Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Carbonite Inc | d348469d8k.htm |

Tuesday, May 08, 2012

©

Carbonite, Inc | Company Confidential

Carbonite, Inc. (NASDAQ: CARB)

Investor Presentation

May 2012

1

Exhibit 99.1 |

2

©

Carbonite, Inc | Company Confidential

Safe Harbor Statement

Cautionary Language Concerning Forward-Looking Statements

These slides and the accompanying oral presentation contain

"forward-looking statements" within the meaning of the Securities Act of

1933, as amended, the Securities Exchange Act of 1934, as amended, and the Private

Securities Litigation Reform Act of 1995. These forward-looking

statements represent the Company’s views as of the date that they were first made based on the current intent,

belief or expectations, estimates, forecasts, assumptions and projections of the

Company and members of our management team. Words

such

as

“expect,”

“anticipate,”

“should,”

“believe,”

“hope,”

“target,”

“project,”

“goals,”

“estimate,”

“potential,”

“predict,”

“may,”

“will,”

“might,”

“could,”

“intend,”

and any variations of these terms or the negative of these terms and similar

expressions are intended to identify these forward-looking statements.

Those statements include, but are not limited to, statements regarding guidance on our

future financial results and other projections or measures of future performance,

and our expectations concerning market opportunities and our ability to

capitalize on them. Forward-looking statements are subject to a number of risks and uncertainties, many of which

involve factors or circumstances that are beyond the Company’s control. The

Company’s actual results could differ materially from those stated or

implied in forward-looking statements due to a number of factors, including, but not limited to, the Company’s ability to

profitably attract new customers and retain existing customers, the Company’s

dependence on the market for online computer backup services, the

Company’s ability to manage growth, and changes in economic or regulatory conditions or other trends affecting the

Internet and the information technology industry. These and other important risk

factors are discussed or referenced in our Quarterly Report

on

Form

10-Q

for

the

fiscal

quarter

ended

March

31,

2012,

which

is

available

on

www.sec.gov,

under

the

heading

“Risk

Factors”

and elsewhere, and any subsequent periodic or current reports filed by us with the

SEC. The Company anticipates that subsequent events and developments will

cause its views to change. Except as required by applicable law or regulation, the Company

does not undertake any obligation to update our forward-looking statements to

reflect future events or circumstances. |

3

©

Carbonite, Inc | Company Confidential

Rapid growth

in bookings, customers and revenue

Highly scalable

subscription-based model with strong visibility

New products

driving higher ASP, ARPU and margins

High

retention rates

Approaching

free cash flow breakeven

Financial highlights |

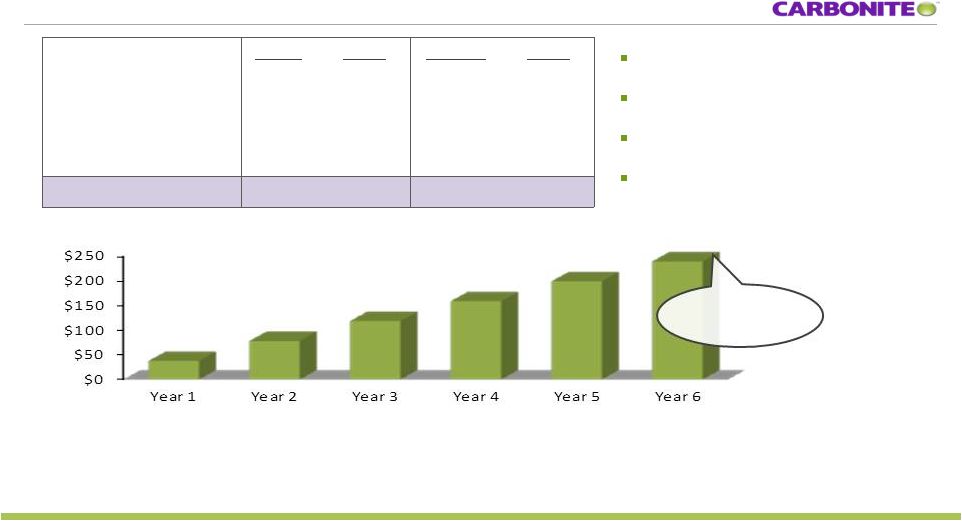

4

©

Carbonite, Inc | Company Confidential

Consistent bookings growth

Highly predictable subscription-based model with consistent bookings

growth Source: Carbonite SEC Filings

Note: Bookings during a period is defined as revenue recognized during the period

plus change in deferred revenue. See appendix for a reconciliation of

bookings to revenue for the periods presented. |

5

©

Carbonite, Inc | Company Confidential

Rapid revenue growth

Predictable revenue growth: record revenue every quarter since launch

Source: Carbonite SEC Filings |

6

©

Carbonite, Inc | Company Confidential

Our highly scalable business model

High lifetime value

Highly scalable

Strong visibility

Significant operating leverage

Cumulative gross margin per customer

$38

$78

$119

$159

$240

Source: Carbonite filings and management estimates

Based

on

1

year

Home

subscription,

5.99

year

customer

life

based

on

85.7%

annual

retention

rate

for

today’s

core

business

and

cost

structure.

Does

not

account

for

projected

future

decline

in storage, bandwidth costs or customer support. Excludes stock based compensation.

CAC represents $43.14 average customer acquisition costs based on full year 2011 advertising expense/

new

bookings

during

the

same

period

times

$59

purchase

price

for

a

one

year

Home

product

subscription.

Year 1

% rev

Lifetime

% rev

Revenue per customer

$59

100%

$354

100%

Depreciation & hosting

(13)

(22%)

(80)

(23%)

Customer support

(8)

(14%)

(34)

(10%)

Gross margin

$38

64%

$240

68%

$200

Business model illustration

5.6x gross

margin return

on CAC |

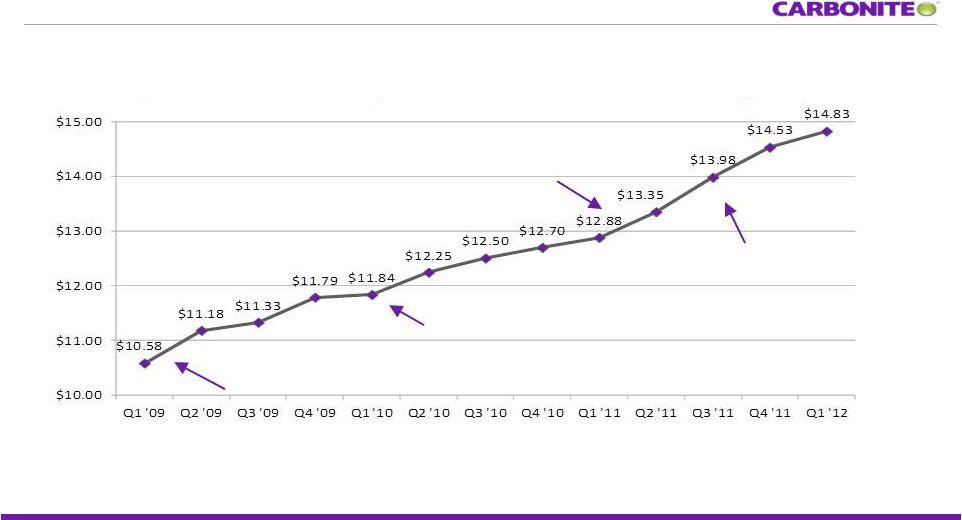

Tuesday, May 08, 2012

©

Carbonite, Inc | Company Confidential

Increasing revenue per customer

Consistent growth in revenue per customer, with further upside

potential from the recently launched Consumer and SMB offerings

Price increase and release of second

generation business products

Release of first generation

business product

Price increase

Release of two new

consumer products

Source: Carbonite filings

Note:

Calculated

as

revenue

for

any

given

quarter

divided

by

the

average

number

of

subscribers

during

that

quarter.

Average

number

of

subscribers

is

the

sum

of

the

total

number

of

subscribers

at

the

end

of

a

quarter

plus

the

total

number

of

subscribers

at

the

end

of

the

prior

quarter,

divided

by

2.

7 |

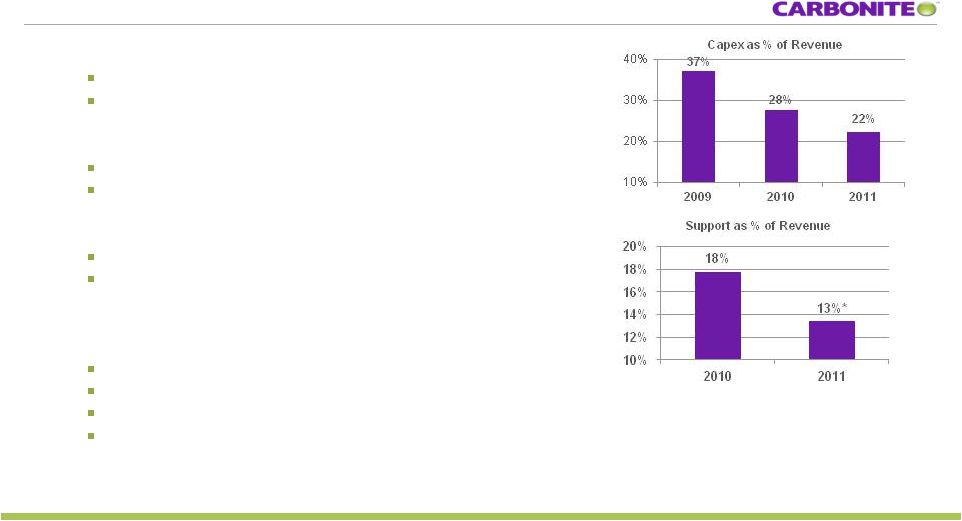

8

©

Carbonite, Inc | Company Confidential

Mix shift toward new products

Adoption and upsell upon renewal ramps over time

Higher ASP and higher gross margins

Rapid decline in storage costs at ~30-40% per year

4 year depreciable life, delayed impact to P&L

Temporary flattening in 2012 from Thailand flooding

Unlimited free support: major differentiator to our offerings

50% of lifetime support contacts during trial and year 1,

remainder over next ~5 years of a customer's life

Electricity and broadband: largest components of COS

after support and depreciation

Datacenter locations moving to lower cost electricity areas

Economies achieved by increasing equipment density

High BB consumption during initial upload

Purchasing power at scale

Source: Carbonite filings and management estimates. Support excludes stock based

compensation expense. Drivers of margin expansion

*2011 Included transition

of support to US |

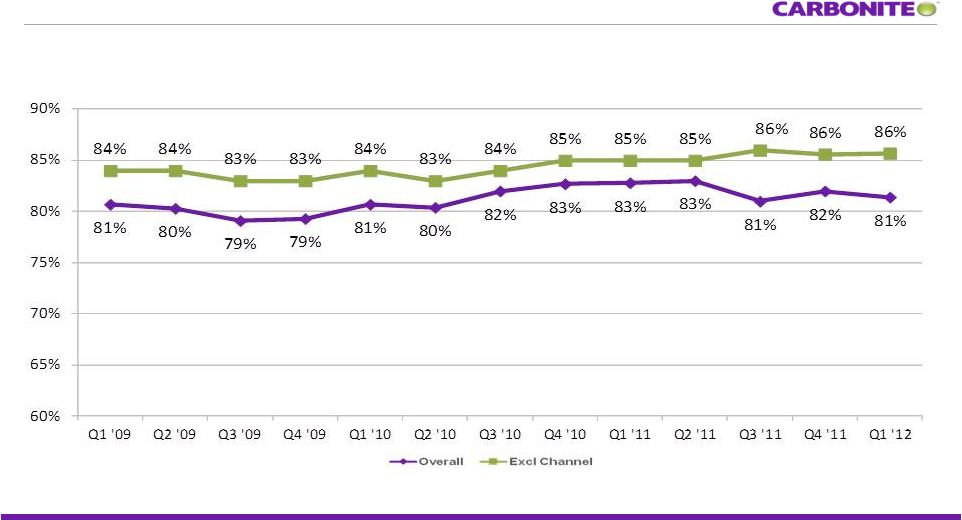

Tuesday, May 08, 2012

©

Carbonite, Inc | Company Confidential

Strong customer retention

Consistently high customer retention rates, key to our model

Overall includes discontinued channel including force

churn customers (20K in Q3 2011 and 15K in Q1 12)

9

Source: Carbonite filings

Note: Annual retention rate is the percentage of customers on the last day of the

prior period who remain customers on the last day of the current period.

Channel sales being deliberately phased out. |

10

©

Carbonite, Inc | Company Confidential

Business model with declining costs per customer leading to

expanding margin profile:

Gross profit

per customer

Source: Carbonite SEC Filings

1. Adjusted for stock-based compensation and amortization of intangibles.

Improving

margins

Gross Margin

*2011 included costs of transition support to US

and duplicate datacenter cost

(DC relocation completed end of Q1 2012)

1

1 |

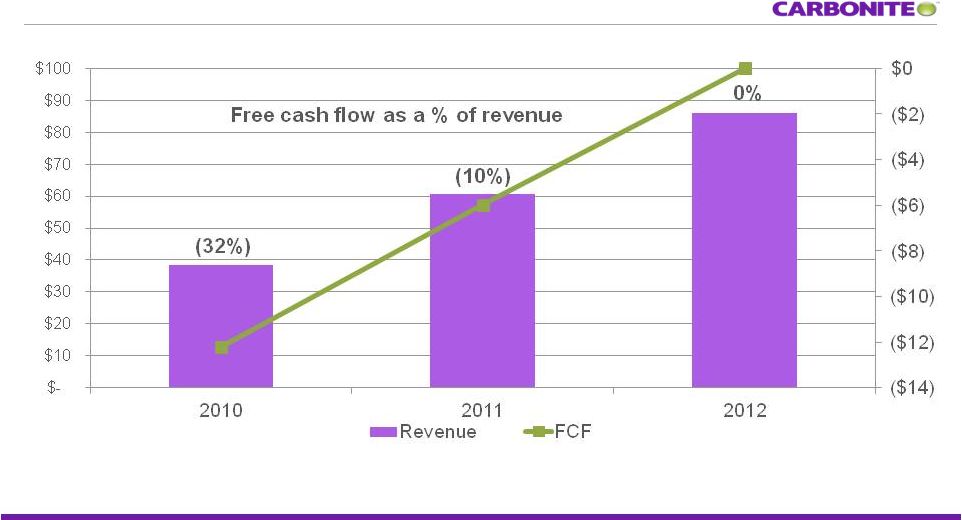

Revenue

and free cash flow trajectory (in million’s)

Source: Carbonite filings

2012 FCF expectation and revenue at mid point of guidance range provided in Q1 2012

earnings release. FCF expected at or near breakeven and excludes cash impact

of non GAAP adjustments Revenue

FCF (Burn)

11

©

Carbonite, Inc | Company Confidential |

12

©

Carbonite, Inc | Company Confidential

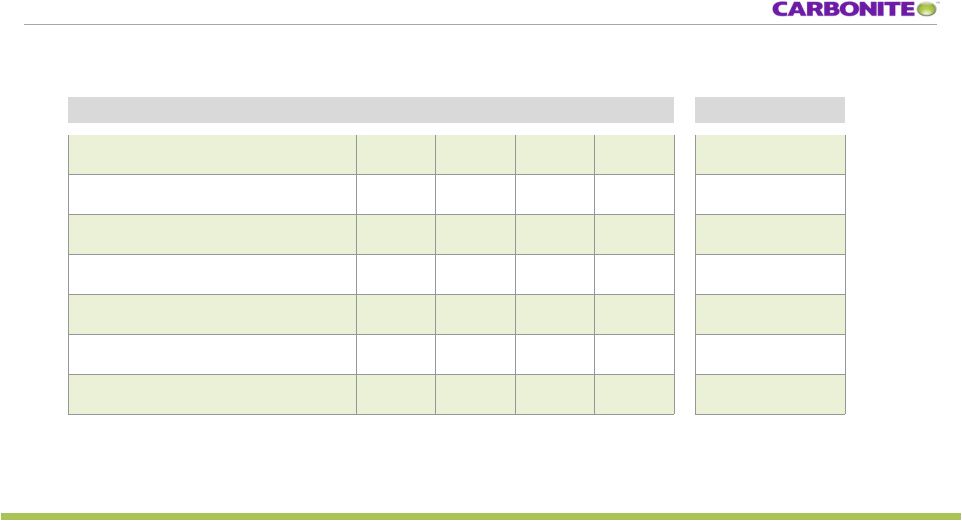

Long term financial model

Financial metric

Historical performance¹

LT Objectives²

2008

2009

2010

2011

% of revenue

Revenue

100%

100%

100%

100%

100%

Gross margin*

48%

53%

58%

62%

76-78%

Research & development*

56%

32%

28%

26%

19-21%

General & administrative*

28%

12%

10%

9%

8-9%

Sales & marketing*

179%

110%

86%

62%

34-36%

EBITDA margin*

(197%)

(85%)

(53%)

(22%)

20-25%

FCF margin*

(151%)

(42%)

(32%)

(10%)

25-30%

1.

Source: Carbonite filings. Financials exclude stock based compensation,

amortization of intangibles and patent litigation expenses. 2.

These objectives are forward-looking, are subject to significant business,

economic, regulatory and competitive uncertainties and contingencies, many of which are beyond the

control

of

the

Company

and

its

management,

and

are

based

upon

assumptions

with

respect

to

future

decisions,which

are

subject

to

change.

Actual

results

will

vary

and

those

variations

may

be

material.

For

discussion

of

some

of

the

important

factors

that

could

cause

these

variations,

please

consult

the

“Risk

Factors”

section

of

the

preliminary

prospectus.

Nothing

in

this

presentation

should

be

regarded

as

a

representation

by

any

person

that

these

objectives

will

be

achieved

and

the

Company

undertakes

no

duty

to

update its objectives.

Business model with significant operating leverage

* Percent of revenue |

13

©

Carbonite, Inc | Company Confidential

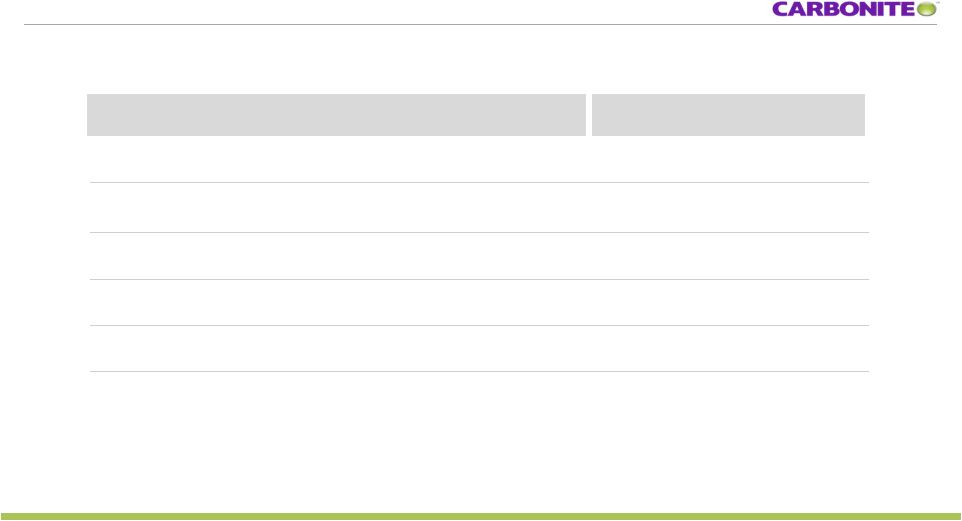

Strong balance sheet

Cash and short-term investments

$68.1

Working capital (deficit)

$9.1

Total assets

$98.3

Deferred revenue, including current portion

$65.6

Total liabilities

$78.5

Total

stockholders’

equity

(deficit)

$19.9

Source: Carbonite SEC Filings

$ in millions

As of March 31, 2012

($mm) |

14

©

Carbonite, Inc | Company Confidential

Investment highlights

•

Enormous world-wide market opportunity

•

“Category killer”

with established brand leadership

•

Personal cloud important market opportunity

•

Proprietary technology & scale

•

Strong competitive advantages

•

Proven direct marketing expertise

•

Multiple avenues for sustained growth |

©

Carbonite, Inc | Company Confidential

Questions?

15 |

16

©

Carbonite, Inc | Company Confidential

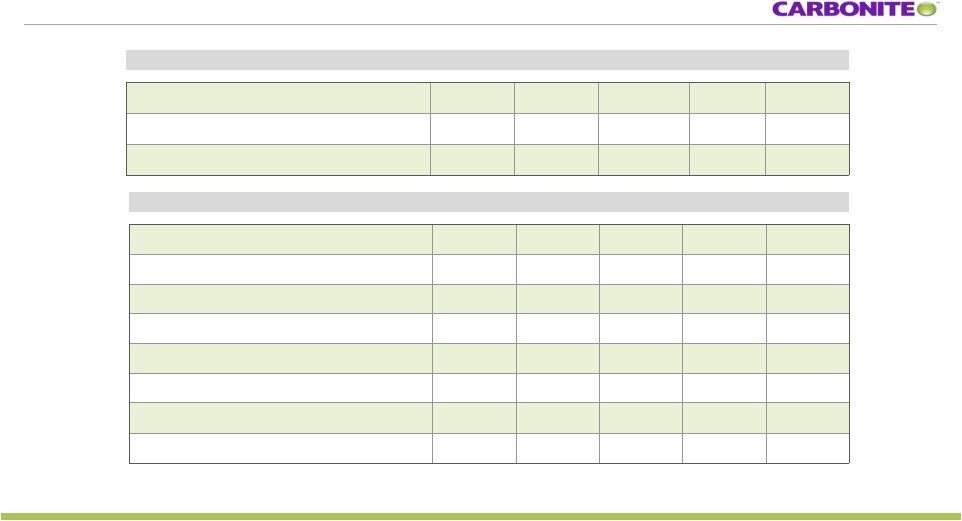

Non-GAAP reconciliation

Source: Carbonite SEC Filings

1. Excludes $586k from acquisitions

$ in thousands

2008

2009

2010

2011

Q1 2012

Revenue

$8,202

$19,114

$38,563

$60,512

18,547

Plus: Change in deferred revenue

5,867

13,743

15,578

20,388

(1)

5,947

Bookings

$14,069

$32,857

$54,141

$80,900

$24,494

$ in thousands

2008

2009

2010

2011

Q1 2012

GAAP Loss from Operations

$(17,852)

$(19,602)

$(25,896)

$(23,554)

$(9,103)

Add: Stock-based Compensation

203

390

542

1,445

956

Add: Amortization of Intangibles

0

0

0

155

67

Add: Patent Litigation Expenses

0

0

39

966

207

Add: Lease exit charge

0

0

0

0

1,174

Non-GAAP Loss from Operations

$(17,649)

$(19,212)

$(25,315)

$(20,988)

$(6,699)

Plus: D&A Less Amort. Of Intangibles

1,481

2,977

5,060

7,715

2,337

Adjusted EBITDA

$(16,168)

$(16,235)

$(20,255)

$(13,273)

$(4,362) |