Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - HG Holdings, Inc. | Financial_Report.xls |

| EX-21 - EXHIBIT 21 - HG Holdings, Inc. | d284665dex21.htm |

| EX-23 - EXHIBIT 23 - HG Holdings, Inc. | d284665dex23.htm |

| EX-32.2 - EXHIBIT 32.2 - HG Holdings, Inc. | d284665dex322.htm |

| EX-32.1 - EXHIBIT 32.1 - HG Holdings, Inc. | d284665dex321.htm |

| EX-31.1 - EXHIBIT 31.1 - HG Holdings, Inc. | d284665dex311.htm |

| EX-10.16 - EXHIBIT 10.16 - HG Holdings, Inc. | d284665dex1016.htm |

| EX-31.2 - EXHIBIT 31.2 - HG Holdings, Inc. | d284665dex312.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2011

Commission file number 0-14938

STANLEY FURNITURE COMPANY, INC.

(Exact name of Registrant as specified in its Charter)

| Delaware | 54-1272589 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

4100 Mendenhall Oaks Parkway, Suite 200, High Point, North Carolina, 27265

(Address of principal executive offices, Zip Code)

Registrant’s telephone number, including area code: (276) 627-2010

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| Common Stock, par value $.02 per share | Nasdaq Stock Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act: Yes ¨ No x

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act: Yes ¨ No x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days: Yes x No ¨

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate website, if any, every Interactive Date File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Section 232.504 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (Section 229.405 of this chapter) is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act, (check one):

| Large accelerated filer |

¨ |

Accelerated filer |

¨ | |||

| Non-accelerated filer |

x (Do not check if a smaller reporting company) |

Smaller reporting company |

¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act): Yes ¨ No x

Aggregate market value of the voting and non-voting common equity held by non-affiliates of the Registrant based on the closing price on June 30, 2011: $57 million.

Indicate the number of shares outstanding of each of the Registrant’s classes of common stock as of January 29, 2012:

| Common Stock, par value $.02 per share |

14,524,015 | |

| (Class of Common Stock) | Number of Shares |

Documents incorporated by reference: Portions of the Registrant’s Proxy Statement for our Annual Meeting of Stockholders scheduled for April 18, 2012 are incorporated by reference into Part III.

Table of Contents

2

Table of Contents

Stanley Furniture Company, Inc.

General

We are a leading designer, manufacturer and importer of wood furniture in the premium segment of the residential market. We offer two major product lines that diversify us across all major style and product categories within our segment. Our fashion furniture line for the adult market is sold under the Stanley Furniture brand while our children’s furniture is sold under the Young America brand. Our product depth and extensive style selection makes us a complete wood furniture resource for retailers and interior designers serving the upscale consumer. To support our customers and cater to the specific factors which drive consumer demand for our two branded product lines, we have implemented distinct operating strategies for each brand. An import model serves the demands of the Stanley Furniture customer, while a domestic manufacturing model supports Young America.

Products

Our Stanley Furniture brand, is marketed as upscale home furnishings which differentiate from other products in the market through styling and finish execution as well as wide selections for the entire home including dining, bedroom, home office, home entertainment, and accent items. We believe the end consumer for the Stanley Furniture brand is typically a mature, affluent consumer who values the interior aesthetics of her home.

Our Young America brand is marketed as the trusted brand for child safety. Controlling its production in our North Carolina manufacturing facility allows us to proudly market a product “Made in the USA”, which we believe our customers associate with a higher level of product safety and quality. Additionally, certain products have achieved third party certifications for both indoor air quality and product safety. Product selection through color and choice also differentiate the Young America brand and attract the consumer wishing to customize her purchase and make an investment in furniture that grows with her child from crib to college and beyond. While the typical consumer purchasing Young America is a parent between the ages of 25 and 40, grandparents are often involved in the purchase.

We believe that the diversity of our product lines enables us to anticipate and address changing consumer preferences and provide retailers a complete wood furniture resource in the premium segment. We believe that our products represent good value and that the quality and design of our furniture combined with our broad selection and dependable service differentiates our products in the marketplace.

We provide products in a variety of woods and finishes. Our products are designed to appeal to a broad range of consumer tastes in the premium segment and cover all major style categories including traditional, continental, contemporary, transitional and cottage designs.

We continually design and develop new styles to replace those discontinued and, if desired, to expand our product lines. Our product design process begins with marketing personnel identifying customer preferences and marketplace trends and conceptualizing product ideas. A variety of sketches are produced, usually by company designers, from which prototype furniture pieces are built for review prior to full-scale engineering and production. We consult with our marketing and operations personnel, core suppliers, independent sales representatives and selected customers throughout this process and introduce our new product designs primarily at the fall and spring international furniture markets.

Distribution

We have developed a broad domestic and international customer base and sell our furniture mainly through independent sales representatives to independent furniture stores, interior designers, smaller specialty retailers, regional furniture chains, buying clubs and e-tailers. We believe this broad network reduces exposure to fluctuations in regional economic conditions and allows us to capitalize on emerging channels of distribution. We offer tailored marketing programs to address each specific distribution channel.

The primary marketing practice followed in the furniture industry is to exhibit products at international and regional furniture markets. In the spring and fall of each year, a furniture market is held in High Point, North Carolina, which is attended by the majority of our retail customer base and is regarded by most of the industry as the most important international market. We utilize showroom space at this market to introduce new products, increase retail placements of existing products and test concepts for future products and services.

3

Table of Contents

In 2011, we sold product to approximately 2,300 customers and recorded approximately 11% of our sales from international customers. No single customer accounted for more than 10% of our sales in 2011 and no part of the business is dependent upon a single customer, the loss of which would have a material effect on our business. The loss of several major customers could have a material impact on our business.

Manufacturing and Offshore Sourcing

In 2010, we announced a change in strategy in our manufacturing and sourcing for each of our brands. We believe this move better aligns the operations and associated cost structures with the driving forces of demand for each product line.

Stanley Furniture

We ceased manufacturing at our Stanleytown, Virginia facility in December 2010 completing the transformation of the Stanley Furniture product line to a completely sourced operations model in 2011. With this transition, we developed a support organization in Asia to manage vendor relationships, sourcing decisions, engineering and quality control. While we operate solely as a purchaser, we maintain a presence in each of our partners’ factories.

We are subject to the usual risks inherent in importing products manufactured abroad, including, but not limited to, supply disruptions and delays, currency exchange rate fluctuations, economic and political developments and instability, as well as the laws, policies and actions of foreign governments and the United States affecting trade, including tariffs.

Our Stanley Furniture product line is imported from a small number of specialized furniture manufacturers in Southeast Asia, primarily in Indonesia and Vietnam. A sudden disruption in our supply chain from any of our strategic vendors could significantly compromise our ability to fill customer’s orders. If a disruption were to occur, we believe we would have sufficient inventory to meet a portion of demand for approximately three to four months. We believe that we could source any impacted products from other strategic suppliers but could potentially experience service gaps and short-term increases in cost.

We enter into standard purchase arrangements with certain overseas suppliers for finished goods inventory to support our Stanley Furniture product line. The terms of these arrangements are customary for our industry and do not contain any long-term purchase obligations. We generally negotiate firm pricing with our foreign suppliers in U.S. Dollars for a term of one year. We accept exposure to exchange rate movement after this period and do not use any derivative instruments to manage currency risk. We generally expect to recover any substantial price increases from these suppliers in the price we charge for these goods.

Young America

In 2011, we continued our efforts to improve operations in our Robbinsville, North Carolina manufacturing facility to support the Young America product line as the trusted brand for child safety, color and choice, quick delivery, and quality to better differentiate our children’s furniture in the marketplace. Late in 2010, we completed the consolidation of all Young America manufacturing into this facility and have since focused our efforts and capital on modernizing and automating the factory.

Domestic manufacturing supports our product and distribution strategy allowing us to drive continuous improvement in product safety, quality and customer service, while offering maximum choice and customization with minimum inventory. Our domestic manufacturing strategy includes:

| • | Smaller, more frequent and cost-effective production runs, |

| • | Standardized engineering to improve quality and lower cost, |

| • | Identification and elimination of manufacturing bottlenecks and waste, |

| • | Use of cellular manufacturing in the production of components, and |

| • | Improved relationships with a core group of suppliers. |

In addition, we continue to involve all personnel and vendor partners in the improvement of the manufacturing, assembly and finishing processes by encouraging an open and collaborative environment that embraces continuous improvement.

4

Table of Contents

Warehousing and Delivery

We warehouse Young America products in our manufacturing facility in North Carolina and lease three warehouse facilities to support the Stanley Furniture product line. We consider our facilities to be generally modern, well equipped and well maintained.

Production of our two product lines is scheduled based upon both actual and forecasted demand. To support our service objectives, we plan to maintain a higher inventory of imported products compared to those manufactured domestically. We ship the majority of orders within 30 days from receipt of order. Our backlog of unshipped orders was $11.6 million at December 31, 2011 and $11.0 million at December 31, 2010.

Raw Materials

Virtually all raw materials we use support the domestic manufacturing of our Young America product line. The principal materials used include lumber, plywood, veneers, particle board, hardware, glue, finishing materials, glass products, laminates, and metals. We use two main species of lumber: poplar and maple. Domestic lumber availability and prices fluctuate over time based primarily on supply and demand.

Our five largest raw material suppliers accounted for approximately 51% of our purchases in 2011. We believe we keep adequate inventory of lumber and other supplies to maintain production levels. We believe that our sources of supply for these materials are adequate and that we are not dependent on any one supplier.

Competition

The furniture industry is highly competitive and includes a large number of competitors, none of which dominates the market. In addition, competition has significantly increased as the industry’s worldwide manufacturing capacity remains relatively underutilized due to a lack of demand driven by the ongoing economic recession and its impact on housing. Significant manufacturing capacity was added during the housing boom that our economy experienced pre-recession. This excess capacity has created intense downward price pressure as industry participants attempt to generate sales to better utilize their manufacturing capacity. The vast majority of our competitors own manufacturing facilities abroad or source finished goods from Asian suppliers.

The markets in which we compete include a large number of relatively small manufacturers. However, certain competitors have substantially greater sales volume and financial resources compared to us. Competitive factors in the premium segment include design, quality, service, selection, price, and for our Young America brand, child safety. We believe the changes to our operational strategy, our long-standing customer relationships and customer responsiveness, our consistent support of high-quality and diverse product lines, and our mixture of youth and experience in our management team are all competitive advantages.

Associates

At December 31, 2011, we employed 540 associates domestically and 55 associates overseas. We consider our relationship with our associates to be good. None of our associates are represented by a labor union.

Trademarks

Our trade names represent many years of continued business, and we believe these names are well recognized and associated with excellent quality and styling in the furniture industry. We own a number of trademarks and design patents, none of which are considered to be material.

Governmental Regulations

We are subject to federal, state and local laws and regulations in the areas of safety, health and environmental protection. Compliance with these laws and regulations has not in the past had any material effect on our earnings, capital expenditures or competitive position. However, the impact of such compliance in the future cannot be predicted. We believe that we are in material compliance with applicable federal, state and local safety, health and environmental regulations.

5

Table of Contents

Forward-Looking Statements

Certain statements made in this report are not based on historical facts, but are forward-looking statements. These statements can be identified by the use of forward-looking terminology such as “believes,” “estimates,” “expects,” “may,” “will,” “should,” or “anticipates,” or the negative thereof or other variations thereon or comparable terminology, or by discussions of strategy. These statements reflect our reasonable judgment with respect to future events and are subject to risks and uncertainties that could cause actual results to differ materially from those in the forward-looking statements. Such risks and uncertainties include our success in profitably producing Young America products in our domestic manufacturing facility, disruptions in foreign sourcing including those arising from supply or distribution disruptions or those arising from changes in political, economic and social conditions, as well as laws and regulations, in countries from which we source products, international trade policies of the United States and countries from which we source products, lower sales due to worsening of current economic conditions, the cyclical nature of the furniture industry, business failures or loss of large customers, the inability to raise prices in response to inflation and increasing costs, failure to anticipate or respond to changes in consumer tastes and fashions in a timely manner, competition in the furniture industry including competition from lower-cost foreign manufacturers, the inability to obtain sufficient quantities of quality raw materials in a timely manner, environmental, health, and safety compliance costs, failure or interruption of our information technology infrastructure, limited use of operating loss carry forwards due to ownership change and extended business interruption at our manufacturing facility. In addition, we have made certain forward looking statements with respect to payments we expect to receive under the Continued Dumping and Subsidy Offset Act, which are subject to the risks and uncertainties described in our discussion of those payments that may cause the actual payments to differ materially from those in the forward looking statements. Any forward-looking statement speaks only as of the date of this filing, and we undertake no obligation to update or revise any forward-looking statements, whether as a result of new developments or otherwise.

Available Information

Our principal Internet address is www.stanleyfurniture.com. We make available free of charge on this web site our annual, quarterly and current reports, and amendments to those reports, as soon as reasonably practicable after we electronically file such material with, or furnish it to, the Securities and Exchange Commission.

In addition, you may request a copy of these filings (excluding exhibits) at no cost by writing, telephoning, faxing or e-mailing us at the following address, telephone number, fax number or e-mail address.

Stanley Furniture Company, Inc.

4100 Mendenhall Oaks Parkway, Suite 200

High Point, North Carolina 27265

Attention: Mr. Micah S. Goldstein

Telephone: 276-627-2565

Fax: 276-629-5114

Or e-mail your request to: Investor@Stanleyfurniture.com

Our results of operations and financial condition can be adversely affected by numerous risks. You should carefully consider the risk factors detailed below in conjunction with the other information contained in this document. Should any of these risks actually materialize, our business, financial condition and future prospects could be negatively impacted.

Our strategic decision to transition our Young America children’s furniture product line from a blended manufacturing base comprised of both our own domestic factories and foreign sources to a completely domestic manufacturing platform utilizing only our Robbinsville, NC facility has, and will in the near term, increase our capital investment requirements and operating expenses. If we are not successful in the implementation of this strategy, we may experience disruptions to our operations that may result in a decline in revenues and liquidity; and an increase in our operating expenses.

We believe our decision to manufacture all children’s furniture products in our North Carolina facility was necessary to regain control of our entire production process and position and differentiate the Young America brand through product safety, color and choice, quick delivery and the cache that products “Made in USA” bring at retail in our premium segment. This transition has increased operating expenses due to the disruption caused by the transition of

6

Table of Contents

approximately one-third of our Young America product line from overseas sources to our domestic manufacturing facility. We expect long-term benefits as we distinguish our Young America product line from overseas competition in the marketplace. If we are unsuccessful in implementing this strategy and do not lower our overall operating expenses through process improvements and capital investments, we may experience disruptions in our operations that may result in a decline in revenues and liquidity and an increase in operating expenses.

We may experience asset impairment or other charges, as well as a decrease in revenues, if our strategy to improve operating efficiencies to achieve a profitable Young America product line is not successful or if our marketing strategy for this product line is unsuccessful.

If we do not achieve operating efficiencies sufficient to profitably manufacture our Young America product line domestically, or if our marketing strategy for this product line is unsuccessful, we may need to reposition our Young America product line, consider closing our Robbinsville facility and transition the manufacturing of Young America products to other sources, or we may need to cease production of our Young America product line altogether. In this event, we could experience asset impairment or other restructuring charges. In addition, if any of these actions are necessary, they could affect our ability to meet product demand which may in turn negatively impact customer relations and result in loss of market share.

As a result of our reliance on foreign sourcing for our Stanley Furniture product line:

| • | Our ability to service customers could be adversely affected and result in lower sales, earnings and liquidity. |

Our supply of goods could be interrupted for a variety of reasons. A natural disaster or other causes of physical damage to any one of our sourcing partners’ factories could interrupt production for an extended period of time. Our sourcing partners may not supply goods that meet our manufacturing, quality or safety specifications, in a timely manner and at an acceptable price. We may reject goods that do not meet our specifications, requiring us to find alternative sourcing arrangements at a higher cost, or may force us to discontinue the product. Also, delivery of goods from our foreign sourcing partners may be delayed for reasons not typically encountered with domestic manufacturing or sourcing, such as shipment delays caused by customs or labor issues.

| • | Our ability to properly forecast consumer demand on product with extended lead times could result in lower sales, earnings and liquidity. |

Our use of foreign sources exposes us to risks associated with forecasting future demand on product with extended order lead time. Extended order lead times may adversely affect our ability to respond to sudden changes in demand, resulting in the purchase of excess inventory in the face of declining demand, or lost sales due to insufficient inventory in the face of increasing demand, either of which would also have an adverse effect on our sales, earnings and liquidity.

| • | Changes in political, economic and social conditions, as well as laws and regulations, in the countries from which we source products could adversely affect us. |

Foreign sourcing is subject to political and social instability in countries where our sourcing partners are located. This could make it more difficult for us to service our customers. Also, significant fluctuations of foreign exchange rates against the value of the U.S. dollar could increase costs and decrease earnings. In addition, an outbreak of the avian flu or similar epidemic in Asia or elsewhere may lower our sales and earnings by disrupting our supply chain in the countries impacted.

| • | International trade policies of the United States and countries from which we source products could adversely affect us. |

Imposition of trade sanctions relating to imports, taxes, import duties and other charges on imports could increase our costs and decrease our earnings.

We may not be able to sustain sales, earnings and liquidity levels due to economic downturns.

The furniture industry historically has been cyclical in nature and has fluctuated with economic cycles including the current economic recession. During economic downturns, the furniture industry tends to experience longer periods of

7

Table of Contents

recession and greater declines than the general economy. We believe that the industry is significantly influenced by economic conditions generally and particularly by housing activity, consumer confidence, the level of personal discretionary spending, demographics and credit availability. These factors not only affect the ultimate consumer, but also impact furniture retailers, which are our primary customers. As a result, a worsening of current conditions could further lower our sales and earnings and impact our liquidity.

Business failures, or the loss, of large customers could result in a decrease in our future sales and earnings.

Although we have no single customer representing 10% or more of our total annual sales, the possibility of business failures, or the loss, of large customers could result in a decrease of our future sales and earnings. Lost sales may be difficult to replace and any amounts owed to us may become uncollectible.

We may not be able to maintain or to raise prices in response to inflation and increasing costs.

Future market and competitive pressures may prohibit us from successfully raising prices to offset increased costs of finished goods, raw materials, freight and other inflationary items. This could lower our earnings.

Failure to anticipate or respond to changes in consumer tastes and fashions in a timely manner could result in a decrease in our sales and earnings.

Residential furniture is a fashion business based upon products styled for a changing marketplace and is sometimes subject to rapidly changing consumer trends and tastes. If we are unable to predict or respond to changes in these trends and tastes in a timely manner, we may lose sales and have to sell excess inventory at reduced prices. This could lower our sales and earnings.

We may not be able to sustain current sales and earnings due to the actions and strength of our competitors.

The furniture industry is very competitive and fragmented. We compete with many domestic and overseas manufacturers. Competition from overseas producers has increased dramatically in recent years, with most residential wood furniture sold in the United States now coming from imports. These overseas producers typically have lower selling prices due to their lower operating costs and often replicate our designs closely enough to attract a portion of our customer base, but not closely enough to warrant legal action that would result in any substantial effect towards thwarting this practice. In addition, some competitors have greater financial resources than we have and often offer extensively advertised, highly promoted products. As a result, we are continually subject to the risk of losing market share, which may lower our sales and earnings.

We may not be able to obtain sufficient quantities of quality raw materials in a timely manner, which could result in a decrease in our sales and earnings.

Because we are dependent on outside suppliers for all of our raw material needs, we must obtain sufficient quantities of quality raw materials from our suppliers at acceptable prices and in a timely manner. We have no long-term supply contracts with our key suppliers. Unfavorable fluctuations in the price, quality and availability of these raw materials could negatively affect our ability to meet the demands of our customers and could result in a decrease in sales and earnings.

Future cost of compliance with environmental, safety and health regulations could reduce our earnings.

We are subject to federal, state and local laws and regulations in the areas of safety, health and environmental protection. The timing and ultimate magnitude of costs for compliance with environmental, health and safety regulations are difficult to predict and could reduce our earnings.

Our business and operations would be adversely impacted in the event of a failure or interruption of our information technology infrastructure.

The proper functioning of our information technology infrastructure is critical to the efficient operation and management of our business. If our information technology systems fail or are interrupted, our operations may be adversely affected and operating results could be harmed. Over the next two years, we are pursuing an initiative to improve our information technology infrastructure. These changes may be costly and disruptive to our operations, and could impose substantial demands on management time and resources. Our information technology systems, and those of third parties providing service to us, may also be vulnerable to damage or disruption caused by circumstances beyond our control. These

8

Table of Contents

include catastrophic events, power anomalies or outages, natural disasters, computer system or network failures, viruses or malware, physical or electronic break-ins, unauthorized access and cyber attacks. Any material disruption, malfunction or similar challenges with our information technology infrastructure, or disruptions or challenges relating to the transition to new processes, systems or providers, could have a material adverse effect on the operation of our business and our results of operations.

An “ownership change” could limit the use of our net operating loss carry forwards and decrease a potential acquirer’s valuation of our business, both of which could decrease our liquidity and earnings.

If an “ownership change” occurs pursuant to applicable statutory regulations, we are potentially subject to limitations on the use of our net operating loss carry forwards which in turn could adversely impact our future liquidity and profitability. The limitations triggered by an “ownership change” could also decrease a potential acquirer’s valuation of our business and discourage a potential acquirer. In general, an “ownership change” would occur if there is a cumulative change in the ownership of our common stock of more than 50 percentage points by one or more “5% shareholders” during a three-year test period.

Extended business interruption at our manufacturing facility could result in reduced sales.

Furniture manufacturing creates large amounts of highly flammable wood dust. Additionally, we utilize other highly flammable materials such as varnishes and solvents in our manufacturing processes and are therefore subject to the risk of losses arising from explosions and fires. Our inability to fill customer orders during an extended business interruption could negatively impact existing customer relationships resulting in the loss of market share.

Item 1B. Unresolved Staff Comments

None.

Set forth below is certain information with respect to our principal properties. We believe that all these properties are well maintained and in good condition. A majority of our production and distribution facilities are equipped with automatic sprinkler systems and modern fire protection equipment, which we believe are adequate. All facilities set forth below are active and operational. Production capacity and the utilization of our Robbinsville manufacturing facilities is difficult to quantify as we continue to modernize and increase its available capacity.

| Approximate | Owned | |||||||

| Facility Size | or | |||||||

| Location |

Primary Use |

(Square Feet) | Leased | |||||

| Stanleytown, VA |

Warehouse and Office Space | 950,000 | (1) | Leased | ||||

| Robbinsville, NC |

Manufacturing/ Distribution | 562,100 | Owned | |||||

| Martinsville, VA |

Distribution | 300,000 | Leased | |||||

| High Point, NC |

Office Space | 5,600 | Leased | |||||

| High Point, NC |

Showroom | 51,000 | Leased | |||||

| Vietnam |

Distribution | 50,000 | Leased | |||||

| (1) | Distribution utilization as of December 31, 2011 was approximately 75% of leased square footage. We expect to be at approximately 50% by the end of the first half of 2012. |

In the normal course of business, we are involved in claims and lawsuits none of which currently, in our opinion, will have a material adverse affect on our consolidated financial statements.

Item 4. (Removed and Reserved)

9

Table of Contents

Executive Officers of the Registrant

Our executive officers and their ages as of January 1, 2012 are as follows:

| Name |

Age |

Position | ||

| Glenn Prillaman |

40 | President and Chief Executive Officer | ||

| Micah S. Goldstein |

41 | Chief Operating and Financial Officer |

Glenn Prillaman has been President, Chief Executive Officer since February 2010. Mr. Prillaman was President and Chief Operating Officer from August 2009 until February 2010. He was our Executive Vice President – Marketing and Sales from September 2008 until August 2009. He held the position of Senior Vice President – Marketing and Sales from September 2006 until September 2008 and was our Senior Vice President – Marketing/Sales – Young America® from August 2003 to September 2006. Mr. Prillaman held various management positions in product development from June 1999 to August 2003.

Micah S. Goldstein has been Chief Operating Officer since August 2010 and has also served as Chief Financial Officer since December 2010. From January 2006 until August 2010, Mr. Goldstein was President and Chief Executive Officer of Bri-Mar Manufacturing, LLC, a manufacturer of hydraulic equipment trailers.

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

Our common stock is quoted on the Nasdaq Stock Market (“Nasdaq”) under the symbol STLY. The table below sets forth the high and low sales prices per share, for the periods indicated, as reported by Nasdaq.

| 2011 | 2010 | |||||||||||||||||||||||

| High | Low | Dividends Paid |

High | Low | Dividends Paid |

|||||||||||||||||||

| First Quarter |

$ | 6.13 | $ | 3.15 | — | $ | 11.12 | $ | 7.50 | — | ||||||||||||||

| Second Quarter |

5.87 | 4.04 | — | 11.14 | 4.01 | — | ||||||||||||||||||

| Third Quarter |

4.75 | 2.90 | — | 4.29 | 3.35 | — | ||||||||||||||||||

| Fourth Quarter |

3.60 | 2.50 | — | 4.00 | 2.98 | — | ||||||||||||||||||

As of January 20, 2012, we have approximately 2,300 beneficial stockholders. On January 28, 2009, our Board of Directors voted to suspend quarterly cash dividend payments. Our dividend policy and the decision to suspend dividend payments is subject to review and revision by the Board of Directors and any future payments will depend upon our financial condition, our capital requirements and earnings, as well as other factors the Board of Directors may deem relevant.

10

Table of Contents

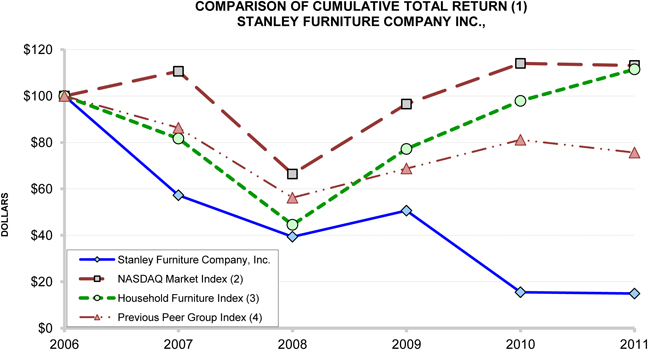

Performance Graph

The following graph compares cumulative total stockholder return for our company with a broad performance indicator, the Nasdaq Market index (an industry index) and a Peer group index for the period from December 31, 2006 to December 31, 2011.

| (1) | The graph shows the cumulative total return on $100 invested at the market close on December 31, 2006, the last trading day in 2006, in common stock or the specified index, including reinvestments of dividends. |

| (2) | Nasdaq Market Index as prepared by Zacks Investment Research, Inc. |

| (3) | Household Furniture Index as prepared by Zacks Investment Research, Inc. consists of SIC Codes 2510 and 2511. At January 14, 2012, Zacks Investment Research, Inc. reported that these two SIC Codes consisted of Bassett Furniture Industries, Inc., Chromcraft Revington, Inc., Dorel Industries, Inc., Ethan Allen Interiors, Inc., Flexsteel Industries, Inc., Furniture Brands International, Inc., Hooker Furniture Corporation, Industrie Natuzzi ADR, Krause’s Furniture, Inc., La-Z-Boy, Inc., Leggett & Platt, Inc., Rowe Companies, Sealy Corp., Select Comfort Corp., Stanley Furniture Company, Inc. and Tempur Pedic International, Inc. We have selected the Household Furniture Index because Peer Group Index we have previously used consisting of SIC Codes 2511 and 2512, now only consists of three companies other than Stanley Furniture Company, Inc. . |

| (4) | Previous Peer Group Index as prepared by Zacks Investment Research, Inc. consists of SIC Codes 2511 and 2512. At January 14, 2012, Zacks Investment Research, Inc. reported that these two SIC Codes consisted of Bassett Furniture Industries, Dorel Industries, Inc., Ethan Allen Interiors, Inc. and Stanley Furniture Company, Inc. |

Equity Compensation Plan Information

The following table summarizes our equity compensation plans as of December 31, 2011:

| Number of shares to be issued upon exercise of outstanding options, warrants and rights |

Weighted-average exercise price of outstanding options, warrants and rights |

Number of shares remaining available for future issuance under equity compensation plans |

||||||||||

| Equity compensation plans approved by stockholders |

1,814,956 | $ | 6.39 | 178,696 | ||||||||

|

|

|

|

|

|

|

|||||||

11

Table of Contents

Item 6. Selected Financial Data

| Years Ended December 31, | ||||||||||||||||||||

| 2011 | 2010 | 2009 | 2008 | 2007 | ||||||||||||||||

| (in thousands, except per share data) | ||||||||||||||||||||

| Income Statement Data: |

||||||||||||||||||||

| Net sales |

$ | 104,646 | $ | 137,012 | $ | 160,451 | $ | 226,522 | $ | 282,847 | ||||||||||

| Cost of sales (1) |

92,175 | 153,115 | 158,695 | 197,995 | 240,932 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Gross profit (loss) |

12,471 | (16,103 | ) | 1,756 | 28,527 | 41,915 | ||||||||||||||

| Selling, general and administrative expenses (2) |

19,250 | 20,625 | 26,666 | 32,375 | 34,578 | |||||||||||||||

| Goodwill impairment charge |

9,072 | |||||||||||||||||||

| Pension plan termination charge |

6,605 | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Operating income (loss) |

(6,779 | ) | (45,800 | ) | (24,910 | ) | (3,848 | ) | 732 | |||||||||||

| Income from Continued Dumping and Subsidy Offset Act, net |

3,973 | 1,556 | 9,340 | 11,485 | 10,429 | |||||||||||||||

| Other income, net |

112 | 25 | 160 | 308 | 265 | |||||||||||||||

| Interest expense, net |

2,330 | 3,534 | 3,703 | 3,211 | 2,679 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income (loss) before income taxes |

(5,024 | ) | (47,753 | ) | (19,113 | ) | 4,734 | 8,747 | ||||||||||||

| Income taxes (benefit) |

1 | (3,963 | ) | (7,362 | ) | 998 | 2,845 | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) |

$ | (5,025 | ) | $ | (43,790 | ) | $ | (11,751 | ) | $ | 3,736 | $ | 5,902 | |||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Basic Earnings (loss) Per Share: |

||||||||||||||||||||

| Net income (loss) |

$ | (.35 | ) | $ | (4.11 | ) | $ | (1.14 | ) | $ | .36 | $ | .56 | |||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Weighted average shares |

14,345 | 10,650 | 10,332 | 10,332 | 10,478 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Diluted Earnings (loss) Per Share: |

||||||||||||||||||||

| Net income (loss) |

$ | (.35 | ) | $ | (4.11 | ) | $ | (1.14 | ) | $ | .36 | $ | .55 | |||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Weighted average shares |

14,345 | 10,650 | 10,332 | 10,332 | 10,677 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Cash dividends paid per share |

$ | $ | $ | $ | .40 | $ | .40 | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Balance Sheet and Other Data: |

||||||||||||||||||||

| Cash |

$ | 15,700 | $ | 25,532 | $ | 41,827 | $ | 44,013 | $ | 31,648 | ||||||||||

| Inventories |

31,084 | 25,695 | 37,225 | 47,344 | 58,086 | |||||||||||||||

| Working capital |

46,066 | 52,769 | 87,277 | 97,059 | 91,852 | |||||||||||||||

| Total assets |

80,608 | 88,396 | 150,462 | 165,871 | 173,731 | |||||||||||||||

| Capital leases |

852 | |||||||||||||||||||

| Long-term debt including current maturities |

27,857 | 29,286 | 30,714 | |||||||||||||||||

| Stockholders’ equity |

57,040 | 61,795 | 92,847 | 103,108 | 102,851 | |||||||||||||||

| Capital expenditures |

$ | 4,352 | $ | 857 | $ | 2,621 | $ | 2,261 | $ | 3,951 | ||||||||||

| (1) | Included in cost of sales in 2011 are restructuring and related charges of $416,000 for the conversion of the Stanleytown manufacturing facility to a warehouse and distribution center, the sale of the Martinsville, Virginia facility and other restructuring related cost. Included in 2010 cost of sales is $10.4 million for accelerated depreciation and restructuring and related charges, also related to the Stanleytown facility conversion. Included in cost of sales in 2009 is $5.2 million for restructuring and related charges for a warehouse consolidation, elimination of certain positions, and a write-down of inventories. Included in cost of sales in 2008 is $5.9 million for the consolidation of two manufacturing facilities into one. Included in cost of sales in 2007 is $3.6 million for the conversion of a manufacturing facility to a warehouse operation. |

| (2) | Included in selling, general and administrative expenses in 2009 is $876 thousand and in 2008 is $1.4 million of restructuring charges. |

12

Table of Contents

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operation

Overview

Significant declines in housing activity, consumer confidence and disposable income have led to depressed consumer demand for residential furniture. We began to see signs of this slowdown in early 2005 and it intensified through the early part of 2011 when demand began to show signs of stabilizing. As a result, our revenues have declined dramatically over this time period. In response to these deteriorating industry conditions, we took several significant steps over the last five years to align our cost structure and operating models with lower sales volumes.

| • | During 2007 and 2008, we consolidated various production and warehousing operations to improve asset utilization and production efficiencies at our Virginia facilities. The related pre-tax restructuring cost was $3.6 million in 2007 and $7.3 million in 2008. |

| • | In 2009, pre-tax restructuring charges of $6.1 million were incurred for three major items. We ceased operations at our former Lexington, North Carolina warehouse facility with a $2 million pre-tax charge. The real estate was sold in early 2010. We eliminated approximately 25% of our salaried positions through a combination of early-retirement incentives and layoffs resulting in about $2 million of pre-tax charges. The remainder of about $2 million pre-tax restructuring expense was due to a write-down of inventories as a result of reducing the number of items offered in our adult product line. |

| • | In the second half of 2009, we began implementing a strategy to differentiate our Young America product line. This led us to shift the production of sourced items from overseas to our domestic facilities. These items were primarily youth beds and cribs. This transition began in late 2009 and our Young America children’s furniture product line is now exclusively manufactured in one facility in Robbinsville, North Carolina. |

| • | In 2010, we concluded that demand for products in the premium segment resulted in a unit volume below that necessary to profitably operate a facility the size of ours in Stanleytown, Virginia. Accordingly, we transitioned the manufacturing of the Stanley Furniture product line from our Stanleytown, Virginia facility to several strategic offshore vendors and ceased manufacturing operations in December 2010. A pre-tax accelerated depreciation and restructuring related cost of $10.4 million was incurred in 2010. Also in December 2010 we sold our Stanleytown, Virginia property and leased back a substantial portion for five years to accommodate our anticipated warehousing needs. Simultaneously, we sold our Martinsville, Virginia facility and leased back the facility on a rent-free basis for an initial one-year term. The Martinsville transaction was accounted for as a financing arrangement. In late 2011, we agreed to a five year lease term that commenced at the end of the rent free period, December 31, 2011. |

| • | In 2011, we evaluated our overall warehousing and distribution requirements for our Stanley Furniture product line. We concluded that with a distribution warehouse in Asia and our Martinsville, Virginia warehouse, we would have adequate space to service our Stanley Furniture product line. Therefore, included in the 2011 restructuring charges are $499,000 in future lease payments for the portions of the facility at Stanleytown, Virginia we no longer use. Currently we are using our leased Martinsville, Virginia facility and a portion of the leased facility at Stanleytown for domestic warehousing and distribution. We also lease a warehouse in Asia to assist with the distribution of our direct container program. During the first half of 2012, we expect to further reduce the warehouse footage required at our leased facility in Stanleytown, Virginia. This will result in an additional restructuring charge for the future lease commitment in the range of $400,000 to $600,000. |

The above actions resulted in significant losses in 2009 and 2010 and to a lesser extent in 2011. However, the decisions made and changes endured during the economic downturn allowed us to shift our operational strategy so that we could respond to the demands of a new marketplace. The transition of our Stanley Furniture product line from a largely domestic operation to one that operates on an exclusively overseas manufacturing platform is now complete. Our transition away from overseas sources for our Young America product line made progress over the past year with significant improvements in our Robbinsville facility, and we believe we have dedicated the appropriate resources to improve efficiencies and processes.

13

Table of Contents

We will continue to evaluate our warehousing and manufacturing capacity needs considering offshore sourcing opportunities, current and anticipated demand for our products, overall market conditions and other factors we consider relevant. Should further capacity reductions become necessary, this could cause additional restructuring charges in the future, however we remain committed to our distinct operating strategies for each product line. We will continue to focus on effective balance sheet management and cost control in 2012.

Results of Operations

2011 Compared to 2010

Net sales decreased $32.4 million, or 23.6%, in 2011 compared to 2010. The decrease was due primarily to lower unit volume. We believe the overall decline was the result of loss of market share and continued weakness in demand for residential wood furniture in the premium segment. We believe the loss of market share resulted from the transition caused by the major restructuring of our business. Partially offsetting the unit decline was higher average selling prices for our Young America products.

Gross profit in 2011 increased to $12.5 million, or 11.9% of net sales, from a loss of $16.1 million in 2010. Included in gross profit in 2011 and 2010 is $416,000 and $10.4 million, respectively, in restructuring and related charges. See Note 8 of the Notes to the Consolidated Financial Statements for further details on restructuring and related charges. The remaining improvement in gross profit for 2011 compared to 2010 resulted primarily from the Stanley product line operating with a globally sourced model with little fixed cost burden. Also contributing to the improved margins was the progression of operational improvements throughout the year in Robbinsville combined with higher average selling prices for Young America.

Selling, general and administrative expenses for 2011 were $19.3 million, or 18.4% of net sales, compared to $20.6 million, or 15.1% of net sales, in 2010. The decline in this expense is primarily due to the impact that lower sales has on variable selling expenses. Partially offsetting these lower costs were increased spending on marketing related expenses to educate the consumer on the reinvention of our product lines and increased bad debt expense. The higher percentage in 2011 is primarily due to lower sales.

During the first quarter of 2010, we completed an impairment analysis of goodwill and recognized a charge of $9.1 million, the entire amount of goodwill at the time.

As a result of the above, operating loss improved to $6.8 million in 2011 compared with an operating loss of $45.8 million in 2010.

We recorded income, net of legal expenses, of $4.0 million in 2011 from the receipt of funds under the Continued Dumping and Subsidy Offset Act of 2000 (CDSOA) involving wooden bedroom furniture imported from China and other related payments compared to $1.6 million in 2010.

Interest expense in 2011 declined from 2010 due to the repayment of all outstanding debt in December 2010. Interest expense in the current year is composed of interest on insurance policy loans from a legacy deferred compensation plan and imputed interest on a lease related obligation.

Our effective tax rate for 2011 was essentially zero compared to a tax benefit rate of 8.3% in 2010. The 2011 rate is the result of using all available carry-back income and maintaining a full valuation allowance for our deferred tax assets in excess of our deferred tax liabilities. The effective tax benefit rate for 2010 was 8.3% which differs from the U.S. federal statutory rate of 35% because of the establishment of a deferred tax valuation allowance and to a lesser extent the goodwill impairment charge.

2010 Compared to 2009

Net sales decreased $23.4 million, or 14.6%, in 2010 compared to 2009. The decrease was due primarily to lower unit volume, resulting from continued weakness in demand for the premium segment of residential wood furniture, which we believe was consistent with current economic and industry trends. We also believe some loss of market share resulting from the transition caused by the major restructuring of our business contributed to the decline. Partially offsetting the unit decline was higher average selling prices for our Young America products.

14

Table of Contents

Gross profit in 2010 decreased to a loss of $16.1 million from a profit of $1.8 million in 2009. Included in gross profit in 2010 and 2009 is $10.4 million and $5.2 million, respectively, in restructuring and related charges. See Note 8 of the Notes to the Consolidated Financial Statements for further details on restructuring and related charges. The remaining decline in gross profit for 2010 compared to 2009, resulted primarily from lower sales and production levels, manufacturing inefficiencies and increased cost of transitioning approximately one-third of our Young America product line revenues from overseas vendors into our Robbinsville, North Carolina production facility, and inefficiencies associated with ceasing manufacturing at our Stanleytown, Virginia facility. Partially offsetting these factors were lower expenses resulting from previous restructuring efforts, on-going cost reductions, and increased selling prices in the second half of 2010 on our Young America product line.

Selling, general and administrative expenses for 2010 decreased $6.0 million compared to 2009, due primarily to lower selling expenses resulting from lower sales and cost reduction initiatives. Restructuring and related expenses of $876,000 are included in 2009.

During the first quarter of 2010, we determined that goodwill impairment indicators existed based on our first quarter operating loss and restructuring plans. Upon completing our impairment analysis, a goodwill impairment charge of $9.1 million, the entire amount of goodwill associated with the business, was recognized.

As a result of the above, operating loss was $45.8 million in 2010 compared to an operating loss of $24.9 million in 2009.

We recorded income of $1.6 million in 2010 from the receipt of funds under the CDSOA involving wooden bedroom furniture imported from China and other related payments, net of legal expenses, compared to $9.3 million in 2009.

Interest expense for 2010 declined from 2009 due to lower average debt levels, partially offset by higher interest rates on outstanding debt.

The effective tax benefit rate for 2010 was 8.3% which differs from the U.S. federal statutory rate of 35% due primarily to the establishment of a deferred tax valuation allowance and to a lesser extent the goodwill impairment charge.

Financial Condition, Liquidity and Capital Resources

Sources of liquidity include cash on hand and cash generated from operations. We expect these sources of liquidity to be adequate for ongoing expenditures and capital expenditures for the foreseeable future. We expect our ongoing efforts with our Young America product line to positively impact operating income and cash flows from operations in 2012. We believe that cash on hand will be adequate during 2012 in the event we do not generate cash from operations. In 2012, our capital projects will include continued investment to modernize our Young America manufacturing facility, investment in adequate finished goods inventory to support projected growth of our Stanley Furniture product line and the investment in systems and business intelligence tools that will allow us to convey timely, accurate and transparent information. We have the ability to delay or reduce planned capital expenditures should liquidity become more of a concern. At December 31, 2011 cash on hand was $17.3 million including $1.6 million in restricted cash.

Working capital, excluding cash and restricted cash, increased during 2011 to $28.8 million from $27.2 million on December 31, 2010. The increase was primarily the result of a build in finished goods inventory resulting from the transitioning of the Stanley Furniture product line to a completely offshore sourcing model. Partially offsetting the increase in inventories was a decrease in income tax receivables and other miscellaneous receivables.

Cash used by operations was $7.3 million in 2011 compared to cash used of $9.4 million in 2010 and $1.2 million in 2009. The decrease in cash used by operations in 2011 was primarily due to lower cash paid to suppliers and employees resulting from savings related to our operational transitions of our Stanley Furniture product line and improved operational efficiencies in our Young America product line. Also, contributing to the lower cash used from operations was higher average selling prices on our Young America product line, increased proceeds from the Continued Dumping and Subsidy Offset Act and lower interest payments. These improvements were partially offset by a decrease in cash received from customers due to lower sales and a reduction in income tax refunds. The increase in cash used by operations in 2010 was primarily due to lower receipts from customers due to lower sales and higher cash paid to suppliers and employees due to manufacturing inefficiencies, the incremental cost of transitioning approximately one-third of our Young America product line revenues from overseas into domestic facilities, and inefficiencies associated with ceasing production at our Stanleytown facility. Partially offsetting this increase was the receipt of tax refunds and increased prices on our Young America product line.

15

Table of Contents

Net cash used by investing activities was $4.4 million in 2011 compared to cash provided of $4.8 million in 2010 and cash used of $1.3 million in 2009. Included in 2011 activity was a $1.6 million transfer of cash to restricted cash to secure letters of credit. Sale of assets provided cash of $1.6 million, $5.7 million and $1.3 million in 2011, 2010 and 2009, respectively. During 2011, we began a strategic investment program in our Young America operations which should improve our ability to service our customers and lower our costs. We invested $4.4 million in capital expenditures in 2011 compared to $857,000 in 2010 and $2.6 million in 2009. Capital expenditures in 2012 are anticipated to be approximately $4.0 million in support of the strategic investment in our Robbinsville, North Carolina manufacturing facility and we plan to invest approximately $3.0 million over the next two years in new systems.

Net cash provided by financing activities was $1.9 million in 2011 compared to cash used of $11.7 million in 2010 and cash provided of $318,000 in 2009. In 2011, proceeds from insurance policy loans provided cash of $2.0 million. In 2010, cash of $27.9 million was used to retire outstanding debt. Cash proceeds of $11.8 million (net of expenses) were received from the issuance of 4 million shares of our common stock. Proceeds of $2.4 million were received from the sale of our Martinsville, Virginia facility which was accounted for as a financing obligation. In 2009, proceeds from insurance policy loans were partially offset by debt service on outstanding debt.

The following table sets forth our contractual cash obligations and other commercial commitments at December 31, 2011 (in thousands):

| Payment due or commitment expiration | ||||||||||||||||||||

| Total | Less Than 1 year |

2-3 years | 4-5 years | Over 5 years |

||||||||||||||||

| Contractual cash obligations: |

||||||||||||||||||||

| Postretirement benefits other than pensions(1) |

$ | 3,465 | $ | 370 | $ | 651 | $ | 562 | $ | 1,882 | ||||||||||

| Operating leases |

5,489 | 1,357 | 2,647 | 1,485 | ||||||||||||||||

| Capital lease |

894 | 147 | 294 | 294 | 159 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total contractual cash obligations |

$ | 9,848 | $ | 1,874 | $ | 3,592 | $ | 2,341 | $ | 2,041 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Other commercial commitments: |

||||||||||||||||||||

| Letters of credit |

$ | 1,587 | $ | 1,587 | ||||||||||||||||

|

|

|

|

|

|||||||||||||||||

| (1) | The RP-2000 Combined Health Mortality Table with generational mortality improvements were used in estimating future benefit payments, and the health care cost trend rate for determining payments is 9.0% for 2011 and gradually declines to 5.5% in 2018 where it is assumed to remain constant for the remaining years. |

Not included in the above table is unrecognized tax benefits of $650,000, due to the uncertainty of the date of occurrence.

Continued Dumping and Subsidy Offset Act (CDSOA)

We received proceeds of $4.0 million, $1.6 million, and $9.3 million in 2011, 2010, and 2009, respectively, from CDSOA payments and other related payments, net of legal expenses. These payments came from the antidumping case involving Wooden Bedroom Furniture imported from China. The CDSOA provides for distribution of monies collected by U.S. Customs and Border Protection (CBP) for imports covered by antidumping duty orders entering the United States through September 30, 2007 to qualified affected domestic producers. Antidumping duties for merchandise entering the U.S. after September 30, 2007 remain with the U.S. Treasury.

Approximately $152 million of CDSOA funds that otherwise would have been available for distribution to qualifying affected domestic producers of wooden bedroom furniture were withheld by the government over the past five years, excluding 2011, as a result of two court cases involving challenges to the CDSOA on constitutional grounds. In 2009, the U.S. Court of Appeals for the Federal Circuit determined in one of those cases that the CDSOA does not violate the Constitution’s free speech and equal protection guarantees. In May 2010, the U.S. Supreme Court denied a petition for certiorari that sought review of the Federal Circuit’s decision. In 2010, the Federal Circuit also summarily dismissed the constitutional claims in the second of the two court cases. Other CDSOA-related cases specific to wooden bedroom furniture are pending before the U.S. Court of International Trade and the Federal Circuit. During the second quarter of 2011, we received $1.2 million in funds that were previously withheld due to pending litigation and then released following the dismissal of several of these constitutional claims. Also, for distributions made in the fourth quarter 2011 the government did not withhold any funds related to these remaining cases. The resolution of these remaining cases will have a significant impact on the amount of CDSOA funds that may be distributed to qualifying affected domestic producers of wooden bedroom furniture. Based on our allocation of the CDSOA funds distributed in each of the past six years, we could receive an additional $40 million of the remaining funds set aside by the government, although the extent to which and

16

Table of Contents

when such distributions ultimately may be received is uncertain. The fact that some claims were dismissed and funds distributed during the second quarter of 2011 and the fact that no funds were withheld from the fourth quarter 2011 distribution are not necessarily indications that the remaining funds withheld due to litigation will be distributed in the future.

According to CBP, as of October 1, 2011, approximately $9.1 million in duties had been secured by cash deposits and bonds on unliquidated entries of wooden bedroom furniture that are subject to the CDSOA, and this amount is potentially available for distribution under the CDSOA to eligible domestic manufacturers in connection with the case involving wooden bedroom furniture imported from China. The amount ultimately distributed will be impacted by appeals concerning the results of the annual administrative review process, which can retroactively increase or decrease the actual duties owed on entries secured by cash deposits and bonds, by collection efforts concerning duties that may be owed, and by any applicable legislation and CBP’s interpretation of that legislation. Assuming that such funds are distributed and that our percentage allocation in future years is the same as it was for the 2011 distribution (approximately 30% of the funds distributed) and the $9.1 million collected by the government as of October 1, 2011 does not change as a result of the annual administrative review process or otherwise, we could receive approximately $2.7 million in CDSOA funds in addition to the funds held back and withheld pending the final resolution of the court cases discussed above.

Due to the uncertainty of the various legal and administrative processes, we cannot provide assurances as to the amount of additional CDSOA funds that ultimately will be received, if any, and we cannot predict when we may receive any additional CDSOA funds.

Critical Accounting Policies

We have chosen accounting policies that are necessary to accurately and fairly report our operational and financial position. Below are the critical accounting policies that involve the most significant judgments and estimates used in the preparation of our consolidated financial statements.

Allowance for doubtful accounts – We maintain an allowance for doubtful accounts for estimated losses resulting from the failure of our customers to make required payments. We perform ongoing credit evaluations of our customers and monitor their payment patterns. Should the financial condition of our customers deteriorate, resulting in an impairment of their ability to make payments, additional allowances may be required which would reduce our earnings.

Inventory valuation – Inventory is valued at the lower of cost or market. Cost for all inventories is determined using the first-in, first-out (FIFO) method. We evaluate our inventory to determine excess or slow moving items based on current order activity and projections of future demand. For those items identified, we estimate our market value based on current trends. Those items having a market value less than cost are written down to their market value. If we fail to forecast demand accurately, we could be required to write off additional non-saleable inventory, which would also reduce our earnings.

Deferred Taxes – We recognize deferred tax assets and liabilities based on the estimated future tax effects of differences between the financial statements and the tax basis of assets and liabilities given the enacted tax laws. We evaluate the need for a deferred tax asset valuation allowance by assessing whether it is more likely than not that the company will realize its deferred tax assets in the future. The assessment of whether or not a valuation allowance is required often requires significant judgment, including the forecast of future taxable income. Adjustments to the deferred tax valuation allowance are made to earnings in the period when such assessment is made.

In preparation of the company’s financial statements, management exercises judgments in estimating the potential exposure to unresolved tax matters and applies a more likely than not criteria approach for recording tax benefits related to uncertain tax positions. While actual results could vary, in management’s judgment, the company has adequate tax accruals with respect to the ultimate outcome of such unresolved tax matters.

Long-lived assets – Property, plant and equipment is reviewed for possible impairment when events indicate that the carrying amount of an asset may not be recoverable. Assumptions and estimates used in the evaluation of impairment may affect the carrying value of long-lived assets, which could result in impairment charges in future periods that would lower our earnings. Depreciation policy reflects judgments on the estimated useful lives of assets. If the estimated remaining useful lives of our assets decrease, we would be required to depreciate our assets more quickly, which would also lower our earnings.

17

Table of Contents

Off-Balance Sheet Arrangements

We do not have transactions or relationships with “special purpose” entities, and we do not have any off-balance sheet financing other than normal operating leases primarily for warehousing, showroom and office space, and certain technology equipment.

Item 7A. Quantitative and Qualitative Disclosures about Market Risk

None of our foreign sales or purchases are denominated in foreign currency and we do not have any foreign currency hedging transactions. While our foreign purchases are denominated in U.S. dollars, a relative decline in the value of the U.S. dollar could result in an increase in the cost of products obtained from offshore sourcing and reduce our earnings, unless we are able to increase our prices for these items to reflect any such increased cost.

Item 8. Financial Statements and Supplementary Data

The consolidated financial statements and schedule listed in items 15(a) (1) and (a) (2) hereof are incorporated herein by reference and are filed as part of this report.

Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

None.

Ite m 9A. Controls and Procedures

Conclusion Regarding the Effectiveness of Disclosure Controls and Procedures

Under the supervision and with the participation of our management, including our principal executive officer and principal financial officer, we conducted an evaluation of our disclosure controls and procedures, as such term is defined under Rule 13a-15(e) promulgated under the Securities Exchange Act of 1934, as amended (the Exchange Act). Based on this evaluation, our principal executive officer and our principal financial officer concluded that our disclosure controls and procedures were effective as of the end of the period covered by this annual report.

Management’s Report on Internal Control over Financial Reporting

Our management is responsible for establishing and maintaining adequate internal control over financial reporting, as such term is defined in Exchange Act Rule 13a-15(f). Under the supervision and with the participation of our management, including our principal executive officer and principal financial officer, we conducted an evaluation of the effectiveness of our internal control over financial reporting based on the framework in Internal Control-Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission. Based on our evaluation under the framework in Internal Control – Integrated Framework, our management concluded that our internal control over financial reporting was effective as of December 31, 2011. The effectiveness of our internal control over financial reporting as of December 31, 2011 has been audited by PricewaterhouseCoopers LLP, our independent public accounting firm, as stated in their report, which is included on page F-2 of this Annual Report on Form 10-K.

Changes in Internal Controls over Financial Reporting

There were no changes in our internal control over financial reporting that occurred during the fourth quarter that have materially affected, or are reasonably likely to materially affect, our internal control over financial reporting.

None.

18

Table of Contents

Item 10. Directors, Executive Officers and Corporate Governance

Information related to our directors is set forth under the caption “Election of Directors” of our proxy statement (the “2012 Proxy Statement”) for our annual meeting of shareholders scheduled for April 18, 2012. Such information is incorporated herein by reference.

Information relating to compliance with section 16(a) of the Exchange Act is set forth under the caption “Section 16(a) Beneficial Ownership Reporting Compliance” of our 2012 Proxy Statement and is incorporated herein by reference.

Information relating to the Audit Committee and Board of Directors’ determinations concerning whether a member of the Audit Committee of the Board is a “financial expert” as that term is defined under Item 407(d) (5) of Regulation S-K is set forth under the caption “Board and Board Committee Information” of our 2012 Proxy Statement and is incorporated herein by reference.

Information concerning our executive officers is included in Part I of this report under the caption “Executive Officers of the Registrant.”

We have adopted a code of ethics that applies to our associates, including the principal executive officer, principal financial officer, principal accounting officer or controller, or person performing similar functions. Our code of ethics is posted on our website at www.stanleyfurniture.com. Amendments to and waivers from our code of ethics will be posted to our website when permitted by applicable SEC and NASDAQ rules and regulations.

Item 11. Executive Compensation

Information relating to our executive compensation is set forth under the captions “Compensation of Executive Officers,” “Compensation Committee Interlocks and Insider Participation” and “Compensation Committee Report” of our 2012 Proxy Statement. Such information is incorporated herein by reference.

Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

Our information relating to this item is set forth under the caption “Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters” of our 2012 Proxy Statement. Such information is incorporated herein by reference.

Information concerning our equity compensation plan is included in Part II of this report under the caption “Equity Compensation Plan Information.”

Item 13. Certain Relationships and Related Transactions, and Director Independence

Our information relating to this item is set forth under the caption “Compensation of Executive Officers – Employment Agreements and Related Transactions” and “Board and Board Committee Information” of our 2012 Proxy Statement. Such information is incorporated herein by reference.

Item 14. Principal Accounting Fees and Services

Our information relating to this item is set forth under the caption “Independent Registered Public Accountants” of our 2012 Proxy Statement. Such information is incorporated herein by reference.

Item 15. Exhibits, Financial Statement Schedules

| (a) | Documents filed as a part of this Report: |

| (1) | The following consolidated financial statements are included in this report on Form 10-K: |

Report of Independent Registered Public Accounting Firm

Consolidated Balance Sheets as of December 31, 2011 and 2010

Consolidated Statements of Income for each of the three years in the period ended December 31, 2011

19

Table of Contents

Consolidated Statements of Changes in Stockholders’ Equity for each of the three years in the period ended December 31, 2011.

Consolidated Statements of Cash Flow for each of the three years in the period ended December 31, 2011

Notes to Consolidated Financial Statements

| (2) | Financial Statement Schedule: |

Schedule II – Valuation and Qualifying Accounts for each of the three years in the period ended December 31, 2011.

| (b) | Exhibits: | |

| 3.1 | The Restated Certificate of Incorporation of the Registrant (incorporated by reference to Exhibit 3.1 to the Registrant’s Form 10-Q (Commission File No. 0-14938) for the quarter ended July 2, 2005). | |

| 3.2 | By-laws of the Registrant as amended (incorporated by reference to Exhibit 3.1 to the Registrant’s Form 8-K (Commission File No. 0-14938) filed February 3, 2010). | |

| 4.1 | The Certificate of Incorporation and By-laws of the Registrant as currently in effect (incorporated by reference to Exhibits 3.1 and 3.2 hereto). | |

| 10.1 | Supplemental Retirement Plan of Stanley Furniture Company, Inc., as restated effective January 1, 1993 (incorporated by reference to Exhibit 10.8 to the Registrant’s Form 10-K (Commission File No. 0-14938) for the year ended December 31, 1993).(1) | |

| 10.2 | First Amendment to Supplemental Retirement Plan of Stanley Furniture Company, Inc., effective December 31, 1995, adopted December 15, 1995 (incorporated by reference to Exhibit 10.7 to the Registrant’s Form 10-K (Commission File No. 0-14938) for the year ended December 31, 1995).(1) | |

| 10.3 | Stanley Interiors Corporation Deferred Compensation Capital Enhancement Plan, effective January 1, 1986, as amended and restated effective August 1, 1987 (incorporated by reference to Exhibit 10.12 to the Registrant’s Registration Statement on Form S-1 (Commission File No. 0-14938), No. 33-7300).(1) | |

| 10.4 | 2000 Incentive Compensation Plan (incorporated by reference to Exhibit A to the Registrant’s Proxy Statement (Commission File No. 0-14938) for the special meeting of stockholders held on August 24, 2000).(1) | |

| 10.5 | Second Amendment to Supplemental Retirement Plan of Stanley Furniture Company, Inc. effective January 1, 2002 (incorporated by reference to Exhibit 10.33 to the Registrant’s Form 10-K (Commission File No. 0-14938) for the year ended December 31, 2002).(1) | |

| 10.6 |

Form of Stock Option Award under 2000 Incentive Plan (ISO) (incorporated by reference to Exhibit 10.23 to the Registrant’s Form 10-K (Commission File No. 0-14938) for the year ended December 31, 2004).(1) | |