Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - EXPONENT INC | Financial_Report.xls |

| EX-31.1 - EXHIBIT 31.1 - EXPONENT INC | v242932_ex31-1.htm |

| EX-31.2 - EXHIBIT 31.2 - EXPONENT INC | v242932_ex31-2.htm |

| EX-32.1 - EXHIBIT 32.1 - EXPONENT INC | v242932_ex32-1.htm |

| EX-21.1 - EXHIBIT 21.1 - EXPONENT INC | v242932_ex21-1.htm |

| EX-32.2 - EXHIBIT 32.2 - EXPONENT INC | v242932_ex32-2.htm |

| EX-23.1 - EXHIBIT 23.1 - EXPONENT INC | v242932_ex23-1.htm |

| EX-10.40 - EXHIBIT 10.40 - EXPONENT INC | v242932_ex10-40.htm |

| EX-10.41 - EXHIBIT 10.41 - EXPONENT INC | v242932_ex10-41.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

________________________________

FORM 10-K

________________________________

| S | Annual Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the fiscal year ended December 30, 2011. |

OR

| £ | Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the transition period from ________ to _________. |

Commission File Number 0-18655

________________________________

EXPONENT, INC.

(Exact name of registrant as specified in its charter)

________________________________

| Delaware | 77-0218904 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| 149 Commonwealth Drive, Menlo Park, California | 94025 |

| (Address of principal executive offices) | (Zip Code) |

(650) 326-9400

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Name of Each Exchange on Which Registered | |

| Common Stock, $0.001 par value per share | The NASDAQ Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

| Yes £ | No S |

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

| Yes £ | No S |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Act during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

| Yes S | No £ |

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

| Yes S | No £ |

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. £

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer £ | Accelerated filer S | Non-accelerated filer £ | Smaller reporting company £ |

| (Do not check if a smaller | |||

| reporting company) |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

| Yes £ | No S |

The aggregate market value of the voting and non-voting stock held by non-affiliates of the registrant based on the closing sales price of the Common Stock as reported on the NASDAQ National Market on July 1, 2011, the last business day of the registrant’s most recently completed second quarter, was $502,877,855. Shares of the registrant’s common stock held by each executive officer and director and by each entity or person that, to the registrant’s knowledge, owned 10% or more of registrant’s outstanding common stock as of July 1, 2011 have been excluded in that such persons may be deemed to be affiliates of the registrant. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

The number of shares of the issuer’s Common Stock outstanding as of February 17, 2012 was 13,322,962.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s Definitive Proxy Statement for the Registrant’s 2012 Annual Meeting of Stockholders to be held on May 31, 2012, are incorporated by reference into Part III of this Form 10-K.

| 2 |

EXPONENT, INC.

FORM 10-K ANNUAL REPORT

FISCAL YEAR ENDED DECEMBER 30, 2011

TABLE OF CONTENTS

| Page | ||

| PART I | ||

| Item 1. | Business | 4 |

| Item 1A. | Risk Factors | 13 |

| Item 1B. | Unresolved Staff Comments | 16 |

| Item 2. | Properties | 17 |

| Item 3. | Legal Proceedings | 17 |

| Item 4. | Mine Safety Disclosures | 17 |

| PART II | ||

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 17 |

| Item 6. | Selected Financial Data | 19 |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 19 |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 29 |

| Item 8. | Financial Statements and Supplementary Data | 29 |

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 29 |

| Item 9A. | Controls and Procedures | 29 |

| Item 9B. | Other Information | 30 |

| PART III | ||

| Item 10. | Directors, Executive Officers and Corporate Governance | 30 |

| Item 11. | Executive Compensation | 30 |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 30 |

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | 30 |

| Item 14. | Principal Accounting Fees and Services | 30 |

| PART IV | ||

| Item 15. | Exhibits, Financial Statement Schedules | 31 |

| Signatures | 59 | |

| Exhibit Index | 60 |

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains, and incorporates by reference, certain “forward-looking” statements (as such term is defined in the Private Securities Litigation Reform Act of 1995, and the rules promulgated pursuant to the Securities Act of 1933, as amended, and the Securities Exchange Act of 1934, as amended), including but not limited to statements regarding future growth and market opportunities, revenue, margins, headcount, utilization and operating expenses, that are based on the beliefs of the Company’s management, as well as assumptions made by, and information currently available to, the Company’s management. Such forward-looking statements are subject to the safe harbor created by the Private Securities Litigation Reform Act of 1995. When used in this document and in the documents incorporated herein by reference, statements other than statements of current or historical fact are forward-looking statements. The words “anticipate,” “believe,” “estimate,” “expect” and similar expressions, as they relate to the Company or its management, identify certain of such forward-looking statements. Such statements reflect the current views of the Company or its management with respect to future events and are subject to certain risks, uncertainties and assumptions. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, the Company’s actual results, performance, or achievements could differ materially from those expressed in, or implied by, any such forward-looking statements. Factors that could cause or contribute to such material differences include the possibility that the demand for our services may decline as a result of changes in general and industry specific economic conditions, the timing of engagements for our services, the effects of competitive services and pricing, tort reform and liabilities resulting from claims made against us. Additional risks and uncertainties are discussed in this Report under the heading “Risk Factors” and elsewhere. The inclusion of such forward-looking information should not be regarded as a representation by the Company or any other person that the future events, plans, or expectations contemplated by the Company will be achieved. The Company undertakes no obligation to update or revise any such forward-looking statements.

| 3 |

PART I

Item 1. Business

GENERAL

The history of Exponent, Inc. goes back to 1967, with the founding of the partnership Failure Analysis Associates, which was incorporated the following year in California and reincorporated in Delaware as Failure Analysis Associates, Inc. in 1988. The Failure Group, Inc. was organized in 1989 as a holding company for Failure Analysis Associates, Inc. and changed its name to Exponent, Inc. in 1998. Exponent, Inc. (together with its subsidiaries, “Exponent” or the “Company”) is a science and engineering consulting firm that provides solutions to complex problems. Our multidisciplinary team of scientists, physicians, engineers, business and regulatory consultants brings together more than 90 different technical disciplines to solve complicated issues facing industry and government today. Our professional staff can perform in-depth scientific research and analysis, or very rapid-response evaluations to provide our clients with the critical information they need.

CLIENTS

General

Exponent serves clients in automotive, aviation, chemical, construction, consumer products, energy, government, health, insurance, manufacturing, technology and other sectors of the economy. Many of our engagements are initiated directly by large corporations or by lawyers or insurance companies, whose clients anticipate, or are engaged in, litigation related to their products, equipment, processes or service. Our services in failure prevention and technology evaluation have grown as the technological complexity of products has increased over the years.

Pricing and Terms of Engagements

We generally provide our services on either a fixed-price basis or on a “time and material” basis, charging hourly rates for each staff member involved in a project, based on his or her skills and experience. Our standard rates for professionals range from $135 to $600 per hour. Our engagement agreements typically provide for monthly billing, require payment of our invoices within 30 days of receipt and permit clients to terminate engagements at any time. Clients normally agree to indemnify us and our personnel against liabilities arising out of the use or application of the results of our work or recommendations.

SERVICES

Exponent provides high quality engineering and scientific consulting services to clients around the world. Our service offerings are provided on a project-by-project basis. Many projects require support from multiple practices. We currently operate 23 practices and centers, including:

| · | Biomechanics |

| · | Biomedical Engineering |

| · | Buildings & Structures |

| · | Civil Engineering |

| · | Construction Consulting |

| · | Defense Technology Development |

| · | Ecological & Biological Sciences |

| · | Electrical Engineering & Computer Science |

| · | Engineering Management Consulting |

| · | Environmental & Earth Sciences |

| · | Health Sciences |

| o | Center for Chemical Regulation & Food Safety |

| o | Center for Epidemiology, Biostatistics & Computational Biology |

| o | Center for Exposure Assessment & Dose Reconstruction |

| o | Center for Occupational Medicine & Environmental Health |

| o | Center for Toxicology & Mechanistic Biology |

| · | Human Factors |

| · | Industrial Structures |

| · | Materials & Corrosion Engineering |

| · | Mechanical Engineering |

| · | Polymer Science & Materials Chemistry |

| · | Statistical & Data Sciences |

| · | Thermal Sciences |

| · | Vehicle Analysis |

| 4 |

Biomechanics

Our biomechanics staff uses engineering and biomedical science to solve complex problems at the intersection of biology and engineering. Our expertise is used to understand and evaluate the interaction between the human body as a biological system and the physical environment to explore the cause, nature, and severity of injuries.

During the past year our biomechanics staff performed analyses of human injury related to a variety of products including recreational vehicles, sporting goods, trucks, trains, aircraft and motor cars. They also looked at the implications of using protective devices (such as restraint systems and helmets) on reducing potential injuries and assessed injuries in the workplace, during recreational activities and in the home.

Biomedical Engineering

Our Biomedical Engineering Practice applies engineering principles to the medical field, including the evaluation of designs and performance of medical devices and biotechnology. Our engineers and scientists assist clients with characterization of biomaterials, biological tissues, and medical devices. As part of regulatory compliance, we can perform preclinical testing and formulate a related regulatory strategy, conduct design verification and validation, as well as design and manufacturing failure analyses, recall management, and medical device explant analysis. In addition, our staff can perform analysis of clinical outcomes for medical devices using administrative claims databases. Our expertise is also utilized in product liability, intellectual property litigation, technology acquisition and due diligence matters.

Buildings & Structures

The basic function of a building is to provide structurally sound, durable and environmentally controlled space to house and protect occupants and contents. If this basic function is not achieved, it is because some aspect(s) of the building design or construction failed to perform its intended function. Our architects, engineers, and scientists have been investigating such failures for decades, and we use this experience to solve problems with building systems and components, including finding the best repair options and mitigating the risk of future failures.

During the past year, we have evaluated numerous problems with residential, commercial and industrial structures for insurers, attorneys and owners. Our evaluations often included property inspections, testing, engineering analysis and development of repair recommendations. In addition, we have worked with owners to assess and mitigate the risk of failure associated with hazards such as hurricanes, earthquakes, tsunamis and aging infrastructure. We have assessed these risks to industrial facilities, pipelines and nuclear power plant structures. Finally, we continue to pursue activities to address green/sustainable building issues both from a construction as well as human health standpoint to confront major social and economic decisions regarding the relationship between people-environment-profit and the built environment.

Civil Engineering

Our Civil Engineering Practice provides broad expertise that includes geotechnical engineering, geological engineering, engineering geology, and geology to address a host of geo-failures, including landslides, foundation and retaining wall failures, dam and levee failures and earthwork construction claims. We also provide peer review services for complicated structures such as new nuclear power plant construction. Our Water Resources staff specializes in the application of proven hydrologic, hydraulic, hydrodynamic, and sediment transport research and science to provide scientifically sound and cost-effective solutions to our clients.

Over the past year, our consultants have been engaged in a number of investigations related to landslides, retaining wall and foundation failures, pipeline performance, flooding and flood mitigation, and peer review of new nuclear reactor designs. This practice has had a diverse portfolio of projects and clients that represent a broad spectrum of industries.

Construction Consulting

Our Construction Consulting Practice provides project advisory, risk analysis, strategic planning, dispute resolution, and financial damages services. During the past year, we increased the depth and breadth of our expertise by adding experience in the government contract and claim advisory services arena with particular emphasis in aerospace and defense programs. Our multi-disciplinary staff, which includes engineers, architects, construction managers, schedulers, accountants, and technical specialists, provides these services to both the public and private sectors for clients who represent a diverse mix of companies and agencies and are involved in a wide range of projects – from complex construction and capital projects to Department of Defense aerospace and defense procurements.

| 5 |

Our projects include many sectors of the construction industry as well as facilities and systems which include power plants, transmission and distribution facilities, petrochemical facilities, water/wastewater treatment plants, bridges and roads, marine structures, rail systems, tunnels, airports, detention facilities, commercial buildings, institutional buildings, industrial and manufacturing facilities, sporting arenas, resorts and gaming facilities, rotary and fixed-wing aircraft, shipbuilding, missiles, missile defense systems, simulators and space launch vehicles. We provide services to most construction, aerospace and defense industry participants: owners, lending agencies, prime contractors, subcontractors, designers, attorneys and insurance carriers.

Defense Technology Development

Drawing on our multidisciplinary engineering, testing, failure analysis, and prevention expertise, our Defense Technology Development Practice specializes in harnessing advanced technologies and practices from the commercial world to help our defense clients rapidly achieve solutions to their pressing technology integration and development problems. We identify and leverage the best in commercial off-the-shelf technologies to create solutions ranging from fully integrated systems to mission support modules. Our focus is on cost effectiveness, ease of use, reliability, high quality and speed of engineering design and execution. Our engineers and scientists continue to work in Afghanistan war zone laboratories embedded with U.S. and NATO military personnel to ensure we understand their problems and can rapidly deliver solutions to high priority military technology capability gaps.

During the past year we continued to refine our ground penetrating radar (GPR) system to provide a real-time improvised explosive device/mine detection capability for a range of ground vehicles. Internationally, additional GPR system deliveries were made to the U.K. Ministry of Defence for their operationally deployed route clearance capability, and to the Swedish Ministry of Defence for developmental testing. With our U.S. military client, we have continued our work on the development program to deliver next-generation GPR capability and performance. Our sales in the area of ISR (Intelligence, Surveillance and Reconnaissance) have continued with both the Rapid Deployment Integrated Surveillance Systems and the Mid-Range Thermal Imager System for soldiers in Afghanistan, who require increased situational awareness coupled with night vision capabilities. Also over the past year, we have expanded our mission support and technology quality and evaluation services in the areas of personnel identification, radio-frequency identification, physical and logical access control, biometrics, smart credentials, and data analytics for cyber security.

Ecological & Biological Sciences

Our ecological scientists provide strategic support to clients on issues related to natural resources damages associated with chemicals and forest fires, international environmental disputes, ecosystem service assessments for businesses, climate change, ecological risk assessment, novel remediation methods, restoration of wetlands and other natural resources, large development projects, resource utilization (mineral mining, oil and gas, wood pulp), and the use of chemicals and other products in commerce. The practice specializes in assessing the fate and effects of chemical, biological, and physical stressors on aquatic and terrestrial ecosystems. The practice is comprised of nationally recognized experts that cover all disciplines related to the ecological implications and risks associated with these projects.

Electrical Engineering & Computer Science

Our team of electrical engineers and computer scientists performs a wide array of investigations ranging from electric power systems and equipment to integrated circuits, and contributes to safer, more reliable designs in new products. We operate laboratories for testing both heavy equipment and electronics. In addition we have a broad capability in analyzing computer software.

During the past year our electrical engineers and computer scientists continued to broaden our expertise in computer science consulting. Our team expertise encompasses a breadth of areas including information and numerical sciences, algorithms and data structures, computer graphics, computer architecture, networking and communications, as well as security and cryptography. In software, our team experience includes many aspects of software analysis and design ranging from evaluating the intellectual property content of a software product to resolving failures related to embedded processors and machine control. We also perform complex software review, study the interaction of hardware and software layers, as well as evaluate safety and reliability issues related to device control for safety-critical applications such as medical devices.

| 6 |

Engineering Management Consulting

This practice provides multi-disciplinary expertise and rapid response to assist clients with technical and management consulting services, often in extremely short time frames. Our consultants provide services in the areas of asset strategy and planning, project management, engineering, construction, maintenance, operations, environmental, and risk analysis. This practice primarily services the electric and gas utility industries, focusing on transmission and distribution as well as fossil fuel and nuclear generation.

We provide unique and advanced services in performing risk and reliability assessments. Our scientists and engineers assist our clients in minimizing bottom-line losses in their business or operation. Accidents, unanticipated events, and system failures are the primary causes of deferred or lost production interruptions and may lead to loss of life, injury, property damage, and undesired releases. Our multi-disciplinary staff has performed diverse technical, business-interruption, and compliance-related risk and reliability assessments for chemical, petrochemical, petroleum, and manufacturing clients worldwide.

Environmental & Earth Sciences

Our environmental scientists and engineers provide cost-effective, scientifically defensible and realistic assessments and solutions to complex environmental issues. We offer technical, regulatory and litigation support to industries that include manufacturing, mining and minerals, oil and gas, chemicals, forest products, railroads, aerospace, and trade associations. Our consultants specialize in the areas of environmental chemistry and forensics, hydrogeology, air toxics, modeling and monitoring, remediation consulting, environmental engineering and waste management, and evaluation of environmental and social risks for large international capital projects. Our work often involves complex and high visibility environmental scenarios, claims, or toxic tort matters, where evaluation of contamination and historical reconstruction of events, releases, and doses are central to problem resolution.

Health Centers

Center for Chemical Regulation & Food Safety

Our Center for Chemical Regulation and Food Safety includes experienced staff of both technical and regulatory specialists who are experienced in dealing with foods, and with pesticide and non-pesticide products including conventional chemicals, biochemicals, microbials, biocides, products of biotechnology, and industrial chemicals. We provide practical, creative, scientific and regulatory support to meet global business objectives at every stage of the product cycle, from research and development to retail and beyond.

During the past year our chemical regulation & food safety staff have conducted a wide array of work. The European side of our business was involved with many projects related to plant protection product regulatory submissions, from new active substances to product-specific dossiers for individual member states. In addition, we provided many specialist assessments relating to human and environmental exposure and product efficacy. The first work for the next REACH submission deadline in 2013 also began. REACH (Registration, Evaluation, Authorisation and Restriction of Chemical substances) is the European Union chemicals policy that requires all new substances supplied at greater than 1 tonne (approx. 2,205 lbs.) per year to be registered. In the U.S. we continued to provide services related to pesticide product development and new U.S. product registration, registration review, due diligence, and data compensation, as well as the approval of new pesticide inert ingredients and new non-pesticide chemical approvals. Our food safety consultants assisted clients with food additives, food contact notifications, and nutrition-related analyses, as well as product recall and litigation support.

| 7 |

Center for Epidemiology, Biostatistics & Computational Biology

Our health scientists apply epidemiology to examine and address complex health issues in a variety of settings. Through the principles of epidemiology, we analyze the interaction of host, agent, and environment to reach conclusions about the causes and occurrence of disease in human populations.

Our consultants combine the expertise of several medical specialties, exposure assessment professionals, and other scientists who have advanced degrees in statistics and public health. All of our physicians have graduate training in epidemiology and biostatistics. Our research work has included numerous community health assessments, disease cluster investigations, survey research, occupational cohort and case-control studies, exposure assessment studies, cancer modeling, meta-analyses, and state of the art reviews.

Our health economics and outcomes research scientists determine the value of new medical technologies. We specialize in evaluating the impact of pharmaceuticals, medical devices, biotechnology products, and diagnostics on treatment patterns, medical care resource utilization, and health care costs; we assess the changes in health outcomes that result from new medical technologies, including decreased mortality, reduced disease cases or symptoms, improved quality of life, and increased patient satisfaction; and we quantify changes in health outcomes relative to their costs and to the costs of competing health care interventions, allowing assessment of the appropriate value for these new medical technologies.

Center for Exposure Assessment & Dose Reconstruction

Exposure assessment is the science of estimating human exposure to chemical, physical, and biological agents, accounting for the frequency, magnitude, and duration of the exposure events. Exposure estimates can be compared to toxicity benchmarks or guidelines to assess potential risks to human health, and provide critical inputs to human epidemiology studies, risk assessment, and regulatory compliance.

During the past year we expanded our capabilities in air quality and atmospheric sciences with the addition of staff that provide air quality and meteorological modeling, permitting, and licensing support services. They investigate potential and accidental releases of chemicals to the atmosphere, simulate transport and fate of chemical substances, and develop measures of prevention and control, such as emergency preparedness and response. Our atmospheric scientists work closely with our thermal and process engineers to predict and evaluate the dispersion of air emissions, and work with our risk assessors to evaluate health risks posed by atmospheric releases to the ambient air and to indoor environments.

Center for Occupational Medicine & Environmental Health

This center is composed of industrial hygienists, safety professionals, physicians, and scientists, with specialized training in the anticipation, recognition, evaluation, risk assessment, and control of human health hazards.

Our staff has partnered with and assisted clients with health-related issues involving workers, products, and manufacturing processes, and issues concerning communities and the environment. We draw on the expertise and resources of staff located throughout the U.S. Our team includes senior physicians and experienced health scientists specializing in the fields of epidemiology, industrial hygiene, toxicology, safety, occupational health, veterinary medicine and engineering. This unique multidisciplinary team provides the necessary insight to address complex health issues facing businesses, corporations, property owners and others. We help to investigate a broad variety of environmental health concerns, such as evaluating claims of illnesses from environmental exposures to chemicals, dusts, molds and micro-organisms, and we develop strategies to aid in controlling such exposures, when needed. We also have assisted clients with their preventive health program needs in the workplace and provide external verification of health services performance. Common medical conditions, if not managed well, can erode worker productivity and have consequent effects on the competitiveness of an enterprise.

| 8 |

Center for Toxicology & Mechanistic Biology

We have exceptional expertise and depth in toxicology and mechanistic biology. We provide knowledge and experience that improves decisions affecting the regulation of important substances in commerce. We work with our clients to resolve important issues that affect the safe use of a wide variety of substances. We evaluate the mechanisms by which substances can affect complex biological systems, provide perspectives on potential effects at realistic human and environmental exposure levels, and develop strategies to manage human health and environmental risks. We are recognized for our outstanding credentials and decades of experience from government, academia and industry.

During the past year we continued to provide toxicology and clinical toxicology support in nearly all phases of pharmaceutical and combination drug development from preclinical studies to post-marketing safety assessments. We reviewed existing data and developed new studies on potential endocrine toxicity of chemical substances. Our radiation toxicologists evaluated contamination levels at several Japanese facilities in the Fukushima area after the March 2011, earthquake and subsequent tsunami. We are also extremely active in the research related to the identification, assessment, and prioritization of risks (the probability of adverse effects) associated with engineered nanomaterial development and manufacturing processes.

Human Factors

Our Human Factors staff evaluates human performance and safety in product and system use. Our consultants study how the limitations and capabilities of people, including memory, perception, reaction time, judgment, physical size and dexterity, affect the way they use a product, interact with an organization or environment, process information or participate in an activity.

During the past year our scientists evaluated the human performance issues and behaviors that may have contributed to accident causation. We addressed the reliability of human memory and retrospective reporting in the gathering of fact-based evidence. We continued to review warnings and labeling issues related to consumer products, pharmaceuticals, motor vehicles, medical devices and industrial products. In addition, we assisted manufacturers with compliance of regulatory guidelines related to products and worked with them regarding the Consumer Product Safety Commission’s new publicly available consumer product safety database.

Industrial Structures

Our Industrial Structures Practice, based in Düsseldorf, Germany, specializes in design and assessment of industrial structures subject to extreme conditions. Our Düsseldorf office has provided design reviews and assessments on more than 1,000 structures around the world, and our staff has participated in the creation of several engineering standards.

Our Industrial Structures Practice provides planning, assessment, rehabilitation and dismantling analysis of bearing structures in four particular areas: antenna masts, power plants, buildings and special structures like refractories or tanks. One service we provide in over 800 locations throughout the year is quality assurance of antenna masts for a variety of facilities including telecommunications, wind energy and industrial chimneys. Our consultants provide inspection services related to new construction and assess design deficiencies related to new and existing facilities, as well as assist our clients with on-time, quality construction on their projects.

With the use of our self-developed computer software for non-linear material behavior, close-to-reality assessment of a wide variety of structures such as cracked reinforced concrete structures, multi-layer refractories or masonry towers is provided. Beyond industrial structures more and more commercial property projects are becoming part of this practice.

| 9 |

Materials & Corrosion Engineering

Our in-depth knowledge of materials and electrochemistry, combined with the breadth of collective expertise in many areas of engineering and science, is used to understand how and why materials fail, as well as to prevent future failures. Our engineers and scientists use their broad background in field investigations, root-cause assessments, and materials engineering to solve complex problems for both industrial and legal clients. During the past year we conducted failure analysis, failure prevention, and integrity assessment investigations for a wide variety of clients including medical, aerospace, chemical processing, pipeline, automotive, construction, consumer electronics, recreational, and other industries.

Mechanical Engineering

We provide clients with a thorough comprehension of current or alternative designs to determine potential vulnerabilities before failures occur, develop appropriate risk mitigation methods, and provide post failure investigations. Our consultants review the safety and reliability of processes and products for a variety of industries, including transportation, heavy industry, energy, and consumer products. Our scientists and engineers also provide services in the area of intellectual property and are often asked to interpret the language of a patent from a scientific and engineering perspective and provide valuable insight regarding the proper technical interpretation of patent claims. During the past year our mechanical engineers worked on a wide variety of projects ranging from high profile consumer product recall investigations to pipeline integrity evaluations and worker safety issues. Our staff developed and utilized detailed, validated computational models to evaluate equipment, consumer products and medical devices to solve a variety of technical challenges associated with their design and optimization.

Polymer Science & Materials Chemistry

Our polymer science and materials chemistry staff consults with industrial, government, and insurance clients, as well as their outside counsels, regarding polymers used in diverse applications and chemical aspects of batteries, drug delivery systems, and other products that depend on highly controlled manufacturing environments. We assist clients in understanding the short- and long-term performance of plastic, rubber, adhesive, coating, composite and power systems when challenged by physical, chemical, thermal and other operational stresses. During the past year we added key members to our staff with expertise in performance textiles, engineering plastics, and materials for medical applications. We also increased our presence in our China office and added staff in our new Atlanta office. We continue to work on a number of projects in which polymers and chemistry are important to the performance of medical devices, food packaging, high-performance coatings, utilities and infrastructure, energy and power systems, and general consumer products.

Statistical & Data Sciences

Our Statistical & Data Sciences staff comprises our company’s core capabilities in statistical methodology and offers its expertise to serve clients at any and all stages of the empirical research process including product development, manufacturing, and regulatory stages. The practice specializes in determining whether a particular activity or product poses an unreasonable risk. Risk estimation involves establishing a reference period and then collecting information about the number of injuries (or other adverse events) suffered and the amount of exposure during this period. Through analysis and synthesis of client-supplied data, combined with information from public sources, we help clients measure their own risk in the context of similar risks and determine appropriate courses of action. During the past year, we worked on a variety of projects for government, industry, and legal clients. Our statisticians and data scientists performed assessments of manufacturing quality systems, investigated data mining methods to improve classification tools, and analyzed the reliability of home appliances during use by consumers.

Thermal Sciences

We have investigated and analyzed thousands of fires and explosions ranging from high loss disasters at manufacturing facilities to small insurance claims. Information gained from these analyses has helped us assist clients in assessing preventive measures related to the design of their products. Based on our investigation experience, we also assist industry to minimize their risk of fires and explosions, provide regulatory consulting for permitting new industrial facilities, and assist manufacturers in addressing allegations of the risk of fires associated with consumer products. Our engineers use fire modeling and other computational fire dynamics modeling tools to supplement our analytical, experimental, and field-based activities. Preventive services include process safety hazard analysis for the chemical and oil and gas industries, fire protection engineering and dust explosion consulting.

| 10 |

During the past year, in the context of consumer product safety, our staff reviewed lithium-ion battery technology, its failure modes and past failure history, and studied the life cycle of the storage and distribution of batteries. This work was conducted on behalf of the Fire Protection Research Foundation, a part of the National Fire Protection Association. The review laid out a research approach for evaluating and identifying battery storage facility fire protection strategies. This is part of a larger study of the hazards associated with lithium-ion battery storage, with an aim of developing fire protection strategies to protect battery and battery-powered products, bulk storage and distribution facilities.

Vehicle Analysis

We have performed thousands of investigations for the automotive, trucking, recreational vehicle, marine, aviation, aerospace, and rail industries. Information gained from these analyses has assisted clients in assessing preventive measures related to the design of their products, as well as evaluating failures.

Our Test and Engineering Center located in Phoenix, Arizona, is the setting for our most complex tests, along with rigorous analysis of results. We have gained a worldwide reputation for our ability to mobilize resources expeditiously and efficiently, integrate a broad array of technical disciplines, and provide valuable insight that is objective and withstands rigorous scrutiny. Many of our projects involve addressing the cause of accidents. Our clients rely on us to determine what happened in an accident and why it happened. In many cases, they also want us to discover what could have been done to reduce the severity of the accident or to reduce injuries to those involved. Whether the objective is design analysis, component testing, or accident reconstruction, our knowledge of vehicle systems and accident reconstruction principles and our experience from conducting full-scale tests add insight and proficiency to every project.

COMPETITION

The marketplace for our services is fragmented and we face different sources of competition in providing various services. In addition, the services that we provide to some of our clients can be performed in-house by those clients. Clients that have the capability to perform such services themselves will retain Exponent or other independent consultants because of independence concerns.

In each of the foregoing practices and centers, we believe that the principal competitive factors are: technical capability and breadth of services, ability to deliver services on a timely basis, professional reputation and knowledge of the litigation and regulatory processes. Although we believe that we generally compete favorably in each of these areas, some of our competitors may be able to provide services acceptable to our clients at lower prices.

We believe that the barriers to entry are low and that for many of our technical disciplines, competition is increasing. In response to competitive forces in the marketplace, we continue to explore new markets for our various technical disciplines.

BUSINESS SEGMENTS OVERVIEW

We report two operating segments based on two primary areas of service. One operating segment is a broad service group providing technical consulting in different practices primarily in the areas of engineering and technology development. Our other operating segment provides services in the area of environmental, epidemiology and health risk analysis. This operating segment provides a wide range of consulting services relating to environmental hazards and risks and the impact on both human health and the environment. For more information about the financial condition and results of operations of each segment, please see Part II - “Item 7: Management's Discussion and Analysis of Financial Condition and Results of Operations” and “Item 8: Financial Statements and Supplementary Data.”

EMPLOYEES

As of December 30, 2011, we employed 937 full-time and part-time employees, including 682 engineering and scientific staff, 80 technical support staff and 175 administrative and support staff. Our staff includes 600 employees with advanced degrees, of which 385 employees have achieved the level of Ph.D., Sc.D. or M.D.

ADDITIONAL INFORMATION

The address of our internet website is www.exponent.com. We make available, free of charge through our website, access to our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and other periodic Securities and Exchange Commission (SEC) reports, along with amendments to all of those reports, as soon as reasonably practicable after we file the reports with the SEC. Additionally, copies of materials filed by us with the SEC may be accessed at the SEC’s Public Reference Room at 100 F Street NE, Washington, D.C. or at the SEC’s website at http://www.sec.gov. For information about the SEC’s Public Reference Room, the public may contact 1-800-SEC-0330. Copies of material filed by us with the SEC may also be obtained by writing to us at our corporate headquarters, Exponent, Inc., Attention: Investor Relations, 149 Commonwealth Drive, Menlo Park, CA 94025, or by calling (650) 326-9400. The content of our internet website is not incorporated into and is not part of this Annual Report on Form 10-K.

| 11 |

EXECUTIVE OFFICERS

The executive officers of Exponent and their ages as of February 24, 2012 are as follows:

| Name | Age | Position |

| Paul R. Johnston, Ph.D. | 58 | President, Chief Executive Officer and Director |

| Elizabeth L. Anderson, Ph.D. | 71 | Group Vice President |

| Paul D. Boehm, Ph.D. | 63 | Group Vice President |

| Robert D. Caligiuri, Ph.D. | 60 | Group Vice President |

| Robert C. Lange | 64 | Group Vice President |

| Subbaiah V. Malladi, Ph.D. | 65 | Chief Technical Officer |

| John E. Moalli, Sc.D. | 47 | Group Vice President |

| John D. Osteraas, Ph.D. | 57 | Group Vice President |

| Richard L. Schlenker, Jr. | 46 | Executive Vice President, Chief Financial Officer and Corporate Secretary |

Executive officers of Exponent are appointed by the Board of Directors and serve at the discretion of the Board or until the appointment of their successors. There is no family relationship between any of the directors and officers of the Company.

Paul R. Johnston, Ph.D., joined the Company in 1981, was promoted to Principal Engineer in 1987, and to Vice President in 1996. In 1997, he assumed responsibility for the firm’s network of offices. In July 2003, he was appointed Chief Operating Officer and added responsibility for the Health and Environmental Groups. In 2006, he assumed line responsibility for all of the firm’s consulting groups. Dr. Johnston was named President in May 2007. He was named Chief Executive Officer and elected to the Board of Directors in May 2009. Dr. Johnston received his Ph.D. (1981) in Civil Engineering and M.S. (1977) in Structural Engineering from Stanford University. He received his B.A.I. (1976) in Civil Engineering with First Class Honors from Trinity College, University of Dublin, Ireland where he was elected a Foundation Scholar in 1975. Dr. Johnston is a Registered Professional Civil Engineer in the State of California and a Chartered Engineer in Ireland.

Elizabeth L. Anderson, Ph.D., joined the Company in June 2006 as a Group Vice President and Principal Scientist. Prior to joining Exponent, Dr. Anderson was President and CEO of Sciences International, a health and environmental consulting firm. Dr. Anderson received her Ph.D. (1970) in Organic Chemistry from The American University, M.S. (1964) in Organic Chemistry from the University of Virginia and B.S. (1962) in Chemistry from the College of William and Mary. Dr. Anderson is a Fellow of the Academy of Toxicological Sciences, a founder and past-President of the Society for Risk Analysis and Editor-in-Chief of the journal, Risk Analysis: An International Journal.

Paul D. Boehm, Ph.D., joined the Company in April 2004 as a Group Vice President and Principal Scientist. Prior to joining the Company, Dr. Boehm was Vice President and Market Manager, Oil and Gas Sector, at Battelle Memorial Institute from 2001 to 2004. From 1999 to 2001, Dr. Boehm was Vice President and Managing Director, Environmental Health and Safety Consulting at Arthur D. Little, Inc. Dr. Boehm received his Ph.D. (1977) and M.S. (1973) in Oceanography from the University of Rhode Island and B.S. (1970) in Chemical Engineering from the University of Rochester. Dr. Boehm has published more than 100 articles in peer-reviewed journals and authored numerous reports on environmental forensics and impact assessments. Dr. Boehm has been chosen to serve on several National Research Council panels.

| 12 |

Robert D. Caligiuri, Ph.D., joined the Company in 1987. He was promoted to Principal Engineer in 1990 and Group Vice President in 1999. Dr. Caligiuri received his Ph.D. (1977) and M.S. (1974) in Materials Science and Engineering from Stanford University and B.S. (1973) in Mechanical Engineering from the University of California, Davis. Prior to joining the Company he was a Program Manager and Materials Scientist for SRI International. He is a Registered Professional Metallurgical Engineer in the States of California, Utah, Michigan and North Carolina and a Fellow of the American Society for Materials.

Robert C. Lange worked for the Company from 1982 to 1994. During this period, he was promoted to Principal Engineer and Vice President in 1985. Mr. Lange rejoined Exponent in November 2008 as Group Vice President and Principal Engineer. From 1994 to 2008, Mr. Lange was Executive-In-Charge, Engineering Director, and Executive Director Vehicle Structure and Safety Integration at General Motors Corporation. Mr. Lange received his M.S. (1975) and B.S. (1969) in Mechanical Engineering from the University of Michigan. Mr. Lange is a past Director of the National Safety Council. Mr. Lange is a member of the Transportation Research Board Advisory Committee for Congressional Report on the Strategic Highway Research Plan, SHRP-2 and a past member of the Board of Directors of the National Safety Council. He was Chair of the Society of Automotive Engineers’ Motor Vehicle Systems Board from 2004 to 2008.

Subbaiah V. Malladi, Ph.D., joined the Company in 1982 as a Senior Engineer, becoming a Senior Vice President in January 1988 and a Corporate Vice President in September 1993. In October 1998, Dr. Malladi was appointed Chief Technical Officer of the Company. Dr. Malladi also served as a Director of the Company from March 1991 through September 1993. He was re-appointed as a Director in April 1996 and served on the Board until May 2005. He received a Ph.D. (1980) in Mechanical Engineering from the California Institute of Technology, M.Tech (1972) in Mechanical Engineering from the Indian Institute of Technology, B.E. (1970) in Mechanical Engineering from SRI Venkateswara University, India and B.S. (1966) in Physics, Chemistry and Mathematics from Osmania University, India. Dr. Malladi is a Registered Professional Mechanical Engineer in the State of California.

John E. Moalli, Sc.D., joined the Company in 1992. He was promoted to Principal in 1997, served as an Office and Practice Director and became Group Vice President in 2002. Dr. Moalli received his Sc.D. (1992) in Polymers from the Massachusetts Institute of Technology and B.S. (1987) in Civil Engineering from Northeastern University. Dr. Moalli is a nationally recognized expert in polymetric materials and has an academic appointment at Stanford University.

John D. Osteraas, Ph.D., worked for the Company from 1982 to 1985 as a Senior Engineer. He rejoined the Company in 1990 as a Managing Engineer. He was promoted to Principal Engineer in 1992 and Group Vice President in 2006. Dr. Osteraas received his Ph.D. (1990) in Civil Engineering, M.S. (1977) in Civil Engineering: Structural Engineering from Stanford University and B.S. (1976) in Civil and Environmental Engineering from the University of Wisconsin. Dr. Osteraas is a Registered Professional Engineer in 13 states and is a Fellow of the American Society of Civil Engineers.

Richard L. Schlenker, Jr. joined the Company in 1990. Mr. Schlenker is the Executive Vice President, Chief Financial Officer and Corporate Secretary of the Company. He was appointed Executive Vice President in April 2010, Chief Financial Officer in July 1999 and Secretary of the Company in November 1997. Mr. Schlenker was the Director of Human Resources from 1998 until his appointment as Chief Financial Officer. He was the Manager of Corporate Development from 1996 until 1998. From 1993 to 1996, Mr. Schlenker was a Business Manager, where he managed the business activities for multiple consulting practices within the Company. Prior to 1993, he held several different positions in finance and accounting within the Company. Mr. Schlenker holds a B.S. in Finance from the University of Southern California.

Item 1A. Risk Factors

Exponent operates in a rapidly changing environment that involves a number of uncertainties, some of which are beyond our control. These uncertainties include, but are not limited to, those mentioned elsewhere in this report and those set forth below.

Lack of sizable backlog may lead to less predictable, and perhaps lower, future revenues.

Revenues are primarily derived from services provided in response to client requests or events that occur without notice, and engagements, generally billed as services are performed, are terminable or subject to postponement or delay at any time by clients. As a result, backlog at any particular time is small in relation to our quarterly or annual revenues and is not a reliable indicator of revenues for any future periods. Revenues and operating margins for any particular quarter are generally affected by staffing mix, resource requirements and timing and size of engagements.

| 13 |

Failure to attract and retain key employees may adversely affect our business.

Exponent’s business involves the delivery of professional services and is labor-intensive. Our success depends in large part upon our ability to attract, retain and motivate highly qualified technical and managerial personnel. Qualified personnel are in great demand and are likely to remain a limited resource for the foreseeable future. We cannot provide any assurance that we can continue to attract sufficient numbers of highly qualified technical and managerial personnel and to retain existing employees. The loss of key managerial employees, business generators or any significant number of employees could have a material adverse impact on our business, including our ability to secure and complete engagements.

Competition could reduce our pricing and adversely affect our business.

The markets for our services are highly competitive. In addition, there are relatively low barriers to entry into our markets and we have faced, and expect to continue to face, additional competition from new entrants into our markets. Competitive pressure could reduce the market acceptance of our services and result in price reductions that could have a material adverse effect on our business, financial condition or results of operations.

The loss of a large client could adversely affect our business.

We currently derive a significant portion of our revenues from clients in the consumer electronics, insurance, petrochemical, transportation, and utilities industries and the government sector. The loss of any large client, organization or insurer could have a material adverse effect on our business, financial condition or results of operations.

Our business can be adversely affected by downturns in the overall economy.

The markets that we serve are cyclical and subject to general economic conditions. The direction and relative strength of the global economy continues to be uncertain. If the economic growth in the United States, where we primarily operate, continues to be slow and not improve, our clients may consolidate or go out of business and thus demand for our services could be reduced significantly.

Our clients may be unable to pay for our services.

If a client's financial difficulties become severe, the client may be unwilling or unable to pay our invoices in the ordinary course of business, which could adversely affect collections of both our accounts receivable and unbilled services. On occasion, some of our clients have entered bankruptcy, which has prevented us from collecting amounts owed to us. The bankruptcy of a client with substantial accounts receivable could have a material adverse effect on our financial condition and results of operations.

We hold substantial investments that could present liquidity risks.

Our cash equivalent and short-term investment portfolio as of December 30, 2011, consisted primarily of obligations of state and local government agencies and the U.S. Treasury. We follow an established investment policy to monitor, manage and limit our exposure to interest rate and credit risk. The policy sets forth credit quality standards and limits our exposure to any one issuer, as well as our maximum exposure to various asset classes.

As a result of current adverse financial market conditions, investments in some financial instruments may pose risks arising from liquidity and credit concerns. As of December 30, 2011, we had no impairment charge associated with our investment portfolio relating to such adverse financial market conditions. Although we believe our current investment portfolio has a low risk of impairment, we cannot predict future market conditions or market liquidity and can provide no assurance that our investment portfolio will remain unimpaired.

Our business is dependent on our professional reputation.

The professional reputation of Exponent and its consultants is critical to our ability to successfully compete for new client engagements and attract or retain professionals. Proven or unproven allegations against us may damage our professional reputation. Any factors that damage our professional reputation could have a material adverse effect on our business.

| 14 |

Our business can be adversely impacted by deregulation or reduced regulatory enforcement.

Public concern over health, safety and preservation of the environment has resulted in the enactment of a broad range of environmental and/or other laws and regulations by local, state and federal lawmakers and agencies. These laws and the implementing of new regulations affect nearly every industry, as well as the agencies of federal, state and local governments charged with their enforcement. To the extent changes in such laws, regulations and enforcement or other factors significantly reduce the exposures of manufacturers, owners, service providers and others to liability, the demand for our services may be significantly reduced.

Tort reform can reduce demand for our services.

Several of our practices have a significant concentration in litigation support consulting services. To the extent tort reform reduces the exposure of manufacturers, owners, service providers and others to liability, the demand for our litigation support consulting services may be significantly reduced.

Our quarterly results may vary.

Variations in our revenues and operating results occur from time to time, as a result of a number of factors, such as the significance of client engagements commenced and completed during a quarter, the timing of engagements, the number of working days in a quarter, employee hiring and utilization rates, and integration of companies acquired. Because a high percentage of our expenses, particularly personnel and facilities related expenses, are relatively fixed in advance of any particular quarter, a variation in the timing of the initiation or the completion of our client assignments can cause significant variations in operating results from quarter to quarter.

Our engagements may result in professional or other liability.

Our services typically involve difficult engineering and scientific assignments and carry risks of professional and other liability. Many of our engagements involve matters that could have a severe impact on a client's business, cause a client to lose significant amounts of money, or prevent a client from pursuing desirable business opportunities. Accordingly, if a client is dissatisfied with our performance, the client could threaten or bring litigation in order to recover damages or to contest its obligation to pay our fees. Litigation alleging that we performed negligently, disclosed client confidential information, lost or damaged evidence, infringed on patents, or otherwise breached our obligations to a client could expose us to significant liabilities to our clients or other third parties or tarnish our reputation.

Potential conflicts of interests may preclude us from accepting some engagements.

We provide litigation support consulting and other services primarily in connection with significant disputes, or other matters that are usually adversarial or that involve sensitive client information. The nature of our consulting services may preclude us from accepting engagements with other potential clients because of conflicts. Accordingly, the nature of our business limits the number of both potential clients and potential engagements.

The market price of our common stock may be volatile.

Many factors could cause the market price of our common stock to rise and fall. These include the risk factors listed above, changes in estimates of our performance or recommendations by securities analysts, future sales of shares of common stock in the public market, market conditions in the industry and economy as a whole, acquisitions or strategic alliances involving us or our competitors, restatement of financial results and changes in accounting principles or methods. In addition, the stock market often experiences significant price fluctuations. These fluctuations are often unrelated to the operating performance of particular companies. These broad market fluctuations may adversely affect the market price of our common stock. When the market price of a company's stock drops significantly, shareholders often institute securities class action litigation against that company. Any litigation against us could cause us to incur substantial costs, divert the time and attention of our management and other resources, or otherwise harm our business.

| 15 |

Impairment of goodwill may require us to record a significant charge to earnings.

On our balance sheet, we have $8,607,000 of goodwill subject to periodic evaluation for impairment. Failure to achieve sufficient levels of cash flow at reporting units, the loss of key employees, changes to the scope of operations of our business or a significant and sustained decline in our stock price could result in goodwill impairment charges. During times of financial market volatility, significant judgment is required to determine the underlying cause of the decline and whether stock price declines are short-term in nature or indicative of an event or change in circumstances.

Impairment of long-lived assets or restructuring activities may require us to record a significant charge to earnings.

Our long-lived assets, including our office and laboratory space in Menlo Park, California and our test and engineering center in Phoenix, Arizona, are subject to periodic testing for impairment. Failure to achieve sufficient levels of cash flow at reporting units could result in impairment of our long-lived assets. In addition, we have operating lease commitments for office, warehouse and laboratory space of $20,542,000 as of December 30, 2011. Changes in the business environment could lead to changes in the scope of operations of our business. These changes, including the closure of one or more offices, could result in restructuring and/or asset impairment charges.

Our international operations create special risks that could adversely affect our business.

In addition to our offices in the United States, we have physical offices in the United Kingdom, Germany, Switzerland and China and conduct business in several other countries. We expect to continue to expand globally and our international revenues may account for an increasing portion of our revenues in the future. Our international operations carry special financial, business and legal risks, including cultural and language differences; employment laws and related factors that could result in lower utilization, higher staffing costs, and cyclical fluctuations of utilizations and revenues; currency fluctuations that adversely affect our financial position and operating results; burdensome regulatory requirements and other barriers to conducting business; managing the risks associated with engagements with foreign officials and governmental agencies, including the risks arising from the Foreign Corrupt Practices Act; greater difficulties in managing and staffing foreign operations; successful entry and execution in new markets; restrictions on the repatriation of earnings, and potentially adverse tax consequences.

Inherent risks related to government contracts may adversely affect our business.

We work for various United States and foreign governmental entities and agencies. Government entities reserve the right to audit our contracts and conduct inquiries and investigations of our business practices with respect to government contracts. Findings from an audit may result in fees being refunded to the government or prospective adjustment to previously agreed upon rates that will affect future margins. If a government client discovers improper or illegal activities in the course of audits or investigations, we may become subject to various civil and criminal penalties and administrative sanctions, which may include termination of contracts, forfeiture of profits, suspension of payments, fines and suspensions or debarment from doing business with other agencies of the government. The inherent limitations of internal controls may not prevent or detect all improper or illegal activities, regardless of the adequacy of such controls. Government contracts, and the proceedings surrounding them, are often subject to more extensive scrutiny and publicity than other commercial contracts. Negative publicity related to our government contracts, regardless of whether it is accurate, may further damage our business by affecting our ability to compete for new contracts.

Item 1B. Unresolved Staff Comments

None.

| 16 |

Item 2. Properties

Our Silicon Valley office facilities consist of a 153,738 square foot building, with office and laboratory space located on a 6.3-acre tract of land we own in Menlo Park, California and an adjacent 27,000 square feet of leased warehouse storage space.

Our Test and Engineering Center (TEC) occupies 147 acres in Phoenix, Arizona. We lease this land from the state of Arizona under a 30-year lease agreement that expires in January 2028 and have options to renew for two fifteen-year periods. We constructed an indoor test facility as well as an engineering and test preparation building at the TEC.

In addition, we lease office, warehouse and laboratory space in 18 other locations in 13 states and the District of Columbia, as well as in Germany, China, Switzerland and the United Kingdom. Leases for these offices, warehouse and laboratory facilities have terms generally ranging between one and ten years. Aggregate lease expense in fiscal 2011 for all leased properties was $5,180,000.

Item 3. Legal Proceedings

Exponent is not engaged in any material legal proceedings.

Item 4. Mine Safety Disclosures

Not applicable.

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Exponent’s common stock is traded on the NASDAQ Global Select Market, under the symbol “EXPO”. The following table sets forth for the fiscal periods indicated the high and low sales prices for our common stock.

| Stock prices by quarter | High | Low | ||||||

| Fiscal Year Ended December 31, 2010: | ||||||||

| First Quarter | $ | 29.94 | $ | 25.13 | ||||

| Second Quarter | $ | 33.92 | $ | 26.71 | ||||

| Third Quarter | $ | 35.00 | $ | 28.36 | ||||

| Fourth Quarter | $ | 41.26 | $ | 30.87 | ||||

| Fiscal Year Ended December 30, 2011: | ||||||||

| First Quarter | $ | 45.53 | $ | 35.06 | ||||

| Second Quarter | $ | 45.53 | $ | 39.86 | ||||

| Third Quarter | $ | 47.93 | $ | 35.56 | ||||

| Fourth Quarter | $ | 51.17 | $ | 38.13 | ||||

As of February 17, 2012, there were 332 holders of record of our common stock. Because many of the shares of our common stock are held by brokers and other institutions on behalf of stockholders, we believe that there are considerably more beneficial holders of our common stock than record holders.

We have never paid cash dividends on our common stock. See Item 7 of Part II “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Liquidity and Capital Resources.”

| 17 |

The following table provides information on the Company’s share repurchases (of Company common stock) for the quarter ended December 30, 2011 (in thousands, except price per share):

| Total Number of Shares Purchased | Average Price Paid Per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | Approximate Dollar Value of Shares That May Yet Be Purchased Under the Plan or Program | |||||||||||||

| October 1 to October 28 | 25 | $ | 40.75 | 25 | $ | 9,627 | ||||||||||

| October 29 to November 25 | - | - | - | $ | 9,627 | |||||||||||

| November 26 to December 30 | 5 | $ | 44.01 | 5 | $ | 9,406 | ||||||||||

| Total | 30 | $ | 41.30 | 30 | ||||||||||||

On February 9, 2012, the Company’s Board of Directors authorized an additional $35 million for the repurchase of the Company’s common stock.

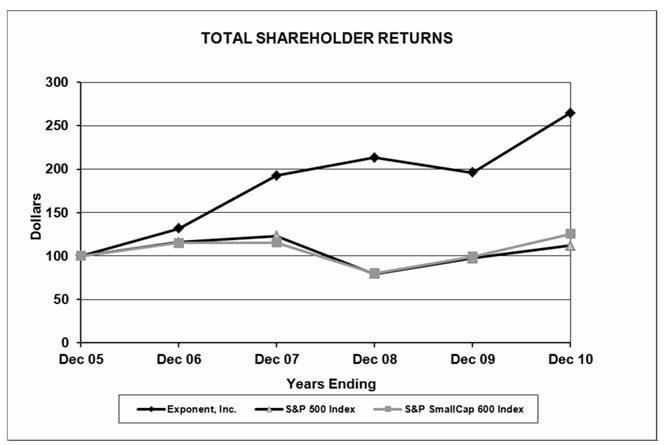

COMPANY STOCK PRICE PERFORMANCE GRAPH

The graph compares the Company’s cumulative total stockholder return calculated on a dividend-reinvested basis from 2006 through 2011 with those of the Standard & Poor’s (“S&P”) 500 Index and the S&P SmallCap 600 Index. The Company does not have a comparable peer group and thus has selected the S&P Small Cap 600 Index. The graph assumes that $100 was invested on the last day of 2006. Note that the historic stock price performance is not necessarily indicative of future stock price performance.

| 18 |

Item 6. Selected Financial Data

The following selected consolidated financial data are derived from our consolidated financial statements. This data should be read in conjunction with the consolidated financial statements and notes thereto, and with Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations.

| Fiscal Year | ||||||||||||||||||||

| (In thousands, except per share data) | 2011 | 2010 | 2009 | 2008 | 2007 | |||||||||||||||

| Consolidated Statements of Income Data: | ||||||||||||||||||||

| Revenues before reimbursements | $ | 246,667 | $ | 221,860 | $ | 205,714 | $ | 206,194 | $ | 183,139 | ||||||||||

| Revenues | $ | 272,446 | $ | 248,753 | $ | 227,882 | $ | 228,838 | $ | 205,148 | ||||||||||

| Operating income | $ | 53,460 | $ | 43,241 | $ | 33,262 | $ | 36,722 | $ | 29,944 | ||||||||||

| Net income | $ | 32,695 | $ | 27,521 | $ | 22,127 | $ | 23,160 | $ | 20,341 | ||||||||||

| Net income per share: | ||||||||||||||||||||

| Basic | $ | 2.31 | $ | 1.92 | $ | 1.56 | $ | 1.57 | $ | 1.36 | ||||||||||

| Diluted | $ | 2.22 | $ | 1.83 | $ | 1.47 | $ | 1.47 | $ | 1.25 | ||||||||||

| Consolidated Balance Sheet Data: | ||||||||||||||||||||

| Cash and cash equivalents | $ | 84,439 | $ | 106,549 | $ | 67,895 | $ | 32,598 | $ | 10,700 | ||||||||||

| Short-term investments | $ | 25,260 | $ | - | $ | 7,490 | $ | 24,772 | $ | 53,034 | ||||||||||

| Working capital | $ | 137,803 | $ | 136,860 | $ | 103,253 | $ | 82,073 | $ | 88,794 | ||||||||||

| Total assets | $ | 268,788 | $ | 258,892 | $ | 206,481 | $ | 183,090 | $ | 182,391 | ||||||||||

| Long-term liabilities | $ | 21,298 | $ | 17,358 | $ | 11,333 | $ | 6,761 | $ | 6,509 | ||||||||||

| Total stockholders’ equity | $ | 186,715 | $ | 183,800 | $ | 150,071 | $ | 128,094 | $ | 131,919 | ||||||||||

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

OVERVIEW

Exponent, Inc. is a science and engineering consulting firm that provides solutions to complex problems. Our multidisciplinary team of scientists, physicians, engineers, business and regulatory consultants brings together more than 90 different technical disciplines to solve complicated issues facing industry and government today. Our services include analysis of products, people, property, processes and finances related to litigation, product recall, regulatory compliance, research, development and design.

CRITICAL ACCOUNTING ESTIMATES

In preparing our consolidated financial statements, we make assumptions, judgments and estimates that can have a significant impact on our revenue, operating income and net income, as well as on the value of certain assets and liabilities on our consolidated balance sheet. We base our assumptions, judgments and estimates on historical experience and various other factors that we believe to be reasonable under the circumstances. Actual results could differ materially from these estimates under different assumptions or conditions. On a regular basis we evaluate our assumptions, judgments and estimates and make changes accordingly. We believe that the assumptions, judgments and estimates involved in the accounting for revenue recognition and estimating the allowance for doubtful accounts have the greatest potential impact on our consolidated financial statements, so we consider these to be our critical accounting policies. We discuss below the assumptions, judgments and estimates associated with these policies. Historically, our assumptions, judgments and estimates relative to our critical accounting policies have not differed materially from actual results. For further information on our critical accounting policies, see Note 1 of our Notes to Consolidated Financial Statements.

Revenue recognition. We derive our revenues primarily from professional fees earned on consulting engagements, product sales in our defense technology development practice, fees earned for the use of our equipment and facilities, as well as reimbursements for outside direct expenses associated with the services that are billed to our clients.

| 19 |

Substantially all of our engagements are performed under time and material or fixed-price billing arrangements. For time and material and fixed-price projects, revenue is generally recognized as the services are performed. For substantially all of our fixed-price engagements we recognize revenue based on the relationship of incurred labor hours at standard rates to our estimate of the total labor hours at standard rates we expect to incur over the term of the contract. Our estimate of total labor hours we expect to incur over the term of the contract is based on the nature of the project and our past experience on similar projects. We believe this methodology achieves a reliable measure of the revenue from the consulting services we provide to our customers under fixed-price contracts.

Significant management judgments and estimates must be made and used in connection with the revenues recognized in any accounting period. These judgments and estimates include an assessment of collectibility and, for fixed-price engagements, an estimate as to the total effort required to complete the project. If we made different judgments or utilized different estimates, the amount and timing of our revenue for any period could be materially different.

All contracts are subject to review by management, which requires a positive assessment of the collectibility of contract amounts. If, during the course of the contract, we determine that collection of revenue is not reasonably assured, we do not recognize the revenue until its collection becomes reasonably assured, which in those situations would generally be upon receipt of cash. We assess collectibility based on a number of factors, including past transaction history with the client, as well as the credit-worthiness of the client. Losses on fixed-price contracts are recognized during the period in which the loss first becomes evident. Contract losses are determined to be the amount by which the estimated total costs of the contract exceeds the total fixed price of the contract.

Estimating the allowance for doubtful accounts. We must make estimates of our ability to collect accounts receivable and our unbilled work-in-process. In circumstances where we are aware of a specific customer’s inability to meet its financial obligations to us, we record a specific allowance to reduce the net recognized receivable to the amount we reasonably believe will be collected. For all other customers we recognize allowances for doubtful accounts based upon historical bad debts, customer concentration, customer credit-worthiness, current economic conditions, aging of amounts due and changes in customer payment terms. As of December 30, 2011, our accounts receivable balance was $73,065,000, net of an allowance for doubtful accounts of $2,339,000.

| 20 |

The following table sets forth, for the periods indicated, the percentage of revenues of certain items in our consolidated statements of income and the percentage increase (decrease) in the dollar amount of such items year to year:

| PERCENTAGE OF REVENUES | PERIOD TO | |||||||||||||||||||

| FOR FISCAL YEARS | PERIOD CHANGE | |||||||||||||||||||

| 2011 | 2010 | 2009 | 2011 vs. 2010 | 2010 vs. 2009 | ||||||||||||||||

| Revenues | 100.0 | % | 100.0 | % | 100.0 | % | 9.5 | % | 9.2 | % | ||||||||||

| Operating expenses: | ||||||||||||||||||||

| Compensation and related expenses | 57.6 | 58.2 | 61.5 | 8.3 | 3.4 | |||||||||||||||

| Other operating expenses | 8.5 | 8.6 | 9.4 | 8.5 | 0.3 | |||||||||||||||

| Reimbursable expenses | 9.5 | 10.8 | 9.7 | (4.1 | ) | 21.3 | ||||||||||||||

| General and administrative expenses | 4.8 | 5.0 | 4.8 | 6.1 | 12.3 | |||||||||||||||

| 80.4 | 82.6 | 85.4 | 6.6 | 5.6 | ||||||||||||||||

| Operating income | 19.6 | 17.4 | 14.6 | 23.6 | 30.0 | |||||||||||||||

| Other income, net | 0.5 | 1.4 | 1.6 | (60.8 | ) | (7.8 | ) | |||||||||||||

| Income before income taxes | 20.1 | 18.8 | 16.2 | 17.4 | 26.2 | |||||||||||||||

| Provision for income taxes | 8.1 | 7.7 | 6.5 | 15.3 | 28.8 | |||||||||||||||

| Net income | 12.0 | % | 11.1 | % | 9.7 | % | 18.8 | % | 24.4 | % | ||||||||||

EXECUTIVE SUMMARY