Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - STRATEGIC HOTELS & RESORTS, INC | d8k.htm |

Investor Presentation

September 2011

Exhibit 99.1 |

2

I.

Company Overview

II.

Industry Update

III.

Operating Trends

IV.

Financial Overview

Agenda |

3

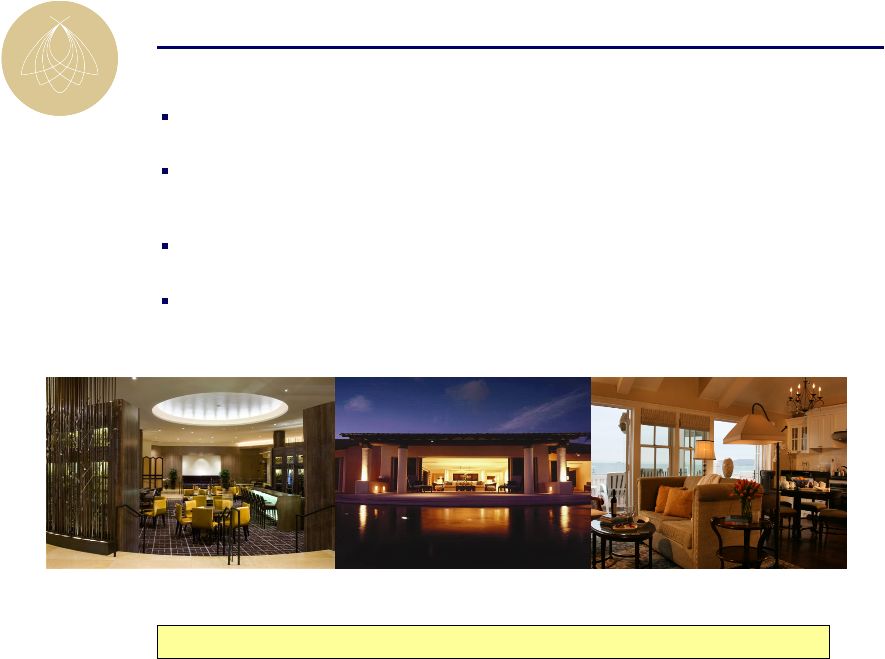

World-class luxury hotels supported by unique real-estate value

Luxury segment has historically outperformed the overall industry in a

recovery

Industry leading asset management capabilities

Management team and board members with significant hospitality

industry experience

Strategic Hotels Overview

Fairmont Chicago

Lobby and ENO Wine Bar

Four Seasons Punta Mita

Coral Suite

Hotel del Coronado

Beach Village

Highest quality hotel portfolio in the public markets |

4

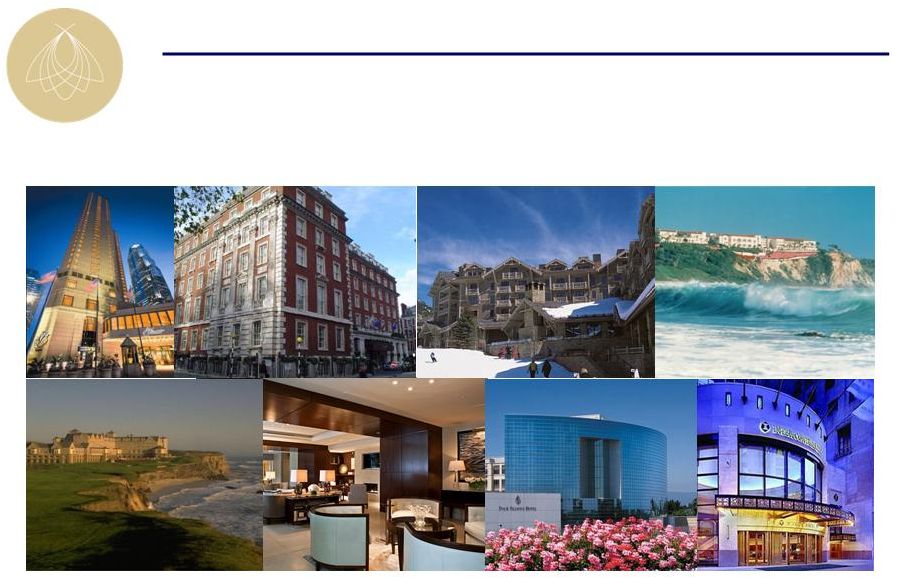

17 hotels and resorts with 7,762 rooms

World-Class Hotels in High Barrier to Entry Markets

|

5

Unique and Irreplaceable Hotel Portfolio

Fairmont Chicago

Marriott Grosvenor Square

Four Seasons Jackson Hole

Ritz-Carlton Laguna Niguel

Ritz-Carlton Half Moon Bay

Four Seasons Washington, D.C.

Four Seasons Silicon Valley

InterContinental Chicago |

6

Revenue enhancement through market research based programs

Exceptional asset management supported by internally developed operating

systems

Aggressive and early cost cutting initiatives implemented in advance of the

downturn

Proactively maintaining fixed cost reduction at hotels during recovery phase

Rigorous oversight of brand managers to ensure alignment of interests

Evaluation and implementation of value add ROI projects

Industry Leading Asset Management Capabilities |

7

Notable 2008

capital

projects

Notable 2009

capital

projects

InterContinental Miami –

Room and lobby renovation

InterContinental Chicago –

Michael Jordan Steak House addition

Four Seasons Washington, D.C. –

ENO wine tasting room

Four Seasons Washington, D.C –

Retail outlet renovation

Marriott Lincolnshire –

Lobby renovation

Westin St. Francis –

Michael Mina Steakhouse conversion

Four Seasons Washington, D.C. –

Lobby renovation, 11-room

expansion, new restaurant, 63-room and suite renovation

Westin St. Francis –

Clock Bar

Fairmont Chicago –

ENO wine tasting room, lobby renovation,

guestroom renovation, new spa and fitness center

Four Seasons Punta Mita –

New lobby bar

Ritz-Carlton Half Moon Bay –

ENO wine tasting room,

restaurant and lounge renovation, suite renovation

Notable 2010

capital

projects

2011 Planned

Projects

Fairmont Chicago Lobby

Four Seasons Washington, D.C.

Lobby

Four Seasons Washington, D.C.

Retail

InterContinental Miami Guestroom

Portfolio Well-Positioned To Enhance Cash Flow Growth

|

8

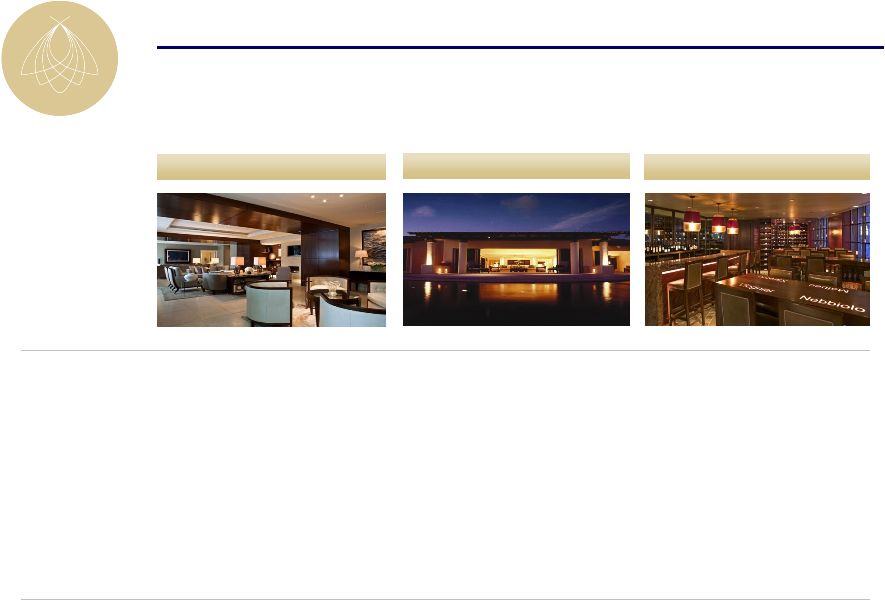

Four Seasons Washington, D.C.

Four Seasons Punta Mita

InterContinental Chicago

Value Enhancement Projects

11.5%

8.5%

15.0%

2010 EBITDA

Description:

Bourbon Steakhouse and 11-

room expansion

Two, 5-bedroom suite expansion,

23-room expansion with river pool

ENO wine room

Year of project:

2008-2009

2006-2007

2006

Investment

($mm):

$22.1

$19.7

$1.7

yield (%): |

9

I.

Company Overview

II.

Industry Update

Agenda |

10

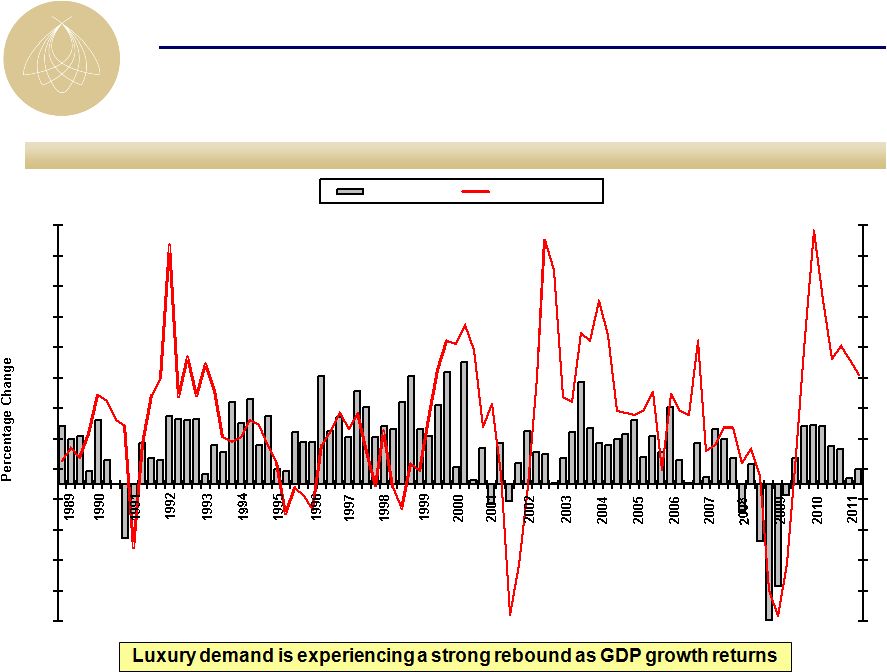

U.S. luxury demand vs. GDP growth

U.S. Luxury Demand Correlated with GDP

Quarterly percentage change to prior year

-9.0

-7.0

-5.0

-3.0

-1.0

1.0

3.0

5.0

7.0

9.0

11.0

13.0

15.0

17.0

-9.0

-7.0

-5.0

-3.0

-1.0

1.0

3.0

5.0

7.0

9.0

11.0

13.0

15.0

17.0

GDP % Change

Demand % Change |

11

Source: Smith Travel Research

Note: Data represents trends within the United States

Project pipeline forecast as of 6/30/11

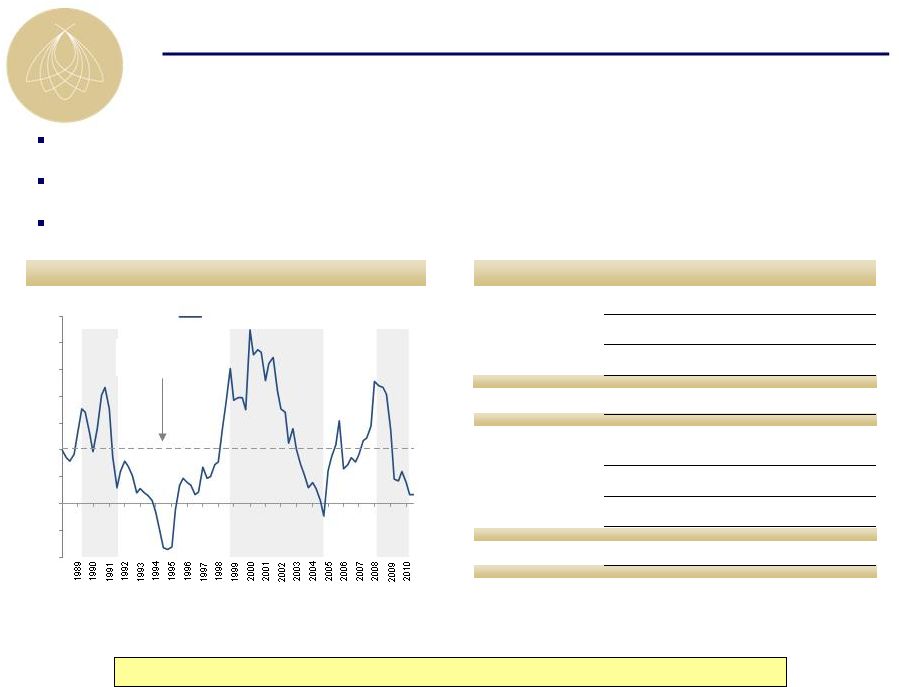

Supply growth was lower leading into this downturn than past downturns and remains

minimal Projects in planning and under construction have decreased

significantly Less than 1% new luxury supply projected in SHR markets

Quarterly luxury supply YoY % change

1988 –

Q2 2011

Average: 4.1%

Favorable Supply Outlook

Minimal supply growth in BEE markets

Rooms in

construction

2010

2011

% of 2011

supply

% change

Luxury

2,382

820

0.7%

(65.6%)

Upper-Upscale

6,475

9,146

1.7%

41.3%

Luxury & Upper-Upscale

8,857

9,966

1.5%

12.5%

Other

55,950

40,243

1.0%

(28.1%)

Total

73,664

60,175

1.2%

(22.5%)

Total active

pipeline

2010

2011

% of 2011

supply

% change

Luxury

5,775

4,117

3.3%

(28.7%)

Upper-Upscale

20,821

22,497

4.1%

8.0%

Luxury & Upper-Upscale

26,596

26,614

3.9%

0.1%

Other

332,143

291,327

6.9%

(12.3%)

Total

385,335

344,555

7.1%

(10.6%)

(4%)

(2%)

0%

2%

4%

6%

8%

10%

12%

14%

YoY % supply growth |

12

Source: Smith Travel Research

Note: Data represents trends within the United States

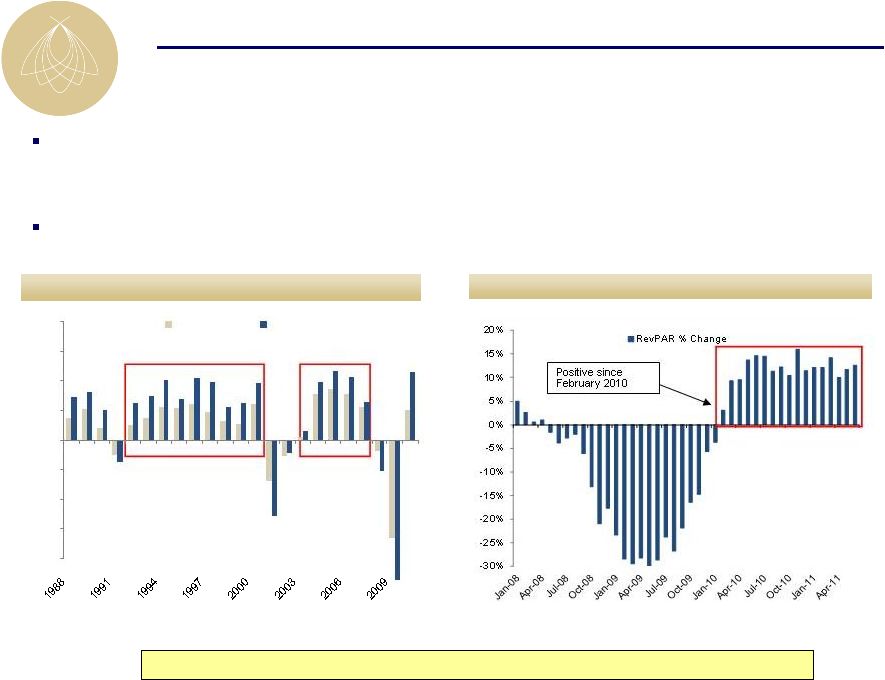

Annual % change in RevPAR

Monthly YoY % change in luxury RevPAR

Luxury

hotels

have

experienced

prolonged

RevPAR

growth

following

past

industry

downturns

–

1991: 9 consecutive years of annual luxury RevPAR growth totaling 100% or 8%

annually –

2001/2002: 5 consecutive years of annual luxury RevPAR growth totaling 47% or 8%

annually After 21 months of negative RevPAR growth, luxury RevPAR has

exhibited significant growth since February 2010

Luxury Hotels Outperform in a Recovery

Luxury RevPAR growth has remained positive since February 2010

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

Total U.S.

Luxury |

13

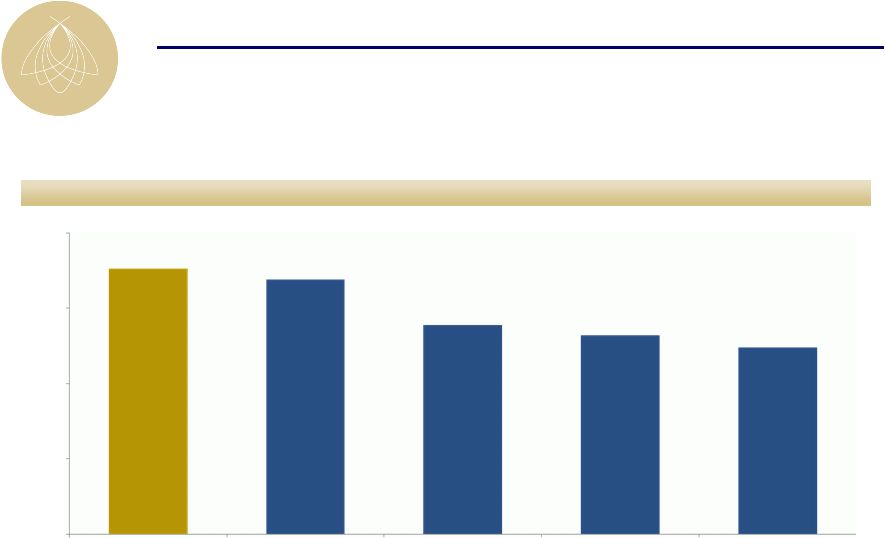

Second Quarter 2011 RevPAR

Source: Company filings as of 6/30/11

1

North American Same Store portfolio

#1 in RevPAR in the Public Lodging Sector

$0

$50

$100

$150

$200

BEE¹

LHO

HST

SHO

DRH |

14

I.

Company Overview

II.

Industry Update

III.

Operating Trends

Agenda |

15

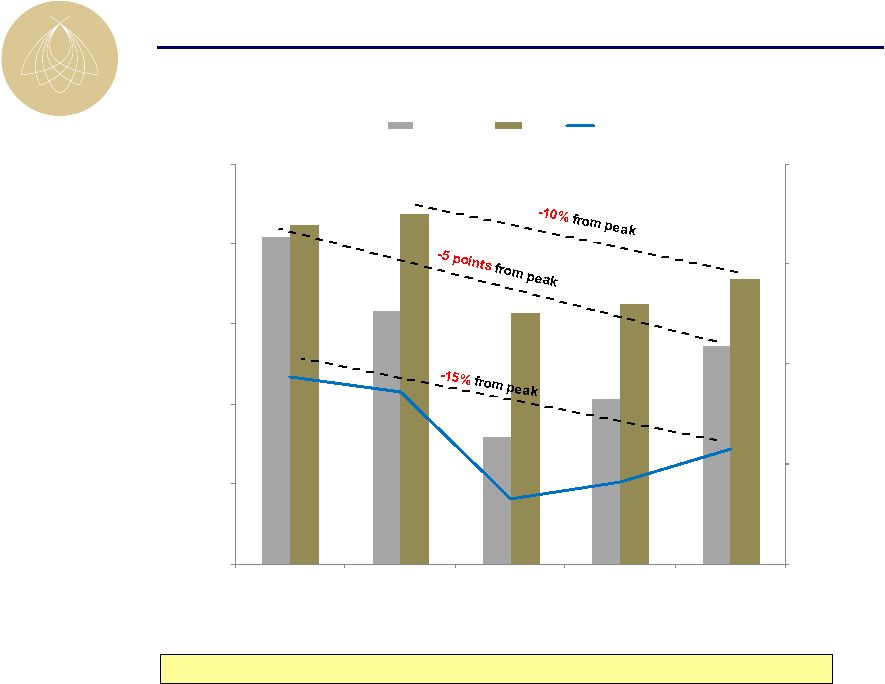

Historical Comparison

Operating performance improving; still significantly below peak

(Same Store North American Portfolio)

Portfolio excludes: Hotel del Coronado, Fairmont Scottsdale Princess, Four Seasons

Jackson Hole, Four Seasons Silicon Valley $120

$160

$200

$240

$280

60.0%

64.0%

68.0%

72.0%

76.0%

80.0%

2007

2008

2009

2010

2011F

ADR / RevPAR

Occupancy

Occupancy

ADR

RevPAR |

16

(EBITDA in millions)

(a)

Excludes Fairmont Scottsdale Princess, Four Seasons Jackson Hole, Four Seasons

Silicon Valley, and Hotel del Coronado Operations

Corporate Results

Strong Second Quarter Results

Comparable EBITDA

$37.7

12.9%

$42.5

Comparable FFO /share

$0.04

25.0%

$0.05

(Same Store U.S. Portfolio)

(a)

Q2

2010

Q2

2011

ADR

$215

6.5%

$229

RevPAR

$154

12.6%

$173

Total RevPAR

EBITDA Margins

$290

20.9%

11.5%

390bps

$323

24.8% |

17

I.

Company Overview

II.

Industry Update

III.

Operating Trends

IV.

Financial Overview

Agenda |

18

2011 Guidance

(EBITDA in millions)

(b)

2010 results exclude $4.9 mm of real estate tax refunds and no adjustments for

cancellation fees (c)

2010 excludes $12.6 mm of VCP expense; 2011 VCP expense excluded

Operations

(a)

Corporate Results

(c)

EBITDA

$132.0

10%-17%

$145.0-$155.0

FFO / share

$0.05

60%-180%

$0.08-$0.14

(a)

Portfolio excludes Fairmont Scottsdale Princess, Four Seasons Jackson Hole, Four

Seasons Silicon Valley, and Hotel del Coronado 2010

2011

Guidance

RevPAR

$153

8%-9.5%

$165-$167

Total RevPAR

$286

8%-9%

$309-$312

EBITDA

Margins

(b)

19.0%

200 -

300 bps

21%-22% |

19

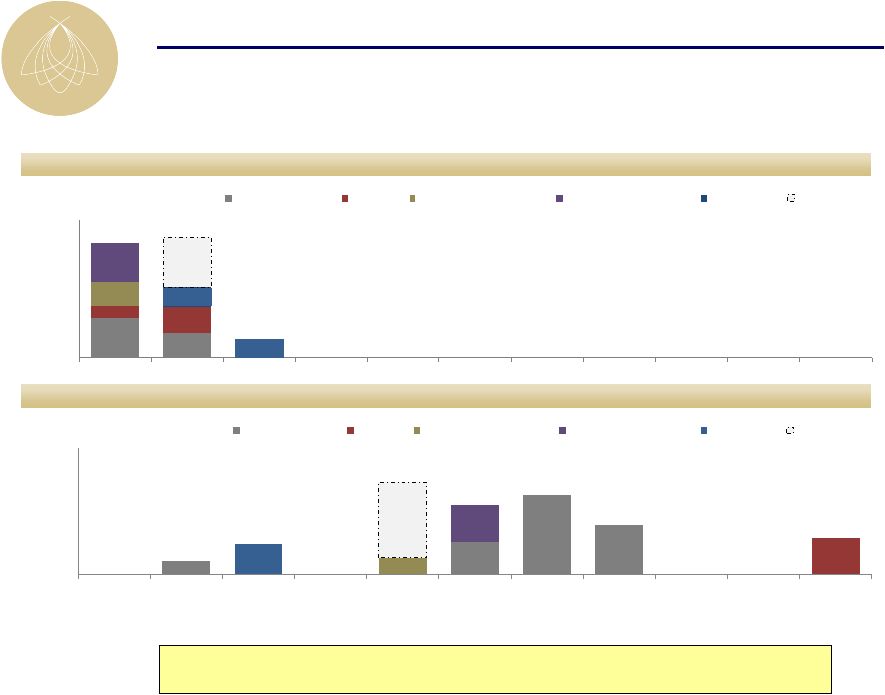

12/31/09 Actual ($mm)

Today ($mm)

Debt Maturity Profile Update

Significant accomplishments in debt maturity profile; final refinancing

stage to be executed throughout 2011

Note: Debt shown at pro rata amount of unconsolidated and consolidated joint

ventures $52.2

$130.0

$317.8

$195.0

$145.0

$66.5

$145.8

$119.0

$0.0

$100.0

$200.0

$300.0

$400.0

$500.0

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

Bank / Life Co.

CMBS

Fairmont Scottsdale

Hotel del Coronado

European

Corporate

$300.0

Capacity

$275.8

$281.7

$173.5

$90.0

$194.8

$180.0

$282.8

$148.9

$124.9

$358.0

$0.0

$200.0

$400.0

$600.0

$800.0

$1,000.0

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

Bank / Life Co.

CMBS

Fairmont Scottsdale

Hotel del Coronado

European

Corporate

$834.5

$875.2 |

20

Except

for

historical

information,

the

matters

discussed

in

this

press

release

are

forward-looking

statements

subject

to

certain risks and uncertainties. Actual results could differ materially from the

Company's projections and forward-looking statements

are

not

guarantees

of

future

performance.

These

forward

looking

statements

are

identified

by

looking

their

use

of terms and phrases such as “anticipate,”

“believe,”

“could,”

“estimate,”

“expect,”

“intend,”

“may,”

“plan,”

“predict,”

“project,”

“should,”

“will,”

“continue”

and other similar terms and phrases, including references to assumptions and

forecasts of future results.

Factors that may contribute to these differences include, but are not limited to

the following: ability

to

obtain,

refinance

or

restructure

debt

or

comply

with

covenants

contained

in

our

debt

facilities;

volatility

in

equity

or

debt

markets;

availability

of

capital;

rising

interest

rates

and

operating

costs;

rising

insurance

premiums;

cash

available

for

capital

expenditures;

competition;

demand

for

hotel

rooms

in

our

current

and

proposed

market

areas;

economic

conditions

generally and in the real estate market specifically, including deterioration of

economic conditions and the extent of its effect on business and leisure

travel and the lodging industry; ability to dispose of existing properties in a manner

consistent

with

our

disposition

strategy;

delays

in

construction

and

development;

the

failure

of

closing

conditions

to

be

satisfied; risks related to natural disasters; the effect of threats of terrorism

and increased security precautions on travel patterns and hotel bookings;

the outbreak of hostilities and international political instability; legislative or regulatory

changes, including changes to laws governing the taxation of REITs; and changes in

generally accepted accounting principles, policies and guidelines

applicable to REITs. Certain of these risks and uncertainties are described in greater

detail in our filings with the Securities and Exchange Commission. Although we

believe our current expectations to be based

upon

reasonable

assumptions,

we

can

give

no

assurance

that

our

expectations

will

be

attained

or

that

actual

results

will

not

differ

materially.

We

undertake

no

obligation

to

update

any

forward-looking

statement

to

conform

the

statement

to

actual results or changes in our expectations.

Disclaimer |

|