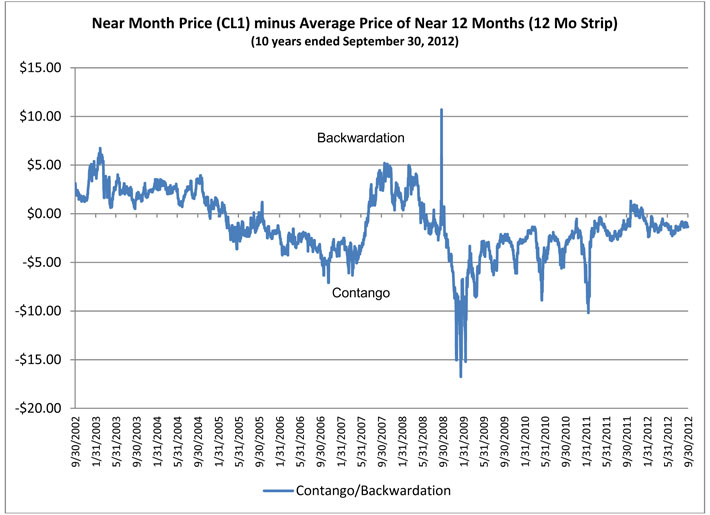

During the nine months ended September 30, 2012, the level of contango remained mild, meaning that the price of the near month crude Oil Futures Contract was less than the price of the next month crude Oil Futures Contract, or contracts further away from expiration. Crude oil inventories, which reached historic levels in January 2009 and February 2009 and which appeared to be the primary cause of the steep level of contango, began to drop in March 2009 and continued to drop for the remainder of 2009 and the beginning of 2010. During the year ended December 31, 2011, crude oil inventories began to climb higher, which contributed to the crude oil futures market remaining in contango through the end of December 2011. During the nine months ended September 30, 2012, crude oil inventories maintained present levels, which contributed to the crude oil futures market remaining in contango through the end of September 2012. For a discussion of the impact of backwardation and contango on total returns, see “Term Structure of Crude Oil Prices and the Impact on Total Returns” below.

Valuation of Oil Futures Contracts and the Computation of the Per Unit NAV

The per unit NAV of USOF’s units is calculated once each NYSE Arca trading day. The per unit NAV for a particular trading day is released after 4:00 p.m. New York time. Trading during the core trading session on the NYSE Arca typically closes at 4:00 p.m. New York time. USOF’s administrator uses the NYMEX closing price (determined at the earlier of the close of the NYMEX or 2:30 p.m. New York time) for the contracts held on the NYMEX, but calculates or determines the value of all other USOF investments, including ICE Futures contracts or other futures contracts, as of the earlier of the close of the NYSE Arca or 4:00 p.m. New York time.

Results of Operations and the Crude Oil Market

Results of Operations. On April 10, 2006, USOF listed its units on the American Stock Exchange (the “AMEX”) under the ticker symbol “USO.” On that day, USOF established its initial offering price at $67.39 per unit and issued 200,000 units to the initial authorized purchaser, KV Execution Services LLC, in exchange for $13,479,000 in cash. As a result of the acquisition of the AMEX by NYSE Euronext, USOF’s units no longer trade on the AMEX and commenced trading on the NYSE Arca on November 25, 2008.

Since its initial offering of 17,000,000 units, USOF has registered seven subsequent offerings of its units: 30,000,000 units which were registered with the SEC on October 18, 2006, 50,000,000 units which were registered with the SEC on January 30, 2007, 30,000,000 units which were registered with the SEC on December 4, 2007, 100,000,000 units which were registered with the SEC on February 7, 2008, 100,000,000 units which were registered with the SEC on September 29, 2008, 300,000,000 units which were registered with the SEC on January 16, 2009 and 1,000,000,000 units which were registered with the SEC on June 29, 2009. Units offered by USOF in the subsequent offerings were sold by it for cash at the units’ per unit NAV as described in the applicable prospectus. As of September 30, 2012, USOF had issued 779,600,000 units, 33,100,000 of which were outstanding. As of September 30, 2012, there were 847,400,000 units registered but not yet issued.

More units may have been issued by USOF than are outstanding due to the redemption of units. Unlike funds that are registered under the Investment Company Act of 1940, as amended, units that have been redeemed by USOF cannot be resold by USOF. As a result, USOF contemplates that additional offerings of its units will be registered with the SEC in the future in anticipation of additional issuances and redemptions.

As of September 30, 2012, USOF had the following authorized purchasers: ABN Amro, Banc of America Securities LLC, Citigroup Global Markets Inc., Credit Suisse USA, Deutsche Bank Securities Inc., Fimat USA LLC, Goldman Sachs & Company, Goldman Sachs Execution & Clearing LP, JP Morgan Securities Inc., Merrill Lynch Professional Clearing Corp., Morgan Stanley & Company Inc., Nomura Securities International Inc., Pru Global Securities, LLC, RBC Capital Markets Corporation, SG Americas Securities LLC, Timber Hill LLC, Virtu Financial Capital Markets, Virtu Financial DB LLC and Wedbush Securities Inc.

For the Nine Months Ended September 30, 2012 Compared to the Nine Months Ended September 30, 2011

As of September 30, 2012, the total unrealized loss on Oil Futures Contracts owned or held on that day was $50,051,830 and USOF established cash deposits and investments in short term obligations of the United States of two years or less (“Treasuries”) and money market funds that were equal to $1,137,901,137. USOF held 74.37% of its cash assets in overnight deposits and money market funds at its custodian bank, while 25.63% of the cash balance was held as investments in Treasuries and margin deposits for the Oil Futures Contracts purchased. The ending per unit NAV on September 30, 2012 was $34.18.

20

Table of Contents