Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - FAIRPOINT COMMUNICATIONS INC | d318991d8k.htm |

March

2012 Investor Presentation

Exhibit 99.1 |

2

Notices and Safe Harbors

The information contained herein is current only as of the date hereof. The business,

prospects, financial condition or performance of FairPoint Communications, Inc.

(“FairPoint”) and its subsidiaries described herein may have changed since that

date. FairPoint does not intend to update or otherwise revise the information contained herein.

FairPoint makes no representation or warranty, express or implied, as to the completeness of

the information contained herein. If any other information is given or any other

representations are made, they should not be relied upon as having been authorized by

FairPoint. Market data used throughout this presentation is based on surveys and studies conducted by

third parties, as well as industry and general publications. FairPoint has no obligation

(express or implied) to update any or all of the information or to advise you of any changes; nor does FairPoint make any express or implied warranties or

representations as to the completeness or accuracy nor does it accept responsibility for

errors. Some statements herein are known as “forward-looking statements” within the

meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the

Securities Exchange Act of 1934, as amended. These forward-looking statements

include, but are not limited to, statements about our plans, objectives, expectations and

intentions and other statements contained herein that are not historical facts. When used

herein, the words “expects,” “anticipates,” “intends,” “plans,” “believes,” “seeks,”

“estimates” and similar expressions are generally intended to identify forward-

looking statements. Because these forward-looking statements involve known and unknown

risks and uncertainties, there are important factors that could cause actual results, events or

developments to differ materially from those expressed or implied by these

forward-looking statements, including our plans, objectives, expectations and intentions

and other factors. You should not place undue reliance on such forward-looking

statements, which are based on the information currently available to us and speak only as of

the date hereof. FairPoint does not undertake any obligation to publicly update or revise

any forward-looking statements, whether as a result of new information, future events or otherwise.

Throughout this presentation, reference is made to Consolidated EBITDAR or EBITDAR and

Unlevered Free Cash Flow. EBITDAR and Unlevered Free Cash Flow are non-GAAP

financial measures. Management believes that EBITDAR and Unlevered Free Cash Flow may be useful

in assessing our operating performance and our ability to meet our debt service

requirements. EBITDAR and Unlevered Free Cash Flow, as used herein, however, are not necessarily comparable to similarly titled measures of other companies.

Furthermore, EBITDAR and Unlevered Free Cash Flow have limitations as analytical tools and

should not be considered in isolation from, or as an alternative to, net income or loss,

operating income, cash flow or other combined income or cash flow data prepared in accordance with GAAP. Because of these limitations, EBITDAR, Unlevered Free Cash

Flow and related ratios should not be considered as measures of discretionary cash available to

invest in business growth or reduce indebtedness. We compensate for these limitations by

relying primarily on our GAAP results using EBITDAR and Unlevered Free Cash Flow only supplementally. The Securities and Exchange Commission (“SEC”) has

adopted rules to regulate the use in filings with the SEC and public disclosures and press

releases of non-GAAP financial measures, such as EBITDAR and Unlevered Free Cash

Flow, that are derived on the basis of methodologies other than in accordance with GAAP. Our

presentation of EBITDAR and Unlevered Free Cash Flow may not comply with these rules.

We provide guidance as to certain financial information herein, which consists of

forward-looking statements. Our guidance is not prepared with a view toward compliance with

the published guidelines of the American Institute of Certified Public Accountants, and neither

our independent registered public accounting firm nor any other independent expert or

outside party compiles or examines the guidance and, accordingly, no such person expresses any opinion or any other form of assurance with respect thereto.

Guidance is based upon a number of assumptions and estimates that, while presented with

numerical specificity, are inherently subject to significant business, economic and

competitive uncertainties and contingencies, many of which are beyond our control and are based

upon specific assumptions with respect to future business decisions, some of which will

change. We generally state possible outcomes as high and low ranges which are intended to provide a sensitivity analysis as variables are changed but are not

intended to represent our actual results which could fall outside of the suggested ranges. The

principal reason that we release this data is to provide a basis for our management to

discuss our business outlook with analysts and investors. Notwithstanding this, we do not accept any responsibility for any projections or reports published by

any such outside analysts or investors. Guidance is necessarily speculative in nature, and it

can be expected that some or all of the assumptions or the guidance furnished by us will

not materialize or will vary significantly from actual results. Accordingly, our guidance is only an estimate of what management believes is realizable as of the date

hereof. Actual results may vary from the guidance and the variations may be material. Investors

should also recognize that the reliability of any forecasted financial data diminishes

the farther in the future that the data is forecast. In light of the foregoing, investors are urged to put the guidance in context and not to place undue reliance on it.

Any inability to successfully implement our operating strategy or the occurrence of any of the

events or circumstances discussed therein could result in the actual operating results

being different than the guidance, and such differences may be material.

Unless otherwise indicated, financial information contained herein is as of December 31, 2011. |

3

Company Overview

•

Operate in 18 states with over 1.3M access

line equivalents

1

80% northern New England (NNE)

20% Telecom Group (TG)

•

NNE: 3 contiguous states with ubiquitous

next-generation network

Incumbent’s network

Insurgent’s market share

27% broadband penetration

2

•

Telecom Group: 30 RLECs in 18 states with

lower competitive profile

47% broadband penetration

2

•

Broadband, voice, video and high-capacity

bandwidth offerings

•

Extensive capital investment to date

15,000 fiber route miles

85% avg. broadband availability in NNE

90% avg. broadband availability in TG

•

Over $1B annual revenue and ~3,500

employees

Service Territory

Telecom Group

Northern New England

Access Line Equivalents

as of Dec. 31, 2011

Northern

New

England

Telecom

Group

Total

Switched access lines:

Residential

514,256

131,197

645,453

Business

262,798

48,443

311,241

Wholesale³

76,065

NM

76,065

Total switched access lines

853,119

179,640

1,032,759

High-speed data

230,563

83,572

314,135

Total access line equivalents

1,083,682

263,212

1,346,894

(1)

Switched access lines plus broadband subscribers as of Dec. 31, 2011

(2)

Broadband subscribers as a % of switched access lines

(3)

UNE-P and Resale lines. Excludes UNE-L and Special Access circuits

|

4

Our Path to Increasing Free Cash Flow

Increasing Free Cash Flow

Operational

Improvements

Regulatory

Progress

Revenue

Transformation

Human

Resource

Strategy |

5

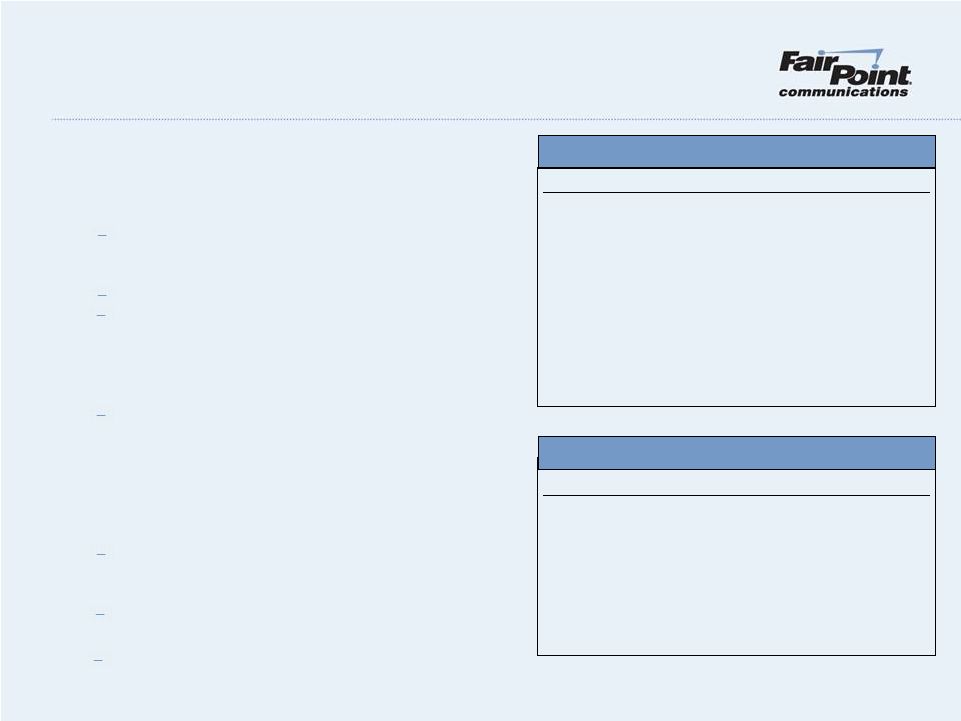

Operational Improvements

FairPoint made significant operational

improvements in 2010 and 2011

•

8.4% growth in 2011

0.4% growth in 2010

•

800+ towers served with fiber

Opportunities for further expansion

•

12% reduction in workforce

$34 million in annual savings

•

Call center volumes decreased

Installation intervals shortened

•

•

8.4% loss in 2011

10.3% loss in 2010

Towers Served with Fiber

2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

-

0

200

400

600

800

1000

1Q11

2Q11

3Q11

4Q11

Broadband Growth (YoY)

Broadband subscriber growth accelerated

Fiber-to-the-Tower initiative

Enabled workforce reduction in 2H11

Service quality has improved

Service quality penalties down

Access line loss has slowed |

6

Regulatory Progress

Regulators in Maine, New Hampshire and

Vermont are beginning to understand the

need for a level playing field in order for

FairPoint to be a strong carrier of last resort

•

Maine PUC submitted a plan to the Legislature

describing actions necessary to ensure all

telecom providers are regulated equally

Legislation is in process

Eliminated service quality penalty multiplier

Improved competitive responsiveness

•

Decreased scope of regulation

Caps retail service quality penalties at $1.7M,

down from $10.5M

Pricing discretion on all products except basic

local voice service

•

Legislation pertaining to the retail deregulation of

companies like FairPoint is advancing in the New

Hampshire Legislature

Maine LD 1466 –

“An Act To Ensure

Regulatory Parity among

Telecommunications Providers”

Vermont Incentive Regulation Plan

New Hampshire

Level

Playing

Field

Carrier of

Last

Resort |

7

Low market share, especially in business

market, creates opportunity for organic growth

in northern New England

Revenue Transformation

FairPoint plans to change the composition of its

revenue base in order to stabilize and then

grow our top line

•

Legacy products in decline

Residential voice

Switched access

ATM/Frame

•

Growth-oriented products

Broadband (residential and business)

Carrier Ethernet Service

Other high-capacity/special access circuits

Revenue Transformation

Total

Revenue

Growth

Products

Declining

Products

Next-generation network in northern New

England provides platform for growth

•

400G of capacity at the core

•

350 COs with inter-office fiber

•

14,000 fiber route miles |

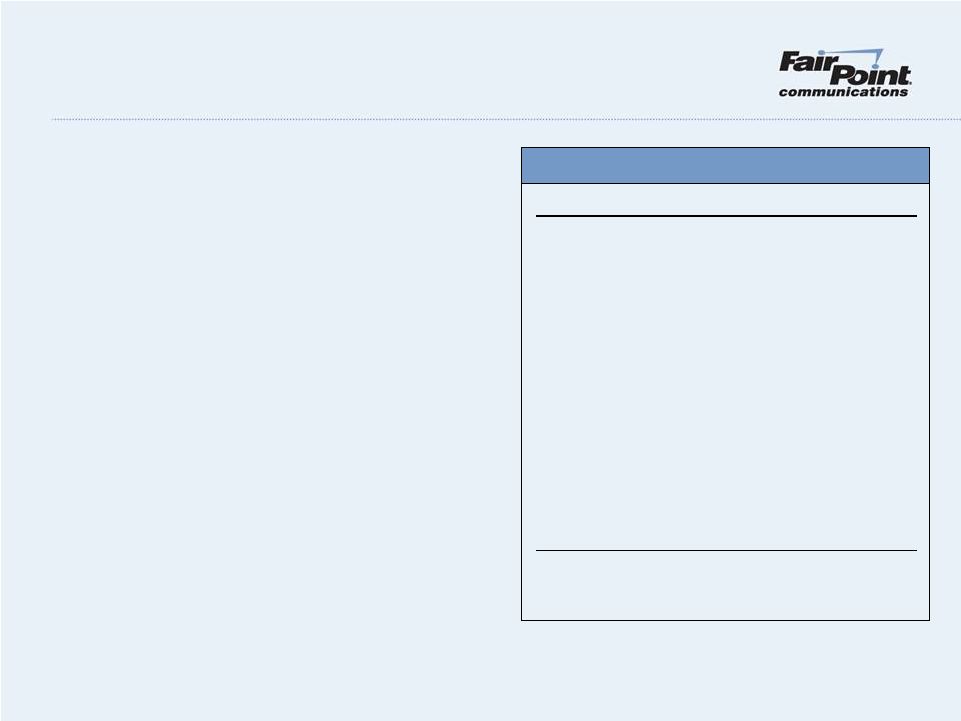

8

Human Resource Strategy

FairPoint must align its human resource

assets with the changing telecom landscape

•

12% workforce reduction in 2011

Lump sum pension distributions of $25 million

•

3,500 employees as of Dec. 31, 2011

1,250 management

2,250 union

Contract expires August, 2014

GAAP figures represent status quo into

perpetuity and reflect continuation of past

practices

Pension and OPEB are highly sensitive to the

discount rate assumption (i.e. interest rates)

OPEB liability is highly sensitive to the medical

cost trend assumption

Pension & OPEB Liability

Pension & OPEB Sensitivity

($ in millions)

2010

2011

Pension

Plan assets

$176.5

$160.3

Projected benefit obligation

$265.8

$318.3

Key assumptions:

Discount rate

5.56%

4.63%

OPEB

Plan assets

$0.2

$1.0

Projected benefit obligation

$344.9

$533.2

Key assumptions:

Discount rate

5.65%

4.66%

Healthcare cost trend (<65 years)

7.70%

8.40%

Healthcare cost trend (>65 years)

8.20%

8.40%

($ in millions)

Pension

OPEB

Impact on liability given 1%

change in the discount rate

assumption

19%

23%

Impact on liability given 1%

increase in healthcare cost trend

assumption

N/A

$134.1

Impact on liability given 1%

decrease in healthcare cost trend

assumption

N/A

($101.1)

•

2,000 union employees covered by

collective

bargaining agreements with the

CWA and IBEW in northern New England

•

Increased labor relations competencies

with telecommunications focus

•

Pension & OPEB liabilities arise from

northern New England union contracts |

9

As of December 31, 2011:

•

Liquidity of $80 million

–

$17 million unrestricted cash

–

$63 million of revolver availability, after $12

million LOCs

•

Leverage of 4.07x vs. 4.75x covenant

•

Interest

coverage

of

3.94x

vs.

3.25x

•

Covenant limiting capital expenditures to:

2011: $200 million

2012: $190 million

2013: $170 million

2014: $150 million

2015: $150 million

Capital Structure

Capital Structure Summary

(1)

Excludes letters of credit of $12 million and capital lease obligations of $4 million

(2)

Before applying letters of credit of $12 million, which reduces revolver availability

(3)

Includes management restricted stock and common stock held in reserve for certain

pre-petition claims as of Dec. 31, 2011

(in millions)

Cash and cash equivalents (unrestricted)

$17

$1,000

Revolver

2

$75

Amortization schedule:

2011

$0

2012

$10

2013

$10

2014

$25

2015

$38

January 24, 2016

$918

L+450, with LIBOR floor of 200

No dividends if leverage > 2.0x

Interest coverage and leverage covenants

Common stock outstanding

3

26.2

Warrants (7 yr, $48.81 strike)

3.6

Gross debt

1

covenant |

10

FairPoint

generated

nearly

$74

million

in

Unlevered

Free

Cash

Flow

1

in

2011

and

grew

cash from $10 million at emergence to over $17 million at Dec. 31, 2011

2012 Guidance:

•

Unlevered Free Cash Flow of $90 to $100 million

•

Continued focus on improving EBITDAR

•

Disciplined capital spending

•

Interest of approximately $68 million

•

Debt amortization of $10 million

Financial Results and Guidance

2011 Financial Highlights

($ in millions)

1Q11

2Q11

3Q11

4Q11

2011

Revenue

$254.8

$262.6

$257.9

$254.2

$1,029.5

Consolidated EBITDAR

2

49.1

70.5

60.5

70.0

250.0

Capital expenditures

53.7

52.1

35.2

35.1

176.1

Unlevered Free Cash Flow

($4.6)

$18.4

$25.3

$34.9

$73.9

(1)

Unlevered Free Cash Flow means Consolidated EBITDAR minus capital expenditures.

Unlevered Free Cash Flow is a non-GAAP financial measure. For a reconciliation of

Net Income (Loss) to Unlevered Free Cash Flow, see our fourth quarter 2011 earnings release furnished on March 7, 2012

on Form 8-K

(2)

As defined in FairPoint’s credit facility. Consolidated EBITDAR is a non-GAAP

financial measure. For a reconciliation of Net Income (Loss) to Consolidated

EBITDAR, see our fourth quarter 2011 earnings release furnished on March 7, 2012 on Form 8-K

Before any possible cash flow sweep as required under FairPoint’s credit facility

(3)

3 |

11

Summary

•

Operational improvements create foundation for transformation

Broadband, FTTT and service quality improvements

Productivity enhancements and 12% workforce reduction

Focusing on productivity gains arising from process and systems enhancements

•

Regulators want a strong carrier of last resort

Supportive of FairPoint’s need for a level playing field

Legislation in process in Maine and New Hampshire

Incentive Regulation Plan in Vermont

•

Transforming revenue by adding sustainable, growth-oriented revenues on our

next-generation network in northern New England

3 contiguous states with network ubiquity

14,000 fiber route miles

26% business market share

•

Focus on increasing free cash flow to drive value |