Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - SEFE, INC. | Financial_Report.xls |

| EX-31 - EXHIBIT 31 - SEFE, INC. | ex31.htm |

| EX-32 - EXHIBIT 32 - SEFE, INC. | ex32.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

|

[X]

|

Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

|

|

|

For the Fiscal Year Ended December 31, 2011

|

||

|

[ ]

|

Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

|

|

|

For the Transition Period from __________ to

|

||

|

Commission File Number: 000-51842

|

||

|

SEFE, INC.

|

||

|

(Name of small business issuer in its charter)

|

||

|

Nevada

|

20-1763307

|

|

|

(State or other jurisdiction of incorporation or organization)

|

(I.R.S. employer identification number)

|

|

|

6821 East Thomas Road

Scottsdale, Arizona

|

85251

|

|

|

(Address of principal executive offices)

|

(Zip code)

|

|

|

Issuer’s telephone number: (480) 294-6407

|

||

|

Securities Registered Pursuant to Section 12(b) of the Act:

|

||

|

Title of each class

|

Name of each exchange on which registered

|

|

|

None

|

None

|

|

|

Securities Registered Pursuant to Section 12(g) of the Act:

|

||

|

Common Stock

|

||

|

(Title of class)

|

||

|

(Title of class)

|

||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that ht registrant was required to submit and post such files). Yes [X] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.:

|

Large accelerated filer

|

o |

Accelerated filer

|

o |

|

Non-accelerated filer

|

o |

Smaller reporting company

|

x |

(Do not check if a smaller reporting company)

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act)

Yes [ ] No [X]

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter. $_____.

The number of shares outstanding of each of the issuer's classes of common equity, as of March 29, 2012 was 52,278,998.

DOCUMENTS INCORPORATED BY REFERENCE

If the following documents are incorporated by reference, briefly describe them and identify the part of the Form 10-KSB (e.g., Part I, Part II, etc.) into which the document is incorporated: (1) any annual report to security holders; (2) any proxy or information statement; and (3) any prospectus filed pursuant to Rule 424(b) or (c) of the Securities Act of 1933 ("Securities Act"). The listed documents should be clearly described for identification purposes (e.g., annual report to security holders for fiscal year ended December 24, 1990).

None.

Transitional Small Business Disclosure Format (Check one): Yes [ ] No [X]

SEFE, INC.

FORM 10-K

For the year ended December 31, 2011

TABLE OF CONTENTS

| 1 | ||

| 1 | ||

| 5 | ||

| 8 | ||

| 8 | ||

| 8 | ||

| 8 | ||

| 9 | ||

| 9 | ||

| 11 | ||

| 12 | ||

| 21 | ||

| 41 | ||

| OTHER INFORMATION | 41 | |

| 42 | ||

| 42 | ||

| 45 | ||

| 46 | ||

| 46 | ||

| 47 | ||

| 48 | ||

| 49 | ||

| 50 | ||

FORWARD LOOKING STATEMENTS

This Annual Report contains forward-looking statements about our business, financial condition and prospects that reflect our management’s assumptions and beliefs based on information currently available. We can give no assurance that the expectations indicated by such forward-looking statements will be realized. If any of our assumptions should prove incorrect, or if any of the risks and uncertainties, underlying such expectations should materialize; our actual results may differ materially from those indicated by the forward-looking statements.

The key factors that are not within our control and that may have a direct bearing on operating results include, but are not limited to, acceptance of our services, our ability to expand its customer base, managements’ ability to raise capital in the future, the retention of key employees and changes in the regulation of our industry.

There may be other risks and circumstances that management may be unable to predict. When used in this Report, words such as, "believes," "expects," "intends," "plans," "anticipates," "estimates" and similar expressions are intended to identify and qualify forward-looking statements, although there may be certain forward-looking statements not accompanied by such expressions.

PART I

ITEM 1 - DESCRIPTION OF BUSINESS

Business Development and Summary

We were originally incorporated in the State of Nevada on September 24, 2004 under the name Midnight Candle Company.

On July 16, 2010, we entered into and closed an Intellectual Property Assignment Agreement by and between SEFE, Inc., a Delaware corporation (“SEFE Delaware”), Midnight Candle Company and Ms. Helen C. Cary, the majority shareholder of Midnight Candle Company’s issued and outstanding common stock. In accordance with the Assignment, we acquired all of SEFE Delaware’s right, title and interest in and to various information, inventions, discoveries, writings, expressions, ideas, know-how, concepts, techniques, innovations, systems, processes, procedures, methods, prototypes, designs, and technical data involving or relating to certain atmospheric static electricity collectors, generators, and converters as generally described in four U.S. Patent Applications (“Patents”). In exchange for the assignment of the Patents, we agreed to the following:

|

1.

|

The assumption of liabilities of SEFE Delaware, in the aggregate of $250,000;

|

|

2.

|

The issuance of 30,000,000 shares of the unregistered common stock of Midnight Candle Company; and

|

|

3.

|

The cancellation by Ms. Cary of 144,900,000 shares of Midnight Candle Company’s common stock owned by her.

|

On July 16, 2010, in connection with the Assignment, we issued 30,000,000 shares of our common stock to SEFE, Inc., a Delaware Corporation in exchange for the assignment of four patent applications. No other consideration was used by SEFE Delaware. Accordingly, SEFE Delaware became the majority shareholder of Midnight Candle Company, owning 72.1% of its outstanding common stock. Control was assumed from Ms. Cary, who is no longer a principal shareholder of Midnight Candle Company. There is no arrangement between members of the former and current control group regarding election of directors or any other matters.

On July 20, 2010, we amended our articles of incorporation in the State of Nevada to change our name from Midnight Candle Company to SEFE, Inc.

In October 2011, the Principals of SEFE Delaware agreed to return 26,000,000 shares of SEFE, Inc. to the Company as a result of negotiations with the Company in exchange for an executed Separation Agreement and retention by the principals of SEFE Delaware of 4,000,000 shares of SEFE, Inc. common stock.

Our administrative office is located at 6821 East Thomas Road, Scottsdale, AZ 85251, telephone (480) 294-6407.

Our fiscal year end is December 31.

Business of Issuer

Principal Products and Principal Markets

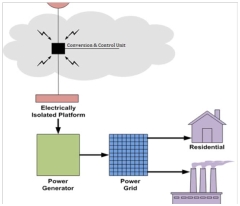

SEFE was founded to develop and bring to market a renewable source of energy that naturally occurs in the atmosphere. The goal of our company is to use our proprietary methodologies and inventions to capture and convert this naturally occurring atmospheric static electric energy to usable energy. SEFE’s energy production strategies aim to create and proliferate technologies that are un-intrusive to existing communities, are easily adoptable, provide high output and leave a small carbon footprint. The SEFE system is designed to operate by capturing static electricity from the atmosphere and making it usable for mining, manufacturing, and construction companies; utility companies; mining relief organizations; among others. This is a renewable source, but also one that is non-polluting, efficient, and economical.

The SEFE system generally operates in the following manner:

|

·

|

An electrical lead held aloft by a suspension mechanism

|

|

·

|

Static electricity is absorbed by the lead

|

|

·

|

The direct current of electricity is converted to an alternating current using our proprietary methods

|

|

·

|

The collected electricity is sent to an isolated platform

|

|

·

|

The platform sends the current to a converter to do either one of the following:

|

|

·

|

Translate the direct current into an alternating current in usable form and

|

|

·

|

Convert the electricity back into direct current and stores it in batteries for later use

|

|

·

|

Electricity is communicated to existing residential and commercial locations (using the existing power distribution infrastructure from the utility companies)

|

SEFE’s patented and patent-pending technology allows for the capture of existing static electricity from the atmosphere, the transformation of that static electricity into usable power, and the mechanisms to either direct this power directly into existing grids or generators, or to store the energy for later use. There is considerably low implementation cost relative to the amount of power that can be created by utilization of our devices, technology, and network operations center. Additionally, the use of our technology leaves a relatively small carbon footprint compared to existing technologies.

Our initial potential client base is comprised of mining, manufacturing, and construction operations. There are plentiful concerns of this type of various sizes across the country, and a large portion of their costs (often up to 70% depending on the location of individual mines) is related to transportation of the fuel required to operate the operations. We have been focusing on how best to develop relationships with multiple participants in these spaces that we anticipate will provide us into an entrance into their markets. Our strategy with these large client platforms is to license our units to potential clients and sell the electricity that our units produce. This will provide us with recurring and ongoing revenue streams as each unit can be re-deployed to a new client as needed. These clients also represent SEFE’s fastest path to market as each will be able to help build the correctly constructed units around our agnostic energy-harvesting technology based on their needs and protocols. Our potential customer base also consists of existing utility companies and cooperatives (co-ops) thereof. There are currently 900 co-ops in the US market which collectively control over 50% of the grid and service much of the market in the US. We have an established relationship with one of these co-ops which will allow us an entry into the co-op market and provide a strong strategic position with regard to nationwide alliance. These strategies, we believe, will eventually provide a springboard for expansion into foreign markets and protection therein.

A key to SEFE’s ability to provide value to its shareholders is through the protection afforded by the Company’s intellectual property portfolio. This is an ever-developing asset owned by the Company and its shareholders. It is consistently evolving due to the ongoing tests and research conducted by SEFE’s scientific team into how to best improve the Harmony product as well as to expand into other product offerings in the future. It will be highlighted later in this document.

Distribution Methods of the Products and Services

We plan on generating revenue by selling the electricity produced by our Harmony III commercial grade units. Milestones to be met on the way to this goal include:

|

1.

|

Deployment of our proprietary detection system in order to determine which factors most strongly affect the availability of atmorspheric electricity in any given area. This will determine schedules of ongoing tests as well as where to actively begin educating clients about how SEFE’s products can affect their businesses.

|

|

2.

|

Ongoing data collection to determine how much electricity can be generated/ stored by each unit over a period of time based on location, altitude, weather, and other factors;

|

|

3.

|

Fabrication of our initial commercial grade unit;

|

|

4.

|

Securing contracts with mining/manufacturing/construction organizations

|

|

5.

|

Implementation of the communications, monitoring methodologies, and security for each unit through our Network Operations Center

|

|

6.

|

Ongoing grant writing in order to prove our technology for implementation in utility companies and other regulated spaces

|

We currently have no marketable units and therefore have not begun to distribute any products.

Industry Background and Competition

There exists in our global community a large and ever expanding need for affordable energy. Events of the past several years have illustrated an urgency for the United States to break free of its independence on foreign oil sources and traditional fossil fuels and have created an environment that is open to other, cheaper sources of power. SEFE’s technology provides for direct supplemental electricity supplies to the existing power grids at a fraction of the cost co-operatives and utility companies – and, by extension consumers – are currently paying. We do not seek to replace or rebuild the current electricity infrastructure. However, we see an attractive opportunity to use our technology to take pressure off power plants and provide an affordable enhancement to supplies of electricity. We also see a large opportunity to have a tangible effect on the structure of disaster relief in our nation and others. Natural disasters of the past several years (Haiti, Hurricane Katrina, earthquakes in South America and Asia, etc.) have illustrated a need for impromptu medical centers as well as temporary housing for displaced victims. We aim to provide an affordable method to support these efforts by providing electricity that can be deployed rapidly to power these communities as the needs arise.

When compared with fossil fuel, SEFE systems are non-polluting and produce no carbon dioxide emissions in their energy production. Recent estimates placed the amount of carbon dioxide produced by fossil fuels each year at nearly 22 gigatons. Based on projections, this amount could be dramatically reduced with the implementation of the SEFE network.

SEFE systems are additionally more economical when compared with other alternative energy solutions. Our systems will supplement existing alternative energy solutions, turning them from competitors into partners. There are currently large national initiatives aimed at increasing our reliance on various forms of alternative energy over fossil fuels. One initiative calls for the implementation of a wind based alternative energy infrastructure to be rolled out within the United States. A cost analysis of other sources of alternative energy has taught us that the capital and energy required to produce solar and wind power and transmit it to the power grid make it very difficult for those methods to be efficient in the current market. We have already conducted field tests to prove the existence of static electricity in the atmosphere and that it can generate sufficient power to meet energy needs when harnessed correctly. The cost-effectiveness of SEFE-generated electricity is based on the fact that our units require very little overhead cost compared to the amount of power that we anticipate they will produce.

Significantly, all of our competitors have longer operating histories, as well greater financial, management, sales, marketing and other resources than we do. Competitors include all local, regional and national electric companies. We are a small company with limited capital resources, no saleable products and negative cash flows. As such, we currently compete unfavorably in the general marketplace. Unless we find a way to increase our revenue generating ability, we will not be able to continue as a going concern.

Intellectual Property

SEFE currently has four patents issued by the US Patent and Trademark Office; another patent has been recently allowed by the USPTO and we are awaiting its patent number assignment; and we have submitted eighteen additional United States Patent Applications. These applications have been researched, written, and filed to protect the Company’s core intellectual property. Upon issuance, our patents will continue to provide barriers to entry and fortify our foundational business construct. In addition, SEFE will continue its forward-looking strategy resulting in additional patent filings and applications with the U.S.P.T.O. with the goal of protecting our inventions through the development of our business model. Our U.S.P.T.O strategies provide what we hope will be a level of risk mitigation and a protection of value for our shareholders now and in the future. We feel our ownership of the space related to SEFE products and services are vital to the growth of our company and enhanced value to our shareholders.

Effect of Existing or Probable Governmental Regulations

Government regulations require that utility companies produce a certain amount of power through sources not owned by themselves. They also require that certain levels of renewable energy are utilized each year.

In addition, with the EU and other European countries firmly positioned to mandate carbon credits, SEFE, Inc. could fill a large void in those markets where value is associated with clean energy resources over, and therefore a higher price paid, over traditional or direct reductions from fossil fuel or non-green energy consortiums.

Number of total employees and number of full time employees

SEFE is currently in the development stage. During the development stage, we plan to rely exclusively on the services of a few employees, our officers, support staff, independent contractors, and our directors to set up our initial business operations. Our CEO is involved in our business on a daily basis and is prepared to dedicate additional time, as needed to execute our business strategies. At this time, there are three additional full-time employee and several part-time independent contractors. Our full-time employees are working in SEFE’s Science and Technology center and in marketing our company to potential clients. Our support staff comprises the majority of our executive services and financial systems in conjunction with our executive management and Audit Committee Chairman. We expect to hire additional employees over the next 12 months as we continue to enhance our Science and Technology center, move into fabrication of Harmony Units, and contemplate additional product offerings in order to increase value to our shareholders.

Reports to Security Holders

|

1.

|

We will furnish shareholders with annual financial reports certified by our independent registered public accountants.

|

|

2.

|

We are a reporting issuer with the Securities and Exchange Commission. We file periodic reports, which are required in accordance with Section 15(d) of the Securities Act of 1933, with the Securities and Exchange Commission to maintain the fully reporting status.

|

|

3.

|

The public may read and copy any materials we file with the SEC at the SEC's Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. Our SEC filings will be available on the SEC Internet site, located at http://www.sec.gov.

|

ITEM 1A - RISK FACTORS

Our technology is still unproven and we may be unable to commercially develop the Harmony Units. Investors may lose their entire investment if we are unable to continue as a going concern.

The company is in the process of commercially developing our Harmony Units. Our technology is new and commercially untested and there can be no assurance that the Company can develop commercially salable products. We have a limited operations record, on which you can evaluate our business and prospects. Our prospects must be considered in light of the risks, uncertainties, expenses and difficulties frequently encountered by companies in their early stages of development. These risks include, without limitation, competition, the absence of ongoing revenue streams, established distribution channels and lack of brand recognition. SEFE cannot guarantee that we will be successful in executing our proposed alternative energy business. If we fail to implement and create a base of operations for our proposed business, we may be forced to cease operations, in which case investors may lose their entire investment.

We may not be able to attain profitability without additional funding, which may be unavailable.

We have limited capital resources. To date, we have not generated positive cash inflows from our operations. Unless we begin to generate sufficient revenues from our proposed business objective of producing and selling atmospheric electricity to finance operations as a going concern, we may experience liquidity and solvency problems. Such liquidity and solvency problems may force us to go out of business if additional financing is not available. We have no intention of liquidating. In the event our cash resources are insufficient to continue operations, we intend to raise addition capital through offerings and sales of equity or debt securities. In the event we are unable to raise sufficient funds, we will be forced to go out of business and will be forced to liquidate. A possibility of such outcome presents a risk of complete loss of investment in our common stock.

The Company may not be able to retain the key personnel it needs to succeed and new, qualified personnel may be extremely difficult to attract.

The Company believes that its continued success will depend to a significant extent upon the efforts and abilities of its executive officers and certain key employees. The Company has employment agreements with its executive officer, however, failure of the Company to retain the services of its executive officers, or to attract and retain additional qualified personnel, could adversely affect the Company’s business, financial condition and results of operations. The Company does not carry key-man life insurance on any of its executive officers.

There is no assurance that the pending patents within our portfolio will be allowed by the USPTO and, if they are, that others will not develop functionally similar products outside the patents.

There can be no assurance that SEFE will obtain allowance on any of the pending patents in our portfolio or, if obtained, that others will not develop functionally similar products that do not infringe on the patents.

Because of competitive pressures from competitors with more resources, SEFE may fail to implement its business model profitably.

SEFE operates in a highly competitive market segment. Our competitors include larger and more established companies at local, regional, and national levels. Generally, our actual and potential competitors have longer operating histories, significantly greater financial and marketing resources, as well as greater name recognition.Therefore, many of these competitors may be able to devote greater resources than SEFE to sales and marketing efforts, expanding their operations and hiring and retaining key employees. There can be no assurance that our current or potential competitors will not develop or offer comparable or superior products to those expected to be offered by us. Increased competition could result in lower than expected operating margins or loss of market share, any of which would materially and adversely affect our business, results of operation and financial condition.

We cannot assure you of market acceptance of our technology.

We believe that public pressure and government initiatives are important factors in creating a market for affordable and clean electricity in which we would offer our Harmony units. However, there can be no assurance that there will be sufficient public pressure or that further legislation or other governmental initiatives will be enacted, or that current legislation will not be repealed, amended, or have its implementation delayed. In addition, we are subject to the risk that even if as the alternative electricity market develops, a different form of zero-carbon-footprint electric generator will dominate the market. Another solution could achieve greater market acceptance than atmospheric electricity generation. The failure of a significant market for atmospheric electricity generation and translation developing would have a material adverse effect on our ability to commercialize this aspect of our technology.

We may not be able to protect our patents and intellectual property and we could incur substantial costs defending against infringers of our proprietary technology or defending against claims that our products infringe on the proprietary or other rights of third parties.

We expect to rely on patents and other policies and procedures related to confidentiality to protect our intellectual property. However, some of our intellectual property may not be covered by any patent or patent application. Moreover, we do not know whether any of our pending patent applications or, in the case of patents issued or to be issued, that the claims allowed are or will be sufficiently broad to protect our technology and processes. Even if all of our patent applications are issued and are sufficiently broad, our patents may be challenged, invalidated or competitors may develop functionally similar products to ours that are not covered by our patents. We could incur substantial costs in prosecuting or defending patent infringement suits or otherwise protecting our intellectual property rights. While we have attempted to safeguard and maintain our proprietary rights, we do not know whether we have been or will be completely successful in doing so. Moreover, patent applications filed in foreign countries may be subject to laws, rules and procedures that are substantially different from those of the United States, and any resulting foreign patents may be difficult and expensive to enforce.

Asserting, defending and maintaining our intellectual property rights could be difficult and costly and failure to do so may diminish our ability to compete effectively and may harm our operating results. We may need to pursue lawsuits or legal action in the future to enforce our intellectual property rights, to protect our trade secrets and domain names and to determine the validity and scope of the proprietary rights of others. If third parties prepare and file applications for trademarks used or registered by us, we may oppose those applications and be required to participate in proceedings to determine the priority of rights to the trademark. Similarly, competitors may have filed applications for patents, may have received patents and may obtain additional patents and proprietary rights relating to products or technology that block or compete with ours. We may have to participate in interference proceedings to determine the priority of invention and the right to a patent for the technology. Litigation and interference proceedings, even if they are successful, are expensive to pursue and time consuming, and we could use a substantial amount of our financial resources in either case.

Our internal controls may be inadequate, which could cause our financial reporting to be unreliable and lead to misinformation being disseminated to the public.

Our management is responsible for establishing and maintaining adequate internal control over financial reporting. As defined in Exchange Act Rule 13a-15(f), internal control over financial reporting is a process designed by, or under the supervision of, the principal executive and principal financial officer and effected by the board of directors, management and other personnel, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles and includes those policies and procedures that: (i) pertain to the maintenance of records that in reasonable detail accurately and fairly reflect the transactions and dispositions of the assets of the Company; (ii) provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial statements in accordance with generally accepted accounting principles, and that receipts and expenditures of the Company are being made only in accordance with authorizations of management and directors of the Company; and (iii) provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use or disposition of the Company’s assets that could have a material effect on the financial statements. Our internal controls may be inadequate or ineffective, which could cause our financial reporting to be unreliable and lead to misinformation being disseminated to the public. Investors relying upon this misinformation may make an uninformed investment decision.

The costs and expenses of SEC reporting and compliance may inhibit our operations.

We are currently subject to the reporting requirements of the Securities Exchange Act of 1934, as amended. The costs of complying with such requirements may be substantial. In the event we are unable to establish a base of operations that generates sufficient cash flows or cannot obtain additional equity or debt financing, the costs of maintaining our status as a reporting entity may inhibit out ability to continue our operations.

Because our common stock is deemed a low-priced “Penny” stock, an investment in our common stock should be considered high risk and subject to marketability restrictions.

Since our common stock is a penny stock, as defined in Rule 3a51-1 under the Securities Exchange Act, it will be more difficult for investors to liquidate their investment even if and when a market develops for the common stock. Until the trading price of the common stock rises above $5.00 per share, if ever, trading in the common stock is subject to the penny stock rules of the Securities Exchange Act specified in rules 15g-1 through 15g-10. Those rules require broker-dealers, before effecting transactions in any penny stock, to:

|

1.

|

Deliver to the customer, and obtain a written receipt for, a disclosure document;

|

|

2.

|

Disclose certain price information about the stock;

|

|

3.

|

Disclose the amount of compensation received by the broker-dealer or any associated person of the broker-dealer;

|

|

4.

|

Send monthly statements to customers with market and price information about the penny stock; and

|

|

5.

|

In some circumstances, approve the purchaser’s account under certain standards and deliver written statements to the customer with information specified in the rules.

|

Consequently, the penny stock rules may restrict the ability or willingness of broker-dealers to sell the common stock and may affect the ability of holders to sell their common stock in the secondary market and the price at which such holders can sell any such securities. These additional procedures could also limit our ability to raise additional capital in the future.

FINRA sales practice requirements may also limit a stockholder's ability to buy and sell our stock.

In addition to the “penny stock” rules described above, the Financial Industry Regulatory Authority (FINRA) has adopted rules that require that in recommending an investment to a customer, a broker-dealer must have reasonable grounds for believing that the investment is suitable for that customer. Prior to recommending speculative low priced securities to their non-institutional customers, broker-dealers must make reasonable efforts to obtain information about the customer's financial status, tax status, investment objectives and other information. Under interpretations of these rules, the FINRA believes that there is a high probability that speculative low priced securities will not be suitable for at least some customers. The FINRA requirements make it more difficult for broker-dealers to recommend that their customers buy our common stock, which may limit your ability to buy and sell our stock and have an adverse effect on the market for our shares.

ITEM 1B - UNRESOLVED STAFF COMMENTS

None.

ITEM 2 - PROPERTIES

We use office space at 6821 East Thomas Road, Scottsdale, Arizona 85251. A related party provides this space to us at no charge. We believe that this arrangement is suitable given that our current administrative needs are minimal and are being met by this arrangement. We also believe that we will not need to lease additional administrative offices for at least the next 12 months. Our Science and Technology Center is currently located at 3200 Valmont Boulder, CO 80301. We rent this office at a rate of approximately $1,300 per month plus common area maintenance fees. We have been leasing this facility for the past year and are currently planning a move to a larger space in the Boulder area in order to meet our expanding needs for fabrication testing and acquisition of like technologies.

Our management does not currently have policies regarding the acquisition or sale of real estate assets primarily for possible capital gain or primarily for income. We do not presently hold any investments or interests in real estate, investments in real estate mortgages or securities of or interests in persons primarily engaged in real estate activities.

ITEM 3 - LEGAL PROCEEDINGS

No Director, officer, significant employee, or consultant of SEFE has been convicted in a criminal proceeding, exclusive of traffic violations.

No Director, officer, significant employee, or consultant of SEFE has been permanently or temporarily enjoined, barred, suspended, or otherwise limited from involvement in any type of business, securities or banking activities.

No Director, officer, significant employee, or consultant of SEFE has been convicted of violating a federal or state securities or commodities law.

SEFE is not a party to any pending legal proceedings.

No director, officer, significant employee or consultant of SEFE has had any bankruptcy petition filed by or against any business of which such person was a general partner or executive officer either at the time of the bankruptcy or within two years prior to that time.

ITEM 4 - SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS

None.

PART II

ITEM 5 - MARKET FOR REGISTRANT’S COMMON EQUITY AND RELATED STOCKHOLDER MATTERS MARKET INFORMATION FOR COMMON STOCK

Market information

Our common stock is quoted on the NASD’s OTC Bulletin Board under the trading symbol “SEFE.ob.” The high and low closing prices of our common stock for the periods indicated are set forth below. These closing prices do not reflect retail mark-up, markdown or commissions.

|

Year ended December 31, 2011

|

High

|

Low

|

||||||

|

First Quarter

|

$ | 1.01 | $ | 1.00 | ||||

|

Second Quarter

|

$ | 1.35 | $ | 1.02 | ||||

|

Third Quarter

|

$ | 1.35 | $ | 0.60 | ||||

|

Fourth Quarter

|

$ | 1.01 | $ | 0.51 | ||||

On December 30, 2011 the closing bid price on the OTC Bulletin Board for our common stock was $0.51 per share.

The shares quoted are not now, but could become subject to the provisions of Section 15(g) and Rule 15g-9 of the Securities Exchange Act of 1934, as amended (the Exchange Act”), commonly referred to as the “penny stock” rule. Section 15(g) sets forth certain requirements for transactions in penny stocks and Rule 15g-9(d)(1) incorporates the definition of penny stock as that used in Rule 3a51-1 of the Exchange Act.

The Commission generally defines penny stock to be any equity security that has a market price less than $5.00 per share, subject to certain exceptions. Rule 3a51-1 provides that any equity security is considered to be a penny stock unless that security is: registered and traded on a national securities exchange meeting specified criteria set by the Commission; authorized for quotation on The NASDAQ Stock Market; issued by a registered investment company; excluded from the definition on the basis of price (at least $5.00 per share) or the registrant’s net tangible assets; or exempted from the definition by the Commission. Trading in the shares is subject to additional sales practice requirements on broker-dealers who sell penny stocks to persons other than established customers and accredited investors, generally persons with assets in excess of $1,000,000 or annual income exceeding $200,000, or $300,000 together with their spouse.

For transactions covered by these rules, broker-dealers must make a special suitability determination for the purchase of such securities and must have received the purchaser’s written consent to the transaction prior to the purchase. Additionally, for any transaction involving a penny stock, unless exempt, the rules require the delivery, prior to the first transaction, of a risk disclosure document relating to the penny stock market. A broker-dealer also must disclose the commissions payable to both the broker-dealer and the registered representative, and current quotations for the securities. Finally, the monthly statements must be sent disclosing recent price information for the penny stocks held in the account and information on the limited market in penny stocks. Consequently, these rules may restrict the ability of broker dealers to trade and/or maintain a market in the company’s common stock and may affect the ability of shareholders to sell their shares.

Shares Available Under Rule 144

As of December 31, 2011, we had 31,196,000 shares of common stock outstanding, In general, under the recently amended Rule 144 which became effective on February 15, 2008 a person, or persons whose shares are aggregated, who owns shares that were purchased from us, or any affiliate, at least six months (subject only to the Rule 144(c) public information requirement until the securities have been held for one year), previously, including a person who may be deemed our affiliate, is entitled to sell within any three month period, a number of shares that does not exceed the greater of:

|

1.

|

1% of the then outstanding shares of our common stock; or

|

|

2.

|

The average weekly trading volume of our common stock during the four calendar weeks preceding the date on which notice of the sale is filed with the Securities and Exchange Commission.

|

Sales under Rule 144 are also subject to manner of sale provisions, notice requirements and the availability of current public information about us. Any person who is not deemed to have been our affiliate at any time during the 90 days preceding a sale, and who owns shares within the definition of “restricted securities” under Rule 144 under the Securities Act that were purchased from us, or any affiliate, at least one year previously, is entitled to sell such shares under Rule 144(k) without regard to the volume limitations, manner of sale provisions, public information requirements or notice requirements.

Future sales of restricted common stock under Rule 144 or otherwise or of the shares could negatively impact the market price of our common stock. We are unable to estimate the number of shares that may be sold in the future by our existing stockholders or the effect, if any, that sales of shares by such stockholders will have on the market price of our common stock prevailing from time to time. Sales of substantial amounts of our common stock by existing stockholders could adversely affect prevailing market prices.

Holders

As of December 31, 2011, we had 31,196,000 shares of $0.001 par value common stock issued and outstanding held by 76 shareholders of record. Our transfer agent is: Island Stock Transfer, Inc., 100 Second Avenue South, Suite 705S, St. Petersburg, Florida 33701, and phone: (727) 289-0010, fax: (727) 289-0069.

Dividends

We have never declared or paid any cash dividends on our common stock. For the foreseeable future, we intend to retain any earnings to finance the development and expansion of our business, and we do not anticipate paying any cash dividends on our common stock. Any future determination to pay dividends will be at the discretion of the Board of Directors and will be dependent upon then existing conditions, including our financial condition and results of operations, capital requirements, contractual restrictions, business prospects and other factors that the board of directors considers relevant.

Recent Sales of Unregistered Securities

Sales conducted under an exemption from registration provided under Section 4(2).

On June 25, 2010, we entered into three Bridge Loan Agreements, with collectively, the “Holders”, for $145,000, $120,000, and $25,000, respectively, for an aggregate amount of $290,000. The Notes bear an interest rate of 10% per annum, payable on Maturity. During the year ended December 31, 2011, the Holders sold the Notes to third-party investors in transactions not involving the Company. As of December 31, 2011, the notes were in default. In connection with the Notes, and for no additional consideration, we issued to the Holders an aggregate of 1,000,000 shares of common stock. Subsequent to December 31, 2011, the period covered by this annual report the holders converted the principal amount of the notes into 8,847,456 shares of common stock and all interest accrued thereupon has been forgiven.

As a result of the Intellectual Property Assignment Agreement entered into on July 13, 2010, we issued an aggregate of 30,000,000 shares of common stock to SEFE Delaware.

On July 16, 2010, in accordance with the Intellectual Property Assignment Agreement, Ms. Helen Cary cancelled 144,900,000 of the 150,000,000 shares of our common stock owned by her. Subsequent to the cancellation, Ms. Cary continues to hold 5,100,000 shares of our common stock.

Additionally, in connection with the July 16, 2010 Intellectual Property Assignment Agreement, we assumed liabilities totaling $250,000 in the form of convertible notes payable, due equitably to two holders, one of which is a related party entity. The notes bear an interest rate of 5% per annum. During the year ended December 31, 2010, the Holders sold the Notes to four individuals. The Notes were due and payable in full on May 5, 2011. As of December 31, 2011, the loan is in default. The notes are convertible by the holders into shares of our common stock at a rate of $0.50 per share. Subsequent to December 31, 2011, the holders converted the principal amount of the notes into 7,627,118 shares of common stock and all interest accrued has been forgiven.

On August 3, 2010, we issued warrants to purchase shares of our par value common stock to one non-affiliated entity in conjunction with a legal services agreement. The warrant holder was granted the right to purchase 125,000 shares of common stock at an exercise price of $1.00 per share, for an aggregate purchase price of $125,000. The warrants expire in August of 2012.

On November 2, 2010, we entered into a Bridge Loan Agreement, whereby we borrowed $50,000 from a related party entity. As of December 31, 2011, the loan is in default. The loan bears an interest rate of 10% per annum, payable on maturity. During the year ended December 31, 2011, the lender sold the promissory note to an individual. Subsequent to December 31, 2011, the holder converted the principal amount of the note into 1,525,424 shares of common stock and all interest accrued has been forgiven.

On November 29, 2010, we issued a total of 17,000,000 restricted shares of common stock to David Ide and Shannon Kerr, both of whom serve on our board of directors.

From January through March 2011, we entered into three Convertible Debenture Agreements with a third-party entity to borrow an aggregate $270,000 from a third party entity. The notes are convertible at our sole discretion into shares of our par value common stock at a rate of $0.50 per share of common stock.

As of October 1, 2011, we entered into Separation Agreements, with Addendums thereto, for the principals of SEFE Delaware to return for cancellation 26,000,000 of the 30,000,000 shares of common stock issued to SEFE Delaware originally issued in connection with the July 13, 2010 Intellectual Property Assignment Agreement. Messrs. Rod and Ogram are each retaining 2,000,000 of the remaining 4,000,000 shares still issued and outstanding.

We believe that the transactions delineated above are exempt from the registration provisions of Section 5 of the Securities Act as such exemption is provided under Section 4(2) because:

|

1.

|

This issuance did not involve underwriters, underwriting discounts or commissions;

|

|

2.

|

Restrictive legends are placed on all certificates issued;

|

|

3.

|

The distribution did not involve general solicitation or advertising; and

|

|

4.

|

The distribution was made only to insiders, accredited investors or investors who were sophisticated enough to evaluate the risks of the investment. All sophisticated investors were given access to all information about our business and the opportunity to ask questions and receive answers about our business from our management prior to making any investment decision.

|

During the year ended December 31, 2011, we sold 1,274,000 shares of common stock for total cash raised of $637,000. The shares were issued at a price of $0.50 per share. There were no commissions or discounts, was not underwritten and was offered only to accredited investors. The shares bear a restrictive transfer legend. These transactions involved no general solicitation and involved only accredited purchasers. Each purchaser was given the opportunity to ask questions of us and was able to examine all publicly available information filed with the SEC. Thus, we believe that these sales are exempt from registration under Section 4(2) and Regulation D, Rule 506 of the Securities Act of 1933, as amended.

ITEM 6 - SELECTED FINANCIAL DATA

Not applicable.

ITEM 7 - MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Forward-Looking Statements

The statements contained in all parts of this document that are not historical facts are, or may be deemed to be, "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Such forward-looking statements include, but are not limited to, those relating to the following: our ability to secure necessary financing; expected growth; future operating expenses; future margins; fluctuations in interest rates; ability to continue to grow and implement growth, and regarding future growth, cash needs, operations, business plans and financial results and any other statements that are not historical facts.

When used in this document, the words "anticipate," "estimate," "expect," "may," "plans," "project," and similar expressions are intended to be among the statements that identify forward-looking statements. Our results may differ significantly from the results discussed in the forward-looking statements. Such statements involve risks and uncertainties, including, but not limited to, those relating to costs, delays and difficulties related to the Company’s dependence on its ability to attract and retain skilled managers and other personnel; the uncertainty of the Company's ability to manage and continue its growth and implement its business strategy; its vulnerability to general economic conditions; accuracy of accounting and other estimates; the Company's future financial and operating results, cash needs and demand for services; and the Company's ability to maintain and comply with permits and licenses; as well as other risk factors described in this Annual Report. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual outcomes may vary materially from those projected.

Overview

We were originally incorporated in the State of Nevada on September 24, 2004 as “Midnight Candle Company.” Our prior stated business objective was to distribute candles and candle-related products. Through the date of this quarterly report, we only generated minimal revenues from that line of business.

On July 16, 2010, we entered into an Intellectual Property Assignment Agreement by and between SEFE, Inc., a Delaware corporation, Ms. Helen C. Cary, the majority shareholder of our issued and outstanding common stock, and Midnight Candle Company. In accordance with the Assignment, we acquired all of SEFE’s right, title and interest in and to various information, inventions, discoveries, writings, expressions, ideas, know-how, concepts, techniques, innovations, systems, processes, procedures, methods, prototypes, designs, and technical data involving or relating to certain atmospheric static electricity collectors, generators, and converters, as generally described in four U.S. Patent Applications. In exchange for the assignment of the Patents, we agreed to the following:

|

1.

|

The assumption of liabilities of SEFE, in the aggregate of $250,000;

|

|

2.

|

The issuance of 30,000,000 shares of the Registrant’s unregistered common stock; and

|

|

3.

|

The cancellation by Ms. Cary of 144,900,000 shares of the Registrant’s common stock owned by her.

|

For a more detailed explanation of the above transactions please see the Company’s Form 8-K filed with the SEC on July 19, 2010, and subsequent amendments made thereto.

On July 20, 2010, we amended our articles of incorporation with the Secretary of State of Nevada to change our name from Midnight Candle Company to “SEFE, Inc.”

As of October 1, 2011, we entered into Separation Agreements, with Addendums thereto, for the principals of SEFE Delaware to return for cancellation 26,000,000 of the 30,000,000 shares of common stock issued to SEFE Delaware originally issued in connection with the July 13, 2010 Intellectual Property Assignment Agreement. Messrs. Rod and Ogram are each retaining 2,000,000 of the remaining 4,000,000 shares still issued and outstanding.

SEFE was founded to develop and bring to market a renewable source of energy that naturally occurs in the atmosphere. The zero carbon footprint of static electric energy can be captured and converted to usable electricity with the proprietary methodology developed by our company. SEFE’s energy production methodologies and technologies are un-intrusive to existing communities, easily adoptable, aim to have high output and leave a low carbon footprint. The SEFE system operates by capturing static electricity from the atmosphere and making it usable for utility companies. This is a renewable source, but also one that is non-polluting and economical.

Our patents will provide barriers to entry and fortify our foundational business construct. In addition, SEFE will continue its forward-looking strategy resulting in additional patent filings and applications with the United States Patent and Trademark Office with the goal of protecting our Inventions through the development of our business model. Through the date of this quarterly report, we have one issued patent, three allowed by the USPTO awaiting patent numbers and 19 more at various stages of the filing process:

|

1.

|

Issued Patent Number:.: 77,855,476

|

Title: Atmospheric Electrical Generator

|

2.

|

Issued Patent Number: 8,102,078

|

Title: Dynamic Electrical Converter System

|

3.

|

IssuedIssued Patent Number: 8,102,082

|

Title: Atmospheric Electricity Collector

|

4.

|

IssuedIssued Patent Number: 8,102,083

|

Title: Atmospheric Electrical Generator with Change of State

|

5.

|

Application No.: 13/103,988

|

Title: Strain Reduction On A Balloon System In Extreme Weather Conditions

|

6.

|

Application No.: 13/103,963

|

Title: Atmospheric Energy Collection

|

7.

|

Application No.: 13/106,759

|

Title: Collection of Atmospheric Ions

Results of Operations

During the year ended December 31, 2010, we discontinued our prior candle business and have dedicated our focus on developing our proprietary technology that harvests static electricity in the earth’s atmosphere. We have not generated revenues from this new line of business. Our operations remain in the development stage and we are unable to predict when, if ever, we will begin to generate revenues. Due to a change in business, year-to-year comparisons are not significant and are not a reliable indicator of future prospects.

Operating Expenses

In the course of our operations, we incur operating expenses composed largely of general and administrative costs and professional fees. General and administrative expenses are essentially the cost of doing business, and encompass, without limitation, the following: licenses; taxes; general office expenses, such as postage, supplies and printing; utilities; bank charges; website costs; and other miscellaneous expenditures not otherwise classified. Accounting fees include: auditing by our independent registered public accountants, bookkeeping, tax preparation fees for filing Federal and State income tax returns and other accounting-specific consulting services. Professional fees include: transfer agent fees for printing stock certificates; consulting costs for marketing and advertising; general business development; and Edgarization fees for the submission of reports and information statements with the U.S. Securities and Exchange Commission. We have also incurred costs that are the result of the development and testing of our proprietary technologies, which aim to harvest atmospheric electricity.

For the year ended December 31, 2011, we incurred operating expenses in the amount of $895,867, composed of $113,116 in advertising and marketing fees, $23,547 in depreciation related to furniture, fixtures and equipment acquired from SEFE (Delaware), $3,608 in amortization expense attributable to certain intangible assets acquired from SEFE (Delaware), executive compensation paid to officers of $262,500, $193,634 in general and administrative expenses and $299,462 in professional fees.

In the comparable year ended December 31, 2010, we incurred operating expenses in the amount of $513,331, composed of impairment expense in the amount of $213,976, executive compensation of $126,395 and professional fees in the amount of $96,212. Via the July 2010 Intellectual Property Assignment Agreement, we acquired four U.S. patent applications valued at $213,976. However, estimating potential revenues and cash flows that may be generated as a result of monetizing the subject technologies is difficult. As a result, during the year ended December 31, 2010, we determined it necessary to impair the value of the patents in full.

Since our inception on September 24, 2004 through December 31, 2011, aggregate operating expenditures were $1,463,634. Our operating expenses are tied directly to our ongoing operations and research and development. As a result, we anticipate expenditures increasing through the foreseeable future and may vary dramatically from period to period.

Interest Expense

In 2010, we entered into several bridge loans, aggregating $860,000, bearing varying interest rates. During the year ended December 31, 2011, we recorded interest expense of $192,856, related to debt financing we have obtained to fund our expected operational strategies. Interest expense incurred during the year ended December 31, 2010 was $25,082. Since inception to December 31, 2011, we incurred $217,938 in interest expense.

Net Losses

We have experienced net losses in all periods since our inception. Our net losses for the years ended December 31, 2011 and 2010 were $1,088,723 and $538,413, respectively. Our net loss since the date of our inception through December 31, 2011 was $1,681,476. We anticipate incurring ongoing operating losses and cannot predict when, if at all, we may expect these losses to plateau or narrow.

Liquidity and Capital Resources

Cash used in operations during the year ended December 31, 2011 was $840,137, compared to $282,963 of cash used in operations during the comparable period ended December 31, 2010. Since inception, we have used $1,177,315 in cash for general operations and developmental activities.

Cash used in investing activities was $12,147 during the year ended December 31, 2011, compared to $54,476 in the year ago period ended December 31, 2010. From inception to December 31, 2010, cash used in investing activities was $66,623 related to the purchase and acquisition of fixed assets and intellectual property.

During the year ended December 31, 2011, net cash provided by financing activities totaled $913,668. The bulk of cash was provided by sales of our common stock, to the tune of $637,000, as well as issuances of debt securities totaling $307,627 during the year ended December 31, 2011. In comparison, during the year ended December 31, 2010, financing activities provided $337,428 in cash, primarily from issuances of our notes payable aggregating $349,544 in cash, of which $170,000 is owed to a related party. Since our inception through December 31, 2011, $1,305,322 in cash was provided by financing activities.

As of December 31, 2011, we had $61,384 of cash on hand. Our management believes this amount is not sufficient to maintain our operations for at least the next 12 months. We are actively raising additional capital by conducting additional issuances of our equity and debt securities for cash. We cannot assure you that any financing can be obtained or, if obtained, that it will be on reasonable terms. As such, our principal accountants have expressed doubt about our ability to continue as a going concern because we have limited operations and have not fully commenced planned principal operations.

Subsequent to the year ended December 31, 2011, the period covered by this annual report, our management has made significant attempts to bolster our balance sheet and obtain operating capital. To this end, we have arranged with our note holders to convert $590,000 of our bridge notes, into 17,999,998 shares of our common stock. All interest accrued thereupon has been forgiven as of the dates of conversion. Additionally, we sold 383,000 shares of common stock for cash of $179,000, between January 1, 2012 and March 29, 2012.

Our management expects to incur up to, but not in excess of, $425,000 in research and development costs.

We do not have any off-balance sheet arrangements.

We currently do not own any significant plant or equipment that we would seek to sell in the near future.

We have not paid for expenses on behalf of any of our directors. Additionally, we believe that this fact shall not materially change.

Plan of Operation

SEFE has recognized an alternative source of energy that naturally occurs in the atmosphere. This energy can be captured and converted to usable electricity with a proprietary methodology developed or otherwise owned by SEFE. The SEFE system operates by capturing static electricity from the atmosphere and making it usable for utility companies. This is a renewable source, but also one that is non-polluting and economical. The SEFE system is designed to operate in the following manner:

|

·

|

An electrical lead held aloft by a suspension mechanism

|

|

·

|

Static electricity is absorbed by the lead

|

|

·

|

The direct current of electricity is converted to an alternating current using our proprietary methods

|

|

·

|

The collected electricity is sent to an isolated platform

|

|

·

|

The platform sends the current to a converter to do either one of the following:

|

|

·

|

Translate the direct current into an alternating current in usable form and

|

|

·

|

Convert the electricity back into direct current and stores it in batteries for later use

|

|

·

|

Electricity is communicated to existing residential and commercial locations (using the existing power distribution infrastructure from the utility companies)

|

We currently work with a number of professional firms who provide various consulting, advisory and/or other service essential to our operations:

|

1.

|

Greenberg Traurig, LLP – securities counsel

|

|

2.

|

Mintz, Levin, Cohn, Ferris, Glovsky and Popeo, PC – intellectual property, mergers and acquisitions and general counsel

|

|

3.

|

Weaver, Martin & Samyn, LLC - independent registered certified public accounting firm.

|

For additional information about our company and our business, you can visit our corporate website at www.sefelectric.com. It currently contains access to our reporting information and we plan to continue providing access to our reporting information through this corporate website.

Ongoing data collection continues to measure the amount of atmospheric electricity available in various weather conditions, amounts of cloud cover, altitudes, and elevations above sea level. We will capitalize on the information gleaned from our most recent and upcoming tests in order to move into fabrication of our commercial grade units. We have strategically studied topography and weather conditions throughout the United States in order to determine the areas where we might harvest the maximum amount of electricity. Much of 2011 has been spent developing, building, and doing in-lab testing of SEFE’s proprietary detection system. This system will help determine where we might find maximum available atmospheric energy sources in order to best concentrate our sales efforts. We have also conducted research into the relevant details of the largest mining, manufacturing, and construction concerns across the United States to determine how much electricity our units would be able to generate for those potential clients under their current conditions and, by extension, how much our units would be able to provide in savings to these potential customers. In the event that we are unable to receive funding, it may be impossible for us to meet these stated milestones and continue on the path toward the generation of revenue.

We plan on generating revenue by selling the electricity produced by our Harmony III commercial grade units,, as well as by leasing the units themselves. The key to our Harmony III unit is its ability to capture and translate the electrical source found in the atmosphere into a usable current that can be utilized in generators and existing power grids without changes to the current power infrastructure.

Milestones to be met on the way to commercializing the Harmony III include:

|

1.

|

Completing the data collection to determine how much electricity can be generated and stored by each unit over a period of time based on location, altitude, weather, and other factors;

|

|

2.

|

Fabrication of our initial commercial grade unit;

|

|

3.

|

Securing contracts with mining organizations and/or utility companies

|

|

4.

|

Implementation of the communications, monitoring methodologies, and security for each unit through our Network Operations Center

|

Through the current year ended December 31, 2011, we have made the following advancements in our business objectives:

|

1.

|

Field tests prove that we have obtained wattage at low altitudes and in sub-optimal weather conditions;

|

|

2.

|

Initial development and fabrication of proprietary Atmospheric Energy Detection System with mechanisms to measure changes in available power in various weather conditions and at a range of altitude, elevation, and humidity levels.

|

|

3.

|

The United States Patent and Trademark Organization has issued the following patents:

|

|

a.

|

Issued Patent Number:.: 7,855,476

Title: Atmospheric Electrical Generator

|

|

b.

|

Issued Patent Number: 8,102,078

Title: Dynamic Electrical Converter System

|

|

c.

|

Issued Patent Number: 8,102,082

Title: Atmospheric Electricity Collector

|

|

d.

|

Issued Patent Number: 8,102,083

Title: Atmospheric Electrical Generator with Change of State

|

|

4.

|

The USPTO has accepted the applications for the following patents:

|

|

|

Application No.: 13/103,988

Title: Strain Reduction On A Balloon System In Extreme Weather Conditions

Application No.: 13/103,963

Title: Atmospheric Energy Collection

Application No.: 13/106,759

Title: Collection of Atmospheric Ions

|

|

5.

|

Expanded our intellectual patent portfolio to 22 patents in various stages.

|

|

6.

|

Ongoing development of new technologies to improve the commercial scalability of our technology

|

|

7.

|

Formation of capital to move forward with development, testing, and fabrication

|

|

8.

|

Research into potential clients across multiple industries which will allow SEFE to generate revenue through several channels (licensing of hardware, maintenance, sale of power, etc.)

|

We are a small, development stage company attempting to establish ourselves in a relatively new, untapped niche in the energy industry. We are actively engaged in building our infrastructure, upon which we will establish a base of operations. We are currently working on solidifying partnerships with multiple accredited universities in the United States. We anticipate that these relationships will provide us with the manpower to complete the design, testing, and implementation elements for our commercial grade units as well as to build our intellectual property portfolio. We are also developing a grant-writing program to generate interest and support for our project on a national basis. We anticipate securing equity financing in order to provide the funding for our continued operation and move us into the fabrication of our commercial units.

Anticipated costs of all of the aforementioned efforts are estimated to total about $3,000,000 over the next twelve months. In order to fund our proposed plan of operation, we are currently contemplating conducting an offering of our common stock to raise a minimum of approximately $3,000,000 up to a maximum of $8,000,000 to finance our plan of operations. These funds are expected to be raised through equity financing, which will result in further dilution in the equity ownership of the shares currently issued and outstanding. We are significantly dependent upon obtaining at least the minimum proceeds of this proposed offering in order to pursue the plan of operations set forth herein. We cannot provide investors with any assurance that we will be able to raise any funds and we have no commitments to raise the additional funding. In the event we are unable to locate at least the minimum offering amount contemplated, we may be unable to fully execute our business.

Critical Accounting Policies

Our Management’s Discussion and Analysis of Financial Condition and Results of Operations section discusses our financial statements, which have been prepared in accordance with accounting principles generally accepted in the United States of America. The preparation of the financial statements requires us to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. On an on-going basis, we evaluate our estimates and judgments, including those related to revenue recognition, recoverability of intangible assets, and contingencies and litigation. We base our estimates and judgments on historical experience and on various other factors that are believed to be reasonable under the circumstances, the results of which form the basis for making judgments about the carrying value of assets and liabilities that are not readily apparent from other sources. Actual results may differ from these estimates under different assumptions or conditions. The most significant accounting estimates inherent in the preparation of our consolidated financial statements include estimates as to the appropriate carrying value of certain assets and liabilities which are not readily apparent from other sources, primarily the valuation of intangible assets. The methods, estimates and judgments we use in applying these most critical accounting policies have a significant impact on the results we report in our consolidated financial statements.

Use of estimates

The preparation of financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the reporting period. Actual results could differ from those estimates.

Intangible assets

Management regularly reviews property, equipment, intangibles and other long-lived assets for possible impairment. This review occurs quarterly, or more frequently if events or changes in circumstances indicate the carrying amount of the asset may not be recoverable. If there is indication of impairment, then management prepares an estimate of future cash flows expected to result from the use of the asset and its eventual disposition. If these cash flows are less than the carrying amount of the asset, an impairment loss is recognized to write down the asset to its estimated fair value. Management believes that the accounting estimate related to impairment of its property and equipment, is a “critical accounting estimate” because: (1) it is highly susceptible to change from period to period because it requires management to estimate fair value, which is based on assumptions about cash flows and discount rates; and (2) the impact that recognizing an impairment would have on the assets reported on our balance sheet, as well as net income, could be material. Management’s assumptions about cash flows and discount rates require significant judgment because actual revenues and expenses have fluctuated in the past and are expected to continue to do so.

The Company capitalizes the costs associated with the development of the Company’s website pursuant to ASC Topic 350. Other costs related to the maintenance of the website are expensed as incurred. Amortization is provided over the estimated useful lives of 3 years using the straight-line method for financial statement purposes. The Company commenced amortization during the quarter ended September 30, 2010, once the economic benefits of the assets began to be consumed. Amortization expense for the years ended December 31, 2011 and 2010 totaled $3,608 and $1,369, respectively.

The Company reviews the carrying value of intangible assets for impairment whenever events and circumstances indicate that the carrying value may not be recoverable from the estimated future cash flows expected to result from its use and eventual disposition. In cases where undiscounted expected future cash flows are less than the carrying value, an impairment loss is recognized equal to the amount by which the carrying value exceeds the fair value. The factors considered by management in performing this assessment include current operating results, trends and prospects, the manner in which the property is used, and the effects of obsolescence, demand, competition and other economic factors. On July 16, 2010, the Company obtained certain intangible assets through an Intellectual Property Assignment Agreement. Management of the Company reviewed the intangible assets and has decided to write down the value of the assets. As a result of this assessment, the Company recorded impairment expense of $213,976 during the year ended December 31, 2010.

Property and equipment

Property and equipment is recorded at cost. Expenditures for major additions and improvements are capitalized and minor replacements, maintenance, and repairs are charged to expense as incurred. When property and equipment is retired or otherwise disposed of, the cost and accumulated depreciation are removed from the accounts and any resulting gain or loss is included in the results of operations for the respective period. Depreciation is provided over the estimated useful lives of the related assets using the straight-line method for financial statement purposes. The Company uses other depreciation methods (generally accelerated) for tax purposes where appropriate. The estimated useful lives for significant property and equipment categories are as follows:

|

Furniture and fixtures

|

5 years

|

|

Equipment

|

5 years

|

The Company reviews the carrying value of property and equipment for impairment whenever events and circumstances indicate that the carrying value of an asset may not be recoverable from the estimated future cash flows expected to result from its use and eventual disposition. In cases where undiscounted expected future cash flows are less than the carrying value, an impairment loss is recognized equal to an amount by which the carrying value exceeds the fair value of assets. The factors considered by management in performing this assessment include current operating results, trends and prospects, the manner in which the property is used, and the effects of obsolescence, demand, competition and other economic factors. Based on this assessment there was no impairment as December 31, 2011 or 2010. Depreciation expense for the years ended December 31, 2011 and 2010 totaled $23,546 and $6,325, respectively.

Revenue recognition

The Company recognizes revenue when all of the following conditions are satisfied: (1) there is persuasive evidence of an arrangement; (2) the service has been provided to the customer; (3) the amount of fees to be paid by the customer is fixed or determinable; and (4) the collection of our fees is probable. There was no revenue for the years ended December 31, 2011 or 2010.