Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - NuStar Energy L.P. | d295754d8k.htm |

Steve Blank, Senior Vice President, CFO and Treasurer

February 7, 2012

2012 Credit Suisse Energy Summit

1

Exhibit 99.1 |

Statements contained in this presentation that state management’s

expectations or predictions of the future are forward-looking statements as

defined

by

federal

securities

law.

The

words

“believe,”

“expect,”

“should,”

“targeting,”

“estimates,”

and

other

similar

expressions

identify

forward-

looking

statements.

It

is

important

to

note

that

actual

results

could

differ

materially from those projected in such forward-looking statements. We

undertake no duty to update any forward-looking statement to conform the

statement to actual results or changes in the company’s expectations.

For more information concerning factors that could cause actual results to

differ from those expressed or forecasted, see NuStar Energy L.P.’s and

NuStar GP Holdings, LLC’s respective annual reports on Form 10-K and

quarterly reports on Form 10-Q, filed with the Securities and Exchange

Commission and

available

on

NuStar’s

websites

at

www.nustarenergy.com

and

www.nustargpholdings.com.

Forward Looking Statements

2 |

NuStar Overview

3 |

NuStar Energy L.P. (NYSE: NS) is

a leading publicly traded

partnership with a market

capitalization of approximately

$4.2 billion and an enterprise

value of approximately $6.6 billion

NuStar GP Holdings, LLC (NYSE:

NSH) holds the 2% general

partner interest, incentive

distribution rights and 14.3% of the

common units in NuStar Energy

L.P. NSH has a market

capitalization of around $1.4 billion

Two Publicly Traded Companies

NS

NSH

IPO Date

4/16/2001

7/19/2006

Unit Price (01/31/12)

$58.79

$33.65

Annualized Distribution/Unit

$4.38

$1.98

Yield (01/31/12)

7.45%

5.88%

Market Capitalization

$4,159 million

$1,432 million

Enterprise Value

$6,626 million

$1,441 million

Credit Ratings –

Moody’s

Baa3/Stable

n/a

S&P

BBB-/Stable

n/a

Fitch

BBB-/Negative

n/a

82.3%

Membership Interest

83.7%

L.P. Interest

Public Unitholders

35.0 Million NSH Units

Public Unitholders

60.4 Million NS Units

17.7%

Membership

Interest

2.0% G.P. Interest

14.3% L.P. Interest

Incentive Distribution Rights

William E. Greehey

7.6 Million NSH Units

NYSE: NSH

NYSE: NS

4 |

Large

and Diverse Geographic Footprint

with Assets in Key Locations

Asset Stats:

Operations in the U.S.,

Canada, Mexico, the

Netherlands, including St.

Eustatius in the Caribbean,

the United Kingdom and

Turkey.

Own 89 terminal and

storage facilities

Approximately 98 million

barrels of storage capacity

8,417 miles of crude oil and

refined product pipelines

2 asphalt refineries and a

fuels refinery capable of

processing 118,500 bpd of

crude oil

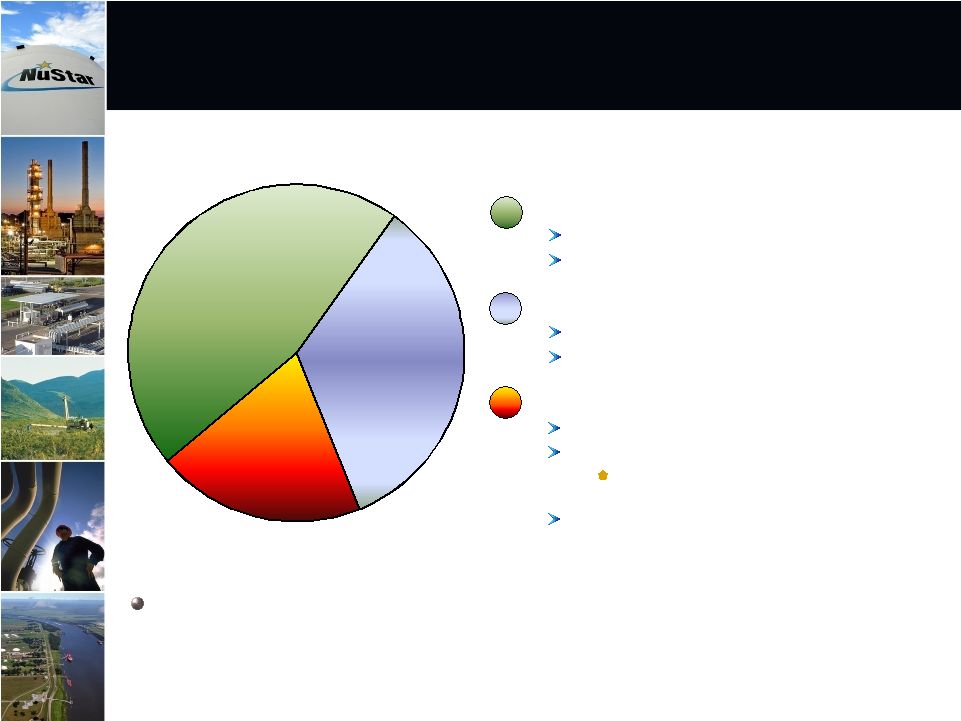

5 |

46%

34%

20%

Percentage of Full Year 2011

Segment Operating Income

Approximately 80% of NuStar Energy’s 2011 segment operating income came

from fee-based transportation and storage segments

Storage: 46%

Transportation: 34%

Refined Product Terminals

Crude Oil Storage

Refined Product Pipelines*

Crude Oil Pipelines

Asphalt & Fuels Marketing: 20%

Asphalt Operations

Fuels Marketing Operations

Product Supply, Crude Oil Trading, Bunkering

and Fuel Oil Marketing

San Antonio Refinery

Diversified Operations from Three

Business Segments

* Includes primarily distillates, gasoline, propane, jet fuel, ammonia and

other light products. Does not include natural gas. 6

|

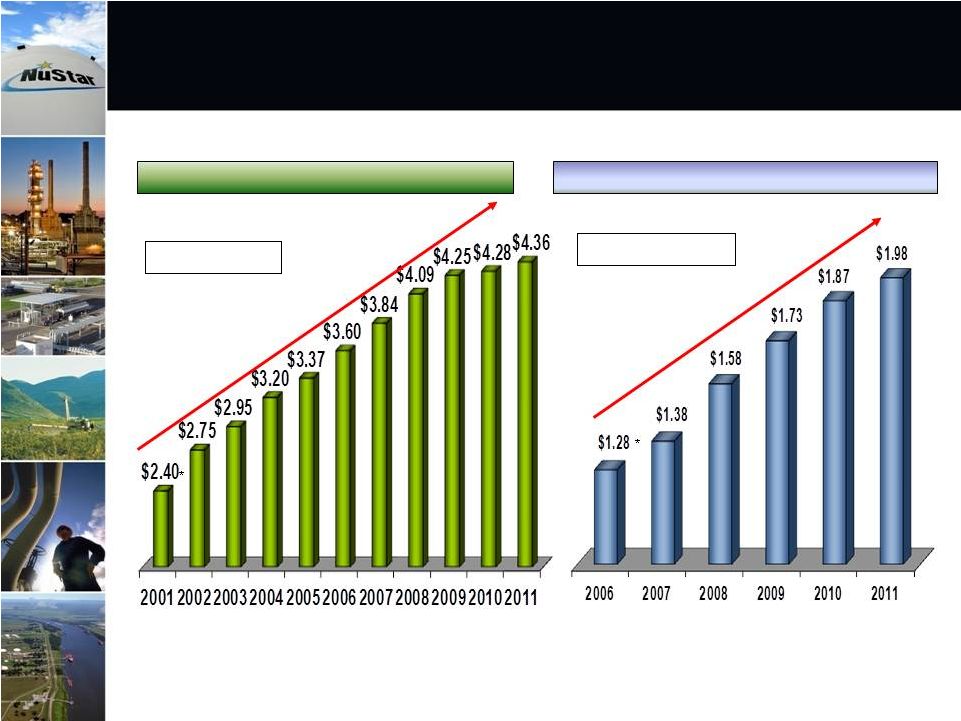

Distributions for both

NS and NSH have grown every year since IPO’s.. should

continue to grow distribution in the future NS Distribution ($ per Unit)

NSH Distribution ($ per Unit)

~6.2% CAGR

~9.1% CAGR

* Annualized Distribution

7 |

Storage Segment Overview

8 |

Outlook

2012 segment EBITDA expected to be higher than 2011

St.

James,

LA

storage

expansion

project

completed

in

3rd

quarter

of

2011

should

provide a full year’s benefit to results in 2012

Expect to complete additional internal growth projects in St. James, Texas City and

St. Eustatius during 2012

1 –

Please see slide 31 for a reconciliation of Storage Segment EBITDA to its most

directly comparable GAAP measure, Operating Income Storage

Segment

EBITDA

($

in

Millions)¹

Storage Contract Renewals (% of Revenues)

Storage Segment EBITDA

expected to continue to increase

9

< 1 Year

1 to 3 Years

3 to 5 Years

> 5 Years

24%

47%

12%

17%

2006

2007

2008

2009

2010

2011

$162

$177

$208

$242

$256

$281 |

Storage expansion continues at our

St. James, Louisiana Terminal

St. James Terminal

10

St. James Third-Party Expansion – Phase 2

Should be similar in size and cost to Phase 1 project Phase 1 project 3.2 million barrels at a cost of $140 million Most tankage should be crude

storage

Expected in-service early 2013

|

Have

begun the construction of a unit train offloading facility at our St. James

facility Entered into an agreement with two subsidiaries of EOG Resources,

Inc. EOG is a large independent oil and natural gas company

Proved reserves in the United States, Canada, the UK and China

Project description:

New rail and unit train offloading facilities jointly developed by NuStar and

two EOG Resources, Inc. subsidiaries

Facility will be equipped to handle at least one 70,000-barrel train per

day Two new storage tanks with a combined capacity of 360,000 barrels

Costs and completion dates:

Project expected to be completed and in service 2nd quarter 2012

NuStar’s share of the costs should be approximately $35 million

11 |

In

the process of constructing new tanks for distillate service at our St.

Eustatius terminal Constructing one million barrels of new storage for

distillate service Customer is a large national oil company

Projected cost around $50 million

Expected in-service 4th quarter 2012

Currently evaluating a major expansion project at the St. Eustatius

terminal

12 |

Transportation Segment

Overview

13 |

Transportation Segment EBITDA ($ in

Millions)¹ Pipeline Receipts by

Commodity Growth in Eagle Ford Shale should lead to future

growth in Transportation Segment EBITDA

Gasoline

29%

Other*

13%

*Other includes ammonia, jet fuel, propane, naphtha

and light end refined products

Crude Oil

40%

Distillate

18%

Outlook

2012 segment EBITDA expected to be higher than 2011

2012 results should receive a full year benefit from two Eagle Ford shale crude

pipeline internal growth projects brought on-line during 2011

Throughputs projected to increase in 2012 primarily as a result of 2011 internal

growth projects

14

2006

2007

2008

2009

2010

2011

$170

$176

$186

$190

$199

$197

1 –

Please see slide 31 for a reconciliation of Transportation Segment EBITDA to its

most directly comparable GAAP measure, Operating Income |

Various shale

formations could provide growth opportunities

Key shale formations located in NuStar’s Mid-Continent and Gulf

Coast regions, include the Eagle Ford, Bakken, Granite Wash,

Barnett, and Niobrara

15 |

NuStar has modified

existing pipeline assets and plans to construct new pipeline assets

for Valero in Eagle Ford Shale

Reversed

an

existing

8-inch

refined

products

pipeline

Line moved products from Corpus Christi to Three Rivers

Placed in crude oil service after September 2011 reversal

Capital spending required to reverse the line around $2 million

NuStar

also

plans

to

build

55

miles

of

new

12-inch

pipeline

that

will

connect

to

existing

NuStar

pipeline

segments

Expect to move crude and condensate from Corpus Christi to Valero’s Three

Rivers refinery

Projected cost $60 to $70 million

Expected

to

be

in

service

in

the

3

quarter

of

2012

16

rd |

Plan to

modify existing pipeline assets and construct new pipeline assets

for Valero in Eagle Ford Shale

New NuStar Pipeline

Existing NuStar Pipeline

Valero

West Plant

CORPUS CHRISTI

THREE RIVERS

REFINERY

8”

line

12”

line

17 |

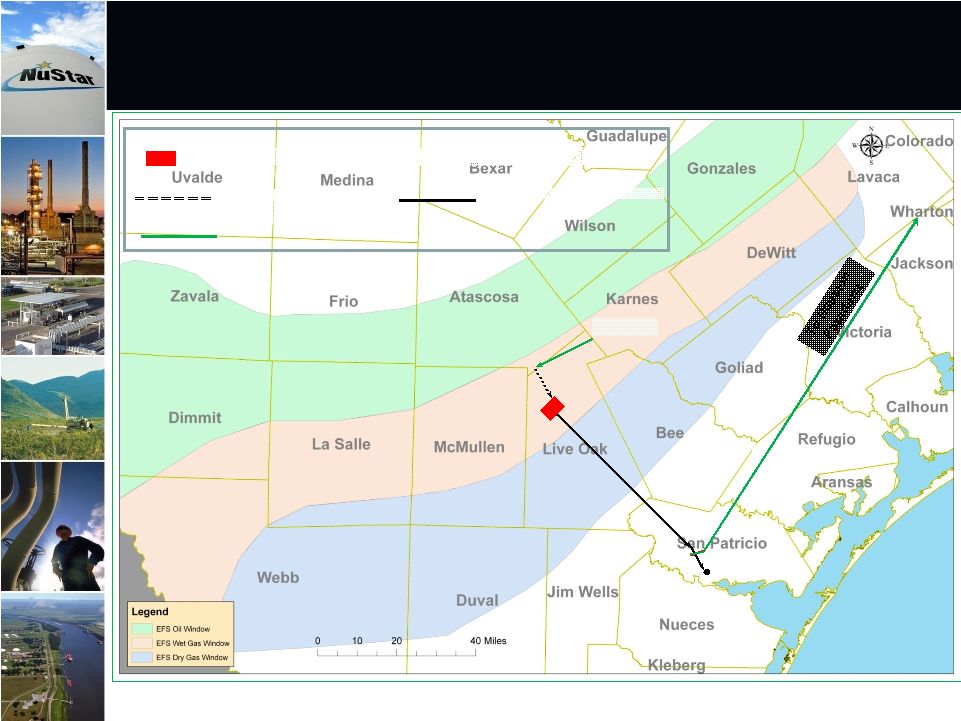

Plan to develop new

pipeline systems in the Eagle Ford Shale

18

TexStar plans to construct a pipeline that transports crude and condensate to Three

Rivers, TX

Pipeline should be interconnected with a new storage facility to be constructed at Three

Rivers, TX by NuStar

.

Plan to connect the storage facility to NuStar’s existing 16-inch pipeline that can

transport 200,000 BPD to NuStar’s Corpus Christi North Beach storage terminal Currently evaluating others pipeline projects in South Texas with several major oil

companies

Project

expected

to

be

in-service

4th

quarter

2012 |

Plan

to develop a new pipeline system in the Eagle Ford Shale as a result of a

Letter of Intent entered into with TexStar in the 2nd Quarter of 2011

Potential New 3 Party

Pipeline

Existing NuStar Pipeline

Potential New Storage Facility

NORTH BEACH

OAKVILLE

16”

line

19

rd |

Pursuing additional projects in the Eagle Ford Shale to

better utilize Houston 12”

line and idle 8”

line out of Pettus

Potential New NuStar

Pipeline

Existing NuStar Pipeline

Potential New Storage Facility

NORTH BEACH

OAKVILLE

16”

line

PETTUS

Underutilized Existing NuStar Pipeline

8”

line

12”

line

20 |

Asphalt & Fuels Marketing

Segment Overview

21 |

Despite weaker than expected Asphalt demand

Asphalt & Fuels Marketing Segment 2011 EBITDA

comparable to 2010

Outlook

2012 segment results expected to be higher than 2011

U.S. asphalt demand projected to continue to be weak in 2012

Asphalt operations margins for 2012 forecasted to improve over 2011

2012 projections include a full year of results from the San Antonio refinery

Asphalt & Fuels Marketing Segment EBITDA ($ in Millions)¹ 22

2006

2007

2008

2009

2010

2011

$27

$22

$127

$80

$111

$108

1 –

Please see slide 31for a reconciliation of Asphalt & Fuels Marketing Segment

EBITDA to its most directly comparable GAAP measure, Operating Income

|

Financial Overview

23 |

2011

Financial Results 2011 Full Year Distributable Cash Flow available to limited

partners, EBITDA and Operating Income higher than 2010

Distributable Cash Flow available to limited to partners increased from $281 million

to $308 million

EBITDA increased from $483 million to $490 million

Operating income increased from $303 million to $314 million

December 31, 2011 Debt balance $2.3 billion

Debt to capitalization ratio 44.5%

24

–

Please see slide 32 for a reconciliation of Distributable Cash Flow available to

limited partners and EBITDA to their most comparable GAAP measures. |

2009

2010

2011 Estimate

$164

$262

$294

2009 -

2011 Internal Growth Project Spending

Internal Growth Project Spending continues to

grow…..2012 internal growth spending should be

in the $350 to $400 million range

(

Dollars in Millions)

25 |

$0

$250

$500

$750

$1,000

2011

2012

2013

2018

2020

2038-2041

$456

$350

$33

Misc. Note

UK Term Loan

GO Zone Financing

Senior Public Notes

Revolver

$1

$840

$480

$350

$450

$365

Debt Maturity Profile

Debt Maturities as of September 30, 2011

(Millions $)

26

Debt

structure

approximately

50%

fixed

rate

–

50%

variable

rate

As of January 31st

, 2012 revolver balance $320 million

2012

total

maturities

as

of

January

31st

~

$700

million |

2012

Financing Plan Recently closed on $250 Million bond issuance

Coupon 4.75%, bonds mature February 2022

Proceeds initially used to paydown revolver balance, eventually used to pay off

$250 million February 2012 bond maturity

$100 million bond matures in July

Plan to refinance with borrowings under the revolver

Refinance $1.2 billion revolver (matures December 2012) by end of second quarter

2012 At time of refinancing may upsize to $1.5 billion

Refinance $30 million NuStar GP Holdings revolver in second quarter 2012 (matures

July 2012)

Refinance 21 million pound UK Term Loan in the fourth quarter 2012 (matures December

2012)

27 |

High quality, large and diverse asset footprint supporting energy infrastructure

both in the U.S. and internationally

Contracted fee-based storage and transportation assets provide stable cash

flows, delivering approximately 80% of 2011 segment operating income

Diverse and high quality customer base composed of large integrated oil companies,

national oil companies and refiners

Strong balance sheet, credit metrics and commitment to maintain investment grade

credit ratings

Experienced and proven management team with substantial equity ownership and

industry experience

Recognized nationally for safety and environmental record as well as one of the

best places to work

Successfully raised $311 million of equity in December 2011

NuStar Highlights

28 |

29 |

Appendix

30 |

Reconciliation of Non-GAAP Financial

Information -

Segmental

31

(Unaudited, Dollars in Thousands)

The following is a reconciliation of operating income to EBITDA for the Storage Segment:

2006

2007

2008

2009

2010

2011

Operating income

108,486

$

114,635

$

141,079

$

171,245

$

178,947

$

193,395

$

Plus depreciation and amortization expense

53,121

62,317

66,706

70,888

77,071

87,737

EBITDA

161,607

$

176,952

$

207,785

$

242,133

$

256,018

$

281,132

$

The following is a reconciliation of operating income to EBITDA for the Transportation

Segment: 2006

2007

2008

2009

2010

2011

Operating income

122,714

$

126,508

$

135,086

$

139,869

$

148,571

$

145,613

$

Plus depreciation and amortization expense

47,145

49,946

50,749

50,528

50,617

51,175

EBITDA

169,859

$

176,454

$

185,835

$

190,397

$

199,188

$

196,788

$

The following is a reconciliation of operating income to EBITDA for the Asphalt and Fuels

Marketing Segment: 2006

2007

2008

2009

2010

2011

Operating income

26,815

$

21,111

$

112,506

$

60,629

$

90,861

$

85,229

$

Plus depreciation and amortization expense

-

423

14,734

19,463

20,257

22,636

EBITDA

26,815

$

21,534

$

127,240

$

80,092

$

111,118

$

107,865

$

NuStar

Energy

L.P.

utilizes

a

financial

measure,

EBITDA,

that

is

not

defined

in

United

States

generally

accepted

accounting

principles.

Management

uses

this

financial

measure

because

it

is

a

widely

accepted

financial

indicator

used

by

investors

to

compare

partnership

performance.

In

addition,

management

believes

that

this

measure

provides

investors

an

enhanced

perspective

of

the

operating

performance

of

the

partnership's

assets.

EBITDA

is

not

intended

nor

presented

as

an

alternative

to

operating

income.

EBITDA

should

not

be

considered

in

isolation

or

as

a

substitute

for

a

measure

of

performance

prepared

in

accordance

with

United

States generally accepted accounting principles.

EBITDA

in

the

following

reconciliations

relate

to

our

operating

segments.

For

purposes

of

segment

reporting

we

do

not

allocate

general

and

administrative

expenses

to

our

reported

operating

segments

because

those

expenses

relate

primarily

to

the

overall

management

at

the

entity

level.

Therefore,

EBITDA

reflected

in

the

following

reconciliations

exclude

any

allocation

of

general

and

administrative

expenses

consistent

with

our

policy

for

determining

segmental

operating

income,

the most directly comparable GAAP measure.

Year Ended December 31,

Year Ended December 31,

Year Ended December 31,

Our

independent

registered

public

accounting

firm

has

not

completed

its

audit

of

NuStar

Energy's

financial

statements

for

the

year

ended

December

31,

2011.

As

a

result, the financial results for the full year ended December 31, 2011, which appear below, are

subject to change. |

Reconciliation of Non-GAAP Financial

Information -

Consolidated

32

(Unaudited, Dollars in Thousands)

The following is a reconciliation of net income to EBITDA and distributable cash flow:

2011

2010

Net income

221,601

$

238,970

$

Plus interest expense, net

83,681

78,280

Plus income tax expense

16,879

11,741

Plus depreciation and amortization expense

168,286

153,802

EBITDA

490,447

482,793

Less equity in earnings of joint venture

(11,458)

(10,500)

Less interest expense, net

(83,681)

(78,280)

Less reliability capital expenditures

(50,339)

(54,031)

Less income tax expense

(16,879)

(11,741)

Plus distributions from joint venture

14,374

9,625

Mark-to-market impact on hedge transactions (a)

456

(17,640)

Contingent loss adjustment

3,250

-

Other non-cash items

5,093

-

Distributable cash flow

351,263

$

320,226

$

EBITDA

490,447

$

482,793

$

EBITDA attributable to noncontrolling interest

415

-

EBITDA attributable to NuStar Energy L.P.

490,032

$

482,793

$

Distributable cash flow

351,263

$

320,226

$

Distributable cash flow attributable to noncontrolling interest

441

-

Distributable cash flow attributable to NuStar

Energy L.P. 350,822

$

320,226

$

General partner's interest in distributable cash flow

42,956

39,531

Limited partners' interest in distributable cash flow

307,866

$

280,695

$

a)

NuStar

Energy

L.P.

utilizes

two

financial

measures,

EBITDA

and

distributable

cash

flow,

which

are

not

defined

in

United

States

generally

accepted

accounting

principles.

Management

uses

these

financial

measures

because

they

are

widely

accepted

financial

indicators

used

by

investors

to

compare

partnership

performance.

In

addition,

management

believes

that

these

measures

provide

investors

an

enhanced

perspective

of

the

operating

performance

of

the

partnership's

assets

and

the

cash

that

the

business

is

generating.

Neither

EBITDA

nor

distributable

cash

flow

are

intended

to

represent

cash

flows

for

the

period,

nor

are

they

presented

as

an

alternative

to

net

income.

They

should

not

be

considered

in

isolation

or

as

substitutes

for

a

measure

of

performance

prepared

in

accordance

with

United

States

generally

accepted

accounting principles.

Year Ended December 31,

Our

independent

registered

public

accounting

firm

has

not

completed

its

audit

of

NuStar

Energy's

financial

statements

for

the

year

ended

December

31,

2011.

As

a

result, the financial results for the full year ended December 31, 2011, which appear below, are

subject to change. Distributable cash flow excludes the impact of unrealized

mark-to-market gains and losses that arise from valuing certain derivative contracts,

as well as the associated hedged inventory. The gain or loss associated with these contracts

is realized in distributable cash flow when the contracts are settled. |