Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - SUNOCO INC | d249878d8k.htm |

| EX-99.1 - PRESS RELEASE - SUNOCO INC | d249878dex991.htm |

3Q11 Earnings Conference Call

November 3, 2011

Exhibit 99.2 |

2

This

slide

presentation

should

be

reviewed

in

conjunction

with

Sunoco’s

Third

Quarter

2011

earnings

conference

call

held

on

November

3,

2011

at

4:30

p.m.

ET.

You

may

listen

to

the

audio

portion

of

the

conference

call

on

the

website

or

an

audio

recording

will

be

available

after

the

call’s

completion

by

calling

1-866-465-1304

and

entering

conference

ID

#8748773.

Statements

in

this

presentation

that

are

not

historical

facts

are

forward-looking

statements

intended

to

be

covered

by

the

safe

harbor

provisions

of

Section

27A

of

the

Securities

Act

of

1933

and

Section

21E

of

the

Securities

Exchange

Act

of

1934.

These

forward-looking

statements

are

based

upon

assumptions

by

Sunoco

concerning

future

conditions,

any

or

all

of

which

ultimately

may

prove

to

be

inaccurate,

and

upon

the

current

knowledge,

beliefs

and

expectations

of

Sunoco

management.

These

forward-looking

statements

are

not

guarantees

of

future

performance.

Forward-looking

statements

are

inherently

uncertain

and

involve

significant

risks

and

uncertainties

that

could

cause

actual

results

to

differ

materially

from

those

described

during

this

presentation.

Such

risks

and

uncertainties

include

economic,

business,

competitive

and/or

regulatory

factors

affecting

Sunoco's

business,

as

well

as

uncertainties

related

to

the

outcomes

of

pending

or

future

litigation.

In

accordance

with

the

safe

harbor

provisions

of

the

Private

Securities

Litigation

Reform

Act

of

1995,

Sunoco

has

included

in

its

Annual

Report

on

Form

10-K

for

the

year

ended

December

31,

2010,

and

in

its

subsequent

Form

10-Q

and

Form

8-K

filings,

cautionary

language

identifying

important

factors

(though

not

necessarily

all

such

factors)

that

could

cause

future

outcomes

to

differ

materially

from

those

set

forth

in

the

forward-looking

statements.

For

more

information

concerning

these

factors,

see

Sunoco's

Securities

and

Exchange

Commission

filings,

available

on

Sunoco's

website

at

www.SunocoInc.com.

Sunoco

expressly

disclaims

any

obligation

to

update

or

alter

its

forward-looking

statements,

whether

as

a

result

of

new

information,

future

events

or

otherwise.

This

presentation

includes

certain

non-GAAP

financial

measures

intended

to

supplement,

not

substitute

for,

comparable

GAAP

measures.

Reconciliations

of

non-GAAP

financial

measures

to

GAAP

financial

measures

are

provided

in

the

Appendix

at

the

end

of

the

presentation.

Investors

are

urged

to

consider

carefully

the

comparable

GAAP

measures

and

the

reconciliations

to

those

measures

provided

in

the

Appendix,

or

on

our

website

at

www.SunocoInc.com.

Safe Harbor Statement |

3

After-tax income before special items of $65MM* ($0.57/share diluted),

pretax

income of $57MM*

Strong performance from Logistics and Retail

Refining & Supply (R&S) reported a pretax loss of $17MM

Continue to deliver value to shareholders and position the Company for future

success

Completed $500 MM share repurchase program

Completed IPO of SunCoke in July

Pursuing growth in logistics and retail businesses

Completed exit from underperforming chemicals business

Pursuing sale of northeast refineries and plan to exit business by July

2012

Performing comprehensive strategic review

* For reconciliation to Net Income (Loss), see Slide 12. Special

Items in 3Q11 include a net

loss of $1,161MM after-tax.

Summary of 3

rd

Quarter 2011 Performance |

4

Retail Marketing –

Pretax Earnings of $48MM

Average gasoline margins of 10.5 cpg in 3Q11

Higher volumes driven by growth; same store sales down ~2.9%, consistent with

EIA data

Logistics –

Pretax Earnings of $53MM

Record

quarterly

earnings

for

Sunoco

Logistics

Partners

for

the

2

nd

straight

quarter

driven

by

market

opportunities

in

the

crude

oil

segment,

as

well

as

contribution from recent acquisitions

SXL also had record acquisition growth in 2011 of almost $500 MM

Coke –

Pretax Earnings of $24MM

Improved operational performance/record domestic coke production

Successful Middletown plant start-up

Purchase of GE’s stake in Indiana Harbor

R&S –

Pretax Loss of $17MM

July and August profitable

Strong operational performance with 3Q crude utilization ~90%

September market margins deteriorated, averaging ~$2/B

* Pretax Business Unit Income (Loss) Before Special Items, excluding Income

Attributable to Noncontrolling Interests. For reconciliation to Net Income

(Loss), see Slide 12. Segment Pretax Results* -

3Q11 |

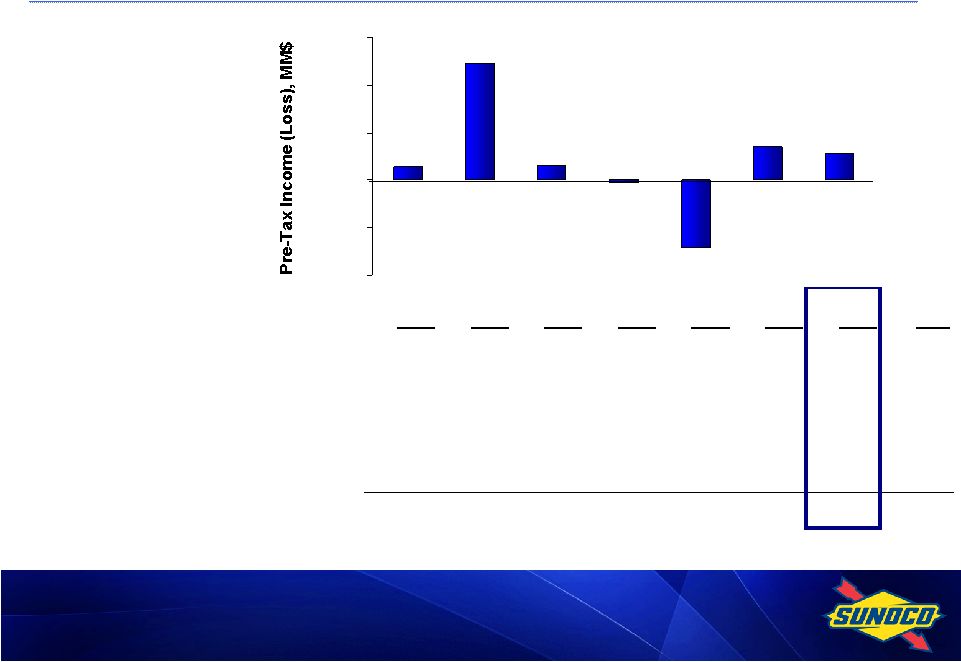

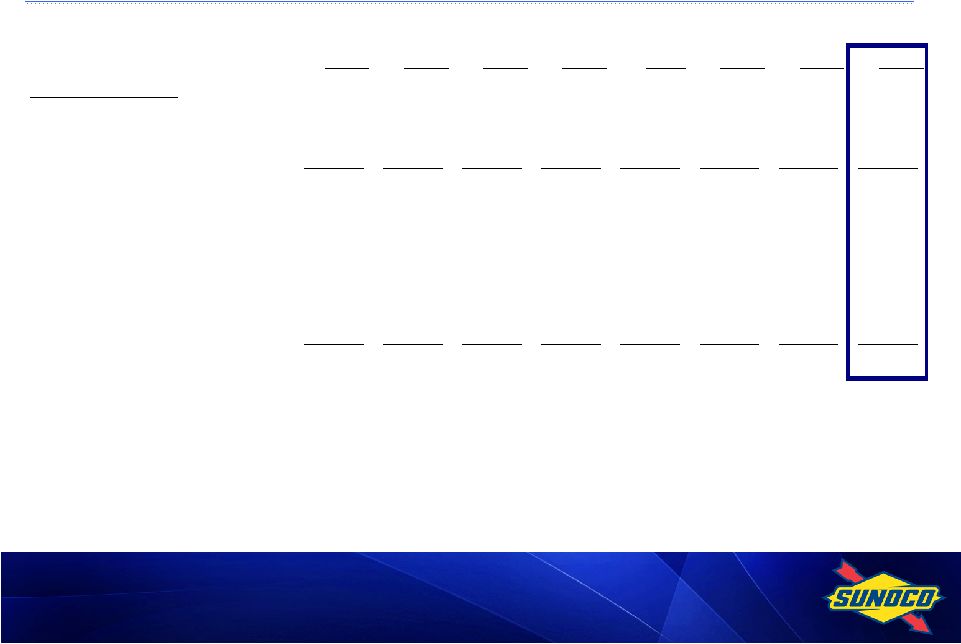

5

YTD

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

2011

Refining & Supply

(70)

138

(70)

(17)

(138)

(44)

(17)

(199)

Retail Marketing

34

73

68

1

12

69

48

129

Logistics

27

30

40

35

31

54

53

138

Coke

51

56

44

25

9

20

24

53

Discontinued Chemicals Operations

38

7

5

6

(9)

6

1

(2)

Corporate Expenses

(23)

(30)

(28)

(27)

(22)

(18)

(23)

(63)

Net Financing Expenses & Other

(28)

(27)

(28)

(27)

(24)

(16)

(29)

(69)

Pretax Income (Loss) Before Special Items

29

247

31

(4)

(141)

71

57

(13)

Pretax Income (Loss) Before Special Items*, MM$

57

71

(141)

(4)

31

247

29

($200)

($100)

$0

$100

$200

$300

* For reconciliation to Net Income (Loss), see Slide 12.

|

6

1Q10

2Q10

3Q10

4Q10

FY10

1Q11

2Q11

3Q11

Refining & Supply

Realized Margin

4.08

7.34

3.88

4.77

5.04

3.14

4.31

4.89

Benchmark*

4.93

6.12

4.22

5.19

5.11

5.19

6.11

5.87

Differential

(0.85)

1.22

(0.34)

(0.42)

(0.07)

(2.05)

(1.80)

(0.98)

Margin Capture Rate

83%

120%

92%

92%

99%

61%

71%

83%

Actual vs. Benchmark:

Crude

(0.52)

0.73

(0.52)

(0.25)

(0.09)

(1.08)

(0.51)

(0.20)

Product

(0.33)

0.49

0.18

(0.17)

0.02

(0.97)

(1.29)

(0.78)

Differential

(0.85)

1.22

(0.34)

(0.42)

(0.07)

(2.05)

(1.80)

(0.98)

* For calculation, see Slide 21. Weighted benchmark in effect in 2010 and through

March 1, 2011. Realized R&S Margin vs. Benchmark, $/B

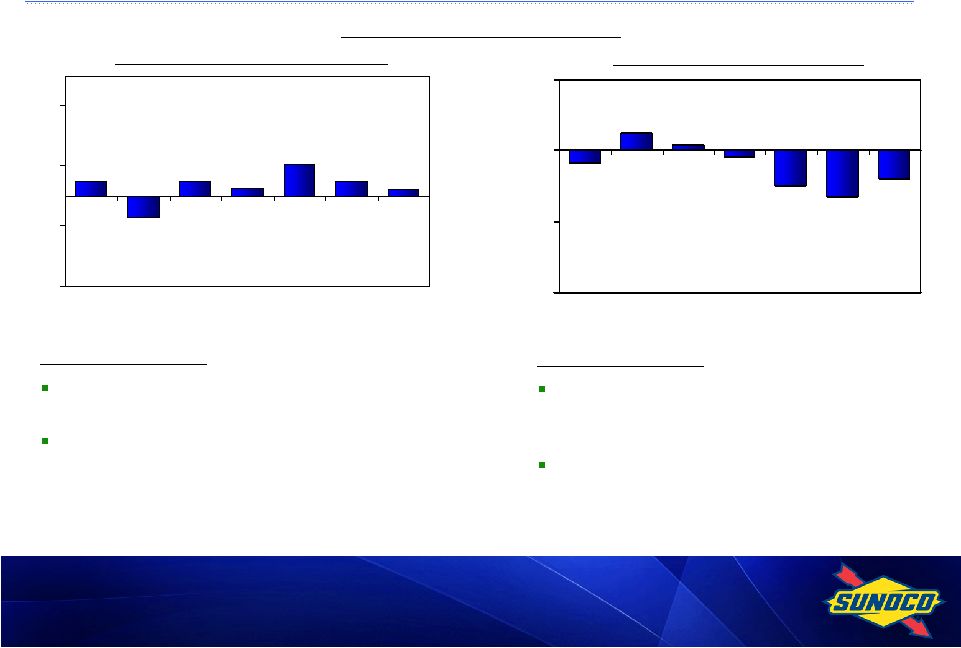

|

7

0.20

0.51

0.25

1.08

0.52

(0.73)

0.52

-3.00

-1.00

1.00

3.00

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

Crude Cost vs. Benchmark

(0.78)

(1.29)

(0.97)

(0.17)

0.18

0.49

(0.33)

-4.00

-2.00

0.00

2.00

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

Products vs. Benchmark

Total Refining & Supply

3Q11 Comments:

Quality differentials benefited from higher

volume of discounted crude purchases

Overall purchase volumes dropped in

September due to rate cuts, minimizing benefit

from falling prices

3Q11 Comments:

Vs 3Q 10, produced fuel net of yield gain

worse by over $1/B due to ~$35/B higher

absolute prices and lower yield volume gains

Propane and other non-crack margins lower

by ~.40/B vs

3Q 10 due to higher crude

prices

Realized R&S Margin vs. Benchmark*, $/B

* For calculation, see Slide 21. Weighted benchmark in effect in 2010 and through

March 1, 2011. |

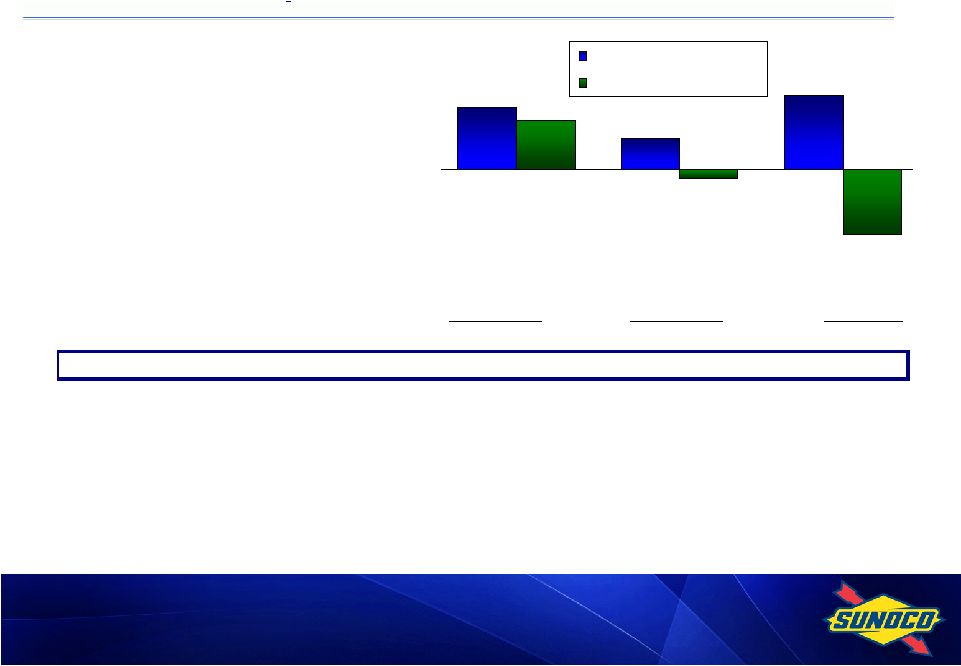

8

12/31/09

12/31/10

9/30/11

Sunoco (ex-SXL/SXC)*

32%

-6%

-43%

Sunoco (Consolidated)*

41%

20%

48%

Sunoco Net Debt/(Cash)

1,223

(182)

(389)

SXL Net Debt**

866

1,227

1,790

SXC Net Debt

N/A

N/A

587

Consolidated Net Debt, MM$

2,089

945

1,888

Total Cash, MM$***

375

1,483

1,537

* Sunoco Revolver Covenant basis. For calculation, see Slide 17.

** Includes intercompany loan due to Sunoco from SXL at 12/31/2010 and 9/30/2011

which is eliminated in consolidation.

*** Excludes cash on balance sheet of Sunoco Logistics Partners for all periods and

SunCoke Energy as of 9/30/11. Net Debt-to-Capital Ratio, %

41%

20%

48%

32%

-6%

-43%

Sunoco (Consolidated)*

Sunoco (ex-SXL/SXC)* |

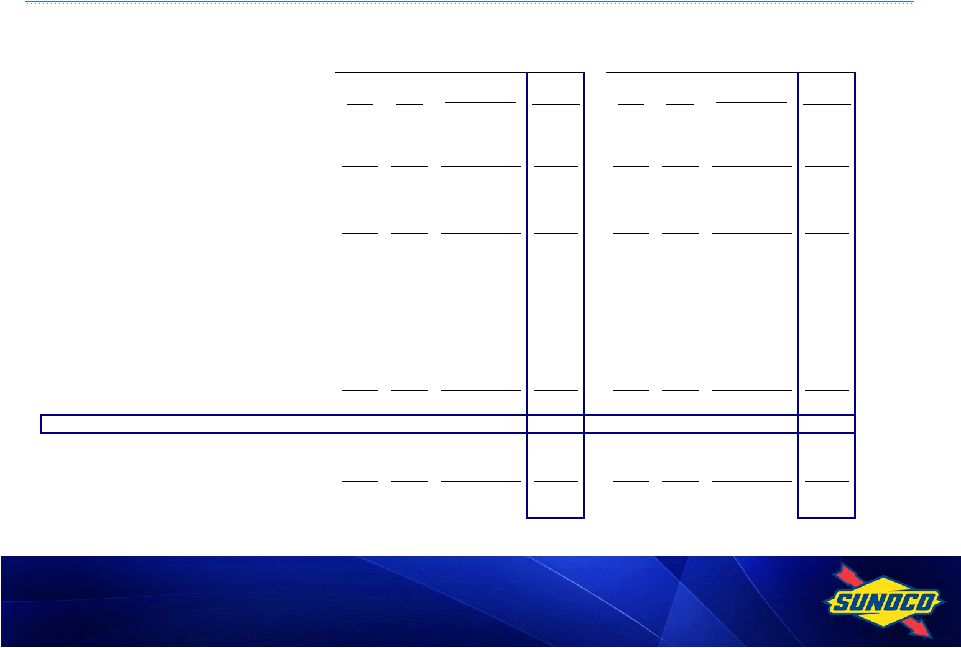

9

Cash Flow Split, MM$

SUN

SUN

SXL

SXC

(ex SXL/SXC)

Sunoco

SXL

SXC

(ex SXL/SXC)

Sunoco

Cash from ops excluding working capital

114

46

160

320

300

124

63

487

Working capital including interco activity

(40)

(3)

(358)

(401)

(183)

(60)

(682)

(925)

Cash flow from operations

74

43

(198)

(81)

117

64

(619)

(438)

Capital expenditures

(350)

(56)

(70)

(476)

(518)

(222)

(194)

(934)

Free cash flow

(276)

(13)

(268)

(557)

(401)

(158)

(813)

(1,372)

Divestments and other

-

-

113

113

-

-

955

955

Dividends to Sunoco shareholders

-

-

(19)

(19)

-

-

(55)

(55)

Distributions & other

(27)

(34)

2

(59)

(83)

(35)

5

(113)

Repurchase of common stock

-

-

(500)

(500)

-

-

(500)

(500)

SunCoke IPO /debt exchange

-

-

192

192

-

-

192

192

SXL distributions to Sunoco

(25)

-

25

-

(73)

-

73

-

Net cash flow before net debt activity

(328)

(47)

(455)

(830)

(557)

(193)

(143)

(893)

Intercompany debt activity*

-

(551)

551

-

-

(413)

413

-

Net debt activity, 3rd party

330

680

-

1,010

563

677

(176)

1,064

Net increase in cash & cash equivalents

2

82

96

180

6

71

94

171

YTD11

3Q11

*

Includes $575 MM paid to Sunoco from SunCoke with proceeds from debt issuance as repayment of

intercompany debt payable; the remaining balance represents a capital contribution from

Sunoco to SunCoke. |

10

Remain focused on delivering value to shareholders

Strong results in retail and logistics

Completed $500MM share repurchase program

SunCoke IPO

Comprehensive strategic review

Positioning for future success

Growth through SXL ($500 million in acquisitions in 2011) and Retail (Central

PA, Ohio turnpike)

Divestment of non-core assets (e.g., Frankford, Haverhill)

Exit refining

Balance sheet: Cash balance provides strategic flexibility

Key Takeaways/Path Forward |

Appendix |

12

Earnings Profile, MM$

YTD

1Q10

2Q10

3Q10

4Q10

FY10

1Q11

2Q11

3Q11

2011

Refining & Supply

(70)

138

(70)

(17)

(19)

(138)

(44)

(17)

(199)

Retail Marketing

34

73

68

1

176

12

69

48

129

Logistics

27

30

40

35

132

31

54

53

138

Coke

51

56

44

25

176

9

20

24

53

Discontinued Chemicals Operations

38

7

5

6

56

(9)

6

1

(2)

Corporate and Other:

Corporate Expenses

(23)

(30)

(28)

(27)

(108)

(22)

(18)

(23)

(63)

Net Financing Expenses & Other

(28)

(27)

(28)

(27)

(110)

(24)

(16)

(29)

(69)

Pretax Income (Loss) attributable to Sunoco, Inc.

shareholders before special items

29

247

31

(4)

303

(141)

71

57

(13)

Income Tax Expense (Benefit) attributable to

Sunoco, Inc. shareholders

12

89

4

(17)

88

(19)

22

(8)

(5)

Income (Loss) attributable to Sunoco, Inc.

shareholders before special items

17

158

27

13

215

(122)

49

65

(8)

Special Items:

Continuing Operations*

(45)

(22)

62

123

118

51

(7)

(1,966)

(1,922)

Discontinued Operations**

(169)

-

-

-

(169)

-

(287)

32

(255)

Pretax Income (Loss) from special items

(214)

(22)

62

123

(51)

51

(294)

(1,934)

(2,177)

Income Tax Expense (Benefit)

(134)

(9)

24

49

(70)

30

(120)

(773)

(863)

Income (Loss) from special items

(80)

(13)

38

74

19

21

(174)

(1,161)

(1,314)

Net Income (Loss) attributable to

Sunoco, Inc. shareholders

(63)

145

65

87

234

(101)

(125)

(1,096)

(1,322)

* In 3Q 2011, recorded a $1,959MM noncash provision to write down assets at the

Philadelphia and Marcus Hook refineries to their

estimated

fair

values

in

connection

with

decision

to

exit

refining

business.

** In 1Q 2010 and 2Q 2011, recognized losses in connection with the divestment of

the chemicals business; In 3Q 2011, recognized a $14MM

gain on the divestment of the Frankford chemical facility and an $18 million gain attributable to a

settlement

connected

to

the

Tulsa

refining

operation

which

was

sold

in

2009. |

13

Earnings Summary and EPS

YTD

MM$

1Q10

2Q10

3Q10

4Q10

FY10

1Q11

2Q11

3Q11

2011

Income (Loss) attributable to Sunoco, Inc.

shareholders before special items

17

158

27

13

215

(122)

49

65

(8)

Special Items:

Continuing Operations*

(45)

(22)

62

123

118

51

(7)

(1,966)

(1,922)

Discontinued Operations**

(169)

-

-

-

(169)

-

(287)

32

(255)

Pretax Income (Loss) from special items

(214)

(22)

62

123

(51)

51

(294)

(1,934)

(2,177)

Income Tax Expense (Benefit)

(134)

(9)

24

49

(70)

30

(120)

(773)

(863)

Income (Loss) from special items

(80)

(13)

38

74

19

21

(174)

(1,161)

(1,314)

Net Income (Loss) attributable to

Sunoco, Inc. shareholders

(63)

145

65

87

234

(101)

(125)

(1,096)

(1,322)

$/Share (diluted)

Earnings (Loss) per share of common stock (diluted):

Income (Loss) attributable to Sunoco, Inc.

shareholders before special items

0.14

1.31

0.22

0.11

1.79

(1.01)

0.40

0.57

(0.07)

Income (Loss) from special items

(0.67)

(0.11)

0.32

0.61

0.16

0.17

(1.43)

(10.19)

(11.08)

Net Income (Loss) attributable to

Sunoco, Inc. shareholders

(0.53)

1.20

0.54

0.72

1.95

(0.84)

(1.03)

(9.62)

(11.15)

* In 3Q 2011, recorded a $1,959MM noncash provision to write down assets at the

Philadelphia and Marcus Hook refineries to their estimated fair values in

connection with decision to exit refining business.

** In 1Q 2010 and 2Q 2011, recognized losses in connection with the divestment of

the chemicals business; In 3Q 2011, recognized

a

$14MM

gain

on

the

divestment

of

the

Frankford

chemical

facility

and

an

$18

million

gain

attributable

to

a

settlement

connected

to

the

Tulsa

refining

operation

which

was

sold

in

2009. |

14

YTD

1Q10

2Q10

3Q10

4Q10

FY10

1Q11

2Q11

3Q11

2011

Total Refining & Supply

Crude Throughputs, MB/D

533

618

632

572

589

460

425

453

446

% Capacity

79

92

94

85

87

74

84

90

82

Net Prod. Available for Sale, MB/D

591

664

682

634

643

512

461

487

487

Net Prod. Available for Sale, MMB

53

61

62

58

234

46

42

45

133

Key Volume Indicators –

Refining & Supply |

15

YTD

1Q10

2Q10

3Q10

4Q10

FY10

1Q11

2Q11

3Q11

2011

Realized Margin Indicators

Refining & Supply, $/B

4.08

7.34

3.88

4.77

5.04

3.14

4.31

4.89

4.10

Retail Marketing, cpg

Gasoline

8.9

11.5

10.5

6.6

9.4

6.9

12.4

10.5

10.0

Distillate

8.0

9.0

7.8

5.6

7.6

7.1

12.5

9.6

9.8

Market Indicators

Dated Brent Crude Oil, $/B

76.24

78.30

76.86

86.53

79.48

104.90

117.63

113.49

112.01

Natural Gas, $/DT

5.04

4.34

4.23

3.97

4.40

4.20

4.37

4.06

4.21

Key Indicators |

16

YTD

1Q10

2Q10

3Q10

4Q10

FY10

1Q11

2Q11

3Q11

2011

Retail Marketing

Gasoline Sales, MM Gal

1,026

1,130

1,171

1,171

4,498

1,086

1,161

1,196

3,443

Middle Distillate Sales, MM Gal

91

114

117

110

432

97

106

118

321

Total Sales, MM Gal

1,117

1,244

1,288

1,281

4,930

1,183

1,267

1,314

3,764

Gasoline and Diesel Throughput

147

159

156

161

156

150

162

168

160

(Company-Owned or Leased Outlets)

(M Gal/Site/Month)

Merchandise Sales (M$/Store/Month)

87

101

103

92

96

85

97

105

96

Coke

Production, M Tons:

United States

842

883

953

916

3,594

861

922

964

2,747

Brazil

413

422

431

370

1,636

364

412

373

1,149

Key Volume Indicators –

Retail and Coke |

17

Financial Ratios, MM$ except ratios

* Represents intercompany loan due to Sunoco from SXL which is eliminated in

consolidation. **

Represents

Partners’

Capital

for

SXL

and

Shareholders’

Equity

for

Sunoco.

*** The Net Debt / Capital ratio is used by Sunoco management in its internal

financial analysis and by investors and creditors

in

the

assessment

of

Sunoco’s

financial

position;

calculation

excludes

noncontrolling

interests

except

for

SXL as prescribed by the revolver covenant.

Proforma

Proforma

Proforma

SUN

SUN

SUN

(ex SXL

SXL

(ex SXL)

Sunoco

SXL

(ex SXL)

Sunoco

SXC

SXL

& SXC)

Sunoco

Debt

868

1,596

2,464

1,129

1,300

2,429

698

1,698

1,128

3,524

Intercompany Debt*

-

-

-

100

-

-

-

100

-

-

Plus: Debt Guarantees

-

2

2

-

1

1

-

-

20

20

Less: Cash

(2)

(375)

(377)

(2)

(1,483)

(1,485)

(111)

(8)

(1,537)

(1,656)

Net Debt

866

1,223

2,089

1,227

(182)

945

587

1,790

(389)

1,888

Equity**

862

2,557

2,557

965

3,046

3,046

569

1,081

1,302

1,302

SXL Noncontrolling Interest

-

-

488

77

-

692

-

101

-

754

SunCoke Noncontrolling Interest

-

-

74

-

-

61

35

-

-

149

Capital

1,728

3,780

5,208

2,269

2,864

4,744

1,191

2,972

913

4,093

Net Debt / Capital (Sunoco

Revolver Covenant

N/A

32%

41%

N/A

-6%

20%

N/A

N/A

-43%

48%

Basis)***

Debt / Capital

50%

38%

44%

54%

30%

39%

54%

60%

46%

62%

(GAAP Basis)

9/30/2011

12/31/2009

12/31/2010 |

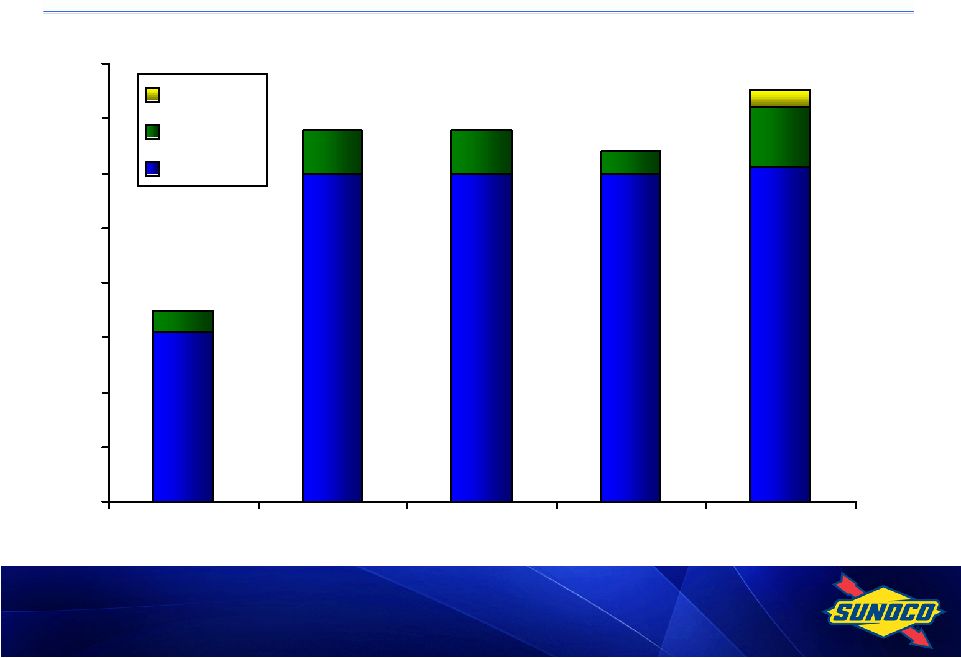

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

12/31/2009

12/31/2010

3/31/2011

6/30/2011

9/30/2011

SunCoke

SXL

Sunoco

18

Liquidity*, B$

*

Includes cash and cash equivalents of $0.4B, $1.5B, $1.5B, $1.5B, and $1.7B at

12/31/09, 12/31/10, 3/31/11, 6/30/11, and 9/30/11 respectively.

1.7

3.4

3.7

3.2

3.4 |

19

YTD

1Q10

2Q10

3Q10

4Q10

FY10

1Q11

2Q11

3Q11

2011

Total Refining & Supply

Net Production, MB/D

590.5

664.2

681.5

633.9

642.8

512.4

461.1

487.0

486.8

Gasoline

52%

52%

52%

54%

52%

52%

51%

51%

51%

Middle Distillates

34%

37%

37%

35%

36%

36%

36%

37%

37%

Residual Fuel

6%

6%

5%

4%

5%

5%

7%

7%

6%

Petrochemicals

4%

3%

4%

4%

4%

3%

3%

3%

3%

Other

9%

7%

7%

8%

8%

9%

8%

7%

8%

Less Refinery Fuel

-5%

-5%

-5%

-5%

-5%

-5%

-5%

-5%

-5%

Refining & Supply –

Products Manufactured |

20

YTD

1Q10

2Q10

3Q10

4Q10

FY10

1Q11

2Q11

3Q11

2011

Total Refining & Supply

Gasoline Production, MB/D

306.3

343.1

357.9

339.9

337.0

265.4

234.6

249.0

249.6

RFG / RBOB

47%

48%

43%

45%

46%

49%

63%

65%

59%

Conventional / CBOB

53%

52%

57%

55%

54%

51%

37%

35%

41%

Distillate Production, MB/D

202.4

244.5

250.1

225.1

230.6

183.6

165.5

181.9

177.0

On-Road Diesel Fuel

53%

66%

62%

52%

59%

52%

58%

64%

58%

Heating Oil / Off-Road Diesel

28%

15%

18%

25%

21%

26%

27%

19%

24%

Jet Fuel

17%

19%

19%

21%

19%

20%

13%

14%

16%

Kerosene / Other

2%

0%

1%

2%

1%

2%

2%

3%

2%

Refining & Supply –

Gasoline and Distillate Production |

21

Toledo 4-3-1 Benchmark

4 WTI Crude: NYMEX Futures Close + $2.00 for transportation

3 Unleaded Gasoline: Chicago Pipeline Platt’s Low

1 Distillate: 50% ULSD Chicago Pipeline Platt’s Low

50% Jet Gulf Coast Pipe Platt’s Low

Northeast 6-3-2-1 Value-Added Benchmark**

6 Dated Brent Crude: Platt’s Mid + $2.75 for transportation

3 Gasoline: 50% Unleaded RBOB NY Harbor Barge Platt's Low

50% 83 CBOB NY Harbor Barge Platt's Low

2 Distillate: 55% ULSD NY Harbor Barge Platt's Low

20% Jet/Kero NY Harbor Barge Platt's Low

25% No.2 Fuel Oil NY Harbor Barge Platt's Low

1 Resid: 60% No. 6 0.3% Sulfur High Pour Resid: NY Harbor Barge Platt’s

Low 40% No. 6 1.0% Sulfur High Pour Resid: NY Harbor Barge Platt’s Low

YTD

1Q10

2Q10

3Q10

4Q10

FY10

Jan 11

Feb 11

Mar 11

1Q11

2Q11

3Q11

2011

Northeast 6-3-2-1

Value-Added Benchmark

5.17

5.42

3.39

4.90

4.72

3.93

2.79

5.11

3.94

6.11

5.87

5.31

Toledo 4-3-1

Benchmark

3.99

8.89

7.50

6.33

6.68

9.89

15.52

n/a

12.70

n/a

n/a

12.70

YTD

1Q10

2Q10

3Q10

4Q10

FY10

Jan 11

Feb 11

Mar 11

1Q11

2Q11

3Q11

2011

Northeast 6-3-2-1

at 80% weight*

4.13

4.34

2.72

3.92

3.78

3.14

2.24

5.11

3.50

6.11

5.87

5.16

Toledo 4-3-1

at 20% weight*

0.80

1.78

1.50

1.27

1.33

1.98

3.10

n/a

1.69

n/a

n/a

0.56

R&S Weighted Benchmark*

4.93

6.12

4.22

5.19

5.11

5.12

5.34

5.11

5.19

6.11

5.87

5.72

Sunoco R&S Benchmark Margin, $/B

*

Beginning

in

March

2011,

the

R&S

benchmark

is

no

longer

weighted

with

20%

of

Toledo

4-3-1

margin

due

to

the

sale of the Toledo refinery on 3/1/2011.

Prior to Toledo sale: 80% of NE 6-3-2-1 Value Added Margin and 20%

of Toledo 4-3-1 margin.

Post Toledo sale: 100% of NE 6-3-2-1 Value Added Margin.

**

Adjusted

in

2Q11

to

reflect

market

conditions

more

closely

associated

with

NE

refining

system.

2010

amounts

have been restated for comparative purposes. |

22

Media releases and SEC filings are available

on our website at www.SunocoInc.com

Contact for more information:

Clare McGrory

(215) 977-6764

For More Information |