Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - ONCOR ELECTRIC DELIVERY CO LLC | d388275d8k.htm |

Exhibit 99.1

|

ONCOR

Second Quarter 2012 Investor Call

July 31, 2012

Oncor Electric Delivery

|

Forward Looking Statements

This presentation contains forward-looking statements, which are subject to various risks and uncertainties. Discussion of risks and uncertainties that could cause actual results to differ materially from management’s current projections, forecasts, estimates and expectations is contained in filings made by Oncor Electric Delivery Company LLC (Oncor) with the Securities and Exchange Commission (SEC). Specifically, Oncor makes reference to the section entitled “Risk Factors” in its annual and quarterly reports. In addition to the risks and uncertainties set forth in Oncor’s SEC filings, the forward-looking statements in this presentation could be affected by, among other things: prevailing governmental policies and regulatory actions; legal and administrative proceedings and settlements, including the exercise of equitable powers by courts; weather conditions and other natural phenomena; acts of sabotage, wars or terrorist or cyber security threats or activities; economic conditions, including the impact of a recessionary environment; unanticipated population growth or decline, or changes in market demand and demographic patterns; changes in business strategy, development plans or vendor relationships; unanticipated changes in interest rates or rates of inflation; unanticipated changes in operating expenses, liquidity needs and capital expenditures; inability of various counterparties to meet their financial obligations to Oncor, including failure of counterparties to perform under agreements; general industry trends; hazards customary to the industry and the possibility that Oncor may not have adequate insurance to cover losses resulting from such hazards; changes in technology used by and services offered by Oncor; significant changes in Oncor’s relationship with its employees; changes in assumptions used to estimate costs of providing employee benefits, including pension and other post-retirement employee benefits, and future funding requirements related thereto; significant changes in critical accounting policies material to Oncor; commercial bank and financial market conditions, access to capital, the cost of such capital, and the results of financing and refinancing efforts, including availability of funds in the capital markets and the potential impact of disruptions in US credit markets; circumstances which may contribute to future impairment of goodwill, intangible or other long-lived assets; financial restrictions under Oncor’s revolving credit facility and indentures governing its debt instruments; Oncor’s ability to generate sufficient cash flow to make interest payments on its debt instruments; actions by credit rating agencies; and Oncor’s ability to effectively execute its operational strategy. Any forward-looking statement speaks only as of the date on which it is made, and Oncor undertakes no obligation to update any forward-looking statement to reflect events or circumstances after the date on which it is made or to reflect the occurrence of unanticipated events.

Regulation G

This presentation includes certain non-GAAP financial measures. A reconciliation of these measures to the most directly comparable GAAP measures is included in this presentation, which is available on Oncor’s website, www.oncor.com, under the ‘News’ tab in the Investor Information section, and also filed with the SEC.

Oncor Electric Delivery 1

|

2nd Quarter 2012 Investor Call Agenda

Financial Overview David Davis

Chief Financial Officer

Operational Review Bob Shapard

Chairman and CEO

Q&A

Oncor Electric Delivery 2

|

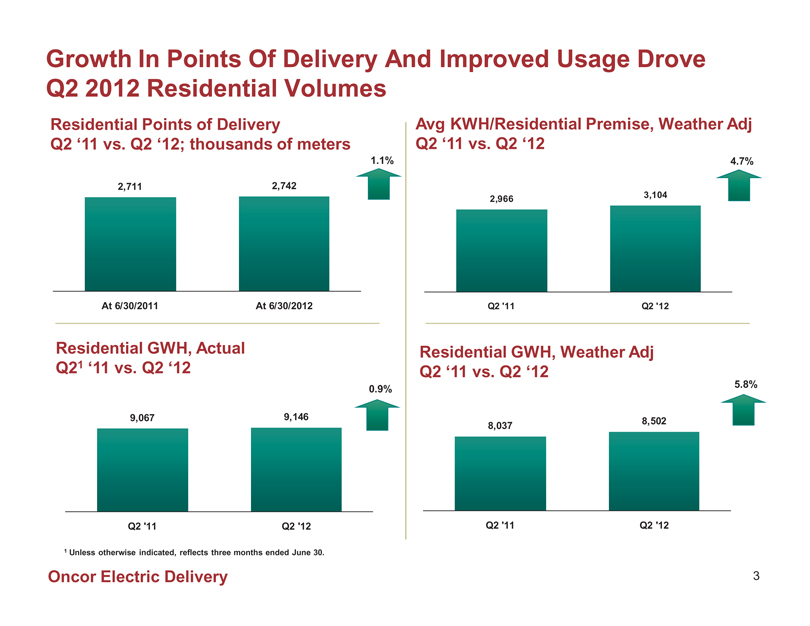

Growth In Points Of Delivery And Improved Usage Drove Q2 2012 Residential Volumes

Residential Points of Delivery

Q2 ‘11 vs. Q2 ‘12; thousands of meters

1.1%

2,711

2,742

At 6/30/2011 At 6/30/2012

Residential GWH, Actual Q21 ‘11 vs. Q2 ‘12

0.9%

9,067

9,146

Q2 ‘11 Q2 ‘12

1 Unless otherwise indicated, reflects three months ended June 30.

Avg KWH/Residential Premise, Weather Adj Q2 ‘11 vs. Q2 ‘12

4.7%

3,104 2,966

Q2 ‘11 Q2 ‘12

Residential GWH, Weather Adj Q2 ‘11 vs. Q2 ‘12

5.8%

8,502 8,037

Q2 ‘11 Q2 ‘12

Oncor Electric Delivery 3

|

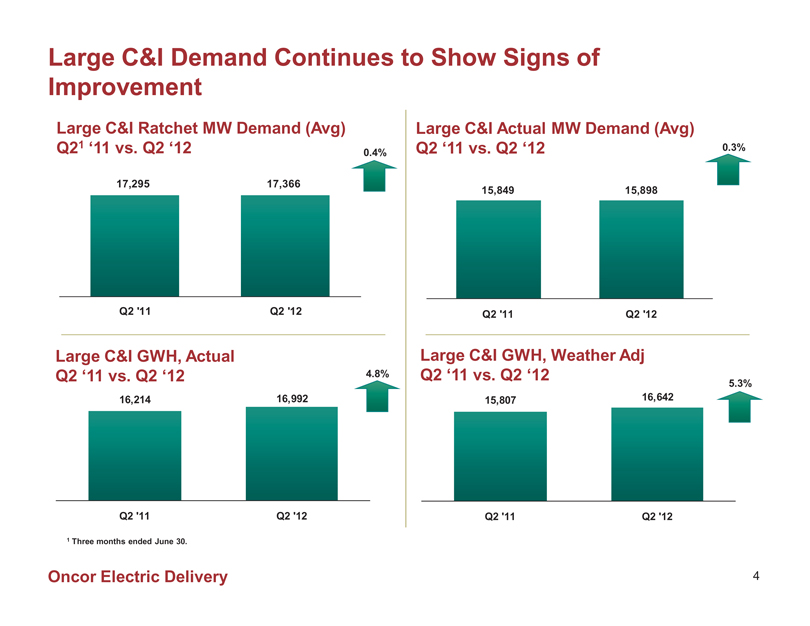

Large C&I Demand Continues to Show Signs of Improvement

Large C&I Ratchet MW Demand (Avg) Q21 ‘11 vs. Q2 ‘12

0.4%

17,295 17,366

Q2 ‘11 Q2 ‘12

Large C&I GWH, Actual Q2 ‘11 vs. Q2 ‘12

4.8%

16,214 16,992

Q2 ‘11 Q2 ‘12

1 Three months ended June 30.

Large C&I Actual MW Demand (Avg) Q2 ‘11 vs. Q2 ‘12

0.3%

15,849 15,898

Q2 ‘11 Q2 ‘12

Large C&I GWH, Weather Adj Q2 ‘11 vs. Q2 ‘12

5.3% 15,807 16,642

Q2 ‘11 Q2 ‘12

Oncor Electric Delivery 4

|

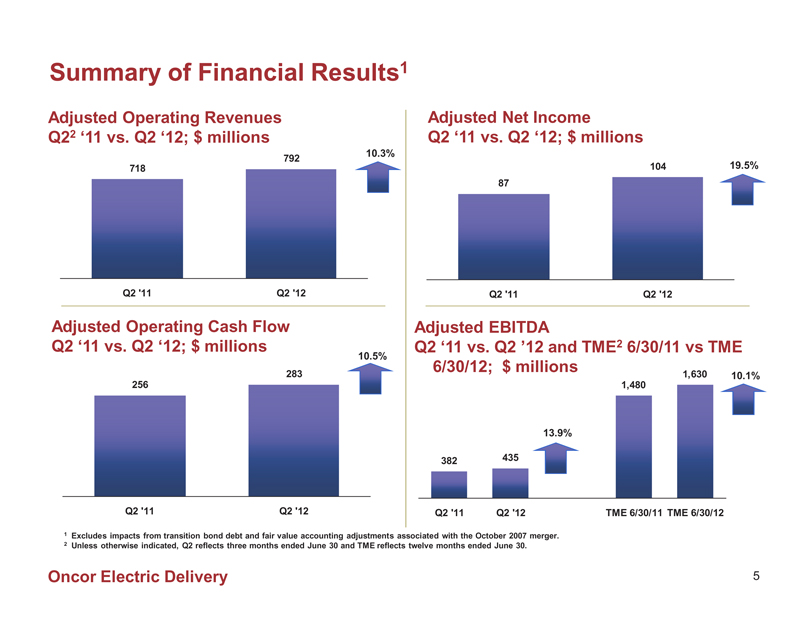

Summary of Financial Results1

Adjusted Operating Revenues Q22 ‘11 vs. Q2 ‘12; $ millions

10.3% 792 718

Q2 ‘11 Q2 ‘12

Adjusted Operating Cash Flow Q2 ‘11 vs. Q2 ‘12; $ millions

10.5%

283 256

Q2 ‘11 Q2 ‘12

Adjusted Net Income

Q2 ‘11 vs. Q2 ‘12; $ millions

104 19.5% 87

Q2 ‘11 Q2 ‘12

Adjusted EBITDA

Q2 ‘11 vs. Q2 ’12 and TME2 6/30/11 vs TME 6/30/12; $ millions

1,630 10.1% 1,480

13.9% 382 435

Q2 ‘11 Q2 ‘12 TME 6/30/11 TME 6/30/12

1 Excludes impacts from transition bond debt and fair value accounting adjustments associated with the October 2007 merger.

2 Unless otherwise indicated, Q2 reflects three months ended June 30 and TME reflects twelve months ended June 30.

Oncor Electric Delivery 5

|

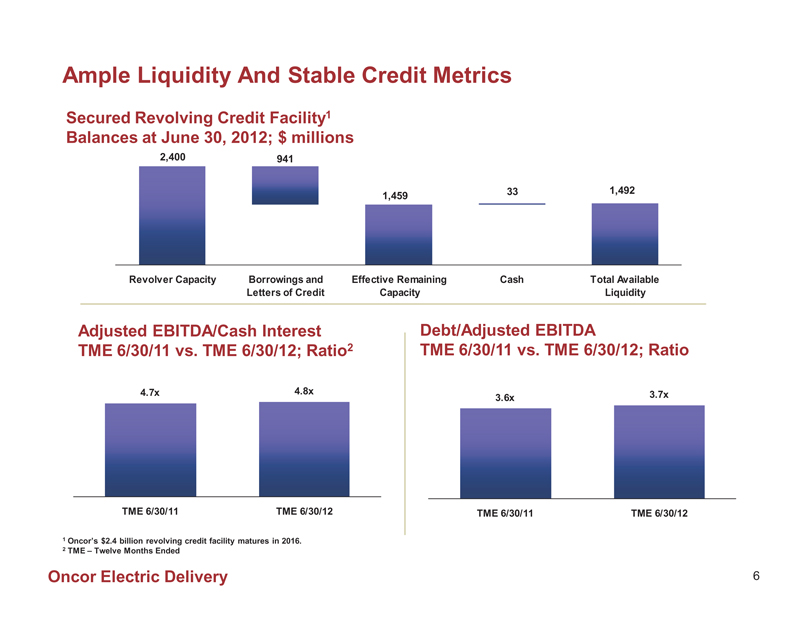

Ample Liquidity And Stable Credit Metrics

Secured Revolving Credit Facility1 Balances at June 30, 2012; $ millions

2,400

941

33

1,492

1,459

Revolver Capacity

Borrowings and Letters of Credit

Effective Remaining Capacity

Cash

Total Available Liquidity

Adjusted EBITDA/Cash Interest TME 6/30/11 vs. TME 6/30/12; Ratio2

4.7x 4.8x

TME 6/30/11 TME 6/30/12

Debt/Adjusted EBITDA

TME 6/30/11 vs. TME 6/30/12; Ratio

3.6x 3.7x

TME 6/30/11 TME 6/30/12

1 Oncor’s $2.4 billion revolving credit facility matures in 2016.

2 TME – Twelve Months Ended

Oncor Electric Delivery 6

|

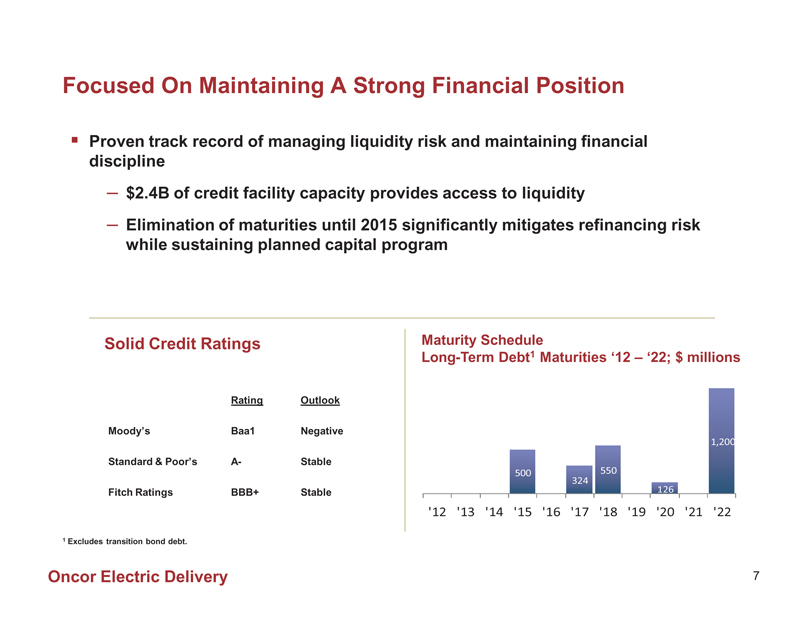

Focused On Maintaining A Strong Financial Position

Proven track record of managing liquidity risk and maintaining financial discipline

– $2.4B of credit facility capacity provides access to liquidity

– Elimination of maturities until 2015 significantly mitigates refinancing risk while sustaining planned capital program

Solid Credit Ratings

Rating Outlook

Moody’s Baa1 Negative

Standard & Poor’s A- Stable

Fitch Ratings BBB+ Stable

Maturity Schedule

Long-Term Debt1 Maturities ‘12 – ‘22; $ millions

500

324

550

126

1,200

‘12 ‘13 ‘14 ‘15 ‘16 ‘17 ‘18 ‘19 ‘20 ‘21 ‘22

1 Excludes transition bond debt.

Oncor Electric Delivery 7

|

2nd Quarter 2012 Investor Call Agenda

Financial Overview David Davis

Chief Financial Officer

Operational Review Bob Shapard

Chairman and CEO

Q&A

Oncor Electric Delivery 8

|

Appendix -

Regulation G Reconciliations and Supplemental Data

Oncor Electric Delivery 9

|

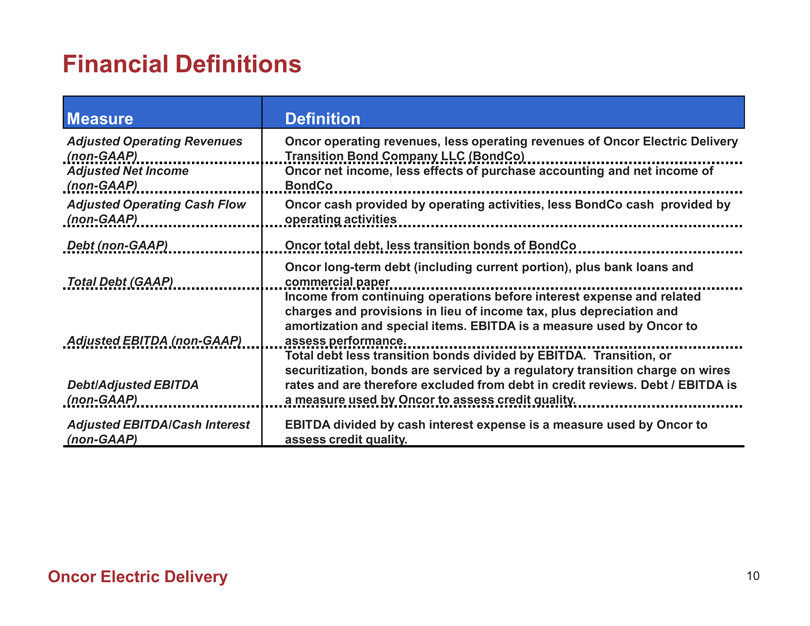

Financial Definitions

Measure Definition

Adjusted Operating Revenues (non-GAAP) Oncor operating revenues, less operating revenues of Oncor Electric Delivery Transition Bond Company LLC (BondCo)

Adjusted Net Income (non-GAAP) Oncor net income, less effects of purchase accounting and net income of BondCo

Adjusted Operating Cash Flow (non-GAAP) Oncor cash provided by operating activities, less BondCo cash provided by operating activities

Debt (non-GAAP) Oncor total debt, less transition bonds of BondCo

Total Debt (GAAP) Oncor long-term debt (including current portion), plus bank loans and commercial paper

Adjusted EBITDA (non-GAAP) Income from continuing operations before interest expense and related charges and provisions in lieu of income tax, plus depreciation and amortization and special items. EBITDA is a measure used by Oncor to assess performance.

Debt/Adjusted EBITDA (non-GAAP) Total debt less transition bonds divided by EBITDA. Transition, or securitization, bonds are serviced by a regulatory transition charge on wires rates and are therefore excluded from debt in credit reviews. Debt / EBITDA is a measure used by Oncor to assess credit quality.

Adjusted EBITDA/Cash Interest (non-GAAP) EBITDA divided by cash interest expense is a measure used by Oncor to assess credit quality.

Oncor Electric Delivery 10

|

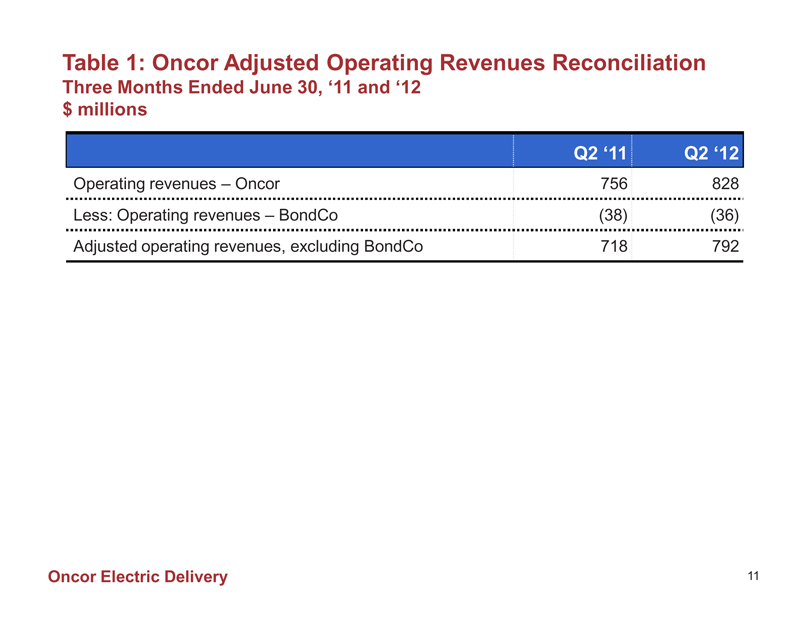

Table 1: Oncor Adjusted Operating Revenues Reconciliation

Three Months Ended June 30, ‘11 and ‘12 $ millions

Q2 ‘11 Q2 ‘12

Operating revenues – Oncor 756 828

Less: Operating revenues – BondCo (38) (36)

Adjusted operating revenues, excluding BondCo 718 792

Oncor Electric Delivery 11

|

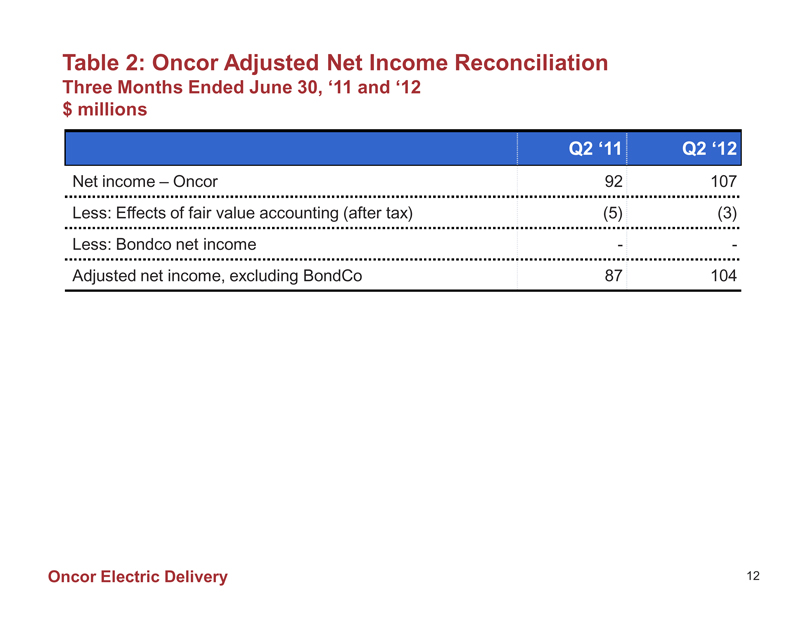

Table 2: Oncor Adjusted Net Income Reconciliation

Three Months Ended June 30, ‘11 and ‘12 $ millions

Q2 ‘11 Q2 ‘12

Net income – Oncor 92 107

Less: Effects of fair value accounting (after tax) (5) (3)

Less: Bondco net income - -

Adjusted net income, excluding BondCo 87 104

Oncor Electric Delivery 12

|

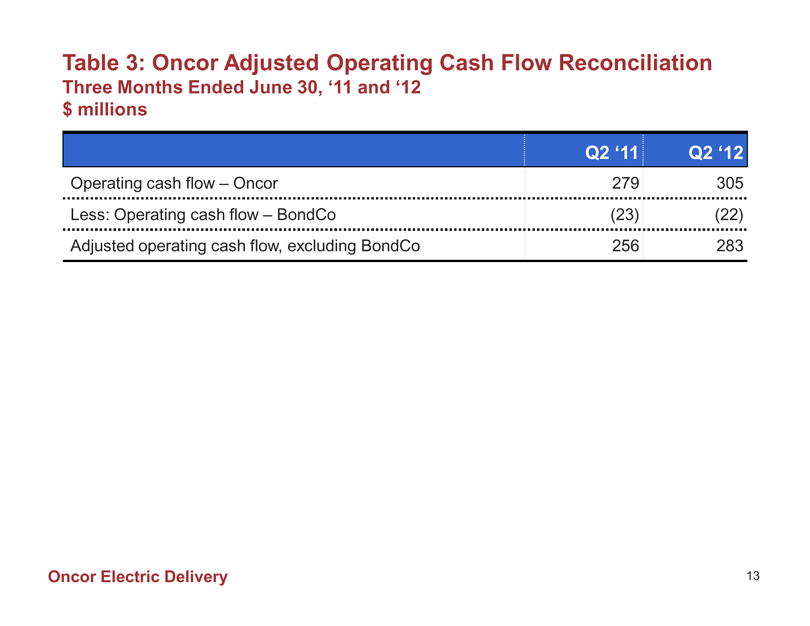

Table 3: Oncor Adjusted Operating Cash Flow Reconciliation

Three Months Ended June 30, ‘11 and ‘12 $ millions

Q2 ‘11 Q2 ‘12

Operating cash flow – Oncor 279 305

Less: Operating cash flow – BondCo (23) (22)

Adjusted operating cash flow, excluding BondCo 256 283

Oncor Electric Delivery 13

|

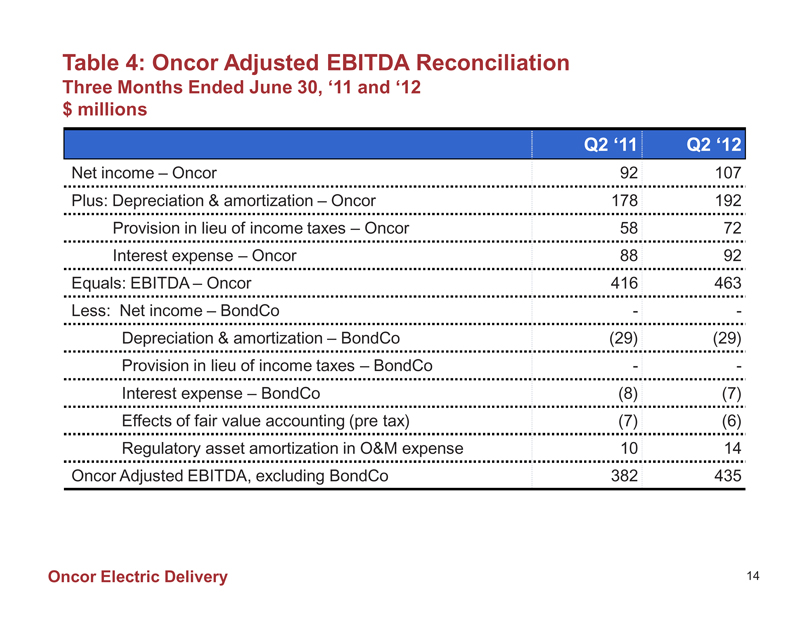

Table 4: Oncor Adjusted EBITDA Reconciliation

Three Months Ended June 30, ‘11 and ‘12 $ millions

Q2 ‘11 Q2 ‘12

Net income – Oncor 92 107

Plus: Depreciation & amortization – Oncor 178 192

Provision in lieu of income taxes – Oncor 58 72

Interest expense – Oncor 88 92

Equals: EBITDA – Oncor 416 463

Less: Net income – BondCo - -

Depreciation & amortization – BondCo (29) (29)

Provision in lieu of income taxes – BondCo - -

Interest expense – BondCo (8) (7)

Effects of fair value accounting (pre tax) (7) (6)

Regulatory asset amortization in O&M expense 10 14

Oncor Adjusted EBITDA, excluding BondCo 382 435

Oncor Electric Delivery 14

|

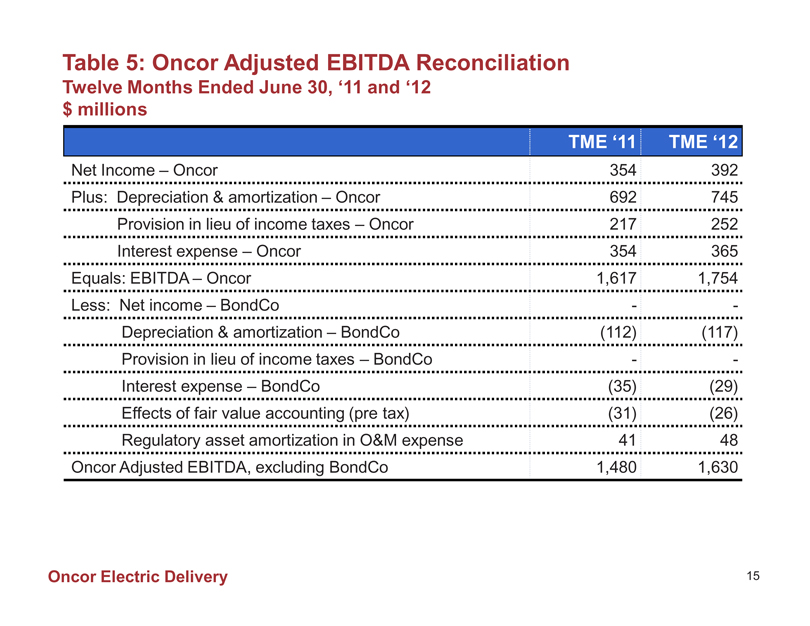

Table 5: Oncor Adjusted EBITDA Reconciliation

Twelve Months Ended June 30, ‘11 and ‘12 $ millions

TME ‘11 TME ‘12

Net Income – Oncor 354 392

Plus: Depreciation & amortization – Oncor 692 745

Provision in lieu of income taxes – Oncor 217 252

Interest expense – Oncor 354 365

Equals: EBITDA – Oncor 1,617 1,754

Less: Net income – BondCo - -

Depreciation & amortization – BondCo (112) (117)

Provision in lieu of income taxes – BondCo - -

Interest expense – BondCo (35) (29)

Effects of fair value accounting (pre tax) (31) (26)

Regulatory asset amortization in O&M expense 41 48

Oncor Adjusted EBITDA, excluding BondCo 1,480 1,630

Oncor Electric Delivery 15

|

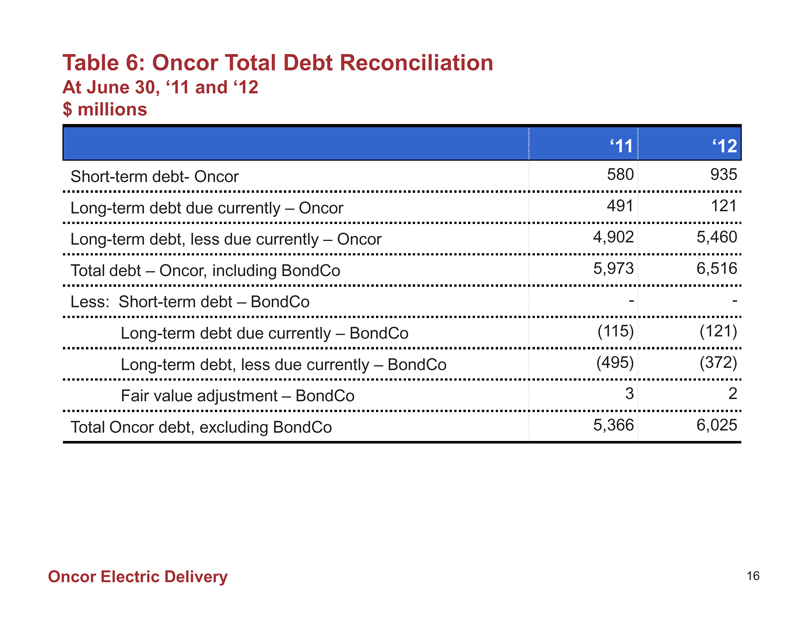

Table 6: Oncor Total Debt Reconciliation

At June 30, ‘11 and ‘12 $ millions

‘11 ‘12

Short-term debt- Oncor 580 935

Long-term debt due currently – Oncor 491 121

Long-term debt, less due currently – Oncor 4,902 5,460

Total debt – Oncor, including BondCo 5,973 6,516

Less: Short-term debt – BondCo - -

Long-term debt due currently – BondCo (115) (121)

Long-term debt, less due currently – BondCo (495) (372)

Fair value adjustment – BondCo 3 2

Total Oncor debt, excluding BondCo 5,366 6,025

Oncor Electric Delivery 16

|

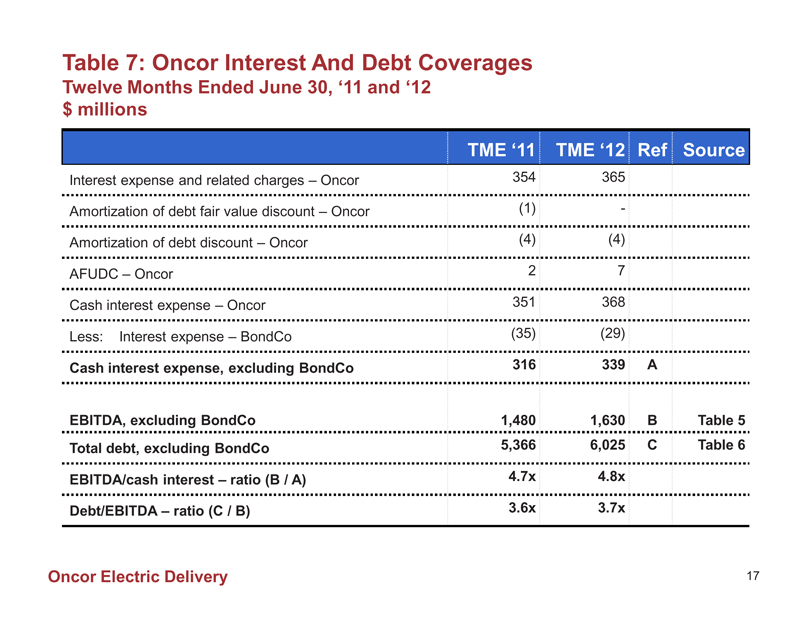

Table 7: Oncor Interest And Debt Coverages

Twelve Months Ended June 30, ‘11 and ‘12 $ millions

TME ‘11 TME ‘12 Ref Source

Interest expense and related charges – Oncor 354 365

Amortization of debt fair value discount – Oncor (1) -

Amortization of debt discount – Oncor (4) (4)

AFUDC – Oncor 2 7

Cash interest expense – Oncor 351 368

Less: Interest expense – BondCo (35) (29)

Cash interest expense, excluding BondCo 316 339 A

EBITDA, excluding BondCo 1,480 1,630 B Table 5

Total debt, excluding BondCo 5,366 6,025 C Table 6

EBITDA/cash interest – ratio (B / A) 4.7x 4.8x

Debt/EBITDA – ratio (C / B) 3.6x 3.7x

Oncor Electric Delivery 17