Attached files

| file | filename |

|---|---|

| EX-99.1 - EXHIBIT 99.1 - TECHPRECISION CORP | ex99-1.htm |

| 8-K - TECHPRECISION CORPORATION FORM 8-K - TECHPRECISION CORP | tcps8k.htm |

Q4 FY12 Shareholder Conference Call

July 16, 2012

© 2012. All rights reserved.

© 2012. All rights reserved.

2

Safe Harbor Statement

Safe Harbor Statement Under the Private Securities Litigation Reform Act of 1995: Any

statements set forth in this presentation that are not historical facts are forward-looking

statements that involve risks and uncertainties that could cause actual results to differ materially

from those in the forward-looking statements, which may include, but are not limited to, such

factors as unanticipated changes in product demand, increased competition, downturns in the

economy, failure to comply with specific regulations pertaining to government projects,

fluctuation of revenue due to the nature of project lifecycles, and other information detailed

from time to time in the Company filings and future filings with the United States Securities and

Exchange Commission. The forward-looking statements contained in this presentation are made

only of this date, and the Company is under no obligation to revise or update these forward-

looking statements.

statements set forth in this presentation that are not historical facts are forward-looking

statements that involve risks and uncertainties that could cause actual results to differ materially

from those in the forward-looking statements, which may include, but are not limited to, such

factors as unanticipated changes in product demand, increased competition, downturns in the

economy, failure to comply with specific regulations pertaining to government projects,

fluctuation of revenue due to the nature of project lifecycles, and other information detailed

from time to time in the Company filings and future filings with the United States Securities and

Exchange Commission. The forward-looking statements contained in this presentation are made

only of this date, and the Company is under no obligation to revise or update these forward-

looking statements.

Agenda

© 2012. All rights reserved.

3

• Q4 Overview

• Q4 and FY 2012 Financial Detail

• Ranor Challenges and Responses

• Product Diversification

• FY13 Outlook

Q4 Income Statement

|

Consolidated Income

Statement ($ in Millions except

Shares & EPS) |

Q4 2012

|

Q4 2011

|

FY 2012

|

FY 2011

|

|

Revenues

|

$6.1

|

$8.1

|

$33.3

|

$32.3

|

|

Gross Margin

|

0.03%

|

26.7%

|

15.3%

|

30.7%

|

|

Operating Income (loss)

|

$(2.8)

|

$0.4

|

$(3.4)

|

$4.7

|

|

Net Income (loss)

|

$(1.3)

|

$0.2

|

$(2.1)

|

$2.7

|

|

EPS - Diluted

|

$(0.07)

|

$0.00

|

$(0.13)

|

$0.12

|

4

© 2012. All rights reserved.

4

• Legacy pricing and

operational issues at

Ranor with prototypes

or first-article products

contributed to lower

top line revenue and

bottom-line loss

operational issues at

Ranor with prototypes

or first-article products

contributed to lower

top line revenue and

bottom-line loss

• China ramp progressing;

particularly in the

Sapphire market sector

particularly in the

Sapphire market sector

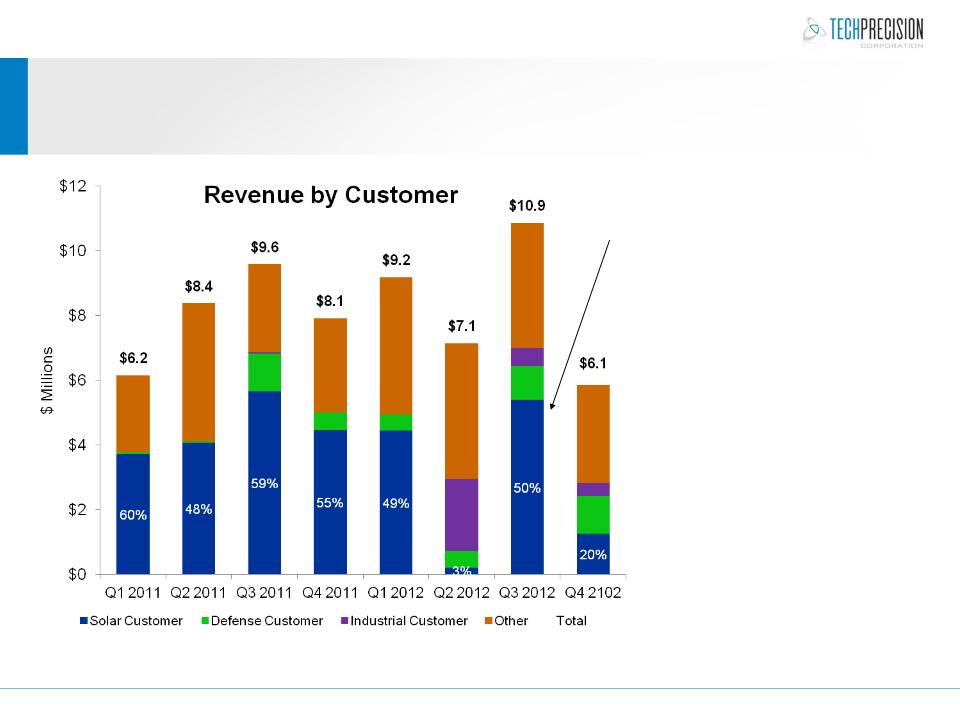

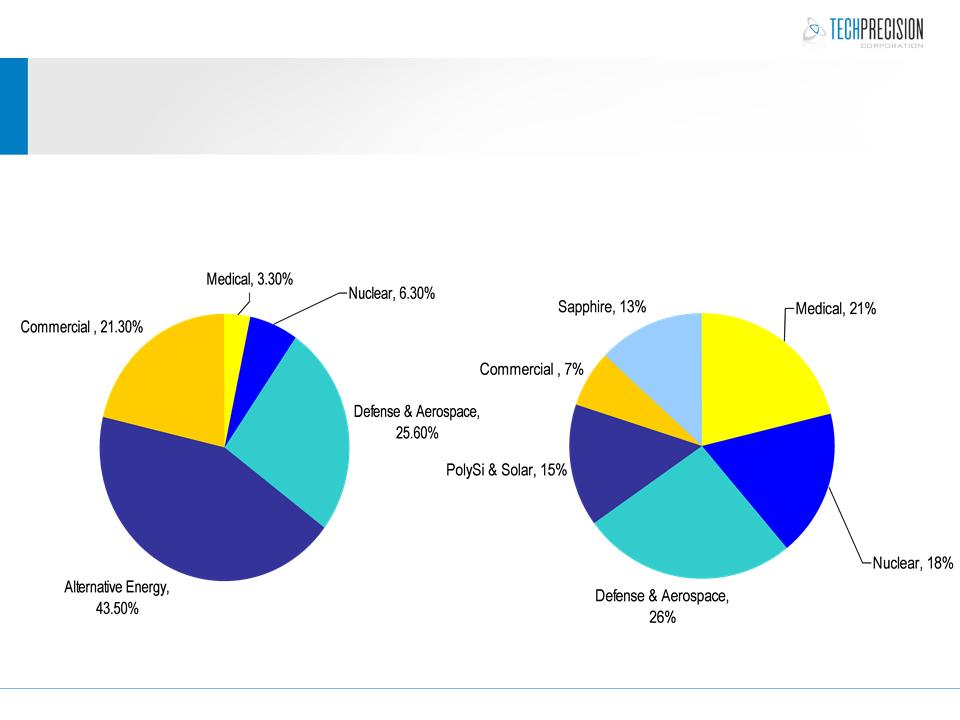

Revenue Distribution

© 2012. All rights reserved.

5

Solar Production

from Q2

recognized in Q3

from Q2

recognized in Q3

• Solar equipment revenues

decreased from ~50% to 20%

of total business

decreased from ~50% to 20%

of total business

• WCMC division revenue was

$4.6-million from Solar

Customer(s) from 9-months of

volume production in fiscal

2012

$4.6-million from Solar

Customer(s) from 9-months of

volume production in fiscal

2012

• Ranor division missed its

internal revenue plan by ~$5-

million

internal revenue plan by ~$5-

million

• For FY2013; growth will be in

Medical, Defense, Nuclear and

Sapphire

Medical, Defense, Nuclear and

Sapphire

• Medical and Sapphire expected

to be the largest year-on-year

growth sectors (% basis)

to be the largest year-on-year

growth sectors (% basis)

Q4 Income Statement

|

Consolidated Income Statement

($ in Millions except Shares & EPS)

|

Q4 2012

|

Q4 2011

|

FY 2012

|

FY 2011

|

|

Revenues

|

$6.1

|

$8.1

|

$33.3

|

$32.3

|

|

Gross Profit

|

$0.002

|

$2.2

|

$5.1

|

$9.9

|

|

Gross Margin

|

0.03%

|

26.7%

|

15.3%

|

30.7%

|

|

Operating Expenses

|

$2.8

|

$1.8

|

$8.5

|

$5.2

|

|

Operating (Loss) Income

|

$(2.8)

|

$0.4

|

$(3.4)

|

$4.7

|

|

Operating Margin

|

(45.9%)

|

5.0%

|

(10.2%)

|

14.7%

|

|

Net (Loss) Income

|

$(1.3)

|

$0.2

|

$(2.0)

|

$2.7

|

|

Net Margin

|

(21.3%)

|

2.5%

|

(6.0%)

|

8.3%

|

|

Weighted Average Shares - Basic

|

17.8

|

15.0

|

16.7

|

14.5

|

|

EPS - Diluted

|

$(0.07)

|

$0.00

|

$(0.11)

|

$0.12

|

6

© 2012. All rights reserved.

6

Balance Sheet Highlights

© 2010. All rights reserved.

7

|

($ in Millions)

|

March 31, 2012

|

March 31, 2011

|

|

Cash

|

2.8

|

7.5

|

|

Current Assets

|

16.3

|

17.7

|

|

Total Assets

|

24.0

|

22.9

|

|

Current Liabilities

|

6.1

|

4.1

|

|

Total Liabilities

|

11.9

|

9.3

|

|

Total Stockholders’ Equity

|

12.2

|

13.9

|

|

Long-Term Debt

|

March 31, 2012

|

|

Term Note

|

571,429

|

|

Series A & B Bonds

|

5,627,082

|

|

Capex Debt/Capital Lease

|

936,716

|

|

Total Long-Term Debt

|

7,135,227

|

Ranor Challenges and Transition

Moving the Ranor division from dominant single customer and repetitious

“production environment” of the previous 5+ years to larger-scale prototypes

which will evolve to volume products in Medical, Nuclear and Defense sectors

“production environment” of the previous 5+ years to larger-scale prototypes

which will evolve to volume products in Medical, Nuclear and Defense sectors

Bob Francis was hired to lead Ranor through the challenges and has

established a new senior management team to support the transition

established a new senior management team to support the transition

© 2012. All rights reserved.

8

Cultural improvements:

empowerment, teamwork,

accountability for all

management levels

empowerment, teamwork,

accountability for all

management levels

Improve and enhance ERP

systems, reporting

functionalities and information

gathering capabilities

systems, reporting

functionalities and information

gathering capabilities

Maintain and enhance quality

and on-time shipments:

Delight our customers

and on-time shipments:

Delight our customers

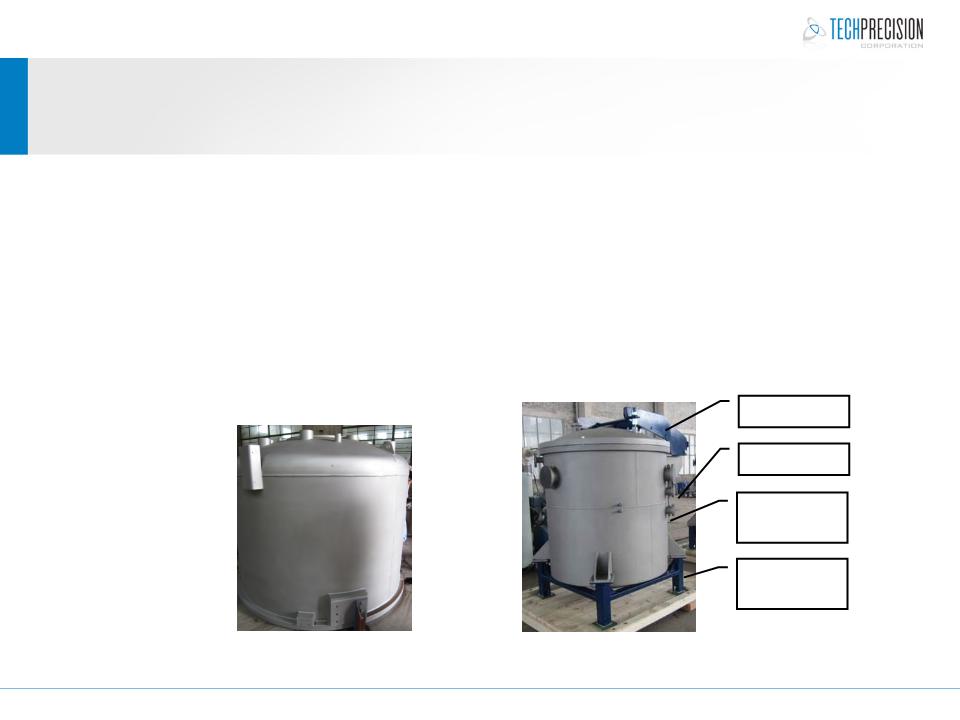

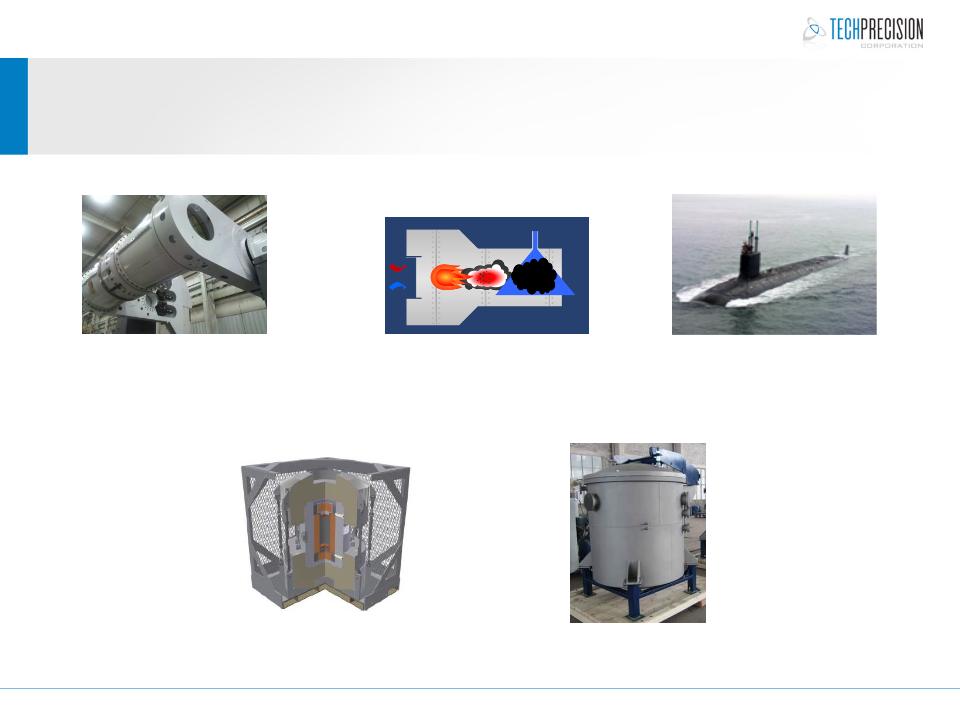

Product Solution Strategy

© 2012. All rights reserved.

9

• Historically the Company produced piece-part (highly competitive/less value-add to

customers) vs. product solutions (less competitive/more value-add to customers)

customers) vs. product solutions (less competitive/more value-add to customers)

• Product Solution involves supplying the manufacturing engineering, large-parts,

small parts (mechanical and electrical) in a complete/tested solution

small parts (mechanical and electrical) in a complete/tested solution

• Example: solar furnace “piece-part” vs. sapphire furnace “product solution”

Electro/Mechanical

Actuation Cylinder

Assembled and

Tested Assembly

Tested Assembly

Small Value-add

Parts (Completed

Assembly)

Parts (Completed

Assembly)

Support and Install

Frame (Completed

Assembly)

Frame (Completed

Assembly)

Sapphire Furnace

“Product Solution”

Solar Furnace

“Piece Part”

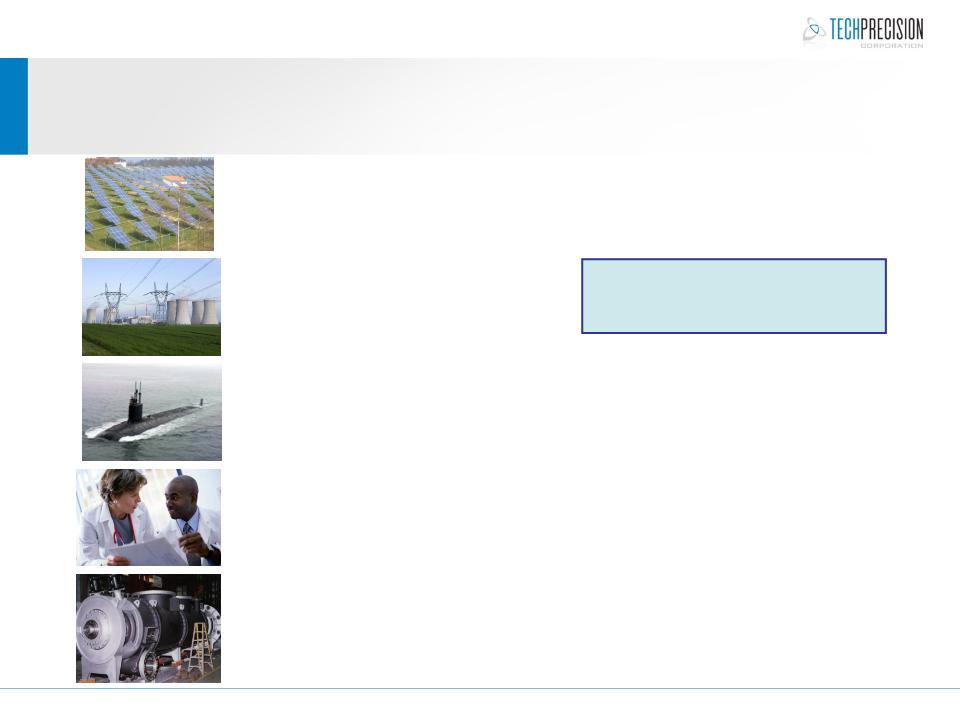

Strategic Production Solutions for Profitable Growth

© 2012. All rights reserved.

10

NRC approved Nuclear Isotope and

Fissile (pending) Transport Casks

Fissile (pending) Transport Casks

S250 Proton Beam

Cancer Treatment

(510k clearance)

Carbon Black

Furnaces

GDEB/BAE: Multiple

Confidential Virginia Class

Product Assemblies

Confidential Virginia Class

Product Assemblies

Sapphire Furnaces

FY2013 Customer and Sector Pipeline

© 2012. All rights reserved.

11

Alternative Energy:

Sapphire Pipeline: $6 - $12M

Solar Pipeline: $5 - $8M

Nuclear: $7 - $12M

Defense and Aerospace: $10 - $14M

Medical: $8 - $10M

Commercial Industrial: $3 - $6M

Current Backlog

(July 13th) $28.9-million

Served Markets: “Achieving Balance” in FY2013

12

© 2012. All rights reserved.

FY2012: Single Product

Dependence and Risk

Dependence and Risk

FY2013 Outlook:

Balance with Multiple Volume

Products

Products

www.TechPrecision.com

www.ranor.com

www.wcmcsolutions.com