Attached files

| file | filename |

|---|---|

| 8-K - 8-K - Enventis Corp | form8k.htm |

Exhibit 99.1

First Quarter 2011

Earnings Conference Call

May 3, 2011

NASDAQ: HTCO

“Safe Harbor” Statement

Information set forth in this presentation contains financial estimates

and other forward-looking statements that are subject to risks and

uncertainties; therefore, actual results might differ materially from such

statements, whether as a result of new information, future events or

otherwise. You are cautioned not to place undue reliance on these

forward-looking statements. A discussion of factors that may effect

future results is contained in HickoryTech’s filings with the Securities

and Exchange Commission. HickoryTech disclaims any obligation to

update and revise statements contained in this presentation based on

new information or otherwise. This presentation also contains certain

non-GAAP financial measures. Reconciliations of these non-GAAP

measures to the most directly comparable GAAP measures are

available in our presentation.

First Quarter 2011 Highlights

• Consolidated revenue totaled $38.6 million

– Fiber and data revenue grew 13%

– Equipment support services revenue up

20%

20%

– Broadband revenue grew 14%

– Surpassed 20,000 DSL subscribers

• Net debt position improved $10 M

• Focus on leveraging fiber network upgrades

and route expansion, pursuing business and

wholesale services growth

and route expansion, pursuing business and

wholesale services growth

Consolidated Revenue

Q1 ’11 compared to Q1 ’10

• Fiber and data revenue +13%

• Equipment sales -17%

• Equip. support services +20%

• Broadband revenue +14%

($ in Millions)

Quarterly Revenue

68% of Q1-11 revenue was from Business Sector & Broadband Services

Revenue Diversification

Q1 ’11 compared to Q1 ’10

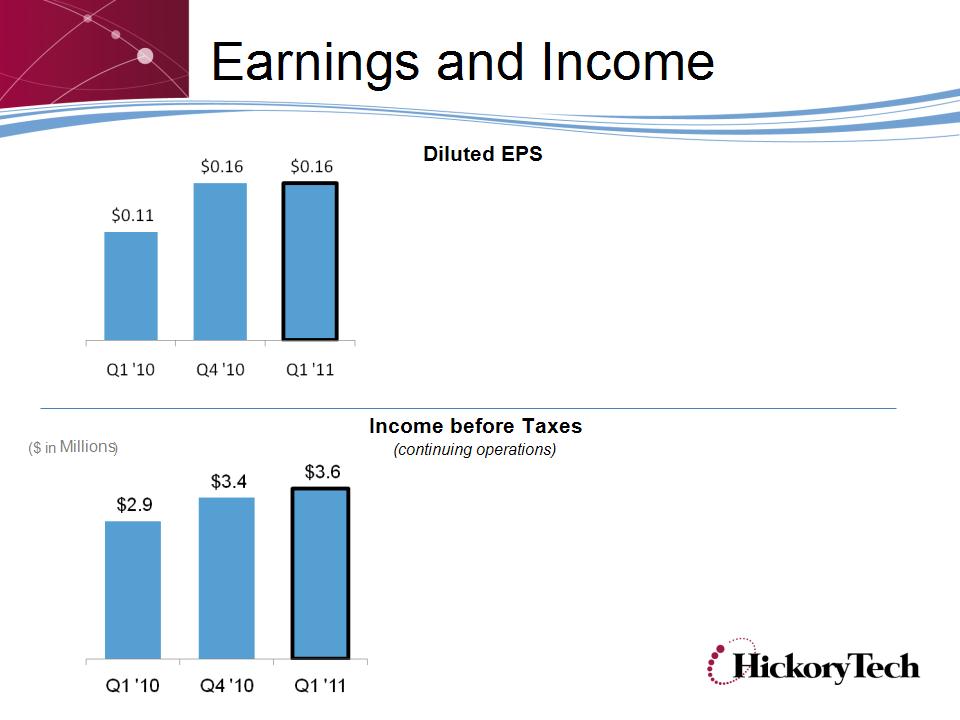

• Interest expense is 33% lower

• Q1-10 included $279,000 income tax

expense due to the 2010 Patient Protection

and Affordable Care Act and Health Care

and Education Reconciliation Act

Q1 ’11 compared to Q1 ’10

• Interest expense 33%

• Strong fiber and data sales and

equipment support services positively

impacted income

equipment support services positively

impacted income

Business Sector

• Fiber construction project (Dakotas expansion)

added $0.6 M in Q4 ‘10

added $0.6 M in Q4 ‘10

• Steady wholesale services growth;

SMB and enterprise market expansion

SMB and enterprise market expansion

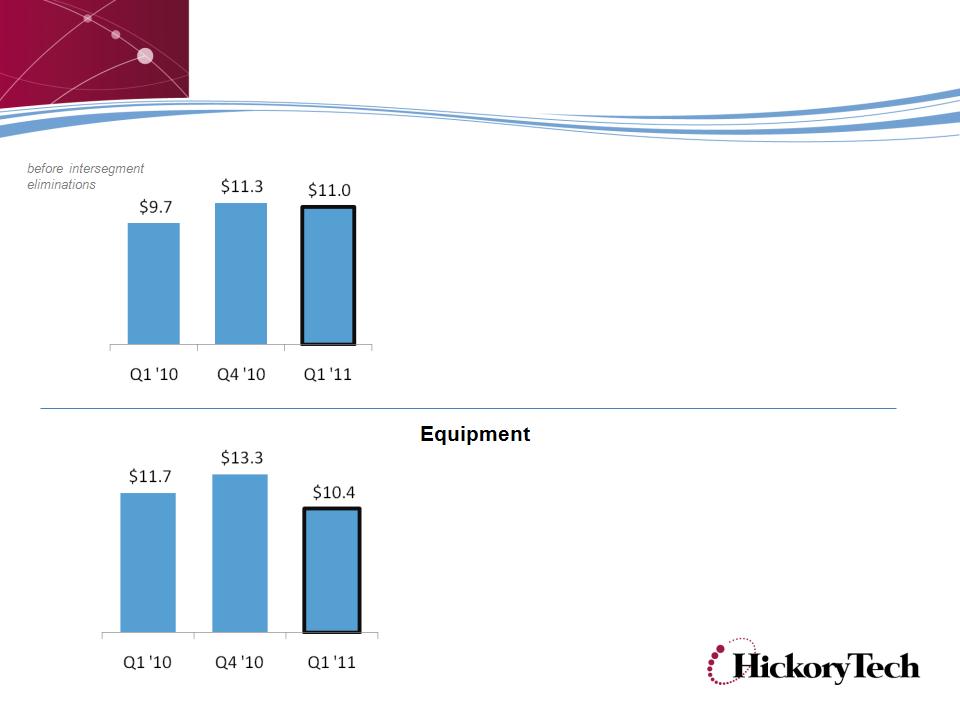

Q1 ’11 compared to Q1 ’10

• Equipment sales down 17%,

fluctuate on a quarterly basis

fluctuate on a quarterly basis

• Support services up 20%

• Continued profitability within product line

($ in Millions)

Fiber and Data

Formerly referred to as “Enventis Sector”

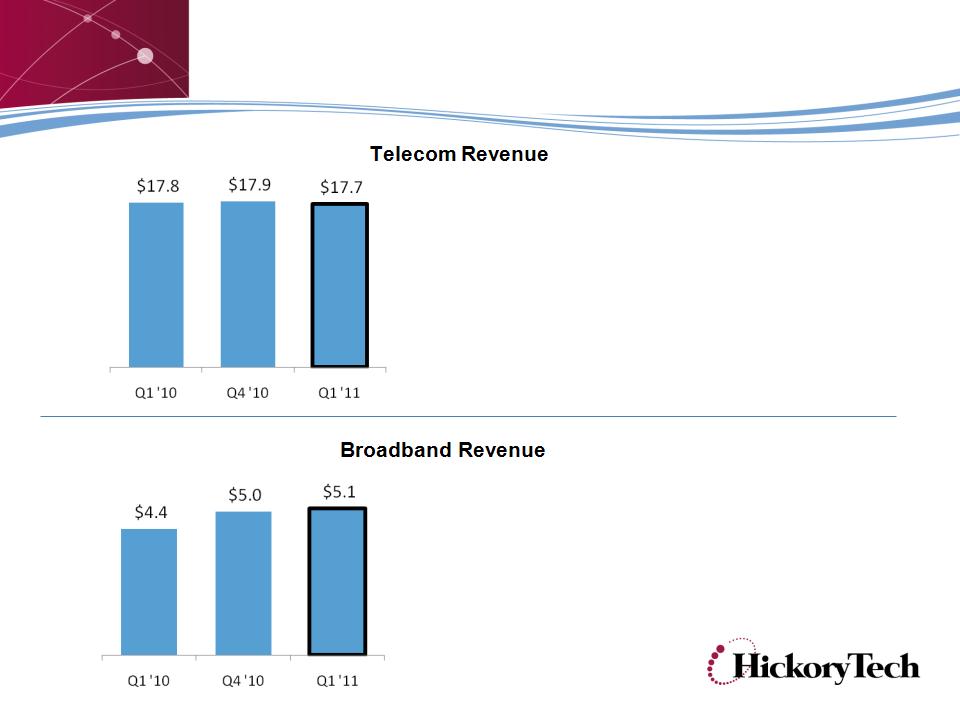

Telecom Sector

• Broadband revenue up 14%

• Network Access revenue down 5% and

Local Service revenue down 4%

Local Service revenue down 4%

• Total costs and expenses down 1%

• Strong business Ethernet and data sales

• Digital TV subscribers +8%

• DSL subscribers exceeded 20,000

($ in Millions)

before intersegment

eliminations

eliminations

Debt Balance

• Net debt was $108.9 M,

down $10 M from 12/31/10

down $10 M from 12/31/10

• Lower intra-quarter borrowing

and interest rates in 2011

contributing to 33% reduction in

interest expense

and interest rates in 2011

contributing to 33% reduction in

interest expense

• New senior debt agreement

expected by Q3-11

expected by Q3-11

Continued debt improvement

2011 Fiscal Outlook

2011 guidance provided in fourth quarter 2010 earnings release issued Feb. 28, 2011.

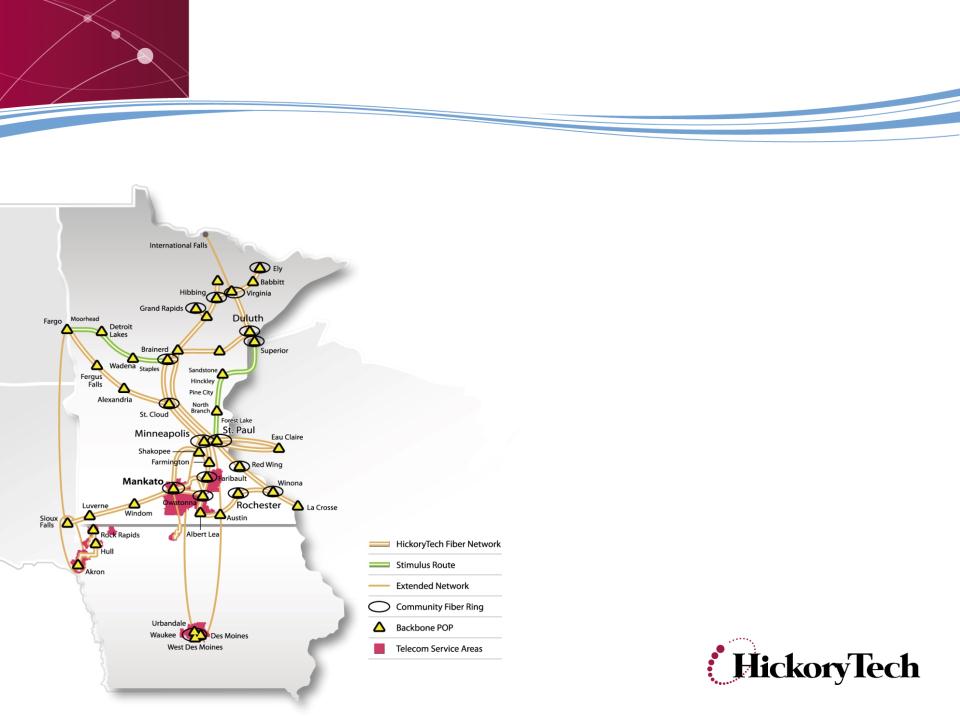

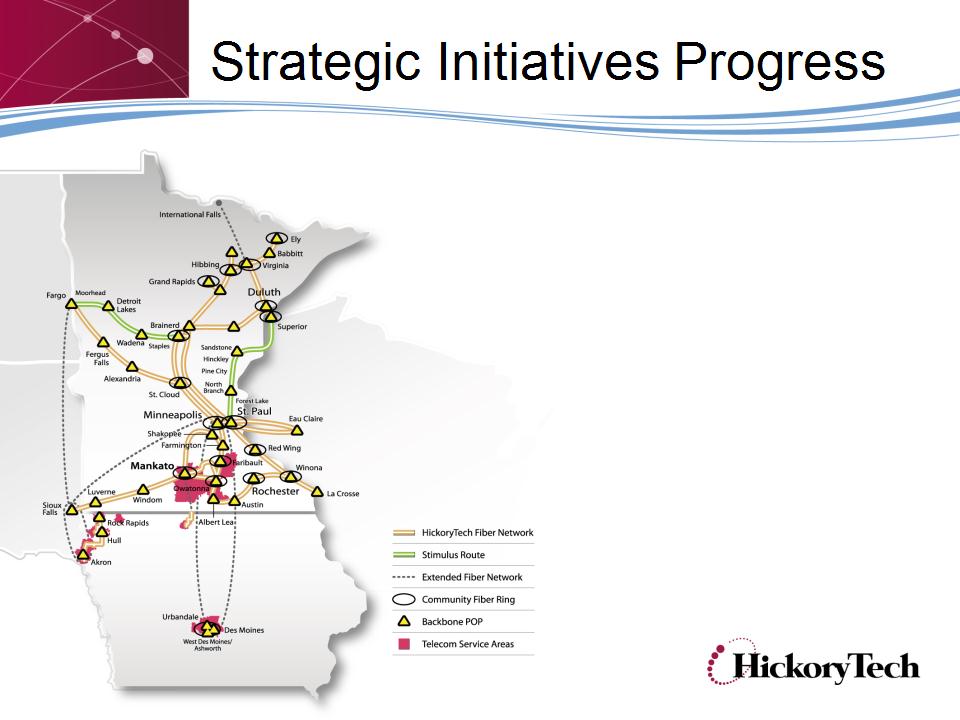

Recent Network Expansion

• Extended fiber network to Sioux Falls, So.

Dakota and Fargo, No. Dakota

Dakota and Fargo, No. Dakota

• Increased network capacity between

Minnesota and Des Moines, Iowa, added

local fiber network in Des Moines, Iowa

Minnesota and Des Moines, Iowa, added

local fiber network in Des Moines, Iowa

• Added network collocations to expand

Mid-band Ethernet services.

Mid-band Ethernet services.

• Secured Broadband stimulus grant, network

expansion plans in progress

expansion plans in progress

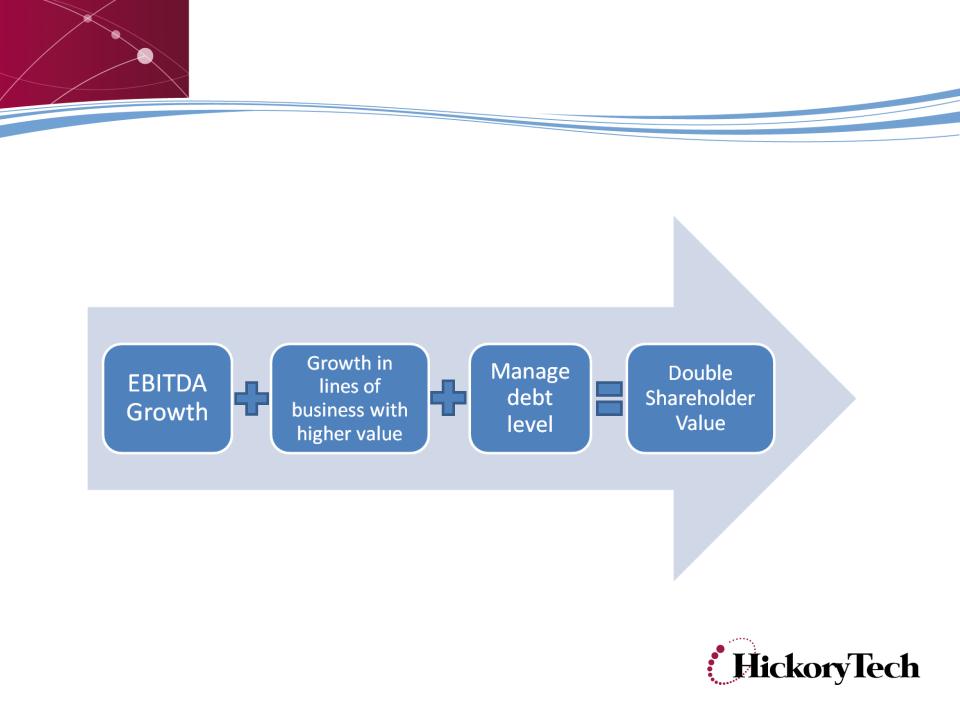

Five-Year Growth Goal

Our Goal: Double HickoryTech’s value by 2014

By way of example using 2009 EBITDA of $40 M and approximately $120 M of

debt, HickoryTech hypothetical shareholder value in 2009 was approximately $170 M.

By way of example using 2009 EBITDA of $40 M and approximately $120 M of

debt, HickoryTech hypothetical shareholder value in 2009 was approximately $170 M.

Our goal is to double shareholder value by the end of 2014 by growing EBITDA,

driving growth in lines of business with higher value and management of our debt

level.

driving growth in lines of business with higher value and management of our debt

level.

This should not be construed as guidance.

Strategic Initiatives

• Focus on growing business services:

Ø Fiber network expansion

Ø Accelerated SMB market plan

Ø Pursue fiber builds to wireless towers

Ø Target last-mile fiber builds

Ø Construction of broadband stimulus project

• Grow broadband services and focus on customer retention

• Increase capital spending on key strategic initiatives

• Manage free cash flow, manage costs and reduce debt in long term

Goal: double the value of HickoryTech over five years

HTCO Investment Highlights

• Stable growth and cash flows; 60+ years of dividend payments,

yield approximately 5-6%

yield approximately 5-6%

• Business transformation from a pure telephone company to an

integrated communications company serving businesses and

consumers

integrated communications company serving businesses and

consumers

• Emerging growth through B2B strategy and fiber network expansion

• High level of recurring revenue, dominant consumer market share,

expanded broadband service area

expanded broadband service area

• Experienced Company with 112-year track record generating

stable operating results and financial position with strong strategic

plan

stable operating results and financial position with strong strategic

plan

Appendix

Reconciliation of Non-GAAP Measures