Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - ASSEMBLY BIOSCIENCES, INC. | v240385_8k.htm |

| EX-99.2 - EXHIBIT 99.2 - ASSEMBLY BIOSCIENCES, INC. | v240385_ex99-2.htm |

Exhibit 99.1

1 This material contains estimates and forward - looking statements. The words “believe,” “may,” “might,” “will,” “aim,” “estimate,” “continue,” “would,” “anticipate, ”“intend,” “expect,” “plan” and similar words are intended to identify estimates and forward - looking statements. Our estimates and forward - looking statements are mainly based on our current expectations and estimates of future events and trends, which affect or might affect our businesses and operations. Although we believe that these estimates and forward - looking statements are based upon reasonable assumptions, they are subject to many risks and uncertainties and are made in light of information currently available to us. Our estimates and forward - looking statements may be influenced by the following factors, among others : risks related to the costs, timing, regulatory review and results of our studies and clinical trials; our ability to obtain FDA approval of our product candidates; differences between historical studies on which we have based our planned clinical trials and actual results from our trials; our anticipated capital expenditures, our estimates regarding our capital requirements, and our need for future capital; our liquidity and working capital requirements; the risks of not closing the acquisition of VEN 309 from Sam Amer & Co.; our expectations regarding our revenues, expenses and other results of operations; the unpredictability of the size of the markets for, and market acceptance of, any of our products, including VEN 309; our ability to sell any approved products and the price we are able realize; our need to obtain additional funding and our ability to obtain future funding on acceptable terms; our ability to retain and hire necessary employees and to staff our operations appropriately; our ability to compete in our industry and innovation by our competitors; our ability to stay abreast of and comply with new or modified laws and regulations that currently apply or become applicable to our business; estimates and estimate methodologies used in preparing our financial statements; the future trading prices of our common stock and the impact of securities analysts’ reports on these prices; and the risks set out in our filings with the SEC, including our Annual Report on Form 10 - K. Estimates and forward - looking statements involve risks and uncertainties and are not guarantees of future performance. As a result of known and unknown risks and uncertainties, including those described above, the estimates and forward - looking statements discussed in this material might not occur and our future results and our performance might differ materially from those expressed in these forward - looking statements due to, including, but not limited to, the factors mentioned above. Estimates and forward - looking statements speak only as of the date they were made, and, except to the extent required by law, we undertake no obligation to update or to review any estimate and/or forward - looking statement because of new information, future events or other factors. Forward Looking Statements

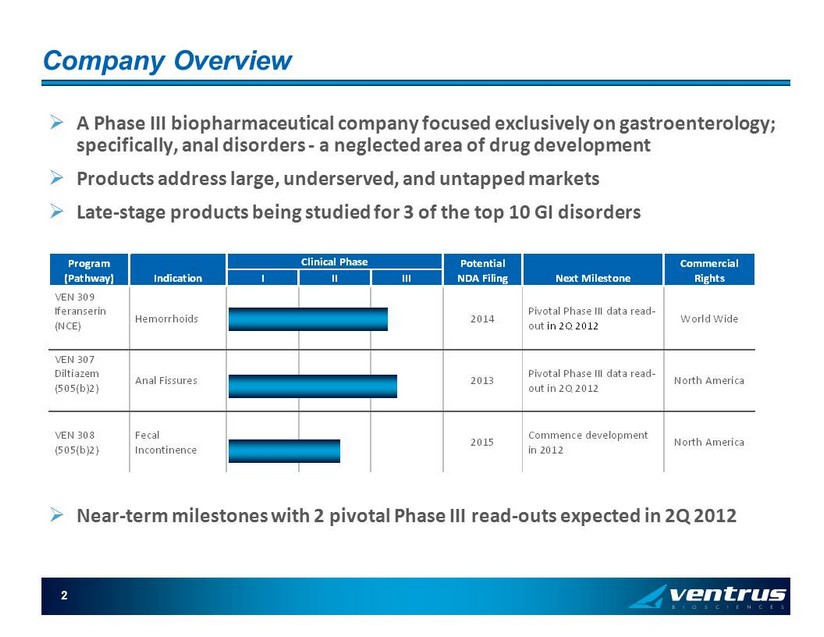

Program (Pathway) Indication Clinical Phase Potential NDA Filing Next Milestone Commercial Rights I II III VEN 309 Iferanserin (NCE) Hemorrhoids 2014 Pivotal Phase III data read- out in 2Q 2012 World Wide VEN 307 Diltiazem (505(b)2) Anal Fissures 2013 Pivotal Phase III data read- out in 2Q 2012 North America VEN 308 (505(b)2) Fecal Incontinence 2015 Commence development in 2012 North America 2 Company Overview » A Phase III biopharmaceutical company focused exclusively on gastroenterology; specifically, anal disorders - a neglected area of drug development » Products address large, underserved, and untapped markets » Late - stage products being studied for 3 of the top 10 GI disorders » Near - term milestones with 2 pivotal Phase III read - outs expected in 2Q 2012

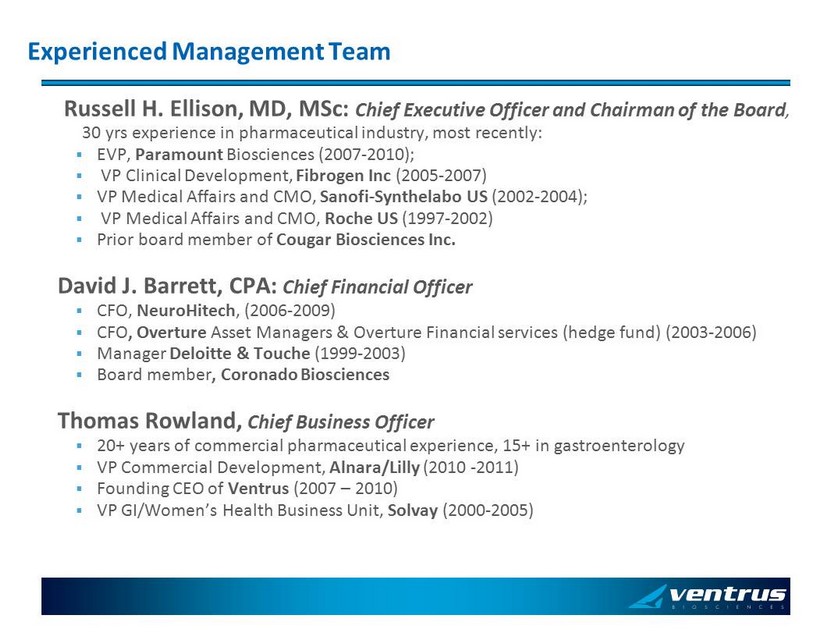

Russell H. Ellison, MD, MSc : Chief Executive Officer and Chairman of the Board , 30 yrs experience in pharmaceutical industry, most recently: ▪ EVP, Paramount Biosciences (2007 - 2010); ▪ VP Clinical Development, Fibrogen Inc (2005 - 2007) ▪ VP Medical Affairs and CMO, Sanofi - Synthelabo US (2002 - 2004); ▪ VP Medical Affairs and CMO, Roche US (1997 - 2002) ▪ Prior board member of Cougar Biosciences Inc. David J. Barrett, CPA: Chief Financial Officer ▪ CFO, NeuroHitech , (2006 - 2009) ▪ CFO , Overture Asset Managers & Overture Financial services (hedge fund) (2003 - 2006) ▪ Manager Deloitte & Touche (1999 - 2003) ▪ Board member , Coronado Biosciences Thomas Rowland, Chief Business Officer ▪ 20+ years of commercial pharmaceutical experience, 15+ in gastroenterology ▪ VP Commercial Development, Alnara/Lilly (2010 - 2011) ▪ Founding CEO of Ventrus (2007 – 2010) ▪ VP GI/Women’s Health Business Unit, Solvay (2000 - 2005) Experienced Management Team

VEN 309: Iferanserin NCE for Hemorrhoids

5 Physiology of Hemorrhoids Increased intra - pelvic pressure Dilatation of the hemorrhoidal plexus, increased pressure, swelling Local serotonin (5HT) release 5HT2a receptor activation Efferent venous constriction & platelet aggregation Internal hemorrhoid External hemorrhoid VEN 309 Primary Symptoms: Bleeding, itching & Pain

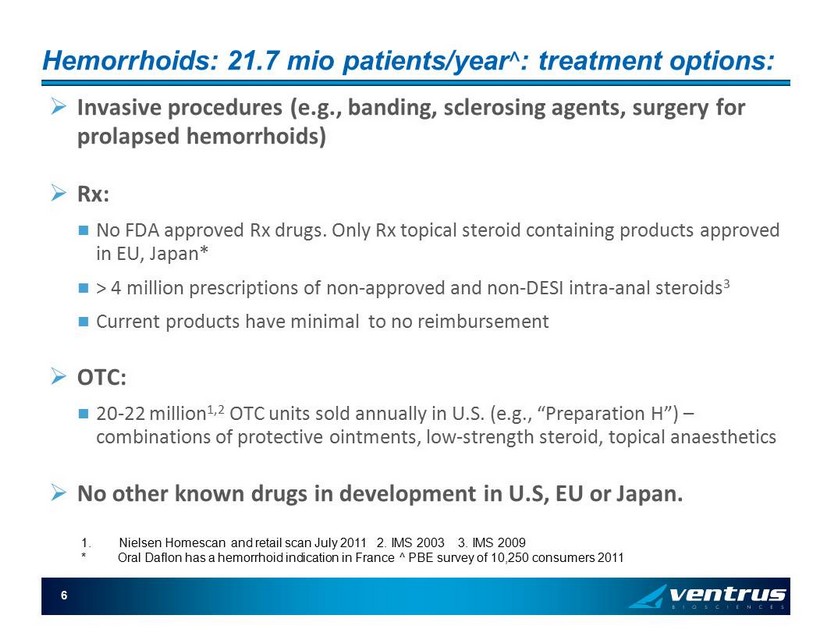

6 Hemorrhoids: 21.7 mio patients/year ^ : treatment options: » Invasive procedures (e.g., banding, sclerosing agents, surgery for prolapsed hemorrhoids) » Rx: No FDA approved Rx drugs. Only Rx topical steroid containing products approved in EU, Japan* > 4 million prescriptions of non - approved and non - DESI intra - anal steroids 3 Current products have minimal to no reimbursement » OTC: 20 - 22 million 1,2 OTC units sold annually in U.S. (e.g., “Preparation H”) – combinations of protective ointments, low - strength steroid, topical anaesthetics » No other known drugs in development in U.S, EU or Japan. 1. Nielsen Homescan and retail scan July 2011 2. IMS 2003 3. IMS 2009 * Oral Daflon has a hemorrhoid indication in France ^ PBE survey of 10,250 consumers 2011

7 Hemorrhoids: Current OTC use: In the last 52 weeks ending July 2 nd 2011 1 » 9.5 million unique households purchased 1 or more OTC hemorrhoid preps ( Representing 1 in 12 households ) » On average each purchasing household bought 1.7 units per year ▪ 30% of purchasing households bought 2 or more units per year ( ie : chronic or recurrent use); average time for repeat purchases was 2 months » 77% of purchasers were 45 years old or older ▪ 55% of all ambulatory care visits are for patients 45 years of age or older - ( ie 600 mio . visits/yr, 5 visits/person) 2 » 55% of households had income >$50,000/year A highly prevalent solution seeking population with favorable demographics 1. Nielsen Homescan July 2011 2. Schappert SM. Ambulatory medical care utilization estimates for 2007. National Center for Health Statistics. Vital Health Sta t 1 3(169). 2011.

8 VEN 309 (Iferanserin) Summary Mechanism of Action » Selective 5HT2a antagonist » Does not cross the blood brain barrier except at doses much higher than to be used therapeutically Preclinical Safety » Systemic exposure is < 10% » Therapeutic ratio is > 17x Clinical Pharmacology » Metabolized by CYP2D6 in liver (similar to Prozac) » No accumulation of the drug on twice daily dosing Clinical Data » Seven clinical trials in 359 subjects (220 exposures) » No SAEs, limited AEs (mainly GI), similar AE profile vs placebo » Significant improvements in symptoms related to hemorrhoids including bleeding, pain and itching Rights » Scheduled to acquire world-wide rights paying royalties between 1% and 4% (closing expected Nov 14 2011) Market and Data Exclusivity » Filed a new concentration range patent (August 2010) » Composition of matter expires August 2015 in the U.S. - 5 years and 10 years of data exclusivity in the U.S. and E.U. under Hatch-Waxman Act, respectively » Topical GI Product with low bioavailability Topical rectal ointment applied intra - anally BID x 2 weeks (with proprietary single - use applicator)

9 VEN 309 Clinical Data: Efficacy Phase IIb » 5 sites in Germany, conducted in 2003/2004 121 patients randomized to Iferanserin 0.5% BID vs. placebo ointment x 14 days Baseline and weekly visits for 2 week treatment; follow - up at 45 days Symptoms recorded in daily diaries (scale of 1 - 10; 1 = no symptoms) » Endpoints Primary - bleeding scale at Day 7 and Day 14; 111 evaluable patients Secondary - itching and pain scales at Day 7 and Day 14; 60 evaluable patients with itching, 40 evaluable patients with pain Other - tenderness, fullness, throbbing, gas, difficulty in defecation and physician’s assessment

10 VEN 309 Clinical Data: Efficacy Phase IIb » Primary endpoint Bleeding: rapid sustained effect Day 7 VEN 309 vs. placebo p<0.0001 Day 14 VEN 309 vs. placebo p < 0.0075 1 2 3 4 5 6 7 M e a n ( B l e e d ) 0 1 2 3 4 5 6 7 8 9 1011121314 Day VEN 309 PLACEBO Mean (Bleed) BLEEDING (n=111 patients) P < 0.05

11 1 2 3 4 5 6 7 M e a n ( P a i n ) 0 1 2 3 4 5 6 7 8 9 1011 12 13 14 Day VEN 309 Clinical Data: Efficacy Phase IIb Secondary endpoints: rapid, sustained effect 1 2 3 4 5 6 7 M e a n ( I t c h ) 0 1 2 3 4 5 6 7 8 9 1011121314 Day * = P < 0.05 * ITCHING (n=60 patients) PAIN (n=40 patients) P < 0.05 DAY 7 P < 0.0008; DAY 14 P < 0.02 * VEN 309 PLACEBO Mean (Itch) Mean (Pain)

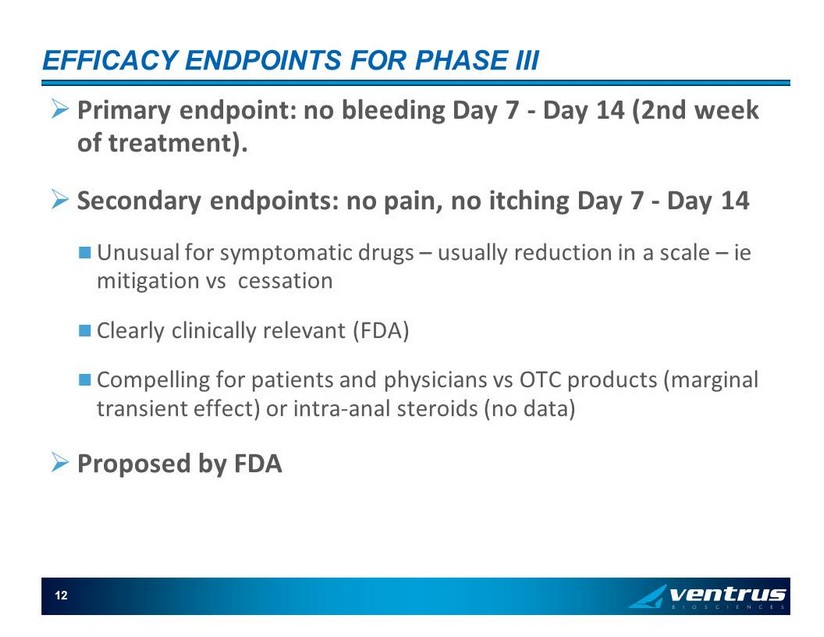

12 EFFICACY ENDPOINTS FOR PHASE III » Primary endpoint: no bleeding Day 7 - Day 14 (2nd week of treatment). » Secondary endpoints: no pain, no itching Day 7 - Day 14 Unusual for symptomatic drugs – usually reduction in a scale – ie mitigation vs cessation Clearly clinically relevant (FDA) Compelling for patients and physicians vs OTC products (marginal transient effect) or intra - anal steroids (no data) » Proposed by FDA

13 Modeling of Phase IIb Data for Phase III Endpoints * Absence of symptom Day 7 through Day 14 n = 111 with bleeding, n = 60 with itching; n = 40 with pain, at entry Majority of responders in the treatment arm respond by Day 3 *Post hoc » Secondary Endpoints Itching: 59% vs. 32% p<0.034 Pain: 50% vs. 18% p<0.032 57% 20% 0% 10% 20% 30% 40% 50% 60% Iferanserin Placebo P = ≤ 0.0001 PRIMARY ENDPOINT: No Bleeding from Day 7 to Day 14 (2nd week of Treatment) Response

14 Development Plan » Chronic repeated use product (FDA definition – may or may not be the case in Japan and EU) » 1,500 subjects needed for complete safety profile (US and possibly EU) » Two pivotal Phase III trials (and one double blind Phase III recurrence trial to determine safety/efficacy and treatment for recurrence for the US) » Clinical pharmacology program including: DDI, PK in poor metabolizers, QT and special populations (to start Q4 2011) » Preclinical: 2 species 6 & 9 mo. Chronic tox Carcinogenicity studies in two species exposed for 104 weeks and dose ranging study and chronic tox in rats and dogs (only for FDA?) Carcinogenicity is critical path for NDA , clinical trials can be done serially without losing time » Potential FDA approval 2015 (if no carc required, ROW 2014)

VEN309 (Iferanserin) for the Treatment of Hemorrhoids » Ongoing Phase III trial: iferanserin 0.5% ointment b.i.d. Design 3 arms, 200 patients per arm (placebo, 14 day treatment, 7 day treatment), total 600 patients, 70 sites 2 week treatment followed by 2 week observation, double - blind 1 year open - label extension (treatment for recurrence of symptoms) Primary endpoint, cessation of bleeding day 7 – 14; secondary endpoints, cessation of pain, itching day 7 - 14. Endpoints collected daily using Integrated Voice Response System (IVRS) Patients need 2 consecutive days of bleeding and either pain or itching at randomization: meaningful symptoms to get meaningful improvement Due to 1 year open - label extension Colonoscopy required pre - randomization if > 3 yrs ago No DDI data re CYP2D6: exclude history of and current depression, SSRI’s Exclude history of heart disease, BMI > 36, other chronic diseases Discussion with FDA on all major elements of the protocol Progress Initiated early August with 65 sites; currently all 70 sites screening Enrolling correct patients, minimal loss of key outcome data on IVRS, continuous data review Large number of patients entering screening as expected 15

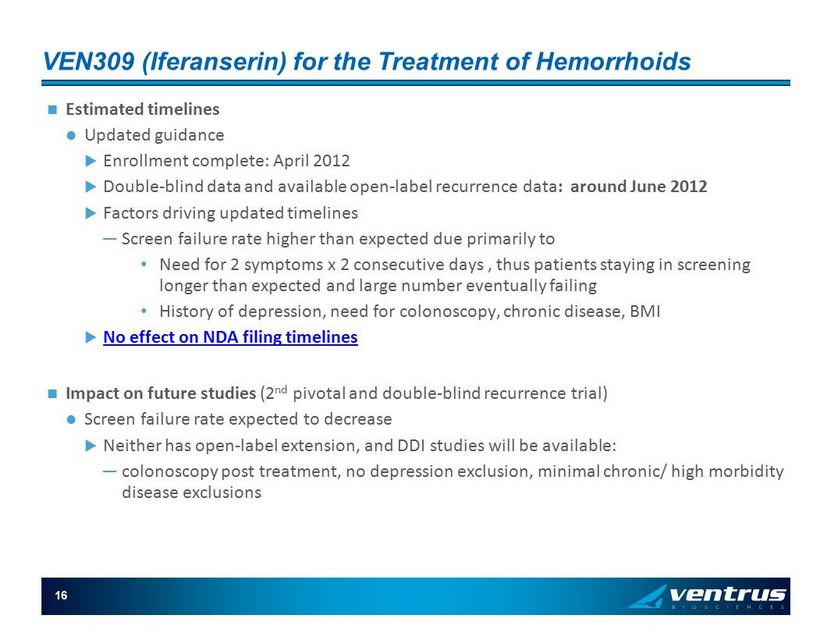

VEN309 (Iferanserin) for the Treatment of Hemorrhoids Estimated timelines Updated guidance Enrollment complete: April 2012 Double - blind data and available open - label recurrence data : around June 2012 Factors driving updated timelines ─ Screen failure rate higher than expected due primarily to • Need for 2 symptoms x 2 consecutive days , thus patients staying in screening longer than expected and large number eventually failing • History of depression, need for colonoscopy, chronic disease, BMI No effect on NDA filing timelines Impact on future studies (2 nd pivotal and double - blind recurrence trial) Screen failure rate expected to decrease Neither has open - label extension, and DDI studies will be available: ─ colonoscopy post treatment, no depression exclusion, minimal chronic/ high morbidity disease exclusions 16

17 VEN309 ( Iferanserin) for the Treatment of Hemorrhoids » Pharmacology program: CYP2D6 metabolism Iferanserin is dependant on CYP2D6 for metabolism and inhibits CYP2D6 in the liver (Prozac) Advantage: GI topical drug with low systemic exposure Program designed to generate following data Poor metabolizers (missing genes): safety and exposure, needed for QT study One poor metabolizer (2 genes missing) in Ph I had no adverse events Drug interaction with CYP2D6 dependant/inhibiting drugs (Cymbalta [duloxetine], dextromethorphan) Data anticipated Q2 2012 (wihen pivotal trial data expected) Allow less restrictions in exclusion criteria for the next studies Provide high dose arm for QT study De - risk safety profile

18 Hemorrhoid Rx Commercial Potential: Study » Ventrus commissioned an omnibus survey and predictive modeling market research in September 2011 of 800 physicians and 1,125 hemorrhoid patients Physician project is beginning the analysis stage Consumer project is in analysis stage and initial results are available » Study Approach Each respondent sees only one profile PBE factors (discounts) the self - stated survey responses regarding VEN 309 adoption to accurately reflect real world behavior, based on extensively validated in - market models » Princeton Brand Econometrics Founded in 1991 and has worked for 9 of the top 10 pharmaceutical companies Chosen based on their track record of accurately predicting physician and consumer behavior given a range of product profiles and promotional levels Mean absolute percentage error over 31 validated forecasts is 2.68%

Study Results » 10,202 adult consumers were screened (designed to match US demographics) » 1,125 (11%) consumers reported suffering from hemorrhoids within the last two years…ie : hemorrhoid patients 2010 US Adult population – 234,564,000 (2010 US census) » Period prevalence: 2 years: 11% - 25.8 million 1 year: 9.3% - 21.7 million 1 month: 6.0% - 14.0 million Day of survey: 2.9% - 6.7 million » Treatments 15% reported never using OTC or Rx treatment Of those treating, 86% reported using an OTC preparation or 14% Rx as their last treatment 10% of all patients reported having an invasive procedure (61% surgery) with 75% reporting recurrence of symptoms after surgery 19

20 Patient response to VEN 309 DTC/PR concept » Strong willingness to ask their doctor for VEN 309 at the next visit In the whole sample: (complete range of current satisfaction, severity frequency of hemorrhoids, time of last episode, and income): 75% stated* that they would request a prescription at the next visit 25% would actually request a prescription (75% factored by PBE algorithm) 66% receiving a prescription would fill the Rx at a $35 patient out - of - pocket co - pay^ 78% with household income above $50k/year would fill the Rx at a $35 copay^ For patients who are having symptoms now , (estimated at 6.7 mm) 88% stated* they would request a prescription and 80% would actually request it (PBE factored) *Stated includes “Definitely, Probably and Might” ^ PBE factored

VEN 307: Diltiazem Cream Novel Treatment for Anal Fissures

22 Anal Fissures: Cause and Management Increased sphincter tone Local ischemia Tear (fissure) in anal canal Cause Severe pain on defecation Treatment options Control constipation, topical steroids Reduce sphincter tone Topical drugs: • GTN • diltiazem Botox Surgery Sphincters (muscles) Anal fissure 1.1 mio office vists /year Anal fistula

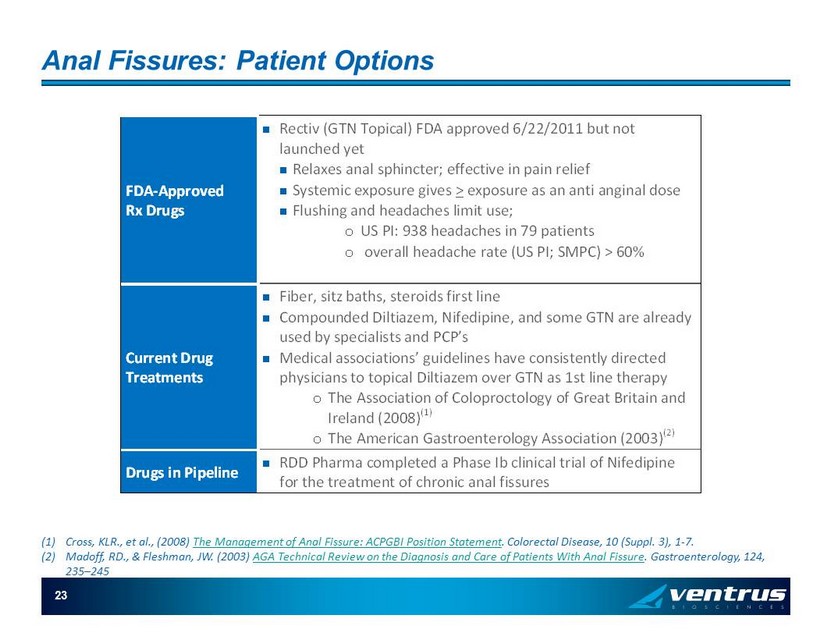

23 Anal Fissures: Patient Options FDA-Approved Rx Drugs Rectiv (GTN Topical) FDA approved 6/22/2011 but not launched yet Relaxes anal sphincter; effective in pain relief Systemic exposure gives > exposure as an anti anginal dose Flushing and headaches limit use; o US PI: 938 headaches in 79 patients o overall headache rate (US PI; SMPC) > 60% Current Drug Treatments Fiber, sitz baths, steroids first line Compounded Diltiazem, Nifedipine, and some GTN are already used by specialists and PCP’s Medical associations’ guidelines have consistently directed physicians to topical Diltiazem over GTN as 1st line therapy o The Association of Coloproctology of Great Britain and Ireland (2008) (1) o The American Gastroenterology Association (2003) (2) Drugs in Pipeline RDD Pharma completed a Phase Ib clinical trial of Nifedipine for the treatment of chronic anal fissures (1) Cross, KLR., et al., (2008) The Management of Anal Fissure: ACPGBI Position Statement . Colorectal Disease, 10 (Suppl. 3), 1 - 7. (2) Madoff, RD., & Fleshman, JW. (2003) AGA Technical Review on the Diagnosis and Care of Patients With Anal Fissure . Gastroenterology, 124, 235 – 245

24 VEN 307 (Diltiazem) Summary Mechanism of Action » Calcium channel blocker Relaxes the internal anal sphincter, reducing pain and increasing tissue blood flow Preclinical Safety » Preclinical topical safety with 2% Diltiazem twice daily for ninety days Clinical Pharmacology » Topical has < 10% systemic exposure as oral dose but significantly greater effect on sphincter tone – i.e., blood levels do not predict activity. Low exposure = better tolerability than oral Diltiazem Clinical Data » Ten clinical trials in 453 individuals » Infrequent mild AEs reported » Similar or better reduction in pain, significantly better tolerability than GTN Rights » North American rights paying mid to upper single digit royalties Market and Data Exclusivity » Method of use patent expires Feb 2018 » Topical GI product; systemic levels do not predict efficacy and will not guarantee generic drug approval » Extended Release formulations (b.i.d.) under development to extend exclusivity 2% Topical Diltiazem cream applied peri - anally TID

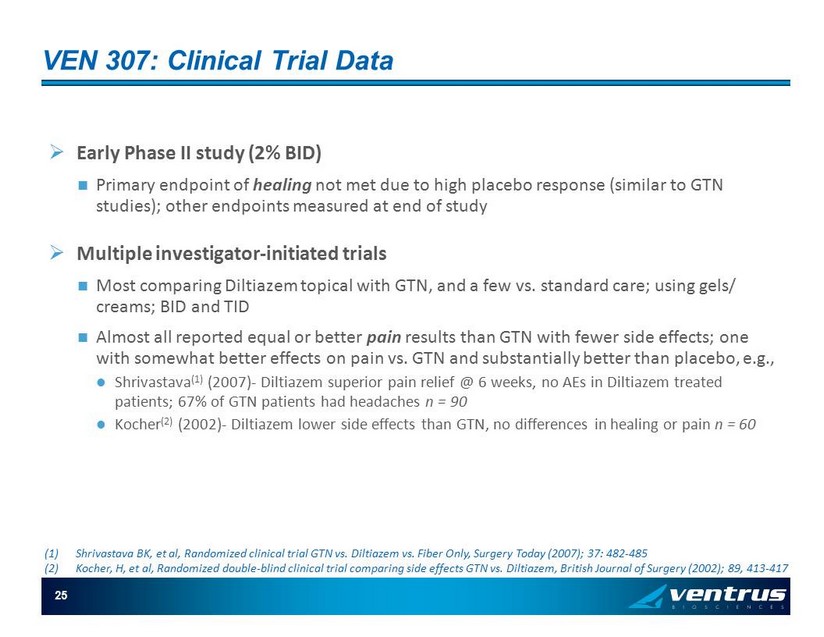

25 VEN 307: Clinical Trial Data » Early Phase II study (2% BID) Primary endpoint of healing not met due to high placebo response (similar to GTN studies); other endpoints measured at end of study » Multiple investigator - initiated trials Most comparing Diltiazem topical with GTN, and a few vs. standard care; using gels/ creams; BID and TID Almost all reported equal or better pain results than GTN with fewer side effects; one with somewhat better effects on pain vs. GTN and substantially better than placebo, e.g., Shrivastava (1) (2007) - Diltiazem superior pain relief @ 6 weeks, no AEs in Diltiazem treated patients; 67% of GTN patients had headaches n = 90 Kocher (2) (2002) - Diltiazem lower side effects than GTN, no differences in healing or pain n = 60 (1) Shrivastava BK, et al, Randomized clinical trial GTN vs. Diltiazem vs. Fiber Only, Surgery Today (2007); 37: 482 - 485 (2) Kocher, H, et al, Randomized double - blind clinical trial comparing side effects GTN vs. Diltiazem, British Journal of Surgery (2 002); 89, 413 - 417

26 VEN 307: First Pivotal Phase III Trial Initiated » FDA (analgesia division) pre - IND meeting conducted in August 2007 Confirmed Phase III multi - dose plan; 505b(2) status Achieved clarity on primary endpoint: reduction in pain Confirmed safety database and tox requirement » Phase III trial initiated (November 2010) with data anticipated around May 2012 Licensor (SLA) is conducting trial 465 patients in 30 sites in Europe; initiated in November 2010 Treated for 2 months: randomized 1:1:1 double blind; fiber plus 2%, 4% VEN 307, and placebo; primary endpoint at 1 month NRS scale, daily diaries 1 week observation to ensure sufficient pain prior to randomization Primary endpoint: reduction in pain on defecation using a validated scale (Likert, NRS) Ventrus did detailed review of blinded data and study operations 10/2011: Correct patients enrolled, IVRS compliance is good, data are being reviewed continuously » Planned Second Phase III trial(s): We intend to conduct enabling toxicity Developing 4 possible extended release formulations: may test some or all in human manometry trial in 2012 Could be 2 trials with extended release formulation if one is acceptable, or 1 with original formulation

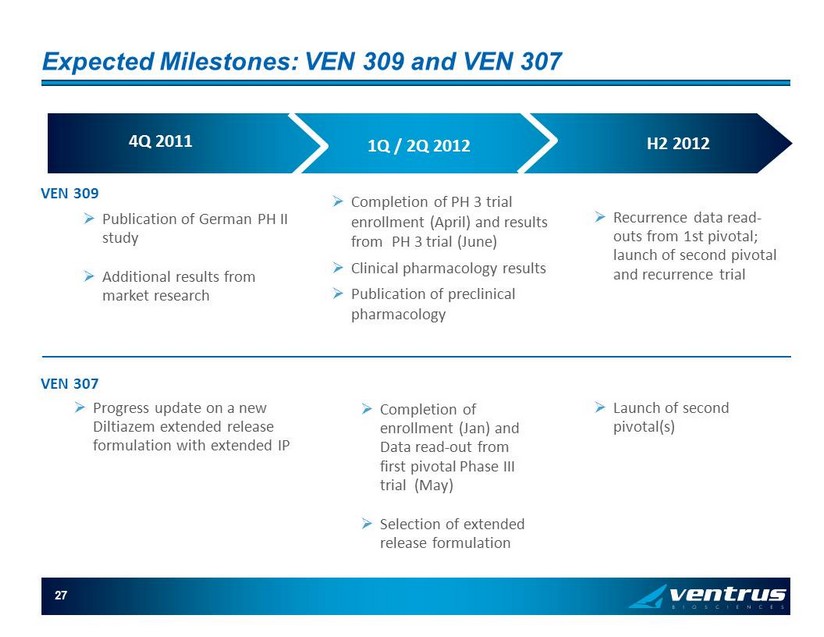

27 Expected Milestones: VEN 309 and VEN 307 4Q 2011 1Q / 2Q 2012 H2 2012 » Publication of German PH II study » Additional results from market research » Completion of PH 3 trial enrollment (April) and results from PH 3 trial (June) » Clinical pharmacology results » Publication of preclinical pharmacology » Recurrence data read - outs from 1st pivotal; launch of second pivotal and recurrence trial VEN 309 VEN 307 » Progress update on a new Diltiazem extended release formulation with extended IP » Completion of enrollment (Jan) and Data read - out from first pivotal Phase III trial (May) » Selection of extended release formulation » Launch of second pivotal(s)

Corporate Overview

After data readouts expected in 2Q 2012: » Strategic options In 2012, 5 - 6 major pharma companies with primary care and/or GI products and field forces Four with an OTC division 2 - 3 GI specialty companies » Partnerships We intend to seek a marketing partner for VEN 309 for ex - U.S. territories (EU, Asia) Co - promotion opportunities exist for broader PCP coverage of VEN 309 and VEN 307 in US » Estimated continued development of products by Ventrus : VEN 309 US filing 2H 2014 approval possible 2015; may be earlier in EU, and/or Japan (PH I and II done in Japan) VEN 307 diltiazem cream filing 2H 2013; approval possible 2014 (later if extended release) Future Scenarios: VEN 309 and VEN 307

30 Possible Commercialization Strategy » Specialty sales force can be highly effective Diltiazem is the established gold - standard treatment for anal fissures among GIs and the launch of Rectiv will allow cost effective targeting of prescribers, with the AE advantage of VEN 307 and already established preference Highly selective specialty sales force targeting of prescribers of the 4 million prescriptions of steroids for hemorrhoids (using IMS data), to convert these to VEN 309 No data to support the use of intra anal steroids as effective treatment; not approved Yearly DTC campaign (cost efficient with this indication) » Co - promotion possibilities with existing primary care field forces for broad coverage » Pricing and Reimbursement VEN 309: No other drugs in class or indication: Medicare Part D and managed care implications (anticipate blended 2 nd tier/3 rd tier formulary ) VEN 307: Anticipate 2 nd tier/3 rd tier formulary. Anticipate Medicare part D (side effect difference vs GTN). The nature of the markets we target provide Ventrus with the option of US commercialization

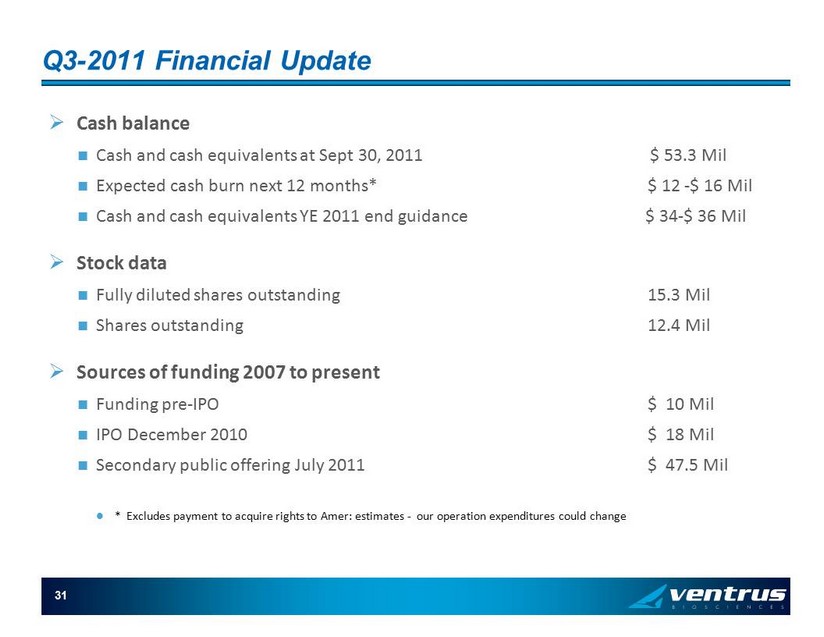

31 Q3 - 2011 Financial Update » Cash balance Cash and cash equivalents at Sept 30, 2011 $ 53.3 Mil Expected cash burn next 12 months* $ 12 - $ 16 Mil Cash and cash equivalents YE 2011 end guidance $ 34 - $ 36 Mil » Stock data Fully diluted shares outstanding 15.3 Mil Shares outstanding 12.4 Mil » Sources of funding 2007 to present Funding pre - IPO $ 10 Mil IPO December 2010 $ 18 Mil Secondary public offering July 2011 $ 47.5 Mil * Excludes payment to acquire rights to Amer: estimates - our operation expenditures could change

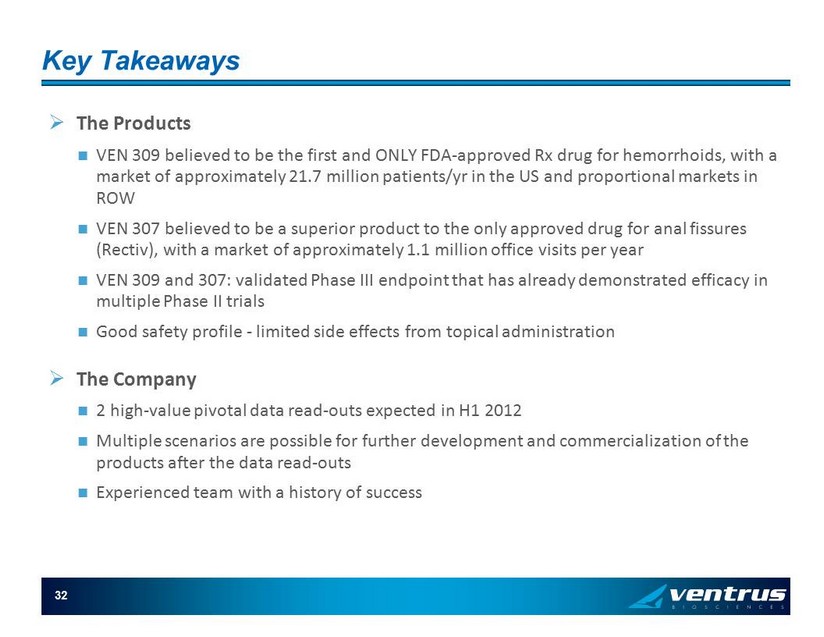

32 Key Takeaways » The Products VEN 309 believed to be the first and ONLY FDA - approved Rx drug for hemorrhoids , with a market of approximately 21.7 million patients/yr in the US and proportional markets in ROW VEN 307 believed to be a superior product to the only approved drug for anal fissures ( Rectiv ), with a market of approximately 1.1 million office visits per year VEN 309 and 307: validated Phase III endpoint that has already demonstrated efficacy in multiple Phase II trials Good safety profile - limited side effects from topical administration » The Company 2 high - value pivotal data read - outs expected in H1 2012 Multiple scenarios are possible for further development and commercialization of the products after the data read - outs Experienced team with a history of success