Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - Alternate Energy Solutions, Inc. | Financial_Report.xls |

| EX-32.1 - EXHIBIT 32.1 - Alternate Energy Solutions, Inc. | v308417_ex32-1.htm |

| EX-31.1 - EXHIBIT 31.1 - Alternate Energy Solutions, Inc. | v308417_ex31-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2011

¨ TRANSITION REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ________ to ________

Commission File No.: 000-53107

| ALTERNATE ENERGY SOLUTIONS, INC. | ||

| (Exact name of registrant as specified in its charter) |

| Nevada | 26-0875492 | |

|

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

1061 Highway 92 N, Fayetteville Georgia 30214

(Address of principal executive offices)

(678)489-6055

Issuer’s telephone number

Securities registered under Section 12(b) of the Exchange Act:

None

Securities registered under Section 12(g) of the Exchange Act:

Common Stock, par value $0.0001 per share

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

¨ Yes x No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act.

¨ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

¨ Yes ¨ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ | Accelerated filer ¨ |

| Non-accelerated filer ¨ | Smaller reporting company x |

| (Do not check if a smaller reporting company) |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ¨Yes x No

The aggregate market value of the voting and non-voting common equity held by non-affiliates was approximately $-0- based upon a closing price of $-0- per share on June 30, 2011.

As of April 6, 2012 there were 15,547,134 shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None.

| TABLE OF CONTENTS | |

| FORWARD-LOOKING STATEMENTS | ii |

| PART I | |

| Item 1. Business | 1 |

| Item 1A. Risk Factors | 26 |

| Item 1B.Unresolved Staff Comments. | 40 |

| Item 2. Properties. | 40 |

| Item 3. Legal Proceedings. | 40 |

| Item 4. Reserved | 40 |

| PART II | |

| Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. | 41 |

| Item 6. Selected Financial Data. | 41 |

| Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations. | 42 |

| Item 7A. Quantitative and Qualitative Disclosure about Market Risk | 51 |

| Item 8. Consolidated Financial Statements and Supplementary Data | 52 |

| Item 9A. Controls and Procedures | 53 |

| Item 9B. Other Information | 55 |

| PART III | |

| Item 10. Directors, Executive Officers and Corporate Governance | 55 |

| Item 11. Executive Compensation | 57 |

| Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 59 |

| Item 13. Certain Relationships and Related Transactions, and Director Independence | 59 |

| Item 14. Principal Accountant Fees and Services | 60 |

| PART IV | |

| Item 15. Exhibits and Financial Statement Schedules | 60 |

| i |

FORWARD-LOOKING STATEMENTS

Statements in this Annual Report on Form 10-K contain various forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 (the “Securities Act”) and Section 21E of the Securities Exchange Act of 1934 (the “Exchange Act”), which represent our management’s beliefs and assumptions concerning future events. When used in this document and in documents incorporated by reference, forward-looking statements include, without limitation, statements regarding financial forecasts or projections, and our expectations, beliefs, intentions or future strategies that are signified by the words “anticipate,” “believe,” “estimate,” “expect,” “intend,” “may,” “objective,” “outlook,” “plan,” “project,” “possible,” “potential,” “should,” “continue” and similar expressions. The forward-looking statements in this Annual Report on Form 10-K speak only as of the date of this Annual Report on Form 10-K. We disclaim any obligation to update these statements (unless required by securities laws), and we caution you not to rely on them unduly. We have based these forward-looking statements on our current expectations and assumptions about future events. While our management considers these expectations and assumptions to be reasonable, they are inherently subject to significant business, economic, competitive, regulatory and other risks, contingencies and uncertainties, most of which are difficult to predict and many of which are beyond our control. These and other important factors, including those discussed in Item 1A “Risk Factors” of this report, may cause our actual results, performance or achievements to differ materially from any future results, performance or achievements expressed or implied by these forward-looking statements.

These risks, contingencies and uncertainties include, but are not limited to, the following:

| · | We may not be able to implement our strategy as planned or at all; |

| · | We may not be able to secure an optimal site for our plant; |

| § | We may not be able to obtain the approvals and permits that will be necessary in order to construct our facility as planned; |

| · | We may encounter unanticipated difficulties in constructing our plant; |

| § | Delays and defects may cause our costs to increase to a level that would make our facility too expensive to construct or unprofitable; |

| § | The absence of operations and revenues raises substantial doubt about our ability to continue as a going concern. |

| § | We are not generating any revenue, have limited capital resources and are dependent entirely upon our management to fund our operations; |

| § | Our proprietary equipment, systems and processes have never been deployed on a commercial scale and they may not function as efficiently or effectively as we anticipate or at all; |

| · | Our management has never operated a biodiesel facility; |

| · | Factors beyond our control may impact the efficient and effective operation of our plant; |

| § | If we fail to develop a market for our biodiesel at favorable prices, our business, operating results and financial condition may be adversely affected; |

| § | The EPA has not approved palm-oil/PKO, our proposed feedstock to produce fuel as a qualified pathway from which to produce biodiesel under RFS2; |

| · | We will rely on third parties to supply feedstock, which may impact our operations in many ways; |

| ii |

| § | If our proposed palm oil suppliers are unable to satisfy our requirements for PKO at the prices at which they have committed, we will have to identify other sources of feedstock, the price and availability of which is subject to significant volatility; |

| § | Upon commissioning of our production facilities, we will have to demonstrate that they comply with applicable EPA regulations which could be costly and time consuming; |

| § | Initial and ongoing compliance and reporting under RFS2 will be difficult, costly and time consuming; |

| § | We are highly dependent on our management team and the loss of their services would have a material adverse effect on our business; |

| § | Problems with product quality or product performance could result in a decrease in customers and revenue; |

| § | Biodiesel gels in colder temperatures, which could have an adverse effect on our sales and the biodiesel industry generally; |

| § | Our inability to effectively protect our intellectual property could negatively affect our ability to comp |

| · | We may not be able to compete effectively in our industry; |

| · | Technological advances in our industry may render our intellectual property obsolete; |

| § | Competition resulting from advances in alternative fuels may reduce the demand for biodiesel and negatively impact our profitability; |

| § | We expect that our business will be subject to seasonal fluctuations, which could adversely affect our financial results; |

| § | A variety of factors could cause the price of biodiesel to decline, including, for example, if supply outpaces demand, which would have a significant negative impact on our financial performance; |

| § | Imported biodiesel may be a less expensive alternative to our biodiesel, which could impair our ability to sell our product and negatively impact our financial condition and results of operations; |

| § | There is uncertainty regarding the use of biodiesel in newer diesel engines, which may inhibit or deter the use of biodiesel as a transportation fuel; |

| § | Growth in the sale and distribution of biodiesel depends on the development of new technologies and infrastructure, which may not occur on a timely basis, if at all, and our operations could be adversely affected by infrastructure disruptions; |

| § | Environmental, health and safety laws, regulations and liabilities may have an adverse effect on our operations; |

| § | Changes in industry specification standards for biodiesel may increase production costs or require additional capital expenditures to upgrade and/or modify our biodiesel production facilities to meet them. Such upgrades and/or modifications may entail delays in or stoppages of production; |

| § | Adverse public opinions relating to the environmental impact of biodiesel could constrain the demand for our product and harm our business; |

| · | Adverse public opinions concerning the biodiesel industry in general could harm our business; |

| § | Our management has identified material weaknesses in our internal controls over financial reporting, and we may be unable to develop, implement and maintain appropriate controls in future periods; |

| iii |

| · | we have no independent audit committee and rely on our full board of directors functions in such capacity which may hinder its effectiveness in fulfilling the functions of the audit committee; |

| · | the issuance of stock to fund our operations may dilute your investment and reduce your equity interest;. |

| · | the issuance of preferred stock could adversely impact the rights of holders of our common stock; |

| · | There is no trading market for our common stock; |

| · | any market that develops for our common stock likely will be illiquid and the trading price of our common stock could be volatile and unrelated to our operations; |

| · | substantial sales of our common stock, or the perception that such sales are likely to occur, could cause the price of our common stock to decline in any market that may develop for our common stock; |

| · | our failure to maintain effective internal control over financial reporting could have a material adverse effect on our business, our operating results and the value of our common stock. |

| iv |

PART I

Item 1. Business

Overview

We are a development stage company that has no operating history or revenue. We are planning to construct and operate a biodiesel manufacturing facility that, when completed, will have the capacity to produce up to 80 million gallons per year, or MGY, nameplate capacity of biodiesel fuel. We also expect the biodiesel plant to annually produce approximately 750,000 gallons of crude glycerin, which is a co-product of the biodiesel production process. Glycerin has many applications as an ingredient or processing aid in cosmetics, toiletries, personal care, drugs and food products.

Our plan of operation contemplates that we will construct a temporary facility at a leased site that will have a production capacity of 11.2 MGY upon full build-out. At such time as our financial resources permit and demand for our biodiesel warrants, we will construct a permanent facility near the proposed site of our temporary facility to which we will relocate our operations.

The effectuation of our business plan is contingent upon the receipt of financing. We cannot be certain that financing will available on acceptable terms, if at all.

Our business plan reflects our core principals encompassing an intense commitment to cost control and sensitivity to environmental sustainability. We have been considerate and deliberate in devising solutions to the operating constraints that we believe have inhibited the biodiesel industry from achieving its potential. We believe that we have developed a business model that will allow us to achieve success as the industry continues to struggle with a range of economic challenges, the most pressing of which has been the cost and availability of biomass, which accounts for 70% to 90% of the total production cost. The high cost producers' pay for biomass has prevented them from selling product at prices competitive with diesel fuel because, even accounting for government incentives that have been made available to producers, it is more expensive to produce biodiesel than diesel fuel.

We have developed our business plan on the basis that we would utilize palm kernel oil, or PKO, as the biomass, or feedstock, from which we will manufacture biodiesel. PKO is a variety of palm-oil extracted from the kernel, or seed, of the fruit of the African oil palm tree. We believe that we have locked-in a stable supply of PKO for our operations at purchase prices that will provide us with a distinct competitive advantage compared to soy, corn and waste oils, the biomass utilized by most US biodiesel manufacturers, and allow us to produce biodiesel at prices competitive with petroleum based diesel fuel.

As of the date of this Annual Report, the Environmental Protection Agency, or EPA, had not qualified palm oil/PKO as a pathway to producing renewable fuel under the renewable fuel standards set by Congress under the Energy Independence and Security Act (EISA) of 2007, which we refer to as RFS2. When RFS2 went into effect in July 2010, the EPA stated that it was actively analyzing palm-oil based pathways to determine if it qualifies as a valid pathway for the production of biodiesel and that its preliminary modeling and analysis indicated that palm-oil would qualify as a valid pathway. At the time, the EPA anticipated that this analysis would be completed by the end of 2010. The EPA has not yet concluded its analysis to determine if a palm-oil based pathway to producing renewable fuel qualifies under RFS2.

We have developed proprietary processes and systems for manufacturing biodiesel, from which we expect to derive a meaningful competitive advantage. Our production equipment is based on an innovative combination of existing, proven technologies that integrate multiple types of programmable control systems to maximize the efficiency in throughput that we believe will increase production efficiency, reduce production costs and improve plant economics when compared to other biodiesel production plants. We will produce biodiesel using a series of small batch/flow processing systems, when compared to the large single line plants being constructed today. We believe that we can construct our production equipment less expensively and more quickly than other biodiesel producers. We will fabricate our production equipment in-house from readily available parts and equipment. These factors will allow us to add capacity quickly as demand warrants. We believe that our technology will enable us to produce biodiesel that meets the standard for biodiesel established by The American Society of Testing and Materials, or ASTM, which is called ASTM D-6751, that has been adopted by the EPA.

| 1 |

We believe that the EPA’s delay in qualifying palm oil/PKO as an approved pathway for the production of renewable fuels under RFS2 has inhibited our ability to raise the cash we require to construct our temporary production facility. In order to further the development of our business, it is our intention to develop a single reactor facility capable of producing approximately 624,000 gallons per year of biodiesel that would allow us to validate our concepts, equipment, manufacturing techniques and revenue potential. We would site the unit at laboratory space currently provided to us free of charge by our President. Upon production of first biodiesel, we would seek to obtain ASTM – D 6751 certification that would allow us to sell it in any state after registering under state tax codes. Regardless of whether the EPA has qualified palm oil/PKO as a pathway to producing renewable fuel, we likely will utilize PKO as the feedstock in our operations, though we may also utilize other biomasses to demonstrate the multi-feedstock capabilities of our equipment. We believe that though the fuel we manufacture from PKO will not qualify as a renewable fuel under RFS2, we will be able to sell our biodiesel into numerous other markets that require cleaner burning fuel to blend with diesel to comply with applicable clean air regulations.

Corporate Information

The Company was incorporated under the name “The Forsythe Group Two, Inc.” in the State of Nevada on October 12, 2007. We were originally organized as a “blank check” shell company to investigate and acquire a target company or business seeking the perceived advantages of being a publicly held corporation.

On July 27, 2010, we closed a share exchange transaction (“Share Exchange”), described below, pursuant to which we (i) became the 100% parent of BioFuel Technologies, Inc., a Georgia corporation (“BFT”), (ii) assumed the operations of BFT and (iii) changed our name from The Forsythe Group Two, Inc. to Alternate Energy Solutions, Inc.

BFT was incorporated in the State of Georgia on August 1, 2008 and since inception had engaged in developing and refining its business model.

Our corporate offices are located at 1061 Highway 92 N., Fayetteville, Georgia 30214, where our telephone number is (678) 489-6055.

Recent Events

Completion of Share Exchange

On June 16, 2010, we entered into a share exchange agreement (the “Exchange Agreement”) with all fourteen holders of outstanding shares of the common stock of BFT. Pursuant to the Exchange Agreement, we agreed to issue shares of our common stock in exchange for all of the issued and outstanding securities of BFT (the “Share Exchange”). The Share Exchange closed on July 27, 2010. Upon the closing of the Share Exchange, we (i) became the 100% parent of BFT, (ii) assumed the operations of BFT and (iii) changed our name from The Forsythe Group Two, Inc. to Alternate Energy Solutions, Inc.

Upon the closing of the Share Exchange, we issued one share of our common stock for each share of BFT common stock outstanding resulting in the issuance of an aggregate of 14,697,134 shares of our common stock to the shareholders of BFT. Immediately after the closing of the Share Exchange, there were 15,397,134 shares of our common stock outstanding, of which approximately 95.45% were held by the former stockholders of BFT and approximately 4.55% were held by our sole stockholder prior to the closing date.

Upon the closing of the Share Exchange, our sole director and officer, Hunt Keith, appointed Kenneth Rakestraw and Mark Harris as directors of the Company and resigned from all positions he held with the Company.

As a condition to the obligations of BFT shareholders under the Exchange Agreement, we entered into a Indemnification Agreement with Quality Investment Services, LLC (“QIS”), our sole stockholder prior to the Share Exchange, whereby it (i) cancelled and forgave all amounts due under a series of Non-Negotiable Demand Promissory Note executed by the Company in favor of QIS which accrued interest at the rate of 8% per year and (ii) surrendered for cancellation 300,000 shares of common stock that it owned. As of the closing of the Share Exchange, we owed QIS an aggregate of $64,090 under the Note, including $55,684 in principal and $8,406 in accrued interest.

| 2 |

As a condition to the consummation of the Exchange Agreement, we entered into a series of Lock-Up Agreements with respect to 14,870,000 shares of our common stock, that comprises the shares held by QIS (700,000 shares), all of shares issued to BFT's directors and officers (13,000,000 shares) and 1,170,000 shares issued to two additional holders of our common stock. Under the Lock Up Agreements, the stockholders have agreed that (i) they will not sell or transfer any shares of our common stock held as of the closing of the Share Exchange until a date that is one hundred and eighty days after the effective date of the registration statement that includes their shares to be filed pursuant to the Registration Rights Agreement described below and (ii) upon the conclusion of the initial lock up period, such persons will not sell or transfer more than 1/36th of the shares of common stock they held as of the date of the Share Exchange during any month thereafter.

Pursuant to the terms of the Exchange Agreement, we entered into a Registration Rights Agreement with 16 persons holding an aggregate of 1,237,134 shares of our common stock issued in the Share Exchange, which includes 10,000 shares held by the directors and officers of BFT, and 700,000 shares held by QIS. Pursuant to the Registration Rights Agreement, we will (i) file the registration statement within 180 days of the date of the Share Exchange, subject to our right to withdraw the registration statement under certain circumstances without penalty, (ii) pay all costs and expenses incident to such registration and (iii) maintain the effectiveness of the registration statement filed for the benefit of the holders of the shares included therein for a minimum of twelve months following its effective date.

For accounting purposes, the Share Exchange was treated as a reverse acquisition with BFT as the acquirer and the Company as the acquired party. As a result, the business and financial information included in this report is the business and financial information of BFT.

Our Competitive Strengths

We believe that the following competitive strengths will enable us to compete effectively and to capitalize on the growth of the market for biodiesel fuel:

| · | Biomass Supply and Price – We have received commitment letters from biomass growers that will allow us to purchase all of our feedstock requirements at favorable prices. We believe that we have locked-in a stable supply of biomass that will allow us to purchase quantities in excess of twice our projected annual requirements for a period of one year from the date of the first shipment at highly favorable prices when compared to current domestic feedstock prices. Our suppliers have indicated their willingness to discuss renewing these commitments on one year terms on prices to be negotiated. |

| · | Scalability and Flexibility of Production Equipment – We can construct our multi-feedstock, small batch/flow production equipment quickly and economically, which will allow us to commence operations promptly after receiving financing and to add capacity quickly and inexpensively by building new production systems as demand for our product warrants and our financial condition permits. This scalability and flexibility we allow us to maintain a close balance between production capacity and market demand for our product. |

| · | Logistics – We have selected an urban port location at which to develop our facility, which should reduce costs and maximize profits, particularly by minimizing the cost of biomass and reducing transportation costs, and provide us access to a well-developed transportation infrastructure and a wide base of customers within our target markets. |

| · | Management – Our current management team has considerable experience with the intricacies of the equipment, processes and systems that comprise our technology and equipment. They have participated in the commissioning, operation and management of large-scale facilities. |

| · | In-house Engineering and Construction Expertise – We will fabricate our production systems in-house, which will decrease our time to market, reduce our construction costs and allow us to expand capacity as plant economics dictate within our financial and operational parameters. |

| 3 |

Our Growth Strategy

We are committed to enhancing profitability and cash flows through the following strategies:

| · | Progressive Asset Growth through Profit Reinvestment – The modular nature of our equipment will allow us to construct individual diesel production systems quickly and inexpensively and commence generating revenue with a relatively small investment. We will reinvest our profits to increase capacity to construct additional production systems. |

| · | Maintain a Close Balance of Capacity to Demand – The ability to fabricate our production equipment quickly and economically will allow us to maintain a close balance between production capacity and market demand for our product. |

| · | Dedication to Cost Control and Efficiency – We will develop and construct our facility with a focus on minimizing cost inputs such as biomass and transportation. Once our plant is operational, we will continue to promote a culture of cost control and efficiency regardless of economic cycle. |

Our Industry

Biodiesel

Biodiesel is a clean-burning alternative to petroleum-based diesel. Biodiesel is manufactured from renewable feedstocks such as soybean, palm, canola and sunflower oil, as well as from animal fats, fish oils, algae and recycled cooking oils. New feedstocks from which biodiesel is manufactured are being developed rapidly. Biodiesel is produced by reacting a feedstock with methanol in the presence of a catalyst, which yields biodiesel and glycerin as a co-product. Biodiesel can be a direct replacement for diesel and can be blended with diesel fuel in any ratio. Biodiesel blends are primarily used as a fuel for trucks and automobiles. It can also be used as home heating oil and as an alternative fuel in a variety of other applications, including marine transportation, electrical generation, farm equipment and mining operations.

According to the National Biodiesel Board, or NBB, among other environmental benefits, biodiesel:

| · | in its pure, or neat, form, reduces the net gain in carbon dioxide, or CO2, emissions by 78% compared to petroleum fuels; |

| · | reduces tailpipe emissions of particulate matter (soot or black carbon) by 47%, which is recognized as a major contributor to global warming, as well as a critical air pollutant associated with reduced human health, particularly among children and asthmatics; |

| · | reduces emissions of unburned hydrocarbons by 67%; |

| · | produces 48% less carbon monoxide than diesel fuels; and |

| · | contains no sulfur and generates no sulfur emissions, a major source of acidification in rain and surface water. |

Biodiesel has better lubricating properties and a much higher cetane rating (the diesel equivalent of octane) than today's lower sulfur diesel fuels. The use of biodiesel in its neat form, B100, or in a blend with petroleum-based diesel reduces fuel system wear and in low levels in high pressure systems increases the life of the fuel injection equipment that relies on the fuel for its lubrication, including high pressure injection pumps, pump injectors and fuel injectors.

U.S. Biodiesel Production

In 2007, the U.S. consumed approximately 64 billion gallons of diesel according to the Energy Information Administration, or EIA. Biodiesel production in the U.S. peaked in 2008 at approximately 691 million gallons and was approximately 545 million gallons in 2009. Analysts attribute the decline in production in 2009 to poor economic conditions as a result of the recession. Production in 2010 dropped to an estimated 315 million gallons, which many attribute to the expiration of the biodiesel tax credit, which provides a $1 credit for each gallon of biodiesel produced and which has allowed biodiesel to remain competitive with diesel fuel, and a tariff imposed by the European Union on biodiesel imported from the United States. Congress restored the tax credit for 2011. The NBB estimates that in 2008, U.S. biodiesel producers sold just over 600 million gallons of biodiesel, including approximately 300 million gallons in the U.S.

| 4 |

According to the National Biodiesel Board, or NBB, as of June 2009, there were 173 biodiesel production facilities in operation in the U.S. with reported aggregate capacity of approximately 2.68 BGY and 29 facilities under construction or expansion with expected additional annual production capacity of approximately 427 MGY. (The foregoing statistics cannot be currently verified given the recent spate of plant closures or curtailed production as a result of the downturn in the economy, the lapse in the biodiesel production tax credit during 2010 and the tariff imposed by the EU on US imports ). While it appears that there currently exists overcapacity, a condition that will be exacerbated by the new plants that may come on line (based upon pre 2010 information), we believe that the market potential for biodiesel remains significantly higher than current and projected production levels and the EIA predicts that the market will continue to absorb biodiesel supply for the foreseeable future. We believe that biodiesel production will begin to increase in response to regulations promulgated by the EPA that became effective on July 1, 2010 (RFS2) implementing the revised renewable fuel standards established by Congress under the Energy Independence and Security Act (EISA) of 2007 and the renewal of the biodiesel tax credit.

Industry Drivers

We believe that federal legislative initiatives that encompass a diverse range of critical national interests are driving the current growth in the alternative fuels industry and will continue to spur robust growth in the decades to come. The federal legislation addresses energy security issues, environmental interests, health concerns and economic objectives. In addition, we believe that market forces are generating demand for biofuels worldwide.

| · | Environmental and Health Concerns. Legislative initiatives have been enacted over the last several years that target the environment and public health concerns by seeking to reduce GHG emissions that are considered by many to be the primary cause of global warming. These measures require low sulfur, lighter, clean-burning fuels, such as biodiesel, and mandate the introduction of specified minimum quantities of alternative fuels derived from renewable sources into the national fuel supply. We believe that the implementation of the regulations implementing RFS2 on July 1, 2010 should reinvigorate the industry in the short- and long-term. A discussion of the specific legislative measures follows, under the heading “ – Federal Government Initiatives Affecting Biodiesel Production and Use.” |

| · | Economic Dynamics. A host of economic factors are driving the growth of domestically produced alternative, renewable fuels, such as biodiesel. Key economic factors include dwindling global oil reserves; mitigating the economic uncertainty and instability resulting from the price volatility of petroleum-based fuels and the development of the biofuels industry as a domestic economic engine that would create new jobs and taxable revenues. |

| · | Strategic Issues. Strategic factors that encompass the security and diversity of the nation's energy supply serve as long-term drivers of our industry. Biodiesel and the feedstocks from which it is produced can be grown domestically and throughout the world, thereby allowing the nation to diversify its sources of fuel and reduce reliance on energy imported from the Middle East and the vulnerability inherent in such reliance. Biodiesel can be blended with petroleum-based diesel fuel to extend the life of existing petroleum reserves and, as a source of ultra-clean fuel, to blend with heavier/dirtier conventionally refined diesel to comply with environmental regulations. |

| · | Market Forces. Many of the factors referenced above are creating a global growth in demand for clean diesel fuel which can be satisfied with alternative fuels, such as biodiesel. For example, the U.S. is experiencing an increasing shortage of petroleum refining capacity during a period in which demand for refined petroleum products is expected to increase. The expanded use of biodiesel could mitigate the shortage of refining capacity. Biodiesel can be integrated into the existing U.S. fuels distribution infrastructure (tankers, pipelines, trucks and filling stations) by making relatively minor modifications to such equipment, obviating the need to develop new and costly infrastructure. Biodiesel can be used directly in existing diesel engines, the use of which is increasing in the U.S., given their higher fuel efficiency as compared to conventional gas burning engines. The use of biodiesel can improve engine performance given its higher cetane number (the diesel equivalent of octane) than most diesel fuel, and extend engine life because it burns more cleanly than diesel fuel. Blending biodiesel with ultra low sulfur diesel, or ULSD, even at low levels (1 to 2%), also provides added lubricity, which improves engine performance. |

| 5 |

U.S. Market Opportunity for Biodiesel

Biodiesel can be substituted for petroleum-based diesel in virtually every potential context, either in its blended or pure form. Biodiesel allows users who are subject to federal and state laws that mandate the use of alternative fuels to satisfy these obligations. In addition, users in certain industries that are subject to federal and state clean air laws (such as farm vehicles and trucking fleets), can blend biodiesel with diesel fuel to reduce emissions to mandated levels and allow them to satisfy those laws. Therefore, we believe that biodiesel markets are diverse and that biodiesel could be attractive to a large number of current diesel consumers, including:

Government/Public Sector Users: These include municipal fleet owners at every tier, federal, state and city, in every sector, including, for example, department of transportation vehicles, city and school buses, and state university-owned vehicles. In view of laws and regulations adopted by the federal government and many states that require the use of alternative fuels in government-owned vehicles and the purchase of alternative fuel vehicles, or AFV's, where economically comparable, and in their effort to satisfy the requirements of the EPAct and EISA (discussed below), we expect early adoption and deep penetration of municipal and public sector fleets.

Retail Users: These include, private fleet owners/operators, such as trucking companies; commercial farm equipment owners; the aviation industry; construction vehicles and equipment; and retail customers such as fueling stations. Penetration of biodiesel in the retail market will be achieved primarily by distribution to oil companies, independent fuel station owners, marinas and railroad operators. We believe that retail distribution may offer the best potential for higher margin customers.

Wholesale Market/Biodiesel Marketers: The wholesale market includes selling biodiesel directly to fuel blenders or through biodiesel marketers. Fuel blenders purchase pure biodiesel (B100) from biodiesel production plants, blend it with regular diesel fuel according to specifications, and deliver a final product to retailers.

Additional Markets: Additional markets for biodiesel are emerging because of the biodiesel incentives, high energy prices and innovation. These may include sales to power generation facilities or by developing cogeneration power plants using biodiesel to provide electricity to power industrial plants, in which excess electricity could be sold back to electrical grids allowing electric companies to meet Renewable Portfolio Standards (described below). Further, a potential market exists for sales of biodiesel to customers as a cleaner burning heating oil replacement or additive.

Federal Government Initiatives Affecting Biodiesel Production and Use

In recent years, federal, state and local governments have enacted legislative incentives and mandates to encourage the production and use of biodiesel. The present strong Presidential support for renewable fuels is driven by an increased embrace of the economic, environmental and security benefits of renewable fuels. The renewable fuel standard, or RFS, is the most significant piece of legislation affecting the biofuel industry and is discussed below. Other key regulatory initiatives include:

| · | Energy Policy Act of 1992 which established a goal of 30% alternative fuel usage in government fleets by 2010 and under which biodiesel was designated as an alternative fuel for which credits could be earned for blends with diesel in products that included 20% biofuels or greater. |

| · | Energy Conservation and Re-Authorization Act of 1998 which allows vehicle fleets that are required to purchase alternative fuel vehicles (AFVs) to generate credits toward fulfilling this requirement by purchasing and using biodiesel in conventional-fuel vehicles. |

| · | American Jobs Creation Act of 2004 which created an excise tax credit for producers’ and blenders’ of biodiesel of up to $1.00 per gallon. |

| 6 |

| · | Highway Diesel Fuel Rules. In 2006, the EPA promulgated the Ultra-Low Sulfur Diesel, or ULSD, regulations. These rules require that all diesel fuel, diesel fuel additives and distillate fuels blended with diesel for on-road use contain no more sulfur content than 15 parts per million and provide that using biodiesel as a blend with petroleum-based diesels allows distributors to comply with these regulations. |

Renewable Fuels Standard

The renewable fuel standard, or RFS, program was adopted by EPA to implement the provisions of the Energy Policy Act of 2005, or EPAct, which added section 211(o) to the Clean Air Act. Under the EPAct, Congress established minimum nationwide levels of renewable fuels, including biodiesel, ethanol and liquid fuel produced from biomass or biogas, to be blended into the domestic gasoline supply. The EPAct specifies that the amount of biofuel that must be blended with gasoline sold in the United States was to have increased to 4 billion gallons, or bg, by 2006, 6.1 bg by 2009 and 7.5 bg by 2012. The typical compliance fuel under EPAct is ethanol made from corn starch. The obligated parties under the system are petroleum refiners and importers of gasoline.

Under the RFS, obligated parties were required to demonstrate that they have complied with their percentage obligations over the gallons of gasoline they sold into the marketplace during a compliance period. The EPA developed a system of volume accounting and tracking of the credits associated with renewable fuels known as Renewable Identification Numbers, or RINs. The system is based on the assignment of unique numbers to each batch of renewable fuel by the gasoline producer or importer. The use of RINs allows the EPA to measure and track renewable fuel volumes at the point of their introduction into the national fuel supply rather than at the point when they are blended into conventional fuels, which provides more accurate measurements that can be easily verified. The RFS program requires RINs to be transferred with renewable fuel until the point at which the renewable fuel is purchased by an obligated party or is blended into gasoline by a blender. RINs are accumulated to allow an obligated party to satisfy its renewable volume obligations, or RVOs. The RFS program contemplated that RINs would be sold among obligated parties so that a deficient party could acquire RINs from another obligated party that generated excess RINs to satisfy its requirements.

The RFS program was expanded under the Energy Independence and Security Act (EISA) of 2007. Under the EISA, the mandatory RFS program, known after the adoption of EISA as RFS2, was expanded in several key ways, including by:

| · | expanding the RFS program to include diesel, in addition to gasoline, and covers virtually every type of engine used in automotive, marine, jet or locomotive applications; |

| · | increasing the volume of renewable fuel required to be blended into transportation fuel from 9 bg in 2008 to 36 bg by 2022; |

| · | establishing new categories of renewable fuel and setting separate volume requirements for each one; and |

| · | requiring EPA to apply lifecycle greenhouse gas, or GHG, performance threshold standards to ensure that each category of renewable fuel emits fewer GHGs than the petroleum fuel it replaces. |

RFS2 was adopted with the expectation that it would lay the foundation for achieving significant reductions of greenhouse gas emissions from the use of renewable fuels, for reducing imported petroleum and encouraging the development and expansion of the nation's renewable fuels sector.

RFS2 represents a new regulatory regime for the transportation fuel industry including producers of both petroleum-based fuels and alternative fuels. It impacts every aspect of an obligated party's business and will be, we believe, the stimulus that will drive the growth and development of the biofuel industry in the coming years. The following discussion of the general provisions of RFS2 is intended to demonstrate the breadth of the regulations generally and as they will apply to our business and to serve as a reference as we discuss our business throughout this report.

Volume Standards

For 2010, the volume of renewable fuels required to be produced or imported in the U.S. is 12.95 bg. This total volume must consist of specific amounts in each of the following fuel categories created by RFS2: biomass-based diesel, cellulosic biofuel and advanced biofuel. The remaining volume falls into the “renewable fuel” category. We expect to produce bio-mass-based diesel at our facility.

| 7 |

The volume standard for biomass-based diesel (the type of fuel we propose to produce) has been set at 0.80 bg for 2011. The 2010 requirement was 0.65 bg but because compliance mechanisms were not previously in place, obligated parties are required to meet a combined 2009/2010 requirement by the end of the 2010 compliance year it was combined with the 2009 volume requirement of 0.5 bg. A preliminary standard for biomass-based diesel for 2012 has been set by the EPA at 1 bg. The volume standards for biomass-based diesel reach 15 bg by 2022.

The annual standards may be reset each year by the EPA based upon information provided by the EIA or stakeholders. For instance, each year, the EIA estimates the volume of transportation fuel that will be consumed for the following year as well as the amount of renewable fuel that may be available.

Renewable Fuels

Under RFS2, the term “renewable fuel” has been redefined. A renewable fuel must (i) be produced from renewable biomass (as defined in the regulations), (ii) replace or reduce the quantity of fossil fuel present in a transportation fuel, heating oil, or jet fuel and (iii) have a GHG, emission at least 20% less than baseline lifecycle greenhouse gases (50%, in the case of biomass-based biodiesel), unless the fuel is exempted. The second component merely refers to the use of the renewable fuel that falls under this rule.

The analysis to determine the eligibility of a renewable fuel under RFS2 in meeting one of the four volume requirements necessarily encompasses a review of the type of feedstock used for renewable fuel production, the land on which the biomass was grown, the process used to convert the feedstock into fuel, and the lifecycle greenhouse gas (GHG) emissions that are emitted in comparison to the gasoline or diesel that the renewable fuel displaces.

Renewable Biomass

EISA presents a revised definition of "renewable fuel" that requires it to be made from feedstocks that qualify as "renewable biomass." EISA’s definition of the term ‘‘renewable biomass’’ limits the types of biomass that may be used as well as the types of land from which the biomass may be harvested. Under EISA, feedstock for renewable fuel must originate from among the following types of lands: planted crops and crop residue from agricultural land cleared prior to December 19, 2007 and actively managed or fallow on that date; planted trees and tree residue from tree plantations cleared prior to December 19, 2007 and actively managed on that date; animal waste material and byproducts; slash and pre-commercial thinnings from non-federal forestlands that are neither old-growth nor listed as critically imperiled or rare by a State Natural Heritage program; biomass cleared from the vicinity of buildings and other areas at risk of wildfire; algae and separated yard waste and food waste. The EPA provided structure to these definitions in the implementing regulations. Foreign-grown biomass must originate from this list of approved sources, as well.

EISA prohibits the generation of RINs for renewable fuel made from feedstock that does not meet the definition of renewable biomass.

Lifecycle GHG Analysis

A further qualification requires that lifecycle GHG emissions of a renewable fuel must be less than the lifecycle GHG emissions of the 2005 baseline average gasoline or diesel fuel that it replaces by a set percentage. Under EISA, "lifecycle greenhouse gas emissions" means the aggregate quantity of greenhouse gas emissions (including direct emissions and significant indirect emissions such as significant emissions from land use changes) related to the full fuel lifecycle, including all stages of fuel and feedstock production and distribution, from feedstock generation or extraction through the distribution and delivery and use of the finished fuel to the ultimate consumer, where the mass values for all greenhouse gases are adjusted to account for their relative global warming potential.

The EPA has devised a complex methodology to determine whether the lifecycle GHG emissions of a particular biofuel meet the GHG emissions standards. For example, the EPA’s methodology takes into account indirect emissions when looking at lifecycle emissions from biofuels, particularly in the context of commodity feedstocks, which consider the market interactions of biofuel demand on feedstock and agricultural markets of the region in which they are grown. The EPA recognizes that the methodology it adopted is inherently uncertain. In addition, each analysis necessarily will require significant time to complete.

| 8 |

Qualifying Fuel Pathways

As of the date the final RFS2 rules were published (February 3, 2010), EPA had modeled and approved only a limited number of specific fuel pathways that qualify as renewable fuels under RFS2, signifying that they had satisfied the renewable biomass and lifecycle GHG emissions analysis. These include: soy oil, waste oils, fats, greases and algal oils.

In the preamble to the adopting regulations, the EPA noted that threshold determinations for certain pathways were not possible at the time of promulgation because sufficient modeling or data was not available. In some of these cases, the EPA recognizes that a renewable fuel is already being produced from an alternative feedstock and that although it has the data needed for analysis, it did not have sufficient time to complete the necessary lifecycle GHG impact assessment for the final rule. The EPA has advised that it will model and evaluate additional pathways after the final rule on the basis of current or likely commercial production in the near-term and the status of current analysis at the EPA. In the preamble to the adopting regulations, the EPA advised that it anticipated completing modeling palm oil, grain sorghum ethanol and woody pulp ethanol within six months of February 2010. The EPA noted that, based on current and projected commercial trends and the status of current analysis at EPA, biofuels from these three pathways are either currently being produced or are planned production in the near-term. EPA's analyses project that they will be used in meeting the RFS2 volume standard in the near-term. In fact, EPA notes in the preamble that it has not finalized a provision for the assignment of RIN generating codes for these feedstocks pending completion of its analysis of these biomasses. As of the date of this Annual Report, the EPA had not completed modeling palm oil (the primary biomass we are proposing to use in our facilities).

Registration of Plant, Feedstock and Fuel

RFS2 imposes a complex set of compliance and reporting obligations to ensure that each obligated party satisfies its RVO for a particular compliance period, under the regulations. These regulations extend over the entire range of an obligated party's operations. All producers of renewable fuel that produce more than 10,000 gallons of fuel annually must register with the EPA’s fuels program prior to generating RINs. A biofuel producer will have to supply the EPA with extensive information concerning plant operations, processes and products, including the fuels produced, the feedstocks that may be used, co-products produced, the source of energy used to produce the biodiesel, compliance with clean air regulations and applicable air permits for permitted capacity and records that support the facility’s baseline volume. In addition, producers must provide the EPA with an independent chemical engineer's report with respect to its plant upon initial registration and every 3 years thereafter or upon changing the feedstock from which it produces biodiesel. The EPA deems the information collected as essential to generating and assigning a certain category of RIN to a volume of fuel and to verifying the validity of RINs generated. In addition, a producer will have to demonstrate that the biodiesel produced is ASTM D6751 compliant. A producer also will have to register its renewable fuels as a motor vehicle fuel, which will subject it to additional reporting and other requirements.

Generation of RINs and Equivalence Values

Under RFS2, each RIN is generated by the producer or importer of the renewable fuel, as in the RFS1 program. In order to determine the number of RINs generated by and assigned to a batch of renewable fuel, the actual volume of the batch of renewable fuel must be multiplied by the appropriate equivalence value. The producer or importer must also determine the appropriate code to assign to the RIN to identify which of the four standards the RIN can be used to meet.

The equivalence value of a renewable fuel represents the number of gallons that can be claimed for compliance purposes for every physical gallon of renewable fuel. The EPA takes the position that the use of equivalence values based on energy content of a fuel is an appropriate measure of the extent to which a renewable fuel would replace or reduce the quantity of petroleum or other fossil fuel present in a fuel mixture. Under RFS1, ethanol was ascribed an equivalence value of 1.0. Under EPAct, additional credit was to be assigned to cellulosic and waste-derived renewable fuels and the EPA was directed to establish appropriate credit for biodiesel and renewable fuel volumes in excess of the mandated volumes. Under RFS2, the EPA assigned an equivalence value to ethanol of 1.0, to butanol of 1.3, to biodiesel (mono alkyl ester) of 1.5, and for non-ester renewable diesel of 1.7.

| 9 |

The producer or importer must also determine the appropriate code to assign to the RIN to identify which of the four standards the RIN can be used to meet and which equivalency value applies to determine the number of RINs generated. The fuel pathway of the product is determinative of the equivalence value and thus the quantity of RINs generated for each batch of finished product produced.

Renewable Volume Obligations

Under EISA, each obligated party must satisfy certain annual renewable volume obligations, or RVOs. An RVO represents the volume of renewable fuel that the obligated party is required to ensure was used in the U.S. in a given calendar year. Obligated parties have an RVO under each of the four RFS2 renewable fuel categories. Obligated parties calculate their RVO at the end of a calendar year based on the volume of gasoline or diesel fuel they produced during the year. Obligated parties are required to meet their RVOs through the accumulation of RINs. By acquiring RINs and applying them to their RVOs, obligated parties are deemed to have satisfied their obligation to cause the renewable fuel represented by the RINs to be consumed as transportation fuel in highway or non-road vehicles or engines. Obligated parties are not required to physically blend the renewable fuel into gasoline or diesel fuel themselves.

The EPA keeps track of the RINs using the EPA Moderated Transaction System, or EMTS. Any deficit may be carried into the following year but only that one year. Alternatively, if an obligated party acquires more RINs than it requires, it may carry over a certain percentage (generally 20%) to the next year or transfer them to another party. Obligated parties will also have to comply with reporting and recordkeeping procedures as noted above. Civil penalties in the amount of $37,500 per day may ensue for violation of the RFS program for each day and for each type of violation.

RINless Biofuel

Under RFS2, the EPA mandates that producers of biofuels register their products as transportation fuels. All producers of transportation fuels are subject to RVOs. Producers of biofuels that qualify as renewable fuels will generate RINs to apply to the satisfaction of its RVOs. However, EPA allows for the possibility of the production of some biofuel that does not generate RINs, a fuel that EPA refers to as RINless, the producers of which will not be subject to RVOs. For example, producers may use foreign-grown feedstocks that have not been qualified by the EPA as a renewable fuel pathway. Until these producers demonstrate that their feedstocks meet the renewable biomass definition, including the associated land use restrictions, their fuel will be RINless. RINless biofuel likely will be consumed as a transportation fuel and, unless exempted, subject to all of the RFS2 standards, including that the producer of such fuel satisfy applicable RVOs with respect to the biofuel that they sell. This would necessitate that a producer of RINless biofuel blend its product with qualifying renewable fuels. However, the EPA has specifically exempted RINless biofuel producers from satisfying applicable RVOs with respect to the biofuel that they sell, thereby precluding the need to blend their fuel with renewable fuels.

State and Local Biodiesel Mandates.

As of the date of this Annual Report, nearly every state has adopted, to some extent, laws, regulations, tax credits and/or incentives that positively impact the biodiesel production industry and users of biodiesel. They vary significantly from state to state in their mandate, scope and enforcement but may encompass such areas as biodiesel production and blending tax credits, biofuels technology research and development support and grants, biodiesel retailer tax credits, biodiesel price preferences, mandatory use requirements in school buses and government vehicles, among others. In addition, laws and regulations that target emissions and greenhouse gases benefit the biodiesel industry. California is at the vanguard of the alternative fuels revolution, pulling the federal government with it on many issues, including vehicle emissions standards and fuel efficiency laws.

Georgia Initiatives

The State of Georgia, where we are negotiating to site our plant, has adopted a myriad of laws and regulations and granted tax credits and incentives to promote the use of biofuels. Under Georgia law, biodiesel produced or sold in the state, including for the purpose of blending with petroleum diesel, must meet ASTM specification D6751, which we expect our biodiesel will.

| 10 |

Georgia Incentives and Laws for Biodiesel

Alternative Fuel Vehicle (AFV) Tax Credit. An income tax credit is available for 10% of the cost to purchase or lease a new dedicated AFV or to convert a vehicle to operate solely on an alternative fuel, or $2,500 per vehicle, whichever is less. Eligible alternative fuels include E85, natural gas, propane, hydrogen, coal derived liquid fuels, fuels other than alcohol derived from biological materials, and electricity. Any portion of the credit not used in the year the AFV is purchased or converted may be carried over for up to five years.

Alternative Fuels Production Assistance. The Georgia Division of Energy Resources and the Georgia Environmental Facilities Authority provide assistance to companies that are considering locating alternative fuels production facilities in Georgia.

Alternative Fuel Production Facility Tax Exemption. Tangible personal property used in, or for, the construction of an alternative fuel production facility dedicated to the production of ethanol, biodiesel, butanol, and their by-products is exempt from the state sales and use tax. To qualify, alternative fuels produced in the facility must be derived from biomass materials such as agricultural products, animal fats, or the wastes of such products or fats. The tax exemption does not apply to property purchased after the production and processing of alternative fuels has begun at the facility. The exemption applies to tangible personal property purchased between July 1, 2007, and June 30, 2012.

Georgia Laws and Regulations

Alternative Fuel Use and AFV Acquisition Requirements. State agencies and departments must prioritize the procurement of high fuel efficiency and flexible fuel vehicles when such technologies are commercially available and economically practical. Additionally, all state-owned fueling facilities must purchase gasoline blended with ethanol and diesel fuel blended with biodiesel for use in state vehicles when available and economically practical.

Motor Fuel Excise Tax. An excise tax is imposed at the rate of $0.075 per gallon on distributors who sell or use motor fuel, including special fuels. Motor fuels that are not commonly sold or measured by the gallon and are used in motor vehicles on public highways are taxed according to their gasoline gallon equivalent. Propane and special fuels sold in bulk to a licensed consumer distributor are exempt from this tax.

Other Legislative and Regulatory Market Drivers.

We believe that renewable portfolio standards, or RPS, and other laws and programs that create a market for trading carbon credits, are additional demand drivers for biodiesel. As of the end of 2010, 30 had established an RPS, which are guidelines or rules regarding the amount of renewable power used to generate electricity. Currently, states with RPS requirements mandate that between 4 and 30 percent of electricity be generated from renewable sources by a specified date. While RPS requirements differ across states, there are generally three ways that electricity suppliers can comply with the RPS: owning a renewable energy facility and its output generation; purchasing Renewable Energy Certificates (RECs); purchasing electricity from a renewable facility inclusive of all renewable attributes (sometimes called “bundled renewable electricity”).For example, the State of California’s RPS requires that, by 2010, 20% of electricity sold in the state must be generated by renewable power, such as biodiesel, though the standard had not been met as of the June 1, 2010. The power generation market relies in part on diesel generators to produce electricity. Biodiesel offers electricity utilities the opportunity to satisfy RPS requirements by switching from diesel to biodiesel in the electricity production process, rather than incurring capital expenditures to build wind, solar, geothermal or other facilities to satisfy RPS requirements.

| 11 |

Several states that collectively account for approximately 20% of U.S. carbon dioxide emissions have launched initiatives to reduce greenhouse emissions using cap-and-trade regimes. The Regional Greenhouse Gas Initiative, or RGGI, is a market-based effort by Connecticut, Delaware, Maine, Maryland, Massachusetts, New Hampshire, New Jersey, New York, Rhode Island and Vermont to reduce carbon dioxide emissions from power plants. The initiative has set up the nation’s first mandatory cap-and-trade program for carbon dioxide. Under the RGGI Memorandum of Understanding, the governors of the member states committed to state regulations that will cap and then reduce the amount of the greenhouse gas carbon dioxide (CO2) that power plants are allowed to emit. The carbon dioxide, or CO2 emissions budget (cap) established the limit on power plant CO2 emissions in the region at 188 million tons of CO2; the cap will decrease by 2.5 percent each year from 2015 through 2018 for a total reduction of 10 percent. Emission permit auctioning began in September 2008 and the first three-year compliance period began on January 1, 2009. Sources that emit more than their allowance must buy credits from those who emit less than their allowance, thus creating a financial incentive for sources to reduce their own emissions. Other states are creating market-based compliance programs, including California that is considering a program that would permit trading with the European Union, the RGGI and other jurisdictions.

In addition to greenhouse gas and clean air legislation, a variety of government programs specifically assist the biodiesel industry. Certain notable programs that support the biodiesel industry include:

| · | The Renewable Energy and Energy Efficiency Program, administered by the Rural Business Cooperative Service of the U.S. Department of Agriculture, which provides grants, loans and loan guarantees for the development of renewable energy products. | |

| · | The Biomass Research and Development Initiative, administered jointly by the U.S. Department of Energy and U.S. Department of Agriculture through the National Biomass Coordination Office, provides grants for biomass research, development and demonstration projects. | |

| · | Project grants administered by the U.S. Department of Energy’s Office of Energy Efficiency and Renewable Energy provide bioprocessing facility project funding for cooperative biomass research and development for the production of fuels, electric power, chemicals and other products. | |

| · | The Loan Guarantee Program, administered by the U.S. Department of Energy, provides loan guarantees for energy projects that reduce air pollutants and greenhouse gas emissions, including biofuels projects. |

Our Business

Production of Biodiesel

Biodiesel is produced by chemically reacting a fat or oil with an alcohol in the presence of a catalyst, a process known as transesterification. The product of the reaction is a mixture of biodiesel and glycerol (glycerin), which is a high value co-product.

Most vegetable oils and animal fats contain five principal long hydrocarbon chains, also known as fatty acids or methyl esters. The relative amounts of the five methyl esters in the oil or fat are determinative of the physical properties of the fuel, including the cetane number, cold flow properties and oxidative stability (the ability to withstand oxidation, which breaks down the fuel). Different feedstocks possess different chemical qualities and consequently, different relative amounts of the methyl esters.

In the first step of biodiesel production, methanol, catalyst and the feedstock are combined in a reactor and agitated. The glycerol is not soluble with the esters and settles to the bottom of the reactor, at which time it is removed from the product stream. Due to the low solubility of glycerol in the esters, the separation generally occurs quickly and may be accomplished with either a settling tank or a centrifuge. The glycerol is transferred to separate vessels for purification, as described below.

After separation from the glycerol, the methyl esters are then neutralized and purified in successive vessels. Thereafter, the methanol is stripped and recovered for reuse, usually by way of a vacuum flash process or another type of evaporator, before water washing. The methanol that is removed from the methyl ester and glycerol streams tend to collect any water that may have entered the process. The water is removed in a distillation column before the methanol is recovered and returned to the process.

The water washing stage removes any remaining catalyst, soap, salts, methanol, or free glycerol from the biodiesel. Acid is added to the biodiesel to neutralize any residual catalyst and to split any soap that may have formed during the reaction. Soaps react with the acid to form water soluble salts and free fatty acids. Neutralization before washing reduces the water required and minimizes the potential for emulsions to form when the wash water is added to the biodiesel. Following the wash process, any remaining water is removed from the biodiesel by a vacuum flash process. The biodiesel is analyzed to ensure that it meets quality standards.

| 12 |

The glycerol stream leaving the separator is only about 50% glycerol. It contains some of the excess methanol and most of the catalyst and soap. In this form, the glycerol has little value and disposal may be difficult. The glycerol must be further refined by adding acid to split the soaps into free fatty acids and salts. The free fatty acids are not soluble in the glycerol and will rise to the top where they can be removed and recycled. The glycerol refining process takes the purity up to 99.5% to 99.7% using vacuum distillation or ion exchange processes.

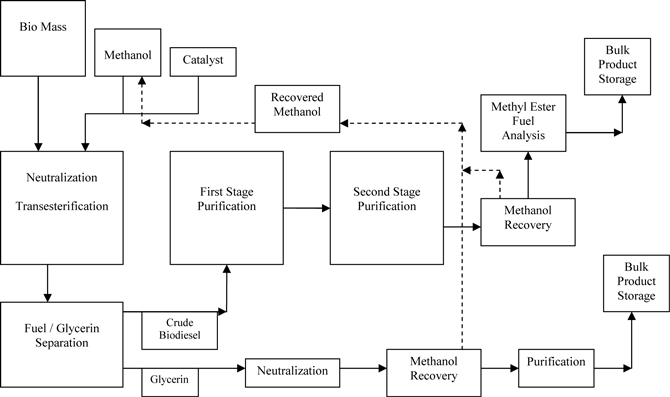

The diagram below depicts a general process flow chart for biodiesel production.

Our Production Equipment and Process

Our production equipment and manufacturing processes reflect our core business principals comprising a fierce commitment to cost control and efficiency and sensitivity to environmental concerns. We expect to derive a meaningful competitive advantage from our proprietary biodiesel production equipment that we believe we can construct less expensively and more quickly than other biodiesel producers and that we believe will enable our Company to produce biodiesel more cost effectively than our competitors. Our production equipment is based on an innovative combination of existing, proven technologies that integrate multiple types of programmable control systems to maximize the efficiency in throughput that we believe will increase production efficiency, reduce production costs and improve plant economics when compared to other biodiesel production processes. We will fabricate our production equipment in-house from readily available parts and equipment.

Our equipment and manufacturing process utilizes the same basic, tested elements as most biodiesel production facilities. However, unlike most commercial biodiesel plants being constructed today that utilize large, single line production techniques consisting of reactors with an average volume of 15,000 – 100,000 gallons, we will produce biodiesel using a series of small batch/flow processing systems that continuously process 1,000 gallons of fuel. An advantage of using our small batch/flow systems will be our ability to add production systems as biodiesel demand warrants and our financial condition permits, as opposed to building a massive facility that may operate at only a fraction of its capacity at any particular time, and our ability to deactivate production systems during periods of low demand.

We believe that our technology will enable us to produce biodiesel that meets the standard for biodiesel established by The American Society of Testing and Materials, or ASTM, which is called ASTM 6751, that has been adopted by the EPA and the State of Georgia. Our production equipment is capable of processing virtually any feedstock. This flexibility will allow us to shift into and out of feedstocks based on customer demand and market cost dynamics without hindering production or increasing our operating costs.

| 13 |

Our production systems are designed to maximize the efficiency in throughput and automate the operation by integrating multiple types of programmable control systems. The fuel processing unit, which is a combination of batch and flow processing, utilizing a smaller reactor with an ultrasonic accelerator manifold, is the foundation for the managed flow process that moves in-process fuel through midpoint separators, methanol recovery distillers and filtration/dryer systems. These systems accelerate the reaction time and increase throughput efficiency. In-process fuel also is managed by an automated control processing system that combines primary logic control and PC based flow management programming. Digital and analog sensors continuously measure pH readings, temperature, time, flow rates, volume and light to ensure quality. Our ability to monitor and adjust the processing temperature, one of the most important variables in the transesterification process, in real time allows us to overcome concerns that small batch processing requires longer reactor residence times as claimed by designers of large single line facilities. In addition, monitoring and adjusting the process temperatures in real time allows us to reduce overall energy costs. Each reactor is independently controlled and in-process fuel can be separated throughout the system for collection and testing or directed to random selected purification collectors and filtration/dryers prior to bulk storage to maintain operating efficiency.

The most significant advantages achieved by our system as compared to the large, single line systems being built today are the significantly lower cost and fabrication time required to construct facilities of comparable output. The capital investment required to construct a single line facility varies based on capacity and the 30 MGY to 50 MGY greenfield facilities being constructed today range from approximately $50 million to $75 million, depending on location and the technologies used in controlling the process. Facilities of this size are constructed over the course of nine to twelve months or more. In contrast, we expect to fabricate our production systems in groups comprising of three reactors, six purification processors, two methanol distillers, in-process transfer manifolds and filtration/dryer units and capable of producing approximately 1,878,000 gallons per year, in two to three weeks at a cost of approximately $165,000. We will be able to build our 80 MGY nameplate capacity plant for a total cost of approximately $20.5 million, or $0.2562 per gallon of nameplate capacity. The substantially accelerated construction time will allow us to begin realizing a return on investment far more quickly than traditional greenfield biodiesel production plants.

We believe that our small batch manufacturing process and equipment will achieve numerous other operating efficiencies compared to the large, single line processing plants including:

| · | accelerating fuel processing time, as determined by the duration of the complete cycle from the start of raw material mixing to finished fuel through thermal displacement of smaller volume heating and cooling cycles; | |

| · | reducing energy cost (i) to obtain and maintain proper processing temperatures during transesterification (the reaction process) and (ii) through gravity fed raw material manifolds; and | |

| · | reducing the number of employees required to operate our plant and the associated labor costs by the use of automated controls throughout the process.. |

We have designed our productions systems to be minimally invasive to the environment. Our processes either consume all raw materials during biodiesel production or recapture and recycle them for reuse, and no liquid or solid waste is produced. This feature limits the extent of waste removal and disposal equipment and services we will require during operation. Moreover, the entire production process, from the introduction of raw materials into reactors through the collection of finished biodiesel, is localized in sealed units within the internal confines of our facility, limiting the possibility of spills or other external environmental contamination. Our equipment and processes allow our personnel to visually monitor and inspect the facility throughout the production process. For example, waste water run-off from the production process will be collected, processed, purified and recycled on-site for reuse in the fuel production process. Moreover, as a result of the size of the overhead feedstock storage cells and spill controls in sealed units, the facility design will maintain all production materials inside of the building subject to constant visual monitoring and facility inspection through our preventive maintenance program. Our production systems incorporate vacuum vapor recovery apparatus and operate at lower temperatures than some producers, which virtually eliminating all atmospheric emissions. We believe that the nature of our processes, which were designed to reduce the environmental impact of our operations, will facilitate and accelerate the environmental permitting process.

| 14 |

Our Biodiesel Production Facilities

We have planned the design of our permanent facility around our proprietary biodiesel production equipment and technologies. The operational blueprint of our facility was designed by our President, Ken Rakestraw, who has drawn upon his considerable experience in the development, design and operation of systems that focus on automated control programming (process logic control development and machine programming), hydraulic design and manufacturing (fluid management, pressure control and applied force calculations), and technical processes and procedures. In addition, he has utilized his experience and knowledge of different process manufacturing facilities to incorporate numerous modifications into our plant that we believe will differentiate it from other biodiesel plant designs and that we believe will improve our plant's output and efficiency.

We have been negotiating with the Georgia Port Authority to lease an unoccupied facility at the Port of Savannah at which we will operate our temporary plant, the extent of which is described below.

We also have been negotiating with a private entity to purchase approximately 14.5 acres of undeveloped real property located on an island supported by the Port of Savannah, approximately six miles from the proposed temporary plant site.

Our management has prepared plans, designs and schematics for each of our temporary and permanent plants. We have designed and will operate our facilities to take advantage of all possible operating efficiencies. Our dedication to cost control and efficiency is evident throughout our facility and production process. Small batch processing systems will reduce the cost and accelerate the fabrication time of our plant and allow us to add capacity as demand warrants and our financial condition allows. We also expect that we will operate on a just in time basis both relating to receiving deliveries of feedstock and production volume, thereby limiting the need to build and maintain substantial storage capacity for our feedstock or finished product. The energy we will use in the production of biodiesel at our facility will be generated from biodiesel that we produce. Another example of facility efficiency contemplates the storage of all raw materials and finished fuels in overhead storage cells constructed as part of the bar joist roof system, thereby reducing material movement and associated manpower and energy costs. The cumulative impact of these and other seemingly insignificant efficiencies is considerable in the context of infrastructural requirements and energy costs, among other expenses that would be incurred when matters such as these are not closely regarded by management.

We will engage a local engineering firm to complete the missing infrastructural elements of our design. This firm has been primarily responsible for the development of the surrounding sites of our permanent facility location,. We also will engage a major construction firm to construct the facility. We will work directly with the development and building engineers of these firms who will finalize the detailed designs for electrical, plumbing and plant infrastructure. The site development engineering firm also will provide environmental consultation as part of its services.