Attached files

| file | filename |

|---|---|

| EX-31.2 - Cheniere Energy, Inc. | cei2011form10kexhibit312.htm |

| EX-21.1 - Cheniere Energy, Inc. | cei2011form10kexhibit211.htm |

| EX-31.1 - Cheniere Energy, Inc. | cei2011form10kexhibit311.htm |

| EX-23.1 - Cheniere Energy, Inc. | cei2011form10kexhibit231.htm |

| EX-32.2 - Cheniere Energy, Inc. | cei2011form10kexhibit322.htm |

| EX-32.1 - Cheniere Energy, Inc. | cei2011form10kexhibit321.htm |

| EX-10.56 - Cheniere Energy, Inc. | cei2011form10kexhibit1056.htm |

| EX-10.93 - Cheniere Energy, Inc. | cei2011form10kexhibit1093.htm |

| EX-10.94 - Cheniere Energy, Inc. | cei2011form10kexhibit1094.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2011

OR

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File No. 001-16383

CHENIERE ENERGY, INC.

(Exact name of registrant as specified in its charter)

Delaware | 95-4352386 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

700 Milam Street, Suite 800 | |

Houston, Texas | 77002 |

(Address of principal executive offices) | (Zip code) |

Registrant’s telephone number, including area code: (713) 375-5000

Securities registered pursuant to Section 12(b) of the Act:

Common Stock, $ 0.003 par value | NYSE Amex Equities |

(Title of Class) | (Name of each exchange on which registered) |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer", "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer x | Accelerated filer o | Non-accelerated filer o | Smaller reporting company o |

(Do not check if a smaller reporting company) | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

The aggregate market value of the registrant’s Common Stock held by non-affiliates of the registrant was approximately $758,000,000 as of June 30, 2011.

129,607,257 shares of the registrant’s Common Stock were outstanding as of February 15, 2012.

Documents incorporated by reference: The definitive proxy statement for the registrant’s Annual Meeting of Stockholders (to be filed within 120 days of the close of the registrant’s fiscal year) is incorporated by reference into Part III.

CHENIERE ENERGY, INC.

TABLE OF CONTENTS

i

CAUTIONARY STATEMENT

REGARDING FORWARD-LOOKING STATEMENTS

This annual report contains certain statements that are, or may be deemed to be, "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933, as amended (the "Securities Act"), and Section 21E of the Securities Exchange Act of 1934, as amended (the "Exchange Act"). All statements, other than statements of historical facts, included herein or incorporated herein by reference are "forward-looking statements." Included among "forward-looking statements" are, among other things:

• | statements relating to the construction or operation of each of our proposed liquefied natural gas ("LNG") terminals or our proposed pipelines, liquefaction facilities or other projects, or expansions or extensions thereof, including statements concerning the completion or expansion thereof by certain dates or at all, the costs related thereto and certain characteristics, including amounts of regasification, transportation, liquefaction and storage capacity, the number of storage tanks, LNG trains, docks, pipeline deliverability and the number of pipeline interconnections, if any; |

• | statements that we expect to receive an order from the Federal Energy Regulatory Commission ("FERC") authorizing us to construct and operate proposed LNG receiving terminals, liquefaction facilities, pipelines or other projects by certain dates, or at all; |

• | statements regarding future levels of domestic natural gas production, supply or consumption; future levels of LNG imports into North America; sales of natural gas in North America or other markets; exports of LNG from North America; and the transportation, other infrastructure or prices related to natural gas, LNG or other energy sources or hydrocarbon products; |

• | statements regarding any financing or refinancing transactions or arrangements, or ability to enter into such transactions or arrangements, whether on the part of Cheniere or any subsidiary or at the project level; |

• | statements regarding any commercial arrangements presently contracted, optioned or marketed, or potential arrangements, to be performed substantially in the future, including any cash distributions and revenues anticipated to be received and the anticipated timing thereof, and statements regarding the amounts of total LNG regasification, liquefaction or storage capacity that are, or may become, subject to such commercial arrangements; |

• | statements regarding counterparties to our commercial contracts, construction contracts and other contracts; |

• | statements regarding any business strategy, any business plans or any other plans, forecasts, projections or objectives, including potential revenues and capital expenditures, any or all of which are subject to change; |

• | statements regarding legislative, governmental, regulatory, administrative or other public body actions, requirements, permits, investigations, proceedings or decisions; |

• | statements regarding our anticipated LNG and natural gas marketing activities; and |

• | any other statements that relate to non-historical or future information. |

These forward-looking statements are often identified by the use of terms and phrases such as "achieve," "anticipate," "believe," "contemplate," "develop," "estimate," "expect," "forecast," "plan," "potential," "project," "propose," "strategy" and similar terms and phrases, or by the use of future tense. Although we believe that the expectations reflected in these forward-looking statements are reasonable, they do involve assumptions, risks and uncertainties, and these expectations may prove to be incorrect. You should not place undue reliance on these forward-looking statements, which are made as of the date of this annual report and speak only as of the date of this annual report.

Our actual results could differ materially from those anticipated in these forward-looking statements as a result of a variety of factors, including those discussed in "Risk Factors." All forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by these risk factors.

ii

DEFINITIONS

In this annual report, unless the context otherwise requires:

• | Bcf means billion cubic feet; |

• | Bcf/d means billion cubic feet per day; |

• | EPC means engineering, procurement and construction; |

• | LNG means liquefied natural gas; |

• | LNG train means an independent modular unit for gas liquefaction; |

• | MMBtu means million British thermal units; |

• | Mtpa means million metric tons per annum; and |

• | TUA means terminal use agreement. |

PART I

ITEMS 1. AND 2. BUSINESS AND PROPERTIES

General

Cheniere Energy, Inc. (NYSE Amex Equities: LNG), a Delaware corporation, is a Houston-based energy company primarily engaged in LNG-related businesses. We own and operate the Sabine Pass LNG terminal in Louisiana through our 88.8% ownership interest in and management agreements with Cheniere Energy Partners, L.P. ("Cheniere Partners") (NYSE Amex Equities: CQP), which is a publicly traded partnership that we created in 2007. We also own and operate the Creole Trail Pipeline, which interconnects the Sabine Pass LNG terminal with natural gas markets in North America. Approximately one-half of the receiving capacity at the Sabine Pass LNG terminal is contracted to two international oil companies. One of our subsidiaries, Cheniere Marketing, LLC ("Cheniere Marketing"), is marketing LNG and natural gas on its own behalf and on behalf of Cheniere Partners, monetizing the other half of the LNG receiving capacity at the Sabine Pass LNG terminal. Cheniere Partners is developing a project to add liquefaction capabilities at the Sabine Pass LNG terminal through a wholly owned subsidiary, Sabine Pass Liquefaction, LLC ("Sabine Pass Liquefaction"). We are in various stages of developing other projects, including LNG and other marine hydrocarbon terminals and pipeline related projects, each of which, among other things, will require acceptable commercial and financing arrangements before we make a final investment decision. Unless the context requires otherwise, references to the "Company", "Cheniere", "we", "us" and "our" refer to Cheniere Energy, Inc. and its subsidiaries, including our publicly traded subsidiary partnership, Cheniere Partners.

LNG is natural gas that, through a refrigeration process, has been reduced to a liquid state that occupies approximately 1/600th of its gaseous volume. LNG remains in a liquid state at -160 degrees Celsius (-260 degrees Fahrenheit) at atmospheric pressure. Liquefying natural gas allows it to be economically transported from areas of the world where natural gas is abundant and inexpensive to produce to areas where natural gas production and other imports are insufficient to meet demand. LNG is transported from liquefaction terminals to regasification facilities using oceangoing LNG vessels specifically constructed for this purpose.

LNG facilities are conventionally designed to either receive LNG or to produce LNG. The Sabine Pass LNG terminal has a receiving configuration with docks to berth LNG vessels, customized unloading arms and transfer piping, cryogenic storage tanks to temporarily store LNG that is unloaded from a vessel, and equipment that pressurizes and heats the LNG to a normal working pressure and temperature in natural gas transmission lines for delivery to markets that consume natural gas. In terminals with a production configuration, the marine, transfer and storage facilities are still required, but specialized feed gas treatment facilities and refrigeration facilities are required to cool the feed gas to its cryogenic state. In constructing the proposed liquefaction facilities at the Sabine Pass LNG terminal, Cheniere Partners proposes to take advantage of the existing marine and storage facilities that were constructed for the LNG receiving terminal, thereby saving a substantial amount of capital cost compared to the cost of constructing a greenfield facility.

1

Our Business Strategy

Our primary business strategy is to identify markets in which the development of marine hydrocarbon terminals presents an opportunity to develop assets based on long-term, take-or-pay type contracts. Our initial development of the Sabine Pass LNG terminal, based on contracts with Chevron U.S.A. Inc. ("Chevron") and Total Gas and Power North America, Inc. ("Total"), has provided us with the opportunity to expand the terminal to add liquefaction capabilities. We plan to implement our strategy by:

• | safely maintaining and operating the Sabine Pass LNG terminal and the Creole Trail Pipeline; |

• | obtaining the requisite regulatory permits and financing to reach a final investment decision on Cheniere Partners' liquefaction project; |

• | expanding the Sabine Pass LNG terminal to add liquefaction capabilities, and modifying the Creole Trail Pipeline to transport natural gas to the Sabine Pass LNG terminal for fuel and for Sabine Pass Liquefaction to satisfy its LNG delivery obligations under its SPAs; |

• | contracting for feed and fuel gas for Cheniere Partners' liquefaction project; |

• | utilizing the 2.0 Bcf/d of regasification capacity at the Sabine Pass LNG terminal held by one of Cheniere Partners' wholly owned subsidiaries, Cheniere Energy Investments, LLC ("Cheniere Investments"), for short-term and spot LNG purchases and sales until such capacity is used in connection with Cheniere Partners' liquefaction project; |

• | developing business relationships for the marketing of additional long-term and short- term agreements for excess LNG volumes at the Sabine Pass LNG terminal that have not been sold to our long-term customers, and for long-term and short-term contracts for potential future projects at other sites; and |

• | optimizing our capital structure to finance the construction and operation of the facilities needed to serve our customers. |

Market Factors

Because we have entered into contracts to sell LNG from all four of the currently-planned LNG trains at the Sabine Pass LNG terminal, we anticipate that market factors affecting the U.S. natural gas market and global LNG market will have little impact on the commercial success of Cheniere Partners' liquefaction project. Similarly, we have entered into a lump-sum turnkey contract with Bechtel Oil, Gas and Chemicals, Inc. ("Bechtel") to construct the first two LNG trains of Cheniere Partners' liquefaction project. Therefore, we believe that global materials prices and labor costs will have little impact on the cost of LNG trains 1 and 2. Financing the construction of LNG trains 1 and 2 will be primarily dependent upon our ability to access capital markets at reasonable rates and our receipt of regulatory approvals. In order to construct LNG trains 3 and 4 of Cheniere Partners' liquefaction project, we may be affected by higher engineering, procurement, and construction costs, and we will again require access to capital markets at reasonable rates in order to finance construction.

Our ability to sell any seasonal quantities of LNG available from LNG trains 1, 2, 3 and 4 at the Sabine Pass LNG terminal, develop additional trains at the Sabine Pass LNG terminal, or develop other new projects is subject to a broader array of market factors, including: changes in worldwide supply and demand for natural gas, LNG and substitute products; the relative prices for natural gas, oil and substitute products in North America and international markets; economic growth in developing countries; investment in energy infrastructure; the rate of fuel switching for power generation from coal, nuclear, or oil to natural gas; and access to capital markets.

We expect global demand for natural gas to grow significantly as more nations are seeking environmentally cleaner and more abundant and reliable fuel alternatives to oil and coal. Industry sources indicate that global natural gas demand is projected to rise by over 2% per year through 2030, and global LNG demand is projected to rise at twice that rate, from 210 mtpa in 2010 to 483 mtpa in 2030. This projected increase in LNG demand is driven by a number of factors, including: continuing demand growth in Asia, the Middle East, and South America due primarily to a build-out of natural gas fired electric power generation capacity; a reduction in nuclear power generation in established LNG importing regions such as Japan and Europe; and switching from coal- and oil-fired power generation to power generated from natural gas. In addition, with continued population growth in developing countries, industrial consumption of natural gas is expected to continue to increase due to applications such as fertilizer production, which increase is also expected to be driven by fuel switching dynamics as global fertilizer producers switch from naphtha feedstock to natural gas feedstock.

2

While global natural gas consumption is rising internationally, natural gas production in North America has undergone a technological transformation that has resulted in a substantial increase in annual production capacity, decrease in the cost of production, and expansion of technically recoverable reserves. Technologies related to both horizontal drilling and hydraulic fracturing, which had been under development since the 1980s, have now allowed the exploration and production industry to develop unconventional reservoirs composed predominantly of shales, but also containing tight sands and coal seam methane. Unconventional reservoirs are also known as continuous reservoirs; they extend over very large geographic sections of North America. The primary obstacle in the development of these resources is not about finding the formations, but about designing optimal well placement for their most efficient exploitation. This has been greatly facilitated by new drilling technologies that permit very deep and long horizontal wells with drill bores located at single drilling sites to minimize the cycle time between wells and the environmental impact of drilling operations.

These technological improvements have significantly increased natural gas reserves and production capacity in North America; however, growth in demand for natural gas has not increased at the same rate. Since reaching a peak at over $13.00/MMBtu during 2008, natural gas prices have been on a declining trend ever since, and are now below $3.00/MMBtu. We believe that this development, coupled with global demand fundamentals and the fact that global LNG and natural gas prices have generally been linked to oil prices and relatively non-responsive to changes in aggregate natural gas supply, is a fundamental reason for Sabine Pass Liquefaction's success in entering into contracts with respect to Cheniere Partners' liquefaction project.

Our ability to continue to develop new facilities in the United States will be driven by the continued success of the North American upstream natural gas sector in exploiting new unconventional reservoirs, continuing to drive down costs and exploiting higher valued condensates and natural gas liquids in conjunction with natural gas production. Any such facilities will compete with other international LNG export projects principally on a price basis. These projects generally require development capital not only to build the marine, storage and liquefaction facilities, but also to drill wells and build processing and pipeline transportation infrastructure. Because we rely on the natural gas market and transportation infrastructure already existing in the United States, we generally require less capital expenditures and, therefore, are able to sell LNG at a lower price. Furthermore, because feed natural gas is purchased from the United States market at a Henry Hub related price, we can offer LNG for sale on an alternative price index that is not related to crude oil prices, thereby allowing our customers to realize the benefits of lower cost production in the United States while diversifying their portfolio of supply cost indices.

While development of unconventional natural gas resources in other regions may ultimately reduce demand for LNG in some markets over time, LNG serves a variety of requirements and is substantially more flexible than pipeline-delivered natural gas. We believe that this flexibility has intrinsic value beyond the price of natural gas and will continue to motivate demand even if unconventional resources are developed in regions such as Eastern Europe, China or South America.

We continue to evaluate global energy market fundamentals to identify opportunities to serve customers as needs arise, either from an importation, exportation or transportation perspective. We believe that our primary business model of entering into long-term, take-or-pay type contracts for infrastructure assets will provide a base on which to build a platform that permits the continued development of assets to serve the needs of our customers.

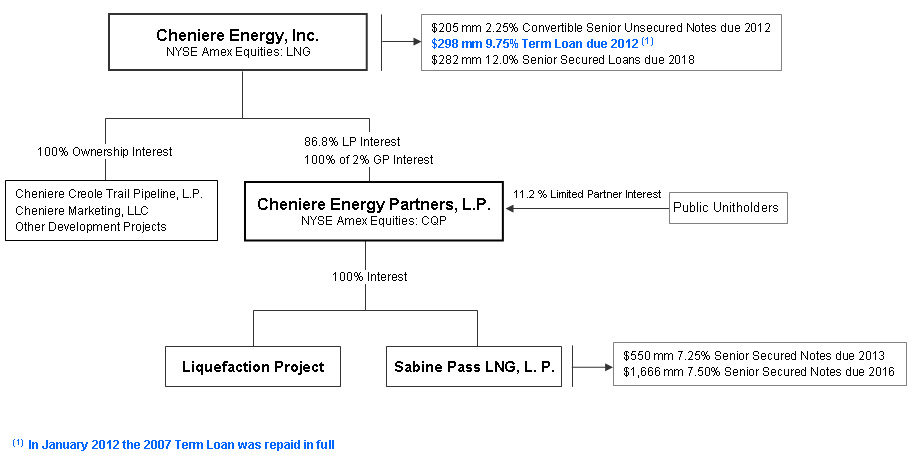

Corporate Structure

As of December 31, 2011, we held approximately 88.8% of Cheniere Partners, including 100% of its general partner. Although results are consolidated for financial reporting, we and Cheniere Partners operate with independent capital structures. Cash flow available to us from Cheniere Partners is primarily in the form of management fees and cash distributions declared and paid to us on our common units and general partner interest. See "Management's Discussion and Analysis of Financial Condition and Results of Operations" for more discussion on how we receive cash flow from Cheniere Partners.

The following diagram depicts our abbreviated capital structure, including our ownership of Cheniere Partners and Sabine Pass LNG, L.P. ("Sabine Pass LNG") as of December 31, 2011. On January 6, 2012, we repaid the $298 million term loan in full, leaving $487 million of debt outstanding at Cheniere Energy, Inc.

3

Business Segments

Our business activities are conducted by three operating segments for which we provide information in our consolidated financial statements for the years ended December 31, 2011, 2010 and 2009. These three segments are our:

• | LNG terminal business; |

• | natural gas pipeline business; and |

• | LNG and natural gas marketing business. |

For information about our segments’ revenues, profits and losses and total assets, see Note 21—"Business Segment Information" of our Notes to Consolidated Financial Statements.

LNG Terminal Business

We began developing our LNG terminal business in 1999 and were among the first companies to secure sites and commence development of new LNG terminals in North America. We focused our development efforts on three LNG terminal projects: Sabine Pass LNG in western Cameron Parish, Louisiana on the Sabine Pass Channel; Corpus Christi LNG near Corpus Christi, Texas; and Creole Trail LNG at the mouth of the Calcasieu Channel in central Cameron Parish, Louisiana. We constructed the Sabine Pass LNG terminal and are developing a project to add liquefaction capabilities at the Sabine Pass LNG terminal which is owned through Cheniere Partners, in which we hold an approximate 88.8% interest. We currently own 100% interests in both the Corpus Christi and Creole Trail LNG terminal projects.

Sabine Pass LNG Terminal

We have constructed the Sabine Pass LNG terminal in western Cameron Parish, Louisiana, on the Sabine Pass Channel. We have long-term leases for five tracts of land consisting of 1,015 acres. We are currently operating LNG receiving facilities at the terminal with regasification capacity of approximately 4.0 Bcf/d (with peak capacity of approximately 4.3 Bcf/d) and aggregate LNG storage capacity of approximately 16.9 Bcf. In addition, we are developing LNG liquefaction facilities at the terminal, which are designed for up to four LNG trains, each with a nominal production capacity of approximately 4.5 mtpa.

4

Regasification Facilities

The Sabine Pass LNG terminal has operational regasification capacity of approximately 4.0 Bcf/d (with peak capacity of approximately 4.3 Bcf/d) and aggregate LNG storage capacity of approximately 16.9 Bcf. Approximately 2.0 Bcf/d of the regasification capacity at the Sabine Pass LNG terminal has been reserved under two long-term third-party TUAs, under which Sabine Pass LNG’s customers are required to pay fixed monthly fees, whether or not they use the LNG terminal. Capacity reservation fee TUA payments are made by Sabine Pass LNG's third-party TUA customers as follows:

• | Total has reserved approximately 1.0 Bcf/d of regasification capacity and is obligated to make monthly capacity payments to Sabine Pass LNG aggregating approximately $125 million per year for 20 years that commenced April 1, 2009. Total, S.A. has guaranteed Total’s obligations under its TUA up to $2.5 billion, subject to certain exceptions; and |

• | Chevron has reserved approximately 1.0 Bcf/d of regasification capacity and is obligated to make monthly capacity payments to Sabine Pass LNG aggregating approximately $125 million per year for 20 years that commenced July 1, 2009. Chevron Corporation has guaranteed Chevron’s obligations under its TUA up to 80% of the fees payable by Chevron. |

The remaining approximately 2.0 Bcf/d of regasification capacity has been reserved by Cheniere Partners through a TUA between Cheniere Investments and Sabine Pass LNG. Cheniere Investments is obligated to make monthly capacity payments to Sabine Pass LNG aggregating approximately $250 million per year through at least September 30, 2028; however, the revenue earned by Sabine Pass LNG from Cheniere Investments' capacity payments under the TUA is eliminated upon consolidation of our financial statements. Cheniere Partners has guaranteed Cheniere Investments' obligations under its TUA. See "—LNG and Natural Gas Marketing Business" below for a discussion of the Variable Capacity Rights Agreement ("VCRA") between Cheniere Investments and Cheniere Marketing entered into in order to monetize Cheniere Investments' 2.0 Bcf/d of regasification capacity at the Sabine Pass LNG terminal.

Liquefaction Facilities

In June 2010, Cheniere Partners formed Sabine Pass Liquefaction, LLC ("Sabine Pass Liquefaction") to own, develop and operate liquefaction facilities at the Sabine Pass LNG terminal. As currently contemplated, the liquefaction facilities are designed for up to four LNG trains, each with a nominal production capacity of approximately 4.5 mtpa. We anticipate LNG exports could commence as early as 2015 with each LNG train commencing operations approximately six to nine months after the previous LNG train.

The Department of Energy ("DOE") has granted Sabine Pass Liquefaction an order authorizing the export of up to the equivalent of 16 mtpa (approximately 800 Bcf) per year of domestically produced LNG by vessel from the Sabine Pass LNG terminal to Free Trade Agreement ("FTA") countries for a 30-year term, beginning on the earlier of the date of first export or September 7, 2020, and another order authorizing the export of up to the equivalent of 803 Bcf per year (approximately 16 mtpa) of domestically produced LNG by vessel from the Sabine Pass LNG terminal to non-FTA countries for a 20-year term, beginning on the earlier of the date of first export or May 20, 2016.

Sabine Pass Liquefaction has submitted an application to the FERC requesting authorization to site, construct and operate liquefaction and export facilities at the Sabine Pass LNG terminal, which we anticipate receiving in the first quarter of 2012.

Customers

Sabine Pass Liquefaction has entered into four LNG sale and purchase agreements ("SPA"), under which customers have committed to purchase, in aggregate, 834.0 million MMBtu of LNG per year (approximately 16 mtpa). The volume of LNG committed to be purchased by these customers represents approximately 89% of the expected nameplate liquefaction capacity that will be available upon completion of Cheniere Partners' proposed liquefaction facilities. In addition, upon completion of all four LNG trains, approximately 100 million MMBtu of LNG per year (approximately 2.0 mtpa) may be produced seasonally to be sold by Sabine Pass Liquefaction on a merchant basis. We anticipate that Sabine Pass Liquefaction will utilize Cheniere Investments' TUA capacity to provide LNG to Sabine Pass Liquefaction's customers.

5

In aggregate, these customers have agreed to pay Sabine Pass Liquefaction approximately $2.3 billion annually, plus an amount per MMBtu of LNG equal to 115% of the final settlement price for the New York Mercantile Exchange natural gas futures contract for the month in which the relevant cargo is scheduled. Subject to the conditions described below, sales charges will be paid by our SPA customers as follows:

• | BG Gulf Coast LNG, LLC ("BG") has agreed to purchase 286.5 million MMBtu of LNG per year (approximately 5.5 mtpa) for a fixed sales charge of (i) $2.25 per MMBtu for 182.5 million MMBtu commencing upon the date of first commercial delivery for LNG train 1, (ii) $3.00 per MMBtu for 36.5 million MMBtu commencing upon the date of first commercial delivery for LNG train 2 (the "Train 2 Tranche"), (iii) $3.00 per MMBtu for 34.0 million MMBtu commencing upon the date of first commercial delivery for LNG train 3 (the "Train 3 Tranche") and (iv) $3.00 per MMBtu for 33.5 million MMBtu commencing upon the date of first commercial delivery for LNG train 4 (the "Train 4 Tranche"), plus in each case a contract sales price for each MMBtu of LNG delivered under the SPA equal to 115% of the final settlement price for the New York Mercantile Exchange Henry Hub natural gas futures contract for the month in which the relevant cargo is scheduled. The fixed sales charge is equivalent to approximately $411 million, $520 million, $622 million and $723 million per year upon completion of LNG trains 1, 2, 3 and 4, respectively, such that after completion of LNG train 4, the fixed sales charge will be a total of approximately $723 million per year; |

• | Gas Natural Aprovisionamientos SDG S.A. ("Gas Natural Fenosa"), an affiliate of Gas Natural SDG S.A., has agreed to purchase 182.5 million MMBtu of LNG per year (approximately 3.5 mtpa) for a fixed sales charge of $2.49 per MMBtu for the full contract quantity, plus a contract sales price for each MMBtu of LNG delivered under the SPA equal to 115% of the final settlement price for the New York Mercantile Exchange Henry Hub natural gas futures contract for the month in which the relevant cargo is scheduled. The fixed sales charge is equivalent to approximately $454 million per year, commencing upon the date of first commercial delivery for LNG train 2; |

• | Korea Gas Corporation ("KOGAS") has agreed to purchase 182.5 million MMBtu of LNG per year (approximately 3.5 mtpa) for a contract sales price equal to $3.00 plus 115% of the final settlement price for the New York Mercantile Exchange Henry Hub natural gas futures contract for the month in which the relevant cargo is scheduled. The fixed portion of the contract sales price is equivalent to approximately $548 million per year, commencing upon the date of first commercial delivery for LNG train 3; and |

• | GAIL (India) Limited ("GAIL") has agreed to purchase 182.5 million MMBtu of LNG per year (approximately 3.5 mtpa) for a contract sales price equal to $3.00 plus 115% of the final settlement price for the New York Mercantile Exchange Henry Hub natural gas futures contract for the month in which the relevant cargo is scheduled. The fixed portion of the contract sales price is equivalent to approximately $548 million per year, commencing upon the date of first commercial delivery for LNG train 4. Prior to the commencement of LNG train 4 operations, GAIL will purchase 10.4 million MMBtu of LNG per year (approximately 0.2 mtpa) commencing upon the date LNG train 2 becomes commercially operable. |

During an event of force majeure declared by BG or Gas Natural Fenosa or Sabine Pass Liquefaction, BG or Gas Natural Fenosa, as applicable, will continue to be obligated to pay the relevant fixed sales charge, subject to reduction under certain circumstances, for a period of 24 months, after which time such customer may have a right to terminate its SPA.

Each SPA has a term of 20 years commencing upon the date of first commercial delivery for the applicable LNG train, and an extension option of up to ten years, or for Gas Natural Fenosa in certain circumstances, up to 12 years. Each SPA is subject to certain conditions precedent, including but not limited to, Sabine Pass Liquefaction receiving regulatory approvals, securing necessary financing arrangements and making a final investment decision to construct the applicable LNG train. Sabine Pass Liquefaction will designate the date for the first commercial delivery of LNG for each customer within the 180-day period commencing a specified number of months after the date that the conditions precedent have been satisfied or waived.

A customer has the right to terminate its SPA if, among other events, (i) Sabine Pass Liquefaction declares an event of force majeure one or more times and the resulting interruptions total 24 or more months in any 36 month period, and such force majeure events result in a reduction of 50 percent or more in the annualized annual contract quantity of LNG available to such customer during such periods of force majeure, (ii) with respect to BG and Gas Natural Fenosa, such customer declares a force majeure event for specified circumstances and such force majeure event has continued for 24 months and has resulted in a reduction in the quantity of LNG that such customer is able to take of at least 50 percent of the annualized contract quantity, (iii) Sabine Pass Liquefaction fails to make available to such customer a specified number of cargoes during a 12-month period, (iv) an applicable LNG train has not commenced commercial operations at the Sabine Pass LNG terminal within 180 days after the date designated

6

for first commercial delivery, (v) with respect to BG and Gas Natural Fenosa, Sabine Pass Liquefaction's authorizations to export LNG from the United States to either FTA or non-FTA countries has been withdrawn, revoked or expired, and such withdrawal, revocation or expiration does not constitute a force majeure, and with respect to GAIL, Sabine Pass Liquefaction's authorization to export LNG from the United States to non-FTA countries has expired, or (vi) with respect to BG and Gas Natural Fenosa, the specified limit on Sabine Pass Liquefaction's liability under the applicable SPA has been reached or exceeded.

Sabine Pass Liquefaction has the right to terminate a customer's SPA if, among other events, (i) any applicable guaranty provided by such customer ceases to be in effect in excess of a specified number of days, (ii) such customer or its applicable guarantor, if any, fails to execute certain agreements with financial lenders in a timely manner, (iii) with respect to GAIL and KOGAS, such customer fails to take 50 percent or more of the cargoes scheduled in any 12-month period, (iv) with respect to GAIL and KOGAS, such customer declares an event of force majeure one or more times and the resulting interruptions total 24 or months in any 36 month period, and such force majeure events result in such customer being prevented from taking 50 percent or more of the annualized annual contract quantity during such periods of force majeure, (v) such customer fails to comply with applicable trade laws or (vi) such customer violates provisions of the SPA restricting parties to which LNG can be marketed and sold.

Either a customer or Sabine Pass Liquefaction would have the right to terminate such customer's SPA if, among other events, (i) a bankruptcy event (as defined in the SPA) occurred with respect to the other party, (ii) the other party failed to pay amounts due under the SPA in excess of a specified dollar amount, (iii) the other party's business practices caused it to violate certain applicable laws or (iv) the conditions to the commencement of the 20-year term specified in the SPA were not satisfied or waived by December 31, 2012 with respect to BG (for LNG train 1) and Gas Natural Fenosa, or June 30, 2013 with respect to GAIL and KOGAS, or a later date if so agreed by the customer and Sabine Pass Liquefaction. In addition, either BG or Sabine Pass Liquefaction has the right to cancel LNG trains 2, 3 and 4 if Sabine Pass Liquefaction has not made a positive final investment decision to proceed with construction of the applicable LNG trains by June 30, 2013.

Construction

We expect to commence construction of LNG trains 1 and 2 during the first half of 2012 and begin operations in late 2015, with each LNG train commencing operations approximately six to nine months after the previous LNG train. We expect to complete our construction plan and cost estimates for LNG trains 3 and 4 by the end of 2012, begin construction by the end of the first quarter of 2013, and begin operations in 2017.

The cost to construct LNG trains 1 and 2 is currently estimated to be approximately $4.5 billion to $5.0 billion, before financing costs. Our cost estimates are subject to change due to such items as change orders, delays in construction, increased component and material costs, escalation of labor costs and increased spending to maintain our construction schedule.

In November 2011, Sabine Pass Liquefaction entered into a lump-sum turnkey agreement ("EPC Contract") with Bechtel, a major international engineering, procurement and construction contractor, for the procurement, engineering, design, installation, training, commissioning and placing into service of LNG trains 1 and 2 of the proposed liquefaction project. The EPC Contract provides that Sabine Pass Liquefaction will pay Bechtel a contract price of $3.9 billion, which is only subject to adjustment by change orders. Bechtel has the right, among other things, to submit change orders in the event Bechtel is adversely affected as a result of a delay in the commencement of construction beyond March 31, 2012. The EPC Contract also entitles Bechtel to a change order amending its rights and obligations to the extent it is adversely affected by any of the following: (i) a change in law, (ii) certain acts or omissions of Sabine Pass Liquefaction, (iii) force majeure, (iv) acceleration of work by Sabine Pass Liquefaction, (v) delay in delivery of insurance proceeds in the case of insured loss, (vi) suspension in work ordered by Sabine Pass Liquefaction, (vii) subsurface soil conditions materially different from those described in the geotechnical studies, (viii) discovery of hazardous materials for which Sabine Pass Liquefaction is responsible, (ix) physical damage caused by a third party not under Bechtel’s control and (x) other specified reasons in the EPC Contract. The EPC Contract entitles Sabine Pass Liquefaction to a change order unilaterally up to certain thresholds and thereafter upon request provided that agreement is reached on any changes to the contract price, project schedule, design, payment schedule, minimum acceptance criteria, performance guarantee and any other obligation of Bechtel under the EPC Contract.

7

In the EPC Contract, Bechtel warrants that the (i) equipment will be new (unless otherwise specified in the EPC Contract) and of good quality, (ii) work and the equipment will meet the requirements of the EPC Contract, including good engineering and construction practices and applicable laws, codes and standards and (iii) work and the equipment will be free from encumbrances to title. Until 18 months after substantial completion of each LNG train, Bechtel will be liable to promptly correct any work that is found defective with respect to such LNG train.

If an LNG train fails to achieve 95% of the performance guarantee set forth in the EPC Contract by the applicable guaranteed substantial completion date, then substantial completion of such LNG train will not occur and Bechtel will pay delay liquidated damages. In addition, Bechtel is required to attempt for 10 months thereafter to correct the work to enable the LNG train to achieve the minimum acceptance criteria and otherwise achieve substantial completion. If the LNG train has not achieved the minimum acceptance criteria and substantial completion at the end of this 10-month period, then Sabine Pass Liquefaction will have the option of either granting Bechtel an additional 10-month correction period or declaring a default. If an LNG train has not achieved the performance guarantee within a specified period after the guaranteed substantial completion date, then Bechtel is required to pay the applicable performance liquidated damages, and if substantial completion of an LNG train occurs after the applicable guaranteed substantial completion date, Bechtel will pay Sabine Pass Liquefaction the delayed liquidated damages as defined in the EPC Contract until substantial completion of such LNG train occurs. Bechtel will be entitled to receive specified bonuses for timely substantial completion of the LNG trains.

The EPC Contract has several termination rights:

• | if Bechtel fails to timely commence the work, abandons the work, fails to materially comply with its material obligations, makes an unpermitted assignment, fails to maintain required insurance, materially disregards applicable law or applicable standards and codes, or an insolvency event occurs with respect to Bechtel or its guarantor, then Sabine Pass Liquefaction will have the right to require that Bechtel cure such default, and if Bechtel fails to cure such default, or if Bechtel or its guarantor experiences an insolvency event, Sabine Pass Liquefaction may terminate the EPC Contract; |

• | Sabine Pass Liquefaction has the right to terminate the EPC Contract for its convenience, in which case Bechtel will be paid the portion of the Contract Price for the work performed, costs reasonably incurred by Bechtel on account of such termination and demobilization, and a lump sum of between $1.0 million and $2.5 million depending on the termination date if the EPC Contract is terminated prior to issuance of the notice to proceed and up to $30.0 million depending on the termination date if the EPC Contract is terminated after issuance of the notice to proceed; |

• | if Sabine Pass Liquefaction fails to pay any undisputed amount, fails to materially comply with any of its material obligations, or experiences an insolvency event, then Bechtel has the right to provide written notice demanding that such default be cured, and if Sabine Pass Liquefaction fails to cure such default or Sabine Pass Liquefaction experiences an insolvency event, Bechtel may terminate the EPC Contract; |

• | if one force majeure event causes suspension of a substantial portion of the work for more than 100 consecutive days or any one or more force majeure events causes suspension of a substantial portion of the work for a period exceeding 180 days in the aggregate during any continuous 24-month period, then either party may terminate the EPC Contract; or |

• | if Sabine Pass Liquefaction fails to issue the notice to proceed by December 31, 2012, then either party may terminate the EPC Contract, and Bechtel will be paid costs reasonably incurred by Bechtel on account of such termination and a lump sum of $5.0 million. |

Bechtel’s liability under the EPC Contract is limited as specified in the EPC Contract, except that this limit does not apply to certain indemnification obligations, to Bechtel’s title warranty, or to Bechtel’s obligation to complete all work required to ensure that each LNG train is ready to receive natural gas and produce LNG.

The cost to construct LNG trains 3 and 4 is currently estimated to be approximately $4.5 billion to $5.0 billion, before financing costs. Sabine Pass Liquefaction has engaged Bechtel to complete front-end engineering and design work and to negotiate a lump-sum turnkey contract based on an open book estimate. Commencement of construction for LNG trains 3 and 4 is targeted during early 2013. Our cost estimates are subject to change due to such items as change orders, delays in construction, increased component and material costs, escalation of labor costs and increased spending to maintain our construction schedule.

8

Corpus Christi LNG Terminal

We formed Corpus Christi LNG, L.P. ("Corpus Christi LNG") in May 2003 to develop the Corpus Christi LNG terminal near Corpus Christi, Texas, which was designed and permitted by the FERC as a regasification terminal, although this order will expire in April 2012. The Corpus Christi site consists of approximately 1,030 acres and is located approximately sixty miles southeast of the Eagle Ford Shale.

In September 2011, we formed Corpus Christi Liquefaction, LLC ("Corpus Christi Liquefaction") to develop an LNG terminal at our Corpus Christi Liquefaction terminal site. As currently contemplated, the proposed Corpus Christi LNG Liquefaction LNG terminal would be designed for up to three LNG trains capable of producing in aggregate of up to 13.5 mtpa. In December 2011, Corpus Christi Liquefaction received approval from the FERC to begin the pre-filing process required to seek authorization to commence construction of the liquefaction project. Corpus Christi Liquefaction has engaged Bechtel to complete preliminary front-end engineering and design work.

Corpus Christi Liquefaction will contemplate making a final investment decision to commence construction of the Corpus Christi LNG Liquefaction LNG project upon, among other things, entering into acceptable commercial arrangements, obtaining an order to export domestically produced natural gas, receiving regulatory authorization to construct and operate the liquefaction assets and obtaining adequate financing.

Other LNG Terminal Sites

We continue to evaluate, and may develop, additional sites that we believe may be commercially desirable locations for LNG terminals and other facilities.

LNG Terminal Competition

All of the available capacity and services at the Sabine Pass LNG terminal has been fully contracted. Other LNG terminal sites that we may develop will compete for customers with other companies that are constructing and operating LNG receiving terminals and liquefaction facilities around the world. Many of the companies with which we compete are major energy corporations with longer operating histories, more development experience, greater name recognition, greater financial, technical and marketing resources and greater access to markets than we do.

LNG Terminal Governmental Regulation

Our LNG terminal operations are subject to extensive regulation under federal, state and local statutes, rules, regulations and laws. These laws require that we engage in consultations with appropriate federal and state agencies and that we obtain and maintain applicable permits and other authorizations. This regulatory burden increases the cost of constructing and operating the LNG terminals, and failure to comply with such laws could result in substantial penalties. Through construction, commissioning and operations of our existing facilities, we have been in substantial compliance with all regulations discussed herein.

FERC

In order to site and construct our proposed LNG terminals, we must receive and are required to maintain authorization from the FERC under Section 3 of the Natural Gas Act of 1938, as amended ("NGA"). We will be required to obtain and maintain authorizations from the FERC to site, construct and operate liquefaction and export facilities at the Sabine Pass LNG and Corpus Christi LNG terminal sites. In addition, orders from the FERC authorizing construction of an LNG terminal are typically subject to specified conditions that must be satisfied throughout the construction, commissioning and operation of LNG terminals. Throughout the life of our LNG terminals, they will be subject to regular reporting requirements to the FERC and the U.S. Department of Transportation regarding the operation and maintenance of the facilities.

9

In 2005, the Energy Policy Act of 2005 ("EPAct") was signed into law. The EPAct gave the FERC exclusive authority to approve or deny an application for the siting, construction, expansion or operation of an LNG terminal. The EPAct amended the NGA to prohibit market manipulation. The EPAct increased civil and criminal penalties for any violations of the NGA, Natural Gas Policy Act of 1978, as amended, and any rules, regulations or orders of the FERC, up to $1.0 million per day per violation. In accordance with the EPAct, the FERC issued a final rule making it unlawful for any entity, in connection with the purchase or sale of natural gas or transportation service subject to the FERC’s jurisdiction, to defraud, make an untrue statement or omit a material fact or engage in any practice, act or course of business that operates or would operate as a fraud.

Other Federal Governmental Permits, Approvals and Consultations

In addition to the FERC authorization under Section 3 of the NGA, our construction and operation of LNG terminals and related projects, and the construction of our proposed liquefaction facilities, are also subject to additional federal permits, orders, approvals and consultations required by other federal agencies, including: DOE, Advisory Council on Historic Preservation, U.S. Army Corps of Engineers, U.S. Department of Commerce, National Marine Fisheries Services, U.S. Department of the Interior, U.S. Fish and Wildlife Service, U.S. Environmental Protection Agency ("EPA") and U.S. Department of Homeland Security.

Our LNG terminals are also subject to U.S. Department of Transportation safety regulations and standards for the transportation and storage of LNG and regulations of the U.S. Coast Guard relating to maritime safety and facility security. Moreover, our LNG terminals are also subject to state and local laws, rules and regulations.

LNG Terminal Environmental Regulation

Our LNG terminal operations, including the proposed liquefaction facilities, are subject to various federal, state and local laws and regulations relating to the protection of the environment. These environmental laws and regulations may impose substantial penalties for noncompliance and substantial liabilities for pollution. Many of these laws and regulations restrict or prohibit the types, quantities and concentration of substances that can be released into the environment and can lead to substantial liabilities for non-compliance or releases. Failure to comply with these laws and regulations may also result in substantial civil and criminal fines and penalties.

Clean Air Act ("CAA")

Our LNG terminal operations, including the proposed liquefaction facilities, are subject to the federal CAA and comparable state and local laws. We may be required to incur certain capital expenditures over the next several years for air pollution control equipment in connection with maintaining or obtaining permits and approvals addressing other air emission-related issues. We do not believe, however, that our operations, or the construction and operations of our proposed liquefaction facilities, will be materially and adversely affected by any such requirements.

The U.S. Supreme Court has ruled that the EPA has authority under existing legislation to regulate carbon dioxide and other heat-trapping gases in mobile source emissions. Mandatory reporting requirements were promulgated by the EPA and finalized in 2009. This rule requires mandatory reporting for greenhouse gases from stationary fuel combustion sources. An additional section, which requires reporting for all fugitive emissions throughout LNG terminals, was finalized in December 2010. In addition, Congress has considered proposed legislation directed at reducing "greenhouse gas emissions." It is not possible at this time to predict how future regulations or legislation may address greenhouse gas emissions and impact our business. However, future regulations and laws could result in increased compliance costs or additional operating restrictions and could have a material adverse effect on our business, financial position, results of operations and cash flows.

Coastal Zone Management Act ("CZMA")

Our LNG terminals, including the proposed liquefaction facilities, are subject to the requirements of the CZMA throughout the construction of facilities located within the coastal zone. The CZMA is administered by the states (in Louisiana, by the Department of Natural Resources, and in Texas, by the Railroad Commission and the General Land Office). This program is implemented in coordination with the Department of the Army construction permitting process to ensure that impacts to coastal areas are consistent with the intent of the CZMA to manage the coastal areas.

10

Clean Water Act ("CWA")

Our LNG terminal operations are subject to the federal CWA and analogous state and local laws. Pursuant to certain requirements of the CWA, the EPA has adopted regulations concerning discharges of wastewater and storm water runoff. This program requires covered facilities to obtain individual permits, participate in a group permit or seek coverage under an EPA general permit.

Resource Conservation and Recovery Act ("RCRA")

The federal RCRA and comparable state statutes govern the disposal of "hazardous wastes." In the event any hazardous wastes are generated in connection with our LNG terminal operations, we are subject to regulatory requirements affecting the handling, transportation, treatment, storage and disposal of such wastes.

Endangered Species Act

Our LNG terminal operations and planned activities, including our proposed liquefaction facilities, may be restricted by requirements under the Endangered Species Act, which seeks to ensure that human activities neither jeopardize endangered or threatened animal, fish and plant species nor destroy or modify their critical habitats.

National Historic Preservation Act ("NHPA")

Construction of our proposed liquefaction facilities will be subject to requirements under Section 106 of the NHPA. The NHPA requires projects to take into account the effects of their actions on historic properties. These programs are administered by the State Historic Preservation Officers ("SHPOs"). Any areas where ground disturbance will occur are required to be reviewed by the affected SHPOs.

Natural Gas Pipeline Business

We formed Cheniere Pipeline Company, a wholly owned subsidiary, to develop natural gas pipelines to provide access to North American natural gas markets for customers of our LNG terminals. We are also developing other pipeline projects not primarily related to our LNG terminals. Our pipeline systems developed in conjunction with our LNG terminals will interconnect with multiple interstate pipelines, providing a means of transporting natural gas between trading points in the Gulf Coast and our LNG terminals. Our other projects are market-focused, seeking to connect natural gas supplies to growing markets. Our ultimate decisions regarding further development of new pipeline projects will depend upon future events, including, in particular, customer preferences and general market demand for pipeline transportation of natural gas from or to a particular LNG terminal.

Creole Trail Pipeline

The Creole Trail Pipeline is a permitted 153-mile natural gas pipeline. We have constructed, placed in-service and are operating the first 94 miles of the Creole Trail Pipeline, connecting the Sabine Pass LNG terminal to numerous interconnection points with existing interstate and intrastate natural gas pipelines in southwest Louisiana. The remaining 59 miles of permitted natural gas pipeline, if constructed, will traverse east starting at the terminus of the first 94 miles of natural gas pipeline, with interconnections to additional existing interstate natural gas pipelines.

Cheniere Marketing and other third parties have entered into interruptible transportation agreements with Creole Trail Pipeline to transport natural gas from the Sabine Pass LNG terminal into North American natural gas markets.

In connection with Cheniere Partners' proposed liquefaction facilities at the Sabine Pass LNG terminal, we are developing a project for the Creole Trail Pipeline to be able to transport natural gas to the Sabine Pass LNG terminal for fuel and for Sabine Pass Liquefaction to satisfy its LNG delivery obligations under its SPAs. We will contemplate making a final investment decision to commence construction of the expansion project upon, among other things, entering into acceptable commercial and financing arrangements.

We will contemplate making a final investment decision to construct the remaining 59 miles of permitted natural gas pipeline upon, among other things, entering into acceptable commercial and financing arrangements.

11

Other Pipelines

We continue to evaluate, and may develop, additional pipelines that we believe may be commercially desirable based on customer preferences and general market demand for natural gas.

We will contemplate making a final investment decision to commence construction of our proposed natural gas pipelines upon, among other things, entering into acceptable commercial and financing arrangements and applying for and receiving governmental authorization to construct and operate the natural gas pipelines.

Natural Gas Pipeline Competition

Our existing and proposed pipelines will compete with intrastate and interstate pipelines throughout the U.S. Gulf Coast region. The principal elements of competition among pipelines are rates, terms of service, access to supply and flexibility and reliability of service. In addition, the FERC’s continuing efforts to increase competition in the natural gas industry are increasing the natural gas transportation options of a pipeline’s traditional customers.

Our pipelines will face competition from other interstate and/or intrastate pipelines that connect with our LNG terminals. In particular, our Creole Trail Pipeline competes with the Kinder Morgan Louisiana Pipeline owned by Kinder Morgan Energy Partners, L.P. (“Kinder Morgan”). Kinder Morgan has built a 3.2 Bcf/d take-away pipeline system from the Sabine Pass LNG terminal. Total and Chevron have both signed agreements with Kinder Morgan securing 100% of the initial capacity on the Kinder Morgan Louisiana Pipeline for 20 years.

Natural Gas Pipeline Governmental Regulation

Interstate Natural Gas Pipelines

Under the NGA, the FERC is granted authority to approve, and if necessary, set "just and reasonable rates" for the transportation or sale of natural gas in interstate commerce. In addition, under the NGA, we are not permitted to unduly discriminate or grant undue preference as to our rates or the terms and conditions of service. The FERC has the authority to grant certificates allowing construction and operation of facilities used in interstate gas transportation and authorizing the provision of services. Under the NGA, the FERC’s jurisdiction generally extends to the transportation of natural gas in interstate commerce, to the sale in interstate commerce of natural gas for resale for ultimate consumption for domestic, commercial, industrial, or any other use, and to natural gas companies engaged in such transportation or sale. However, the FERC’s jurisdiction does not extend to the production, gathering, or local distribution of natural gas.

In general, the FERC’s authority to regulate interstate natural gas pipelines and the services that they provide includes:

• | rates and charges for natural gas transportation and related services; |

• | the certification and construction of new facilities; |

• | the extension and abandonment of services and facilities; |

• | the maintenance of accounts and records; |

• | the acquisition and disposition of facilities; |

• | the initiation and discontinuation of services; and |

• | various other matters. |

Failure to comply with the NGA can result in the imposition of administrative, civil and criminal remedies, including civil and criminal penalties of up to $1.0 million per day per violation under the EPAct.

For a number of years the FERC has implemented certain rules referred to as Standards of Conduct aimed at ensuring that an interstate natural gas pipeline not provide certain affiliated entities with preferential access to transportation service or non-public information about such service. These rules have been subject to revision by the FERC from time to time, most recently in 2008 when the FERC issued a final rule, Order No. 717, on Standards of Conduct for Transmission Providers. Order No. 717

12

eliminated the concept of energy affiliates and adopted a "functional approach" that applies Standards of Conduct to individual officers and employees based on their job functions, not on the company or division in which the individual works. The general principles of the Standards of Conduct are: non-discrimination, independent functioning, no conduit and transparency. These general principles govern the relationship between marketing function employees conducting transactions with affiliated pipeline companies and transportation function employees. We have established the required policies and procedures to comply with the Standards of Conduct and are subject to audit by the FERC to review compliance, policies and our training programs.

Our pipelines that interconnect with our LNG terminals are interstate natural gas pipelines. We are required to obtain authorization from the FERC pursuant to Section 7 of the NGA to construct and operate these pipelines. The rates that we charge are subject to the FERC's regulation under Sections 4 and 5 of the NGA. Our interstate pipelines also are subject to the FERC's open access requirements and the FERC's Standards of Conduct. The FERC's exercise of jurisdiction over interstate natural gas pipelines is substantially broader than its exercise of jurisdiction over LNG terminals.

Natural Gas Pipeline Safety Act

Louisiana and Texas administer federal pipeline safety standards under the Natural Gas Pipeline Safety Act of 1968, as amended ("NGPSA"), which requires certain pipelines to comply with safety standards in constructing and operating the pipelines and subjects the pipelines to regular inspections. Failure to comply with the NGPSA may result in the imposition of administrative, civil and criminal remedies.

The Pipeline Safety Improvement Act of 2002, as amended ("PSIA"), which is administered by the U.S. Department of Transportation Office of Pipeline Safety, governs the areas of testing, education, training and communication. The PSIA requires pipeline companies to perform extensive integrity tests on natural gas transportation pipelines that exist in high population density areas designated as "high consequence areas." Pipeline companies are required to perform the integrity tests on a seven-year cycle. The risk ratings are based on numerous factors, including the population density in the geographic regions served by a particular pipeline, as well as the age and condition of the pipeline and its protective coating. Testing consists of hydrostatic testing, internal electronic testing, or direct assessment of the piping. In addition to the pipeline integrity tests, pipeline companies must implement a qualification program to make certain that employees are properly trained. Pipeline operators also must develop integrity management programs for gas transportation pipelines, which requires pipeline operators to perform ongoing assessments of pipeline integrity; identify and characterize applicable threats to pipeline segments that could impact a high consequence area; improve data collection, integration and analysis; repair and remediate the pipeline, as necessary; and implement preventive and mitigation actions.

In 2010, the U.S. Department of Transportation issued a final rule (known as "Control Room Management Rule") requiring pipeline operators to write and institute certain control room procedures that address human factors and fatigue management. Existing Creole Trail Pipeline written control room management procedures are being implemented per the schedule in the final rule.

Energy Policy Act of 2005

The EPAct and the FERC’s policies promulgated thereunder contain numerous provisions relevant to the natural gas industry and to interstate pipelines. See "—LNG Terminal Business—LNG Terminal Governmental Regulation" above.

Natural Gas Pipeline Environmental Regulation

Our natural gas pipeline business is subject to the same federal, state and local laws and regulations relating to the protection of the environment that are applicable to our LNG terminals. See "—LNG Terminal Business—LNG Terminal Environmental Regulation" above.

LNG and Natural Gas Marketing Business

Our wholly owned subsidiary, Cheniere Marketing, is engaged in the LNG and natural gas marketing business and is seeking to develop a portfolio of long-term, short-term, and spot LNG purchase and sale agreements, assist Cheniere Investments in negotiating with potential customers to monetize its 2.0 Bcf/d of regasification capacity at the Sabine Pass LNG terminal, and enter into business relationships for the domestic marketing of natural gas imported by Cheniere Marketing as LNG to the Sabine Pass LNG terminal.

13

Cheniere Marketing has been purchasing, transporting and unloading commercial LNG cargoes into the Sabine Pass LNG terminal and has used trading strategies intended to maximize margins on these cargoes. In addition, Cheniere Marketing has continued to enter into various business relationships to facilitate purchasing and selling commercial LNG cargoes.

In 2010, Cheniere Marketing entered into various agreements ("LNGCo Agreements") with JPMorgan LNG Co. ("LNGCo"), under which Cheniere Marketing has agreed to develop and maintain commercial and trading opportunities in the LNG industry and present any such opportunities exclusively to LNGCo. Cheniere Marketing also agreed to provide, or arrange for the provision of, all of the operations and administrative services required by LNGCo in connection with any LNG cargoes purchased by LNGCo, including negotiating agreements and arranging for transporting, receiving, storing, hedging and regasifying LNG cargoes. Cheniere Marketing does not have the authority to contractually bind LNGCo under the LNGCo Agreements. In the event LNGCo declines to purchase an LNG cargo presented to it by Cheniere Marketing under the LNGCo Agreements, Cheniere Marketing may pursue the opportunity on its own behalf or present it to third parties. The term of the LNGCo Agreements expires in April 2012; however, either party may terminate the agreements without penalty prior to such date. In return for the services to be provided by Cheniere Marketing, LNGCo will pay a fixed fee to Cheniere Marketing and may pay additional fees depending upon the gross margins of each transaction and the aggregate gross margin earned during the term of the LNGCo Agreements.

In connection with monetizing Cheniere Investments’ reserved capacity under its TUA at the Sabine Pass LNG terminal, Cheniere Marketing has entered into the VCRA. Pursuant to the VCRA, Cheniere Marketing is obligated to pay Cheniere Investments 80% of the expected gross margin of each cargo of LNG that Cheniere Marketing arranges for delivery to the Sabine Pass LNG terminal. To the extent payments from Cheniere Marketing to Cheniere Investments under the VCRA or new Cheniere Partners' business increase Cheniere Partners' available cash in excess of the common unit and general partner distributions and certain reserves, the cash would be distributed to Cheniere in the form of distributions on Cheniere’s subordinated units and related general partner distributions. During the term of the VCRA, Cheniere Marketing is responsible for the payment of taxes and new regulatory costs under the Cheniere Investments TUA. Cheniere has guaranteed all of Cheniere Marketing's payment obligations under the VCRA.

LNG and Natural Gas Marketing Competition

In purchasing LNG, we compete for supplies of LNG with:

• | large, multinational and national companies with longer operating histories, more development experience, greater name recognition, larger staffs and substantially greater financial, technical and marketing resources; |

• | oil and gas producers who sell or control LNG derived from their international oil and gas properties; and |

• | purchasers located in other countries where prevailing market prices can be substantially different from those in the U.S. |

In marketing LNG and natural gas, we compete for sales of LNG and natural gas with a variety of competitors, including:

• | major integrated marketers who have large amounts of capital to support their marketing operations and offer a full-range of services and market numerous products other than natural gas; |

• | producer marketers who sell their own natural gas production or the production of their affiliated natural gas production company; |

• | small geographically focused marketers who focus on marketing natural gas for the geographic area in which their affiliated distributor operates; and |

• | aggregators who gather small volumes of natural gas from various sources, combine them and sell the larger volumes for more favorable prices and terms than would be possible selling the smaller volumes separately. |

14

LNG and Natural Gas Marketing Governmental Regulation

In 1992 and 1993, the FERC concluded that sellers of short-term or long-term natural gas supplies would not have market power over the sale for resale of natural gas. The FERC established light-handed regulation over sales for resale of natural gas and adopted regulations granting blanket certificates to allow entities selling natural gas to make interstate sales for resale at negotiated rates. In 2003, the FERC amended the blanket marketing certificates to require that all sellers adhere to a code of conduct with respect to natural gas sales. The code of conduct addresses such matters as natural gas withholding, manipulation of market prices, communication of accurate information and record retention.

The EPAct contains provisions intended to prohibit the manipulation of the natural gas markets and is applicable to our LNG, pipeline and natural gas marketing businesses. See "—LNG Terminal Business—LNG Terminal Governmental Regulation" and "—Natural Gas Pipeline Business—Natural Gas Pipeline Governmental Regulation."

The prices at which we sell natural gas are not regulated, insofar as the interstate market is concerned and, for the most part, are not subject to state regulation. We are permitted to make sales of natural gas for resale in interstate commerce pursuant to a blanket marketing certificate automatically granted by the FERC. Our sales of natural gas will be affected by the availability, terms and cost of pipeline transportation. As noted above, under "—Natural Gas Pipeline Business—Natural Gas Pipeline Governmental Regulation," the price and terms of access to pipeline transportation are subject to extensive federal and state regulation.

Subsidiaries

Our assets are generally held by or under our operating subsidiaries. We conduct most of our operations through these subsidiaries, including our operations relating to the development and operation of our LNG terminal business, the development and operation of our pipeline business and the development and operation of our LNG and natural gas marketing business.

Employees and Labor Relations

We had 232 full-time employees at February 15, 2012, including 124 employees who directly supported the Sabine Pass LNG terminal operations. We consider our current employee relations to be favorable.

Available Information

Our principal executive offices are located at 700 Milam Street, Suite 800, Houston, Texas 77002, and our telephone number is (713) 375-5000. Our internet address is http://www.cheniere.com. We provide public access to our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to these reports as soon as reasonably practicable after we electronically file those materials with, or furnish those materials to, the Securities and Exchange Commission ("SEC") under the Exchange Act. These reports may be accessed free of charge through our internet website. We make our website content available for informational purposes only. The website should not be relied upon for investment purposes and is not incorporated by reference into this Form 10-K.

We will also make available to any stockholder, without charge, copies of our Annual Report on Form 10-K as filed with the SEC. For copies of this, or any other filing, please contact: Cheniere Energy, Inc., Investor Relations Department, 700 Milam Street, Suite 800, Houston, Texas 77002 or call (713) 562-5000. In addition, the public may read and copy any materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, N.E., Room 1580, Washington, D.C. 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an internet site (www.sec.gov) that contains reports, proxy and information statements and other information regarding issuers, like us, that file electronically with the SEC.

15

ITEM 1A. RISK FACTORS

The following are some of the important factors that could affect our financial performance or could cause actual results to differ materially from estimates or expectations contained in our forward-looking statements. We may encounter risks in addition to those described below. Additional risks and uncertainties not currently known to us, or that we currently deem to be immaterial, may also impair or adversely affect our business, results of operations, financial condition, liquidity and prospects.

The risk factors in this report are grouped into the following categories:

• | Risks Relating to Our Financial Matters; |

• | Risks Relating to Our LNG Terminal Business; |

• | Risks Relating to Our Natural Gas Pipeline Business; |

• | Risks Relating to Our LNG and Natural Gas Marketing Business; |

• | Risks Relating to Our LNG Businesses in General; and |

• | Risks Relating to Our Business in General. |

Risks Relating to Our Financial Matters

Our existing level of cash resources, negative operating cash flow and significant debt could cause us to have inadequate liquidity and could materially and adversely affect our business, financial condition and prospects.

As of December 31, 2011, we had $459.2 million of cash and cash equivalents and $185.1 million of restricted cash and cash equivalents, and we had $3.0 billion of total debt outstanding on a consolidated basis (before debt discounts), although we repaid $298.0 million of this debt in January 2012. We incur significant interest expense relating to the assets at the Sabine Pass LNG terminal, and we anticipate needing to incur additional debt and issue equity to finance the construction of Cheniere Partners' proposed liquefaction project. Our ability to fund our capital expenditures and refinance our indebtedness will depend on our ability to access capital markets. In addition, if we do not make a final investment decision to construct LNG trains 1 and 2 by December 31, 2012, we may not be able to refinance our existing indebtedness when it matures, including the Convertible Senior Unsecured Notes and the Senior Notes. Our costs could increase or future borrowings or equity offerings may be unavailable to us or unsuccessful, which could cause us to be unable to pay or refinance our indebtedness or to fund our other liquidity needs.

We have not been profitable historically, and we have not had positive operating cash flow. Our ability to achieve profitability and generate positive operating cash flow in the future is subject to significant uncertainty.

We had net losses of $198.8 million, $76.2 million and $161.5 million for the years ended December 31, 2011, 2010 and 2009, respectively. In addition, our net cash flow used in operating activities was $42.8 million, $16.9 million and $97.9 million for the years ended December 31, 2011, 2010 and 2009, respectively. In the future, we may incur operating losses and experience negative operating cash flow. We may not be able to reduce costs, increase revenues, or reduce our debt service obligations sufficiently to maintain our cash resources, which could cause us to have inadequate liquidity to continue our business.

In order to generate needed amounts of cash, we may sell equity or equity-related securities or assets, including equity interests in Cheniere Partners. Such sales could dilute our stockholders' proportionate indirect interests in the assets, business operations and proposed liquefaction and other projects of Cheniere Partners or other subsidiaries, and could adversely affect the market price of our common stock.

We have pursued and are pursuing a number of alternatives in order to generate needed amounts of cash, including potential issuances and sales of additional equity or equity-related securities by us, Cheniere Partners, or both, and potential sales of assets, including units of limited partner interest that we currently hold in Cheniere Partners. Such sales, in one or more transactions, could dilute our stockholders' proportionate indirect interests in the assets, business operations and proposed projects of Cheniere Partners, including its proposed liquefaction project, or in other subsidiaries. In addition, such sales, or the anticipation of such sales, could adversely affect the market price of our common stock.

16

Our ability to generate needed amounts of cash is substantially dependent upon the performance by customers under long-term contracts that we have entered into, and we could be materially and adversely affected if any customer fails to perform its contractual obligations for any reason.