Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - DEL TORO SILVER CORP. | Financial_Report.xls |

| EX-32.1 - CERTIFICATION - DEL TORO SILVER CORP. | exhibit32-1.htm |

| EX-31.2 - CERTIFICATION - DEL TORO SILVER CORP. | exhibit31-2.htm |

| EX-32.2 - CERTIFICATION - DEL TORO SILVER CORP. | exhibit32-2.htm |

| EX-31.1 - CERTIFICATION - DEL TORO SILVER CORP. | exhibit31-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C.

20549

FORM 10-K

(Mark One)

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended October 31, 2011

[ ] TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from [ ] to [ ]

Commission file number 000-52499

DEL TORO SILVER

CORP.

(Exact name of registrant as specified in its

charter)

| Nevada | 99-0515290 |

| (State or other jurisdiction of incorporation or | (I.R.S. Employer Identification No.) |

| organization) | |

| 320 North Carson Street, Carson City, NV | 89701 |

| (Address of principal executive offices) | (Zip Code) |

Registrant's telephone number, including area code: 775.782.3999

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Name of Each Exchange On Which Registered |

| N/A | N/A |

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, par value of $0.001

(Title of

class)

Indicate by check mark if the registrant is a well-known

seasoned issuer, as defined in Rule 405 the Securities Act.

Yes [ ] No [ x ]

Indicate by check mark if the registrant is not required to file

reports pursuant to Section 13 or Section 15(d) of the Act

Yes [ ] No [ x ]

Indicate by check mark whether the registrant: (1) has filed all

reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the

registrant was required to file such reports) and (2) has been subject to such

filing requirements for the last 90 days.

Yes [ x ] No [ ]

Indicate by check mark whether the registrant has submitted

electronically and posted on its corporate Website, if any, every Interactive

Data File required to be submitted and posted pursuant to Rule 405 of Regulation

S-K (§229.405 of this chapter) during the preceding 12 months (or for such

shorter period that the registrant was required to submit and post such

files).

Yes [ x ] No [ ]

Indicate by check mark if disclosure of delinquent filers

pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not

contained herein, and will not be contained, to the best of registrant's

knowledge, in definitive proxy or information statements incorporated by

reference in Part III of this Form 10-K or any amendment to this Form

10-K.

[ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer [ ] | Accelerated filer [ ] |

| Non-accelerated filer [ ] | Smaller reporting company [ x ] |

Indicate by check mark whether the registrant is a shell company

(as defined in Rule 12b-2 of the Exchange Act).

Yes [ ] No [ x ]

State the aggregate market value of voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and ask price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter.

The aggregate market value of Common Stock held by non-affiliates of the Registrant on April 29, 2011 was $555,652 based on a $0.08 closing price for the Common Stock on April 29, 2011. For purposes of this computation, all executive officers and directors have been deemed to be affiliates. Such determination should not be deemed to be an admission that such executive officers and directors are, in fact, affiliates of the Registrant.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock as of the latest practicable date.

15,462,240 shares of common stock issued & outstanding as of January 30, 2012

DOCUMENTS INCORPORATED BY REFERENCE

None.

2

Table of Contents

3

PART I

| Item 1. | Business |

This annual report contains forward-looking statements. These statements relate to future events or our future financial performance. In some cases, you can identify forward-looking statements by terminology such as “may”, “should”, “expects”, “plans”, “anticipates”, “believes”, “estimates”, “predicts”, “potential” or “continue” or the negative of these terms or other comparable terminology. These statements are only predictions and involve known and unknown risks, uncertainties and other factors, including the risks in the section entitled “Risk Factors”, that may cause our or our industry’s actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements.

Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Except as required by applicable law, including the securities laws of the United States, we do not intend to update any of the forward-looking statements to conform these statements to actual results.

Our financial statements are stated in United States Dollars (US$) and are prepared in accordance with United States Generally Accepted Accounting Principles.

In this annual report, unless otherwise specified, all dollar amounts are expressed in United States dollars and all references to “common shares” refer to the common shares in our capital stock.

As used in this annual report, the terms “we”, “us”, “our” and “our company” refer to Del Toro Silver Corp., and, unless otherwise indicated, our wholly-owned subsidiary, Minera Plata Del Toro S.A. de C.V., a Mexican corporation.

Corporate Overview

Our company was incorporated on January 9, 2006 as Candev Resource Exploration, Inc. under the laws of the State of Nevada and extra-provincially registered under the laws of the Province of British Columbia on August 15, 2006. Effective July 28, 2009, our company completed a merger with our wholly owned subsidiary, Del Toro Silver Corp., a Nevada corporation which was incorporated on July 7, 2009 solely to change our company’s name to Del Toro Silver Corp.

Our head office is located at 320 North Carson Street, Carson City, Nevada 89701.

Corporate History

We were incorporated pursuant to the laws of the State of Nevada on January 9, 2006.

Effective July 9, 2009, we completed the acquisition of a 50% undivided interest, and the Option to acquire a further 30% interest in, the Dos Naciones Property, located in state of Sonora, Mexico, in accordance with the terms of a Property Option Agreement with Yale dated July 7, 2009. We entered into an amendment agreement dated June 25, 2010, amending certain terms of the option agreement.

We entered into an amendment agreement with Yale Resources Ltd. dated as of October 21, 2010 pursuant to which we amended the Option Agreement with Yale dated July 7, 2009, as earlier amended on June 25, 2010. Pursuant to the terms of the further-amended agreement Yale agreed to grant Del Toro an option to acquire a further 20% interest in the Property (for a total of 70%) in consideration of the issuance of 250,000 more shares of our common stock upon signing of the agreement and 400,000 more shares of our common stock to Yale on or before July 7, 2012. Under the terms of the amendment Yale also agreed to rescind its option to repurchase the property during the option period.

4

In October, 2010 we announced that we expanded the Josefina target at Dos Naciones. Fieldwork completed by our company was successful in identifying multiple new exposures of veins as well as a historic working that was previously unknown. The Josefina target now consists of a series of at least six sub-parallel veins with the core of the silver/lead system having been traced along surface for approximately 600 meters along the strike and over 250 meters in width. Highlights from the 38 samples submitted are channel chip samples from the interior of the Josefina working returning 129g/t Ag with 5.23% Pb over 1.0 meters and 105g/t Ag with 4.21% Pb over 0.50 meters.

In December, 2010 we completed an ASTER (Satellite Imaging) study on the Dos Naciones property and surrounding mines, and continued our field work consisting of detailed geological mapping, sampling and prospecting towards identifying drill targets. A follow up field program in the area was commenced in January, 2011 to expand the mapping and sampling of the surrounding areas based on the ASTER report study. Based on the results of our past field program we intend to commence a drill program in April, 2011 on the La Espanola target to obtain further information on mineralization occurrences on the area.

In October, 2011, we were notified by our joint venture participant, Yale Resources Ltd., that a drilling contract has been signed with Geometrics Mineral Services S.A. de C.V. Drilling on the property began in November 2011.

In November 2011, our management announced that our company will begin to change our corporate strategy to target high grade precious metals properties, located in the western US, that have the potential for near-term production and positive cash flow.

Also on November 14, 2011, we entered into an Asset Sale Agreement with Bowerman Holdings LLC to acquire up to seventy-five percent (75%) of one hundred percent (100%) of Bowerman’s right, title and interest in and to thirty one (31) KM mining claims and seventeen (17) Raddlefinger mining claims located in Siskiyou County, California. Closing of the acquisition is scheduled to occur by May 12, 2012, unless otherwise agreed by the parties, and is subject to satisfactory completion of due diligence by our company.

In consideration of a sixty percent (60%) interest in the property, we have agreed to pay to Bowerman an aggregate purchase price of $6,525,000.00, payable as follows:

- $25,000.00 payable by December 14, 2011 (the date of the payment has been extended to March 14, 2012);

- $4,500,000 payable upon closing by execution and delivery of a promissory note and a first position deed of trust against the property, which secures our company’s full repayment of the amount due under the Promissory Note; and

- $2,000,000 payable upon closing by delivery of 40,000,000 shares of our common stock at $0.05 per Share (issued to Bowerman and certain assignees of Bowerman). We have agreed to use our good faith efforts to file with the SEC a reseller prospectus registering the Shares within 160 days of the closing, failing which we will be required to pay a $10,000 fee to Bowerman in lieu of registration.

The $4,500,000 secured by the promissory note and deed of trust shall accrue interest (on unpaid principal and interest) from November 14, 2011 at the rate of ten percent (10%) interest per annum, compounded monthly. Principal and interest shall be due and payable in full on November 14, 2014 by way of a balloon payment equal to the amount of the entire balance then-due. We may prepay all or any part of the sum due under the promissory note any time without penalty. Delinquent payments under the note will be subject to a late fee equal to 10% of the delinquent payment amount. Subject to timely payment of the promissory note and all consideration due and payable, our company is entitled to acquire, within 48 months from closing, up to an additional fifteen percent (15%) interest in the Property at a rate of $300,000 per 1%.

In addition to the $6,525,000 aggregate purchase price, we have agreed to incur, within 36 months of the closing, not less than $1,500,000 in exploration, development, or operating expenses in respect of the property. Our company’s work commitment shall be carried out in accordance with a joint operations agreement between our company and Bowerman, also entered into on November 14, 2011, whereby Bowerman and our company have agreed to jointly develop the property through January 1, 2017.

5

Pursuant to the agreement, our company and Bowerman shall form a single purpose entity to serve as the sole operator of the property, with our company serving as manager of the entity. Subject to and upon completion of the $1,500,000, 36-month work commitment to be financed by our company, subsequent work programs and budgets shall be determined by our company at our sole discretion, and the operating costs of the entity shall be shared by our company and Bowerman on a pro-rata basis with their respective ownership interest in the property. Net proceeds of the entity shall also be divided between our company and Bowerman on a pro-rata basis with their respective ownership interest in the property.

Bowerman's parent company has caused one of its wholly owned subsidiaries to conditionally license to the entity the use of all equipment, improvements and other items of personal property and improvements overlying the Property. Our company shall have the option to exercise the license by paying to Bowerman a license fee of $100,000.00 per year. At our company’s election and sole determination, our company may pay each license fee either in cash, in common shares of our company discounted by twenty percent (20%) of the then-market value, or by crediting the value of the license fee toward Bowerman’s financial obligation to pay its pro rata interest for work performed under the Joint Operations Agreement, provided that Bowerman’s obligation shall not accrue until our company’s $1,500,000 work commitment has been fully expended. Our company shall also have the option to buy out the licensed equipment and improvements. The entity shall be charged with maintaining, repairing, servicing, supplying, insuring and otherwise keeping in good condition through due care all of the equipment and improvements for the duration of the license.

Our Current Business

We are presently an exploration stage company focused on conducting exploration activities on our Dos Naciones property in Mexico. In November 2011, our management announced that our company will begin to change our corporate strategy to target high grade precious metals properties, located in the western US, with the potential for near-term production and positive cash flow. In keeping with this strategy on November 14, 2011, we entered into an Asset Sale Agreement with Bowerman Holdings LLC to acquire up to seventy-five percent (75%) of one hundred percent (100%) of the Bowerman’s right, title and interest in and to thirty one (31) KM mining claims and seventeen (17) Raddlefinger mining claims located in Siskiyou County, California. Closing of the acquisition is scheduled to occur by May 12, 2012, unless otherwise agreed by the parties, and is subject to satisfactory completion of due diligence by our company.

While our corporate strategy has changed we remain focused on exercising our option under an option agreement with Yale Resources Ltd. dated July 7, 2009, as amended June 25, 2010 and October 21, 2010. The Dos Naciones property is located approximately 140 km north northeast of the city of Hermosillo, in north-central Sonora, Mexico and is approximately 75 km southwest of the important Cananea mining district. The Dos Naciones property is comprised of one mineral concession that covers approximately 2,391 hectares.

Our company received a technical report dated March 25, 2009 from our consulting geologist David J. Pawliuk respecting the Dos Naciones property. Pursuant to the report, Mr. Pawliuk recommended a three phase exploration program on the Dos Naciones property to explore potential mineralization on the property. The report found that Dos Naciones property hosts different styles of significant metallic mineralization and that economic concentrations of silver and lead occur in quartz veins at both the Josefina and the Dos Naciones occurrence areas within the property.

We intend to conduct a three phase exploration program on the Dos Naciones Property at an aggregate estimated cost of $450,000 subject to receiving additional financing. The first phase of our exploration program commenced in July, 2010. The first phase consists of detailed geological mapping, sampling, hand trenching and prospecting. In July, 2010 our operator on the Dos Naciones property engaged geological consultants to conduct mapping and sampling on the property.

We have submitted 38 samples from the July/August 2010 work program to an assay lab to confirm the sampling results. In October, 2010, fieldwork completed by us was successful in identifying multiple new exposures of veins as well as a historic working that was previously unknown. The Josefina target now consists of a series of at least six sub-parallel veins with the core of the silver/lead system having been traced along surface for approximately 600

6

meters along strike and over 250 meters wide. Highlights from the 38 samples submitted are channel chip samples from the interior of the Josefina working returning 129g/t Ag with 5.23% Pb over 1.0 meters and 105g/t Ag with 4.21% Pb over 0.50 meters.

In December, 2010, we completed an ASTER (Satellite Imaging) study on the Dos Naciones property and surrounding mines, and continued our field work consisting of detailed geological mapping, sampling and prospecting towards identifying drill targets. A follow up field program in the area was commenced in January, 2011 to expand the mapping and sampling of the surrounding areas based on the ASTER report study. Based on the results of our past field program, we commenced a drill program at the end of 2011 October on the La Espanola target to obtain further information on mineralization occurrences on the area.

We have completed Phase I and have commenced Phase II of exploration on our Dos Naciones property. Once we complete each phase of exploration, we will make a decision as to whether or not we proceed with each successive phase based upon the analysis of the results of that program. Our management will make these decisions based upon the recommendations of the independent geologist who oversees the program and records the results.

Competition

We are a junior mineral resource exploration company. We compete with other mineral resource exploration companies for financing and for the acquisition of new mineral properties. Many of the mineral resource exploration companies with whom we compete have greater financial and technical resources than those available to us. Accordingly, these competitors may be able to spend greater amounts on acquisitions of mineral properties of merit, on exploration of their mineral properties and on development of their mineral properties. In addition, they may be able to afford more geological expertise in the targeting and exploration of mineral properties. This competition could result in competitors having mineral properties of greater quality and interest to prospective investors who may finance additional exploration and development. This competition could adversely impact on our ability to achieve the financing necessary for us to conduct further exploration of our mineral properties.

We also compete with other junior mineral resource exploration companies for financing from a limited number of investors that are prepared to make investments in junior mineral resource exploration companies. The presence of competing junior mineral resource exploration companies may impact on our ability to raise additional capital in order to fund our exploration programs if investors are of the view that investments in competitors are more attractive based on the merit of the mineral properties under investigation and the price of the investment offered to investors. We also compete with other junior and senior mineral resource exploration companies for available resources, including, but not limited to, professional geologists, camp staff, helicopter or float planes, mineral exploration supplies and drill rigs.

Governmental Regulations

Mexico

In Mexico, mineral resources belong to the Mexican nation and all mining activity requires a concession from the federal government. A concession is granted over free land, pursuant to the first in time, first right principle, which establishes that the first person to request a concession over a portion of land will have the right to the same, provided all other requirements under the Mining Law of Mexico and its associated regulations are met.

A concession owner can perform:

-

exploration works on the ground to identify mineral deposits and quantifying and evaluating economically viable reserves and accordingly perform work to develop areas containing mineral deposits; and

-

exploitation works to detach and extract minerals from such deposits.

Only Mexican nationals or legal entities incorporated under Mexican law may hold concessions, although there are no restrictions on foreign ownership of such entities. Mining concessions are granted for 50 years, and can be

7

renewed for another 50 years. The main obligations to keep them are the semi-annual payment of mining duties (taxes), based on the surface area of the concession, and the performance of work in the areas covered by the concessions, which is evidenced by minimum expenditures or by the production of ore.

In connection with mining and exploration activities in the Dos Naciones Property, we are subject to extensive Mexican federal, state and local laws and regulations governing the protection of the environment, including laws and regulations relating to protection of air and water quality, hazardous waste management and mine reclamation as well as the protection of endangered or threatened species.

Currently, we are not required to submit any environmental impact statement to the Mexican government for our proposed three phase exploration program on the Dos Naciones Property because exploration activities such as mapping and sampling do not require the preparation of the environmental impact statement. However, if, after we conduct our three phase exploration program on the Dos Naciones Property, we decided to conduct a full drilling program, we will have to prepare the environmental impact statement to be submitted to the Mexican government, which will describe the anticipated environmental impact of our planned drilling program, as well as outlining our planned actions to minimize any potential environmental damage. Studies required to support the environmental impact statement include a detailed analysis of the area, among others: soil, water, vegetation, wildlife, cultural resources and socio-economic impacts.

In reviewing the environmental impact statement, the Mexican government looks at potential impact on national Mexican environment, as well as reviewing for local concerns such as proximity to water supplies or potential interference with local farms. The Mexican government has ten days to respond after we file the environmental impact statement, and if it does not respond, authorization is deemed to have been granted. If the Mexican government does respond, then the time within which authorization will be granted can be increased to six to twelve months or longer. It is also possible that no authorization will be granted if the Mexican government is not satisfied that appropriate measures will be taken to protect the environment.

United States

Mining operations and exploration activities are subject to various national, state, provincial and local laws and regulations in the United States, as well as other jurisdictions, which govern prospecting, development, mining, production, exports, taxes, labor standards, occupational health, waste disposal, protection of the environment, mine safety, hazardous substances and other matters.

We believe that we are and will continue to be in compliance in all material respects with applicable statutes and the regulations passed in the United States. There are no current orders or directions relating to our company with respect to the foregoing laws and regulations.

Subsidiaries

We have a wholly-owned subsidiary, Minera Plata Del Toro S.A. de C.V. a Mexican corporation.

Research and Development Expenditures

We have incurred $nil in research and development expenditures over the last two fiscal years.

Employees

As of October 31, 2011, our employees were our directors and officers. We do not expect any material changes in the number of employees over the next 12 month period. We currently conduct and anticipate that we will continue to conduct most of our business through arrangements with consultants and third parties. Our officers and directors do not have an employment agreement with us.

8

REPORTS TO SECURITY HOLDERS

We are required to file annual, quarterly and current reports, proxy statements and other information with the Securities and Exchange Commission and our filings are available to the public over the internet at the Securities and Exchange Commission’s website at http://www.sec.gov. The public may read and copy any materials filed by us with the Securities and Exchange Commission at the Securities and Exchange Commission’s Public Reference Room at 100 F Street N.E. Washington D.C. 20549. The public may obtain information on the operation of the Public Reference Room by calling the Securities and Exchange Commission at 1-800-732-0330. The SEC also maintains an Internet site that contains reports, proxy and formation statements, and other information regarding issuers that file electronically with the SEC, at http://www.sec.gov.

| Item 1A. | Risk Factors |

Risks Associated with Mining

All of our properties are in the exploration stage. There is no assurance that we can establish the existence of any mineral resource on any of our properties in commercially exploitable quantities. Until we can do so, we cannot earn any revenues from operations and if we do not do so we will lose all of the funds that we expend on exploration. If we do not discover any mineral resource in a commercially exploitable quantity, our business could fail.

Despite exploration work on our mineral properties, we have not established that any of them contain any mineral reserve, nor can there be any assurance that we will be able to do so. If we do not, our business could fail.

A mineral reserve is defined by the Securities and Exchange Commission in its Industry Guide 7 (which can be viewed over the Internet at http://www.sec.gov/divisions/corpfin/forms/industry.htm#secguide7) as that part of a mineral deposit which could be economically and legally extracted or produced at the time of the reserve determination. The probability of an individual prospect ever having a “reserve” that meets the requirements of the Securities and Exchange Commission’s Industry Guide 7 is extremely remote; in all probability our mineral resource property does not contain any "reserve" and any funds that we spend on exploration will probably be lost.

Even if we do eventually discover a mineral reserve on one or more of our properties, there can be no assurance that we will be able to develop our properties into producing mines and extract those resources. Both mineral exploration and development involve a high degree of risk and few properties which are explored are ultimately developed into producing mines.

The commercial viability of an established mineral deposit will depend on a number of factors including, by way of example, the size, grade and other attributes of the mineral deposit, the proximity of the resource to infrastructure such as a smelter, roads and a point for shipping, government regulation and market prices. Most of these factors will be beyond our control, and any of them could increase costs and make extraction of any identified mineral resource unprofitable.

Mineral operations are subject to applicable law and government regulation. Even if we discover a mineral resource in a commercially exploitable quantity, these laws and regulations could restrict or prohibit the exploitation of that mineral resource. If we cannot exploit any mineral resource that we might discover on our properties, our business may fail.

Both mineral exploration and extraction require permits from various foreign, federal, state, provincial and local governmental authorities and are governed by laws and regulations, including those with respect to prospecting, mine development, mineral production, transport, export, taxation, labour standards, occupational health, waste disposal, toxic substances, land use, environmental protection, mine safety and other matters. There can be no assurance that we will be able to obtain or maintain any of the permits required for the continued exploration of our mineral properties or for the construction and operation of a mine on our properties at economically viable costs. If we cannot accomplish these objectives, our business could fail.

9

We believe that we are in compliance with all material laws and regulations that currently apply to our activities but there can be no assurance that we can continue to remain in compliance. Current laws and regulations could be amended and we might not be able to comply with them, as amended. Further, there can be no assurance that we will be able to obtain or maintain all permits necessary for our future operations, or that we will be able to obtain them on reasonable terms. To the extent such approvals are required and are not obtained, we may be delayed or prohibited from proceeding with planned exploration or development of our mineral properties.

If we establish the existence of a mineral resource on any of our properties in a commercially exploitable quantity, we will require additional capital in order to develop the property into a producing mine. If we cannot raise this additional capital, we will not be able to exploit the resource, and our business could fail.

If we do discover mineral resources in commercially exploitable quantities on any of our properties, we will be required to expend substantial sums of money to establish the extent of the resource, develop processes to extract it and develop extraction and processing facilities and infrastructure. Although we may derive substantial benefits from the discovery of a major deposit, there can be no assurance that such a resource will be large enough to justify commercial operations, nor can there be any assurance that we will be able to raise the funds required for development on a timely basis. If we cannot raise the necessary capital or complete the necessary facilities and infrastructure, our business may fail.

Mineral exploration and development is subject to extraordinary operating risks. We do not currently insure against these risks. In the event of a cave-in or similar occurrence, our liability may exceed our resources, which would have an adverse impact on our company.

Mineral exploration, development and production involve many risks which even a combination of experience, knowledge and careful evaluation may not be able to overcome. Our operations will be subject to all the hazards and risks inherent in the exploration for mineral resources and, if we discover a mineral resource in commercially exploitable quantity, our operations could be subject to all of the hazards and risks inherent in the development and production of resources, including liability for pollution, cave-ins or similar hazards against which we cannot insure or against which we may elect not to insure. Any such event could result in work stoppages and damage to property, including damage to the environment. We do not currently maintain any insurance coverage against these operating hazards. The payment of any liabilities that arise from any such occurrence would have a material adverse impact on our company.

Mineral prices are subject to dramatic and unpredictable fluctuations.

We expect to derive revenues, if any, either from the sale of our mineral resource properties or from the extraction and sale of precious and base metals such as gold, silver and copper. The price of those commodities has fluctuated widely in recent years, and is affected by numerous factors beyond our control, including international, economic and political trends, expectations of inflation, currency exchange fluctuations, interest rates, global or regional consumptive patterns, speculative activities and increased production due to new extraction developments and improved extraction and production methods. The effect of these factors on the price of base and precious metals, and therefore the economic viability of any of our exploration properties and projects, cannot accurately be predicted.

The mining industry is highly competitive and there is no assurance that we will continue to be successful in acquiring mineral claims. If we cannot continue to acquire properties to explore for mineral resources, we may be required to reduce or cease operations.

The mineral exploration, development, and production industry is largely un-integrated. We compete with other exploration companies looking for mineral resource properties. While we compete with other exploration companies in the effort to locate and acquire mineral resource properties, we will not compete with them for the removal or sales of mineral products from our properties if we should eventually discover the presence of them in quantities sufficient to make production economically feasible. Readily available markets exist worldwide for the sale of mineral products. Therefore, we will likely be able to sell any mineral products that we identify and produce.

10

In identifying and acquiring mineral resource properties, we compete with many companies possessing greater financial resources and technical facilities. This competition could adversely affect our ability to acquire suitable prospects for exploration in the future. Accordingly, there can be no assurance that we will acquire any interest in additional mineral resource properties that might yield reserves or result in commercial mining operations.

If our costs of exploration are greater than anticipated, then we may not be able to complete the exploration program for our Dos Naciones Property without additional financing, of which there is no assurance that we would be able to obtain.

We are proceeding with the initial stages of exploration on our Dos Naciones Property. We intend to carry out an exploration program that has been recommended by a consulting geologist. This exploration program outlines a budget for completion of the recommended exploration program. However, there is no assurance that our actual costs will not exceed the budgeted costs. Factors that could cause actual costs to exceed budgeted costs include increased prices due to competition for personnel and supplies during the exploration season, unanticipated problems in completing the exploration program and delays experienced in completing the exploration program. Increases in exploration costs could result in our not being able to carry out our exploration program without additional financing. There is no assurance that we would be able to obtain additional financing in this event.

Because of the speculative nature of exploration of mining properties, there is substantial risk that no commercially exploitable minerals will be found and our business will fail.

We are in the initial stage of exploration of our mineral property, and thus have no way to evaluate the likelihood that we will be successful in establishing commercially exploitable reserves of gold, silver or other valuable minerals on our Dos Naciones Property. The search for valuable minerals as a business is extremely risky. We may not find commercially exploitable reserves of gold, silver or other valuable minerals in our mineral property. Exploration for minerals is a speculative venture necessarily involving substantial risk. The expenditures to be made by us on our exploration program may not result in the discovery of commercial quantities of ore. The likelihood of success must be considered in light of the problems, expenses, difficulties, complications and delays encountered in connection with the exploration of the mineral properties that we plan to undertake. Problems such as unusual or unexpected formations and other conditions are involved in mineral exploration and often result in unsuccessful exploration efforts. In such a case, we would be unable to complete our business plan.

Because of the inherent dangers involved in mineral exploration, there is a risk that we may incur liability or damages as we conduct our business.

The search for valuable minerals involves numerous hazards. In the course of carrying out exploration of our Dos Naciones Property, we may become subject to liability for such hazards, including pollution, cave-ins and other hazards against which we cannot insure or against which we may elect not to insure. We currently have no such insurance nor do we expect to get such insurance for the foreseeable future. If a hazard were to occur, the costs of rectifying the hazard may exceed our asset value and cause us to liquidate all of our assets, resulting in the loss of your entire investment in our company.

Because access to our mineral property is often restricted by inclement weather, we may be delayed in our exploration and any future mining efforts.

Access to the mineral property is restricted to the period between August to March of each year because the period between April to July is typically rainy season in the area. We can attempt to visit, test or explore our mineral property only when weather permits such activities. These limitations can result in significant delays in exploration efforts, as well as in mining and production in the event that commercial amounts of minerals are found. Such delays can cause our business to fail.

11

As we undertake exploration of our mineral property, we will be subject to compliance with government regulation that may increase the anticipated time and cost of our exploration program, which could increase our expenses.

We will be subject to the mining laws and regulations in Mexico as we carry out our exploration program. We will be required to pay mining taxes to the Mexican government. We will be required to prove our compliance with relevant Mexican environmental and workplace safety laws, regulations and standards by submitting receipts showing the purchase of equipment used for workplace safety or the prevention of pollution or the undertaking of environmental remediation projects before we are able to obtain drilling permits. If our exploration activities lead us to make a decision to go into mining production, before we initiate a major drilling program, we will have to obtain an environmental impact statement authorization. This could potentially take more than 10 months to obtain and could potentially be refused. New regulations, if any, could increase our time and costs of doing business and prevent us from carrying out our exploration program. These factors could prevent us from becoming profitable.

Because our executive officers have limited experience in mineral exploration and do not have formal training specific to the technicalities of mineral exploration, there is a higher risk that our business will fail.

Our executive officers have limited experience in mineral exploration and do not have formal training as geologists or in the technical aspects of management of a mineral resource exploration company. As a result of this inexperience, there is a higher risk of our being unable to complete our business plan for the exploration of our mineral property. With no direct training or experience in these areas, our management may not be fully aware of many of the specific requirements related to working within this industry. Our decisions and choices may not take into account standard engineering or managerial approaches mineral resource exploration companies commonly use. Consequently, the lack of training and experience of our management in this industry could result in management making decisions that could result in a reduced likelihood of our being able to locate commercially exploitable reserves on our mineral property with the result that we would not be able to achieve revenues or raise further financing to continue exploration activities. In addition, we will have to rely on the technical services of others with expertise in geological exploration in order for us to carry out our planned exploration program. If we are unable to contract for the services of such individuals, it will make it difficult and maybe impossible to pursue our business plan. There is thus a higher risk that our operations, earnings and ultimate financial success could suffer irreparable harm and our business will likely fail.

Because our executive officers have other business interests, they may not be able or willing to devote a sufficient amount of time to our business operation, causing our business to fail.

Greg Painter, our president and chief executive officer, devotes approximately 80% of his working time on providing management services to us and Patrick Fagen our chief financial officer, devotes approximately 40% of his working time on providing management services to us. If the demands on our executive officers from their other obligations increase, they may no longer be able to devote sufficient time to the management of our business. This could negatively impact our business development.

Risks Related to Our Company

We have a limited operating history on which to base an evaluation of our business and prospects.

We have been in the business of exploring mineral resource properties since January 2006 and we have not yet located any mineral reserve. As a result, we have never had any revenues from our operations. In addition, our operating history has been restricted to the acquisition and exploration of our mineral properties and this does not provide a meaningful basis for an evaluation of our prospects if we ever determine that we have a mineral reserve and commence the construction and operation of a mine. We have no way to evaluate the likelihood of whether our mineral properties contain any mineral reserve or, if they do that we will be able to build or operate a mine successfully. We anticipate that we will continue to incur operating costs without realizing any revenues during the period when we are exploring our properties. We therefore expect to continue to incur significant losses into the foreseeable future. We recognize that if we are unable to generate significant revenues from mining operations and any dispositions of our properties, we will not be able to earn profits or continue operations. At this early stage of our operation, we also expect to face the risks, uncertainties, expenses and difficulties frequently encountered by companies at the start up stage of their business development. We cannot be sure that we will be successful in

12

addressing these risks and uncertainties and our failure to do so could have a materially adverse effect on our financial condition. There is no history upon which to base any assumption as to the likelihood that we will prove successful and we can provide investors with no assurance that we will generate any operating revenues or ever achieve profitable operations.

The fact that we have not earned any operating revenues since our incorporation raises substantial doubt about our ability to continue to explore our mineral properties as a going concern.

We have not generated any revenue from operations since our incorporation and we anticipate that we will continue to incur operating expenses without revenues unless and until we are able to identify a mineral resource in a commercially exploitable quantity on one or more of our mineral properties and we build and operate a mine. At October 31, 2011 we had a working capital deficit of $3,921. We incurred a net loss of $243,763 for the year ended October 31, 2011 and $1,071,969 since inception. We will require additional financing to sustain our business operations if we are not successful in earning revenues once exploration is complete. If our exploration programs are successful in discovering reserves of commercial tonnage and grade, we will require significant additional funds in order to place the Dos Naciones Property into commercial production. Should the results of our planned exploration require us to increase our current operating budget, we may have to raise additional funds to meet our currently budgeted operating requirements for the next 12 months. As we cannot assure a lender that we will be able to successfully explore and develop our mineral properties, we will probably find it difficult to raise debt financing from traditional lending sources. We have traditionally raised our operating capital from sales of equity and debt securities, but there can be no assurance that we will continue to be able to do so. If we cannot raise the money that we need to continue exploration of our mineral properties, we may be forced to delay, scale back, or eliminate our exploration activities. If any of these were to occur, there is a substantial risk that our business would fail.

These circumstances lead our independent registered public accounting firm, in their report dated January 24, 2012, to comment about our company’s ability to continue as a going concern. When an auditor issues a going concern opinion, the auditor has substantial doubt that the company will continue to operate indefinitely and not go out of business and liquidate its assets. These conditions raise substantial doubt about our company’s ability to continue as a going concern. The financial statements do not include any adjustments relating to the recoverability and classification of recorded assets, or the amounts of and classification of liabilities that might be necessary in the event our company cannot continue in existence. We continue to experience net operating losses.

Risks Associated with Our Common Stock

Trading on the OTC Bulletin Board may be volatile and sporadic, which could depress the market price of our common stock and make it difficult for our stockholders to resell their shares.

Our common stock is quoted on the OTC Bulletin Board service of the Financial Industry Regulatory Authority. Trading in stock quoted on the OTC Bulletin Board is often thin and characterized by wide fluctuations in trading prices, due to many factors that may have little to do with our operations or business prospects. This volatility could depress the market price of our common stock for reasons unrelated to operating performance. Moreover, the OTC Bulletin Board is not a stock exchange, and trading of securities on the OTC Bulletin Board is often more sporadic than the trading of securities listed on a quotation system like NASDAQ or a stock exchange like Amex. Accordingly, shareholders may have difficulty reselling any of their shares.

Our stock is a penny stock. Trading of our stock may be restricted by the Securities and Exchange Commission’s penny stock regulations which may limit a stockholder’s ability to buy and sell our stock.

Our stock is a penny stock. The Securities and Exchange Commission has adopted Rule 15g-9 which generally defines “penny stock” to be any equity security that has a market price (as defined) less than $5.00 per share or an exercise price of less than $5.00 per share, subject to certain exceptions. Our securities are covered by the penny stock rules, which impose additional sales practice requirements on broker-dealers who sell to persons other than established customers and “accredited investors”. The term “accredited investor” refers generally to institutions with assets in excess of $5,000,000 or individuals with a net worth in excess of $1,000,000 or annual income exceeding $200,000 or $300,000 jointly with their spouse. The penny stock rules require a broker-dealer, prior to a transaction in a penny stock not otherwise exempt from the rules, to deliver a standardized risk disclosure document in a form

13

prepared by the Securities and Exchange Commission which provides information about penny stocks and the nature and level of risks in the penny stock market. The broker-dealer also must provide the customer with current bid and offer quotations for the penny stock, the compensation of the broker-dealer and its salesperson in the transaction and monthly account statements showing the market value of each penny stock held in the customer’s account. The bid and offer quotations, and the broker-dealer and salesperson compensation information, must be given to the customer orally or in writing prior to effecting the transaction and must be given to the customer in writing before or with the customer’s confirmation. In addition, the penny stock rules require that prior to a transaction in a penny stock not otherwise exempt from these rules, the broker-dealer must make a special written determination that the penny stock is a suitable investment for the purchaser and receive the purchaser’s written agreement to the transaction. These disclosure requirements may have the effect of reducing the level of trading activity in the secondary market for the stock that is subject to these penny stock rules. Consequently, these penny stock rules may affect the ability of broker-dealers to trade our securities. We believe that the penny stock rules discourage investor interest in, and limit the marketability of, our common stock.

The Financial Industry Regulatory Authority sales practice requirements may also limit a stockholder’s ability to buy and sell our stock.

In addition to the “penny stock” rules described above, the Financial Industry Regulatory Authority, which we refer to as FINRA, has adopted rules that require that in recommending an investment to a customer, a broker-dealer must have reasonable grounds for believing that the investment is suitable for that customer. Prior to recommending speculative low-priced securities to their non-institutional customers, broker-dealers must make reasonable efforts to obtain information about the customer’s financial status, tax status, investment objectives and other information. Under interpretations of these rules, the FINRA believes that there is a high probability that speculative low-priced securities will not be suitable for at least some customers. The FINRA requirements make it more difficult for broker-dealers to recommend that their customers buy our common stock, which may limit your ability to buy and sell our stock and have an adverse effect on the market for shares of our common stock.

Trends, Risks and Uncertainties

We have sought to identify what we believe to be the most significant risks to our business, but we cannot predict whether, or to what extent, any of such risks may be realized nor can we guarantee that we have identified all possible risks that might arise. Investors should carefully consider all of such risk factors before making an investment decision with respect to our common shares.

| Item 1B. | Unresolved Staff Comments |

As a “smaller reporting company”, we are not required to provide the information required by this Item.

| Item 2. | Properties |

Our principal offices are located at 320 North Carson Street, Carson City, Nevada 89701. Our office space is provided to us without cost. We believe that our office space and facilities are sufficient to meet our present needs and do not anticipate any difficulty securing alternative or additional space, as needed, on terms acceptable to us.

Mineral Properties

We own a 50% undivided interest in the Dos Naciones Property and have the option to acquire an additional 20% pursuant to the terms of our Option Agreement, as amended June 25, 2010 and October 21, 2010, with Yale Resources Ltd. The mineral concession that forms the Dos Naciones property was staked by Minera Alta Vista, S.A. de C.V. (Minera Alta Vista), a Mexican company that is a subsidiary of Yale Resources Ltd. Mineral concession Dos Naciones, number 230649, was registered September 28, 2007 and expires September 27, 2057. The concession is registered by the Government of Mexico in Book 366 Page 155 Act 309. This exploration concession covers an area of 2930.8269 ha, and is currently registered in the name of Minera Alta Vista, S.A. de C.V. Title to the concession is currently held in the name of Minera Alta Vista, upon exercise of the Option by our company, title to 70% of the concession will be transferred to our wholly owned Mexican subsidiary. The Dos Naciones mineral

14

concession lies within the municipalities of Opodepe and Cucurpe, Sonora. Payments of 40,394.68 pesos are paid every semester, i.e., twice per year, to the Government of Mexico in order to maintain the rights to the mineral concession. This amount increases every two years. Our joint venture partner Yale Resources Ltd. has spent approximately $100,000 on property exploration to date.

Technical Report

We received a technical report dated March 25, 2009 from its consulting geologist David J. Pawliuk, P. Geo, respecting the Dos Naciones property. Pursuant to the report, Mr. Pawliuk recommended a three phase exploration program on the Dos Naciones Property to explore potential mineralization on the property. The report found that Dos Naciones Property hosts different styles of metallic mineralization and that economic concentrations of silver and lead occur in quartz veins at both the Josefina and the Dos Naciones occurrence areas within the property.

The report also concluded that there were extensive areas of skarn occurring within the Dos Naciones property at the La Espanola area, and at the Dos Naciones occurrence area. These skarns contain potentially economic concentrations of copper, silver and gold. Skarns often form around the periphery of porphyry copper mineralizing systems. Lead- and silver-bearing quartz veining occurs along a fault zone that strikes 130 degrees and dips 55 degrees to the northeast at the east side of the Dos Naciones occurrence area; this veining is approximately parallel to the mineralized quartz veins at Josefina. The report further concluded that the geological setting of the Dos Naciones property area is favourable for bulk-tonnage porphyry copper deposits.

The report recommended a three phase exploration program on the Dos Naciones Property at an aggregate estimated cost of $450,000. The first phase of our exploration program consisted of detailed geological mapping, sampling, hand trenching and prospecting. In July, 2010 our operator on the Dos Naciones property engaged geological consultants to conduct mapping and sampling on the property. In October 2011, we commenced the second phase of our exploration program with a planned 300 metre 3 hole diamond drilling program. The drilling was successful in confirming the high potential for multiple at-surface skarn targets. Drilling in the strongly altered and fractured ground proved very difficult and each of the three holes was terminated before reaching the target depth due to technical reasons. The table below summarizes the results received:

| Drill Hole | From | To | Interval | Cu (%) | Au (g/t) | Ag (g/t) |

| D2N-01 | 0.00 | 10.50 | 10.50 | 1.04 | 0.08 | 33.3 |

| D2N-01 | 29.70 | 30.45 | 0.75 | 0.21 | 1.50 | 88.3 |

| D2N-02 | Hole lost at 12.0 m | |||||

| D2N-03 | 4.50 | 14.50 | 10.00 | 0.76 | 0.12 | 9.3 |

| Including: | 8.85 | 9.45 | 0.60 | 5.45 | 0.58 | 50.7 |

The results of this second phase of our exploration program warrant the continuation into the third phase of the program. The timing and scale of the next phase of work has yet to be determined but the company is working with Yale to determine how best to advance the exploration at Dos Naciones.

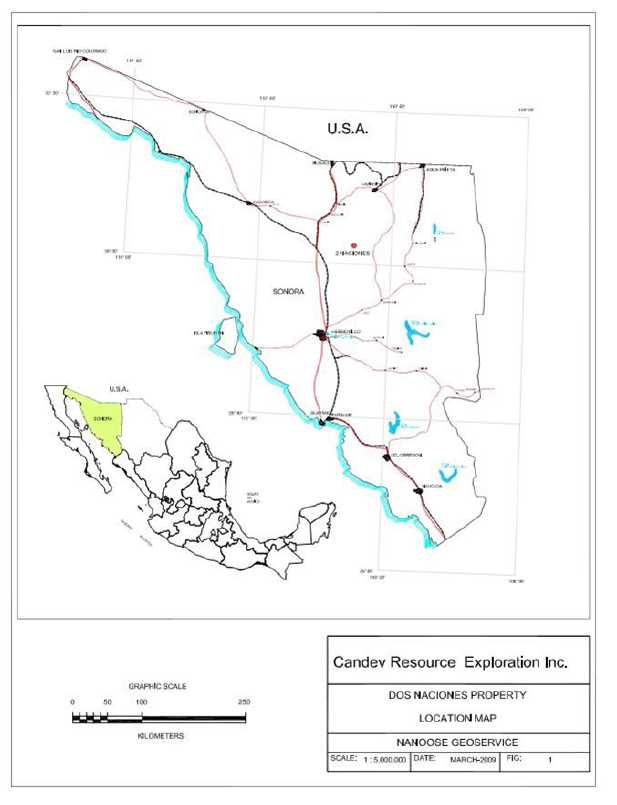

Description of Property, Location, Means and Access

The Dos Naciones Property is located approximately 140 km north northeast of the city of Hermosillo, in north-central Sonora, Mexico (See Figure 1 below). The Dos Naciones Property is located approximately 75 km southwest of the important Cananea mining district (Figure 1). The Dos Naciones Property is comprised of one mineral concession, or lode, that covers approximately 2,391 hectares. The Dos Naciones mineral concession measures approximately 5 km east-west by 5 km north-south; it surrounds the “CRUZ” concession, which covers an area of

15

100 hectares. The Dos Naciones Property is accessible via a gravel road that leads to Rancho Los Janos; this gravel road leads southward from the paved road between Magdalena de Kino and the village of Los Janos. The turnoff southwards to Rancho Los Janos is about 10 km east of the village of Cucurpe. Four-wheel-drive roads extend southwards beyond the ranch buildings and provide good access to all parts of the property. About 3 hours is required to drive from Hermosillo to the Dos Naciones Property.

There is a turf airstrip about 850 m long within the northeast corner of the concession area. However, this airstrip has been de-activated by erecting fence posts at intervals along the length of the airstrip, in order to prevent it’s use. There is an electrical powerline extending north from the village of Cucurpe to the Mina Santa Gertrudis, a former gold-producing mine located about 45 km north of the Dos Naciones Property. Cucurpe is about 20 km northwest of the Dos Naciones Property.

16

Figure 1 – Location of Dos Naciones Claim

17

Climate, Local Resources, Infrastructure And Physiography

The climate within the property area is semi-arid, typical of higher elevations in the Sonoran desert. Seasonal rains occur between April and July. The local ranchers have constructed dams along creek drainages within the property area, to collect runoff water for their livestock. Magdalena de Kino is the nearest community with fuel and full services. Magdalena de Kino is situated along the Pan-American Highway about 85 km south of the United States border at Nogales. The Dos Naciones Property area forms part of the Sierra El Jucaral, a north northwest trending mountain range on the western fringe of the Sierra Madre de Occidental. Elevations range between 1,140 and 1,690 m a.s.l. within the property area. The hillsides are moderately steep and thinly forested by scrub oak trees. Rock outcrop is exposed over about 10 to 20 per cent of the Dos Naciones Project property area.

North-central Sonora has undergone intermittent exploration since the time of the copper discoveries at Nacozari in 1660 and at Cananea in 1760 (Heylmun, 1996). Northern Sonora is one of the most important mining areas in Mexico. A variety of different types of mineral deposits have been mined within the region, including porphyry copper deposits at Cananea and Nacozari, Carlin-type gold deposits at Santa Gertrudis and Amelia, and gold-silver veins at Klondike and Las Chispas (Heylmun, 1996; Figure 1).

History of Exploration

Silver- and lead-bearing quartz veins have been mined in at least two places on the Dos Naciones property, at Josefina and at the Dos Naciones occurrence area. Historic workings on the Dos Naciones property include pits and short adits excavated to extract copper from skarns. Silver- and lead-bearing quartz veins have been mined at the Dos Naciones occurrence area, in the southwest corner of the Dos Naciones property. There is a 30 m deep shaft excavated within granitic intrusive rock at the Dos Naciones occurrence area. From the size of the mine dump piles, the writer estimates that at least 1,000 tonnes of vein material has been mined at Dos Naciones occurrence area. There has been limited historic mining of the copper- and iron-bearing skarns at the Dos Naciones occurrence area. One skarn body in this area extends across 100 m by 20 m, and the other skarn body is 180 m long by 75 m wide.

La Espanola area is on the eastern side of the Dos Naciones property. Minera Alta Vista has determined that six drillholes have been completed in the La Espanola area. Anecdotal evidence suggests that these holes were drilled during the 1990’s by Penoles, the largest mining company in Mexico. The results of this drilling are unknown to the Company’s consulting geologist. Minera Alta Vista is currently seeking additional information pertaining to these drill holes.

The most recent known exploration work on the Dos Naciones property was geological mapping and geochemical rock sampling by Minera Alta Vista, S.A. de C.V., a wholly owned subsidiary of Yale Resources Ltd. The geochemical rock sampling was mainly done in areas of historic workings within the property area. Results of this work indicated that economic concentrations of silver and lead are present in quartz veins which occur at two places on the property.

Geological Setting and Mineralization

The economic mineralization encountered to date on the Dos Naciones Project property is quartz veins containing galena, silver and minor gold. In addition, skarn or calc-silicate rocks at Dos Naciones locally contain gold, silver and copper. Thus, there have been at least two episodes of gold and silver mineralization at the Dos Naciones Property.

The geological setting of the Dos Naciones property is favourable for economic porphyry copper deposits. The Dos Naciones Project property area is within the Cananea district of northern Sonora. The Cananea district was mapped by Teran Martinez et al. (1999) of the Servicio Geologico Mexicano at 1:250,000 scale. A wide variety of sedimentary, igneous and metamorphic rocks of various ages occur in the region; the geologic history of this region is relatively complex. The oldest rock units within the property region are gneisses of Early Proterozoic age that belong to the Bamori Metamorphic Complex, which formed as a result of the Mazatazal Orogeny. These gneisses occur about 15 km to the south, and to the southeast, of the Dos Naciones property area. Granite of Proterozoic age is also exposed south of the property.

18

Areas of Cambrian age quartzite have been mapped within the Dos Naciones property. The next youngest rocks are extensive sedimentary and volcanic rocks of Jurassic age. These include rhyolite and sandstone of possible Early Jurassic age and younger sandstone, siltstone, argillite and minor limestone of Late Jurassic age; andesite flows are locally interstratified with the Late Jurassic sedimentary rocks. Late Jurassic sandstone hosts most of the gold and silver occurrences northeast of Cucurpe. Limestone and shale of Cretaceous age overlie the Late Jurassic sedimentary rocks to the west of the Dos Naciones property. The stratified rock units are intruded by a large body of granodiorite and granite of Late Cretaceous and Early Tertiary age known as the Laramide Batholith. Cretaceous-aged limestone and shale are overlain by Tertiary rhyolite to the east of Dos Naciones. Tertiary conglomerate covers much of the property region, especially the sides of the wide, northerly trending valleys. Regional deformation has resulted in numerous faults crosscutting the Dos Naciones Property area. Most of these faults have likely been reactivated at different times. Regional-scale, northerly trending normal faults indicate that east-west crustal extension has occurred since the Tertiary Period.

Mineralization

The economic mineralization encountered to date on the Dos Naciones Project property is quartz veins containing galena, silver and minor gold. In addition, skarn or calc-silicate rocks at Dos Naciones locally contain gold, silver and copper. Thus, there have been at least two episodes of gold and silver mineralization at the Dos Naciones property. The geological setting of the Dos Naciones property is favourable for economic porphyry copper deposits.

Dos Naciones Occurrence Area

Silver- and lead-bearing quartz veins have been mined at the Dos Naciones occurrence area, in the southwest corner of the Dos Naciones property. There is a 30 m deep shaft excavated within granitic intrusive rock at the Dos Naciones occurrence area, which shows the geology and sampling at the Dos Naciones occurrence area. No vein is exposed in the sides of the shaft opening, and David Pawliuk did not attempt to enter the shaft. The size and attitude of the mineralized vein in these underground workings is unknown. However, the vein is at least 30 cm wide, because vein quartz pieces up to 30 cm in diameter were found in the dump pile. The mineralized vein may possibly occur along the contact between the argillite wallrock and the intrusive granodiorite. A short quartz vein crosscutting argillite is exposed downslope of the old workings, near the contact with the intrusive granodiorite; this vein dips to the southwest. The old mine workings at the Dos Naciones occurrence area are spaced over a distance of about 250 m on surface, indicating that the mineralized silver-lead quartz vein here extends at least 250 m along strike.

From the size of the mine dump piles, David Pawliuk estimates that at least 1,000 tonnes of vein material has been mined at Dos Naciones occurrence area. A select sample, number E51556, of the better-mineralized vein material from this dump collected by David Pawliuk contains 221 parts per million (ppm) or 221 g/t silver, 4.44% lead and 0.636% zinc. Historic sample 464311 of select material from the same dump contained 88 g/t silver, 1.75% lead and 1% zinc.

Josefina Area

Silver- and lead-bearing quartz veins have been mined at the Josefina area in the central part of the Dos Naciones property. There are at least three quartz veins within the Josefina area. These veins dip steeply to the northeast, extend for at least 250 m along strike, and are open along strike and at depth. A short shaft has been excavated within one of these quartz veins.

David Pawliuk collected rock sample E51559 from a mineralized quartz vein at Josefina, as a check on the results for historic sample 464345. The quartz vein here is milky white with traces of light brown limonite along weathered fracture surfaces; no sulphide minerals were seen. The vein dips at about 60 degrees to the east. This vein is almost certainly emplaced along a fault; there is a 6 or 8 cm wide band within the central part of the vein that is finely banded on a mm scale. The vein quartz is sugary and sandy within this band, indicating movement after the vein was emplaced. The quartz vein formed during at a series of pulses; there are at least seven distinct bands within the vein; each of these bands is marked by subhedral quartz crystals lining open spaces within the vein. The bands are up to 4 cm wide. Open cavities within the vein locally are up to 10 by 25 by 8 cm across. Sample E51559 contains 22.3 g/t silver, 0.044 g/t gold, 0.354% lead and 137 ppm zinc across 1.8 m. Historic sample 464345 from the same site contained 39 g/t silver, less than 0.005 g/t gold, 0.40% lead and 69 ppm zinc.

19

In October, 2010, fieldwork completed by our company was successful in identifying multiple new exposures of veins as well as a historic working that was previously unknown. The Josefina target now consists of a series of at least six sub-parallel veins with the core of the silver/lead system having been traced along surface for approximately 600 meters along strike and over 250 meters wide. Highlights from the 38 samples submitted are channel chip samples from the interior of the Josefina working returning 129g/t Ag with 5.23% Pb over 1.0 meters and 105g/t Ag with 4.21% Pb over 0.50 meters.

La Espanola

La Espanola area is on the east side of the Dos Naciones property. Here, David Pawliuk saw a reverse circulation drillsite that appears to be several years old. Minera Alta Vista has determined that six drillholes were completed in the La Espanola area during the 1990’s. Anecdotal evidence suggests that these holes were drilled by Penoles, the largest mining company in Mexico. The results of this drilling are unknown to David Pawliuk. Minera Alta Vista is currently seeking additional information pertaining to these drill holes.

Sample Preparation, Analysis and Security

David Pawliuk collected four geochemical rock samples from the Dos Naciones Project property area on March 9, 2009. Three of these samples were collected from Dos Naciones occurrence area, and one from the Josefina area. The rock samples were bagged, and the bags were sealed by David Pawliuk. The samples were then transported via truck from Dos Naciones property to Minera Alta Vista’s offices at Hermosillo, Sonora. The samples were delivered to ALS Chemex Laboratories in Hermosillo on March 10, 2009 by David Pawliuk. David Pawliuk maintained custody of the samples from the time the samples were collected until the samples were delivered to ALS Chemex Laboratories facility at Hermosillo. The rocks were analyzed for gold by geochemical fire assay, solvent extraction and atomic adsorption spectrometry. A subsample of 30 gm was assayed. The rock sample was also analyzed for silver, mercury, arsenic, antimony and 46 other elements by aqua regia acid digestion ICPMS.

Data Verification

The results of geochemical rock sampling show that economic concentrations of silver and gold occur in quartz veins from two separate areas within the Dos Naciones property. Limited historic production has occurred from these veins. The results of geochemical rock sampling also show that copper-iron skarns within the Dos Naciones property also contain gold and silver. Skarns have also been mined within the property area. As outlined above in the section on mineralization, the results of David Pawliuk’s geochemical rock sampling confirmed the results of historic sampling on the property by Yale Resources Ltd. during 2008.

| Item 3. | Legal Proceedings |

There are no proceedings in which any of our directors, officers or affiliates, or any registered or beneficial shareholder, is an adverse party or has a material interest adverse to our company.

| Item 4. | [Removed and Reserved] |

PART II

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

In the United States, our common shares are quoted on the Over-the-Counter Bulletin Board under the symbol “DTOR.” The following quotations, obtained from Yahoo Finance, reflect the high and low bids for our common shares based on inter-dealer prices, without retail mark-up, mark-down or commission and may not represent actual transactions.

20

Our common shares were originally quoted for trading on the OTCBB on July 12, 2007 under the symbol “CVRX”.

The high and low bid prices of our common stock for the periods indicated below are as follows:

| OTC Bulletin Board(1) | ||

| Quarter Ended | High | Low |

| October 31, 2011 | $0.095 | $0.02 |

| July 31, 2011 | $0.10 | $0.06 |

| April 30, 2011 | $0.20 | $0.07 |

| January 31, 2011 | $0.28 | $0.125 |

| October 31, 2010 | $0.35 | $0.12 |

| July 31, 2010 | $0.35 | $0.04 |

| April 30, 2010 | $0.15 | $0.08 |

| January 31, 2010 | $0.15 | $0.05 |

| October 31, 2009 | $0.28 | $0.05 |

(1) Over-the-counter market quotations reflect inter-dealer prices without retail mark-up, mark-down or commission, and may not represent actual transactions.

Our transfer agent is Valiant Trust Company, of 600 – 750 Cambie Street, Vancouver, BC, Canada V6B 0A2; telephone number: 604-699-4884; facsimile: 604-681-3067.

On October 31, 2011, the shareholders list showed 64 registered shareholders, 15,462,240 common shares.

Dividend Policy

There are no restrictions in our articles of incorporation or bylaws that prevent us from declaring dividends. The Nevada Revised Statutes, however, do prohibit us from declaring dividends where, after giving effect to the distribution of the dividend:

| 1. |

We would not be able to pay our debts as they become due in the usual course of business; or |

| 2. |

Our total assets would be less than the sum of our total liabilities plus the amount that would be needed to satisfy the rights of shareholders who have preferential rights superior to those receiving the distribution. |

We have not declared any dividends and we do not plan to declare any dividends in the foreseeable future.

Recent Sales of Unregistered Securities; Use of Proceeds from Registered Securities

We did not sell any equity securities which were not registered under the Securities Act during the year ended October 31, 2011 that were not otherwise disclosed on our quarterly reports on Form 10-Q or our current reports on Form 8-K filed during the year ended October 31, 2011.

Equity Compensation Plan Information

We have no long-term incentive plans, other than the Stock Option Plan described below.

21

2010 Stock Option Plan

On September 7, 2010 our directors approved the adoption of our 2010 Stock Option Plan which permits our company to grant up to 5,000,000 options to acquire shares of common stock, to directors, officers, employees and consultants of our company.

| Equity Compensation Plan Information | |||

Plan category |

Number of securities to be issued upon exercise of outstanding options, warrants and rights |

Weighted-average exercise price of outstanding options, warrants and rights |

Number of securities

remaining available for future issuance under equity compensation plans (excluding securities reflected in column (a)) |

| Equity compensation plans approved by security holders |

Nil |

Nil |

Nil |

| Equity compensation plans not approved by security holders |

1,000,000 |

$0.10 |

Nil |

| Total | 1,000,000 | $0.10 | Nil |

Purchase of Equity Securities by the Issuer and Affiliated Purchasers

We did not purchase any of our shares of common stock or other securities during the fourth quarter of our fiscal year ended October 31, 2011.

| Item 6. | Selected Financial Data |

As a “smaller reporting company”, we are not required to provide the information required by this Item.

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

The following discussion should be read in conjunction with our audited consolidated financial statements and the related notes for the years ended October 31, 2011 and October 31, 2010 that appear elsewhere in this annual report. The following discussion contains forward-looking statements that reflect our plans, estimates and beliefs. Our actual results could differ materially from those discussed in the forward looking statements. Factors that could cause or contribute to such differences include, but are not limited to those discussed below and elsewhere in this annual report, particularly in the section entitled "Risk Factors" beginning on page 9 of this annual report.

Our audited consolidated financial statements are stated in United States Dollars and are prepared in accordance with United States Generally Accepted Accounting Principles.

Our plan of operation is to carry out exploration work on our Dos Naciones Property in order to ascertain whether it possesses commercially exploitable quantities of gold, silver, and other metals. We intend to primarily explore for gold, silver, and copper but if we discover that our mineral property holds potential for other minerals that our management determines are worth exploring further, then we intend to explore for those other minerals. We will not be able to determine whether or not the Dos Naciones Property contains a commercially exploitable mineral deposit, or reserve, until appropriate exploratory work is done and an economic evaluation based on that work indicates economic viability.

22

The three phase exploration program on the Dos Naciones property carries an aggregate estimated cost of $450,000. The first phase of our exploration program was completed during the quarter ended October 31, 2010and consisted of detailed geological mapping, sampling, hand trenching and prospecting. In July, 2010 our company’s operator on the Dos Nactiones property engaged geological consultants to conduct mapping and sampling on the property. Our company commenced the second phase of its exploration program in September, 2011. The results of this second phase of our exploration program warrant the continuation into the third phase of the program. The timing and scale of the next phase of work has yet to be determined but the company is working with Yale to determine how best to advance the exploration at Dos Naciones. A detailed breakdown of the proposed budget and work exploration program is as follows:

Estimated Dos Naciones Work Program Costs

Phase One

| Detailed geological mapping, stripping and trenching | Cost | ||

| 1 Geologist for 50 days @ $300 per day: | $ | 15,000 | |

| 3 Field Assistants for 50 days @ $100 per day: | $ | 15,000 | |

| Food and accommodation @ $30 per man-day: | $ | 6,000 | |

| Field supplies: | $ | 1,000 | |

| Vehicle rental, fuel and maintenance: | $ | 5,000 | |

| Analytical costs: 300 samples @ $30 per sample: | $ | 9,000 | |

| Total geological mapping, stripping and trenching: | $ | 51,000 | |

| Report preparation | |||

| For reporting on all of the above work, including drafting: | $ | 2,500 | |

| Subtotal Phase One | $ | 53,500 |

Phase Two

| IP surveying in area of aeromagnetic low | |||

| 15 days of surveying along cut grid lines with pickets at 25 m intervals (slope distance) at an all-inclusive cost | $ | 30,000 | |

| Diamond drilling to test mineralized vein structures at Josefina | |||

| 500 meters at an all-inclusive (drilled, logged, split, sampled, water haul) cost of $180 per meter: | $ | 90,000 | |