Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - PIONEER ENERGY SERVICES CORP | d239125d8k.htm |

Johnson Rice Energy

Conference

October 5-6, 2011

Exhibit 99.1

Well Positioned for Unconventional Plays |

2

Forward-looking Statements

This presentation contains various forward-looking statements and information

that are based on

management’s current

expectations and assumptions about future events. Forward-looking statements

are generally accompanied by words such as

“estimate,”

“project,” “predict,”

“expect,”

“anticipate,”

“plan,

” “intend,” “seek,” “will,” “should,” “goal” and other words that convey the uncertainty of future

events and outcomes. Forward-looking information includes, among other matters,

statements regarding the

Company’s anticipated growth, quality of assets, rig utilization rate, capital spending by oil

and gas companies, production rates, the Company's growth strategy, and the Company's

international operations. Although the Company believes that the

expectations and assumptions reflected in such forward-looking statements

are reasonable, it can give no assurance that such expectations and

assumptions will prove to have been correct. Such statements are subject to certain

risks, uncertainties and assumptions, including, among others: general and

regional economic conditions and industry trends; the continued strength of

the contract land drilling industry in the geographic areas where the Company

operates; decisions about onshore exploration and development projects to be made by oil

and gas companies; the highly competitive nature of the contract land drilling

business; the Company’s

future financial performance, including availability, terms and deployment of

capital; the continued availability of qualified personnel; changes in

governmental regulations, including those relating to the environment; the

political, economic and other uncertainties encountered in the Company's

international operations and other risks, contingencies and uncertainties, most of

which are difficult to predict and many of which are beyond our control.

Should one or more of these risks, contingencies or uncertainties materialize,

or should underlying assumptions prove incorrect, actual results may vary

materially from those expected. Many of these factors have been discussed in

more detail in the Company's annual report on Form 10-K for the fiscal

year ended December 31, 2010. Unpredictable or unknown factors that the

Company has not discussed in this presentation or in its filings with the

Securities and Exchange Commission could also have material adverse effects on actual

results of matters that are the subject of the forward-looking

statements. All forward-looking statements speak only as the date on

which they are made and the Company undertakes no duty to update or revise any

forward-looking statements. We advise our shareholders to use caution and common

sense when considering our forward-looking statements. |

Overview

Ticker Symbol:

PDC

Market Cap:

$402.2 million (Sep 29, 2011)

Stock price:

$7.42 (Sep 29, 2011)

Average 3-month daily

trading volume:

1,096,440 shares

Public float:

Approximately 61 million shares

Employees:

2,877

Headquarters:

San Antonio, Texas

Website:

www.pioneerdrlg.com

3 |

4

Pioneer Drilling Overview |

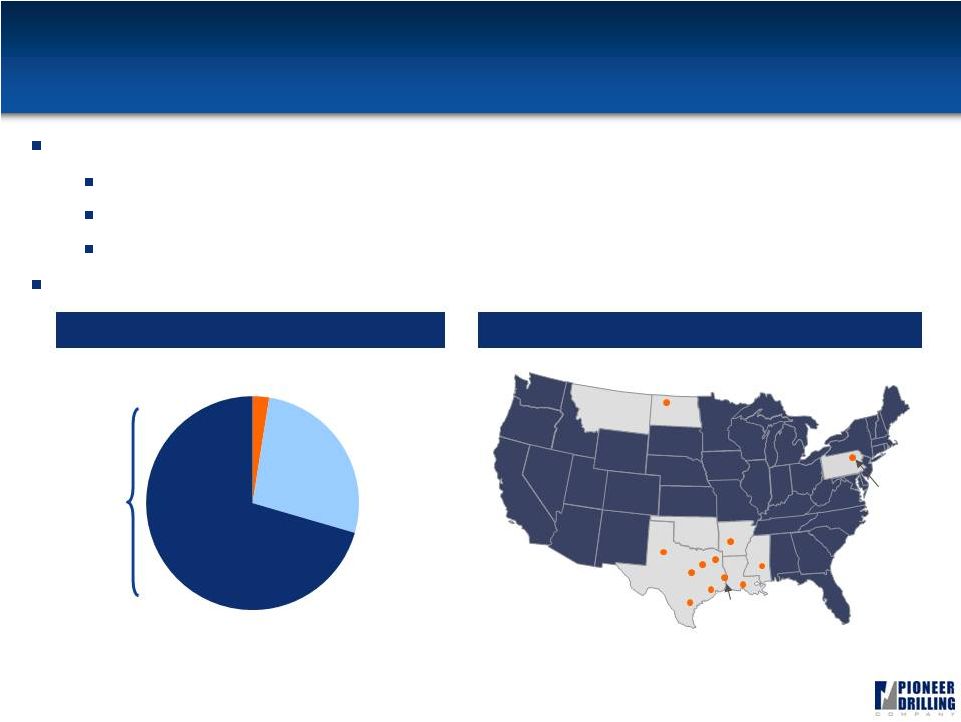

Pioneer Drilling Company

5

71 Drilling Rigs in 8 Locations

Approximately 9th largest contract driller

84 Well Service Rigs operating in 12 Locations

Approximately 7th largest well service

provider

99 Wireline Units in 21 Locations

81 cased hole

18 open hole |

6

Leading Service Provider Across Well Life Cycle

Total Revenue: $609 million

Total Margin: $214 million

Colombia

Services

Production

Services

Services

Production

Services

Diversified Business and Geography Mix

TTM June 30, 2011

63%

37%

58%

42%

Drilling

Drilling |

Investment Considerations

Continued organic growth opportunities in core businesses: land drilling,

well services and wireline

Signed six new-build drilling term contracts for delivery in the first and

second quarters of 2012

Adding 14 well service rigs in 2011

Adding 19 wireline units in 2011

Currently have 14 drilling rigs operating in the West Texas division with

expectations to have 16 to 18 rigs operating by the end of 2011

Strong contract backlog

41 rigs backed by term contracts (approximately 73% of working rigs)

Enhanced balance sheet flexibility

Equity offering of 6,900,000 shares priced on July 14, 2011, netting $94.3MM

Recently amended and restated credit agreement for $250mm, 5-yr, senior secured

credit facility maturing in 2016

7 |

High Quality Drilling Fleet,

Focused on Unconventional Plays

8

Historical Fleet Growth

Drilling Locations

Current Rig Fleet Mix

Note: Rig counts for 2004, 2005 and 2006 represent fiscal years ended March 31,

2004, 2005 and 2006 while 2007, 2008 and 2009 represent fiscal years ended

December 31, 2007, 2008 and 2009. *Cold-stacked

15 rigs

South Texas

Electric

Mechanical

550-999

HP

1,000-1,499

HP

1,500-2,000

HP

49%

31%

20%

58%

42%

40

52

61

70

71

66

71

2004

2005

2006

2007

2008

2009

2010

9 rigs

4 rigs

8 rigs

7 rigs

9 rigs

3 rigs

16 rigs

Oklahoma*

Colombia

Appalachia

West Texas

Utah

North Dakota

East Texas |

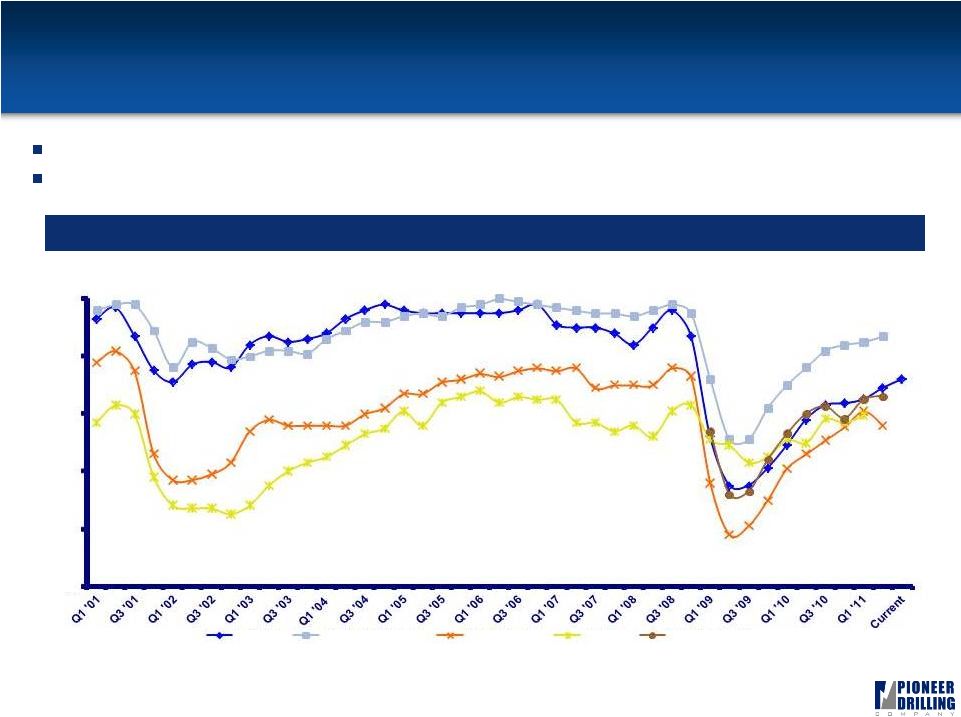

9

Strong Utilization Through the Cycles

Source: Helmerich & Payne, Patterson-UTI, & Precision Drilling

data consists of U.S. domestic utilization rates derived from Form 10-K, Form 10-Q reports, & press releases. Nabors utilization rates for worldwide land fleet obtained from

public documents and industry analysts. Helmerich & Payne Q3 2010 only

estimated based on analyst reports. Pioneer Drilling utilization rates include Colombian operations beginning Q3 2007.

(1) PDC utilization as of August 4, 2011.

Averaged 85% utilization through cycles since 2001, comparing favorably to

peers Utilization

has

rebounded

from

a

monthly

low

of

33%

in

June

2009

to

72%

currently

(1)

Comparable Utilization Rates

0%

20%

40%

60%

80%

100%

Pioneer

Helmerich & Payne

Patterson-UTI

Nabors

Precision (U.S.) |

10

Modern, Efficient Drilling Fleet

35 rigs working with top drives (49%

of fleet)

16 walking/skidding systems on rigs

36 pairs of 1,300/1,600 HP mud pumps

66% of rigs have iron roughnecks

42% of rigs are electric

50 Series Rig |

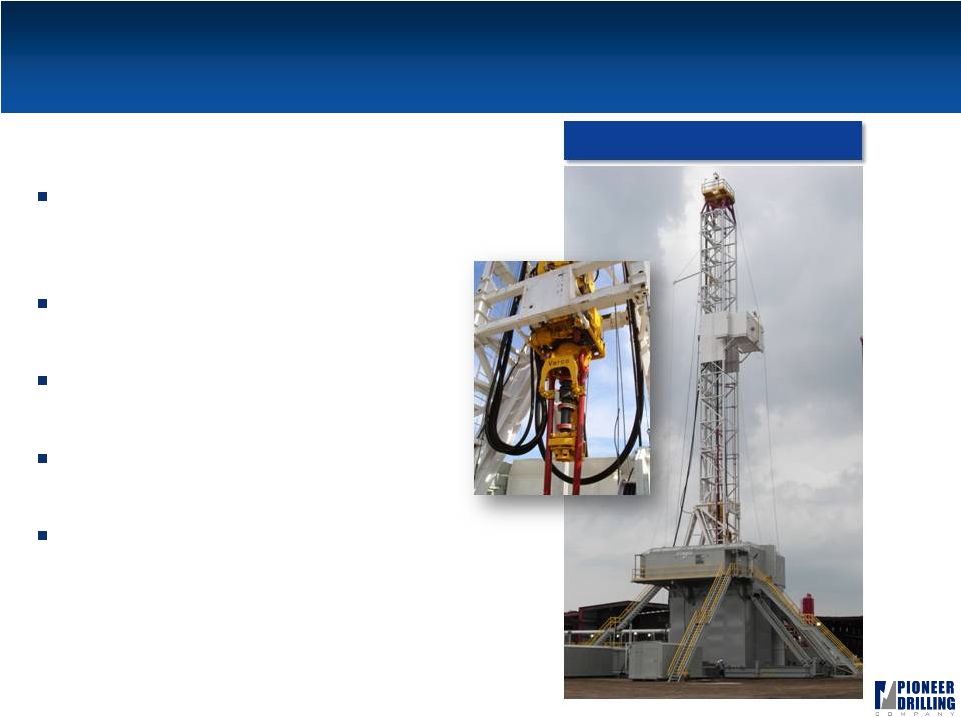

New-Builds Driving Visible Organic Growth

11

Six state-of-the-art AC rigs under construction

Rigs secured with long term contracts up to four

years

Attractive rates of return (20%+ IRR)

Ideal for drilling complex shales such as Bakken,

Eagle Ford and Marcellus |

New-Build Features

12

State-of-the-art 550K and 750K sub & mast AC new-

builds

Integrated 500 ton top drives in mast section for

faster rig up and rig down

Crane free rig up / rig down design

30 loads on base rig for fast moves

BOP handling systems

Automatic catwalk

1,600 HP and 2,000 HP mud pumps

Latest features in rig control software

Ability to drill multi-well single-row pads and walk

easily between wells with above ground heads |

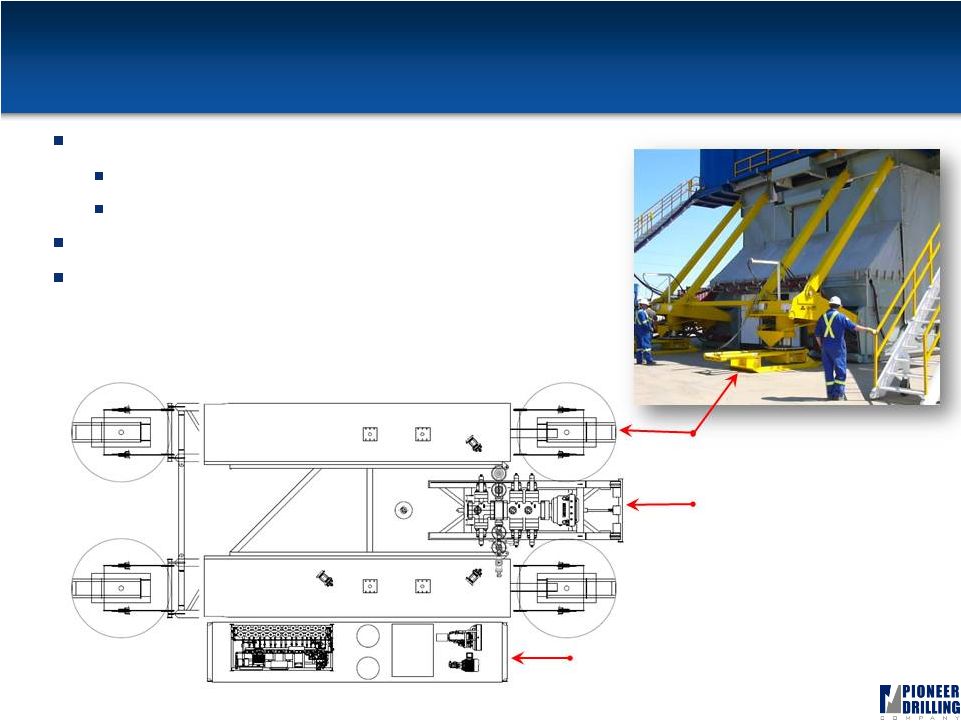

New-Build Pad Drilling Capability

13

BOP Wrangler

Pin On Walking System

One Walker Per Corner

Accumulator/HPU Skid

Pin On Walking System

Can walk in either direction or spin the rig

Can walk with full set back of drill pipes in mast

Accumulator & HPU walks with sub

BOP handling system walks with sub |

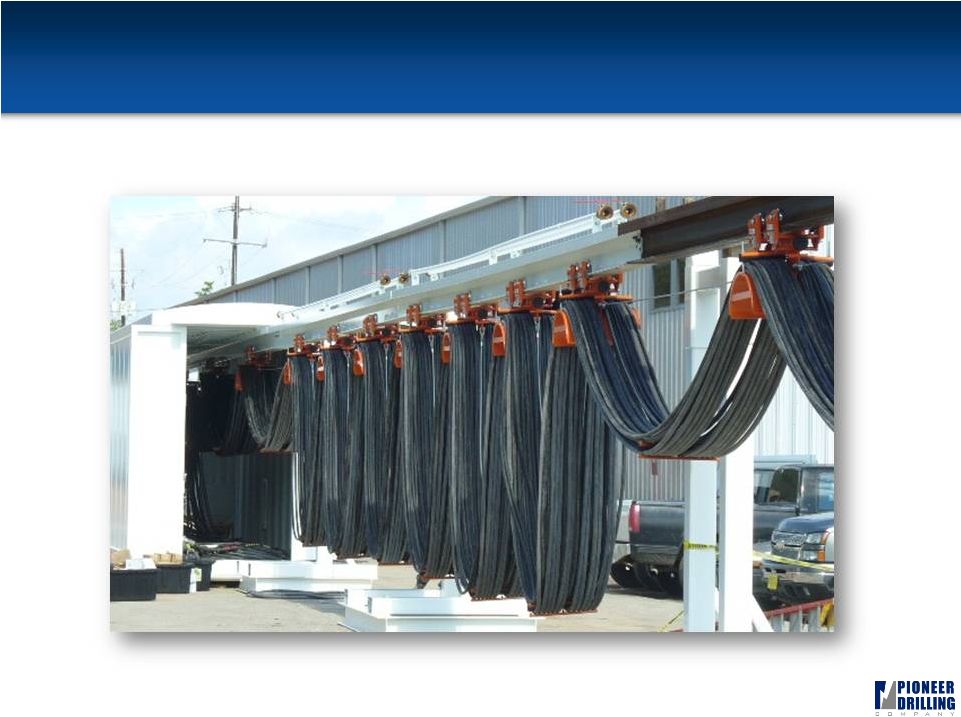

New-Build Advanced Electrical System

14

Festoon System to Manage Electrical Supply to Substructure

|

Premium Well Servicing Fleet,

Established Positions in Emerging Shale Plays

15

One

of

the

newest

and

most

highly

capable

well

service

fleets

in

the

industry

Seventy-five 550 HP rigs

Eight 600 HP rigs

One 400 HP rig

Established in the Bakken, Fayetteville, Haynesville and Eagle Ford shales

Average year in service: 2007

70%

2007 or

newer

Williston

Bryan

Palestine

Longview

New Iberia

El Campo

Liberty

Kenedy

Greenbrier

Laurel

2005-2006

2002-2004

New

Milford

Snyder

Well Service Fleet Age

Well Service Locations

27%

2% |

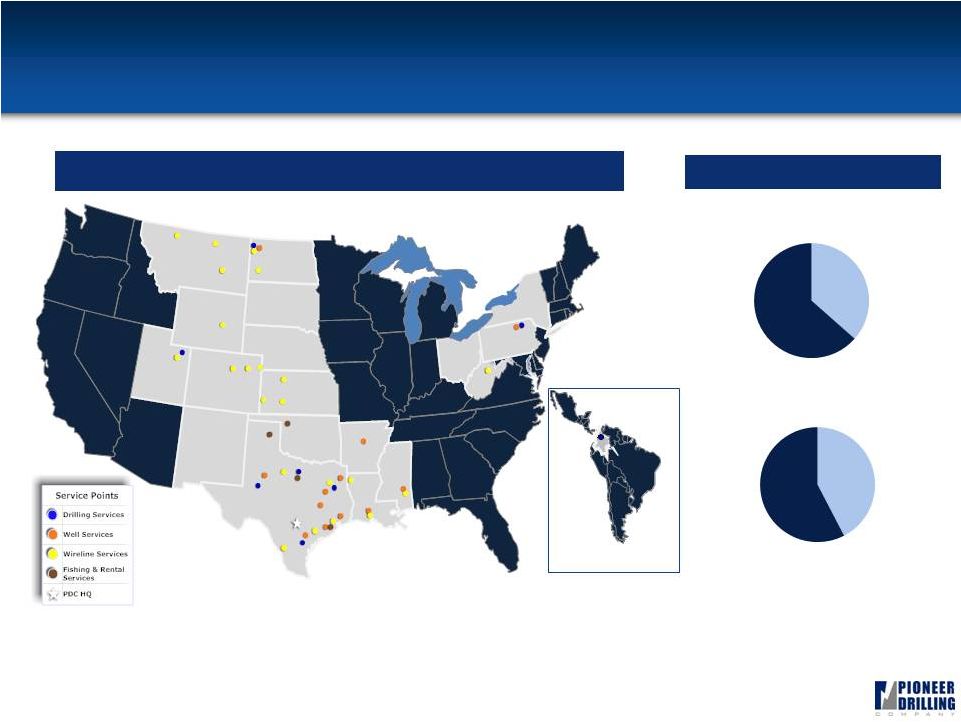

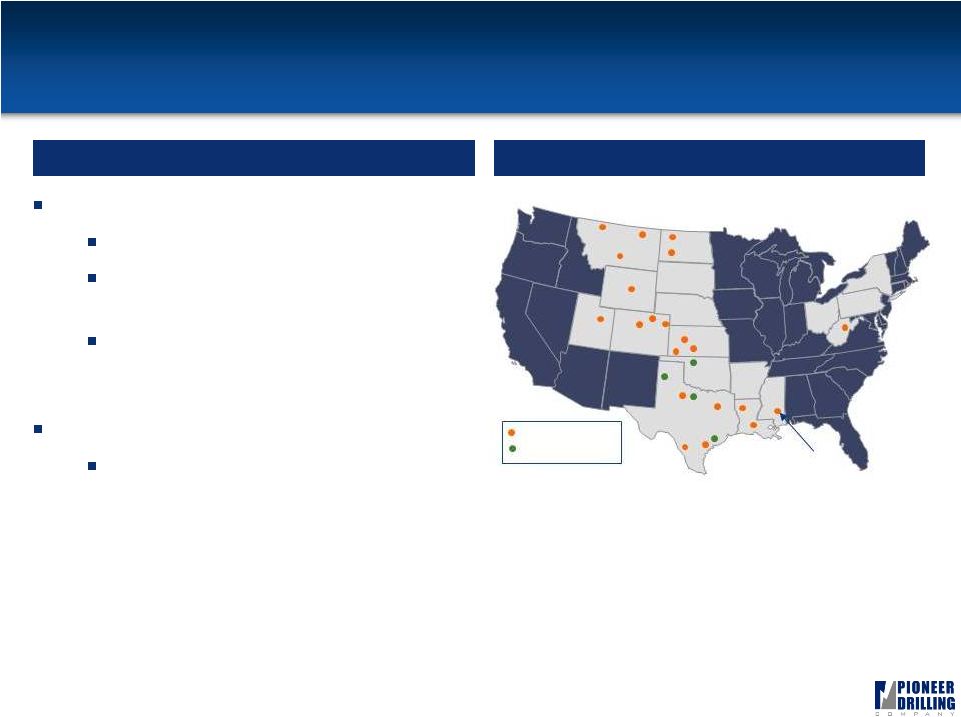

Wireline and Fishing & Rental Overview

16

Wireline Services

Open and cased-hole wireline services

Fleet of 99 wireline units has an

average age of less than 6 years

Established in the Bakken, Barnett,

Marcellus, Haynesville, Niobrara, and

Eagle Ford shales

Fishing & Rental Services

Range of specialized services and

equipment that are utilized on a non-

routine basis for both drilling and well

servicing operations

Overview

Wireline Locations

Williston

Dickinson

Cut Bank

Billings

Havre

Tyler

Bossier City

Broussard

Graham

Roosevelt

Pratt

Liberal

Hays

Casper

Buckhannon

Ft. Morgan

Brighton

Wray

Woodward

Pampa

Springtown

El Campo

Wireline

Fishing & Rental

Laredo

Laurel

Victoria |

17

Industry and Market Conditions |

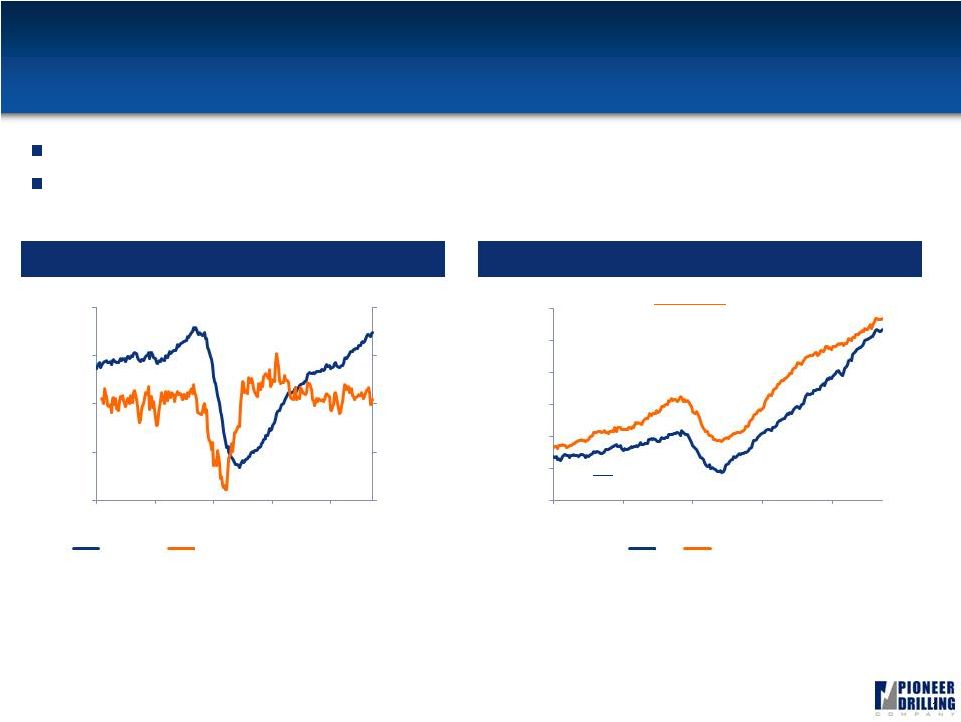

Resurgence in U.S. Land Rig Count

1

18

Steady rig count improvement since the second half of 2009

Horizontal and oil rig counts have surpassed Fall 2008 peak levels

Land Rig Count

Horizontal & Oil Rig Count

Source: Baker Hughes

Source: Baker Hughes.

Oil

Fall ’08 Peak: 442

September 23, 2011: 1,071

Horizontal

Fall ’08 Peak: 650

September 23, 2011: 1,140

0.0%

2.5%

5.0%

600

1,000

1,400

1,800

2,200

Jan-07

Jan-08

Jan-09

Jan-10

Jan-11

Land Rigs

BHI Rolling 4-Week Avg. Weekly Change

0

200

400

600

800

1,000

1,200

Jan-07

Jan-08

Jan-09

Jan-10

Jan-11

Oil

Horizontal

-

5.0%

-

2.5% |

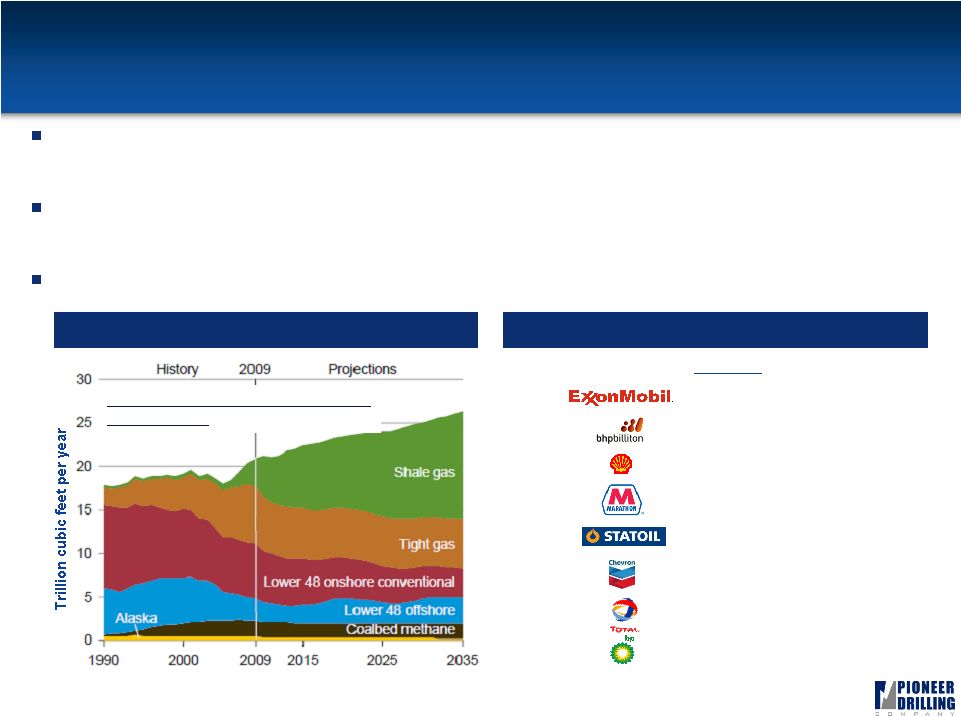

Benefits of Growing Shale Plays

1

19

Oilfield service companies stand to benefit from shale production due to its lower

risk

development

and

increased

service

intensity

(up

to

3

-

5x conventional)

Shale

gas

is

expected

to

make

up

47%

of

total

U.S.

production

in

2035 vs. its 16%

share in 2009

(1)

Reintroduction

of

the

Majors

in

the

U.S.

market

should

result

in

greater activity levels

Recent U.S. Shale Investments

Growing Importance of Shale

$Millions

$40,991

12/14/2009

$12,100

7/13/2011

$4,700

5/28/2010

$3,500

6/1/2011

$3,375

11/11/2008

$3,200

11/9/2010

$2,250

12/30/2009

$1,900

9/2/2008

U.S. NATURAL GAS PRODUCTION

1990 –

2035

(1)

(1) SOURCE: EIA “ANNUAL ENERGY OUTLOOK 2011” APRIL 2011 |

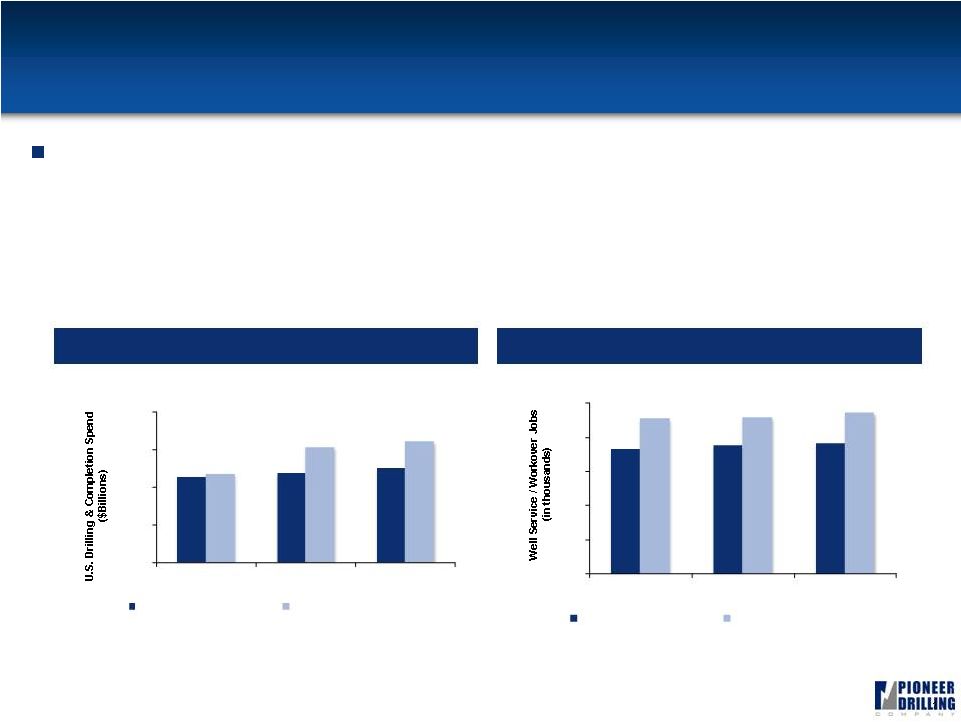

Conclusion: Improving Oil Service Outlook

1

20

North American capital spending and activity outlook is much

improved

Source: Spears & Associates

Source: Spears & Associates.

Upstream Spending Outlook

Well Service / Workover Jobs Outlook

$115

$120

$126

$119

$154

$162

$0

$50

$100

$150

$200

2010

2011

2012

Jun 2010 Estimate

Jun 2011 Estimate

73

76

77

91

92

95

0

20

40

60

80

100

2010

2011

2012

Jun 2010 Estimate

Jun 2011 Estimate |

21

Financials |

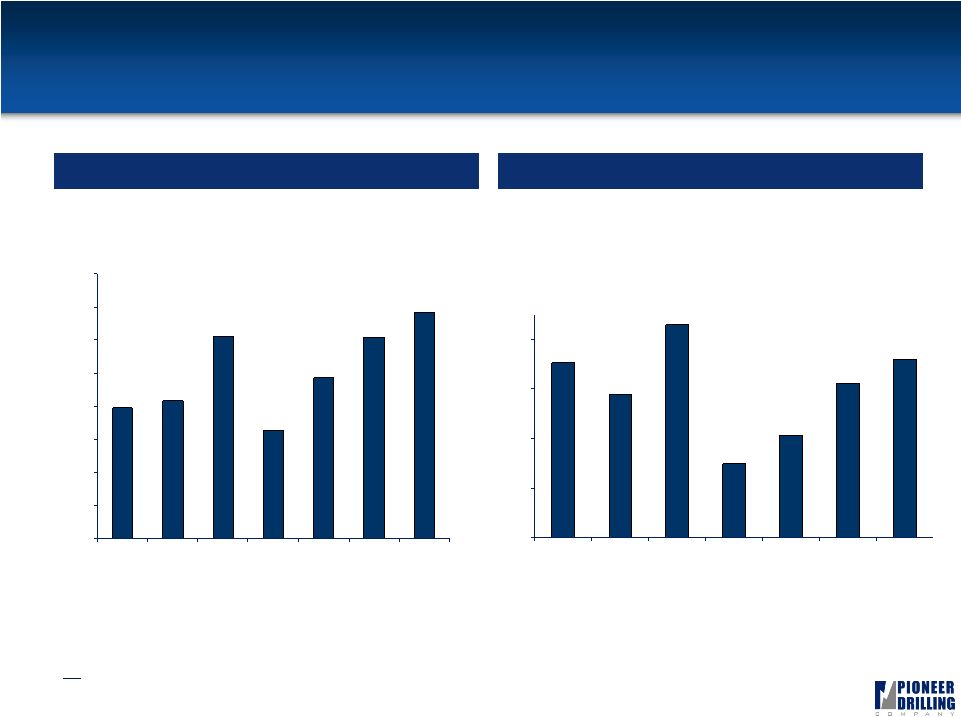

22

$177

$145

$215

$75

$103

$156

$180

$0

$50

$100

$150

$200

2006

2007

2008

2009

2010

Q2 2011

TTM

Q2 2011

Ann.

Strong Revenue and Adjusted EBITDA Growth

Revenue ($ millions)

Adjusted EBITDA ($ millions)

Note:

Fiscal year end was changed from March 31 to December 31 effective on December 31,

2007; all data points reflect calendar year and trailing twelve months information derived from 10K and 10Q filings.

$396

$417

$610

$326

$487

$609

$685

$0

$100

$200

$300

$400

$500

$600

$700

$800

2006

2007

2008

2009

2010

Q2 2011

TTM

Q2 2011

Ann. |

Strong Liquidity and Capital Structure

23

Pro Forma Capitalization (As of June 30, 2011)

Pro Forma

($ in millions)

June 30, 2011

$94MM Net

Equity

Offering

Cash

$

11.5

$

63.8

Revolving Credit Facility ($250)

42.0

-

Sr. Unsecured Notes

240.6

240.6

Other

2.1

2.1

Total Debt

$

284.7

$

242.7

Stockholders' Equity

399.9

494.2

Total Capitalization

$

684.6

$

736.9

Liquidity

210.3

304.6

Debt / LTM EBITDA

1.90x

1.55x

Debt / Total Book Capitalization

41.6%

32.9%

(1) Excludes $9.2 million of LCs outstanding. Pro-Forma for amended and

restated $250 mm credit facility. (2) Defined as remaining credit

facility capacity plus cash less LCs outstanding. (3) Total consolidated

leverage ratio as reported in form 10Q for 2011. (1)

(2)

(3) |

24

Appendix |

25

Reconciliation

of

Adjusted

EBITDA

to

Net

Income

We define Adjusted EBITDA as earnings (loss) before interest income (expense),

taxes, depreciation, amortization, impairments, and the Colombian

Net

Equity

Tax.

Although

not

prescribed

under

GAAP,

we

believe

the

presentation

of

Adjusted

EBITDA

is

relevant

and

useful

because it helps our investors understand our operating performance and makes it

easier to compare our results with those of other companies that have

different financing, capital or tax structures. Adjusted EBITDA should not be considered in isolation from or as a

substitute

for

net

earnings

(loss)

as

an

indication

of

operating

performance

or

cash

flows

from

operating

activities

or

as

a

measure

of

liquidity. A reconciliation of net earnings (loss) to Adjusted EBITDA is included

in the table below. Adjusted EBITDA, as we calculate it, may not be

comparable to EBITDA measures reported by other companies. In addition, Adjusted EBITDA does not represent funds

available for discretionary use.

($ in millions)

Q3

2010

Q4

2010

Q1

2011

Q2

2011

TTM

Adjusted EBITDA

34.2

37.7

38.9

45.1

155.9

Colombian Net Equity Tax

-

-

(7.3)

-

(7.3)

Depreciation & Amortization

(30.8)

(31.5)

(32.3)

(32.4)

(127.0)

Net Interest

(7.6)

(7.8)

(7.5)

(8.0)

(30.9)

Impairment Expense

-

(3.3)

-

-

(3.3)

Income Tax (Expense) Benefit

1.6

(1.0)

2.1

(1.0)

1.7

Net Income (Loss)

(2.6)

(6.0)

(6.0)

3.7

(10.9)

($ in millions)

2006

2007

2008

2009

2010

Adjusted EBITDA

176.6

144.5

214.8

74.9

103.2

Colombian Net Equity Tax

-

-

-

-

-

Depreciation & Amortization

(47.6)

(63.6)

(88.1)

(106.2)

(120.8)

Net Interest

3.6

3.3

(11.8)

(8.9)

(26.6)

Impairment Expense

-

-

(171.5)

-

(3.3)

Income Tax (Expense) Benefit

(47.7)

(27.3)

(6.1)

17.0

14.3

Net Income (Loss)

84.8

56.9

(62.7)

(23.2)

(33.3)

Fiscal Year |

26 |