Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - OmniAmerican Bancorp, Inc. | d315590d8k.htm |

Exhibit 1

| Supplemental Informationat December 31, 2011 Tim Carter Deborah WilkinsonChief Executive Officer Chief Financial Officer |

| Forward Looking Statements 2 This information contains forward-looking statements, which can be identified by the use of words such as "estimate," "project," "believe," "intend," "anticipate," "plan," "seek," "expect," "will," "may" and words of similar meaning. These forward-looking statements include, but are not limited to statements of our goals, intentions and expectations; statements regarding our business plans, prospects, growth and operating strategies; statements regarding the asset quality of our loan and investment portfolios; and estimates of our risks and future costs and benefits. These forward-looking statements are based on our current beliefs and expectations and are inherently subject to significant business, economic and competitive uncertainties and contingencies, many of which are beyond our control. In addition, these forward-looking statements are subject to assumptions with respect to future business strategies and decisions that are subject to change. Because of these and other uncertainties, our actual future results may be materially different from the results indicated by these forward-looking statements. |

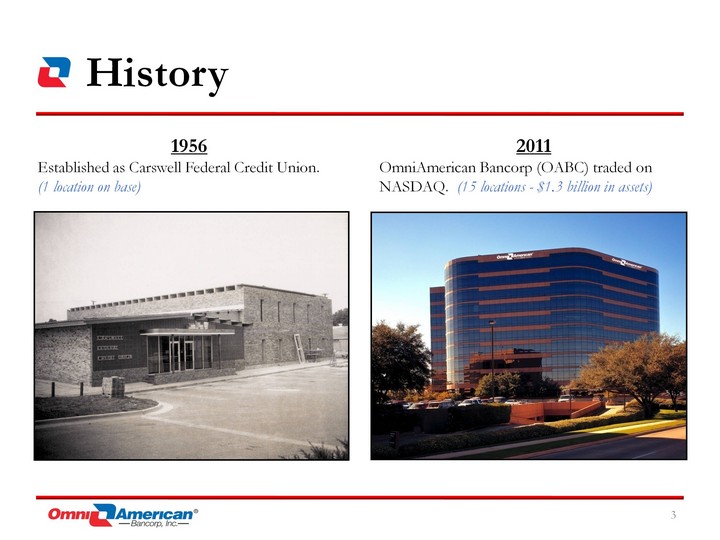

| 1956Established as Carswell Federal Credit Union. (1 location on base) 3 History 2011OmniAmerican Bancorp (OABC) traded on NASDAQ. (15 locations - $1.3 billion in assets) |

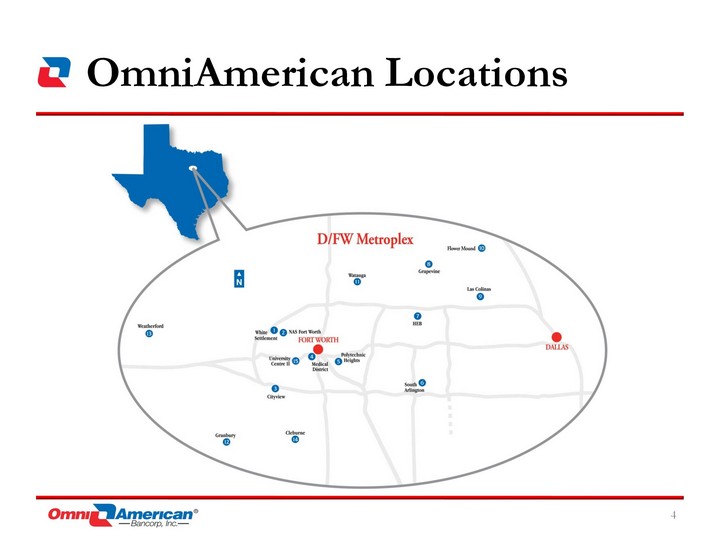

| 4 OmniAmerican Locations OmniAmerican Locations |

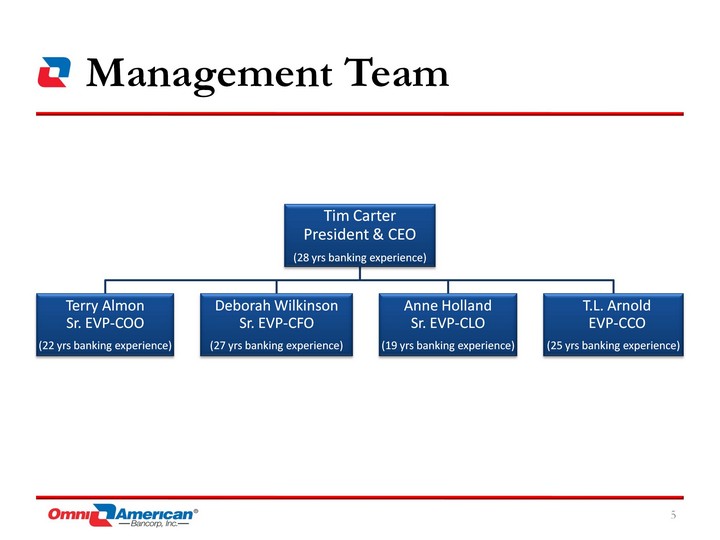

| 5 Management Team Management Team |

| 6 Strategic Plan Our GoalGrow organically through:Life-cycle marketing to our existing customer base; Develop new commercial and business lending relationships. How will we achieve this growth?By focusing on:Cross-SellingLending ServicesCustomer Convenience |

| 7 Strategic Plan How will we support our growth efforts? Commitment to electronic banking & online delivery channelsRedesign website; Improve online banking and bill payOffer online account opening for both deposit & loan productsMobile banking |

| 8 Challenges Regulatory ReformLoan DemandEfficiency RatioName Recognition |

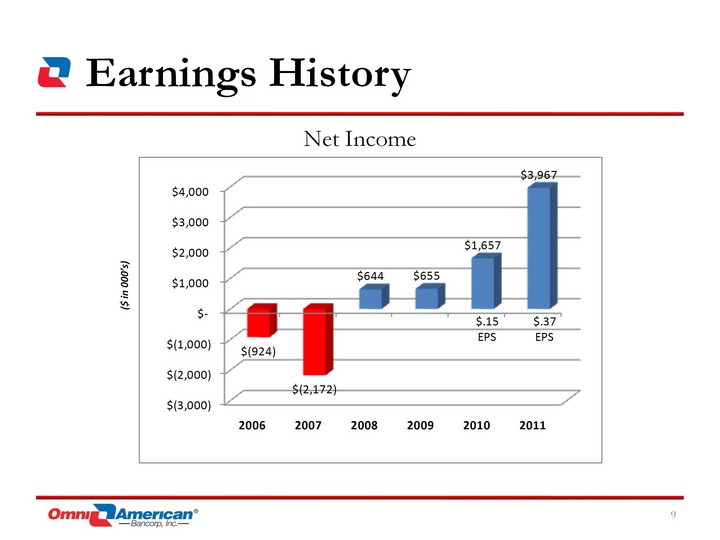

| Net Income 9 Earnings History ($ in 000's) |

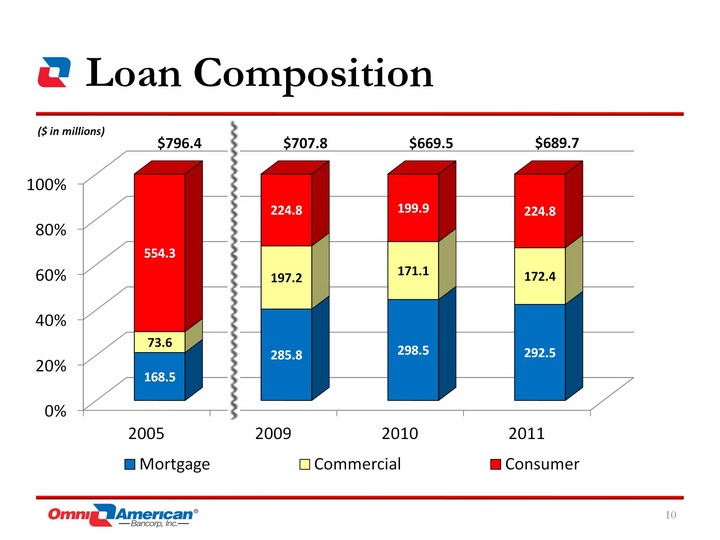

| 10 Loan Composition Loan Composition $796.4 $707.8 $669.5 $689.7 ($ in millions) |

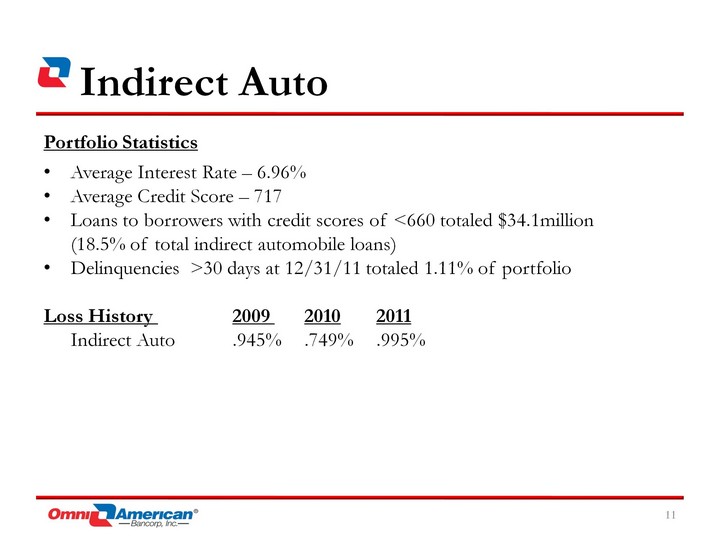

| Indirect Auto 11 Portfolio StatisticsAverage Interest Rate - 6.96%Average Credit Score - 717Loans to borrowers with credit scores of <660 totaled $34.1million (18.5% of total indirect automobile loans)Delinquencies >30 days at 12/31/11 totaled 1.11% of portfolio Loss History 2009 2010 2011 Indirect Auto .945% .749% .995% |

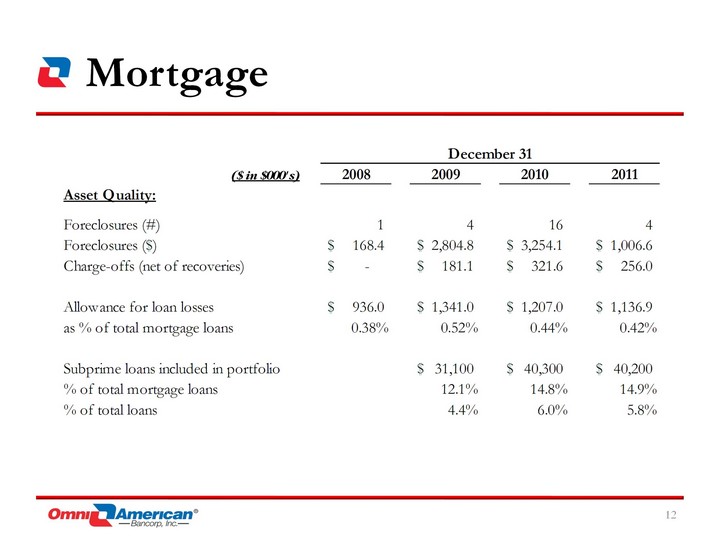

| 12 Mortgage |

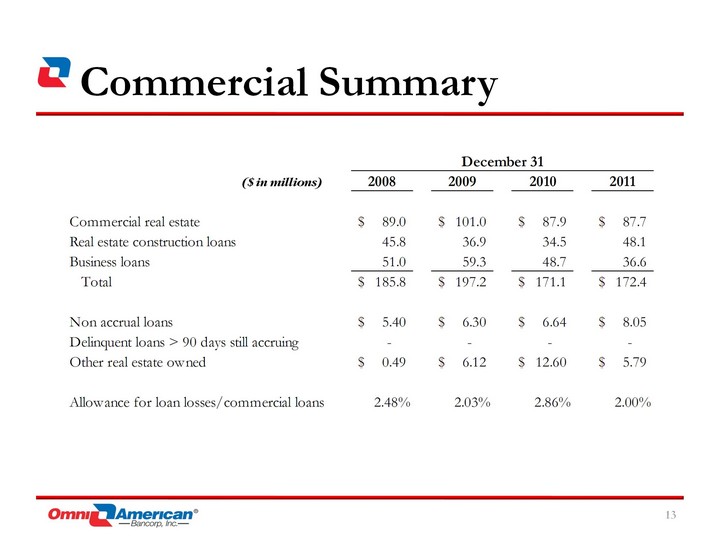

| Commercial Summary 13 |

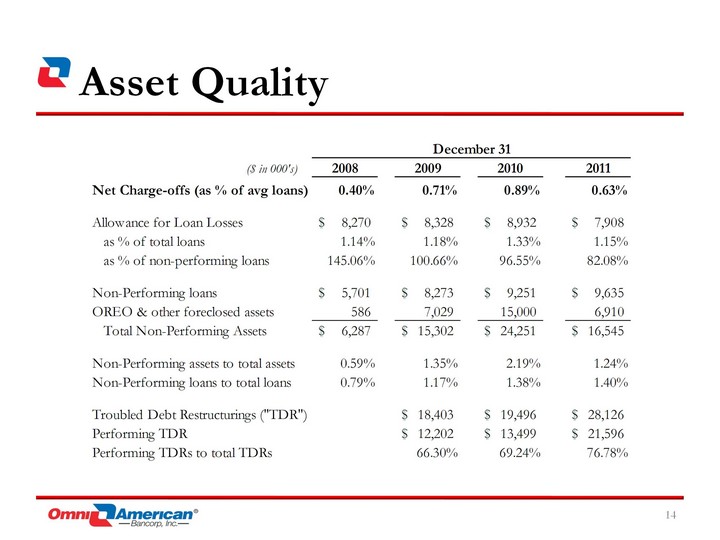

| Asset Quality 14 |

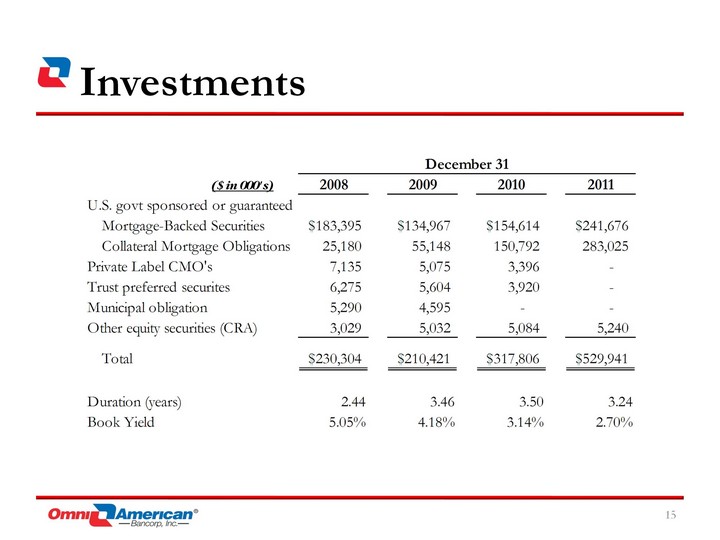

| Investments 15 |

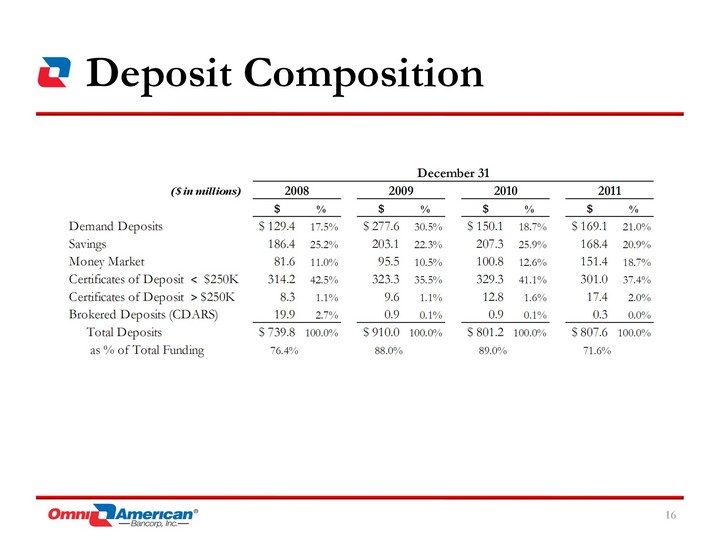

| 16 Deposit Composition |

| 17 Stock Repurchase Program 9/2/11 - Board of Directors approved a second share repurchase of up to 565,369 shares (5% of our outstanding shares on that date)The Company completed its previous 5% (595,125 share) stock repurchase program at an average cost of $14.61 per share |

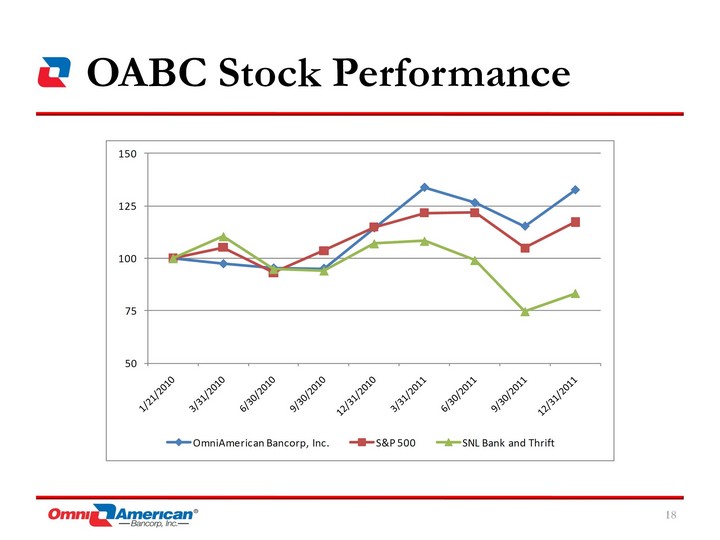

| 18 OABC Stock Performance |

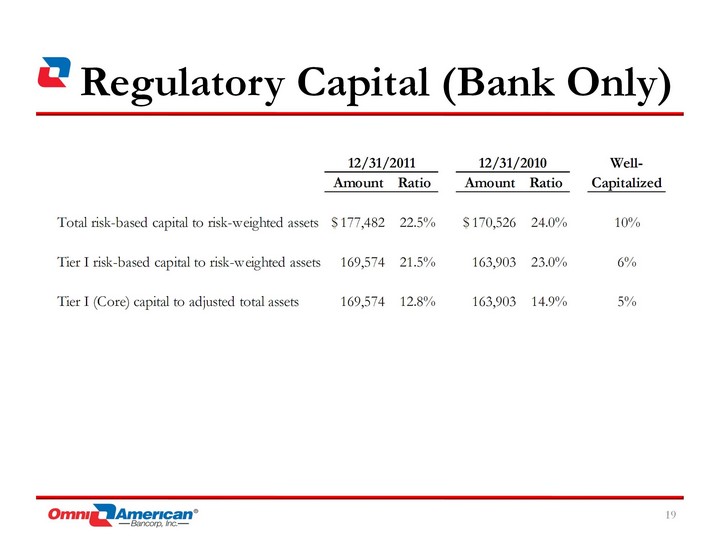

| Regulatory Capital (Bank Only) 19 |