Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - INTERPHASE CORP | Financial_Report.xls |

| EX-21.A - SUBSIDIARIES OF THE REGISTRANT - INTERPHASE CORP | d263712dex21a.htm |

| EX-31.B - CERTIFICATION PURSUANT TO RULE 13A-14(A) AND 15D-14(A) - INTERPHASE CORP | d263712dex31b.htm |

| EX-31.A - CERTIFICATION PURSUANT TO RULE 13A-14(A) AND 15D-14(A) - INTERPHASE CORP | d263712dex31a.htm |

| EX-32.B - CERTIFICATION PURSUANT TO 18 U.S.C. SECTION 1350 - INTERPHASE CORP | d263712dex32b.htm |

| EX-32.A - CERTIFICATION PURSUANT TO 18 U.S.C. SECTION 1350 - INTERPHASE CORP | d263712dex32a.htm |

| EX-23.A - CONSENT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM - INTERPHASE CORP | d263712dex23a.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2011

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 1-35267

INTERPHASE CORPORATION

(Exact name of registrant as specified in its charter)

| Texas | 75-1549797 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

2901 North Dallas Parkway, Suite 200,

Plano, Texas 75093

(Address of Principal Executive Offices and Zip Code)

(214) 654-5000

Registrant’s telephone number, including area code:

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| Common Stock, $.10 par value | NASDAQ Global Market |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer”, “accelerated filer”, and a “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ¨ Accelerated filer ¨ Non-accelerated filer ¨ Smaller Reporting Company x

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act.): Yes ¨ No x

The aggregate market value of common stock held by non-affiliates of the registrant on June 30, 2011, was approximately $32,000,000. As of March 14, 2012, shares of common stock outstanding totaled 6,914,960.

DOCUMENTS INCORPORATED BY REFERENCE

The information required by Part III of this Report, to the extent not set forth herein, is incorporated herein by reference from the registrant’s definitive proxy statement relating to the Annual Meeting of Shareholders to be held in 2012, which definitive proxy statement shall be filed with the Securities and Exchange Commission within 120 days after the end of the fiscal year to which this Report relates.

PART I

This report contains forward-looking statements about the business, financial condition and prospects of the Company. These statements are made under the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995. The actual results of the Company could differ materially from those indicated by the forward-looking statements because of various risks and uncertainties, including (without limitation) effects of the ongoing issues in global credit and financial markets, our reliance on a limited number of customers, the lack of spending improvements in the telecommunications and computer networking industries, significant changes in product demand, the development and introduction of new products and services, changes in competition, various inventory risks due to changes in market conditions and other risks and uncertainties indicated in Item 1A of this report and in the Company’s other filings and reports with the Securities and Exchange Commission. All of the foregoing risks and uncertainties are beyond the ability of the Company to control, and in many cases, the Company cannot predict the risks and uncertainties that could cause its actual results to differ materially from those indicated by the forward-looking statements. When used in this report, the words “believes,” “plans,” “expects,” “will,” “intends,” and “anticipates” and similar expressions as they relate to the Company or its management are intended to identify forward-looking statements.

Item 1. Business.

Company Background

Founded in 1974, Interphase Corporation and its subsidiaries (“Interphase” or the “Company”), a diversified information and communications technology company, delivers embedded communications networking and computing solutions for LTE and WiMAX, interworking gateways, packet processing, network connectivity, and security for key applications for communications and enterprise markets. The Company also offers a comprehensive portfolio of desktop virtualization solutions. Interphase provides expert engineering design and electronics manufacturing services in addition to its commercial-off-the-shelf (COTS) portfolio of products. Interphase is headquartered in Plano, Texas, with sales offices in the United States and Europe. Clients include Alcatel-Lucent, Emerson Network Power, Fujitsu Ltd., Genband, Hewlett Packard, Nokia Siemens Networks, Oracle, and Samsung.

Key Terms and Definitions

Because Interphase is a technology company, many terms used by the Company may be unfamiliar to those outside the industry. The following are some key terms that may be useful in helping the reader understand the products, technologies, and markets relevant for the Company:

AdvancedMC™ or AMC (Advanced Mezzanine Card) – Specifications that define the mezzanine card form factor for use with Advanced Telecommunications Computing Architecture (ATCA) or MicroTCA platforms. AdvancedMC enhances ATCA flexibility by extending its high-bandwidth, multi-protocol interface to individual hot-swappable modules, which are optimized for packet-based telecom applications. Together, ATCA blades equipped with AdvancedMC modules give telecom equipment manufacturers (or TEMs) a versatile platform for quickly building modular telecom systems that could be designed, manufactured, scaled, upgraded and serviced at a much lower cost. AdvancedMC is a trademark of PCI Industrial Computer Manufacturers Group (PICMG).

1

Baseband—A transmission medium through which digital signals are sent without frequency shifting. In general, only one communication channel is available at any given time. Ethernet is an example of a baseband network.

Base Station—A fixed station used in the wireless network for communications between the mobile client (most commonly handsets) and the telecommunications infrastructure. Each cell in a cellular network requires a base station.

Broadband—A transmission facility (communications link) that has bandwidth (capacity) greater than a traditional voice-grade line.

Building Blocks—The basic board-level products used in a system. These products are combined with other hardware and software building blocks to build a network element, system and/or application.

CompactPCI (cPCI)—An industrial-grade variation of the PCI bus standard that utilizes the Versa Module Eurocard (VME) form factor. CompactPCI was widely adopted by telecom equipment suppliers because of its high-density connectors, support for front or rear I/O access and hot-swap capabilities important for “Five 9s” (i.e., 99.999%) reliability. Often referred to as cPCI, it is a standardized architecture for printed circuit boards (governed by PICMG) used in the embedded systems industry, particularly in carrier communications and industrial computing market segments.

Desktop Virtualization—As a concept, separates a personal computer desktop environment from a physical machine using the client–server model of computing. The desktop virtualization model allows the use of virtual machines to let multiple network subscribers maintain individualized desktops on a single, centrally located computer or server. The central machine may operate at a residence, business, or data center. Users may be geographically scattered, but all must be connected to the central machine by a local area network, a wide area network, or the public Internet.

Embedded Computing Systems—Computer systems designed to perform specific and dedicated functions, often with real-time computing constraints. It is embedded as part of a complete device often including hardware and software. By contrast, a general-purpose computer, such as a personal computer, is designed to be flexible and to meet a wide range of end-user needs. Embedded systems control many devices in common use today.

eNodeB—The base station in the LTE radio access network. In contrast with UMTS base stations, eNodeB uses OFDMA/SC-FDMA as air transport technology. An eNodeB contains one or more radio frequency transmitters and receivers used to communicate directly with mobile devices, which move freely around it.

Femtocell—A small cellular base station typically designed for use in residential or small business environments. Originally known as an Access Point Base Station, it connects to the service provider’s network via broadband (such as DSL or cable); current designs typically support two to four active mobile phones in a residential setting. A femtocell allows service providers to extend service indoors, especially where access would otherwise be limited or unavailable. The femtocell incorporates the functionality of a typical base station, but extends it to allow a simpler, self-contained deployment.

2

Gateway Appliances—Network elements that provide translation functions between multiple protocols used for transfer of data and to control information across networks.

Gigabit Ethernet (GigE)—A family of frame-based computer networking technologies for local area networks (LANs). Ethernet operates over twisted wire, coaxial cable and fiber optic cables at speeds starting at 10 Mbps. The original 10 Mbps specification was extended to a speed of 100 Mbps transmission bandwidth with Fast Ethernet and to 1 Gbps with Gigabit Ethernet. GigE is now the most popular variant being deployed. Ethernet itself has evolved to the next 10 Gbps transmission bandwidth capability. As network bandwidth usage continues to rapidly expand world-wide, 10 Gbps is becoming a commonplace offering in enterprise and service provider networks.

Interworking—The ability to seamlessly communicate between devices supporting dissimilar protocols, such as frame relay and Asynchronous Transfer Mode (ATM), by translating between the protocols, not through encapsulation.

Internet Protocol (IP)—The standard method or protocol by which data is sent from one computer to another on the Internet.

Long Term Evolution (LTE or 3GPP LTE)—The project within the 3rd Generation Partnership Project (3GPP) to improve the Universal Mobile Telecommunications System (UMTS) mobile phone standard to cope with future technology evolutions. Goals include improving spectral efficiency, lowering costs, improving services, making use of new spectrum and reframed spectrum opportunities, and better integration with other open standards. A characteristic of so-called “4G” networks such as LTE is that they are fundamentally based upon TCP/IP, the core protocol of the Internet, with higher-level services such as voice, video, and messaging, built on top of this.

Macrocell—A large radio cell. SMR (Specialized Mobile Radio), also known as TMR (Trunk Mobile Radio), systems use macrocells. They work on the basis of a large omni-directional antenna placed at the highest spot in an area, in order to maximize the direct line-of-sight and, therefore, the quality of the signal. SMR systems generally cover a radius of 50 miles or so. A microcell is smaller and a picocell is smaller still.

Microcell—A cell in a mobile communications network served by a low-power cellular base station that covers a limited area, such as a mall, hotel or transportation hub.

OC-3/STM-1—The American and the European standards (respectively) for optical connections at 155.52 Mbps. This line speed is very common in telecommunications access networks.

Packet Processing—Real-time wire-speed analysis and processing of packets in an IP network.

PCI Mezzanine Card (PMC)—A low-profile mezzanine card that is electronically equivalent to the Peripheral Component Interconnect (PCI) specification. PMC cards are used as a quick and cost-effective method to add modular I/O to other card formats such as VME and CompactPCI, thus expanding the processing or I/O density of a single system slot.

Picocell—A mobile communications base station system that provides smaller and more localized coverage (e.g., indoor areas) than a microcell.

3

Small Cell—An umbrella term that incorporates femtocells, picocells and microcells.

SS7 (Signaling System 7)—The protocols used in the public switch telephone network (PSTN) for setting up calls and providing modern transaction services such as caller ID, automatic recall and call forwarding. When you dial “1” in front of a number, SS7 routes the call to your long distance carrier, and it also routes local calls based on the first three digits of the phone number.

System on Chip (SoC or SOC)—An integrated circuit (IC) that integrates all components of a computer or other electronic system into a single chip. It may contain digital, analog, mixed-signal, and often radio-frequency functions all on a single chip substrate. A typical application is in the area of embedded systems.

T1/E1—A digital transmission link with a capacity of 1.544 Mbps (1,544,000 bits per second) or 2.048 Mbps for the European E1 standard. T1 links normally handle 24 voice conversations, but with digital encoding can handle many more voice channels. T1 lines are also used to connect networks across remote distances.

Time-division multiplexing (TDM)—A type of digital or analog multiplexing in which two or more signals, or bit streams, are transferred apparently simultaneously as sub-channels in one communication channel, but physically are taking turns on the channel.

Worldwide Interoperability of Microwave Access (WiMAX)—A standard formed in June 2001 to promote conformance and interoperability of the IEEE 802.16 standard. The WiMAX Forum describes WiMAX as “a standards-based technology enabling the delivery of last mile wireless broadband access as an alternative to cable and DSL.”

Business Strategy

The Company’s business strategy leverages nearly forty years of development and manufacturing expertise; this experience, coupled with a new process for identifying innovative product and solution ideas, is aimed not only at developing its core business, but also at identifying and launching into new high-growth businesses which will continue to help the Company to diversify its products and services into a variety of potential new markets. The Company’s core business has long been providing networking input/output (I/O) devices that serve as building blocks within a telecommunications or enterprise network infrastructure. The Company is focused upon a multi-tiered strategy to expand its reach into innovative and sometimes disruptive technologies and services where the Company believes it has the technology and process excellence to be successful. The Company’s goal is to increase the breadth of its product line, strengthen its portfolio of new solutions and diversify into attractive adjacent markets. The Company has focused its diversification efforts in six main areas.

LTE Baseband Products

The Company is continuing to develop a new baseband product for use in LTE and WiMAX networks. This product targets the high-performance mobile broadband networks by integrating system-on-chip technology, optimized protocol software, 4th generation (4G) microcell, picocell and enterprise femtocell

4

radio access, while offering customers significant “time to market”, “time to revenue” and cost advantages over traditional macrocell architectures. The product supports all of the critical functions of a wireless base station (excluding the radio head), and it is designed for use in 4G networks, including the LTE eNodeB and next generation WiMAX base stations. The mounting pressure on wireless carriers to attract new customers with higher-performance services has fueled a need to reduce their cost per packet in order to handle the increasing load on their networks at an affordable price. The Company continues to see an interest in its LTE AMC and customized form factor products to quickly enable development of home eNodeB’s and enterprise femtocells as well as public access small cell solutions. The Company expects that it will be asked to provide engineering design services to customize this product to its customers’ specific needs for a variety of wireless broadband applications. The slow adoption of LTE small cells has delayed the Company’s ability to generate significant revenue from this program. However, the Company continues to believe that once the deployment of small cells accelerates in order to alleviate the congestion created by growing media consumption in macrocell networks, this product will be well positioned to support that deployment.

Interworking Products

The Company has expanded its market reach and revenue from its interworking products, which include the iSPAN 3650 AMC, iSPAN 3632 AMC, and the 92XX Gateway family of products. All of these products provide the necessary protocol interworking between the TDM networks and IP-based networks, at various levels of channelization, and typically offer customers a significant cost reduction from alternative approaches to accomplish the interworking function.

Desktop Virtualization Products

The Company formally launched its desktop virtualization products under the brand name clouDevice™ on June 27, 2011, at the ISTE (International Society for Technology in Education) tradeshow in Philadelphia, Pennsylvania. Interphase offers differentiated product features, industry-leading price/performance, and an ability to support all major desktop virtualization platforms and different end-user types. These products have generated interest from numerous resellers and end customers, and the Company is in the process of formalizing several reseller agreements. Interphase will continue to expand its marketing and distribution channel activities and continue to introduce new models to expand its product portfolio. The Company expects to begin generating revenues from its desktop virtualization products in 2012.

Engineering Design Services

The Company’s engineering design services offering has broadened its reach beyond traditional telecommunications and enterprise network technologies into new areas within location-based mobile services offerings and high efficiency enterprise computing solutions. These engagements are expected to be not only revenue generators for Interphase in the near term but also, in many cases, to provide additional opportunities for future growth.

5

Electronics Manufacturing Services

This service is offered to clients in need of outsourcing high-quality, high-mix, and low-to-medium-volume product manufacturing. Interphase differentiates itself on the basis of customer responsiveness, high quality, and low total cost of engagement. The Company has positioned its manufacturing services to offer high-quality manufacturing services to those under-served by the top tier contract manufacturers. With its unique breadth of experience, the Company is further able to differentiate itself by providing additional services to customers who are in need of converting an engineering design to a manufacturing ready product. Several electronics manufacturing services customers have completed their supplier qualification phase, which have led to production orders. This marks the beginning of the anticipated revenue growth associated with the introduction of Interphase’s electronics manufacturing services. There are other customers pursuing qualification acceptance with Interphase, and the Company anticipates accelerated revenue growth as these customers complete their qualification process. This services offering can also make Interphase’s manufacturing capability more financially efficient while expanding the number of markets from which the Company generates revenues.

Embedded Computer Vision

In 2010 the Company selected embedded computer vision technology as a new strategic area of business. Since that time, Interphase has been developing a product using this technology that is expected to be very disruptive to or have a significant impact in large target markets. The Company is also currently focused on developing a new brand-specific website and collateral as well as establishing channel relationships necessary to sell this product. Interphase continues to develop and protect its intellectual property related to this product, and has filed five patents on this technology. The Company expects to announce and release the product in the first half of 2012.

Products

Telecommunications and Enterprise Products

The Company offers innovative, high-performance solutions to the converging voice, data, and video communication segments of the telecommunications market while also offering high-value solutions addressing the enterprise computing and government markets. Interphase offers solutions primarily in the following four categories, supporting various form factors such as AMC, PCI-X, PCIe, cPCI, and PMC as well as related software applications:

Network Connectivity

| • | T1/E1 communication controllers that primarily support SS7 signaling |

| • | OC-3/STM-1 ATM network interface cards (NICs) |

| • | Ethernet NICs |

Interworking

| • | OC-3/STM-1 interworking modules |

| • | Gateway appliances (broadband access gateway and media converter) |

6

Multi-core Packet Processors

| • | GigE packet processors |

| • | 10 GigE packet processors |

Wireless Baseband Modules

| • | LTE eNodeB module |

| • | WiMAX base station module |

Desktop Virtualization Products

Cloud computing is not just limited to on-demand IT-related services delivered over the public Internet, such as SaaS (software as a service). It also includes shared hardware computing resources accessible over a private network. A key enabler and integral component of cloud computing is remote hosted desktop virtualization, a new computing architecture that can run multiple desktop environments simultaneously on a centralized server, eliminating the need to use PCs on the client side. Virtual desktops require the use of a client (cloud client), such as a thin client, a zero client, or a multi-seat client. The clouDevice portfolio includes comprehensive client solutions that enable virtual desktops. clouDevice client types include:

Enterprise thin client

| • | A thin client (sometimes called a lean or slim client) is a networked computer device without local storage that uses a remote server as a processing and data engine. A thin client is typically used to support VDI (virtual desktop infrastructure). These models are Citrix Ready® and VMWare® Ready certified. |

High-performance zero client

| • | A zero client is a type of client device that has neither local storage nor a traditional operating system. It is often deployed to support a remote physical desktop using a blade PC/workstation, enabling both powerful computing capabilities and utmost data security. |

Multi-seat client

| • | A multi-seat client for Microsoft MultiPoint Server 2010/2011 is a low-cost computer device that enables simultaneous multi-user sharing of a single host computer. |

7

Services

Interphase has been designing and manufacturing products for the electronics industry for nearly 40 years and now offers this expertise and capability to customers as a separate service. Since Interphase has honed its processes of design for manufacture, and can supplement these services with engineering design services, Interphase believes it can improve its customers’ ability to meet their outsourcing needs by using Interphase as a qualified “one-stop shop” supplier.

Interphase offers services in two basic categories:

Engineering Design Services

| • | Specifications gathering |

| • | Program management |

| • | Detailed design (high performance/cost optimized) |

| • | Rapid prototyping |

Electronics Manufacturing Services

| • | Supply Chain |

| • | Branding and control |

| • | Production assembly |

| • | Integration |

| • | Testing and delivery |

Marketing and Customers

The Company’s network connectivity, interworking and packet processing products are sold to Telecommunications Equipment Manufacturers (TEMs) for inclusion into telecommunications and networking infrastructure solutions designed for use in wireless carrier networks. Enterprise products are delivered to server manufacturers for integration into server platforms for delivery of high-performance application platforms for enterprise networking. The Company’s engineering design and electronics manufacturing services customers are from a variety of different markets within the electronics industry.

During 2011, sales to Nokia Siemens Networks and Alcatel-Lucent were $6.7 million (or 31%) and $4.6 million (or 21%), respectively, of the Company’s consolidated revenues. During 2010, sales to Alcatel-Lucent and Nokia Siemens Networks were $5.1 million (or 28%) and $2.9 million (or 16%), respectively, of the Company’s consolidated revenues. During 2009, sales to Alcatel-Lucent, Emerson and Nokia Siemens Networks were $6.7 million (or 26%), $5.0 million (or 20%) and $4.8 million (or 19%), respectively, of the Company’s consolidated revenues. No other customer accounted for more than 10% of the Company’s consolidated revenues in any of those years.

The Company markets its products through its direct sales force, manufacturers’ representatives and value-added distributors. In addition to the Company’s headquarters in Plano, Texas, the Company has sales offices located in or near Newark, New Jersey; Seattle, Washington; Amsterdam, Holland; and

8

Helsinki, Finland. The Company’s direct sales force sells products directly to key customers and supports manufacturers’ representatives and the distribution channel. See Note 14 of the accompanying notes to the consolidated financial statements for information regarding the Company’s geographic assets and revenues.

Manufacturing and Supplies

Manufacturing operations are conducted at the Company’s manufacturing facility located in Carrollton, Texas. The Company’s products consist primarily of various integrated circuits, other electronic components and firmware assembled onto internally designed printed circuit boards.

The Company uses sole-sourced components on some of its products, as well as standard off-the-shelf items. Historically, the Company has not experienced any significant problems in maintaining an adequate supply of these parts sufficient to satisfy customer demand. The Company believes that it has good relationships with its vendors.

The Company generally has not manufactured products to stock finished goods inventory. Instead, substantially all of the Company’s production is dedicated to specific customer purchase orders. As a result, the Company has limited requirements to maintain significant finished goods inventories.

Patents, Copyrights, Trademarks, Licenses and Intellectual Property

While the Company believes that its success is ultimately dependent upon the innovative skills of its personnel and its ability to anticipate and adapt to technology changes, its ability to compete successfully will depend, in part, upon its ability to protect proprietary technology contained in its products. The Company is building a patent portfolio related to its embedded computer vision technology currently under development. However, Interphase does not hold any patents relative to its current product lines already deployed or released. Instead, as it relates to product lines already deployed or released, the Company relies upon a combination of trade secrets, copyright and trademark laws and contractual restrictions to establish and protect proprietary rights in its products. The development of alternative, proprietary and other technologies by third parties could adversely affect the competitiveness of the Company’s products. Furthermore, the laws of some countries do not provide the same degree of protection of the Company’s proprietary information as do the laws of the United States. Finally, the Company’s adherence to industry-wide technical standards and specifications may limit the Company’s opportunities to provide proprietary product features suitable for intellectual rights protection.

Interphase, the Interphase logo, iWARE, iSPAN, iNAV, SlotOptimizer, and clouDevice are trademarks or registered trademarks of Interphase Corporation.

Many of the Company’s products are designed to include intellectual property obtained from third parties. The Company has entered into several licensing agreements that allow the Company to incorporate third-party intellectual property into its product line, thereby increasing its functionality, performance and interoperability.

The Company is also subject to the risk of litigation alleging infringement of third-party intellectual property rights. Infringement claims could require the Company to expend significant time and money in litigation, paying damages, developing non-infringing technology or acquiring licenses to the technology which is the subject of asserted infringement.

9

Employees

At December 31, 2011, the Company had 81 regular full-time employees, of which 29 were engaged in manufacturing and quality assurance, 21 in research and development, 17 in sales, sales support, customer service and marketing and 14 in general management and administration.

The Company’s success to date has been significantly dependent on the contributions of a number of its key technical and management employees. The loss of the services of one or more of these key employees could have a material adverse effect on the Company. In addition, the Company believes that its future success will depend, in large part, upon its ability to attract and retain highly skilled and motivated technical, managerial, sales and marketing personnel. Competition for such personnel is significant.

None of the Company’s employees are covered by a collective bargaining agreement, and there have been no work stoppages. The Company considers its relationship with its employees to be good.

Competition

The Company’s primary competition currently includes embedded computing vendors specifically dedicated to telecommunication and enterprise I/O market segments. In the case of specific product offerings, Interphase may also face competition from TEMs’ in-house design teams. Increased competition and commoditization of network interface technologies could result in price reductions, reduced margins and loss of market share. The Company also competes with other, primarily regionally based, contract manufacturers. The Company’s products and services compete on the basis of the following key characteristics: performance, functionality, reliability, pricing, quality, customer support skills, ease of integration, time-to-market delivery capabilities, flexibility and compliance with industry standards. Most of the Company’s major TEM customers have chosen to outsource the design, manufacture and software integration of certain communications controllers and protocol processing, and the recent market conditions and reduction in resources have forced some network equipment providers to utilize additional off-the-shelf products for their product design. As Interphase expands further into new market areas like cloud computing, electronics manufacturing, and the target markets of the embedded computer vision product, the Company’s competition will change and in some cases may intensify.

Available Information

The Company maintains a website at www.interphase.com. Copies of this Annual Report on Form 10-K and copies of the Company’s Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and any amendments thereto are or will be available free of charge at the Company’s website as soon as reasonably practical after they are filed with the Securities and Exchange Commission (“SEC”). The public may read and copy any materials the Company files with the SEC at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. The general public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains a website at www.sec.gov that contains reports, proxy and information statements, and other information regarding issuers, including the Company, that file electronically with the SEC.

10

Item 1A. Risk Factors.

The continued issues in global credit and financial markets could materially and adversely affect our business and results of operations.

The global credit and financial markets have been experiencing significant disruptions for several years, including diminished liquidity and credit availability. There can be no assurance that there will not be continuing, or even further, deterioration in credit and financial markets. These economic uncertainties affect businesses such as ours in a number of ways, making it difficult to accurately forecast and plan our future business activities. The continued tightening of credit in financial markets may lead consumers and businesses to postpone spending, which may cause our customers to decrease or delay their existing and future orders with us. In addition, financial difficulties experienced by our suppliers, distributors, or customers could result in product delays, increased accounts receivable defaults and inventory challenges. We are unable to predict the likely duration and severity of the current and potential future disruptions in the credit and financial markets and adverse global economic conditions. There can be no assurance that if the current uncertain economic conditions continue, it will not have a material adverse effect on our operating results, financial condition and cash flows.

The marketing and sale of our products involve lengthy sales cycles. This and other factors make business forecasting extremely difficult and can lead to significant fluctuations in period-to-period results.

We have experienced fluctuations in our period-to-period revenue and operating results in the past and may experience similar fluctuations in the future. Our sales, on both an annual and a quarterly basis, can fluctuate as a result of a variety of factors, many of which are beyond our control. We may have difficulty predicting the volume and timing of orders for products, and delays in closing orders can cause our operating results to fall short of anticipated levels for any period. Delays by our OEM customers in producing products that incorporate our products could also cause operating results to fall short of anticipated levels. Other factors that may particularly contribute to fluctuations in our revenue and operating results include success in achieving design wins, the market acceptance of the OEM products that incorporate our products, the rate of adoption of new products, competition from new technologies and other companies, and the variability of the life cycles of our customers’ products.

Because fluctuations can happen, we believe that comparisons of the results of our operations for preceding quarters are not necessarily predictive of future quarters and that investors should not rely on the results for any one quarter as an indication of how we will perform in the future. Investors should also understand that, if the revenue or operating results for any quarter are less than the level expected by securities analysts or the market in general, the market price of our common stock could immediately and significantly decline.

The telecommunications signaling and networking business is characterized by rapid technological change and frequent introduction of new products.

The market for our products is characterized by rapid technological change and frequent introduction of products based on new technologies. As these products are introduced, the industry standards change. Additionally, the overall telecommunications and networking industry is volatile, as the effects of new technologies, new standards, new products and short life cycles contribute to changes in the industry and

11

the performance of industry participants. Future revenue will depend upon our ability to anticipate technological change and to develop and introduce enhanced products of our own on a timely basis that comply with new industry standards. New product introductions, or the delays thereof, could contribute to quarterly fluctuations in operating results as orders for new products commence and orders for existing products decline. Moreover, significant delays can occur between a product introduction and commencement of volume production. A typical time period from design-win of one of our products to actual production is 18 to 30 months. This timing has varied significantly during times of mergers, economic instability, and technology changes affecting platform architectures. Our inability to develop and manufacture new products in a timely manner, the existence of reliability, quality or availability problems in our products or their component parts, or the failure to achieve market acceptance for our products could have a material adverse effect on our operating results, financial condition and cash flows.

The Company must successfully manage new product and service introductions and the entry into new markets.

As described under Item 1. “Business – Business Strategy” above, we are focused upon a multi-tiered strategy to expand our reach into innovative and sometimes market-disruptive technologies and services where we believe we have the technology and process excellence to be successful. As a result we intend to introduce new products, services and technologies, enhance existing products and services, and effectively stimulate customer demand for new and upgraded products. We expect that these new product and service introductions will lead us into markets where we have not previously competed. The success of new product and service introductions will depend on a number of factors including, but not limited to, timely and successful development of products or services, market acceptance, our ability to manage the risks associated with new products and production ramp issues, the effective management of purchase commitments and inventory levels in line with anticipated product demand, the availability of products in appropriate quantities and costs to meet anticipated demand, the risk that new products may have quality or other defects in the early stages of introduction, and the availability of qualified persons to perform new services. Accordingly, we cannot determine in advance the ultimate effect that new product and service introductions and the entry into new markets will have on our operating results, financial condition and cash flows.

Litigation against us could require significant time of our management, be costly to defend against and/or negatively impact our operating results.

As noted under Item 3. “Legal Proceedings” below, twenty-five former employees (“Plaintiffs”) of Interphase SAS, a subsidiary of Interphase Corporation, brought suit in France against Interphase SAS alleging various causes of action and rights to damages relating to claims of wrongful dismissal of employment, specific French employment indemnities, general economic losses, and contractual claims relating specifically to their employment relationship and contracts entered into between the individual and Interphase SAS. The lawsuits were filed between November 2010 and April 2011 and are pending in the Labor Court of Boulogne-Billancourt, France and the Administrative Court of Cergy-Pontoise, France. The various claims and assertions arise from, and relate to, the Plaintiffs’ release from employment as part of the restructuring actions taken during the third quarter of 2010. See Note 7 in the notes to the consolidated financial statements for more information regarding the 2010 restructuring plan. The updated statement of claim is for an aggregate payment of approximately €3.1 million, which translated to approximately $4.0 million at December 31, 2011, related to these claims. We believe that the Plaintiffs’

12

claims are without merit and plan to vigorously defend ourselves in this lawsuit. Although we do not believe that the Plaintiffs’ claims have merit, litigation (particularly outside of the United States) is inherently unpredictable, and it is possible that we would be required to pay an additional amount to the Plaintiffs. If the potential required amount is significant, the payment could have a material adverse effect on our financial condition. Further, if this litigation were to continue for an extended time, our defense of the Plaintiffs’ claims, even if successful, could require us to pay significant costs (including fees of counsel) and require time and energy of management that could otherwise be spent on our business, all of which could negatively affect our financial condition and operations.

On April 7, 2011, Interphase Corporation was named as one of the defendants in a lawsuit filed by Mosaid Technologies (“Mosaid”) pending in the United States District Court for the Eastern District of Texas. The complaint includes allegations that Interphase has infringed and is still infringing upon a certain registered U.S. patent to which Mosaid has enforcement rights. The sole infringement allegation directed at Interphase appears to concern communications controller chips that Interphase purchases (indirectly) from Freescale Semiconductor, Inc. (“Freescale”), another defendant in the infringement allegation, which are used in several of Interphase’s products.

The complaint requests a judgment that Mosaid’s patents have been and are being infringed upon and, accordingly, an award of an unspecified amount of damages, plus interest and costs, as well as injunctive relief and any other remedies available under law. Because the complaint claims the alleged infringing conduct is willful, it also requests treble damages and attorneys’ fees under the applicable U.S. patent statute.

We do not know if there is any merit to Mosaid’s allegations. Nevertheless, we intend, and we understand that Freescale intends, to vigorously defend the allegations; and to the extent that the infringement claim relates to the Freescale chips used in Interphase’s products, Freescale will also defend Interphase and indemnify Interphase against damages in the lawsuit.

We operate in an intensely competitive marketplace and many of our competitors have greater resources than we do.

The telecommunications, signaling and networking business is extremely competitive, and we face competition from a number of established and emerging companies, both public and private. Our principal competitors have established brand name recognition and market positions, and have substantially greater financial resources to deploy on promotion, advertising, research and product development. In addition, as we broaden our product and service offerings, we may face competition from new competitors. Companies in related markets could offer products with functionality similar or superior to our product offerings. Increased competition could result in significant pricing pressures, which could result in significantly lower average selling prices for our products and services. We may not be able to offset the effects of any price reductions with an increase in sales volumes, cost reductions or otherwise. We expect competition to increase as a result of industry consolidations and alliances, as well as the potential emergence of new competitors. There can be no assurance that we will be able to compete successfully with existing or new competitors or that competitive pressures will not have a material adverse effect on our operating results, financial condition and cash flows.

13

The loss of one or more key customers, or reduced spending by customers, could significantly impact our operating results, financial condition and cash flows.

While we enjoy very good relationships with our customers, there can be no assurance that our principal customers will continue to purchase products from us at the current levels. Orders from our customers are affected by factors such as new product introductions, product life cycles, inventory levels, manufacturing strategies, contract awards, competitive conditions and general economic conditions. Customers typically do not enter into long-term volume purchase contracts with us, and they have certain rights to extend or delay the shipment of their orders. The loss of one or more of our major customers, or the reduction, delay or cancellation of orders or a delay in shipment of products to such customers, could have a material adverse effect on our operating results, financial condition and cash flows.

Schedule delays, cancellations of programs and changes in customer markets can delay or prevent a design-win from reaching the production phase, which could negatively impact our operating results, financial condition and cash flows.

A design-win occurs when a customer or prospective customer notifies us that our product has been selected to be integrated with their product. Ordinarily, there are a number of steps between the design-win and when customers initiate production shipments. Design-wins reach production volumes at varying rates, typically beginning approximately 18 to 30 months after the design-win occurs. A variety of risks, such as schedule delays, customer consolidations, cancellations of programs and changes in customer markets, can delay or prevent the design-win from reaching the production phase. The customer’s failure to bring its product (into which our product is designed) to the production phase could have an adverse effect on our operating results, financial condition and cash flows.

Design defects, errors or problems in our products or services could harm our reputation, revenue and profitability.

If we deliver products or services with errors, defects or problems, our credibility, market acceptance and sales of our products and services could be harmed. Further, if our products or services contain errors, defects or problems, we may be required to expend significant capital and resources to alleviate such problems. Defects could also lead to product liability lawsuits against us or our customers, tort or warranty claims, increased insurance costs or increased service and warranty costs, any of which could harm our business. We have agreed to indemnify our customers in some circumstances against liability from defects in our products. While no such litigation currently exists, product liability litigation arising from errors, defects or problems, even if it resulted in an outcome favorable to us, would be time consuming and costly to defend. Existing or future laws, or unfavorable judicial decisions, could negate any limitation-of-liability provisions that are included in our license agreements. A product liability claim, whether or not successful, could seriously harm our business, financial condition and results of operations.

We maintain insurance coverage for product liability claims. Although we believe this coverage is adequate, there can be no assurance that coverage under insurance policies will be adequate to cover specific product liability claims made against us. In addition, product liability insurance could become more expensive and difficult to maintain and may not be available in the future on commercially reasonable terms or at all. The amount and scope of any insurance coverage may be inadequate if a product liability claim is successfully asserted against us.

14

If our third party suppliers fail to produce quality products or parts in a timely manner, we may not be able to meet our customers’ demands.

Certain components used in our products are currently available from one or only a limited number of sources. There can be no assurance that future supplies will be adequate for our needs or will be available with acceptable prices and terms. Inability in the future to obtain sufficient limited-source components, or to develop alternative sources, could result in delays in product introduction or shipments, and increased component prices could negatively affect gross margins, either of which could have a material adverse effect on operating results, financial condition and cash flows.

We are dependent on one manufacturing facility and if there is an interruption in production we may not be able to deliver products on a timely basis.

We manufacture our products at our Carrollton, Texas facility, and have established alternative manufacturing capabilities through a third party in the event of a disaster in the current facility. Even though we have been successful in establishing an alternative third-party contract manufacturer, there can be no assurance that we would be able to retain its services at the same costs we currently enjoy. In the event of an interruption in production, we may not be able to deliver products on a timely basis, which could have a material adverse effect on our revenue and operating results. Although we currently have business interruption insurance and a disaster recovery plan to mitigate the effect of an interruption, no assurances can be given that such insurance or recovery plan will adequately cover lost business as a result of such an interruption.

Because business forecasting is extremely difficult, we may fail to accurately forecast demand for our products which may expose us to risk associated with inventory.

We must identify the right product mix and maintain sufficient inventory on hand to meet customer orders. Failure to do so could adversely affect our sales and earnings. However, if circumstances change, there could be a material impact on the net realizable value of our inventory, which could adversely affect our results.

We may be unable to effectively protect our proprietary technology, which would negatively affect our ability to compete. Also, if our products are alleged to violate the proprietary rights of others, our ability to compete would be negatively impacted.

Our success depends partly upon certain proprietary technologies developed within our products. Historically, we have relied principally upon trademark, copyright and trade secret laws to protect our proprietary technologies. Over the last two years, we also filed a number of patents and trademarks with the United States Patent and Trademark Office and internationally. In addition, we generally enter into confidentiality or license agreements with our customers, distributors and potential customers, which limit access to, and distribution of, the source code to our software and other proprietary information. Our employees are subject to our strict employment policy regarding confidentiality. There can be no assurance that the steps taken by us in this regard will be adequate to prevent misappropriation of our technologies or to provide an effective remedy in the event of a misappropriation by others.

15

Although we believe our products do not infringe on the proprietary rights of third parties, there can be no assurance that infringement claims will not be asserted, possibly resulting in costly litigation in which we may not ultimately prevail. Adverse determinations in such litigation could result in the loss of proprietary rights, subject us to significant liabilities, require that we seek licenses from third parties or prevent us from manufacturing or selling our products, any of which could have a material adverse effect on our operating results, financial condition and cash flows. As described in Item 3. “Legal Proceedings” below, we are named as one of three defendants in a pending patent infringement case involving intellectual property we license for use in certain of our products.

It may be necessary to obtain technology licenses from others due to the large number of patents in the telecommunications and computer networking industry and the rapid rate of issuance of new patents and new standards or to obtain important new technology. There can be no assurance that these third party technology licenses will be available on commercially reasonable terms. The loss of, or inability to, obtain any of these technology licenses could result in delays or reductions in product shipments. Such delays or reductions in product shipments could have a material adverse effect on our operating results, financial condition and cash flows.

We depend on key personnel to manage our business effectively.

Our success and the pursuit of our business strategy depend on the continued contributions of our personnel and on our ability to attract and retain skilled employees for our current and future business. Changes in personnel could adversely affect our operating results, financial condition and cash flows.

We have substantial international activities, which expose us to additional business risks, including political, economic and currency risks.

In 2011, we derived approximately 65% of our revenues from sales outside of North America. Economic and political conditions in some of these markets, as well as different legal, tax, accounting and other regulatory requirements, may adversely affect our operating results, financial condition and cash flows. We are exposed to adverse movements in foreign currency exchange rates because we conduct business on a global basis and in some cases in foreign currencies. Our operations in France have been measured in the local currency and converted into U.S. Dollars based on published exchange rates for the periods reported and were therefore subject to risk of exchange rate fluctuations (See Item 7A. “Quantitative and Qualitative Disclosures about Market Risk – Foreign Currency Risk” below).

16

We may require additional working capital to fund operations and expand our business.

We believe our current financial resources will be sufficient to meet our present working capital and capital expenditure requirements for the next twelve months. However, we may need to raise additional capital before this period ends to:

| • | fund research and development of new products beyond what is expected in 2012; |

| • | expand product and service offerings beyond what is contemplated in 2012 if unforeseen opportunities arise; |

| • | respond to a rapid increase in demand for our products; |

| • | take advantage of potential acquisition opportunities in the current economic environment; |

| • | invest in businesses and technologies that complement our current operations; or |

| • | respond to unforeseen competitive pressures. |

Our future liquidity and capital requirements will depend upon numerous factors, including the success of the existing and new product and service offerings and potentially competing technological and market developments. However, any projections of future cash flows are subject to substantial uncertainty. From time to time, we expect to evaluate the acquisition of, or investment in, businesses and technologies that complement our current operations. If current cash, marketable securities, lines of credit and cash generated from operations are insufficient to satisfy our liquidity requirements, we may seek to sell additional equity securities, issue debt securities or increase our working capital line of credit. The sale of additional equity securities could result in additional dilution to shareholders. There can be no assurance that financing will be available in amounts or on terms acceptable, if at all. If adequate funds are not available on acceptable terms, our ability to develop or enhance products and services, take advantage of future opportunities or respond to competitive pressures would be limited. This limitation could negatively impact our results of operations, financial condition and cash flows.

We have incurred significant losses.

We posted net losses of $505,000, $8.4 million and $5.6 million for the years ended December 31, 2011, 2010 and 2009, respectively. In order to achieve consistent profitability, we will need to generate higher revenues while containing costs and operating expenses. We cannot be certain that our revenues will grow or that we will generate sufficient revenues to achieve and maintain profitability on a long-term, sustained basis. If we fail to achieve and maintain profitability, the market price of our common stock will likely be negatively impacted.

We may experience significant period-to-period quarterly and annual fluctuations in our revenue and operating results, which may result in volatility in our stock price.

The trading price of our common stock is subject to wide fluctuations in response to quarter-to-quarter fluctuations in operating results, general conditions in the telecommunications and networking industry and other events or factors. In addition, stock markets have experienced extreme price and trading volume volatility in recent years. This volatility has had a substantial effect on the market price of the securities of many high-technology companies for reasons frequently unrelated to the operating performance of the specific companies. These broad market fluctuations may adversely affect the market price of our common stock, which has historically had relatively small trading volumes. As a result, small transactions in our common stock can have a disproportionately large impact on its price.

17

If our stock does not continue to be traded on an established exchange, an active trading market may not exist and the trading price of our stock may decline.

Our common stock is listed on the NASDAQ Global Market. The NASDAQ Global Market’s continued listing standards for our common stock require, among other things, that (i) the closing bid price for our common stock not fall below $1.00; (ii) we have at least 400 beneficial holders and/or holders of record of our common stock; (iii) our stockholders’ equity not fall below $10 million; (iv) we have more than 750,000 shares held by the public (excluding officers, directors, and beneficial holders of 10% or more) with a market value of at least $5.0 million; and (v) we have at least two registered and active dealers meeting the requirements set forth in the standards. A failure to meet these continued listing requirements is generally required to exist for a period of 10 to 30 consecutive business days (depending upon the type of failure) before a deficiency will be determined to exist. If our common stock was threatened with delisting from the NASDAQ Global Market, we may, depending on the circumstances, seek to extend the period for regaining compliance with NASDAQ listing requirements or we may pursue other strategic alternatives to meet the continuing listing standards.

In addition, we may choose to voluntarily delist from NASDAQ, or “go dark,” in the event we believe we may be subject to a delisting proceeding, or for any other reason our Board of Directors determines it to be in the best interest of our stockholders.

If our common stock is delisted by, or we voluntarily delist from, the NASDAQ Global Market, our common stock may be eligible to trade on the NASDAQ Capital Market, the OTC Bulletin Board, or the Pink OTC Markets. In such an event, it could become more difficult to dispose of, or obtain accurate quotations for the price of, our common stock, and there also would likely be a reduction in our coverage by security analysts and the news media, which could cause the price of our common stock to decline further.

Certain provisions of Texas law and our shareholder rights plan may make it more difficult to acquire us, even if such acquisition may be beneficial to our shareholders.

Certain provisions of the Texas corporate statute, to which we are subject, limits business combinations with any “affiliated shareholder,” which is generally any person or group of persons that is, or has been during the preceding three years, the beneficial owner of 20% or more of our outstanding voting shares. Also, we have in place a shareholder rights plan, commonly referred to as a “poison pill” (see Note 9 in the notes to the consolidated financial statements). The statutory provisions and the rights plan may discourage, delay or prevent a third party from acquiring us or acquiring a large portion of our shares (including by initiating a tender offer), even if our shareholders might receive for their shares in any such acquisition a premium over the then current market price of the shares.

The cost of compliance or failure to comply with the Sarbanes-Oxley Act of 2002 may adversely affect our business.

As a smaller reporting company, we are not subject to the provisions of the Sarbanes-Oxley Act of 2002 that require an attestation report from our independent registered public accounting firm regarding our

18

internal controls over financial reporting. If we cease to qualify as a smaller reporting company or as a non-accelerated filer, we would become subject to this requirement, which could cause us to incur substantial additional costs and may adversely affect our financial results. The failure of our independent registered public accounting firm to concur with management’s assessment of the effectiveness of our internal controls over financial reporting may result in investors losing confidence in the reliability of our financial statements, which may result in a decrease in the trading price of our common stock. It may also prevent us from providing the required financial information in a timely manner which could materially and adversely impact our business, our financial condition and the trading price of our common stock, and it may prevent us from otherwise complying with the standards applicable to us as a public company and subject us to additional regulatory consequences.

Item 1B. Unresolved Staff Comments.

None.

Item 2. Properties.

The Company’s executive offices are located in a 22,000-square-foot leased facility located in Plano, Texas. The executive offices serve as the primary location for the Company’s administrative, development and marketing functions. The Company’s manufacturing and operations center is located in a 24,000-square-foot leased facility in Carrollton, Texas. The executive offices lease extends through February 2014, and the manufacturing and operations center lease extends through March 2014. The Company believes that its facilities and equipment are in good operating condition and are adequate for its operations. The Company owns most of the equipment used in its operations. Such equipment consists primarily of engineering equipment, manufacturing and test equipment, computer equipment and fixtures.

Item 3. Legal Proceedings.

Twenty-five former employees (“Plaintiffs”) of Interphase SAS, a subsidiary of Interphase Corporation, brought suit in France against Interphase SAS alleging various causes of action and rights to damages relating to claims of wrongful dismissal of employment, specific French employment indemnities, general economic losses, and contractual claims relating specifically to their employment relationship and contracts entered into between the individual and Interphase SAS. The lawsuits were filed between November 2010 and April 2011 and are pending in the Labor Court of Boulogne-Billancourt, France and the Administrative Court of Cergy-Pontoise, France. The various claims and assertions arise from, and relate to, the Plaintiffs’ release from employment as part of the restructuring actions taken during the third quarter of 2010. See Note 7 in the notes to the consolidated financial statements for more information regarding the restructuring plan. The updated statement of claim is for an aggregate payment of approximately €3.1 million, which translated to approximately $4.0 million at December 31, 2011, related to these claims. The Company believes that the Plaintiffs’ claims are without merit and plans to vigorously defend itself in this lawsuit.

On April 7, 2011, Interphase was named as one of the defendants in a lawsuit filed by Mosaid Technologies (“Mosaid”) pending in the United States District Court for the Eastern District of Texas. The complaint includes allegations that Interphase has infringed and is still infringing upon a certain registered U.S. patent to which Mosaid has enforcement rights. The sole infringement allegation directed at Interphase appears to concern communications controller chips that Interphase purchases (indirectly) from Freescale Semiconductor, Inc. (“Freescale”), another defendant in the infringement allegation, which are used in several of Interphase’s products.

19

The complaint requests a judgment that Mosaid’s patents have been and are being infringed upon and, accordingly, an award of an unspecified amount of damages, plus interest and costs, as well as injunctive relief and any other remedies available under law. Because the complaint claims that the alleged infringing conduct is willful, it also requests treble damages and attorneys’ fees under the applicable U.S. patent statute.

Interphase does not know if there is any merit to Mosaid’s allegations. Nevertheless, Interphase intends, and understands that Freescale intends, to vigorously defend the allegations; and to the extent that the infringement claim relates to the Freescale chips used in Interphase’s products, Freescale will also defend Interphase and indemnify Interphase against damages in the lawsuit.

Item 4. Mine Safety Disclosures.

None.

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Since January 1984, shares of the Company’s common stock have been traded on the NASDAQ Global Market, or its predecessors, under the symbol INPH. The following table summarizes its high and low closing price for each quarter during 2010 and 2011 as reported by the NASDAQ Global Market.

| 2010 |

High | Low | ||||||

| First Quarter |

3.12 | 2.28 | ||||||

| Second Quarter |

2.73 | 1.55 | ||||||

| Third Quarter |

1.79 | 1.46 | ||||||

| Fourth Quarter |

1.87 | 1.20 | ||||||

| 2011 |

High | Low | ||||||

| First Quarter |

7.23 | 1.78 | ||||||

| Second Quarter |

7.11 | 3.35 | ||||||

| Third Quarter |

5.88 | 3.97 | ||||||

| Fourth Quarter |

5.62 | 4.00 | ||||||

The Company had approximately 1,400 beneficial owners of its common stock, of which 67 were of record, as of March 14, 2012.

The Company has not paid dividends on its common stock since its inception. The Board of Directors does not anticipate payment of any dividends in the foreseeable future and intends to continue its present policy of retaining earnings for reinvestment in the operations of the Company.

20

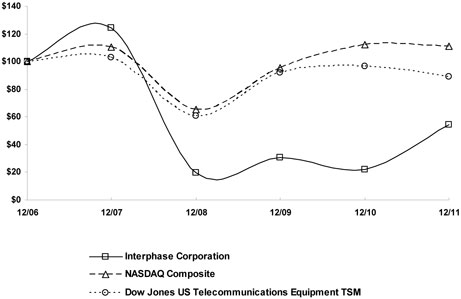

Stock Performance Graph

The following chart compares the cumulative total shareholder return of Interphase common stock during the years ended December 31, 2011, 2010, 2009, 2008 and 2007 with the cumulative total return of the NASDAQ composite index and the Dow Jones US Telecommunications Equipment TSM Index. The Company relied upon information provided by another firm with respect to the stock performance graph. The Company did not attempt to validate the information supplied to it other than review it for reasonableness. The comparison assumes $100 was invested on December 31, 2006 in the common stock of the Company and in each of the foregoing indices, and assumes reinvestment of dividends.

| Cumulative Return | ||||||||||||||||||||||||

| 12/06 | 12/07 | 12/08 | 12/09 | 12/10 | 12/11 | |||||||||||||||||||

| Interphase Corporation |

100 | 124 | 20 | 31 | 22 | 55 | ||||||||||||||||||

| NASDAQ Composite |

100 | 110 | 66 | 95 | 112 | 111 | ||||||||||||||||||

| Dow Jones US Telecommunications Equipment TSM Index |

100 | 103 | 61 | 92 | 97 | 89 | ||||||||||||||||||

COMPARISON OF 5 YEAR CUMULATIVE TOTAL RETURN*

Among Interphase Corporation, the NASDAQ Composite Index,

and the Dow Jones US Telecommunications Equipment TSM Index

| * | $100 invested on 12/31/06 in stock or index, including reinvestment of dividends. |

Fiscal year ending December 31.

Copyright© 2012 Dow Jones & Co. All rights reserved.

21

Item 6. Selected Consolidated Financial Data.

The selected consolidated financial data presented below under the captions “Statement of Operations Data” and “Balance Sheet Data” have been derived from the consolidated balance sheets and the related consolidated statements of operations at or for the years ended December 31, 2011, 2010, 2009, 2008 and 2007, and the notes thereto appearing elsewhere herein, as applicable. In accordance with Accounting Standards Codification (“ASC”) 260-10-45-68B, “Participating Securities and the Two-Class Method,” which became effective January 1, 2009, prior period share data and corresponding EPS figures have been adjusted retrospectively.

It is important that you also read “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements, including the notes thereto, for the years ended December 31, 2011, 2010 and 2009.

Statement of Operations Data:

(In thousands, except per share data)

| Year ended December 31, | ||||||||||||||||||||

| 2011 | 2010 | 2009 | 2008 | 2007 | ||||||||||||||||

| Revenues |

$ | 21,993 | $ | 18,207 | $ | 25,585 | $ | 26,231 | $ | 30,780 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Gross margin |

10,531 | 9,187 | 12,289 | 14,031 | 17,591 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Research and development |

3,814 | 6,572 | 7,970 | 9,198 | 10,216 | |||||||||||||||

| Sales and marketing |

3,498 | 4,512 | 5,753 | 5,237 | 5,614 | |||||||||||||||

| General and administrative |

3,529 | 3,843 | 4,275 | 4,100 | 4,692 | |||||||||||||||

| Restructuring charge |

— | 3,339 | 1,236 | 403 | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Loss from operations |

(310 | ) | (9,079 | ) | (6,945 | ) | (4,907 | ) | (2,931 | ) | ||||||||||

| Other income, net |

22 | 23 | 289 | 618 | 1,128 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Loss before income tax |

(288 | ) | (9,056 | ) | (6,656 | ) | (4,289 | ) | (1,803 | ) | ||||||||||

| Income tax provision (benefit) |

217 | (637 | ) | (1,102 | ) | (1,263 | ) | (609 | ) | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net loss |

$ | (505 | ) | $ | (8,419 | ) | $ | (5,554 | ) | $ | (3,026 | ) | $ | (1,194 | ) | |||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net loss per share |

||||||||||||||||||||

| Basic |

$ | (0.07 | ) | $ | (1.23 | ) | $ | (0.81 | ) | $ | (0.46 | ) | $ | (0.19 | ) | |||||

| Diluted |

$ | (0.07 | ) | $ | (1.23 | ) | $ | (0.81 | ) | $ | (0.46 | ) | $ | (0.19 | ) | |||||

| Weighted average common shares |

6,857 | 6,839 | 6,899 | 6,550 | 6,240 | |||||||||||||||

| Weighted average common and dilutive shares |

6,857 | 6,839 | 6,899 | 6,550 | 6,240 | |||||||||||||||

22

Balance Sheet Data:

(In thousands)

| December 31, | ||||||||||||||||||||

| 2011 | 2010 | 2009 | 2008 | 2007 | ||||||||||||||||

| Working capital |

$ | 13,997 | $ | 13,117 | $ | 21,257 | $ | 25,301 | $ | 27,030 | ||||||||||

| Total assets |

17,818 | 19,314 | 28,647 | 31,248 | 36,180 | |||||||||||||||

| Total liabilities |

6,476 | 8,304 | 9,385 | 6,962 | 8,918 | |||||||||||||||

| Shareholders’ equity |

$ | 11,342 | $ | 11,010 | $ | 19,262 | $ | 24,286 | $ | 27,262 | ||||||||||

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Application of Critical Accounting Policies

The Company’s consolidated financial statements are based on the selection and application of significant accounting policies, which require management to make significant estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. Management believes the following are some of the more critical judgment areas in the application of the Company’s accounting policies that affect the Company’s financial condition, results of operations, and cash flows. Management has reviewed these critical accounting policies and related disclosures with the Audit Committee of the Board of Directors.

Revenue Recognition: Revenues consist of product and service revenues and are recognized in accordance with ASC Topic 605, “Revenue Recognition.” Product revenues and electronics manufacturing services revenues are recognized upon shipment, provided fees are fixed and determinable, a customer purchase order is obtained (when applicable), and collection is probable. Sales tax collected from customers and remitted to the applicable taxing authorities is accounted for on a net basis, with no impact to revenues. Service revenue, other than electronics manufacturing services revenue, is recognized as the services are performed. Deferred revenue consists primarily of service revenue not yet performed.

Our long-term engineering design services are typically provided on a fixed-fee basis. The revenues for such projects that require significant customization and integration are recognized using the percentage of completion method. In using the percentage of completion method, revenues are generally recorded based on the percentage of effort incurred to date on a contract relative to the estimated total expected contract effort. Significant judgment is required when estimating total contract effort and progress to completion on the arrangements, as well as whether a loss is expected to be incurred on the contract. Management uses historical experience, project plans and an assessment of the risks and uncertainties inherent in the arrangement to establish these estimates. Uncertainties include implementation delays or performance issues that may or may not be within our control. Changes in these estimates could result in a material impact on revenues and net earnings (loss). If we are unable to develop reasonably dependable costs or revenue estimates, the completed contract method is applied, under which all revenues and related costs are deferred until the contract is completed.

23

Warranty Reserve: The Company offers to its customers a limited warranty that its products will be free from defect in the materials and workmanship for a specified period. The Company has established a warranty reserve, as a component of accrued liabilities, for any potential claims. The Company estimates its warranty reserve based upon an analysis of all identified or expected claims and an estimate of the cost to resolve those claims. Changes in claim rates and differences between actual and expected warranty costs could impact the warranty reserve estimates.