Attached files

| file | filename |

|---|---|

| 8-K - CURRENT REPORT OF MATERIAL EVENTS OR CORPORATE CHANGES - Monogram Residential Trust, Inc. | a12-19400_18k.htm |

Exhibit 99.1

|

|

The Reserve at La Vista Walk in Atlanta, GA Behringer Harvard Multifamily REIT I, Inc. Update Call |

|

|

Forward-Looking Statements This presentation contains forward-looking statements, including discussion and analysis of the financial condition of Behringer Harvard Multifamily REIT I, Inc. (the “REIT”) and its subsidiaries and other matters. These forward-looking statements are not historical facts but are the intent, belief or current expectations of the REIT’s management based on their knowledge and understanding of the REIT’s business and industry. Words such as “may,” “anticipates,” “expects,” “intends,” “plans,” “believes,” “seeks,” “estimates,” “would,” “could,” “should” and variations of these words and similar expressions are intended to identify forward-looking statements. We intend that such forward-looking statements be subject to the safe harbor provisions created by Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). These statements are not guarantees of future performance and are subject to risks, uncertainties and other factors, some of which are beyond our control, are difficult to predict and could cause actual results to differ materially from those expressed or forecasted in the forward-looking statements. Forward-looking statements that were true at the time made may ultimately prove to be incorrect or false. We caution you not to place undue reliance on forward-looking statements, which reflect the REIT’s management's view only as of the date of this presentation. We undertake no obligation to update or revise forward-looking statements to reflect changed assumptions the occurrence of unanticipated events or changes to future operating results. |

|

|

Forward-Looking Statements Factors that could cause actual results to vary materially from any forward-looking statements made in this presentation include, but are not limited to: absence of a public market for the REIT’s securities; limited operating history; limited transferability and lack of liquidity; risks associated with lending activities ; no assurance that distributions will continue to be made or that any particular rate of distribution will be maintained; until the proceeds from an offering are invested and generating cash flow from operating activities, some or all of the distributions will be paid from other sources, which may be deemed a return of capital, such as from the proceeds of an offering, cash advances by the advisor, cash resulting from a waiver of asset management fees, proceeds from the sales of assets, and borrowings in anticipation of future cash flow from operating activities, which could result in less proceeds to make investments in real estate; reliance on the program’s advisor; payment of significant fees to the advisor and their affiliates ; potential conflicts of interest; lack of diversification in property holdings; Market and economic challenges experienced by the U.S. economy or real estate industry as a whole and the local economic conditions in the markets in which our properties are located; the REIT’s ability to make accretive investments in a diversified portfolio of assets; Availability of cash flow from operating activities for distribution; the REIT’s level of debt and the terms and limitations imposed on the REIT by its debt agreements; the availability of credit generally, and any failure to obtain debt financing at favorable terms or a failure to satisfy the conditions and requirements of that debt; the ability to secure resident leases at favorable rental rates; the ability to raise future capital through equity and debt security offerings and through joint venture arrangements; the ability to retain our executive officers and other key personnel of our advisor, our property manager and their affiliates; conflicts of interest arising out of our relationships with our advisor and its affiliates; unfavorable changes in laws or regulations impacting our business, our assets or our key relationships; factors that could affect our ability to qualify as a real estate investment trust; potential development risks and construction delays; the potential inability to retain current tenants and attract new tenants due to a competitive real estate market; risk that a program’s operating results will be affected by economic and regulatory changes that have an adverse impact on a program’s investments; risks related to investments in distressed properties or debt include possible default under the original loan; unforeseen increases in operating and capital expenses; declines in real estate values; and, lack of availability of due diligence information. These risks may impact the REIT’s financial condition, operating results, returns to its shareholders, and ability to make distributions as stated in the REIT’s offering. Investment in securities of Behringer Harvard real estate programs is subject to substantial risks and may result in the loss of principal invested. Real Estate programs are not suitable for all investors. The forward looking statements should be read in light of these and other risk factors identified in the “Risk Factors” section of the REIT’s Quarterly Report on Form 10-Q for the quarter ended June 30, 2012 and our Annual Report on Form 10-K for the year ended December 31, 2011, as filed with the Securities and Exchange Commission. |

|

|

Questions? During the call, please e-mail questions to: bhreit@behringerharvard.com |

|

|

Today’s Presenters Robert S. Aisner Chief Executive Officer Mark T. Alfieri Chief Operating Officer Howard S. Garfield Chief Financial Officer |

|

|

The Economy: July 2012 Sources: Bureau of Economic Analysis, Bureau of Labor Statistics, Thomson Reuters/University of Michigan Surveys of Consumers Second Quarter 2012 U.S. economy added 952,000 private sector jobs in the first half of 2012, but gains slowed significantly in the Q2 compared to Q1 The U.S. economy slowed in the second quarter amid a slowdown in consumer spending, government cuts, and employment gains European debt crisis and fear of contagion remains at the forefront Spain, the euro area’s fourth-largest economy, has seen the ten-year government bond yields reach 7.75%; unemployment climbs to an all-time high in second quarter to 24.6% U.S. Q2 2012, GDP +1.7% (revised estimate) U.S. Unemployment Rate: 8.2% (June 2012) The Consumer Thomson Reuters/University of Michigan consumer sentiment index: 72.3 (July 2012) News reports about recent economic developments - including a slowdown in job growth - reaching consumers has become increasingly negative. |

|

|

Consumer Sentiment Summer Reversal Used with permission from Doug Short |

|

|

Post-Recession Employment Slowly Recovering |

|

|

Leading Indicators Improving at Moderate Pace Source: Conference Board, National Bureau of Economic Research, Bloomberg Index (2004=100) Recessions The Conference Board Leading Economic Index® The Conference Board Coincident Economic Index® ® Registered Trademark of The Conference Board Inc. |

|

|

Occupancy, Effective Rent Growth Stay Above Trend Used with permission from Witten Advisors LLC. Source: Witten Advisors 85% 90% 95% 100% 1Q 1995 1Q 1996 1Q 1997 1Q 1998 1Q 1999 1Q 2000 1Q 2001 1Q 2002 1Q 2003 1Q 2004 1Q 2005 1Q 2006 1Q 2007 1Q 2008 1Q 2009 1Q 2010 1Q 2011 1Q 2012 Occupancy -5% 0% 5% 10% Year-Year Effective Rent Growth Occupancy Rent Growth +4.7% (+4.5% forecast) 94.6% (94.5% forecast) |

|

|

Effective Rents Still Rising in (almost) All Markets Rent Increase Leaders 12 Months ending 1Q 2012 San Francisco 13.1% San Jose 11.7% Oakland 7.4% Boston 6.6% Denver 6.5% Austin 6.4% Charlotte 6.3% Seattle 5.8% New York 5.5% Miami 5.4% Rent Increase Laggards 12 Months ending 1Q 2012 Fort Lauderdale 3.2% Tampa 2.9% Riverside 2.8% St. Louis 2.7% Phoenix 2.4% Sacramento 2.4% San Diego 2.2% Jacksonville 1.6% Norfolk 1.1% Las Vegas -0.1% U.S. +4.7% Used with permission from Witten Advisors LLC. Source: Witten Advisors |

|

|

Multifamily Starts Rising But Moderate Through May Source: U.S. Department of Commerce Used with permission from Witten Advisors LLC. “U.S. home building slowed in May amid a pull back in multifamily construction” – WSJ, June 19 210 258 0 100 200 300 400 500 600 700 Jan-90 Jan-95 Jan-00 Jan-05 Jan-10 All 5+ Multifamily Units (monthly data, annualized, 000) Annualized Starts Rate, SA Annualized Permits Rate, SA 3-Month Average Starts Rate 3-Month Average Permits Rate |

|

|

Q1 Apartment Starts Rate* Still Low in Many Markets Source: Witten Advisors *Starts rate = last 12 months’ starts as % of existing apartment stock Used with permission from Witten Advisors LLC. W Palm Beach Washington DC San Jose Baltimore Nashville Seattle Fort Worth Denver Houston Charlotte Columbus Austin Raleigh Norfolk Dallas San Antonio Salt Lake City 0.0% 1.0% 2.0% 3.0% 4.0% Austin Raleigh Norfolk Dallas San Antonio Salt Lake City Houston Charlotte Columbus W Palm Beach Washington DC San Jose Baltimore Nashville Seattle Fort Worth Denver Orange County Portland Riverside San Francisco Indianapolis Fort Lauderdale Tampa Los Angeles San Diego Atlanta Orlando Oakland Boston Jacksonville Phoenix Kansas City Las Vegas Minneapolis Miami St. Louis Chicago Sacramento NYC Philadelphia Cincinnati Detroit Metro Starts Rate U.S. |

|

|

Our Strategy Grow revenues and NOI through proactive property management Completed transition from 3rd party management Active management positively impacting NOI Acquire quality multifamily assets in institutional markets Emphasis on urban locations, highly amenitized Higher rents per unit Greater potential for value growth Execute development program Acquire new investments at cost Higher going-in yield than many stabilized acquisitions |

|

|

Portfolio Characteristics 48 Investments* 36 Operating Properties 8 Developments 4 Mezzanine and Land Loans * Includes investments made subsequent to June 30, 2012. Units by Region Florida 7% Georgia 4% Mid-Atlantic 12% Midwest 2% Mountain 14% New England 8% Northern CA 8% Northwest 5% Southern CA 8% Texas 32% |

|

|

Rental Income Growth – YTD 2011 vs 2012 |

|

|

Same Store Revenue Trends There were 28 stabilized comparable properties in the 2nd quarter year over year comparison. There were 35 stabilized comparable properties in the quarterly comparison between 1st and 2nd quarter 2012. 3% Increase $ millions $ millions |

|

|

Same Store Occupancy Trends There were 28 stabilized comparable properties in the 2nd quarter year over year comparison. There were 35 stabilized comparable properties in the quarterly comparison between 1st and 2nd quarter 2012. |

|

|

Same Store Net Operating Income* Trends 4% Increase *Reconciliations of Income (Loss) from continuing operations to same store Combined Net Operating Income can be found in the Current Report on Form 8-K filed on August 30, 2012 with the Securities and Exchange Commission. A copy of this filing is available on our website www.behringerharvard.com There were 28 stabilized comparable properties in the 2nd quarter year over year comparison. There were 35 stabilized comparable properties in the quarterly comparison between 1st and 2nd quarter 2012. $ millions $ millions |

|

|

Performance Comparison with Exchange Listed Apartment REITs Same Store Q2 2012 vs Q1 2012 YTD 2012 vs YTD 2011 Q2 2012 vs Q2 2011 Company Name Ticker SS Revenue Change (%) SS Expense Change (%) SS NOI Change (%) SS Revenue Change (%) SS Expense Change (%) SS NOI Change (%) SS Revenue Change (%) SS Expense Change (%) SS NOI Change (%) Associated Estates AEC 2.5 2.6 2.4 5.8 4.0 7.1 5.9 6.4 5.5 AIMCO* AIV 1.0 0.6 1.2 4.4 1.0 6.3 4.6 2.4 5.9 Avalon Bay AVB 1.5 1.3 1.6 6.2 0.8 8.7 5.8 3.0 7.1 BRE Properties BRE 1.4 1.1 1.5 5.5 4.0 6.2 5.1 4.1 5.6 Camden CPT 2.2 1.9 2.4 6.4 2.3 9.1 6.1 2.1 8.6 Equity Residential EQR 2.4 -2.1 4.9 5.5 1.9 7.5 5.5 2.0 7.5 Essex ESS 1.0 4.0 -0.4 6.7 0.0 10.2 6.3 0.8 9.2 Home Properties HME -0.4 -6.1 3.1 4.7 -1.6 8.9 4.8 -0.3 8.0 Mid-America MAA 1.5 1.1 1.8 4.5 3.2 5.5 4.6 1.9 6.5 Post Properties PPS 2.5 2.4 2.5 7.8 3.5 10.7 7.8 3.9 10.4 UDR UDR 2.0 2.5 1.8 5.5 1.6 7.4 5.6 3.3 6.7 Lowest -0.4 -6.1 -0.4 4.4 -1.6 5.5 4.6 -0.3 5.5 Average 1.6 0.8 2.1 5.7 1.9 8.0 5.6 2.7 7.4 Highest 2.5 4.0 4.9 7.8 4.0 10.7 7.8 6.4 10.4 Behringer Harvard Multifamily REIT I 2.8 1.2 3.8 9.0 0.1 16.0 10.0 0.2 16.6 * Reflects AIV’s conventional same store change (excludes affordable component) Source: SNL |

|

|

Investment Activity Developments: 4140 Fairmount 299 planned units in Dallas, TX Closed land – April 2, 2012 Estimated completion – Q3 2014 The Arpeggio Victory Park 377 planned units in Dallas, TX Closed land – April 16, 2012 Estimated completion – Q3 2014 Museum District 270 planned units in Houston, TX Closed land – July 31, 2012 Estimated completion – Q4 2014 Acquisitions: Pembroke Woods 240 units in Pembroke, MA Mezzanine/Land Loans: Jefferson at One Scottsdale 388 planned units in Scottsdale, AZ Closed loan – June 29, 2012 TDI 121 Custer 444 planned units in Allen, TX Closed loan – August 15, 2012 |

|

|

Spread Widens between Class A Cap Rates and New Development Yields Source: Witten Advisors, Real Capital Analytics, NCREIF Used with permission from Witten Advisors LLC. Estimated New Development Yield (nationwide average) Class A Cap Rate (est.) 4% 5% 6% 7% 8% 9% 1Q01 1Q02 1Q03 1Q04 1Q05 1Q06 1Q07 1Q08 1Q09 1Q10 1Q11 1Q12 |

|

|

Development Pipeline – Equity Investments Property Name Investment Type Location Units Total Costs Incurred as of June 30, 2012 Our Share of Total Estimated Costs (1) Estimated Completion Date The Franklin Delray Wholly owned Delray Beach, FL 180 $13.7 $32.5 Q4 2013 Allegro Phase II Wholly owned Addison, TX 121 $3.8 $16.1 Q2 2013 Renaissance Phase II Joint venture Concord, CA 163 $8.4 $21.0 Q4 2015 7 Rio Joint venture(3) Austin, TX 221 $7.1 $55.6 Q1 2015 The Muse West University Joint venture(3) Houston, TX 231 $10.7 $41.6 Q4 2014 4140 Fairmount Joint venture(3) Dallas, TX 299 $8.1 $45.3 Q3 2014 The Arpeggio Victory Park Joint venture(3) Dallas, TX 377 $12.4 $58.9 Q3 2014 Museum District (2) Joint venture(3) Houston, TX 270 N/A $48.7 Q4 2014 Total 1,862 $64.2 $319.7 We may obtain construction financing. Acquisition of the land occurred subsequent to June 30, 2012. If the development achieves certain milestones primarily related to approved budgets less than maximum amounts, we will reimburse the JV partner for their equity ownership and we will be responsible for all of the development costs. The JV partner would then be entitled to back end interests based on the development achieving certain total returns. Note: These are the estimates as of June 30, 2012 and are subject to change. ($ millions, except units) |

|

|

Loan Investments Property Name Investment Type Location Units Total Commitment Amounts Advanced at June 30, 2012 Fixed Interest Rate Maturity Date Pacifica Land loan option (2) Costa Mesa, CA 113 $4.9 $4.9 10.0% October 2012 Jefferson at One Scottsdale Land loan option (2) Scottsdale, AZ 388 $15.6 $15.6 12.5% June 2013 The Domain Mezzanine loan Houston, TX 320 $10.5 $9.5 14.0% April 2014 TDI 121 Custer (1) Mezzanine loan Allen, TX 444 $14.1 N/A 14.5% August 2015 Total 1,265 $45.1 $30.0 13.2% Investment occurred subsequent to June 30, 2012. We received an option to convert the loan into an equity investment. If we elect to convert to an equity investment, we anticipate that we will be responsible for funding all of the development costs and the JV partner will be entitled to back end interests based on the development achieving certain total returns. ($ millions, except units and interest rates) |

|

|

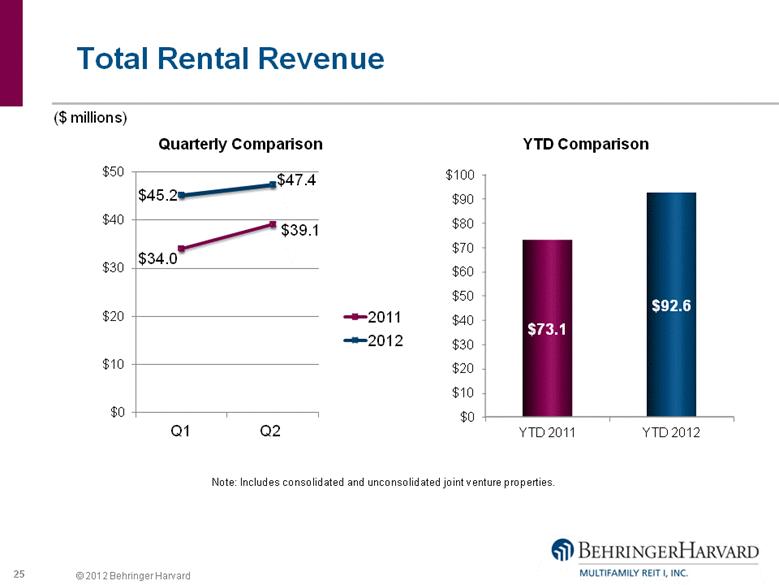

Total Rental Revenue Note: Includes consolidated and unconsolidated joint venture properties. ($ millions) Quarterly Comparison YTD Comparison |

|

|

GAAP Net Income Swing from net income to net loss primarily due to: $18.1 million gain on sale of Waterford Place included in Q2 2011 results Higher non-cash depreciation and amortization expense in Q2 2012 |

|

|

MFFO* Trends *Reconciliations of Net Income (Loss) to FFO to MFFO can be found in the Current Report on Form 8-K filed on August 30, 2012 with the Securities and Exchange Commission. A copy of this filing is available on our website www.behringerharvard.com **Weighted average number of common shares outstanding were 165.6 million and 123.4 million for the three months ended June 30, 2012 and 2011, respectively, and 165.5 million and 115.5 million for the six months ended June 30, 2012 and 2011, respectively MFFO per Share** Total MFFO (millions) MFFO per Share** Total MFFO (millions) |

|

|

Cash Flow from Operations Year-over-year growth due to: Improvements in operations Consolidation of most properties Excludes proceeds from sales ($ millions) YTD Comparison |

|

|

Investment Activity Invested approximately $150 million of equity during first 6 months of 2012 Second quarter activity: $42.4 million in wholly owned acquisitions $19.6 million in developments $18.3 million in buyout of joint venture partner interest $15.9 million in advances on mezzanine and land loans $ millions Investment Equity Deployed |

|

|

Distributions Declared per Share The regular distribution rates for each of the first quarters of 2011 and 2012 was 6%, based on a $10 share. Effective April 1, 2012, the regular distribution rate was reduced to 3.5%. A special cash distribution of $0.06 per share was declared in the first quarter of 2012 and was paid on July 11, 2012 to shareholders of record on July 6, 2012. Quarterly Comparison YTD Comparison |

|

|

Balance Sheet GAAP Assets of $2.7 billion Liabilities of $1 billion Ratio of total liabilities to assets of 37% Mortgage debt (including the credit facility) of $955 million Leverage ratio (to GAAP gross property cost) of 45% Cash and short-term investments balance at June 30, 2012 of $539 million |

|

|

Debt Financing Refinanced loans in Q2 Bailey’s Crossing: 5 year term Fixed interest at 2.82% The Cameron: 7 year term Fixed interest at 3.09% Grand Reserve: 7 year term Fixed interest at 3.41% * Includes $37 million of unconsolidated debt. Note: Includes 100% of property debt balances regardless of our ownership. Debt Maturities |

|

|

Multifamily REIT I, Inc. Investments San Sebastian – Laguna Woods, CA The Lofts at Park Crest– McLean, VA Fitzhugh Urban Flats – Dallas, TX Acappella – San Bruno, CA Allegro – Addison, TX The Reserve at La Vista Walk – Atlanta, GA San Sebastian, Fitzhugh Urban Flats, and The Lofts at Park Crest are joint venture owned communities. Acappella, The Reserve at La Vista Walk, and Allegro are wholly owned communities. |

|

|

Questions? During the call, please e-mail questions to: bhreit@behringerharvard.com |

|

|

Playback Information Representatives may log on to the password protected portion of the Behringer Harvard website (www.behringerharvard.com) for a playback of today’s call Investors may dial toll free (855) 859-2056 and use conference ID 56580495 to access a playback of today’s call Replays will be available until Friday, September 28 |