Attached files

| file | filename |

|---|---|

| EX-3.5 - FORM OF CERTIFICATE - Demandware Inc | d199710dex35.htm |

| EX-23.1 - CONSENT OF DELOITTE & TOUCHE LLP - Demandware Inc | d199710dex231.htm |

| EX-10.17 - INDEMNIFICATION AGREEMENT - Demandware Inc | d199710dex1017.htm |

| EX-10.23 - 2012 EXECUTIVE INCENTIVE COMPENSATION PROGRAM - Demandware Inc | d199710dex1023.htm |

| EX-5.1 - OPINION OF WILMER CUTLER PICKERING HALE AND DORR LLP - Demandware Inc | d199710dex51.htm |

Table of Contents

As filed with the Securities and Exchange Commission on March 1, 2012

Registration No. 333-175595

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 6

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

DEMANDWARE, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 7372 | 20-0982939 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

5 Wall Street

Burlington, Massachusetts 01803

(888) 553-9216

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Thomas D. Ebling

President and Chief Executive Officer

Demandware, Inc.

5 Wall Street

Burlington, Massachusetts 01803

(888) 553-9216

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Mark G. Borden, Esq. Wilmer Cutler Pickering Hale and Dorr LLP 60 State Street Boston, Massachusetts 02109 Telephone: (617) 526-6000 Telecopy: (617) 526-5000 |

William J. Schnoor, Esq. Christopher J. Austin, Esq. Goodwin Procter LLP Exchange Place 53 State Street Boston, Massachusetts 02109 Telephone: (617) 570-1000 Telecopy: (617) 523-1231 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement is declared effective.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | þ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities To Be Registered |

Amount To Be Registered(1) |

Estimated Maximum Offering Price Per Share(2) |

Estimated Maximum Aggregate Offering Price(2) |

Amount of Registration Fee(3)(4) |

||||||||||||

| Common Stock, $0.01 par value per share |

6,325,000 | $ | 14.50 | $ | 91,712,500 | $ | 10,511 | |||||||||

| (1) | Includes 825,000 shares of common stock the underwriters have the option to purchase. |

| (2) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(a) under the Securities Act of 1933, as amended. |

| (3) | Calculated pursuant to Rule 457(a) based on a bona fide estimate of the maximum aggregate offering price. |

| (4) | A registration fee of $11,610 was previously paid in connection with the Registration Statement. Accordingly, no additional registration fee is due. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

PRELIMINARY PROSPECTUS

Subject to Completion. Dated March 1, 2012.

5,500,000 SHARES

DEMANDWARE, INC.

Common Stock

This is the initial public offering of Demandware, Inc. We are offering 5,500,000 shares of our common stock. Prior to this offering, there has been no public market for our common stock. We anticipate that the initial public offering price will be between $12.50 and $14.50 per share.

Our common stock has been approved for listing on the New York Stock Exchange under the symbol “DWRE”.

See “Risk Factors” beginning on page 9 to read about factors you should consider before buying shares of our common stock.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

| Per Share | Total | |||||||

| Initial Public Offering Price |

$ | $ | ||||||

| Underwriting Discount |

$ | $ | ||||||

| Proceeds, before expenses, to Demandware, Inc. |

$ | $ | ||||||

To the extent that the underwriters sell more than 5,500,000 shares of common stock, the underwriters have the option to purchase from us up to an additional 825,000 shares at the initial public offering price less the underwriting discount.

The underwriters expect to deliver the shares against payment in New York, New York on or about , 2012.

| Goldman, Sachs & Co. |

Deutsche Bank Securities |

| William Blair & Company | Oppenheimer & Co. | Canaccord Genuity |

First Analysis Securities Corp.

Prospectus dated , 2012.

Table of Contents

Table of Contents

| Page | ||||

| 1 | ||||

| 9 | ||||

| 29 | ||||

| 30 | ||||

| 31 | ||||

| 31 | ||||

| 32 | ||||

| 34 | ||||

| 36 | ||||

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

37 | |||

| 65 | ||||

| 80 | ||||

| 87 | ||||

| 111 | ||||

| 115 | ||||

| 118 | ||||

| 121 | ||||

| Material U.S. Tax Considerations for Non-U.S. Holders of Common Stock |

124 | |||

| 128 | ||||

| 132 | ||||

| 132 | ||||

| 132 | ||||

| F-1 | ||||

We have not authorized anyone to provide any information or to make any representations other than those contained in this prospectus or in any free writing prospectuses we have prepared. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus is current only as of its date regardless of the time of delivery of this prospectus or of any sale of our common stock.

This prospectus contains registered and unregistered trademarks and service marks of us and our subsidiaries, as well as trademarks and service marks of third parties. All brand names, trademarks and service marks appearing in this prospectus are the property of their respective holders.

For investors outside the United States: we have not and the underwriters have not done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of the shares of common stock and the distribution of this prospectus outside the United States.

Table of Contents

This summary highlights information contained elsewhere in this prospectus. This summary does not contain all of the information you should consider before investing in our common stock. You should read the following summary together with the more detailed information appearing in this prospectus, especially the “Risk Factors” section beginning on page 9 and our consolidated financial statements and related notes, before deciding whether to purchase shares of our common stock.

As used in this prospectus, unless the context otherwise requires, references to “we,” “us,” “our” and “Demandware” refer to the consolidated operations of Demandware, Inc. and its consolidated subsidiaries taken as a whole.

Demandware, Inc.

Overview

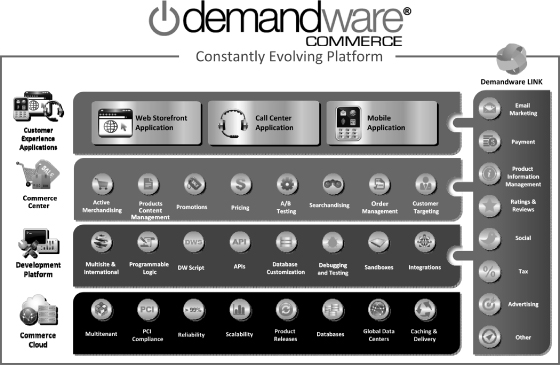

Demandware is a leading provider of software-as-a-service e-commerce solutions that enable companies to easily design, implement and manage their own customized e-commerce sites, including websites, mobile applications and other digital storefronts. Our customers use our highly scalable and integrated Demandware Commerce platform to create a seamless brand experience for consumers across all digital touch points worldwide. By simplifying access to the complex e-commerce functionality required for an effective and engaging consumer experience, we enable our customers to more easily launch and manage multiple e-commerce sites, initiate marketing campaigns more quickly and improve e-commerce site traffic, all of which can lead to increased revenue.

Through our on-demand software-as-a-service, or SaaS, platform, our customers run the latest version of our software and have access to a steady stream of new and innovative e-commerce functionality as soon as it becomes available. By using our platform, our customers avoid the need for a large upfront investment in on-premise hardware infrastructure and in customized software that is difficult and expensive to implement, upgrade and maintain. They also avoid the limitations of generic vendor-created e-commerce solutions that typically do not offer the flexibility and functionality necessary for merchants and retailers to create, manage and control their own customized online brand presence. Through our network of data centers, we continually monitor the environment in which our customers’ e-commerce sites operate for performance, availability and accuracy of content delivery.

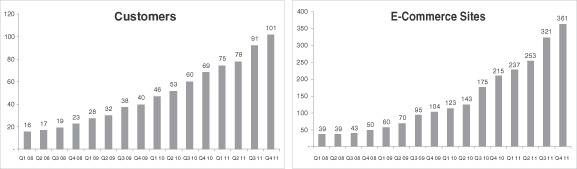

From December 31, 2007 to December 31, 2011, the number of customers using our Demandware Commerce platform increased from 10 to 101, a 78.3% compound annual growth rate, or CAGR, and the number of e-commerce sites operating on our platform increased from 19 to 361, a 108.8% CAGR. Our customers include multinational corporations, large retailers and branded consumer product manufacturers, such as Barneys New York, Burton, Columbia Sportswear, Crocs, House of Fraser, Jewelry Television, Jones Apparel Group, Lifetime Brands, L’Oreal and neckermann.de. We have structured our customer contracts to align our interests with those of our customers by participating in a share of our customers’ gross revenue processed on our platform. We derive our subscription revenue from fees paid to us by our customers for their access to our e-commerce solutions during the term of our subscription contracts, which is typically three years and ranges from one year to seven years.

We generated revenue of $21.4 million, $36.7 million and $56.5 million in 2009, 2010 and 2011, respectively. We had a net loss of $10.4 million, net income of $0.3 million and a net loss of $1.4 million in 2009, 2010 and 2011, respectively.

1

Table of Contents

The Market

We believe our total addressable market is at the center of three large and growing industries: retail, e-commerce and SaaS. According to Euromonitor, the global retail industry in 2010 was $11.6 trillion, of which only 2.7% was conducted online. The overall global retail industry grew at a 4.8% CAGR from 2005 to 2010, while the global e-commerce market grew at a 17.3% CAGR over the same period to reach $316.5 billion in 2010 and is expected to grow to $653.0 billion in 2015, demonstrating the significant service shift from offline to online retail during this period and the increasing importance of e-commerce within the retail industry. In addition, the adoption of SaaS solutions has grown significantly, and, according to Gartner, estimated worldwide total software revenue for SaaS delivery within the enterprise application software markets is expected to grow at a CAGR of 17.9% from $10.0 billion in 2010 to $22.7 billion in 2015, and the adoption of cloud-enabled e-commerce platform services is expected to grow at a CAGR of 21.3% from $4.3 billion in 2010 to $11.3 billion in 2015.

While the e-commerce market is expanding, it is also becoming more complex, particularly for global multi-channel retailers and brands trying to reach consumers with consistent storefronts across multiple channels, geographies and digital touchpoints. Several trends are driving this increased complexity:

| Ÿ | Need to Maintain Scale and Global Presence. Companies that are unable to maintain the quality and functionality of their e-commerce sites as they expand and grow risk losing both existing and prospective consumers, domestically and internationally. |

| Ÿ | Increasing Consumer Demand for Compelling Content and Commerce. As the speed, functionality and sophistication of internet applications continue to improve, consumers increasingly expect a rich, interactive and personalized e-commerce experience, such as active merchandising, social commerce, dynamic product imaging and ratings and reviews. |

| Ÿ | Proliferation of Retail Channels. E-commerce is expanding beyond traditional web storefronts viewed on a personal computer due to the rapid proliferation of internet-enabled devices, including in-store kiosks, smart phones, tablets, and other devices, allowing consumers to access information and shop through an increasing number of digital retail channels. |

| Ÿ | Integration of Systems and Business Processes. Businesses have dramatically recast their online presence from static e-commerce sites focused mainly on presentation of basic product information or simple purchasing to dynamic, interactive hubs for consumer marketing, transactions, communications and services. Businesses require robust, scalable and global e-commerce solutions that can integrate with other enterprise solutions, such as enterprise resource planning, customer relationship management, order management, call centers, supply chain management and business intelligence systems. |

| Ÿ | Rapid Pace of Innovation. As the switching costs for consumers adopting the newest technologies remain low and new shopping models evolve, the pressure for companies to keep up with the pace of e-commerce innovation increases. |

Traditionally, there have been two common solutions for the creation and management of an e-commerce business: on-premise enterprise software, which is built, customized and maintained by the merchant itself; and outsourcing, where the entire e-commerce platform for a retailer or brand is outsourced to a third-party provider. While traditional on-premise enterprise software solutions offer the benefits of in-house control and differentiation through custom development, they typically have relatively high upfront costs and are difficult to maintain, upgrade and scale. While outsourcing an e-commerce site offers the benefits of minimal required resources for internal infrastructure management and ongoing support, it typically offers limited customization and flexibility and may not tightly integrate with the customer’s other business processes.

2

Table of Contents

A SaaS delivery model can combine the lower costs, speed of implementation and other operational benefits of outsourcing with the functionality, flexibility and customization capabilities of on-premise enterprise software solutions. As a result, the adoption of SaaS solutions across industries has grown significantly. We believe there is a significant opportunity in the e-commerce market for a company that can offer a comprehensive SaaS solution designed to address the increasingly complex requirements of retailers and brands seeking to attract and satisfy consumers in the digital world.

The Demandware Solution

Demandware Commerce combines enterprise-class e-commerce capabilities and functionality with a SaaS multi-tenant delivery model. We believe that our on-demand solutions provide the following benefits to our customers:

| Ÿ | Broad Merchandising Functionality. Our platform uses a web-based interface to provide one central location for our customers to control and manage their e-commerce sites—from products to pricing to placement to content. |

| Ÿ | High Reliability, Safety and Security. We provide high uptime, robust security and built-in disaster recovery through our network of state-of-the-art data centers. We have provided 99.98% average site availability (excluding planned downtime) since 2005. |

| Ÿ | Ease of Deployment and Reduced Time To Market. Using our Demandware Commerce platform, customers can easily deploy new e-commerce sites without the need to install or integrate their own hardware and software infrastructure. Through Demandware LINK, our online community of technology partners, customers can access an extensive library of integrations to third-party applications to expand the capabilities and functionality of their e-commerce sites. These features enable our existing customers to accelerate their time-to-market for new e-commerce sites and quickly implement new functionality. In addition, we believe that our typical four to six month platform implementation cycle for new customers is shorter than the period generally required for the development and deployment of comparable on-premise e-commerce software solutions. |

| Ÿ | Customizable E-Commerce Sites. Demandware Commerce allows our customers to quickly and easily customize and deliver a highly flexible digital storefront, using our powerful and intuitive tools based on procedural programming languages such as JavaScript. |

| Ÿ | Continuous Innovation. Through our SaaS platform, we are able to provide a steady stream of new and innovative e-commerce functionality through multiple product upgrades each year, which our customers can deploy with minimal or no effort to access the latest technologies on their e-commerce sites. |

Our Strategy

Our mission is to extend our position as a leading provider of SaaS e-commerce solutions and become the global backbone for digital commerce between retailers or branded consumer product manufacturers and their consumers. Key elements of our strategy include:

Retaining and Expanding Business with Existing Customers

| Ÿ | Increasing Customers’ Gross Revenue. We will continue to work with our customers to help grow their online revenue and optimize the effectiveness, engagement and performance of their e-commerce sites by taking full advantage of the functionality of our Demandware Commerce platform. |

3

Table of Contents

| Ÿ | Increasing the Number of Customers’ E-Commerce Sites. We will continue to assist our customers’ efforts to expand their e-commerce presence by launching additional distinct revenue-generating e-commerce sites for different geographies, brands and channels. |

| Ÿ | Extending the Platform Across Channels. We will continue to extend our Demandware Commerce platform to support established and emerging channels where consumers want to shop, including smart phones, social networks, call centers and in-store kiosks. |

Growing Our Customer Base

| Ÿ | Investing in Direct Sales. We plan to grow our enterprise direct sales team to win more customers domestically and internationally. |

| Ÿ | Significantly Growing Our European Operations. We intend to continue to grow our European operations by further investing in direct sales, strategic alliances, services and support in the region. |

| Ÿ | Expanding and Strengthening Our Strategic Alliances. We intend to continue to grow our distribution channels through key existing and new alliances. |

Targeting New Markets

| Ÿ | Small- and Medium-Sized Businesses. We are building a sales team to target small- and medium-sized retailers and emerging brands that are just starting to implement their e-commerce strategies and want to quickly scale their online business. |

| Ÿ | Asia Pacific. We expect to build sales and service operations in the Asia Pacific region. |

Continuing to Innovate and Add New Functionality to Our Platform

| Ÿ | Develop New Features. We plan to use our expertise in e-commerce to develop new applications, features and functionality that will enhance our platform and expand our addressable market. |

| Ÿ | Add Functionality Through Acquisitions or Partnerships. We also plan to add incremental functionality to our platform opportunistically through acquisitions and to invest in our Demandware LINK program by adding new partners and expanding our relationship with current partners so that our customers have access to a growing library of integrations to third-party applications. |

Risks That We Face

Our business is subject to a number of risks that you should consider carefully before deciding whether to invest in our common stock. These risks are described more fully in the “Risk Factors” section beginning on page 9 and elsewhere in this prospectus and include the following:

| Ÿ | we have had a history of losses, and we may be unable to achieve or sustain profitability; |

| Ÿ | we depend on a limited number of customers for a substantial portion of our revenue, and the loss of a key customer or the significant reduction of business from our largest customer could significantly reduce our revenue; |

| Ÿ | our customers are retailers and branded consumer product manufacturers that typically realize a significant portion of their online sales in the fourth quarter of each year, specifically during the holiday season. The seasonality of our business could create significant fluctuations in our quarterly revenue; |

4

Table of Contents

| Ÿ | we recognize revenue from customer subscriptions over the term of the subscription agreement and, therefore, a significant downturn in our business may not be immediately reflected in our operating results; |

| Ÿ | our business is substantially dependent upon the continued growth of the market for on-demand software solutions; and |

| Ÿ | if we fail to manage our SaaS hosting network infrastructure capacity, our existing customers may experience service outages and our new customers may experience delays in the deployment of our e-commerce solutions. |

Ownership of our Capital Stock

Upon the closing of this offering, our directors and executive officers and their affiliates will beneficially own, in the aggregate, approximately 12,717,891 shares of our common stock, or approximately 45.4% of our outstanding capital stock, assuming no exercise of the underwriters’ option to purchase additional shares of our common stock in this offering, and after giving effect to the 1-for-3 reverse split of our common stock effected on March 1, 2012 and the automatic conversion of all outstanding shares of our preferred stock into 18,028,763 shares of common stock upon the closing of this offering.

Our Corporate Information

We were incorporated in Delaware in February 2004 as SSE Holdings, Inc., and changed our name to Demandware, Inc. in August 2004. Our executive offices are located at 5 Wall Street, Burlington, Massachusetts 01803 and our telephone number is (888) 553-9216. Our website address is www.demandware.com. The information on, or that can be accessed through, our website does not constitute part of this prospectus, and you should not rely on any such information in making the decision whether to purchase our common stock.

5

Table of Contents

THE OFFERING

| Common stock offered by Demandware, Inc. |

5,500,000 shares |

| Common stock to be outstanding after this offering |

27,997,970 shares |

| Option to purchase additional shares offered to underwriters |

The underwriters have an option to purchase a maximum of 825,000 additional shares from us. The underwriters can exercise this option at any time within 30 days from the date of this prospectus. |

| Use of proceeds |

We intend to use the net proceeds to us from this offering for financing our growth, working capital and other general corporate purposes. See “Use of Proceeds” for more information. |

| Risk Factors |

You should read carefully the section entitled “Risk Factors” for a discussion of factors that you should consider before deciding to invest in shares of our common stock. |

| New York Stock Exchange symbol |

“DWRE” |

The number of shares of our common stock to be outstanding after this offering is based on the number of shares of our common stock outstanding as of December 31, 2011 and excludes:

| Ÿ | 4,024,477 shares of common stock issuable upon exercise of stock options outstanding as of December 31, 2011, at a weighted average exercise price of $1.92 per share; |

| Ÿ | 220,968 shares of common stock reserved as of December 31, 2011 for future issuance under our equity incentive plans; and |

| Ÿ | 23,092 shares of common stock issuable upon exercise of a warrant outstanding as of December 31, 2011, at an exercise price of $3.90 per share. |

On February 9, 2012, our board of directors approved a 1-for-3 reverse split of our common stock. The reverse stock split became effective on March 1, 2012. Upon the effectiveness of the reverse stock split (i) every three shares of outstanding common stock was decreased to one share of common stock, (ii) the number of shares of common stock into which each outstanding option to purchase common stock is exercisable was proportionally decreased, (iii) the exercise price of each outstanding option to purchase common stock was proportionately increased, and (iv) the conversion ratio for each share of preferred stock outstanding was proportionately reduced. Unless otherwise indicated, all share numbers, share prices and exercise prices in this prospectus have been adjusted, on a retroactive basis, to reflect this 1-for-3 reverse stock split.

Unless otherwise indicated, this prospectus reflects and assumes the following:

| Ÿ | the conversion of all outstanding shares of our preferred stock into 18,028,763 shares of our common stock, which will occur automatically upon the closing of the offering; |

| Ÿ | the filing of our amended and restated certificate of incorporation and the adoption of our amended and restated by-laws upon the closing of this offering; |

| Ÿ | no exercise by the underwriters of their option to purchase additional shares; and |

| Ÿ | no exercise of outstanding stock options or warrants. |

6

Table of Contents

SUMMARY CONSOLIDATED FINANCIAL DATA

The following table presents our summary consolidated financials and other data for our business for the periods indicated. The summary consolidated statements of operations data presented below for the years ended December 31, 2009, 2010 and 2011 has been derived from our audited financial statements appearing elsewhere in this prospectus. Our historical results are not necessarily indicative of the results to be expected in the future. You should read this summary consolidated financial data in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes, all included elsewhere in this prospectus.

| Year Ended December 31, | ||||||||||||

| 2009 | 2010 | 2011 | ||||||||||

| (in thousands, except per share data) |

||||||||||||

| Consolidated Statements of Operations Data: |

||||||||||||

| Revenue: |

||||||||||||

| Subscription |

$ | 16,085 | $ | 28,714 | $ | 47,219 | ||||||

| Services |

5,312 | 7,976 | 9,328 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total revenue |

21,397 | 36,690 | 56,547 | |||||||||

| Cost of revenue: |

||||||||||||

| Subscription |

3,964 | 6,222 | 9,511 | |||||||||

| Services |

11,533 | 8,282 | 10,196 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total cost of revenue |

15,497 | 14,504 | 19,707 | |||||||||

|

|

|

|

|

|

|

|||||||

| Gross profit |

5,900 | 22,186 | 36,840 | |||||||||

| Operating expenses: |

||||||||||||

| Sales and marketing |

7,304 | 10,883 | 19,847 | |||||||||

| Research and development |

4,950 | 6,091 | 11,182 | |||||||||

| General and administrative |

3,729 | 4,179 | 6,567 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total operating expenses |

15,983 | 21,153 | 37,596 | |||||||||

|

|

|

|

|

|

|

|||||||

| (Loss) income from operations |

(10,083 | ) | 1,033 | (756 | ) | |||||||

| Other (expense) income, net |

(239 | ) | (582 | ) | (443 | ) | ||||||

|

|

|

|

|

|

|

|||||||

| (Loss) income before income taxes |

(10,322 | ) | 451 | (1,199 | ) | |||||||

| Income tax expense |

55 | 142 | 212 | |||||||||

|

|

|

|

|

|

|

|||||||

| Net (loss) income |

(10,377 | ) | 309 | (1,411 | ) | |||||||

| Accretion of redeemable preferred stock |

(4,322 | ) | (5,106 | ) | (5,274 | ) | ||||||

|

|

|

|

|

|

|

|||||||

| Net loss attributable to common stockholders |

$ | (14,699 | ) | $ | (4,797 | ) | $ | (6,685 | ) | |||

|

|

|

|

|

|

|

|||||||

| Net loss per share attributable to common stockholders, basic and diluted |

$ | (7.83 | ) | $ | (2.44 | ) | $ | (1.75 | ) | |||

|

|

|

|

|

|

|

|||||||

| Weighted average common shares outstanding, basic and diluted |

1,878 | 1,967 | 3,823 | |||||||||

|

|

|

|

|

|

|

|||||||

| Pro forma net loss per share attributable to common stockholders, basic and diluted |

$ | (0.06 | ) | |||||||||

|

|

|

|||||||||||

| Pro forma weighted average common shares outstanding, basic and diluted |

21,851 | |||||||||||

|

|

|

|||||||||||

7

Table of Contents

| As of December 31, 2011 | ||||||||||||

| Actual | Pro Forma(1) | Pro Forma As Adjusted(2) |

||||||||||

| (unaudited) | ||||||||||||

| (in thousands) | ||||||||||||

| Consolidated Balance Sheet Data: |

||||||||||||

| Cash and cash equivalents |

$ | 14,939 | $ | 14,939 | $ | 80,459 | ||||||

| Working capital |

8,725 | 8,725 | 74,245 | |||||||||

| Total assets |

42,886 | 42,886 | 108,406 | |||||||||

| Notes payable |

1,882 | 1,882 | 1,882 | |||||||||

| Total preferred stock |

87,603 | — | — | |||||||||

| Total stockholders’ (deficit) equity |

(84,620 | ) | 2,983 | 68,503 | ||||||||

| (1) | The pro forma balance sheet data give effect to the conversion of all outstanding shares of our preferred stock into an aggregate of 18,028,763 shares of common stock upon the closing of this offering. |

| (2) | The pro forma as adjusted balance sheet data also give effect to our issuance and sale of 5,500,000 shares of common stock in this offering at an assumed initial public offering price of $13.50 per share, the midpoint of the price range listed on the cover page of this prospectus, after deducting the estimated underwriting discounts and commissions and estimated offering expenses payable by us. |

A $1.00 increase (decrease) in the assumed initial public offering price of $13.50 per share, which is the midpoint of the range listed on the cover page of this prospectus, would increase (decrease) the pro forma as adjusted amount of each of cash and cash equivalents, working capital, total assets and total stockholders’ equity by approximately $5.1 million, assuming that the number of shares offered by us, as set forth on the cover page of this prospectus, remains the same and after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us.

8

Table of Contents

Investing in our common stock involves a high degree of risk. You should carefully consider the risks and uncertainties described below, together with all of the other information included in this prospectus, including our financial statements and the related notes appearing at the end of this prospectus, before deciding to invest in our common stock. Our business, financial condition, results of operations and future growth prospects could be materially and adversely affected by any of these risks or uncertainties. In that case, the trading price of our common stock could decline, and you may lose all or part of your investment.

Risks Related to Our Business and Our Industry

We have had a history of losses, and we may be unable to achieve or sustain profitability.

We have experienced net losses in each year since our inception, except for the year ended December 31, 2010. We experienced a net loss of $10.4 million for the year ended December 31, 2009, net income of $0.3 million for the year ended December 31, 2010 and a net loss of $1.4 million for the year ended December 31, 2011. We cannot predict if we will achieve sustained profitability in the near future or at all. We expect to make significant future expenditures to develop and expand our business. In addition, as a public company we will incur significant legal, accounting and other expenses that we did not incur as a private company. These increased expenditures will make it harder for us to achieve and maintain future profitability. Our recent growth in revenue and number of customers may not be sustainable, and we may not achieve sufficient revenue to achieve or maintain profitability. We may incur significant losses in the future for a number of reasons, including the other risks described in this prospectus, and we may encounter unforeseen expenses, difficulties, complications and delays and other unknown events. Accordingly, we may not be able to achieve or maintain profitability and we may incur significant losses for the foreseeable future.

Our limited operating history makes it difficult to evaluate our current business and future prospects.

We have been in existence since 2004, and much of our growth has occurred in recent periods. Our limited operating history may make it difficult for you to evaluate our current business and our future prospects. We have encountered and will continue to encounter risks and difficulties frequently experienced by growing companies in rapidly changing industries, including increasing and unforeseen expenses as we continue to grow our business. If we do not manage these risks successfully, our business will be harmed.

We depend on a limited number of customers for a substantial portion of our revenue. The loss of a key customer or the significant reduction of business from our largest customer could significantly reduce our revenue.

We have derived, and we believe that we will continue to derive, a substantial portion of our revenue from a limited number of customers. For example, for the year ended December 31, 2011, our largest ten customers by revenue accounted for an aggregate of approximately 40% of our revenue, and our largest customer by revenue, neckermann.de, accounted for 16% of our revenue. While the percentage of our revenue from neckermann.de is trending down, if we were to lose neckermann.de or one or more of our other key customers, there is no assurance that we would be able to replace such customers with new customers that generate comparable revenue, which would adversely affect our financial condition and results of operations. Our operating results for the foreseeable future will continue to depend on our ability to sell our e-commerce solutions to a small number of customers. Any revenue growth will depend on our success in growing our customers’ online revenue processed on our platform and expanding our customer base to include additional customers.

9

Table of Contents

The seasonality of our business creates significant variance in our quarterly revenue.

Our customers are retailers and branded consumer product manufacturers that typically realize a significant portion of their online sales in the fourth quarter of each year, specifically during the holiday season. As a result of this seasonal variation, our subscription revenue fluctuates, with additional fees in excess of committed annual levels, called overage fees, being higher in the fourth quarter than in other quarters and with revenue generally declining in the first quarter sequentially from the fourth quarter.

We recognize revenue from customer subscriptions over the term of the subscription agreement and, therefore, a significant downturn in our business may not be immediately reflected in our operating results.

We recognize revenue from subscription agreements monthly over the terms of these agreements, which is typically three years. As a result, a significant portion of the revenue we report in each quarter is generated from customer agreements entered into during previous periods. Consequently, a decline in new or renewed subscriptions in any one quarter may not impact our financial performance in that quarter, but might negatively affect our revenue in future quarters. If a number of contracts expire and are not renewed in the same quarter, our revenue may decline significantly in that quarter and subsequent quarters. In addition, we may be unable to adjust our fixed costs in response to reduced revenue. Accordingly, the effect of significant declines in sales and market acceptance of our solutions may not be reflected in our short-term results of operations.

Our business is substantially dependent upon the continued growth of the market for on-demand software solutions.

We derive, and expect to continue to derive, substantially all of our revenue from the sale of our on-demand e-commerce solutions. As a result, widespread acceptance and use of the on-demand business model is critical to our future growth and success. Under the perpetual or periodic license model for software procurement, users of the software would typically run the applications on their hardware. Because many companies are generally predisposed to maintaining control of their information technology, or IT, systems and infrastructure, there may be resistance to the concept of accessing software functionality as a service provided by a third party. In addition, the market for on-demand software solutions is still evolving, and competitive dynamics may cause pricing levels to change, as the market matures and as existing and new market participants introduce new types of solutions and different approaches to enable organizations to address their e-commerce needs. As a result, we may be forced to reduce the prices we charge for our solutions and may be unable to renew existing customer agreements or enter into new customer agreements at the same prices and upon the same terms that we have historically. If the market for on-demand software solutions fails to grow, grows more slowly than we currently anticipate or evolves and forces us to reduce the prices we charge for our solutions, demand for our solutions and our revenue, gross margin and other operating results could be materially adversely affected.

We rely on a variable pricing model and any change in that model could adversely affect our financial results.

We have adopted a variable pricing model whereby we participate in a share of our customers’ gross revenue processed on our platform. This pricing model aligns our interests with those of our customers and reflects the need for us to expand our own processing and support infrastructure as activity on our customers’ e-commerce sites increases. All of our customer contracts are based on a variable pricing model. If customers were to demand a fixed pricing model that did not provide for variability based on their level of usage of our platform, our financial results could be adversely affected.

10

Table of Contents

Our lengthy sales and implementation cycles make it difficult to predict our future revenue and causes variability in our operating results.

Our sales cycle can vary substantially from customer to customer, but typically requires six to nine months depending on the size and complexity of the opportunity. From the time a new contract is signed, four to six months are typically required to implement and launch an e-commerce site for a new customer. A number of factors influence the length and variability of our sales and implementation cycles, including, for example:

| Ÿ | the need to educate potential customers about the uses and benefits of our solutions; |

| Ÿ | the relatively long duration of the commitment customers make in their agreements with us; |

| Ÿ | the discretionary nature of potential customers’ purchasing and budget cycles and decisions; |

| Ÿ | the competitive nature of potential customers’ evaluation and purchasing processes; |

| Ÿ | evolving e-commerce needs and functionality demands of potential customers; |

| Ÿ | announcements or planned introductions of new products by us or our competitors; and |

| Ÿ | lengthy purchasing approval processes of potential customers. |

Lengthy sales and implementation cycles make it difficult to predict the quarter in which revenue from a new customer may first be recognized. We may incur significant sales and marketing expenses in anticipation of selling our products, and if we do not achieve the level of revenue we expected, our operating results will suffer and our stock price may decline. Further, our potential customers frequently need to obtain approvals from multiple decision makers before making purchase decisions. Delays in our sales or implementation cycles could cause significant variability in our revenue and operating results for any particular period.

If we are unable to retain our existing customers, our revenue and results of operations would be adversely affected.

We sell our solutions pursuant to agreements that are generally three years in duration. Our customers have no obligation to renew their subscriptions after their subscription period expires, and these subscriptions may not be renewed on the same or on more profitable terms. As a result, our ability to grow depends in part on subscription renewals. We may not be able to accurately predict future trends in customer renewals, and our customers’ renewal rates may decline or fluctuate because of several factors, including their satisfaction or dissatisfaction with our services, the cost of our services and the cost of services offered by our competitors or reductions in our customers’ spending levels. If our customers do not renew their subscriptions for our services, renew on less favorable terms or do not purchase additional functionality or subscriptions, our revenue may grow more slowly than expected or decline, and our profitability and gross margins may be harmed.

Security and privacy breaches may hurt our business.

Any security breaches, unauthorized access, unauthorized usage, virus or similar breach or disruption could result in loss of confidential information, damage to our reputation, early termination of our contracts, litigation, regulatory investigations or other liabilities. If our, our customers’ or our partners’ security measures are breached as a result of third-party action, employee error, malfeasance or otherwise and, as a result, someone obtains unauthorized access to customer data, our reputation will be damaged, our business may suffer and we could incur significant liability.

Techniques used to obtain unauthorized access or to sabotage systems change frequently and generally are not recognized until launched against a target. As a result, we may be unable to anticipate these techniques or to implement adequate preventative measures. If an actual or perceived

11

Table of Contents

security breach occurs, the market perception of our security measures could be harmed and we could lose sales and customers. Any significant violations of data privacy could result in the loss of business, litigation and regulatory investigations and penalties that could damage our reputation and adversely impact our results of operations and financial condition. Moreover, if a high profile security breach occurs with respect to another software-as-a-service, or SaaS, provider, our customers and potential customers may lose trust in the security of the SaaS business model generally, which could adversely impact our ability to retain existing customers or attract new ones.

Our business and operations have experienced rapid growth and organizational change in recent periods, which has placed, and may continue to place, significant demands on our management and infrastructure. If we fail to manage our growth effectively, we may be unable to execute our business plan, maintain high levels of service or address competitive challenges adequately.

We increased our number of full-time employees from 104 as of December 31, 2009, to 150 as of December 31, 2010 and to 215 as of December 31, 2011, and our revenue grew from $21.4 million in 2009 to $36.7 million in 2010 and to $56.5 million in 2011. Our growth has placed, and may continue to place, a significant strain on our managerial, administrative, operational, financial and other resources. We intend to further expand our overall business, customer base, headcount and operations both domestically and internationally, with no assurance that our business or revenue will continue to grow. Creating a global organization and managing a geographically dispersed workforce will require substantial management effort, the allocation of valuable management resources and significant additional investment in our infrastructure. We will be required to continue to improve our operational, financial and management controls and our reporting procedures and we may not be able to do so effectively. As such, we may be unable to manage our expenses effectively in the future, which may negatively impact our gross margins or operating expenses in any particular quarter. If we fail to manage our anticipated growth and change in a manner that preserves the key aspects of our corporate culture, the quality of our solutions may suffer, which could negatively affect our brand and reputation and harm our ability to retain and attract customers.

Failure to effectively maintain and expand our direct sales teams and develop and expand our indirect sales channel will impede our growth.

We will need to continue to expand our sales and marketing infrastructure in order to grow our customer base and our business. Identifying, recruiting and training these sales and marketing personnel will require significant time, expense and attention. Our business will be seriously harmed and our financial resources will be wasted if our efforts to expand our direct and indirect sales channels do not generate a corresponding increase in revenue. In particular, if we are unable to hire, develop and retain talented sales personnel or if our new direct sales personnel are unable to achieve expected productivity levels in a reasonable period of time, we may not be able to significantly increase our revenue and grow our business.

The global recession and related credit crisis may continue to adversely affect our business and results of operations.

The U.S. and other global economies have experienced a recession that has affected all sectors of the economy, resulting in declines in economic growth and consumer confidence, increases in unemployment rates and uncertainty about economic stability. Global credit and financial markets have also experienced extreme disruptions, including diminished liquidity and credit availability and rapid fluctuations in market valuations. Our business has been affected by these conditions, and there is no certainty that economic conditions will not deteriorate further. These uncertainties may affect our business in a number of ways, making it difficult to accurately forecast and plan our future business

12

Table of Contents

activities. Weak economic conditions may lead consumers and retailers to postpone spending, which may cause our customers to decrease or delay their purchases of our solutions. In addition, the inability of consumers to obtain credit could negatively affect our revenue. Financial difficulties experienced by third parties with whom we have entered relationships and upon whom we depend in order to grow our business could detract from the quality or timeliness of the products or professional services they provide to us, which could adversely affect our reputation and relationships with our customers.

If the current uncertain economic conditions continue or further deteriorate, we could be required to record charges relating to restructuring costs or the impairment of assets, and our business and results of operations could be materially adversely affected.

We are dependent upon consumers’ willingness to use the internet for commerce.

Our success depends upon the general public’s continued willingness to use the internet as a means to purchase goods, communicate, and conduct and research commercial transactions. If consumers became unwilling or less willing to use the internet for commerce for any reason, including lack of access to high-speed communications equipment, congestion of traffic on the internet, internet outages or delays, disruptions or other damage to users’ computers, increases in the cost of accessing the internet and security and privacy risks or the perception of such risks, our business could be materially adversely affected.

Even if demand for e-commerce products and services increases generally, there is no guarantee that demand for SaaS solutions like ours will increase to a corresponding degree.

For our customers and potential customers to be willing to invest in our e-commerce solutions, the internet must continue to be accepted and widely used for commerce and communication. If e-commerce does not grow or grows more slowly than expected, then our future revenue and profits may not meet our expectations or those of analysts. The widespread adoption of our solutions depends not only on strong demand for e-commerce products and services generally, but also for products and services delivered via a SaaS business model in particular. Many companies continue to rely primarily or exclusively on traditional means of commerce that are not internet-based and may be reluctant to change their patterns of commerce. Even if such companies do adopt e-commerce solutions, it is unclear whether they will desire e-commerce solutions like ours. As a result, we cannot assure you that our SaaS e-commerce solutions will achieve and sustain the high level of market acceptance that is critical for the future success of our business.

If we fail to manage our SaaS hosting network infrastructure capacity, our existing customers may experience service outages and our new customers may experience delays in the deployment of our e-commerce solutions.

We have experienced significant growth in the number of users, transactions and data that our hosting infrastructure supports. We seek to maintain sufficient excess capacity in our SaaS hosting network infrastructure to meet the needs of all of our customers. We also seek to maintain excess capacity to facilitate the rapid provision of new customer deployments and the expansion of existing customer deployments. However, the provision of new hosting infrastructure requires significant lead time. If we do not accurately predict our infrastructure capacity requirements, particularly in the fourth quarter when we might experience significant increases in traffic on our customers’ e-commerce sites, our customers could experience service outages that may subject us to financial penalties and financial liabilities and result in customer losses. If our hosting infrastructure capacity fails to keep pace with increased sales, customers may experience delays as we seek to obtain additional capacity, which could harm our reputation and adversely affect our revenue growth.

13

Table of Contents

If we fail to develop our brand cost-effectively, our business may suffer.

We believe that developing and maintaining awareness of our brand in a cost-effective manner is critical to achieving widespread acceptance of our existing and future solutions and is an important element in attracting new customers. Furthermore, we believe that the importance of brand recognition will increase as competition in our market increases. Successful promotion of our brand will depend largely on the effectiveness of our marketing efforts and on our ability to provide reliable and useful services at competitive prices. In the past, our efforts to build our brand have involved significant expenses. Brand promotion activities may not yield increased revenue, and even if they do, any increased revenue may not offset the expenses we incurred in building our brand. If we fail to successfully promote and maintain our brand, or incur substantial expenses in an unsuccessful attempt to promote and maintain our brand, we may fail to attract enough new customers or retain our existing customers to the extent necessary to realize a sufficient return on our brand-building efforts, and our business could suffer.

We may not be able to compete successfully against current and future competitors.

We face intense competition in the market for e-commerce applications and services, and we expect competition to intensify in the future. We have competitors with longer operating histories, larger customer bases and greater financial, technical, marketing and other resources than we do. Increased competition may result in reduced pricing for our solutions, longer sales cycles or a decrease of our market share, any of which could negatively affect our revenue and future operating results and our ability to grow our business.

A number of competitive factors could cause us to lose potential sales or to sell our solutions at lower prices or at reduced margins, including, among others:

| Ÿ | Potential customers may choose to develop e-commerce applications in-house, rather than paying for our solutions; |

| Ÿ | Some of our current and potential competitors have greater financial, marketing and technical resources than we do, allowing them to leverage a larger installed customer base and distribution network, adopt more aggressive pricing policies and offer more attractive sales terms, adapt more quickly to new technologies and changes in customer requirements, and devote greater resources to the promotion and sale of their products and services than we can; |

| Ÿ | Current and potential competitors have established or may establish cooperative relationships among themselves or with third parties to enhance their products and expand their markets, and consolidation in our industry is likely to intensify. Accordingly, new competitors or alliances among competitors may emerge and rapidly acquire significant market share; |

| Ÿ | Current and potential competitors may offer software that addresses one, or a limited number, of e-commerce functions at a lower price point or with greater depth than our solutions; and |

| Ÿ | Software vendors could bundle e-commerce solutions or offer such products at a lower price as part of a larger product sale. |

We cannot assure you that we will be able to compete successfully against current and future competitors. In addition, competition may intensify as our competitors enter into business combinations or alliances or raise additional capital and established companies in other market segments or geographic markets expand into our market segments or geographic markets. If we cannot compete successfully against our competitors, our business, results of operations and financial condition could be negatively impacted.

14

Table of Contents

Mergers of or other strategic transactions by our competitors or our customers could weaken our competitive position or reduce our revenue.

If one or more of our competitors were to merge or partner with another of our competitors, the change in the competitive landscape could adversely affect our ability to compete effectively. Our competitors may also establish or strengthen cooperative relationships with our current or future strategic distributors, systems integrators, third-party consulting firms or other parties with whom we have relationships, thereby limiting our ability to promote our solutions and limiting the number of consultants available to implement our solutions. In addition, we may lose customers that merge with or are acquired by companies using a competitor’s or an internally developed solution. Disruptions in our business caused by these events could reduce our revenue.

Our growth depends in part on the success of our strategic relationships with third parties.

We anticipate that we will continue to depend on various third-party relationships in order to grow our business. In addition to growing our indirect sales channels, we intend to pursue additional relationships with other third parties, such as technology and content providers and implementation consultants. Identifying, negotiating and documenting relationships with third parties require significant time and resources as does integrating third-party content and technology. Some of the third parties that sell our solutions have the direct contractual relationships with our ultimate end-user customers, and therefore we risk the loss of such customers if the third parties fail to perform their obligations. Our agreements with distributors and providers of technology, content and consulting services are typically non-exclusive, do not prohibit them from working with our competitors or from offering competing services and may not have minimum purchase commitments. Our competitors may be effective in providing incentives to third parties to favor their products or services or to prevent or reduce subscriptions to our solutions. In addition, these distributors and providers may not perform as expected under our agreements, and we have had, and may in the future have, disagreements or disputes with such distributors and providers, which could negatively affect our brand and reputation. A global economic slowdown could also adversely affect the businesses of our distributors, and it is possible that they may not be able to devote the resources we expect to the relationship.

If we are unsuccessful in establishing or maintaining our relationships with these third parties, specifically with eCommera, NETRADA and PFSweb, our ability to compete in the marketplace or to grow our revenue could be impaired and our operating results would suffer. Even if we are successful, we cannot assure you that these relationships will result in improved operating results.

We could incur substantial costs as a result of any claim of infringement of another party’s intellectual property rights.

In recent years, there has been significant litigation in the United States involving patents and other intellectual property rights. Companies providing internet-related products and services are increasingly bringing and becoming subject to suits alleging infringement of proprietary rights, particularly patent rights. These risks have been amplified by the increase in third parties, which we refer to as non-practicing entities, whose sole primary business is to assert such claims. We could incur substantial costs in prosecuting or defending any intellectual property litigation. If we sue to enforce our rights or are sued by a third party that claims that our technology infringes its rights, the litigation could be expensive and could divert our management resources.

In addition, in most instances, we have agreed to indemnify our customers against certain claims that our products infringe the intellectual property rights of third parties. We have received indemnification requests from many customers that have received letters from, or been sued by, non-practicing entities claiming infringement of patents owned by them. Most of those underlying claims, and the extent, if any, of our indemnification obligations, have not yet been resolved. Some of these patents are the subject of pending legal proceedings between the patent owners and one or more

15

Table of Contents

major companies engaged in e-commerce, and the outcome of those proceedings could affect the extent to which the patent owners seek to prosecute claims against us or our customers. Also, because the patent owners have asserted the same patents against multiple customers, an adverse resolution in the case of one customer could lead to adverse resolutions in the cases of other customers and such claims could potentially lead to greater exposure for us than for any single customer. Our business could be adversely affected by any significant disputes between us and our customers as to the applicability or scope of our indemnification obligations to them. The results of any intellectual property litigation to which we might become a party, or for which we are required to provide indemnification, may require us to do one or more of the following:

| Ÿ | cease selling or using products or services that incorporate the challenged intellectual property; |

| Ÿ | make substantial payments for legal fees, settlement payments or other costs or damages; |

| Ÿ | obtain a license, which may not be available on reasonable terms, to sell or use the relevant technology; or |

| Ÿ | redesign those products or services to avoid infringement. |

If we are required to make substantial payments or undertake any of the other actions noted above as a result of any intellectual property infringement claims against us or any obligation to indemnify our customers for such claims, such payments or costs could have a material adverse effect upon our business and financial results.

We could incur substantial costs in protecting our intellectual property from infringement, and any failure to protect our intellectual property could impair our business.

We seek to protect the source code for our proprietary software under a combination of patent, copyright and trade secrets law. However, because we make some of the source code available to some customers, third parties may be more likely to misappropriate it. Our policy is to enter into confidentiality agreements with our employees, consultants, vendors and customers and to control access to our software, documentation and other proprietary information. Despite these precautions, it may be possible for someone to copy our software or other proprietary information without authorization or to develop similar software independently.

Despite our efforts to protect our proprietary rights, unauthorized parties may attempt to copy aspects of our products or to obtain and use information that we regard as proprietary. Policing unauthorized use of our products is difficult, and while we are unable to determine the extent to which piracy of our software exists, we expect software piracy to be a persistent problem. Litigation may be necessary in the future to enforce our intellectual property rights, to protect our trade secrets, to determine the validity and scope of the proprietary rights of others or to defend against claims of infringement or invalidity. Such litigation could be costly, time-consuming and distracting to management, result in a diversion of resources, the impairment or loss of portions of our intellectual property and have a material adverse effect on our business, operating results and financial condition. Furthermore, our efforts to enforce our intellectual property rights may be met with defenses, counterclaims and countersuits attacking the validity and enforceability of our intellectual property rights. These steps may be inadequate to protect our intellectual property. We will not be able to protect our intellectual property if we are unable to enforce our rights or if we do not detect unauthorized use of our intellectual property. Despite our precautions, it may be possible for unauthorized third parties to copy our products and use information that we regard as proprietary to create products and services that compete with ours. Some license provisions protecting against unauthorized use, copying, transfer and disclosure of our licensed products may be unenforceable under the laws of certain jurisdictions and foreign countries. Further, the laws of some countries do not protect proprietary rights to the same extent as the laws of the United States. To the extent we expand our international activities, our exposure to unauthorized copying and use of our products and proprietary information may increase.

16

Table of Contents

There can be no assurance that our means of protecting our proprietary rights will be adequate or that our competitors will not independently develop similar technology. If we fail to meaningfully protect our intellectual property, then our business, brand, operating results and financial condition could be materially harmed.

If our software products contain serious errors or defects, then we may lose revenue and market acceptance and may incur costs to defend or settle product liability claims.

Complex software applications such as ours often contain errors or defects, particularly when first introduced or when new versions or enhancements are released. Despite internal testing and testing by our customers, our current and future products may contain serious defects, which could result in lost revenue or a delay in market acceptance.

Since our customers use our products for critical business applications, such as e-commerce, errors, defects or other performance problems could result in damage to our customers. They could seek significant compensation from us for the losses they suffer. Although our customer agreements typically contain provisions designed to limit our exposure to product liability claims, existing or future laws or unfavorable judicial decisions could negate these limitations. Even if not successful, a product liability claim brought against us would likely be time-consuming and costly and could seriously damage our reputation in the marketplace, making it harder for us to sell our products.

Government and industry regulation of the internet is evolving and could directly restrict our business or indirectly affect our business by limiting the growth of e-commerce. Unfavorable changes in government regulation or our failure to comply with regulations could harm our business and operating results.

As e-commerce evolves, federal, state and foreign agencies have adopted and could in the future adopt regulations covering issues such as user privacy, content, and taxation of products and services. Government regulations could limit the market for our products and services or impose burdensome requirements that render our business unprofitable. Our e-commerce solutions enable our customers to collect, manage and store a wide range of consumer data. The United States and various state governments have adopted or proposed limitations on the collection, distribution and use of personal information. Several foreign jurisdictions, including the European Union and the United Kingdom, have adopted legislation (including directives or regulations) that increase or change the requirements governing data collection and storage in these jurisdictions. If our privacy or data security measures fail to comply with current or future laws and regulations, we may be subject to litigation, regulatory investigations or other liabilities, or our customers may terminate their relationships with us.

In addition, although many regulations might not apply to our business directly, we expect that laws regulating the solicitation, collection or processing of personal and consumer information could affect our customers’ ability to use and share data, potentially reducing demand for our services. The Telecommunications Act of 1996 prohibits certain types of information and content from being transmitted over the internet. The prohibition’s scope and the liability associated with a violation are currently unsettled. In addition, although substantial portions of the Communications Decency Act were held to be unconstitutional, we cannot be certain that similar legislation will not be enacted and upheld in the future. It is possible that legislation could expose companies involved in e-commerce to liability, which could limit the growth of e-commerce generally. Legislation like the Telecommunications Act and the Communications Decency Act could dampen the growth in web usage and decrease its acceptance as a medium of communications and commerce. Moreover, if future laws and regulations limit our customers’ ability to use and share consumer data or our ability to store, process and share data with our customers over the internet, demand for our solutions could decrease, our costs could increase, and our results of operations and financial condition could be harmed.

17

Table of Contents

In addition, taxation of services provided over the internet or other charges imposed by government agencies or by private organizations for accessing the internet may also be imposed. Any regulation imposing greater fees for internet use or restricting information exchange over the internet could result in a decline in the use of the internet and the viability of internet-based services, which could harm our business and operating results.

We use a limited number of data centers to deliver our services. Any disruption of service at these facilities could harm our business.

We manage our services and serve all of our customers from a limited number of third-party data center facilities. While we engineer and architect the actual computer and storage systems upon which our platform runs, which we call our grid computing points of delivery, or PODs, and deploy them to the data center facilities, we do not control the operation of these facilities.

The owners of our data facilities have no obligation to renew their agreements with us on commercially reasonable terms, or at all. If we are unable to renew these agreements on commercially reasonable terms, we may be required to transfer to new data center facilities, and we may incur significant costs and possible service interruption in connection with doing so.

Any changes in third-party service levels at our data centers or any errors, defects, disruptions or other performance problems with our services could harm our reputation and may damage our customers’ businesses. Interruptions in our services might reduce our revenue, cause us to issue credits to customers, subject us to potential liability, and cause customers to terminate their subscriptions or harm our renewal rates.

Our data centers are vulnerable to damage or interruption from human error, intentional bad acts, earthquakes, hurricanes, floods, fires, war, terrorist attacks, power losses, hardware failures, systems failures, telecommunications failures and similar events. At least one of our data facilities is located in an area known for seismic activity, increasing our susceptibility to the risk that an earthquake could significantly harm the operations of these facilities. The occurrence of a natural disaster or an act of terrorism, or vandalism or other misconduct, a decision to close the facilities without adequate notice or other unanticipated problems could result in lengthy interruptions in our services.

We may not be able to respond to rapid technological changes with new solutions, which could have a material adverse effect on our sales and profitability.

The on-demand e-commerce market is characterized by rapid technological change, frequent new product and service introductions and evolving industry standards. Our ability to attract new customers and increase revenue from existing customers will depend in large part on our ability to enhance and improve our existing solutions, introduce new solutions and sell into new industry markets. To achieve market acceptance for our solutions, we must effectively anticipate and offer solutions that meet changing customer demands in a timely manner. Customers may require features and capabilities that our current solutions do not have. If we fail to develop solutions that satisfy customer preferences in a timely and cost-effective manner, our ability to renew our contracts with existing customers and our ability to create or increase demand for our solutions will be harmed.

We may experience difficulties with software development, industry standards, design, manufacturing or marketing that could delay or prevent our development, introduction or implementation of new solutions and enhancements. The introduction of new solutions by competitors, the emergence of new industry standards or the development of entirely new technologies to replace existing offerings could render our existing or future solutions obsolete.

If we are unable to successfully develop or acquire new e-commerce capabilities and functionality, enhance our existing solutions to anticipate and meet customer preferences or sell our solutions into new markets, our revenue and results of operations would be adversely affected.

18

Table of Contents

Our quarterly operating results may fluctuate in the future. As a result, we may fail to meet or exceed the expectations of research analysts or investors, which could cause our stock price to decline.

Our quarterly operating results may fluctuate as a result of a variety of factors, many of which are outside of our control. If our quarterly operating results or guidance fall below the expectations of research analysts or investors, the price of our common stock could decline substantially. Fluctuations in our quarterly operating results or guidance may be due to a number of factors, including, but not limited to, those listed below:

| Ÿ | factors affecting our existing customers’ gross revenue processed on our platform; |

| Ÿ | the extent to which our existing customers renew their subscriptions for our solutions and the timing and terms of those renewals; |

| Ÿ | the extent to which existing customers deploy or discontinue use of additional e-commerce sites on our platform; |

| Ÿ | the extent to which new customers are attracted to our solutions to satisfy their e-commerce needs; |

| Ÿ | the timing, committed subscription levels and revenue share rates at which we enter into agreements for our solutions with new customers; |

| Ÿ | the addition or loss of large customers, including through acquisitions or consolidations; |

| Ÿ | the number and size of new customers and the number and size of renewal customers in a particular period; |

| Ÿ | the mix of customers across small, mid-sized and large organizations; |

| Ÿ | changes in our pricing policies or those of our competitors; |

| Ÿ | the financial condition and creditworthiness of our customers; |

| Ÿ | the amount and timing of operating expenses, including those related to the maintenance and expansion of our business, operations and infrastructure; |

| Ÿ | the timing and success of new solutions introduced by us; |

| Ÿ | the timing and success of current and new products and services introduced by our competitors; |

| Ÿ | other changes in the competitive dynamics of our industry, including consolidation among competitors, customers or strategic partners; |

| Ÿ | the timing of expenses related to the development of new products and technologies, including enhancements to our solutions; |

| Ÿ | our ability to manage our existing business and future growth, including increases in the number of customers on our platform, additional customer e-commerce sites and new geographic regions; |

| Ÿ | expenses related to our data centers and the expansion of such data centers; |

| Ÿ | various factors related to disruptions in our SaaS hosting network infrastructure, defects in our solutions, privacy and data security and exchange rate fluctuations, each of which is described elsewhere in these risk factors; |

| Ÿ | our ability to efficiently and cost effectively deploy new customer e-commerce sites on our platform; and |

| Ÿ | general economic, industry and market conditions. |

19

Table of Contents