Attached files

| file | filename |

|---|---|

| EX-32.2 - EX-32.2 - UNITED STATES LIME & MINERALS INC | a2207695zex-32_2.htm |

| EX-31.1 - EX-31.1 - UNITED STATES LIME & MINERALS INC | a2207695zex-31_1.htm |

| EX-31.2 - EX-31.2 - UNITED STATES LIME & MINERALS INC | a2207695zex-31_2.htm |

| EX-99.1 - EX-99.1 - UNITED STATES LIME & MINERALS INC | a2207695zex-99_1.htm |

| EX-23.1 - EX-23.1 - UNITED STATES LIME & MINERALS INC | a2207695zex-23_1.htm |

| EX-21.1 - EX-21.1 - UNITED STATES LIME & MINERALS INC | a2207695zex-21_1.htm |

| EX-95.1 - EX-95.1 - UNITED STATES LIME & MINERALS INC | a2207695zex-95_1.htm |

| EX-32.1 - EX-32.1 - UNITED STATES LIME & MINERALS INC | a2207695zex-32_1.htm |

| EX-23.2 - EX-23.2 - UNITED STATES LIME & MINERALS INC | a2207695zex-23_2.htm |

| EXCEL - IDEA: XBRL DOCUMENT - UNITED STATES LIME & MINERALS INC | Financial_Report.xls |

Use these links to rapidly review the document

TABLE OF CONTENTS

ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA.

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| (Mark One) | ||

ý |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the fiscal year ended December 31, 2011 |

||

OR |

||

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

Commission File Number 000-4197

United States Lime & Minerals, Inc.

(Exact name of Registrant as specified in its charter)

| Texas (State or other jurisdiction of incorporation or organization) |

75-0789226 (I.R.S. Employer Identification Number) |

|

5429 LBJ Freeway, Suite 230, Dallas, Texas (Address of principal executive offices) |

75240 (Zip code) |

(972) 991-8400

Registrant's telephone number, including area code:

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

| Title of Each Class | Name of Each Exchange on Which Registered | |

|---|---|---|

| Common Stock, $0.10 par value | The NASDAQ Stock Market LLC |

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15 (d) of the Exchange Act. Yes o No ý

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by a check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment of this Form 10-K. o

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer o | Accelerated Filer ý | Non-accelerated Filer o (Do not check if a smaller reporting company) |

Smaller Reporting Company o |

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

The aggregate market value of Common Stock held by non-affiliates computed as of the last business day of the Registrant's quarter ended June 30, 2011: $108,683,308.

Number of shares of Common Stock outstanding as of February 29, 2012: 6,241,925.

DOCUMENTS INCORPORATED BY REFERENCE

Part III incorporates information by reference from the Registrant's definitive Proxy Statement to be filed for its 2012 Annual Meeting of Shareholders. Part IV incorporates certain exhibits by reference from the Registrant's previous filings.

i

General.

United States Lime & Minerals, Inc. (the "Company," the "Registrant," "We" or "Our"), which was incorporated in 1950, conducts its business through two segments, Lime and Limestone Operations and Natural Gas Interests.

The Company's principal corporate office is located at 5429 LBJ Freeway, Suite 230, Dallas, Texas 75240. The Company's telephone number is (972) 991-8400, and its internet address is www.uslm.com. The Company's annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (the "Exchange Act"), as well as the Company's definitive proxy statement filed pursuant to Section 14(a) of the Exchange Act, are available free of charge on the Company's website as soon as reasonably practicable after the Company electronically files such material with, or furnishes it to, the Securities and Exchange Commission (the "SEC").

Lime and Limestone Operations.

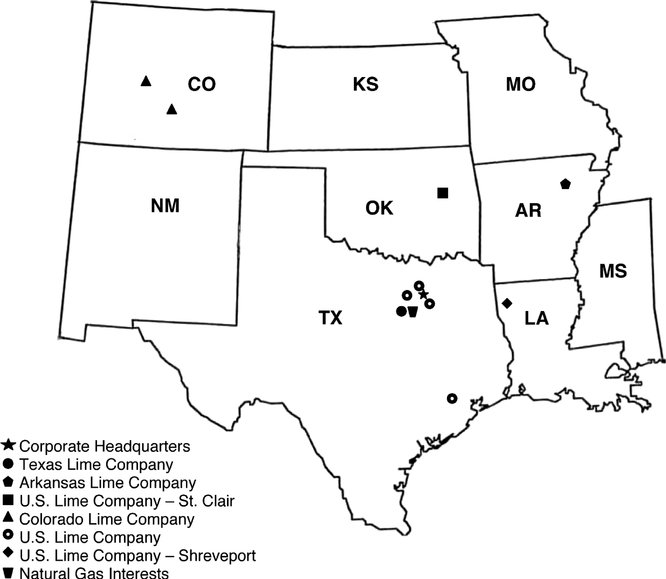

Business and Products. The Company, through its Lime and Limestone Operations, is a manufacturer of lime and limestone products, supplying primarily the construction, steel, municipal sanitation and water treatment, oil and gas services, aluminum, paper, glass, roof shingle and agriculture industries and utilities and other industries requiring scrubbing of emissions for environmental purposes. The Company is headquartered in Dallas, Texas and operates lime and limestone plants and distribution facilities in Arkansas, Colorado, Louisiana, Oklahoma and Texas through its wholly owned subsidiaries, Arkansas Lime Company, Colorado Lime Company, Texas Lime Company, U.S. Lime Company, U.S. Lime Company—Shreveport, U.S. Lime Company—St. Clair and U.S. Lime Company—Transportation.

The Company extracts high-quality limestone from its open-pit quarries and an underground mine and then processes it for sale as pulverized limestone, quicklime, hydrated lime and lime slurry. Pulverized limestone (also referred to as ground calcium carbonate) ("PLS") is a dried product ground to granular and finer sizes. Quicklime (calcium oxide) is produced by heating limestone to very high temperatures in kilns in a process called calcination. Hydrated lime (calcium hydroxide) is produced by reacting quicklime with water in a controlled process. Lime slurry (milk of lime) is a suspended solution of calcium hydroxide produced by mixing quicklime with water in a lime slaker.

PLS is used in the production of construction materials such as roof shingles and asphalt paving, as an additive to agriculture feeds, in the production of glass, as a soil enhancement, in the flue gas desulphurization process for utilities and other industries requiring scrubbing of emissions for environmental purposes and for mine safety dust in coal mining operations. Quicklime is used primarily in metal processing, in the flue gas desulphurization process, in soil stabilization for highway, road and building construction, as well as oilfield roads and drill sites, in the manufacturing of paper products and in sanitation and water treatment systems. Hydrated lime is used primarily in municipal sanitation and water treatment, in soil stabilization for highway, road and building construction, in the flue gas desulphurization process, in asphalt as an anti-stripping agent, as a conditioning agent for oil and gas drilling mud, in the production of chemicals and in the production of construction materials such as stucco, plaster and mortar. Lime slurry is used primarily in soil stabilization for highway and building construction.

Product Sales. In 2011, the Company sold almost all of its lime and limestone products in the states of Arizona, Arkansas, Colorado, Illinois, Indiana, Iowa, Kansas, Kentucky, Louisiana, Maryland,

1

Mississippi, Missouri, New Mexico, Oklahoma, Pennsylvania, Tennessee, and Texas. Sales were made primarily by the Company's nine sales employees who call on current and potential customers and solicit orders, which are generally made on a purchase-order basis. The Company also receives orders in response to bids that it prepares and submits to current and potential customers.

Principal customers for the Company's lime and limestone products are highway, street and parking lot contractors, steel producers, municipal sanitation and water treatment facilities, oil and gas services companies, paper manufacturers, utility plants, glass manufacturers, roof shingle manufacturers and poultry and cattle feed producers. During 2011, the strongest demand for the Company's lime and limestone products was from highway and road contractors, steel producers, paper manufacturers, municipal sanitation and water treatment systems, oil and gas services companies and roof shingle manufacturers.

Approximately 800 customers accounted for the Company's sales of lime and limestone products during 2011. No single customer accounted for more than 10% of such sales. The Company is generally not subject to significant customer risks as its customers are considerably diversified as to geographic location and industrial concentration. However, given the nature of the lime and limestone industry, the Company's profits are very sensitive to changes in sales volume and prices.

Lime and limestone products are transported by truck and rail to customers generally within a radius of 400 miles of each of the Company's plants. All of the Company's 2011 sales were made within the United States.

Order Backlog. The Company does not believe that backlog information accurately reflects anticipated annual revenues or profitability from year to year.

Seasonality. The Company's sales have historically reflected seasonal trends, with the largest percentage of total annual shipments and revenues being realized in the second and third quarters. Lower seasonal demand normally results in reduced shipments and revenues in the first and fourth quarters. Inclement weather conditions generally have a negative impact on the demand for lime and limestone products supplied to construction-related customers, as well as on the Company's open-pit mining operations.

Limestone Reserves. The Company's limestone reserves contain at least 96% calcium carbonate (CaCO3). The Company has two subsidiaries that extract limestone from open-pit quarries: Texas Lime Company ("Texas Lime"), which is located near Cleburne, Texas, and Arkansas Lime Company ("Arkansas Lime"), which is located near Batesville, Arkansas. U.S. Lime Company—St. Clair ("St. Clair") extracts limestone from an underground mine located near Marble City, Oklahoma. Colorado Lime Company ("Colorado Lime") owns property containing limestone deposits at Monarch Pass, located 15 miles west of Salida, Colorado. No mining has taken place on the Colorado property since its acquisition. Existing crushed stone stockpiles on the property are being used to provide feedstock to the Company's plants in Salida and Delta, Colorado. Access to all properties is provided by paved roads and, in the case of Arkansas Lime and St. Clair, also by rail.

Texas Lime operates a quarry, located on approximately 3,200 acres of land that contains known high-quality limestone reserves in a bed averaging 28 feet in thickness, with an overburden that ranges from 0 to 50 feet. Texas Lime also has mineral interests in approximately 560 acres of land adjacent to the northwest boundary of its property. The in-place reserves, as of December 31, 2011, were approximately 26 million tons of proven recoverable reserves plus approximately 91 million tons of probable recoverable reserves. Assuming the current level of production and recovery rate is maintained, the Company estimates that these reserves are sufficient to sustain operations for approximately 75 years.

2

Arkansas Lime operates two quarries and has hydrated lime and limestone production facilities on a second site linked to the quarries by its own standard-gauge railroad. The quarries cover approximately 1,050 acres of land containing a known deposit of high-quality limestone. The average thickness of the high-quality limestone deposit is approximately 60 feet, with an average overburden thickness of approximately 30 feet. The aggregate in-place reserves for the quarries, as of December 31, 2011, were approximately 20 million tons of proven recoverable reserves. During 2008 and 2009, the Company developed its newest quarry (the "South Quarry") by constructing a bridge for traffic on the highway to allow transportation of the limestone under the highway at a total cost of approximately $2.6 million. The Company also spent approximately $2.9 million in 2008 and 2009 primarily for contract development work on the South Quarry, including removal of the overburden on a portion of the reserves. Limestone production from the South Quarry began in the first quarter 2010. In 2005, the Company acquired approximately 2,500 acres of land in nearby Izard County, Arkansas. The in-place high-quality reserves on these 2,500 acres, as of December 31, 2011, were approximately 82 million tons of probable recoverable reserves. Assuming the current level of production and recovery rate is maintained, the Company estimates that its total reserves in Arkansas are sufficient to sustain operations for more than 70 years.

St. Clair, acquired by the Company in December 2005, operates an underground mine located on approximately 700 acres it owns containing high-quality limestone deposits. The in-place reserves, as of December 31, 2011, were approximately 14 million tons of probable recoverable reserves on the 700 acres. Assuming the current level of production and recovery rate is maintained, the Company estimates that the probable reserves on the 700 acres are sufficient to sustain operations for approximately 25 years. St. Clair also has the right to mine the high-quality limestone contained in approximately 1,500 adjacent acres pursuant to long-term mineral leases. Although limestone is being mined from a portion of the leased properties, the Company has not conducted a drilling program to identify and categorize reserves on the 1,500 leased acres.

Colorado Lime acquired the Monarch Pass Quarry in November 1995 and has not carried out any mining on the property. A review of the potential limestone resources has been completed by independent geologists; however, the Company has not initiated a drilling program. Consequently, it is not possible to identify and categorize reserves. The Monarch Pass Quarry, which had been operated for many years until the early 1990s, contains a mixture of limestone types, including high-quality calcium limestone and dolomite. The Company expects the remaining crushed stone stockpiles on the property to supply its plants in Salida and Delta, Colorado for at least 20 years.

Mining. The Company extracts limestone by the open-pit method at its Texas and Arkansas quarries. Monarch Pass is also an open-pit quarry, but is not being mined at this time. The open-pit method consists of removing any overburden comprising soil, trees and other substances, including inferior limestone, and then extracting the exposed high-quality limestone. Open-pit mining is generally less expensive than underground mining. The principal disadvantage of the open-pit method is that operations are subject to inclement weather and overburden removal. The limestone is extracted by drilling and blasting, utilizing standard mining equipment. At its St. Clair underground mine, the Company mines limestone using room and pillar mining. The Company has no knowledge of any recent changes in the physical quarrying or mining conditions on any of its properties that have materially affected its quarrying or mining operations, and no such changes are anticipated.

Plants and Facilities. After extraction, limestone is crushed, screened and ground in the case of PLS, or further processed in kilns, hydrators and slakers in the case of quicklime, hydrated lime and lime slurry, before shipment. The Company processes and distributes lime and/or limestone products at five plants, four lime slurry facilities and one terminal facility in Shreveport, Louisiana. All of its plants and facilities are accessible by paved roads, and in the case of Arkansas Lime, St. Clair and the Shreveport terminal, also by rail.

3

The Cleburne, Texas plant has an annual capacity of approximately 470 thousand tons of quicklime from two preheater rotary kilns. The plant also has PLS equipment, which, depending on the product mix, has the capacity to produce approximately 1.0 million tons of PLS annually.

The Arkansas plant is situated at the Batesville Quarry. Utilizing three preheater rotary kilns, this plant has an annual capacity of approximately 630 thousand tons of quicklime. Arkansas Lime's PLS and hydrating facilities are situated on a tract of 290 acres located approximately two miles from the Quarry, to which it is connected by a Company-owned, standard-gauge railroad. The PLS equipment, depending on the product mix, has the capacity to produce approximately 400 thousand tons of PLS annually.

The St. Clair plant has an annual capacity of approximately 180 thousand tons of quicklime from two rotary kilns, one of which is not a preheater kiln. The plant also has PLS equipment, which has the capacity to produce approximately 150 thousand tons of PLS annually.

The Company also maintains lime hydrating and bagging equipment at the Texas, Arkansas and Oklahoma plants. Storage facilities for lime and limestone products at each plant consist primarily of cylindrical tanks, which are considered by the Company to be adequate to protect its lime and limestone products and to provide an available supply for customers' needs at the expected volumes of shipments. Equipment is maintained at each plant to load trucks and, at the Arkansas and Oklahoma plants, to load railroad cars.

Colorado Lime operates a limestone grinding and bagging facility with an annual capacity of approximately 125 thousand tons, located on approximately three and one-half acres of land in Delta, Colorado and a limestone drying, grinding and bagging facility, with an annual capacity of approximately 50 thousand tons, on eight acres of land in Salida, Colorado. The Salida property is leased from the Union Pacific Railroad for a five-year term ending June 2014 with a five-year renewable option. A mobile stone crushing and screening plant is also situated at the Monarch Pass Quarry to produce agricultural grade limestone, with an annual capacity of approximately 40 thousand tons.

U.S. Lime Company uses quicklime to produce lime slurry and has one facility to serve the Greater Houston area construction market and three facilities to serve the Dallas-Ft. Worth Metroplex. The Company established U.S. Lime Company—Transportation primarily to deliver lime slurry produced by U.S. Lime Company to customers in the Dallas-Ft. Worth Metroplex.

U.S. Lime Company—Shreveport operates a distribution terminal in Shreveport, Louisiana, which is connected to a railroad, to provide lime storage, hydrating, slurrying and distribution capacity to service markets in Louisiana and East Texas.

The Company believes that its plants and facilities are adequately maintained and insured. See "Management's Discussion and Analysis of Financial Condition and Results of Operations—Financial Condition."

Employees. At December 31, 2011, the Company employed 301 persons, 36 of whom were engaged in administrative and management activities, and nine of whom were engaged in sales activities. Of the Company's 256 production employees, 123 are covered by two collective bargaining agreements. The agreement for the Texas facility expires in November 2014, and the agreement for the Arkansas facility expires in January 2014. The Company believes that its employee relations are good.

Competition. The lime industry is highly regionalized and competitive, with quality, price, ability to meet customer demand, proximity to customers, personal relationships and timeliness of deliveries being the prime competitive factors. The Company's competitors are predominantly private companies.

The lime industry is characterized by high barriers to entry, including: the scarcity of high-quality limestone deposits on which the required zoning and permits for extraction can be obtained; the need

4

for lime plants and facilities to be located close to markets, paved roads and railroad networks to enable cost-effective production and distribution; clean air and anti-pollution regulations, including those related to greenhouse gas emissions, which make it more difficult to obtain permitting for new sources of emissions, such as lime kilns; and the high capital cost of the plants and facilities. These considerations reinforce the premium value of operations having permitted, long-term, high-quality limestone reserves and good locations and transportation relative to markets.

Lime producers tend to be concentrated on known limestone formations where competition takes place principally on a regional basis. The industry as a whole has expanded its customer base and, while the steel industry and environmental-related users, including utility plants, are the largest market sectors, it also counts chemical users and other industrial users, including pulp and paper producers and road builders, among its major customers.

Consolidation in the lime industry has left the three largest companies accounting for more than two-thirds of North American production capacity. In addition to the consolidations, and often in conjunction with them, many lime producers have undergone modernization and expansion projects to upgrade their processing equipment in an effort to improve operating efficiency. The Company's Texas and Arkansas modernization and expansion projects, its acquisitions of the St. Clair operations in Oklahoma and the lime slurry operations in Texas, and its recent South Quarry development project in Arkansas should allow the Company to continue to remain competitive, protect its markets and position itself for the future. In addition, the Company will continue to evaluate internal and external opportunities for expansion and growth, as conditions warrant or opportunities arise. The Company may have to revise its strategy or otherwise find ways to enhance the value of the Company, including entering into strategic partnerships, mergers or other transactions.

Impact of Environmental Laws. The Company owns or controls large areas of land, upon which it operates limestone quarries, an underground mine, lime plants and other facilities with inherent environmental responsibilities and environmental compliance costs, including capital, maintenance and operating costs with respect to pollution control facilities, the cost of ongoing monitoring programs, the cost of reclamation and remediation efforts and other similar costs and liabilities.

The Company's operations are subject to various federal, state, and local laws and regulations relating to the environment, health and safety, and other regulatory matters, including the Clear Air Act, the Clean Water Act, the Resource Conservation and Recovery Act, the Comprehensive Environmental Response, Compensation, and Liability Act, and the Mine Safety and Health Act ("Environmental Laws"). These Environmental Laws grant the United States Environmental Protection Agency (the "EPA") and state governmental agencies the authority to promulgate regulations that could result in substantial expenditures on pollution control and waste management. The Company has not been named as a potentially responsible party in any federal superfund cleanup site or state-led cleanup site.

The rate of change of Environmental Laws continues to be rapid, and compliance can require significant expenditures. For example, federal legislation required the Company's plants with operating kilns to apply for Title V operating permits that have significant ongoing compliance monitoring costs. In addition to the Title V permits, other environmental operating permits are required for the Company's operations, and such permits are subject to modification during the permit renewal process, and to revocation. Raw materials and fuels used to manufacture lime products contain chemicals and compounds, such as trace metals, that may be classified as hazardous substances. In 2004, the EPA adopted new National Ambient Air Quality Standards ("NAAQS") for ozone. Pursuant to the 2004 NAAQS, in 2007 the Texas Commission on Environmental Quality (the "TCEQ") adopted regulations to limit emissions of nitrogen oxides ("NOx") from industrial operations, including lime kilns, located in the Dallas-Ft. Worth area, which resulted in substantial expenditures on pollution control measures and emissions monitoring systems. In 2008 and 2009, the Company spent a total of approximately

5

$700 thousand on these systems to be in compliance with NAAQS, to which Texas Lime became subject on March 1, 2009. In 2008, the EPA adopted an even more stringent ozone NAAQS. However, at this time, the TCEQ is not proposing additional emission reductions of NOx from lime kilns to meet the new ozone standard. In 2010, the EPA adopted new NAAQS for sulfur dioxide and nitrogen dioxide. If the Company modifies any of its lime plants, the New Source Review (discussed below) permitting process may entail modeling and, potentially, installation of additional emission controls to demonstrate compliance with those new NAAQS.

As of January 1, 2010, the EPA required large emitters of greenhouse gases, including the Company's plants, to collect and report greenhouse gas emissions data. The EPA indicated it will use the data collected through the greenhouse gas reporting rules to decide whether to promulgate future greenhouse gas emission limits. On May 13, 2010, the EPA issued a final rule "tailoring" its New Source Review permitting and Federal Operating Permit programs to apply to facilities with certain thresholds of greenhouse gas emissions. The emission rates are determined based upon the CO2 equivalent of six greenhouse gases. As of January 2, 2011, this "Tailoring Rule" required facilities that are subject to federal New Source Review for other pollutants to include greenhouse gases in their permits if greenhouse gas emissions will increase by 75,000 tons or more. In July 2011, the Tailoring Rule extended New Source Review and Federal Operating permits to such projects that exceed the emission threshold for only greenhouse gases. Thus, any new facilities or major modifications to existing facilities that exceed the federal New Source Review emission thresholds will be required to use "best available control technology" and energy efficiency measures to minimize greenhouse gas emissions.

Although the timing and impact of climate change legislation and of regulations limiting greenhouse gas emissions are uncertain, the consequences of such legislation and regulation are potentially significant for the Company because the production of carbon dioxide is inherent in the manufacture of lime through the calcination of limestone and combustion of fossil fuels. The EPA's implementation of the Tailoring Rule to New Source Review permitting could result in increased time and costs of plant upgrades and expansions. The passage of climate control legislation, and other regulatory initiatives by the Congress, states or the EPA that restrict or tax emissions of greenhouse gases, could adversely affect the Company. There is no assurance that changes in the law or regulations will not be adopted, such as the imposition of a carbon tax, a cap and trade program requiring the Company to purchase carbon credits, or other measures that would require reductions in emissions or changes to raw materials, fuel use or production rates, that could have a material adverse effect on the Company's financial condition, results of operations, cash flows and competitive position.

In the courts, several cases have been filed and decisions issued that may increase the risk of claims being filed by third parties against companies for their greenhouse gas emissions. Such cases may seek to challenge air permits to force reductions in greenhouse gas emissions or seek damages for alleged climate change impacts to the environment, people and property.

The Company incurred capital expenditures related to environmental matters of approximately $407 thousand, $787 thousand and $480 thousand in 2011, 2010 and 2009, respectively. The Company's recurring costs associated with managing and disposing of potentially hazardous substances (such as fuel and lubricants used in operations) and maintaining pollution control equipment amounted to approximately $744 thousand, $597 thousand and $715 thousand in 2011, 2010 and 2009, respectively.

The Company recognizes legal reclamation and remediation obligations associated with the retirement of long-lived assets at their fair value at the time the obligations are incurred ("Asset Retirement Obligations" or "AROs"). Over time, the liability for AROs is recorded at its present value each period through accretion expense, and the capitalized cost is amortized over the useful life of the related asset. Upon settlement of the liability, the Company either settles the ARO for its recorded amount or recognizes a gain or loss. AROs are estimated based on studies and the Company's process

6

knowledge and estimates, and are discounted using an appropriate interest rate. The AROs are adjusted when further information warrants an adjustment. The Company believes its accrual of $1.5 million for AROs at December 31, 2011 is reasonable.

Map of United States Lime & Minerals, Inc. Operations/Interests.

Natural Gas Interests.

Interests. The Company, through its wholly owned subsidiary, U.S. Lime Company—O & G, LLC ("U.S. Lime O & G"), has royalty interests ranging from 15.4% to 20% and a 20% non-operating working interest with respect to oil and gas rights on the Company's approximately 3,800 acres of land located in Johnson County, Texas, in the Barnett Shale Formation. These interests are derived from the Company's May 2004 oil and gas lease agreement (the "O & G Lease") with EOG Resources, Inc. ("EOG") with respect to oil and gas rights on its Cleburne, Texas property, that will continue so long as EOG is continuously developing, or producing natural gas from, the leased property as set forth in the O & G Lease. During the fourth quarter 2005, drilling of the first natural gas well under the O & G Lease was completed, and natural gas production began in February 2006.

7

The Company's overall average revenue interest is 34.7% in the 34 wells drilled under the O & G Lease.

In November 2006, through U.S. Lime O & G, the Company entered into a drillsite and production facility lease agreement and subsurface easement (the "Drillsite Agreement") with XTO Energy Inc. ("XTO"), which has an oil and gas lease covering approximately 538 acres of land contiguous to the Company's Johnson County, Texas property. Pursuant to the Drillsite Agreement, the Company receives a 3% royalty interest and a 12.5% working interest, resulting in a 12.4% revenue interest, in the six XTO wells drilled from two pad sites located on the Company's property.

U.S. Lime O & G has no direct employees and is not the operator of any wells drilled on the properties subject to either the O & G Lease or the Drillsite Agreement (the "O & G Properties"). The only decision that the Company makes is whether to participate as a non-operating working interest owner and pay its proportionate share of drilling, completing, recompleting, working over and operating a well.

Regulation. Many aspects of the development, production, pricing and marketing of natural gas are regulated by federal and state agencies. Legislation affecting the natural gas industry is under constant review for amendment or expansion, which frequently increases the regulatory burden on affected members of the industry.

Oil and gas development and production operations are subject to various types of regulation at the federal, state and local levels that may impact the Company's royalty and non-operating working interests. Such regulation includes:

- •

- requiring permits for the drilling of wells;

- •

- numerous federal and state safety requirements;

- •

- environmental requirements;

- •

- property taxes and severance taxes; and

- •

- specific state and federal income tax provisions.

The TCEQ has adopted regulations limiting air emissions from oil and natural gas production in the Barnett Shale, where the O & G Properties are located. The EPA has adopted greenhouse gas monitoring and reporting regulations applicable to the petroleum and natural gas industry that require persons that hold state drilling permits that will result in annual greenhouse gas emissions of 25,000 metric tons or more to report annually those emissions from certain sources. The EPA indicated that it will use data collected through the reporting rules to decide whether to promulgate future greenhouse gas emission limits. On July 28, 2011, the EPA proposed regulations that, if finalized, would establish new source performance standards for volatile organic compounds and sulfur dioxide emissions and establish an air toxic standard for oil and natural gas production, transmission, and storage activities. The proposed regulations would limit methane emissions from wells, storage tanks and other equipment, and transmission sources. The EPA expects to take final action on those rules in March or April of 2012.

Additionally, Congress, the EPA and various states have proposed or adopted legislation regulating or requiring disclosure regarding hydraulic fracturing in connection with drilling operations. Hydraulic fracturing is a technique used to produce natural gas from shale, including the Barnett Shale. Hydraulic fracturing has historically been regulated by state oil and natural gas commissions. However, the EPA recently asserted federal regulatory authority over certain hydraulic fracturing activities involving diesel under the Safe Drinking Water Act ("SDWA"). The EPA has begun the process of drafting guidance documents related to this newly asserted regulatory authority, which could include a broad definition of diesel that would cover a variety of oils that are not diesel but that have similar carbon-chain

8

molecules. The EPA also plans to investigate the treatment of wastewater from hydraulic fracturing for the purpose of setting new standards for discharges from natural gas drilling to publicly owned treatment works. In addition, certain other governmental reviews are either underway or being proposed that focus on environmental aspects of hydraulic fracturing practices, including a four-year study by the EPA expected to be completed in 2014. These on-going or proposed reviews, depending on their scope and results, could spur initiatives to further regulate hydraulic fracturing under the SDWA or other regulatory programs.

Customers and Pricing. The pricing of natural gas sales is primarily determined by supply and demand in the marketplace and can fluctuate considerably. As the Company is not the operator of the wells drilled on the O & G Properties, it has limited access to timely information, involvement and operational control over the volumes of natural gas produced and sold and the terms and conditions on which such volumes are marketed and sold, all of which is controlled by the operators. Although the Company has the right to take its portion of natural gas production in kind, it currently has elected to have its natural gas production marketed by the operators.

The prices that the Company receives for its natural gas production is also affected by the amount of natural gas liquids included in the natural gas and the prices for those liquids, which prices normally track the prices of crude oil. In recent years, the demand and prices for crude oil have increased, while the prices of natural gas have tended to decline due to increased supply.

Drilling Activity. No wells were completed as producing wells in 2009. The Company participated as a royalty interest and non-operating working interest owner in the drilling of eight gross (1.6 net) wells under the O & G Lease in the fourth quarter 2009 and first quarter 2010, five of which were completed as producing wells during the fourth quarter 2010, and three of which were completed as producing wells in late June 2011. In addition, the Company participated in the drilling and completion of two gross (0.3 net) wells during 2010 under the Drillsite Agreement. All of these wells are located in Johnson County, Texas. No new wells are currently being drilled. The Company cannot predict the number of additional wells that will be drilled, if any, or their results.

Production Activity. The number of gross and net producing wells and production activity for the years ended December 31, 2011, 2010 and 2009 are as follows:

| |

2011 | 2010 | 2009 | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

Gross | Net(2) | Gross | Net(2) | Gross | Net(2) | |||||||||||||

Producing wells(1) |

|||||||||||||||||||

O & G Lease |

34 | 6.8 | 31 | 6.2 | 26 | 5.2 | |||||||||||||

Drillsite Agreement |

6 | 0.8 | 6 | 0.8 | 4 | 0.5 | |||||||||||||

Total |

40 | 7.6 | 37 | 7.0 | 30 | 5.7 | |||||||||||||

Natural gas production volume (BCF) |

1.6 | 1.0 | 1.2 | ||||||||||||||||

Average sales price per MCF(3) |

$8.27 | $7.78 | $5.74 | ||||||||||||||||

Total cost of revenues per MCF(4) |

$2.37 | $1.89 | $1.25 |

||||||||||||||||

- (1)

- Although

a total of 34 wells have been drilled under the O & G Lease, there was no production from one well during 2011, and that well may be plugged

and abandoned in the future.

- (2)

- The

number of net wells is required to be calculated based on the Company's working interests percentages multiplied by the number of gross wells and does

not consider the Company's royalty interests percentages in each well.

- (3)

- Average

sales price per MCF includes sales prices of natural gas liquids contained in the natural gas.

- (4)

- Includes taxes other than income taxes.

Delivery Commitments. There are no delivery commitments for the Company's natural gas production to which U.S. Lime O & G is a party.

9

Internal Controls Over Reserves Estimates. The Company's policies regarding internal controls over the recording of reserve estimates require reserves to be in compliance with the SEC definitions and guidance and prepared in accordance with generally accepted petroleum engineering principles. In each of the years 2011, 2010 and 2009, the Company retained DeGolyer and MacNaughton, independent third-party petroleum engineers, to perform appraisals of 100% of its proved reserves in compliance with these standards.

Natural Gas Reserves. The following table reflects the proved developed, proved undeveloped and total proved reserves (all of the which are located in Johnson County, Texas), future estimated net revenues and standardized measure at December 31, 2011, 2010 and 2009. The reserves and future estimated net revenues are based on the reports prepared by DeGolyer and MacNaughton. Proved developed reserves included 39 (there was no production from one well during 2011, and it may be plugged and abandoned in the future), 37 and 30 producing wells at December 31, 2011, 2010 and 2009, respectively. The total number of wells ultimately drilled under the O & G Lease and the Drillsite Agreement has not yet been determined, and could be more or less than the number that could be inferred from the estimated number of wells included in proved undeveloped reserves due to, among other factors, irregularities in formations and spacing decisions made by the operators. The Company's proved reserves have not been filed with, or included in, any reports to any federal agency, other than those filed with the SEC.

| |

|

2011(2) | |

|

2010(2) | |

|

2009(2) | |

|||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

Developed | Undeveloped | Total | Developed | Undeveloped | Total | Developed | Undeveloped | Total | |||||||||||||||||||

Proved natural gas reserves (BCF) |

10.3 | 0.0 | 10.3 | 11.7 | 0.6 | 12.3 | 8.9 | 4.4 | 13.3 | |||||||||||||||||||

Proved natural gas liquids and condensate reserves (MMBBLS) |

1.5 | 0.0 | 1.5 | 1.2 | 0.0 | 1.2 | 1.2 | 0.6 | 1.8 | |||||||||||||||||||

Future estimated net revenues (in thousands) |

$ | 88,782 | $ | 0.0 | $ | 88,782 | $ | 67,684 | $ | 3,108 | $ | 70,792 | $ | 45,594 | $ | 22,558 | $ | 68,152 | ||||||||||

Standardized measure(1) (in thousands) |

$ | 29,948 | $ | 0.0 | $ | 29,948 | $ | 25,296 | $ | 1,160 | $ | 26,456 | $ | 15,816 | $ | 7,260 | $ | 23,076 | ||||||||||

- (1)

- This

present value data should not be construed as representative of fair market value, since such data is based upon projected cash flows, which do not

provide for escalation or reduction of natural gas prices or for escalation or reduction of expenses and capital costs.

- (2)

- The reserve estimates as of December 31, 2011, 2010 and 2009 utilized 12-month average pricing, as now required by accounting principles generally accepted in the United States of America, of $4.46, $4.52 and $4.04 per MCF of natural gas and $49.58, $38.71 and $23.20 per BBL of natural gas liquids, respectively. Utilizing year-end prices of natural gas and natural gas liquids as of December 31, 2011, 2010 and 2009 would have resulted in proved reserves of 10.2, 13.1 and 13.8 BCF of natural gas and 1.5, 1.3 and 1.9 MMBBLS of natural gas liquids, respectively.

Undeveloped Acreage. Since the Company is not the operator, it has limited information regarding undeveloped acreage and does not know how many acres the operators classify as undeveloped acreage, if any, or the number of wells that will ultimately be drilled under either the O & G Lease or the Drillsite Agreement.

Glossary of Certain Oil and Gas Terms. The definitions set forth below shall apply to the indicated terms as used in this Report. All volumes of natural gas referred to herein are stated at the legal pressure base of the state or area where the reserves exist and at 60 degrees Fahrenheit and in most instances are rounded to the nearest major multiple.

"BBL" means a standard barrel containing 42 United States gallons.

"BCF" means one billion cubic feet under prescribed conditions of pressure and temperature and represents a basic unit for measuring the production of natural gas.

10

"Depletion" means (i) the volume of hydrocarbons extracted from a formation over a given period of time, (ii) the rate of hydrocarbon extraction over a given period of time expressed as a percentage of the reserves existing at the beginning of such period, or (iii) the amount of cost basis at the beginning of a period attributable to the volume of hydrocarbons extracted during such period.

"Formation" means a distinct geologic interval, sometimes referred to as the strata, which has characteristics (such as permeability, porosity and hydrocarbon saturations) that distinguish it from surrounding intervals.

"Future estimated net revenues" means the result of applying current prices of oil and natural gas to future estimated production from oil and natural gas proved reserves, reduced by future estimated expenditures, based on current costs to be incurred, in developing and producing the proved reserves, excluding overhead.

"MCF" means one thousand cubic feet under prescribed conditions of pressure and temperature and represents a basic unit for measuring the production of natural gas.

"MMBBLS" means one million BBLS.

"Operator" means the individual or company responsible for the exploration, development and production of an oil or natural gas well or lease.

"Proved oil and gas reserves"—Proved oil and gas reserves are those quantities of oil and gas, which, by analysis of geoscience and engineering data, can be estimated with reasonable certainty to be economically producible from a given date forward, from known reservoirs, and under existing economic conditions, operating methods, and government regulations, prior to the time at which contracts providing the right to operate expire, unless evidence indicates that renewal is reasonably certain, regardless of whether deterministic or probabilistic methods are used for the estimation. The project to extract the hydrocarbons must have commenced or the operator must be reasonably certain that it will commence the project within a reasonable time.

- (i)

- The

area of the reservoir considered as proved includes: (A) The area identified by drilling and limited by fluid contacts, if any, and

(B) Adjacent undrilled portions of the reservoir that can, with reasonable certainty, be judged to be continuous with it and to contain economically producible oil or gas on the basis of

available geoscience and engineering data.

- (ii)

- In

the absence of data on fluid contacts, proved quantities in a reservoir are limited by the lowest known hydrocarbons as seen in a well penetration

unless geoscience, engineering, or performance data and reliable technology establishes a lower contact with reasonable certainty.

- (iii)

- Where

direct observation from well penetrations has defined a highest known oil elevation and the potential exists for an associated gas cap, proved oil

reserves may be assigned in the structurally higher portions of the reservoir only if geoscience, engineering, or performance data and reliable technology establish the higher contact with reasonable

certainty.

- (iv)

- Reserves that can be produced economically through application of improved recovery techniques (including, but not limited to, fluid injection) are included in the proved classification when: (A) Successful testing by a pilot project in an area of the reservoir with properties no more favorable than in the reservoir as a whole, the operation of an installed program in the reservoir or an analogous reservoir, or other evidence using reliable technology establishes the reasonable certainty of the engineering analysis on which the project or program was based; and (B) The project has been approved for development by all necessary parties and entities, including governmental entities.

11

- (v)

- Existing economic conditions include prices and costs at which economic producibility from a reservoir is to be determined. The price shall be the average price during the 12-month period prior to the ending date of the period covered by the report, determined as an unweighted arithmetic average of the first-day-of-the-month price for each month within such period, unless prices are defined by contractual arrangements, excluding escalations based upon future conditions.

"Royalty" means an interest in an oil and gas lease that gives the owner of the interest the right to receive a portion of the production from the leased acreage (or of the proceeds of the sale thereof), but generally does not require the owner to pay any portion of the costs of drilling or operating the wells on the leased acreage.

"Severance tax" means an amount of tax, surcharge or levy recovered by governmental agencies from the gross proceeds of oil and natural gas sales. Severance tax may be determined as a percentage of proceeds or as a specific amount per volumetric unit of sales. Severance tax is usually withheld from the gross proceeds of oil and natural gas sales by the first purchaser (e.g., pipeline or refinery) of production.

"Standardized measure of discounted future net cash flows" (also referred to as "standardized measure") means the value of future estimated net revenues, calculated in accordance with SEC guidelines, to be generated from the production of proved reserves net of estimated production and future development costs, using prices and costs at the date of estimation without future escalation, and estimated income taxes without giving effect to non-property related expenses such as general and administrative expenses, debt service and depreciation, depletion and amortization, and discounted using an annual discount rate of 10%.

"Undeveloped acreage" means acreage on which wells have not been drilled or completed to a point that would permit the production of commercial quantities of oil and natural gas regardless of whether such acreage contains proved reserves.

"Working interest" means a real property interest entitling the owner to receive a specified percentage of the proceeds of the sale of oil and natural gas production or a percentage of the production, but requires the owner of the working interest to bear the cost to explore for, develop and produce such oil and natural gas.

General.

Both of our business segments continue to be adversely impacted by difficult economic conditions in the U.S.

The continuing difficult economic conditions in the United States have reduced demand for our lime and limestone products and our natural gas. Our two current largest lime customer industries, the construction and steel industries, have reduced their purchase volumes due to the ongoing difficult economic conditions. The reduced demand for natural gas has also resulted in significantly decreased natural gas prices in recent years while the prices for natural gas liquids have increased.

For us to maintain or increase our profitability, we must maintain or increase our revenues and improve cash flows and continue to control our operational and selling, general and administrative expenses. If we are unable to maintain our revenues and control our costs in these difficult economic times, our financial condition, results of operations, cash flows and competitive position could be materially adversely affected.

12

The ongoing global financial uncertainties may adversely impact our financial condition and results of operations in various ways.

The recent financial crisis and ongoing uncertainties in the global financial markets may adversely impact our financial condition and results of operations in various ways, and we may face increased challenges if the current difficult economic conditions do not improve. While the severe difficulties in the credit markets and increased volatility in the equity markets have abated to some degree, the global recession and unprecedented calls for governmental intervention continue. If the current economic conditions do not improve, it is possible that our customers and counterparties may face financial difficulties that could lead them to default on their obligations to us or seek bankruptcy protection.

We may be adversely affected by any disruption in, or failure of, our information technology systems.

We rely upon the capacity, reliability and security of our information technology ("IT") systems for our manufacturing, financial and administrative functions. We also face the challenge of supporting our IT systems and implementing upgrades when necessary. Our IT systems security measures are focused on the prevention, detection and remediation of damage from computer viruses, natural disasters, unauthorized access, cyber attack and other similar disruptions. However, our IT systems may remain vulnerable to damage despite our implementation of security measures that we feel protect our IT systems. Any failure, accident or security breach involving our IT systems could result in disruption to our operations. A material breach in the security of our IT systems could negatively impact our manufacturing operations or financial and administrative functions, or result in the compromise of personal information of our employees, customers or suppliers. To the extent any that any such failure, accident or security breach results in disruption to our operations, loss or disclosure of, or damage to, our data or confidential information, our reputation, business, results of operations and financial condition could be materially adversely affected.

Lime and Limestone Operations.

In the normal course of our Lime and Limestone Operations, we face various business and financial risks that could have a material adverse effect on our financial position, results of operations, cash flows and competitive position. Not all risks are foreseeable or within our ability to control.

These risks arise from factors including, but not limited to, fluctuating demand for our lime and limestone products, including as a result of downturns in the economy and construction, housing and steel industries, changes in legislation and regulations, including Environmental Laws, health and safety regulations and requirements to renew or obtain operating permits, our ability to produce and store quantities of lime and limestone products sufficient in amount and quality to meet customer demands, the success of our modernization, expansion and growth strategies, including our ability to sell our increased lime capacity at acceptable prices, our ability to execute our strategies and complete projects on time and within budget, our ability to integrate, refurbish and/or improve acquired facilities, our access to capital, increasing costs, especially fuel, electricity, transportation and freight costs, inclement weather and the effects of seasonal trends.

We receive a portion of our coal and petroleum coke by rail, so the availability of sufficient solid fuels to run our plants could be diminished significantly in the event of major rail disruptions. Domestic coal and petroleum coke are also being exported, increasing competition and prices for the domestic supply. In addition, our freight costs to deliver our lime and limestone products are high relative to the value of our products and have increased significantly in recent years. If we are unable to continue to pass along our increasing fuel, electricity, transportation and freight costs to our customers, our financial condition, results of operations, cash flows and competitive position could be materially adversely affected.

13

Our mining and other operations are subject to operating risks that are beyond our control, which could result in materially increased operating expenses and decreased production and shipment levels that could materially adversely affect our Lime and Limestone Operations and their profitability.

We mine limestone in open pit and underground mining operations and process and distribute that limestone through our plants and other facilities. Certain factors beyond our control could disrupt our operations, adversely affect production and shipments and increase our operating costs, all of which could have a material adverse effect on our results of operations, including geological formation problems that may cause poor mining conditions, an accident or other major incident at a site that may cause all or part of our operations to cease for some period of time and increase our expenses, mining, processing and plant equipment failures and unexpected maintenance problems that may cause disruptions and added expenses, and adverse weather and natural disasters, such as heavy rains, flooding, ice storms, drought and other natural events, that may affect operations, transportation or customers.

If any of these conditions or events occurs, our operations may be disrupted, we could experience a delay or halt of production or shipments, our operating costs could increase significantly and we could be exposed to fines, penalties, assessments and other liabilities. If our insurance coverage is limited or excludes certain of these conditions or events, we may not be able to recover any of the losses we may incur as a result of such conditions or events, some of which may be substantial.

We incur environmental compliance costs, including capital, maintenance and operating costs, with respect to pollution control equipment, the cost of ongoing monitoring programs, the cost of reclamation and remediation efforts and other similar costs and liabilities relating to our compliance with Environmental Laws, and we expect these costs and liabilities to continue to increase, including possible new costs, taxes and limitations on operations such as those related to possible climate change initiatives, including regulation of greenhouse gas emissions.

The rate of change of Environmental Laws has been rapid over the last decade, and we may face possible new costs, taxes and limitations on operations, including those related to climate change initiatives. We believe our expenditure requirements for future environmental compliance, including complying with the new nitrogen dioxide, sulfur dioxide and ozone emission limitations under the NAAQS and regulation of greenhouse gas emissions, will continue to increase as operational, reporting and other environmental standards increase. Discovery of currently unknown conditions and unforeseen liabilities could require additional expenditures.

The regulation of greenhouse gas emissions remains an issue for the Company and other similar manufacturing companies. There is no assurance that changes in the law or regulations will not be adopted, such as the imposition of a carbon tax, a cap and trade program requiring the Company to purchase carbon credits, or other measures that would require reductions in emissions or changes to raw materials, fuel use or production rates, that could have a material adverse effect on the Company's financial condition, results of operations, cash flows and competitive position.

We intend to comply with all Environmental Laws and believe our accrual for environmental liabilities at December 31, 2011 is reasonable. Because many of the requirements are subjective and therefore not quantifiable or presently determinable, or may be affected by additional legislation and rulemaking, including those related to climate change and greenhouse gas emissions, there is no assurance that we will be able to continue to renew our operating permits, and it is not possible to accurately predict the aggregate future costs and liabilities of environmental compliance and their effect on our financial condition, results of operations, cash flows and competitive position.

14

We quote on a delivered price basis to certain customers, which requires us to estimate future delivery costs. Our actual delivery costs may exceed these estimates, which would reduce our profitability.

Delivery costs are impacted by the price of diesel. Should diesel prices increase, we incur additional fuel surcharges from freight companies that cannot be passed on to our customers that have been quoted a delivered price. A material increase in the price of diesel could have a material adverse effect on the Company's profitability.

To maintain our competitive position, we may need to continue to expand our operations and production capacity, obtain financing for any such expansion at reasonable interest rates and acceptable terms and sell the resulting increased production at acceptable prices.

We may undertake various capital projects and acquisitions. These may require that we incur additional debt, which may not be available to us at all or at reasonable interest rates or on acceptable terms. Given current and projected demand for lime and limestone products, we cannot guarantee that any such project or acquisition would be successful, that we would be able to sell any resulting increased production at acceptable prices or that any such sales would be profitable.

Although prices for our lime and limestone products have been relatively strong in recent years, we are unable to predict future demand and prices, especially given the continuing economic difficulties, and cannot provide any assurance that current levels of demand and prices will continue or that any future increases in demand or price can be maintained.

The lime industry is highly regionalized and competitive.

Our competitors are predominately large private companies. The primary competitive factors in the lime industry are quality, price, ability to meet customer demand, proximity to customers, personal relationships and timeliness of deliveries, with varying emphasis on these factors depending upon the specific product application. To the extent that one or more of our competitors becomes more successful with respect to any key competitive factor, our financial condition, results of operations, cash flows and competitive position could be materially adversely affected.

Natural Gas Interests.

Historically, the markets for natural gas have been volatile and may continue to be volatile in the future.

Various factors that are beyond our control will affect the demand for and prices of natural gas, such as:

- •

- the worldwide and domestic supplies of natural gas;

- •

- the development of new technologies and reserves of natural gas in the United States;

- •

- the price and level of foreign imports;

- •

- the level of consumer and industrial demand;

- •

- the price and availability of alternative fuels;

- •

- the availability of pipeline capacity;

- •

- weather conditions;

- •

- domestic and foreign governmental regulations and taxes; and

- •

- the overall economic environment.

The natural gas industry is cyclical in nature and tends to reflect general economic conditions. The recent global recession and mild winters in most of the U.S. have led to significant reductions in

15

demand and pricing for our natural gas production, beginning in the second half 2008 and continuing into 2012. In addition, recent technological advances, enabling the industry to access additional reserves, have greatly increased the current supply of natural gas in the United States. Lower natural gas prices may reduce the amount of natural gas that is economical for our operators to develop and produce on the O & G Properties or to shut in wells for extended periods of time. Reduced prices and production could severely reduce our revenues, gross profit and cash flows from our Natural Gas Interests and thus could have a material adverse effect on our financial condition, results of operations and cash flows.

We do not control development and production operations on the O & G Properties, which could impact our Natural Gas Interests.

As the owner of royalty and non-operating working interests, our ability to influence development of, and production from, the O & G Properties is severely limited. All decisions related to development and production on the O & G Properties will be made by the operators and may be influenced by factors beyond our control, including but not limited to natural gas prices, interest rates, budgetary considerations and general industry and economic conditions.

The occurrence of an operational risk or uncertainty that materially impacts the operations of the operators of the O & G Properties could have a material adverse effect on the amount we receive in connection with our interests in production from our O & G Properties, which could have a material adverse effect on our financial condition, results of operations and cash flows.

Our natural gas income is affected by development, production and other costs, some of which are outside of our control, and possible unitizations.

The natural gas income that comes from our working interests, and to a lesser extent our royalty interests, is directly affected by increases in development, production and other costs, as well as unitizations of existing wells. Some of these costs are outside our control, including drilling and production costs, costs of regulatory compliance and severance and other similar taxes. Other expenditures are dictated by business necessity, such as drilling additional wells or working over existing wells to increase recovery rates.

Our natural gas reserves are depleting assets, and we have no ability to explore for new reserves. In addition, our ability to increase our proved developed reserves is limited to the drilling of potential additional wells and reworking of existing wells by the operators on the O & G Properties.

Our revenues from our Natural Gas Interests depend in large part on the quantity of natural gas developed and produced from the O & G Properties. Our producing wells will experience declines in production rates due to depletion of their natural gas reserves, and the operators may determine to temporarily shut in or totally abandon a producing well if they believe that it is then no longer economical to continue production from the well. We have no ability to explore for new reserves. Any increases in our proved developed reserves will come from the operators drilling additional wells or working over existing wells on the O & G Properties. The timing and number of such additional or reworked wells, if any, depend on the market prices of natural gas and on other factors beyond our control.

Drilling activities on the O & G Properties may not be productive, which could have an adverse effect on our financial condition, results of operations and cash flows.

Drilling involves a wide variety of risks, including the risk that no commercially productive natural gas reservoirs will be encountered. The cost of drilling, completing, recompleting, working over and

16

operating wells is often uncertain, and drilling operations may be delayed or canceled as a result of a variety of factors, including:

- •

- Pressure or irregularities in formations;

- •

- Equipment failures or accidents;

- •

- Unexpected drilling conditions;

- •

- Shortages or delays in the delivery of equipment; and

- •

- Adverse weather conditions.

Future drilling activities, if any, recompletions or workovers on the O & G Properties may not be successful. If these activities are unsuccessful, this failure could have an adverse effect on our financial condition, results of operations and cash flows.

A natural disaster, accident or catastrophe could damage pipelines, gathering systems and other facilities that service wells on the O & G Properties, which could substantially limit operations and adversely affect our financial condition, results of operations, and cash flows.

If pipelines, gathering systems or other facilities that serve our O & G Properties are damaged by any natural disaster, accident, catastrophe or other event, revenues from our Natural Gas Interests could be significantly interrupted. Any event that interrupts the development, production, gathering or transportation of our natural gas, or which causes us to share in significant expenditures not covered by insurance, could adversely impact our gross profit from our Natural Gas Interests. We do not carry business interruption insurance on our Natural Gas Interests.

The O & G Properties are geographically concentrated, which could cause net proceeds to be impacted by regional events, including natural disasters and reduced pipeline capacity resulting from production from other wells in the area.

The O & G Properties are all natural gas properties located exclusively in the Barnett Shale Formation. Because of this geographic concentration, any regional events, including natural disasters and production from other wells in the area, that increase costs, reduce availability of equipment, supplies or pipeline capacity, reduce demand or limit production may impact our gross profit from our Natural Gas Interests more than if the Properties were more geographically diversified.

The number of prospective natural gas purchasers and methods of delivery for our gas are also considerably less than would otherwise exist from a more geographically diverse group of interests.

Governmental policies, laws and regulations could have an adverse impact on our O & G Properties and natural gas business.

The O & G Properties and our natural gas business are subject to federal, state and local laws and regulations relating to the oil and natural gas industry, as well as regulations relating to safety matters. These laws and regulations can have a significant impact on production and costs of development and production.

Environmental costs and liabilities and changing environmental regulation associated with our O & G Properties could adversely affect our financial condition, results of operations and cash flows.

As with other companies engaged in the ownership, development and production of natural gas, we always expect to have some risk of exposure to environmental costs and liabilities. The costs associated with environmental compliance or remediation could reduce the gross profits we would receive from our Natural Gas Interests. The O & G Properties are subject to extensive federal, state and local regulatory requirements relating to environmental affairs, health and safety and waste management.

17

Increased regulation of natural gas production could increase development and production costs on our O & G Properties and adversely affect our cash flows. Third parties could also pursue legal actions to enforce compliance or assert claims for damages. Further, under certain environmental laws and regulations, the operators of the underlying properties could also be subject to joint and several, strict liability for the removal or remediation of released materials or property contamination from drilling, including hydraulic fracturing, or waste disposal, regardless of whether the operators were responsible for the release or contamination or if the operations were in compliance with all applicable laws. Drought conditions and increasing demands on the water supply for municipal, agricultural, and other uses may limit the availability of and/or increase the cost of large volumes of water required for hydraulic fracturing.

It is likely that our expenditures in connection with environmental matters, as part of normal capital expenditure programs, will affect the profitability of our O & G Properties. Future Environmental Law developments, such as stricter laws, regulations or enforcement policies, including climate change legislation mandating specific near-term and long-range reductions in greenhouse gas emissions or increased regulation of hydraulic fracturing could significantly increase the costs of production from the O & G Properties and adversely affect our financial condition, results of operations and cash flows.

ITEM 1B. UNRESOLVED STAFF COMMENTS.

None

Reference is made to Item 1 of this Report for a description of the properties of the Company, and such description is hereby incorporated by reference in answer to this Item 2. As disclosed in Note 3 of Notes to Consolidated Financial Statements, the Company's plants and facilities and reserves are subject to encumbrances to secure the Company's loans.

Information regarding legal proceedings is set forth in Note 8 of Notes to Consolidated Financial Statements and is hereby incorporated by reference in answer to this Item 3.

ITEM 4. MINE SAFETY DISCLOSURES.

Under Section 1503(a) of the Dodd-Frank Wall Street Reform and Consumer Protection Act and Item 104 of Resulation S-K, each operator of a coal or other mine is required to include disclosures regarding certain mine safety results in its periodic reports filed with the SEC. The operation of the Company's quarries, underground mine and plants is subject to regulation by the federal Mine Safety and Health Administration ("MSHA") under the Federal Mine Safety and Health Act of 1977. The information required under Section 1503(a) regarding certain mining safety and health matters, broken down by mining complex, for the year ended December 31, 2011 is presented in Exhibit 95.1 to this Report.

The Company believes it is responsible to employees to provide a safe and healthy workplace environment. The Company seeks to accomplish this by: training employees in safe work practices; openly communicating with employees; following safety standards and establishing and improving safe work practices; involving employees in safety processes; and recording, reporting and investigating accidents, incidents and losses to avoid reoccurrence.

Following passage of The Mine Improvement and New Emergency Response Act of 2006, MSHA significantly increased the enforcement of mining safety and health standards on all aspects of mining operations. There has also been an increase in the dollar penalties assessed for citations and orders issued in recent years.

18

ITEM 5. MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES.

The Company's Common Stock is listed on the Nasdaq Global Market® under the symbol "USLM." As of February 29, 2012, the Company had approximately 400 shareholders of record. The Company did not pay any dividends during 2011 or 2010 and does not plan on paying dividends in 2012.

As of February 29, 2012, the Company had 500,000 shares of $5.00 par value preferred stock authorized; however, none has been issued.

The low and high sales prices for the Company's Common Stock for the periods indicated were:

| |

2011 | 2010 | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

Low | High | Low | High | |||||||||

First Quarter |

$ | 37.30 | $ | 44.00 | $ | 33.94 | $ | 41.18 | |||||

Second Quarter |

$ | 37.02 | $ | 42.25 | $ | 35.12 | $ | 41.92 | |||||

Third Quarter |

$ | 38.25 | $ | 43.00 | $ | 35.65 | $ | 42.83 | |||||

Fourth Quarter |

$ | 37.31 | $ | 60.60 | $ | 37.82 | $ | 42.19 | |||||

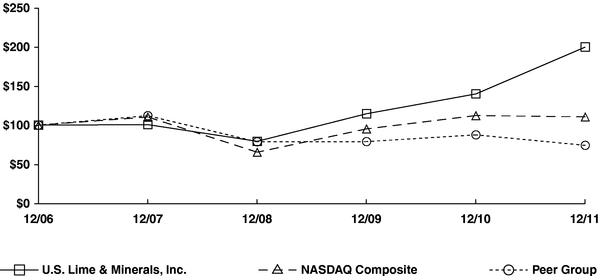

The graph below compares the cumulative five-year total shareholders' return on the Company's Common Stock with the cumulative total return on The NASDAQ Composite Index and a peer group index consisting of Eagle Materials, Inc., Monarch Cement Co., U.S. Concrete, Inc. and Martin Marietta Materials, Inc. The graph assumes that the value of the investment in the Company's Common Stock and each index was $100 on December 31, 2006, and that all dividends have been reinvested.

COMPARISON OF 5 YEAR CUMULATIVE TOTAL RETURN

Among U.S. Lime & Minerals, Inc., the NASDAQ Composite Index, and a Peer Group

| |

2006 | 2007 | 2008 | 2009 | 2010 | 2011 | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

U.S. LIME & MINERALS, INC. |

100.00 | 100.66 | 79.44 | 114.53 | 139.73 | 199.37 | |||||||||||||

NASDAQ COMPOSITE INDEX |

100.00 | 110.38 | 65.58 | 95.27 | 112.22 | 110.58 | |||||||||||||

PEER GROUP INDEX |

100.00 | 112.02 | 78.78 | 79.05 | 87.63 | 74.30 | |||||||||||||

19

ISSUER PURCHASES OF EQUITY SECURITIES

The Company's Amended and Restated 2001 Long-Term Incentive Plan allows employees and directors to pay the exercise price upon the exercise of stock options and the tax withholding liability upon the lapse of restrictions on restricted stock by payment in cash and/or delivery of shares of the Company's Common Stock to the Company. In the fourth quarter 2011, pursuant to these provisions, the Company received a total of 1,124 shares of its Common Stock for payment of tax withholding liability upon the lapse of restrictions on restricted stock and 9,604 shares of its Common Stock in payment to exercise stock options. The 1,124 and 9,604 shares were valued at $59.50 and $55.00 per share, respectively, the fair market value of one share of the Company's Common Stock on the date that they were tendered to the Company.

ITEM 6. SELECTED FINANCIAL DATA.

| |

Years Ended December 31, | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2011 | 2010 | 2009 | 2008 | 2007 | |||||||||||

| |

(Dollars in thousands, except per share amounts) |

|||||||||||||||

Operating results |

||||||||||||||||

Lime and limestone revenues |

$ | 129,704 | 125,169 | 110,406 | 126,165 | 116,569 | ||||||||||

Natural gas revenues |

12,878 | 7,425 | 6,925 | 16,191 | 8,667 | |||||||||||

Total revenues |

$ | 142,582 | 132,594 | 117,331 | 142,356 | 125,236 | ||||||||||

Gross profit |

$ | 41,349 | 36,041 | 28,753 | 31,283 | 26,016 | ||||||||||

Operating profit |

$ | 32,503 | 27,665 | 20,955 | 23,317 | 18,372 | ||||||||||

Income before income taxes |

$ | 30,144 | 25,058 | 18,144 | 19,411 | 14,339 | ||||||||||

Net income |

$ | 22,186 | 18,040 | 13,670 | 14,433 | 10,446 | ||||||||||

Net income per share of common stock: |

||||||||||||||||

Basic |

$ | 3.50 | 2.82 | 2.14 | 2.29 | 1.67 | ||||||||||

Diluted |

$ | 3.49 | 2.81 | 2.14 | 2.27 | 1.65 | ||||||||||

| |

As of December 31, | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2011 | 2010 | 2009 | 2008 | 2007 | |||||||||||

Total assets |

$ | 202,558 | 188,498 | 172,070 | 166,129 | 158,227 | ||||||||||

Long-term debt, excluding current installments |

$ | 26,667 | 31,666 | 36,666 | 46,354 | 54,037 | ||||||||||

Stockholders' equity per outstanding common share |

$ | 22.94 | 20.01 | 17.20 | 14.87 | 12.94 | ||||||||||

Employees |

301 | 295 | 285 | 307 | 318 | |||||||||||

ITEM 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATION.