Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - STRATEGIC HOTELS & RESORTS, INC | d286792d8k.htm |

Exhibit 99.1

Investor Presentation

January 2012

* * * * * * * * * * * * * * * * * * |

2

I.

Company Overview

II.

Industry Update

III.

Operating Trends

IV.

Financial Overview

Agenda |

3

World-class luxury hotels supported by unique real estate value

Investment acumen and discipline

Industry leading asset management capabilities

Brand leadership experience

Value creating hotel management contract renegotiation expertise

Depth and breadth of long-term relationships throughout the hotel

industry BEE Core Competencies

Fairmont Chicago

Lobby and ENO Wine Bar

Four Seasons Punta Mita

Coral Suite

Hotel del Coronado

Beach Village

Highest quality hotel portfolio in the public markets |

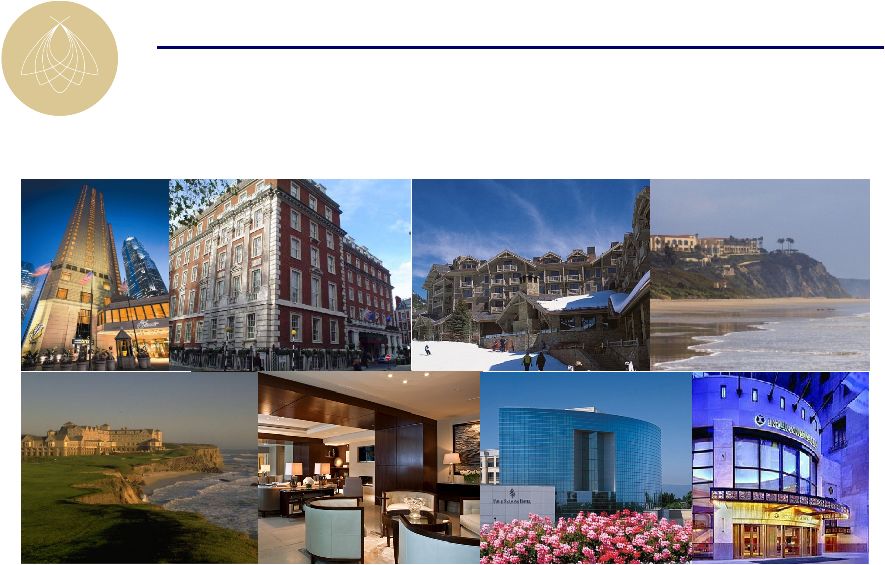

4

17 hotels and resorts with 7,762 rooms

Top-Tier Market Exposure

Assets

located

in

primary

gateway

cities

and

high

barrier

to

entry

markets |

5

Unique and Irreplaceable Hotel Portfolio

Fairmont Chicago

Marriott Grosvenor Square

Four Seasons Jackson Hole

Ritz-Carlton Laguna Niguel

Ritz-Carlton Half Moon Bay

Four Seasons Washington, D.C.

Four Seasons Silicon Valley

InterContinental Chicago |

6

Market share growth and revenue enhancement through market research based

programs

Exceptional asset management supported by internally developed operating

systems Aggressive and early cost cutting initiatives implemented in advance

of the 2008 / 2009 recession

Proactively maintaining fixed cost reduction at hotels during recovery phase

Rigorous oversight of brand managers to ensure alignment of interests

Evaluation and implementation of value add ROI projects; constant pipeline

Industry Leading Asset Management Capabilities |

7

Notable 2008

capital

projects

Notable 2009

capital

projects

InterContinental Miami –

Guestroom renovation

InterContinental Chicago –

Michael Jordan’s Steak House

Four Seasons Washington, D.C –

Retail outlet renovation

Marriott Lincolnshire –

Lobby renovation

Westin St. Francis –

Michael Mina Steakhouse conversion

Four Seasons Washington, D.C. –

Lobby renovation, 11-room

expansion, new restaurant, 63-room and suite renovation

Westin St. Francis –

Clock Bar

Fairmont Chicago –

ENO wine tasting room, lobby renovation,

guestroom renovation, new spa and fitness center

Four Seasons Punta Mita –

New lobby bar

Ritz-Carlton Half Moon Bay –

ENO wine tasting room,

restaurant and lounge renovation, suite renovation

Portfolio Well-Positioned To Enhance Cash Flow Growth

Notable 2010

capital

projects

Notable 2011

capital

projects

Fairmont Chicago Lobby

Four Seasons Washington, D.C.

Lobby

Westin St. Francis Michael Mina

Bourbon Steak

InterContinental Miami Guestroom |

8

Four Seasons D.C.

ROI Capital Project Examples

InterContinental Chicago

Hotel del Coronado

(1)

(1)

(1)

Represents 100% ownership

(1)

(1)

Description:

Bourbon Steakhouse

ENO Wine Room &

Starbucks

North Beach

Development

Year of Project:

2008 - 2009

2006 - 2007

2007

Investment ($mm):

$8.4

$2.9

$68.4

2010 EBITDA Yield (%):

15%

28%

$113 million in unit sales

~$45 million in unit sales profit

$6.6 million in 2010 EBITDA |

9

I.

Company Overview

II.

Industry Update

Agenda |

10

Lodging demand historically correlates with GDP (~80%) but potential exists for

near-term disconnect, particularly at the high-end

To date, little to no indication of a decline in group bookings or an increase in

group cancellations Supply growth remains historically low and development

pipeline indicates muted supply going forward Lodging Outlook

Demand growth exceeds supply growth by 450 bps which should result in

significant ADR growth as recovery continues; lower correlation to GDP

|

11

Source: Smith Travel Research

Note: Data represents trends within the United States

Luxury supply growth was lower leading into this downturn than past downturns

Projects in planning or under construction have decreased significantly

No new competitive luxury or upper-upscale supply projected in BEE

markets 1-2 years estimated time to permit; 3 years estimated time to

build a luxury hotel New hotel construction economic proposition doubtful

with replacement cost estimated at over $700,000 per key

Quarterly luxury supply YoY % change

(4%)

(2%)

0%

2%

4%

6%

8%

10%

12%

14%

YoY % supply growth

1988 –

Q2 2011

Average: 4.1%

Favorable Supply Outlook

Zero supply growth environment and no new

supply growth likely until after 2015

Supply Growth in

BEE Markets = 0.0% |

12

Source: Smith Travel Research and PWC

Luxury

hotels

have

experienced

prolonged

RevPAR

growth

following

past

industry

downturns

–

1992

–

2000:

9

consecutive

years

of

annual

luxury

RevPAR

growth

totaling

109%

or

8.5%

annually

–

2002

–

2007:

5

consecutive

years

of

annual

luxury

RevPAR

growth

totaling

48%

or

8.2%

annually

Overall luxury room nights sold is at an all-time high; 33% higher than

2007 Luxury Hotels Outperform in a Recovery

Luxury room night demand currently at all-

time high

Luxury outperformed Total U.S. 2.0% -

4.0% in previous two downturns

Source: Smith Travel Research |

13

Note: All metrics represent full-year 2010 results

BEE portfolio reflects Same Store North American portfolio as of 12/31/2010.

Source: Public filings

BEE Positioning Compared to Peers

BEE delivers industry leading results |

14

I.

Company Overview

II.

Industry Update

III.

Operating Trends

Agenda |

15

Group Booking Outlook

Year-Over-Year Group Pace

*2012 production in the year assumes the same production as in 2011

Group pace remains the most reliable forward looking indicator

Booking window has shortened forcing more reliance on room nights booked ITYFTY

(“in-the-year-for-the-year”)

Group

room

nights

on

the

books

for

2012

are

up

1.5%

compared

to

same

time

last

year;

ADR

up

5%

compared

to

2011

rate |

16

Embedded Portfolio Growth

Operating performance improving; still significantly below peak

Note: Same store North America portfolio, excludes: Hotel del Coronado, Fairmont

Scottsdale Princess, Four Seasons Jackson Hole, Four Seasons Silicon

Valley $120

$160

$200

$240

$280

60.0%

64.0%

68.0%

72.0%

76.0%

80.0%

2007

2008

2009

2010

2011F

ADR / RevPAR

Occupancy

Occupancy

ADR

RevPAR |

17

(EBITDA in millions)

(a)

Excludes Fairmont Scottsdale Princess, Four Seasons Jackson Hole, Four Seasons

Silicon Valley, and Hotel del Coronado Year-To-Date Results

YTD 9/30/10

YTD 9/30/11

Operations

(Same Store U.S. Portfolio)

(a)

ADR

$211

7.2%

$227

RevPAR

$146

13.5%

$166

Total RevPAR

$272

11.7%

$304

EBITDA Margins

17.9%

330 bps

21.2%

Corporate Results

Comparable EBITDA

$97.6

17.7%

$114.8

Comparable FFO / share

$0.02

350.0%

$0.09 |

18

I.

Company Overview

II.

Industry Update

III.

Operating Trends

IV.

Financial Overview

Agenda |

19

2011 Guidance

(EBITDA in millions)

(b)

2010 results exclude $4.9 mm of real estate tax refunds and no adjustments for

cancellation fees (c)

2010 excludes $12.6 mm of VCP expense; 2011 VCP expense excluded

(a)

Portfolio excludes Fairmont Scottsdale Princess, Four Seasons Jackson Hole, Four

Seasons Silicon Valley, and Hotel del Coronado 2010

2011 Guidance

Operations

(Same Store North America Portfolio)

(a)

RevPAR

$153

9%-10%

$167-$168

Total RevPAR

$287

8%-9%

$309-312

EBITDA Margins

(b)

19.0%

200 - 300bps

21%-22%

Corporate Results

(c)

EBITDA

$132

14%-18%

$150-$156

FFO / share

$0.05

100%-160%

$0.10-$0.13 |

20

Raised $550 million in equity:

$335 mm secondary offering (May 2010)

$145

mm

Woodbridge

transaction

acquiring

two

Four

Seasons

hotels

plus

PIPE

(February

2011)

$70 mm equity placement to GIC for share in InterContinental Chicago (June

2011) Asset sales:

Sold InterContinental Prague for €110.6mm (December 2010)

Sold leasehold position at Marriott Paris Champs-Elysees for approximately $60

million (April 2011) Sold stake in BuyEfficient for $9mm (January

2011) Debt Repayments:

Tendered

and

fully

retired

$180mm

unsecured

convertible

recourse

notes

(May

2010)

Hotel del Coronado complex restructuring (February 2011):

Negotiated new joint-venture with Blackstone and KSL

Closed new CMBS mortgage financing totaling $425mm

Fairmont Scottsdale Princess complex restructuring (June 2011):

Negotiated new joint venture structure with Walton Street Capital

Negotiated amendment and extension to CMBS debt for four years at below market

terms New Line of Credit (June 2011):

Reduced lenders in bank syndicate from 21 banks to 10 banks

Achieved three year term with one year extension

Debt refinancings:

Six property loans refinanced totaling nearly $800 million

Preferred Equity Tender (December 2011):

Successfully tendered for approximately 22% of outstanding preferred equity at a

15% discount to par plus accrued preferred dividends

Accomplishments Since January 1*, 2010

ST |

21

$52.2

$130.0

$317.8

$195.0

$145.0

$66.5

$145.8

$114.0

$0.0

$100.0

$200.0

$300.0

$400.0

$500.0

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

Bank / Life Co.

CMBS

Fairmont Scottsdale

Hotel del Coronado

European

Corporate

$300.0

Capacity

$275.8

$281.7

$173.5

$90.0

$194.8

$180.0

$282.8

$148.9

$124.9

$358.0

$0.0

$200.0

$400.0

$600.0

$800.0

$1,000.0

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

Bank / Life Co.

CMBS

Fairmont Scottsdale

Hotel del Coronado

European

Corporate

$834.5

$875.2

($ in millions)

Note: Assumes full extension periods for all loans.

(1)

Statistics reflect successful completion of preferred equity tender

BEE’s balance sheet is structured for growth, yet prepared for volatility

Strong Recapitalized Balance Sheet

January 1, 2010

September 30, 2011

Key Stats

Net Debt/EBITDA

14.3x

Net Debt+Pref /EBITDA

17.4x

Net Debt/TEV

76.9%

Avg. Maturity (yrs)

3.4

Unencumbered assets

0

Corporate liquidity (MM)

$105.0

Mix of Debt

Bank Debt

17.8%

Life Insurance Co.

25.6%

CMBS

56.6%

Key Stats

(1)

Net Debt/EBITDA

7.6x

Net Debt+Pref /EBITDA

9.5x

Net Debt/TEV

51.2%

Avg. Maturity (yrs)

5.2

Unencumbered assets

2

Corporate liquidity (MM)

$260.0

Mix of Debt

Bank Debt

38.0%

Life Insurance Co.

31.5%

CMBS

30.5% |

22

On December 20th, 2011 the Company announced the

successful repurchase of 3,247,507 preferred shares at a 15% discount to

par + accrued dividends Successful tender provides the following

benefits: One-time savings of $20.2 million in accrued preferred

dividends Recurring savings of $6.7 million in annual preferred

dividends Reduction

in

outstanding

preferred

equity

from

$370.2

million

to

$289.1

million

Accrued

and

unpaid

dividends

through

the

quarter

ending

December

31,

2011

have

been declared and set apart for payment on our books

Successful Preferred Equity Tender

Series of

Preferred

Shares

NYSE

Ticker

Symbol

Offer Price

Per Share

Number of

Shares

Outstanding

Pre-tender

Shares

Tendered

& Accepted

Number of

Shares

Outstanding

Post-tender

Series C Shares

BEEPRC

$26.50

5,750,000

1,922,273

3,827,727

Series B Shares

BEEPRB

$26.50

4,600,000

984,625

3,615,375

Series A Shares

BEEPRA

$26.70

4,488,750

340,609

4,148,141

Total

14,838,750

3,247,507

11,591,243 |

23

Except

for

historical

information,

the

matters

discussed

in

this

press

release

are

forward-looking

statements

subject

to

certain risks and uncertainties. Actual results could differ materially from the

Company's projections and forward-looking statements

are

not

guarantees

of

future

performance.

These

forward

looking

statements

are

identified

by

looking

their

use

of terms and phrases such as “anticipate,”

“believe,”

“could,”

“estimate,”

“expect,”

“intend,”

“may,”

“plan,”

“predict,”

“project,”

“should,”

“will,”

“continue”

and other similar terms and phrases, including references to assumptions and

forecasts of future results.

Factors that may contribute to these differences include, but are not limited to

the following: ability

to

obtain,

refinance

or

restructure

debt

or

comply

with

covenants

contained

in

our

debt

facilities;

volatility

in

equity

or

debt markets; availability of capital; rising interest rates and

operating costs; rising insurance premiums; cash available for

capital expenditures; competition; demand for hotel rooms in our

current and proposed market areas; economic conditions

generally and in the real estate market specifically, including deterioration of

economic conditions and the extent of its effect on business and leisure

travel and the lodging industry; ability to dispose of existing properties in a manner

consistent with our disposition strategy; delays in construction

and development; the failure of closing conditions to be

satisfied; risks related to natural disasters; the effect of threats of terrorism

and increased security precautions on travel patterns and hotel bookings;

the outbreak of hostilities and international political instability; legislative or regulatory

changes, including changes to laws governing the taxation of REITs; and changes in

generally accepted accounting principles, policies and guidelines

applicable to REITs. Certain of these risks and uncertainties are described in greater

detail in our filings with the Securities and Exchange Commission. Although we

believe our current expectations to be based upon reasonable assumptions,

we can give no assurance that our expectations will be attained or that

actual results will not differ materially. We undertake no obligation to

update any forward-looking statement to conform the statement to

actual results or changes in our expectations.

Disclaimer |

24

Non-GAAP to GAAP Reconciliations

Reconciliation of Net Debt + Preferred Equity / EBITDA

($ in 000s)

YE 2009

(a)

3Q 2011

(b)(c)

Preferred equity capitalization

$370,236

$289,102

Consolidated debt

1,658,745

1,000,706

Pro rata share of unconsolidated debt

282,825

212,275

Pro rata share of consolidated debt

(107,065)

(45,548)

Cash and cash equivalents

(116,310)

(10,000)

Net Debt + Preferreds

$2,088,431

$1,446,535

Comparable EBITDA

$119,953

$153,000

Net Debt + Preferreds / EBITDA

17.4x

9.5x

(a) All figures taken from year-end 2009 financial statements.

(b) Comparable EBITDA reflects mid-point of guidance range as of Q3 2011.

(c) Updated to reflect the successful closing of preferred equity tender

Reconciliation of Net Debt / TEV

($ in 000s)

YE 2009

(a)

3Q 2011

(b)(c)

Consolidated Debt

$1,658,745

$1,000,706

Pro rata share of unconsolidated debt

282,825

212,275

Pro rata share of consolidated debt

(107,065)

(45,548)

Cash and cash equivalents

(116,310)

(10,000)

Net Debt

$1,718,195

$1,157,433

Market Capitalization

$144,966

$812,405

Total Debt

1,834,505

1,167,433

Preferred Equity

370,236

289,102

Cash and cash equivalents

(116,310)

(10,000)

Total Enterprise Value

$2,233,397

$2,258,940

Net Debt / Enterprise Value

76.9%

51.2%

(a) All figures taken from year-end 2009 financial statements.

(b) Comparable EBITDA reflects mid-point of guidance range as of Q3 2011.

(c) Updated to reflect the successful closing of preferred equity tender

Reconciliation of Net Debt / EBITDA

($ in 000s)

YE 2009

(a)

3Q 2011

(b)(c)

Consolidated debt

$1,658,745

$1,000,706

Pro rata share of unconsolidated debt

282,825

212,275

Pro rata share of consolidated debt

(107,065)

(45,548)

Cash and cash equivalents

(116,310)

(10,000)

Net Debt

$1,718,195

$1,157,433

Comparable EBITDA

$119,953

$153,000

Net Debt / EBITDA

14.3x

7.6x

(a) All figures taken from year-end 2009 financial statements.

(b) Comparable EBITDA reflects mid-point of guidance range as of Q3 2011.

(c) Updated to reflect the successful closing of preferred equity tender

|

25

Non-GAAP to GAAP Reconciliations

2011

2010

2011

2010

Net loss attributable to SHR common shareholders

(11,902)

$

(39,401)

$

(7,771)

$

(127,102)

$

Depreciation and amortization - continuing operations

25,526

32,209

86,222

98,195

Depreciation and amortization - discontinued

operations -

1,859

-

5,413

Interest expense - continuing operations

21,838

22,118

67,148

68,488

Interest expense - discontinued operations

-

2,378

-

7,716

Income taxes - continuing operations

867

68

279

296

Income taxes - discontinued

operations -

329

379

736

Noncontrolling interests

(16)

(192)

70

(879)

Adjustments from consolidated

affiliates (1,248)

(1,978)

(5,431)

(5,596)

Adjustments from unconsolidated affiliates

7,162

4,332

16,293

11,890

Preferred shareholder dividends

7,721

7,721

23,164

23,164

EBITDA

49,948

29,443

180,353

82,321

Realized portion of deferred gain on sale-leaseback -

continuing operations (42)

(51)

(151)

(154)

Realized portion of deferred gain on

sale-leaseback - discontinued operations -

(1,088)

(1,214)

(3,321)

Gain on sale of assets - continuing operations

-

-

(2,640)

-

Loss (gain) on sale of

assets - discontinued operations 35

-

(100,930)

(1,237)

Loss on early extinguishment of debt

399

39

1,237

925

Loss on early termination of

derivative financial instruments -

-

29,242

18,263

Foreign currency exchange loss (gain) - continuing

operations (a) 209

132

(77)

1,394

Foreign currency exchange loss (gain) -

discontinued operations (a) -

5,096

(51)

(7,490)

Adjustment for Value Creation Plan

(6,921)

3,844

9,078

6,871

Comparable EBITDA

43,628

$

37,415

$

114,847

$

97,572

$

(a)

Foreign currency exchange gains or losses applicable to

third-party and inter-company debt and certain balance sheet items held by

foreign subsidiaries.

September 30,

September 30,

Reconciliation of Net Loss Attributable to SHR Common Shareholders to

EBITDA and Comparable EBITDA (in thousands)

Three Months Ended

Nine Months Ended |

26

Non-GAAP to GAAP Reconciliations

2011

2010

2011

2010

Net loss attributable to SHR common shareholders

(11,902)

$

(39,401)

$

(7,771)

$

(127,102)

$

Depreciation and amortization - continuing operations

25,526

32,209

86,222

98,195

Depreciation and amortization -

discontinued operations -

1,859

-

5,413

Corporate depreciation

(279)

(304)

(868)

(914)

Gain on sale of assets

- continuing operations -

-

(2,640)

-

Loss (gain) on

sale of assets - discontinued operations 35

-

(100,930)

(1,237)

Realized portion of deferred gain on

sale-leaseback - continuing operations (42)

(51)

(151)

(154)

Realized portion of

deferred gain on sale-leaseback - discontinued operations

-

(1,088)

(1,214)

(3,321)

Deferred tax expense on realized portion of

deferred gain on sale-leasebacks -

340

379

1,036

Noncontrolling interests

adjustments (134)

(230)

(440)

(937)

Adjustments from

consolidated affiliates (663)

(1,342)

(3,822)

(4,644)

Adjustments from unconsolidated

affiliates 3,770

2,047

8,023

6,099

FFO

16,311

(5,961)

(23,212)

(27,566)

Redeemable noncontrolling interests

118

38

510

58

FFO

- Fully Diluted 16,429

(5,923)

(22,702)

(27,508)

Non-cash mark to market of interest rate swaps

1,146

5,597

(487)

9,778

Loss on early extinguishment of

debt 399

39

1,237

925

Loss on early

termination of derivative financial instruments -

-

29,242

18,263

Foreign currency exchange loss (gain) -

continuing operations (a) 209

132

(77)

1,394

Foreign currency exchange loss

(gain), net of tax - discontinued operations (a) -

5,085

(51)

(7,515)

Adjustment for Value Creation Plan

(6,921)

3,844

9,078

6,871

Comparable FFO

11,262

$

8,774

$

16,240

$

2,208

$

Comparable FFO per diluted share

0.06

$

0.06

$

0.09

$

0.02

$

Weighted average diluted

shares 188,097

153,093

175,974

114,897

(a)

Foreign currency exchange gains or losses applicable to

third-party and inter-company debt and certain balance sheet items held by foreign

subsidiaries.

Reconciliation of Net Loss Attributable to SHR Common Shareholders to

(in thousands, except per share data)

September 30,

September 30,

Three Months Ended

Nine Months Ended

Funds From Operations (FFO), FFO - Fully Diluted and Comparable

FFO |

27

Non-GAAP to GAAP Reconciliations

Operational Guidance

Low Range

High Range

North American same store Total RevPAR growth (a)

8.0%

9.0%

North American same store RevPAR growth (a)

9.0%

10.0%

(a) Includes North American hotels which are consolidated in our

financial results, but excludes the Four Seasons Jackson Hole and

Four Seasons Silicon Valley hotels.

Comparable EBITDA Guidance

Low Range

High Range

Net loss attributable to common shareholders

(39.7)

$

(33.7)

$

Depreciation and amortization

116.3

116.3

Interest expense

88.4

88.4

Income taxes

1.8

1.8

Adjustments from

consolidated affiliates (6.6)

(6.6)

Adjustments from unconsolidated

affiliates 21.5

21.5

Preferred shareholder dividends

30.9

30.9

Realized portion of deferred gain on

sale-leasebacks (1.4)

(1.4)

Gain on sale of asset

(103.5)

(103.5)

Adjustment for Value Creation Plan

12.0

12.0

Loss on early extinguishment of

debt 1.2

1.2

Loss on early termination of

derivative financial instruments 29.2

29.2

Other adjustments

(0.1)

(0.1)

Comparable EBITDA

150.0

$

156.0

$

Comparable FFO Guidance

Low Range

High Range

Net loss attributable to common shareholders

(39.7)

$

(33.7)

$

Depreciation and amortization

115.1

115.1

Realized portion of deferred gain on

sale-leasebacks (1.4)

(1.4)

Deferred tax on realized portion of

deferred gain 0.4

0.4

Adjustments from

consolidated affiliates (4.3)

(4.3)

Adjustments from unconsolidated

affiliates 9.8

9.8

Gain on sale of asset

(103.5)

(103.5)

Adjustment for Value Creation Plan

12.0

12.0

Loss on early extinguishment of

debt 1.2

1.2

Loss on early termination of

derivative financial instruments 29.2

29.2

Other adjustments

(0.6)

(0.6)

Comparable FFO

18.2

$

24.2

$

Comparable FFO per diluted share

0.10

$

0.13

$

Note: Beginning in the first quarter of 2011,

the definitions of Comparable EBITDA, Comparable FFO and Comparable FFO per diluted

share have been modified to exclude any expense related to our Value

Creation Plan. 2011 Guidance

(in millions, except per share data)

Year Ended

December 31, 2011

December 31, 2011

Year Ended

December 31, 2011

Year Ended |

*

* * * * * * * * * * * * * * *

*

* |