Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Manitex International, Inc. | d8k.htm |

| EX-99.1 - PRESS RELEASE - Manitex International, Inc. | dex991.htm |

“Focused

manufacturer of

engineered lifting

equipment”

Manitex International, Inc.

Conference Call

Second Quarter 2011

August 10th, 2011

Exhibit 99.2 |

2

Forward Looking Statements &

Non GAAP Measures

“Focused

manufacturer of

engineered lifting

equipment”

Safe Harbor Statement under the U.S. Private Securities Litigation Reform Act of

1995: This presentation contains statements that are forward-looking in

nature which express the beliefs and expectations of management including

statements regarding the Company’s expected results of operations or liquidity;

statements concerning projections, predictions, expectations, estimates or forecasts

as to our business, financial and operational results and future economic

performance; and statements of management’s goals and objectives and

other similar expressions concerning matters that are not historical facts. In some

cases, you can identify forward-looking statements by terminology such as

“anticipate,” “estimate,”

“plan,”

“project,”

“continuing,”

“ongoing,”

“expect,”

“we believe,”

“we intend,”

“may,”

“will,”

“should,”

“could,”

and similar expressions. Such statements are based on current plans, estimates and

expectations and involve a number of known and unknown risks, uncertainties

and other factors that could cause the Company's future results, performance

or achievements to differ significantly from the results, performance or

achievements expressed or implied by such forward-looking statements. These factors and additional

information are discussed in the Company's filings with the Securities and Exchange

Commission and statements in this presentation should be evaluated in light of

these important factors. Although we believe that these statements are based

upon reasonable assumptions, we cannot guarantee future results.

Forward-looking statements speak only as of the date on which they are made, and

the Company undertakes no obligation to update publicly or revise any

forward-looking statement, whether as a result of new information, future

developments or otherwise. Non-GAAP

Measures:

Manitex

International

from

time

to

time

refers

to

various

non-GAAP

(generally

accepted accounting principles) financial measures in this presentation.

Manitex believes that this information is useful to understanding its

operating results without the impact of special items. See Manitex’s

Second Quarter 2011 Earnings Release on the Investor Relations section of our

website www.manitexinternational.com

for a description and/or reconciliation of these measures.

|

3

“Focused

manufacturer of

engineered lifting

equipment”

Second Quarter 2011 Summary

•

Performance ahead of expectations

–

Sales of $37.1 million

•

Total sales increase of $17.6 million or 90%

•

Underlying sales increase of 38.5%

–

Net income of $1.0 million or $0.09 per share

•

Increase in backlog to $51 million

•

Significant operational foundations put in place

–

CVS asset acquisition completed

–

Revolving credit facilities maturity extended with 4 year deal,

increased availability and lower interest costs |

4

“Focused

manufacturer of

engineered lifting

equipment”

Commercial Update

Excluding the recent world stock market declines:

•Markets have remained steady

–

US markets stable, recovery based on a few specific sectors, no significant

broad based construction demand increase

–

International markets more strength in demand, project or sector

driven

–

Energy sector continues to be strongest demand sector in US, Canada and

internationally, leading to demand for a range of Manitex products, but

especially larger tonnage boom truck cranes –

Container handling activity increasing

–

Market pricing showing incremental increase for 2 half of

year and 2011. We have implemented increases of 0% -

8% varying by product

•Product

demand

still

focused

on

higher

tonnage

units

or

industry

specific

product

(e.g.

railways). Military and governmental demand currently weaker than at this stage

of 2010 –

Boom truck market tracking to annualized growth of 114%, 131% in

our categories, but still 40% behind 2007

–

Non-US sales account for 41% of year to date revenues (2010 = 38%)

–

Announced in July, 2 new military customers placed orders for $1.9

million •CVS Ferrari

–

We believe commercial prospects will strengthen with transition to ownership

from rental –

$3.1 million of orders announced for Brazilian ports marking return to a key

market •Backlog of $51 million, increase of 27% from

12/31/2010 nd |

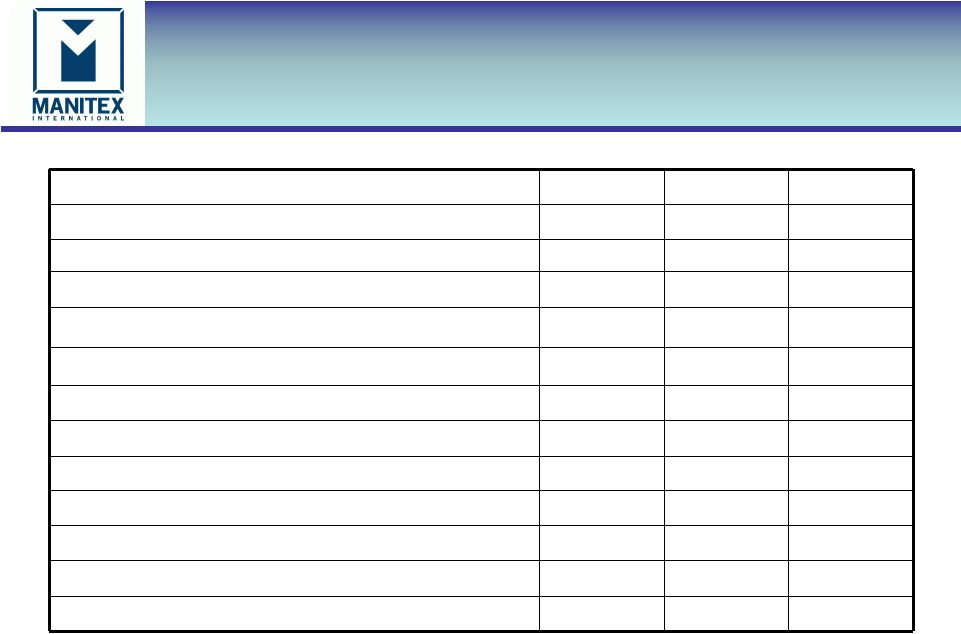

5

Investment Highlights

“Focused

manufacturer of

engineered lifting

equipment”

USD thousands

Q2-2011

Q2-2010

Q1-2011

Net sales

$37,066

$19,502

$31,722

% change in Q2-2011 to prior period

90.1%

16.8%

Gross profit

7,478

4,607

6,459

Gross margin %

20.2%

23.6%

20.4%

Operating expenses

5,237

3,658

5,207

Net Income

1,029

213

442

Ebitda

3,042

1,732

2,055

Ebitda % of Sales

8.2%

8.9%

6.5%

Working capital

38,892

29,276

33,829

Current ratio

2.4

2.9

2.3

Backlog

50,688

24,926

47,736

% change in Q2-2011 to prior period

103%

6.2% |

6

“Focused

manufacturer of

engineered lifting

equipment”

Q2-2011 Operating Performance

$000

$000

Q2-2010 Net income

213

Gross

profit

impact

of

increased

sales

of

$17.6

million

(Q2-

2011 sales less Q2-2010 sales at Q2-2010 gross profit % )

4,145

Impact

from

reduced

margin

(Q2-2011

gross

profit

%

-

Q2-2010

gross

profit % multiplied by Q2-2011 sales)

(1,274)

Increase in gross profit

2,871

Increase in operating expenses (including new operations

expenses of $1.1 million, selling $0.3m and other, including

personnel $0.2)

(1,579)

Interest & Other income / (expense)

6

Increase in tax

(482)

Q2-2011 Net income

$ 1,029 |

7

Working Capital

“Focused

manufacturer of

engineered lifting

equipment”

$000

Q2-2011

Q4 2010

Q2 2010

Working Capital

$38,892

$31,692

$29,276

Days sales outstanding

56

60

69

Days payable outstanding

54

62

57

Inventory turns

3.1

2.9

2.2

Current ratio

2.4

2.4

2.9

Operating working capital

45,070

36,763

32,313

Operating working capital % of

annualized LQS

30.4%

31.1%

41.4%

•Major movements in working capital increase Q2-2011 v Q4-2010 of

$7.2m •Receivables ($3.3m), inventory ($7.3m), offset by

increased short term notes ($1.9m) and increased accounts payable

($2.3m) •Inventory increase v Q4-2010 principally Manitex

cranes and CVS •Current ratio, DSO & DPO remain strong

through growth phase •Operating working capital % improvement

maintained through revenue growth |

8

“Focused

manufacturer of

engineered lifting

equipment”

$000

Q2-2011

Q4-2010

Q2-2010

Total Cash

979

662

1,485

Total Debt

39,699

34,019

34,955

Total Equity

45,102

43,274

41,049

Net capitalization

83,822

76,631

74,519

Net debt / capitalization

46.2%

43.5%

44.9%

YTD EBITDA

5,097

8,676

1,732

YTD EBITDA % of sales

7.4%

9.0%

8.9%

•EBITDA for Q2-2011 of $3.0m, 8.2% of sales

•Increase in debt from 12/31/2010 of $5.7m

•

Increase in lines of credit $4.8m

•

Long

term

debt:

CVS

acquisition

funding

$1.9m;

Payments

on

other

debt

($0.8m)

•N. American revolver facilities, based on available collateral at June 30,

2011 was $25.2m. Additional

transactional

facilities

of

$3.7m

in

place

subject

to

collateral

for

CVS.

•Cash and N. American revolver availability at June 30, 2011 $3.0m

Debt & Liquidity

•

Net capitalization is the sum of debt plus equity minus cash

•

Net debt is total debt less cash |

9

Summary

“Focused

manufacturer of

engineered lifting

equipment”

•

Strong Q2 performance in sales, net income, EPS and EBITDA

•

Markets stable, CVS transaction complete and growth in backlog

provides good visibility for H2-2011

•

Expect 2011 sales growth v 2010 of approximately 46% to

$140m, subject to no dramatic changes to overall economic

environment |