Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - STRATEGIC HOTELS & RESORTS, INC | d361665d8k.htm |

Investor

Presentation June 2012

Exhibit 99.1 |

I.

BEE’s Unique Value Proposition

II.

Company Overview

III.

Industry Update

IV.

Operating Trends

V.

Financial Overview

BEE’s Unique Value Proposition

1 |

o

The only pure play high-end lodging REIT

o

High-end outperforms the industry in a recovery

o

Industry leading asset management expertise

o

Assets are in pristine condition

o

Embedded organic growth through revenue growth and ROI opportunities

o

Historically low supply growth environment, particularly in BEE markets

o

Replacement cost, excluding land, approximately $700,000 per key

o

Balance sheet positioned for growth

The best investment proposition in the lodging space

2

BEE’s Unique Value Proposition |

BEE’s

Unique Value Proposition Proven

Investment

Track Record

Industry Leading

Asset

Management

High-end, Unique

& Irreplaceable

Hotel & Resort

Portfolio

3 |

Highlights

o

Best portfolio in public markets

o

Locations in high-barrier-to-entry markets

o

City-center and resort destinations

o

World-class amenities

o

No new supply in BEE’s markets

Four Seasons Jackson Hole

Ritz-Carlton Laguna Niguel

InterContinental Chicago

BEE’s Unique Value Proposition

Industry

As

High-end, Unique

& Irreplaceable

Hotel & Resort

Portfolio

4 |

Highlights

o

Execution of complex and accretive restructurings

o

Assessment and development of ROI projects

o

Recent success in acquiring hotels through

off-market transactions

o

Maximized proceeds through well-timed

asset sales

Hotel del Coronado

Michael Jordan’s Steak House

Fairmont Scottsdale Princess

BEE’s Unique Value Proposition

Proven

Investment

Track Record

5 |

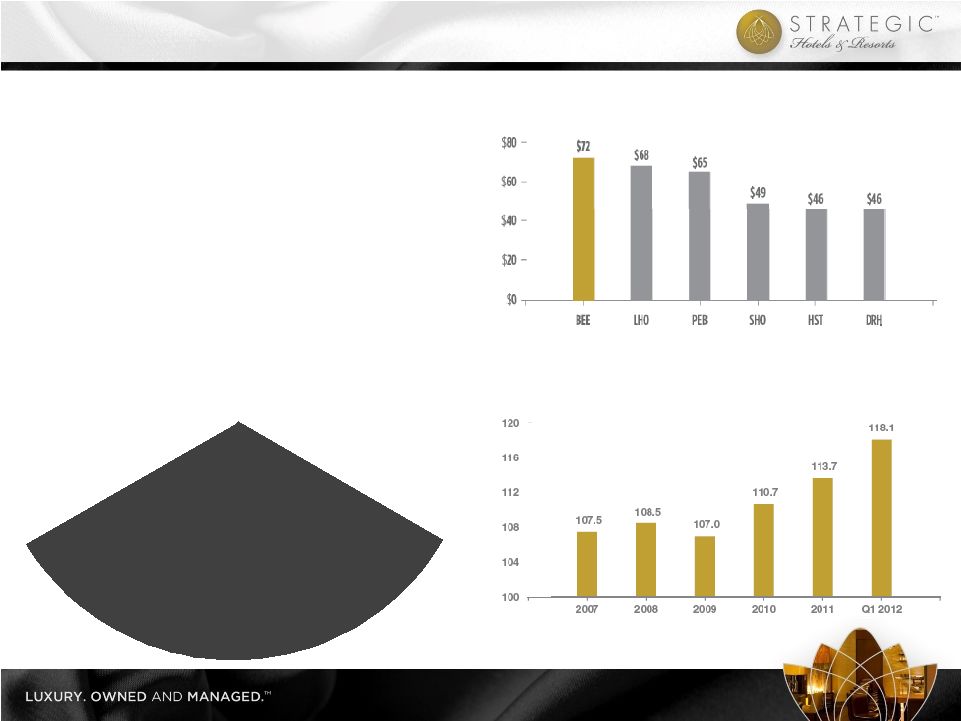

Industry

Leading Asset

Management

Highlights

o

Highest

EBITDA

per

room

in

competitive

set

o

Sustained market share penetration

and revenue growth

o

Implemented cost cutting initiatives

in advance of recession

o

Maintaining fixed cost reductions

in recovery

o

Strong relationships with and rigorous

oversight of brand managers

EBITDA Per Available Room

Annual RevPAR Index

BEE’s Unique Value Proposition

Note:

All

metrics

represent

full-year

2011

results.

BEE

portfolio

reflects

Total

United

States

portfolio

as

of

12/31/2011.

Source:

Public

filings

Source: Smith Travel Research

6 |

I.

BEE’s Unique Value Proposition

II.

Company Overview

III.

Industry Update

IV.

Operating Trends

V.

Financial Overview

Company Overview

7 |

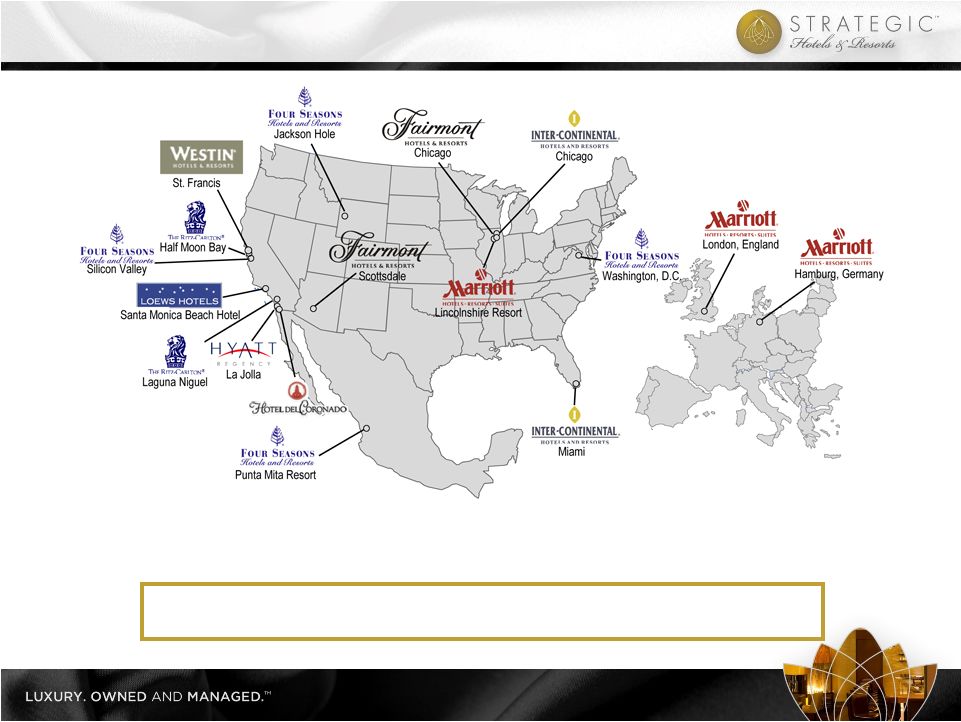

Top-Tier

Market Exposure 17

hotels

located

in

primary

gateway

cities

and

high

barrier

to

entry

markets;

including

7,762

rooms

and

840,000

square

feet

of

meeting

space

8 |

o

InterContinental

Miami

–

Guestroom

renovation

o

InterContinental

Chicago

–

Michael

Jordan’s

Steak

House

o

Four

Seasons

Washington,

D.C.

–

Retail

outlet

renovation

o

Marriott

Lincolnshire

Resort

–

Lobby

renovation

o

Westin

St.

Francis

–

Michael

Mina

Steakhouse

conversion

o

Four

Seasons

Washington,

D.C.

–

Lobby

renovation,

11-room

expansion,

new

restaurant,

63-room

and

suite

renovation

o

Westin

St.

Francis

–

Clock

Bar

o

Fairmont

Chicago

–

ENO

wine

tasting

room,

lobby

renovation,

guestroom

renovation,

new

spa

and

fitness

center

o

Four

Seasons

Punta

Mita

Resort

–

New

lobby

bar

o

Ritz-Carlton

Half

Moon

Bay

–

ENO

wine

tasting

room,

restaurant

and

lounge

renovation,

suite

renovation

Notable 2008

capital projects

Notable 2009

capital projects

Notable 2010

capital projects

Notable 2011

capital projects

Fairmont Chicago Lobby

Four Seasons Washington, D.C. Lobby

Westin St. Francis Michael Mina

Bourbon Steak

InterContinental Miami Guestroom

Portfolio Well-Positioned to Enhance Cash Flow Growth

9 |

Four Seasons

Washington, D.C. o

ENO

Wine

Room

o

Retail

space

optimization

Four

Seasons

Silicon

Valley

o

Qauttro

patio

renovation

o

Meeting

room

renovation

Four Seasons Jackson Hole

o

Restaurant

re-concept

InterContinental Chicago

o

North

tower

guestroom

renovation

o

Meeting

space

expansion

o

Michigan

Ave.

façade

optimization

Ritz-Carlton Laguna Niguel

o

35-room

fire

pit

addition

o

Pool

deck

upgrades

InterContinental Miami

o

Public

space

revitalization

o

Meeting

space

expansion

o

Pool

deck

refurbishment

Fairmont Chicago

o

Meeting

space

renovation

o

Restaurant

re-concept

Westin St. Francis

o

ENO

Wine

Room

Loews Santa Monica Beach Hotel

o

Exterior

/

interior

upgrade

Significant

ROI

capital

investment

opportunities

within

existing

portfolio;

rigorous

analysis

and

approval

process

for

each

project

Potential Capital Projects in the Pipeline

10 |

I.

BEE’s Unique Value Proposition

II.

Company Overview

III.

Industry Update

IV.

Operating Trends

V.

Financial Overview

Industry Update

11 |

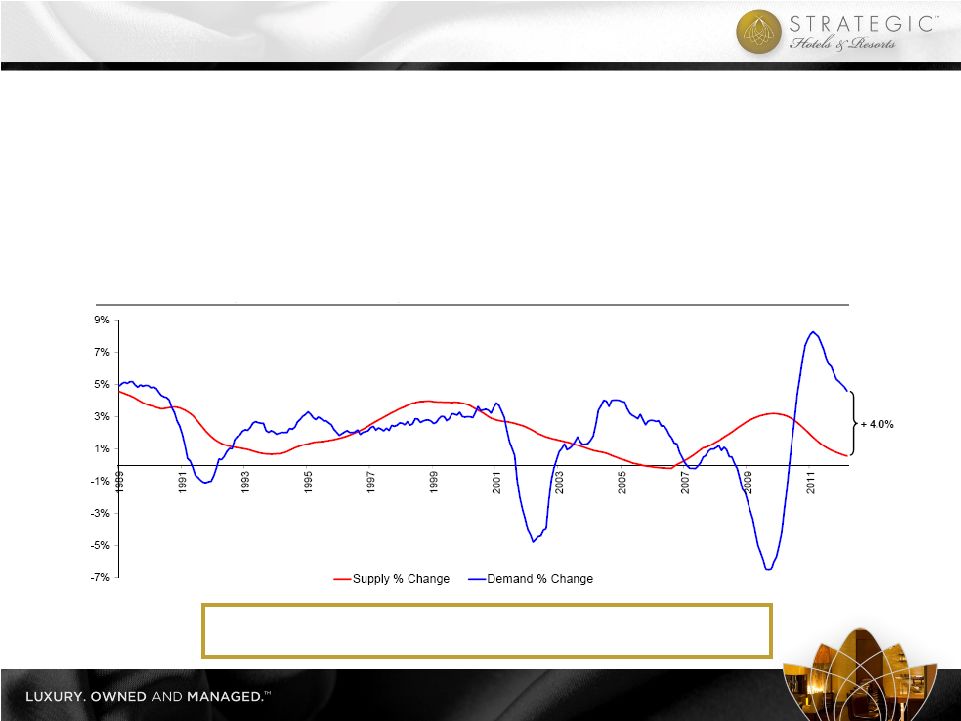

o

Lodging demand historically correlates with GDP (~80%) but potential exists for

near-term disconnect, particularly at the high-end

o

Customer demographics for luxury / high-end very strong –

corporate America and college educated

consumers

o

Supply growth remains historically low and development pipeline indicates muted supply for

the next several years

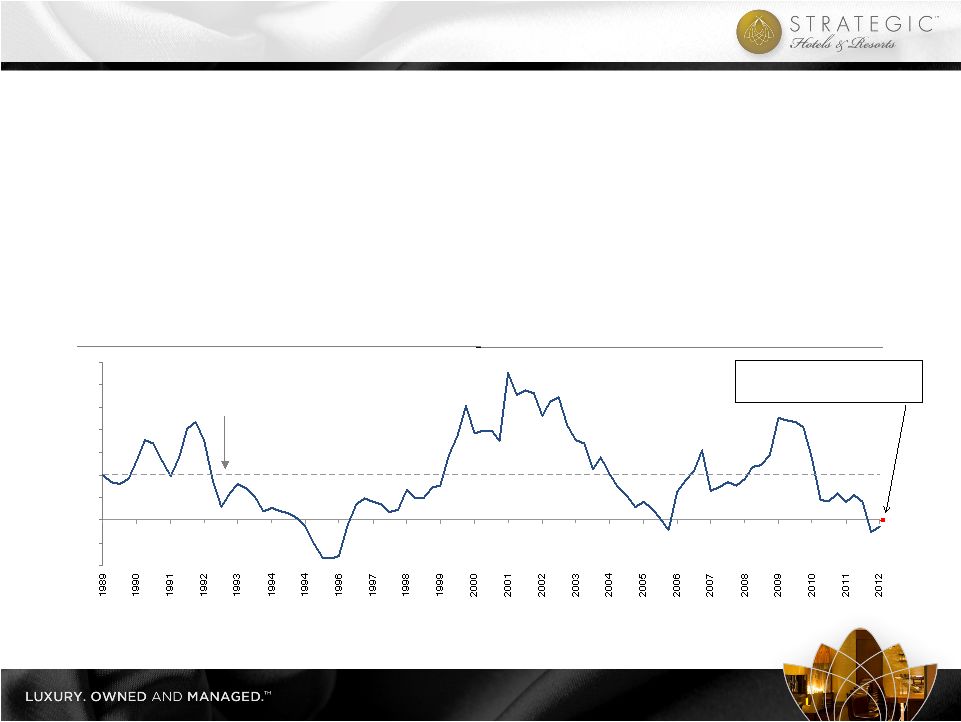

Total U.S. Supply & Demand Change (TTM)

Source: Smith Travel Research

Demand growth exceeds supply growth by 400 bps which should

result in significant ADR growth as recovery continues

Lodging Outlook

12 |

Source: Smith Travel Research

Note: Data represents trends within the United States

o

Luxury supply growth was historically lower leading into the recent recession

o

Projects in planning or under construction have decreased significantly

o

No new competitive luxury or upper-upscale supply projected in BEE markets

o

1-2 years estimated time to permit; 3 years estimated time to build a luxury hotel

o

Economic proposition of hotel construction challenging with replacement cost estimated

at over $700,000 per key

Favorable Supply Outlook

Year-Over-Year % Supply Growth

1988 –

Q1 2012

Average: 4.0%

Supply Growth in

BEE Markets = 0.0%

(4%)

(2%)

0%

2%

4%

6%

8%

10%

12%

14%

13 |

14

Source: Smith Travel Research and PWC

Source: Smith Travel Research

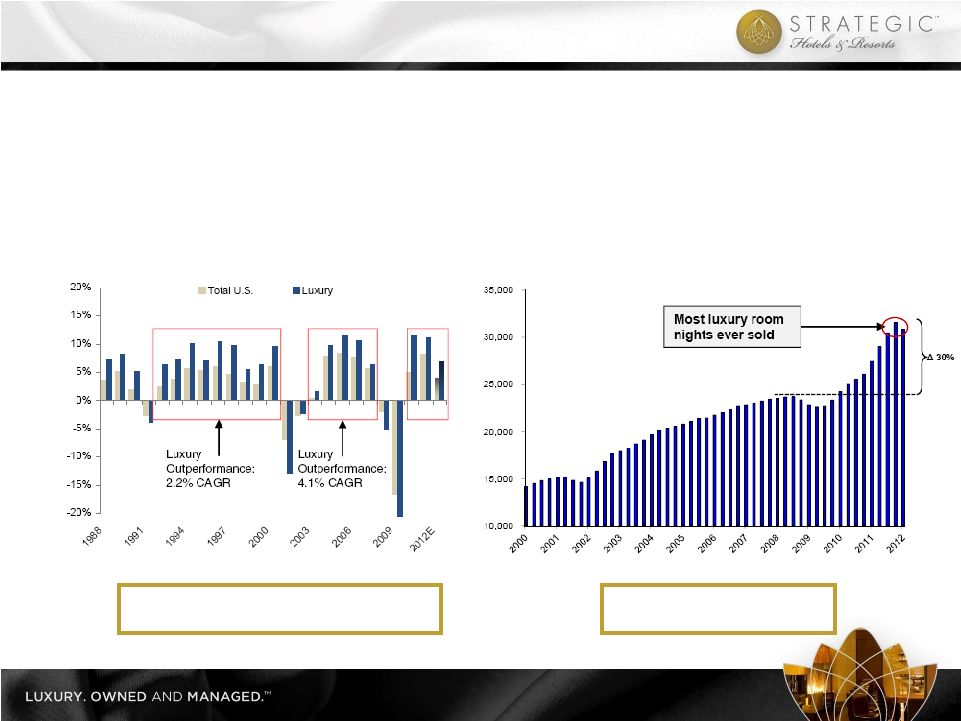

Annual % Change in RevPAR

Quarterly Luxury Room Night Demand (000s)

o

Luxury

hotels

have

experienced

prolonged

RevPAR

growth

following

past

industry

downturns

o

1992

–

2000:

9

consecutive

years

of

annual

luxury

RevPAR

growth

totaling

109%

or

8.5%

annually

o

2002

–

2007:

5

consecutive

years

of

annual

luxury

RevPAR

growth

totaling

48%

or

8.2%

annually

o

Overall

luxury

room

nights

sold

is

at

an

all-time

high;

30%

higher

than

2007

Luxury outperformed Total U.S. hotels

2.0% -

4.0% in previous two downturns

Luxury room night demand

currently at all-time highs

Luxury Hotels Outperform in a Recovery

14 |

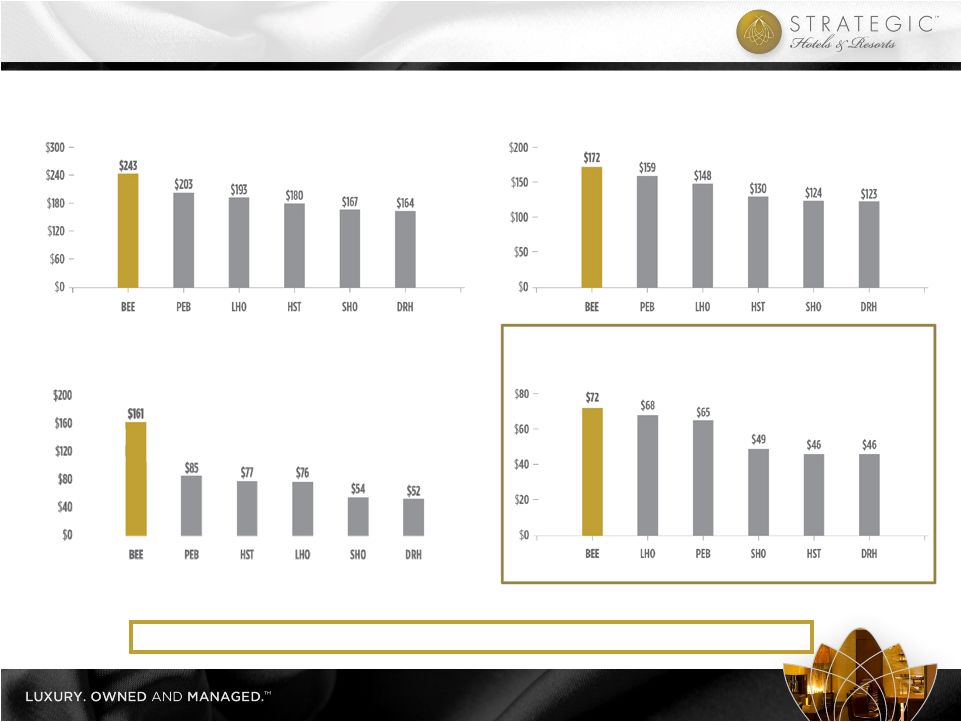

ADR

RevPAR

EBITDA Per Available Room

Non –

Rooms Revenue Per Available Room

Note: All metrics represent full-year 2011 results

BEE

portfolio

reflects

Total

United

States

portfolio

as

of

12/31/2011

Source: Public filings

BEE delivers industry leading results

BEE Outperforms Competitors

15 |

o

Total RevPAR is key top-line performance metric

o

Focus on maximizing RevPAR, non-rooms revenue, and yield per square foot

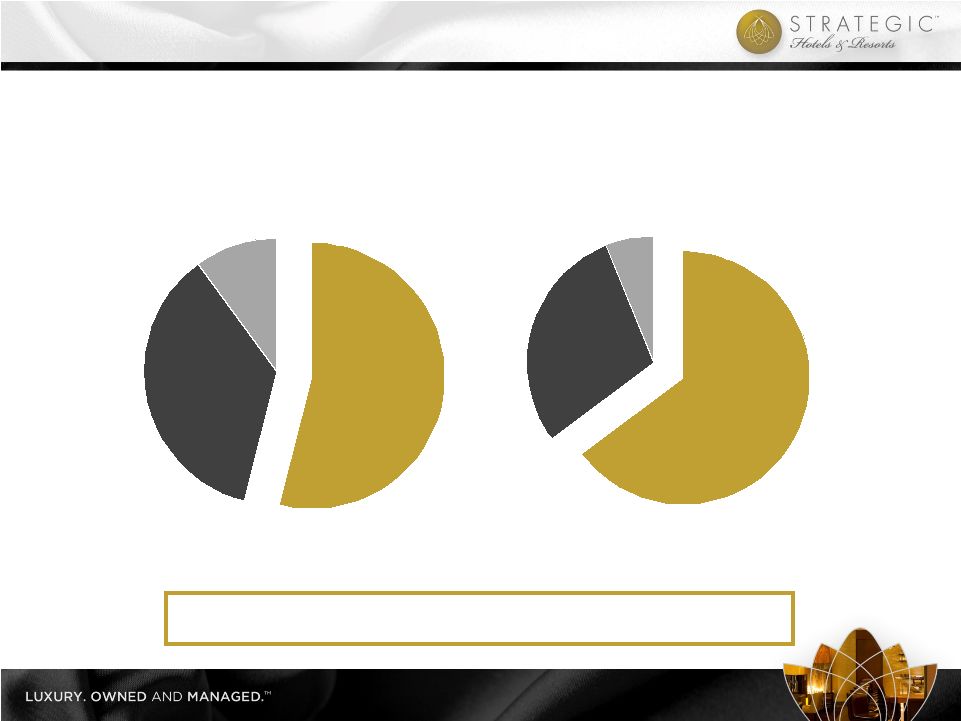

BEE Total Revenue Mix

Peers Total Revenue Mix

Note: All metrics represent the full-year 2011. BEE portfolio reflects the

North America Same Store portfolio Peers include: DRH, HST, LHO, PEB,

SHO Source: Public filings

BEE

revenue

driven

more

heavily

by

non-rooms

revenue

relative

to

peers,

maximizing

yield

per

square

foot

from

our

hotels

BEE Revenue Mix Compared to Peers

54%

36%

10%

Rooms

Other

Food &

Beverage

65%

29%

6%

Rooms

Other

Food &

Beverage

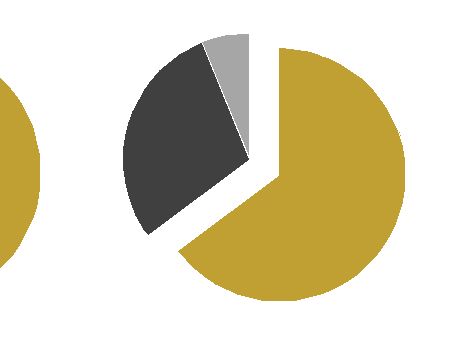

16 |

36%

21%

10%

27%

6%

40%

20%

9%

26%

5%

17

Note: Statistics represent the full year 2011. Portfolio reflects the North America

Same Store portfolio BEE Occupied Room Nights Mix

BEE Room Revenue Mix

o

Targeted mix of business ~50% / 50% group / transient

o

Group business typically yields higher non-rooms revenue than transient business

43% Group

40% Group

57% Transient

60% Transient

BEE

total

revenue

driven

heavily

by

group

business

and

ancillary

group

spend;

still

significant

capacity

to

grow

group

business

BEE Revenue Mix

Transient - Other

Transient - Negotiated

Group - Association

Group - Corporate

Group - Other

17 |

BEE

(1)

Peers

Peer margins

@ BEE

Revenue Mix

Revenue

Rooms

54%

65%

54%

Food & Beverage

36%

29%

36%

Other

10%

6%

10%

Total

100%

100%

100%

Departmental Profit Margin

Rooms

71%

73%

73%

Food & Beverage

26%

27%

27%

EBITDA

21%

24%

18%

3% better than peers

(1) Portfolio includes all North American hotels owned for the full year 2011

Peers include: DRH, HST, LHO, PEB, & SHO

Source: Public filings

BEE’s

margins

significantly

outperform

when

adjusted

for

same

revenue

mix

Industry Leading Operating Margins

18 |

I.

BEE’s Unique Value Proposition

II.

Company Overview

III.

Industry Update

IV.

Operating Trends

V.

Financial Overview

Operating Trends

19 |

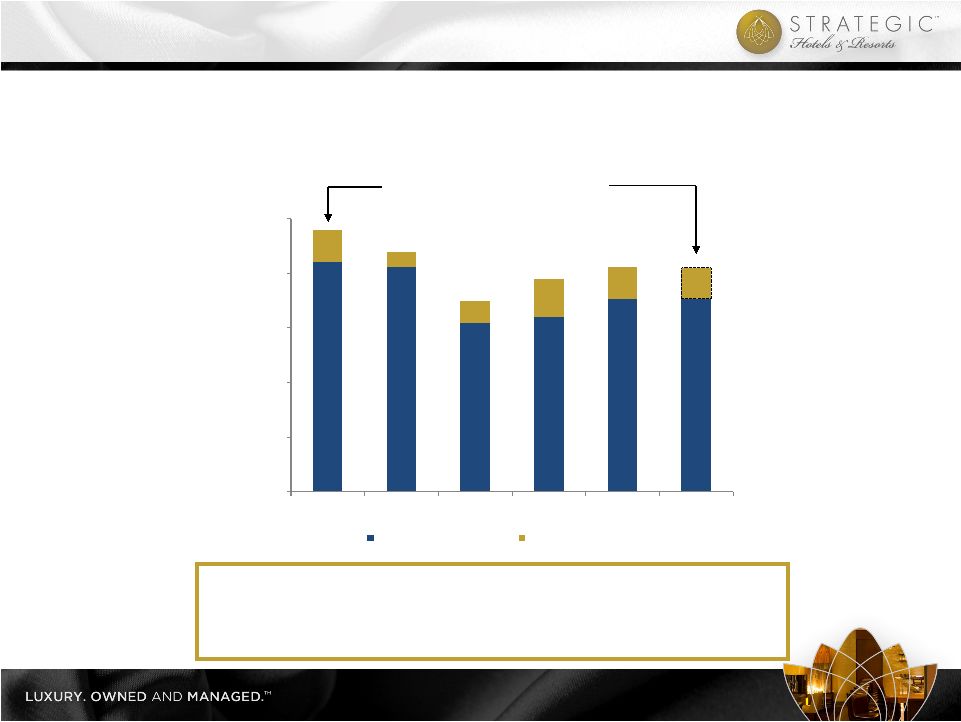

o

Group pace remains the most reliable forward looking indicator

o

Booking window has shortened forcing more reliance on room nights booked ITYFTY

(“in-the-year-for-the-year”)

Year-Over-Year Group Pace

Assuming similar production as 2011,

group room nights 14% below peak

*2012 production in the year assumes the same production as in 2011

Group room nights on the books for 2012 are approximately flat compared

to same time last year; ADR up approximately 4% compared to 2011

rate

Group room nights on the books for 2013 are up approximately 7%

compared to 2012; ADR approximately flat compared to 2012 rate

Group Booking Outlook

0

200,000

400,000

600,000

800,000

1,000,000

2007

2008

2009

2010

2011

2012*

Definite through April

Production in the year

20 |

$100

$120

$140

$160

$180

$200

2007

2008

2009

2010

2011

2012F

$140

$160

$180

$200

$220

2007

2008

2009

2010

2011

2012F

$120

$160

$200

$240

$280

2007

2008

2009

2010

2011

2012F

60%

64%

68%

72%

76%

80%

2007

2008

2009

2010

2011

2012F

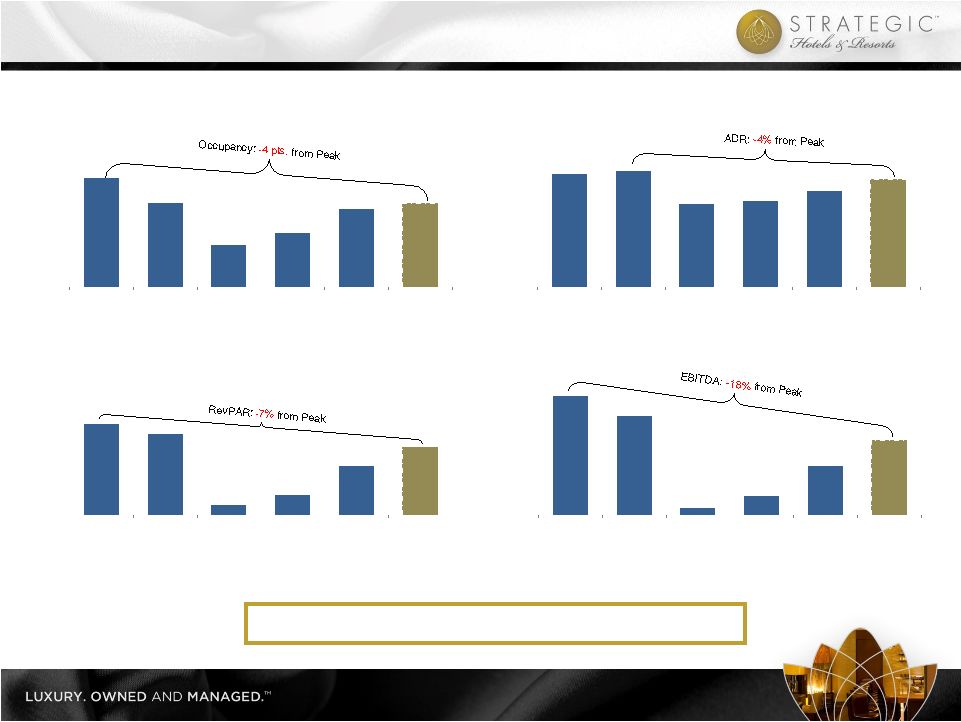

Occupancy

ADR

RevPAR

Property EBITDA (in millions)

Note:

Same

store

North

America

portfolio,

excludes:

Hotel

del

Coronado,

Fairmont

Scottsdale

Princess,

Four

Seasons

Jackson

Hole,

Four

Seasons

Silicon

Valley

2012 forecast assumes midpoint of guidance range

Operating

performance

improving;

still

below

peak

Embedded Portfolio Growth

21 |

I.

BEE’s Unique Value Proposition

II.

Company Overview

III.

Industry Update

IV.

Operating Trends

V.

Financial Overview

Financial Overview

22 |

Raised $665

million in equity: o

$335 mm secondary offering (May 2010)

o

$145 mm Woodbridge transaction acquiring two Four Seasons hotels

plus PIPE (February 2011)

o

$70 mm equity placement to GIC for share in InterContinental Chicago (June 2011)

o

$115 mm overnight equity offering (April 2012)

Asset sales:

o

Sold

InterContinental

Prague

for

€110.6mm

(December

2010)

o

Sold leasehold position at Marriott Paris Champs-Elysees for approximately $60 million

(April 2011) o

Sold stake in BuyEfficient for $9mm (January 2011)

Debt Repayments:

o

Tendered

and

fully

retired

$180mm

unsecured

convertible

recourse

notes

(May

2010)

Hotel del Coronado complex restructuring (February 2011):

o

Negotiated new joint-venture with Blackstone and KSL

o

Closed new CMBS mortgage financing totaling $425mm

Fairmont Scottsdale Princess complex restructuring (June 2011):

o

Negotiated new joint venture structure with Walton Street Capital

o

Negotiated amendment and extension to CMBS debt for four years at below market terms

New Line of Credit (June 2011):

o

Reduced lenders in bank syndicate from 21 banks to 10 banks

o

Achieved three year term with one year extension

Debt refinancings:

o

Six property loans refinanced totaling nearly $800 million

Preferred Equity Tender (December 2011):

o

Successfully tendered for approximately 22% of outstanding preferred equity at a 15%

discount to par plus accrued preferred dividends; 14 quarters accrued dividends

payable June 29, 2012 Accomplishments

Since

January

1

st

,

2010

23 |

$115.5

$130.0

$195.0

$52.2

$315.7

$66.5

$145.8

$145.0

$0.0

$100.0

$200.0

$300.0

$400.0

$500.0

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

Bank

Life Co.

CMBS

Corporate

$300.0

Capacity

$275.8

$148.9

$124.9

$220.0

$173.5

$614.5

$194.8

$358.0

$0.0

$200.0

$400.0

$600.0

$800.0

$1,000.0

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

Bank

Life Co.

CMBS

Corporate

$834.5

$875.2

January 1, 2010

March 31, 2012

BEE’s balance sheet is structured for growth

Strong Recapitalized Balance Sheet ($ in millions)

Note: Assumes full extension periods for all loans.

(a)

Pro-forma for April 2012 equity offering.

(b)

EBITDA reflects mid-point of 2012 guidance range.

Key Stats

(a)(b)

Net Debt/EBITDA

6.1x

Net Debt+Pref /EBITDA

7.8x

Net Debt/TEV

40.7%

Avg. Maturity (yrs)

5.1

Unencumbered assets

2

Corporate liquidity (MM)

$345.0

Mix of Debt

Bank Debt

37.8%

Life Insurance Co.

31.6%

CMBS

30.7%

Key Stats

Net Debt/EBITDA

14.3x

Net Debt+Pref /EBITDA

17.4x

Net Debt/TEV

76.9%

Avg. Maturity (yrs)

3.4

Unencumbered assets

0

Corporate liquidity (MM)

$105.0

Mix of Debt

Bank Debt

18.5%

Life Insurance Co.

26.6%

CMBS

54.8%

24 |

(a) Excludes Fairmont Scottsdale Princess, Four Seasons Jackson

Hole, Four Seasons Silicon Valley, and Hotel del Coronado

1st

Quarter 2012 Results (EBITDA in millions)

2011 Actual

2012 Actual

Operations

(Same Store N.A. Portfolio)

(a)

ADR

$226

5.1%

$238

RevPAR

$146

9.4%

$160

Total RevPAR

$279

7.7%

$301

EBITDA Margins

15.5%

170 bps

17.2%

Corporate Results

Comparable EBITDA

$28.7

15.9%

$33.3

Comparable FFO / share

($0.02)

N/A

$0.02

25 |

(a)

Portfolio excludes Fairmont Scottsdale Princess, Four Seasons Jackson Hole, Four

Seasons Silicon Valley, and Hotel del Coronado (b)

2011 Comparable FFO / share excludes one-time gain associated with preferred

equity tender 2012 Guidance (EBITDA in millions)

2011 Actual

2012 Guidance

Operations

(Same Store N.A. Portfolio)

(a)

RevPAR

$170

6%-8%

$180-$183

Total RevPAR

$314

5%-7%

$330-$336

EBITDA Margins

21.1%

100 - 175bps

22.1%-22.9%

Corporate Results

Comparable EBITDA

$155

7%-16%

$165-$180

Comparable FFO / share

$0.14

50%-107%

$0.21-$0.29

(b)

26 |

o

The only pure play high-end lodging REIT

o

High-end outperforms the industry in a recovery

o

Industry leading asset management expertise

o

Assets are in pristine condition

o

Embedded organic growth through revenue growth and ROI opportunities

o

Historically low supply growth environment, particularly in BEE markets

o

Replacement cost, excluding land, approximately $700,000 per key

o

Balance sheet positioned for growth

The best investment proposition in the lodging space

BEE’s Unique Value Proposition

27 |

Disclaimer

28

Except for historical information, the matters discussed in this presentation are forward-looking

statements subject to certain risks and uncertainties. Forward-looking statements relate to

expectations, beliefs, projections, future plans and strategies, anticipated events or trends, and

similar expressions concerning matters that are not historical facts. These forward-looking

statements are identified by their use of such terms and phrases such as “anticipate,”

“believe,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “predict,” “project,” “should,” “will,”

“continue” and other similar terms and phrases, including references to assumptions and

forecasts of future results. Forward-looking statements are not guarantees of future performance.

Actual results could differ materially from the Company’s projections.

Factors that may contribute to these differences include, but are not limited to the following:

the effects of the recent global economic recession upon business and leisure travel and the

hotel markets in which the Company invests; the Company’s liquidity and refinancing demands; the

Company’s ability to obtain or refinance maturing debt; the Company’s ability to

maintain compliance with covenants contained in the Company’s debt facilities; the Company’s

ability to meet the requirements of the Maryland General Corporation Law with respect to the

payment of preferred dividends on the June 29, 2012 payment date; stagnation or further deterioration in economic and market conditions, particularly impacting business and leisure

travel spending in the markets where the Company’s hotels operate and in which the Company

invests, including luxury and upper upscale product; general volatility of the capital markets

and the market price of the Company’s shares of common stock; availability of capital; the

Company’s ability to dispose of properties in a manner consistent with the Company’s

investment strategy and liquidity needs; hostilities and security concerns, including future terrorist

attacks, or the apprehension of hostilities, in each case that affect travel within or to the

United States, Mexico, Germany, England or other countries where the Company invests; difficulties in

identifying properties to acquire and completing acquisitions; the Company’s failure to

maintain effective internal control over financial reporting and disclosure controls and procedures; risks related to natural disasters; increases in interest rates and operating costs,

including insurance premiums and real property taxes; contagious disease outbreaks, such as the H1N1

virus outbreak; delays and cost-overruns in construction and development; marketing

challenges associated with entering new lines of business or pursuing new business strategies; the Company’s failure to maintain the Company’s status as a REIT; changes in

the competitive environment in the Company’s industry and the markets where the Company invests;

changes in real estate and zoning laws or regulations; legislative or regulatory changes,

including changes to laws governing the taxation of REITS; changes in generally accepted accounting principles, policies and guidelines; and litigation, judgments or settlements.

Additional risks are discussed in the Company’s filings with the Securities and Exchange

Commission, including those appearing under the heading “Item 1A. Risk Factors” in the

Company’s most recent Form 10-K and subsequent Form 10-Qs. Although the Company believes

the expectations reflected in such forward-looking statements are based on reasonable

assumptions, it can give no assurance that its expectations will be attained. The forward-looking

statements are made as of the date of this press release, and the Company undertakes no

obligation to publicly update or revise any forward-looking statement, whether as a result of new

information, future events or otherwise, except as required by law. |

Non-GAAP

to GAAP Reconciliations Reconciliation of Net Debt / EBITDA

($ in 000s)

YE 2009

(a)

1Q 2012

(b)(c)

Consolidated debt

$1,658,745

$1,000,128

Pro rata share of unconsolidated debt

282,825

212,275

Pro rata share of consolidated debt

(107,065)

(45,548)

Cash and cash equivalents

(116,310)

(113,605)

Net Debt

$1,718,195

$1,053,250

Comparable EBITDA

$119,953

$172,500

Net Debt / EBITDA

14.3x

6.1x

(a) All figures taken from year-end 2009 financial statements.

(b) Comparable EBITDA reflects mid-point of guidance range.

(c) All figures taken from 1st quarter 2012 financial statements and adjusted

for April 2012 equity offering.

Reconciliation of Net Debt / TEV

($ in 000s)

YE 2009

(a)

1Q 2012

(b)

Consolidated Debt

$1,658,745

$1,000,128

Pro rata share of unconsolidated debt

282,825

212,275

Pro rata share of consolidated debt

(107,065)

(45,548)

Cash and cash equivalents

(116,310)

(113,605)

Net Debt

$1,718,195

$1,053,250

Market Capitalization

$144,966

$1,243,298

Total Debt

1,834,505

1,166,855

Preferred Equity

370,236

289,102

Cash and cash equivalents

(116,310)

(113,605)

Total Enterprise Value

$2,233,397

$2,585,650

Net Debt / Enterprise Value

76.9%

40.7%

(a) All figures taken from year-end 2009 financial statements.

(b) All figures taken from 1st quarter 2012 financial statements and adjusted

for April 2012 equity offering.

Reconciliation of Net Debt + Preferred Equity / EBITDA

($ in 000s)

YE 2009

(a)

1Q 2012

(b)(c)

Preferred equity capitalization

$370,236

$289,102

Consolidated debt

1,658,745

1,000,128

Pro rata share of unconsolidated debt

282,825

212,275

Pro rata share of consolidated debt

(107,065)

(45,548)

Cash and cash equivalents

(116,310)

(113,605)

Net Debt + Preferreds

$2,088,431

$1,342,352

Comparable EBITDA

$119,953

$172,500

Net Debt + Preferreds / EBITDA

17.4x

7.8x

(a) All figures taken from year-end 2009 financial statements.

(b) Comparable EBITDA reflects mid-point of guidance range.

(c) All figures taken from 1st quarter 2012 financial statements and adjusted

for April 2012 equity offering.

29 |

Non-GAAP

to GAAP Reconciliations 2012

2011

Net loss attributable to SHR common shareholders

(31,516)

$

(35,407)

$

Depreciation and amortization

25,490

30,605

Interest expense

19,605

19,548

Income taxes - continuing operations

465

(1,648)

Income taxes - discontinued operations

-

359

Noncontrolling interests

(117)

(138)

Adjustments from consolidated

affiliates (1,257)

(1,329)

Adjustments from unconsolidated affiliates

6,682

3,890

Preferred shareholder dividends

6,041

7,721

EBITDA

25,393

23,601

Realized portion of deferred gain on sale-leaseback -

continuing operations (51)

(53)

Realized portion of

deferred gain on sale-leaseback - discontinued operations

-

(1,152)

Gain on sale of assets - continuing operations

-

(2,640)

Gain on sale of assets - discontinued

operations -

(14)

Foreign currency exchange

loss (gain) - continuing operations (a) 5

(139)

Foreign currency exchange gain -

discontinued operations (a) -

(58)

Adjustment for Value

Creation Plan 7,939

9,181

Comparable EBITDA

33,286

$

28,726

$

(a)

Foreign currency exchange gains or losses applicable to

third-party and inter-company debt and certain balance sheet items held by

foreign subsidiaries.

March 31,

Reconciliation of Net Loss Attributable to SHR Common Shareholders to

EBITDA and Comparable EBITDA (in thousands)

Three Months Ended

30 |

Non-GAAP

to GAAP Reconciliations 2012

2011

Net loss attributable to SHR common shareholders

(31,516)

$

(35,407)

$

Depreciation and amortization

25,490

30,605

Corporate depreciation

(265)

(299)

Gain on sale of assets

- continuing operations -

(2,640)

Gain on sale of assets - discontinued

operations -

(14)

Realized

portion of deferred gain on sale-leaseback - continuing operations

(51)

(53)

Realized

portion of deferred gain on sale-leaseback - discontinued operations

-

(1,152)

Deferred tax expense on realized portion of

deferred gain on sale-leasebacks -

359

Noncontrolling

interests adjustments (133)

(157)

Adjustments from

consolidated affiliates (667)

(1,561)

Adjustments from unconsolidated

affiliates 3,764

1,839

FFO

(3,378)

(8,480)

Redeemable noncontrolling interests

16

19

FFO

- Fully Diluted (3,362)

(8,461)

Non-cash mark to market of interest rate

swaps (1,530)

(4,366)

Foreign currency exchange loss (gain) -

continuing operations (a) 5

(139)

Foreign currency exchange

gain - discontinued operations (a) -

(58)

Adjustment for

Value Creation Plan 7,939

9,181

Comparable FFO

3,052

$

(3,843)

$

Comparable FFO per diluted share

0.02

$

(0.02)

$

Weighted average diluted shares

188,787

157,333

(a)

Foreign currency exchange gains or losses applicable to

third-party and inter-company debt and certain balance sheet items held by foreign

subsidiaries.

March 31,

Three Months Ended

31 |

Non-GAAP

to GAAP Reconciliations Operational Guidance

Low Range

High Range

North American same store Total RevPAR growth (a)

5.0%

7.0%

North American same store RevPAR growth (a)

6.0%

8.0%

(a) Includes North American hotels which are consolidated in our

financial results, but excludes the Four Seasons Jackson Hole and Four

Seasons Silicon Valley hotels, which were acquired in 2011.

Comparable EBITDA Guidance

Low Range

High Range

Net loss attributable to common shareholders

(79.3)

$

(64.3)

$

Depreciation and amortization

105.0

105.0

Interest expense

83.1

83.1

Income taxes

1.1

1.1

Noncontrolling

interests (0.3)

(0.3)

Adjustments from consolidated

affiliates (5.7)

(5.7)

Adjustments from unconsolidated

affiliates 28.3

28.3

Preferred shareholder dividends

24.2

24.2

Realized portion of deferred gain on

sale-leasebacks (0.2)

(0.2)

Adjustment for Value Creation Plan

8.8

8.8

Comparable

EBITDA 165.0

$

180.0

$

Comparable FFO Guidance

Low Range

High Range

Net loss attributable to common shareholders

(79.3)

$

(64.3)

$

Depreciation and amortization

103.8

103.8

Realized portion of deferred gain on

sale-leasebacks (0.2)

(0.2)

Noncontrolling interests

(0.2)

(0.2)

Adjustments from consolidated

affiliates (2.9)

(2.9)

Adjustments from unconsolidated

affiliates 15.5

15.5

Adjustment for Value Creation Plan

8.8

8.8

Other adjustments

(1.5)

(1.5)

Comparable FFO

44.0

$

59.0

$

Comparable FFO per diluted share

(b) 0.21

$

0.29

$

(b) Comparable FFO per diluted share has been

adjusted to reflect the 18.4 million shares issued in the Company's common equity offering which

closed on April 23, 2012.

2012 Guidance

(in millions, except per share data)

Year Ended

December 31, 2012

December 31, 2012

Year Ended

December 31, 2012

Year Ended

32 |

33

Thank You |