Attached files

| file | filename |

|---|---|

| EX-31.2 - Trunkbow International Holdings Ltd | v216362_ex31-2.htm |

| EX-32.2 - Trunkbow International Holdings Ltd | v216362_ex32-2.htm |

| EX-32.1 - Trunkbow International Holdings Ltd | v216362_ex32-1.htm |

| EX-31.1 - Trunkbow International Holdings Ltd | v216362_ex31-1.htm |

U.S. SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(MARK ONE)

|

x

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the Fiscal Year Ended December 31, 2010

OR

|

¨

|

TRANSITION REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the Transition Period from _______________ to _________________

Commission file number: 000-53934

TRUNKBOW INTERNATIONAL HOLDINGS LIMITED

(Exact name of Registrant as Specified in Its Charter)

|

NEVADA

|

26-3552213

|

|

|

(State or Other Jurisdiction

|

(I.R.S. Employer Identification No.)

|

|

|

of Incorporation or Organization)

|

||

|

Unit 1217-1218, 12F of Tower B, Gemdale Plaza,

No. 91 Jianguo Road Chaoyang District, Beijing,

People’s Republic of China

|

|

100022

|

|

(Address of principal executive offices)

|

(Zip Code)

|

Registrant’s telephone number, including area code:

(86) 10-8571-2518

Securities Registered Pursuant To Section 12 (B) Of The Act:

Common Stock, Par Value $0.001 Per Share

Securities Registered Pursuant To Section 12 (G) Of The Act:

Common Stock, Par Value $0.001 Per Share

Name of each exchange on which registered: The NASDAQ Stock Market LLC

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ¨ Yes x No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ¨ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes £ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes £ No £

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. £

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated

filer £

|

Accelerated

filer £

|

Non-accelerated filer £

(Do not check if a smaller reporting company)

|

Smaller reporting

company x

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes £ No x

The aggregate market value of the shares of common stock, par value $0.001 per share, of the registrant held by non-affiliates on June 30, 2010 was zero.

There were 36,507,075 shares of common stock of the registrant outstanding as of March 29, 2011.

TABLE OF CONTENTS

|

PART I

|

2

|

|

|

Item 1

|

Business

|

2

|

|

Item 1A.

|

Risk Factors

|

18

|

|

Item 1B.

|

Unresolved Staff Comments

|

32

|

|

Item 2

|

Properties.

|

32

|

|

Item 3

|

Legal Proceedings

|

32

|

|

PART II

|

33

|

|

|

Item 5

|

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

|

33

|

|

Item 6

|

Selected Financial Data

|

34

|

|

Item 7

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

34

|

|

Item 8

|

Financial Statements and Supplementary Financial Data

|

43

|

|

Item 9

|

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure.

|

43

|

|

Item 9A.

|

Controls and Procedures

|

43

|

|

Item 9B.

|

Other Information

|

44

|

|

PART III

|

45

|

|

|

Item 10

|

Directors, Executive Officers and Corporate Governance

|

45

|

|

Item 11

|

Executive Compensation

|

50

|

|

Item 12

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters.

|

51

|

|

Item 13

|

Certain Relationships and Related Transactions and Director Independence

|

53

|

|

Item 14

|

Principal Accounting Fees and Services.

|

54

|

|

PART IV

|

55

|

|

|

Item 15

|

EXHIBITS AND FINANCIAL STATEMENT SCHEDULES

|

55

|

i

INTRODUCTORY NOTE

Except as otherwise indicated by the context, references in this Annual Report on Form 10-K (this “Form 10-K”) to the “Company,” “Trunkbow,” “we,” “us” or “our” are references to the combined business of Trunkbow International Holdings Limited and its consolidated subsidiaries. References to “Trunkbow BVI” are references to our wholly-owned subsidiary, Trunkbow International Holdings Ltd., a BVI company; references to “Trunkbow Hong Kong” are references to our wholly-owned subsidiary, Trunkbow (Asia Pacific) Investment Holdings Limited, a Hong Kong company; references to “Trunkbow Shandong” are to our wholly-owned subsidiary, Trunkbow Asia Pacific (Shandong) Company, Limited, a PRC wholly foreign owned enterprise; references to “Trunkbow Shenzhen” are to our wholly-owned subsidiary, Trunkbow Asia Pacific (Shenzhen) Company, Limited, a PRC wholly foreign owned enterprise; references to “Trunkbow Technologies” are to our contractually controlled entity, Trunkbow Technologies (Shenzhen) Company, Limited; and refrences to “Delixunda” are to Beijing Delixunda Technology Co., Ltd., our contractually controlled entity. References to “China” or “PRC” are references to the People’s Republic of China. References to “RMB” are to Renminbi, the legal currency of China, and all references to “$” and dollar are to the U.S. dollar, the legal currency of the United States.

Special Note Regarding Forward-Looking Statements

This report contains forward-looking statements and information relating to Trunkbow International Holdings Limited that are based on the beliefs of our management as well as assumptions made by and information currently available to us. Such statements should not be unduly relied upon. When used in this From 10-K, forward-looking statements include, but are not limited to, the words “anticipate,” “believe,” “estimate,” “expect,” “intend,” “plan” and similar expressions, as well as statements regarding new and existing products, technologies and opportunities, statements regarding market and industry segment growth and demand and acceptance of new and existing products, any projections of sales, earnings, revenue, margins or other financial items, any statements of the plans, strategies and objectives of management for future operations, any statements regarding future economic conditions or performance, uncertainties related to conducting business in China, any statements of belief or intention, and any statements or assumptions underlying any of the foregoing. These statements reflect our current view concerning future events and are subject to risks, uncertainties and assumptions. There are important factors that could cause actual results to vary materially from those described in this Form 10-K as anticipated, estimated or expected, including, but not limited to: competition in the industry in which we operate and the impact of such competition on pricing, revenues and margins, volatility in the securities market due to the general economic downturn; Securities and Exchange Commission (the “SEC”) regulations which affect trading in the securities of “penny stocks,” and other risks and uncertainties. Except as required by law, we assume no obligation to update any forward-looking statements publicly, or to update the reasons actual results could differ materially from those anticipated in any forward- looking statements, even if new information becomes available in the future. Depending on the market for our stock and other conditional tests, a specific safe harbor under the Private Securities Litigation Reform Act of 1995 may be available. Notwithstanding the above, Section 27A of the Securities Act of 1933, as amended (the “Securities Act”) and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) expressly state that the safe harbor for forward-looking statements does not apply to companies that issue penny stock. Because we may from time to time be considered to be an issuer of penny stock, the safe harbor for forward-looking statements may not apply to us at certain times.

1

PART I

|

Item 1.

|

Business.

|

Company Background

Our History and Corporate Structure

Prior to the share exchange transaction described below (the “Share Exchange”), we were a “shell” company with nominal assets organized under the name Bay Peak 5 Acquisition Corp. (“BP5”). We were incorporated in the State of Nevada on September 3, 2004 as a wholly owned subsidiary of Visitalk Capital Corporation (“VCC”). The Company was formed as part of the implementation of the Chapter 11 reorganization plan (the “Visitalk Plan”) of visitalk.com, Inc. (“Visitalk.com”), a former provider of VOIP services. The Visitalk Plan was deemed effective by the Bankruptcy Court on September 17, 2004 (the “Effective Date”). On September 22, 2004, Visitalk.com was merged into VCC, which was authorized as the reorganized debtor under the Visitalk Plan.

On July 28, 2008, pursuant to Stock Purchase Agreements (“SPAs”), we sold 5,971,898 shares of common stock to two parties unaffiliated with us (the “Purchasing Shareholders”) for a total payment of $51,000, or approximately $.008 per share (the “Change of Control Transactions”). On August 29, 2008, the SPAs were approved by our shareholders at a special shareholders’ meeting and all the closing conditions of the SPAs were met. After the Change of Control Transactions, including the impact of a related master settlement agreement, these newly issued shares represented 85.5% ownership of us. One of the parties, Bay Peak, LLC (“Bay Peak”), had contacts with various companies and individuals in Asia, in particular the PRC. Cory Roberts, the managing member of Bay Peak, was appointed to our Board of Directors and elected President in conjunction with the Change of Control Transactions. Mr. Roberts resigned as a member of our Board of Directors on March 30, 2011. On August 28, 2008, shareholders authorized adopting the name of Bay Peak 5 Acquisition Corp. Also on August 28, 2008, shareholders ratified a one-for-seven reverse stock split, which was implemented on January 6, 2010 and in January 2010, authorized a further reverse split of 4.14 for 1, which was implemented on January 27, 2010.

Effective as of September 24, 2008, we entered into a Plan and Agreement of Merger (the “Plan and Agreement of Merger”) with VT Dutch Services, also a subsidiary of VCC, pursuant to which VT Dutch Services merged with and into us. Pursuant to the merger, holders of shares of common stock of VT Dutch Services received the identical number and class of our stock as they held in VT Dutch Services, and holders of warrants of VT Dutch Services received the identical number and class of our warrants as they held in VT Dutch Services. In connection with the Plan and Agreement of Merger, VT Dutch Services also changed its name to “Bay Peak 5 Acquisition Corp.” All shares of common stock of BP5 held prior to the consummation of the transactions contemplated by the Plan and Agreement of Merger were cancelled. The sole purpose of the merger was to change the corporate domicile of VT Dutch Services from Arizona to Nevada and to effect a name change of VT Dutch Services.

In February 2010 we entered into the Share Exchange Agreement with Trunkbow BVI and the shareholders of Trunkbow BVI (the “Shareholders”), who together owned shares constituting 100% of the issued and outstanding ordinary shares of Trunkbow BVI (the “Trunkbow BVI Shares”), and Bay Peak, our former principal shareholder. Pursuant to the terms of the Share Exchange Agreement, the Shareholders transferred to us all of the Trunkbow BVI Shares in exchange for the issuance of 19,562,888 shares of our common stock (the “Share Exchange”). As a result of the Share Exchange, Trunkbow BVI became our wholly owned subsidiary. After giving effect to the Share Exchange, the sale of common stock in the February 2010 Offering (as defined below) and the BP5 Warrant Financing (as defined below) (i) existing shareholders of Trunkbow BVI owned approximately 60.25% of our outstanding common stock, (ii) purchasers of common stock in the February 2010 Offering owned approximately 26.01% of our outstanding common stock (including 7.7% owned by VeriFone, Inc.), (iii) the holders of BP5 warrants owned approximately 8.54% of our outstanding common stock and (iv) the pre-existing shareholders of BP5 owned approximately 5.2% of our outstanding common stock.

2

Concurrent with the Share Exchange, (i) we entered into a securities purchase agreement (the “Purchase Agreement”) with certain investors (the “Investors”) for the sale of an aggregate of 8,447,575 shares (the “Investor Shares”) and 1,689,515 warrants (the “Investor Warrants”), for aggregate gross proceeds equal to $16,895,150 (the “February 2010 Offering”) and (ii) certain holders of our outstanding warrants issued to creditors and claimants of Visitalk.com, in accordance with the Visitalk Plan, referred to herein as the “BP5 Warrant Investors” exercised the 2,774,500 warrants owned by them for an aggregate exercise price of $5.5 million and received warrants to purchase an aggregate of 554,900 shares of common stock (“BP5 Warrant Financing”).

Following the Share Exchange, we are a leading provider of technology platform solutions for mobile telecom operators in the People’s Republic of China. Our patented platforms provide a comprehensive solution for Chinese telecom operators to deliver and manage the distribution of various mobile value-added service (“MVAS”) applications to their subscribers. The Trunkbow brand is regarded by Chinese telecom operators as a well managed, trusted provider of technology solutions. Our R&D focused business model provides us with a defensible market position as a technology solutions provider to the telecom operators.

Trunkbow was founded in 2001 by former Silicon Valley engineers with extensive experience in the telecom industry. We have been able to develop first to market application platforms that enable telecom operators to generate significant new revenue streams by leveraging our extensive knowledge of the mobile network technology. Since our inception, we have invested significant time and resources to develop cutting edge technology solutions for our customers. We were the first to create and develop a Color Ring Back Tone (“CRBT”) application platform for Shandong Unicom in 2003. Since then, this innovative service solution has become the third largest revenue contributor for China Mobile after voice and Short Message Service (“SMS”).

We believe that we have a competitive advantage over our primary competitors by our proven track record of innovation. We believe Chinese telecom operators continue to utilize our technology platforms because of our superior technological solutions and unique product offerings.

On February 8, 2011 we consummated our initial public offering of 4 million shares of our common stock.

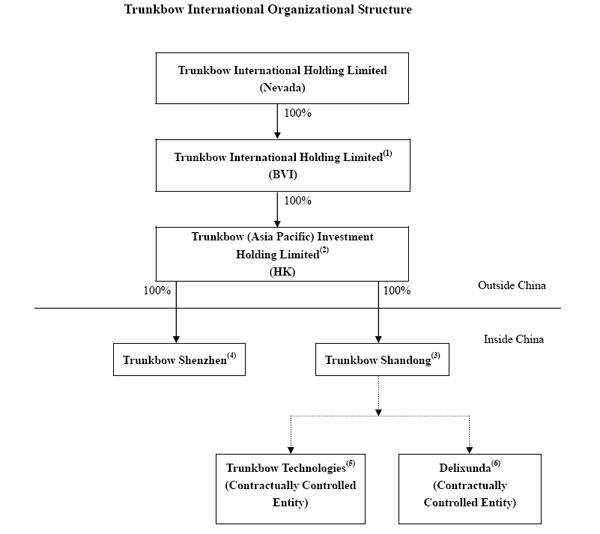

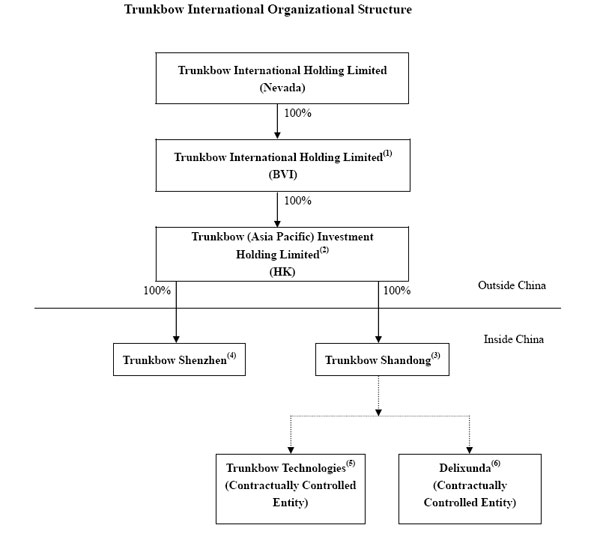

Corporate Structure

Our current corporate structure is set forth below:

3

|

(1)

|

Trunkbow International Holdings Limited (“Trunkbow BVI”) was established in the British Virgin Islands (“BVI”) on July 17, 2009. Trunkbow BVI itself has no significant business operations and assets other than holding of equity interests in its subsidiaries through a series of reorganization activities described below (the “Reorganization”).

|

|

(2)

|

Trunkbow (Asia Pacific) Investment Holdings Limited (“Trunkbow Hong Kong”) was established as an Investment Holding Company in Hong Kong Special Administrative Region of the People’s Republic of China (the “PRC”) on July 9, 2004. As part of the reorganization, on September 16, 2009, the entire issued share capital Trunkbow Hong Kong was transferred to Trunkbow BVI.

|

|

(3)

|

Trunkbow Asia Pacific (Shandong) Company, Limited (“Trunkbow Shandong”) was established as a wholly foreign owned enterprise on December 10, 2007 in Jinan, Shandong Province, the PRC by Trunkbow Hong Kong. It is principally engaged in research and development of application platforms for mobile operators in the PRC.

|

|

(4)

|

Trunkbow Asia Pacific (Shenzhen) Company, Limited (“Trunkbow Shenzhen”) was established as a wholly foreign owned enterprise on June 7, 2007 in Shenzhen, Guangdong Province, the PRC by Trunkbow Hong Kong. It is principally engaged in research and development of application platforms for mobile operators in the PRC.

|

|

(5)

|

Trunkbow Technologies (Shenzhen) Company, Limited (“Trunkbow Technologies”) was established as a limited liability company on December 4, 2001 in Shenzhen, Guangdong Province, the PRC. Trunkbow Technologies was formerly engaged in research and development of application platforms for mobile operators in China as well as wireless application systems for the international market. Trunkbow Technologies no longer accounts for any of our new business, currently represents less than 10% of our current revenues and is being operationally wound down.

|

|

(6)

|

We entered into a series of contractual arrangements with Beijing Delixunda Technology Co., Ltd. (“Delixunda”) and its shareholders on March 10, 2011. Delixunda is a telecom value-added service licensed company and was established as a limited liability company on December 1, 2009 in Beijing, the PRC. Delixunda had no operations prior to February 10, 2011. As a result of the contractual arrangements with Delixunda, we indirectly own the telecom value-added service license, which would enable us to offer telecom wireless value-added content service to individual clients.

|

4

Business Overview

We are an innovative mobile application enabler, offering telecom operators in China application platforms on which to offer Mobile Value Added Solutions (“MVAS”) to subscribers. We enable telecom operators to offer their subscribers access to unique mobile applications, innovative tools, value-added services and an overall superior mobile experience. In doing so, we add value to our clients by helping them increase their average revenue per user and decrease subscriber churn. We develop and implement a range of comprehensive platform solutions for our customers that enable MVAS applications for their subscribers. As a technology enabler, our solutions may be generally classified into two categories: MVAS Technology Platforms and Mobile Payment Solutions. We provide both hardware and software solutions that are integrated into our clients’ existing IT infrastructure. We also offer additional services including technical support and system maintenance for our clients.

We currently have significant market presence in the Chinese MVAS and Mobile Payment markets, as evidenced by our contracts with local branches of China Mobile, China Telecom and China Unicom, the “Big Three” Chinese cellular carriers, or resellers who themselves have such contracts. Combined, these contracts span 10 of 30 provinces, municipalities and autonomous regions and represent a significant portion of the geographic market based on the location of the mobile subscriber base in the PRC. Our patented platforms provide a comprehensive solution for Chinese telecom operators to deliver and manage the distribution of MVAS applications to their subscribers. We believe that the expansion of our platforms and services deployment to the Big Three over the past ten years shows that the Trunkbow brand is regarded by these major Chinese telecom operators as a well managed, trusted provider of technology solutions. Our R&D-focused business model provides us with a defensible market position as a technology solutions provider to the telecom operators.

Developing innovative technology solutions is at the core of our business model. We work extensively with our customers and technology partners in our R&D process to develop cutting edge technology solutions that are relevant to consumer trends and market demand. We have a team of over 100 R&D professionals led by a seasoned senior management team with extensive experience in the telecom industry. Our technology is the subject of 164 filed patent applications, of which 50 have been granted by the National Intellectual Property Administration of the People’s Republic of China. We have recently begun the process of filing for international and U.S. patents in order to protect our intellectual property globally.

Our customers are primarily telecom service providers in the PRC. We have extensive customer relationships with provincial branches of all three of the mobile service providers in China, specifically, China Telecom, China Unicom and China Mobile. The table below shows our revenues generated from direct sales to each of the Big Three, as well as resales of our products to these carriers through intermediaries (i.e., direct and indirect sales to these carriers), for the fiscal years ended December 31, 2010 and 2009.

|

December 31,

|

||||||||

|

|

2010

|

2009

|

||||||

|

Percent of revenues from direct sales to China Telecom

|

7 | 3 | ||||||

|

Percent of revenues from direct sales to China Unicom

|

5 | 6 | ||||||

|

Percent of revenues from direct sales to China Mobile

|

— | — | ||||||

|

Percent of revenues from direct and indirect sales to China Telecom through resellers

|

16 | 42 | ||||||

|

Percent of revenues from direct and indirect sales to China Unicom through resellers

|

47 | 15 | ||||||

|

Percent of revenues from direct and indirect sales to China Mobile through resellers

|

20 | 42 | ||||||

5

The resellers with whom we contract offer value-added services to the carriers, including installation support, hardware sourcing and an established presence and reputation, and they assist us by providing a known quantity aspect to the carrier when doing business with Trunkbow. In addition, once a project is completed, Trunkbow may further rely on these resellers for ongoing maintenance support. We have worked with our resellers for periods between one and five years.

The significant increase in revenues generated from sales to China Mobile for 2009 as compared to 2008 is attributable to the sale in 2009 of two platforms to two resellers that provided an air-charge system to China Mobile in two provinces. The large variations in revenues attributable to China Unicom and China Mobile during 2008 and 2009 are mainly attributable to a reorganization of China Unicom which resulted in that company’s CDMA segment being spun-off into China Telecom and the remaining company being merged with China Netcom. The significant increase in revenues generated from sales to China Unicom for 2010 as compared to 2009 is contributed from the sale in 2010 of the deployment of our systems including Caller CRBT, Color Numbering, Mobile Business Card and Mobile Payment.

We have also entered into a strategic partnership with China UnionPay in order to provide clearing house functions for our Mobile Payment Solutions.

Our relationship with each of the Big Three commences upon the application for, and receipt of, a form of approved vendor certification by the central corporate authority of the relevant Big Three. Following this approval, from time to time we enter into purchase agreements, typically with resellers, who then contract directly with the provincial branches of the Big Three to sell them our equipment, system integration, software licenses and maintenance services. Under the arrangements, we supply the equipment to match the particular specifications set forth in the purchase order, install and integrate the patented software with the hardware and software purchased from third-party suppliers and offer the non-exclusive license of our software and technical support. These contracts generally follow an accepted standard form in the industry and obligate the parties to cooperate to ensure a successful implementation and technology roll-out including testing and remediation requirements, provide for the relevant sharing of revenue received from the mobile subscriber and terms of such payments, contain representations regarding the intellectual property contained in the technology involved and dispute resolution provisions, among other typical provisions for this type of agreement. Our typical form of sales contract or revenue sharing agreement with a reseller is not terminable at will by either party, while our standard mobile payment contracts with a given provincial branch of one of the Big Three allows for termination on written notice of at least two months. Our agreements with resellers typically contain mutually agreed upon sales goals for the resellers to meet that are based on the reseller’s best efforts. The mobile carriers pay us upon receipt and acceptance of the equipment or upon completion of the installation and integration of the software into their IT and networking infrastructure.

We have experienced strong revenue growth and profitability over the last two years driven by customer additions and the introduction of innovative products and services. Our revenues increased to $24.8 million in 2010 from $13.5 million in 2009 and net income to $13.5 million in 2010, from $8.3 million in 2009. Positive macro economic trends, strong consumer demand and our suite of unique platform solutions present us with the opportunity to expand sales rapidly and increase market share.

Our Strategy

Our goal is to become a leader in MVAS application platforms and mobile payment systems for the telecom industry in China. We intend to achieve this goal by implementing the following strategies:

Continue to develop cutting edge technology solutions. We intend to continue to commit significant financial and human resources for research and development purposes. We intend to continue to improve our development and pipeline process in order to introduce first to market technology solutions to our customers. We expect to further leverage the know-how from our custom-design and implementation process to develop and introduce new applications and solutions with higher profit margins for a wider market. We expect to continue to fund research at our research center and increase our collaboration with other research facilities.

6

Leverage our intellectual assets and enter into new markets. We intend to focus our R&D efforts on emerging industries and new market opportunities. We plan to expand our product lines by leveraging our domestic relationships as well as through co-operations with international players.

Expand geographic coverage of current platform solutions. We intend to expand the geographic coverage of our existing product portfolio. We expect to leverage our customer relationships in our current geographic coverage in order to expand into new provinces domestically and new markets globally. We believe our solutions, know-how and successful track record should facilitate our expansion into new and commercially attractive territories.

Continue to build upon our strong relationship with key customers. Our clients include major players in the telecom industry in China. With the rollout of 3G, we expect our clients to offer their customers progressively more sophisticated and captive mobile phone experience. This will require innovative technology solutions for new applications and functions. We intend to help our clients address this demand and continue to work closely with our customers in our development process to ensure that our pipeline is in line with their technology needs.

Attract and retain quality employees. To enhance our development efforts and to support our growth objectives, we intend to continue to attract additional skilled and experienced R&D personnel. We also intend to hire and retain additional sales and service personnel with client and industry knowledge. We expect to continue to build a strong management team with in-house talent and recruit additional management talent, beginning with a CFO with extensive industry and financial background. We plan to continue to leverage our research centers and external resources to provide training programs for our employees.

Form business relationships with strategic partners to expand our presence in the mobile payment business. The MVAS application platform and mobile payment markets are immature and somewhat fragmented. This provides us with the opportunity to assert ourselves and form strategic partnerships to shape the direction of the industry. We intend to enter into synergistic business relationships with key domestic and international players in the mobile payment industry. In February 2010 we entered into an engagement agreement with VeriFone, Inc., a global provider of point of sale payment systems and solutions. We hope to leverage our relationship with VeriFone to expand our market for our mobile payment solutions.

Our Competitive Strengths

We believe the following strengths differentiate us from our competitors and enable us to attain a leadership position in the MVAS application platform and mobile payment markets in China:

“Approved Vendor” to the leading telecom and payment industry participants in the PRC. We have passed a rigorous supplier approval process to become an “approved vendor” to each of the three major telecom providers in the PRC: China Mobile, China Telecom and China Unicom, the “Big Three”. We have entered into business relationships with the provincial branches of the Big Three in 10 provinces in order to better customize their specific application solution needs. Our relationships with market leaders in the PRC telecom industry provide us with reputation, industry knowledge, operational expertise and credibility that we can leverage in marketing to other market participants. As our clients generally prefer to maintain continuity and compatibility among their various systems, we believe our existing relationships favorably position us for selection to address our clients’ future technology needs. We further believe that our continued client relationships allow us to build client trust, anticipate their information technology needs and allow us to better direct our research and development efforts and effectively market to them our solutions and services. Beginning in 2007, we established a business and indirect contractual relationship with China UnionPay in order to develop and commercialize mobile payment solutions. Our relationship with UnionPay and the three telecom operators allows us to provide a comprehensive mobile payment solution that is fully back-end linked, meaning that due to its redundant hardware and communication links, it offers no single point of failure.

Integrated solutions and comprehensive service offerings. Since 2001, Trunkbow has deployed over 150 application service platforms in China. We offer an integrated and customized solution that integrates seamlessly into our clients’ existing IT and networking infrastructure. Additionally, we offer system integration, system management and maintenance services that provide us with multiple access points to our customers in order to build long term relationships.

7

Strong R&D capabilities. Our R&D efforts are led by Dr. Hou Wan Chun, Dr. An Chun Ming and Mr. Wang Xin. Dr. Hou is a telecom veteran with numerous telecom application patents. Dr. Hou previously worked for telecom companies like Lucent in the Silicon Valley as an engineer involved in developing new intelligent network applications. Our overall technical direction has been guided by Dr. An Chun Ming, the pioneer of Next Generation Network (“NGN”). Prior to joining Trunkbow, Dr. An led multiple development efforts as a Bell Labs Fellow during his 30 year tenure. Our experienced senior management team leads a group of over 100 R&D professionals with strong telecom and technical backgrounds.

The primary goal of our research efforts is to develop solutions that may be strategically implemented and commercialized. We are currently developing the next generation of mobile payment solutions and 3G applications. Our commitment to research and development and our focus on commercializing our research results will further enhance our competitive edge in the market with the ability to provide a broad range of quality solutions and the potential for sustained long-term growth.

Proven management team with successful track record. Our senior management team consists of telecom industry veterans and entrepreneurs with extensive management experience in the telecom industry. Our management team brings us complementary skills in the areas of R&D, operations, and sales and marketing. Under the leadership of our senior management team, we have substantially expanded our operations and product lines and achieved significant revenue growth.

Our Products and Services

We develop and implement MVAS Application Platforms and Mobile Payment System solutions for telecom operators. We work closely with the telecom operators to identify future application trends in order to develop new technologies to meet the changing needs and appetites of their subscribers. Once the applications have been developed, we typically work with the operators to integrate the system into their existing network. This is followed by a roll out of the service in trial service areas prior to nationwide deployment. We have a solid track record of developing popular application solutions that contribute significant new revenue streams for the telecom operators.

Mobile Value Added Service Application Platforms

We have built a sophisticated MVAS products pipeline and introduced first to market many MVAS application platforms to our customers for the past ten years. We will constantly improve our MVAS development and pipeline process to offer more innovative technology solutions for new applications and functions.

Caller Color Ring Back Tone. We provide a patented technology platform that enables the operator to offer Caller CRBT to the subscribers. Caller CRBT is an application that allows a caller to set the caller’s own personalized dialing tone when dialing out. The convention today with traditional CRBT is to hear the called party’s choice of dialing tones. The Caller CRBT application provides the subscriber with additional optionality in terms of customizing their mobile phone experience. This service has been deployed in two provinces with China Mobile, three provinces with China Telecom and two provinces with China Unicom, with a planned rollout to all major provinces with China Mobile, China Telecom and China Unicom.

Number Change Notification. Our Number Change Notification solution simplifies the process of switching between carriers for the subscriber. Since the Chinese mobile market does not offer subscribers the option of number portability, a subscriber typically has to subscribe to a new number when switching plans to a new carrier. Our solution enables the new carrier to put in place a voice notification when the old phone number is dialed, thus facilitating the process of changing carriers.

Color Numbering. Our Color Numbering solution enables mobile phone users to subscribe to multiple numbers in different regions with one SIM card and one phone without incurring roaming charges. Additional functionalities under this platform include solutions such as secretary services, fax, and SMS and call spam filtration.

New MVAS Roll-out

SMS-In / SMS-Out. Our SMS-In / SMS-Out MVAS application enables mobile phone users to send and receive short messages (SMS) from either their mobile device or via a computer based SMS client associated to their true mobile phone numbers. Similar to email, a user is able to send message to multiple recipients or send messages in batch and can refer/archive any message sent via this Trunkbow offering. Recipients have no indication that messages are sent from a computer instead of a cell phone. Senders use a full size keyboard which greatly eases the use of SMS.

Mobile Business Card. Our Mobile Business Card MVAS application enables mobile phone callers to send a predefined brief message to a called party. Examples of this brief message include business card content where address, phone, fax, various contact methods, a party invitation, event data or other personalized greetings information. The recipient receives that information much in much the same way he sees a caller name/ID.

8

Mobile Payment System

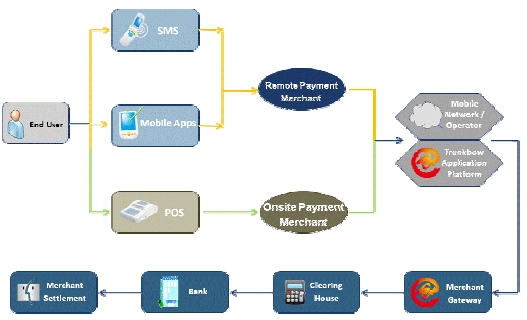

Trunkbow's patented technology platform supports remote mobile payment and contactless mobile payment via various Near Field Communication (NFC) or Radio Frequency ID (RFID) enabled mobile devices. Remote mobile payments are enabled through SMS and mobile phone applet. Contactless mobile payment technology allows NFC or RFID enabled mobile phones, worldwide, to be utilized as payment tools and authentication devices. Specifically, Trunkbow's solution enables the end-user to consolidate a variety of functions such as credit/debit cards, public transit cards, employee identification, facility entrance/exit and membership cards into one device and eliminates the need to carry numerous cards. Trunkbow provides users with access to real-time account information whenever they have access to mobile service. In addition, end users can utilize mobile phones or web interface to perform a variety of account maintenance functions including refilling of prepaid cards, user preferences and archiving transaction records.

Trunkbow uses proprietary technologies to seamlessly transmit secure transaction data between end users and the financial processing infrastructure. A proprietary software technology platform resides within the telecom operators’ network as well as the merchant clearing house network in order to seamlessly facilitate mobile payment transactions.

Diagram I – Mobile Payment Network

Other Products and Services

We also offer other technology solutions that enable value added functionalities on mobile devices. These solutions include missed call reminder, news flash services, roaming greeting, spam intercept and virtual PBX.

Our Revenue Model

We leverage our patented technology platforms to help telecom operators in China to increase their per subscriber revenue and reduce subscriber churn. We generate revenues through direct and indirect revenue sharing agreements with the relevant provincial branch of the telecom operators, one time service and product sales, and maintenance fees. We charge an upfront initial system licensing fee, and an annual maintenance fee of approximately 5 – 10% of the initial system purchasing amount. We also have monthly revenue sharing contracts in place with resellers and directly with the relevant provincial branch of the telecom providers for up to a 50% share in the revenue generated through our proprietary applications platforms. In addition to one-time sales and revenue sharing, we also generate revenue through transaction fees for our Mobile Payment System solution.

Our current MVAS Application Platform solutions generate revenue through one time sales and recurring revenues. For our Caller CRBT and Color Numbering solution, we have a revenue sharing agreements with telecom providers to receive 50% of the subscription revenues generated for up to 5 years and then renewable upon expiration. For our Number Change Notification solution, we receive revenues from one-time system sales and maintenance fees.

9

For our Mobile Payment System solution, we generate both one-time and recurring revenues. We generate non-recurring revenues in the following ways:

· System sales to telecom providers which enables the mobile payment function on their network

· System sales to telecom providers that enables various MPS compatible SIM and mobile payment functions for their corporate clients

· Revenue share on the MPS compatible SIM cards that are sold to the telecom provider

We generate recurring revenues in the following ways:

· Up to a 50% share of the monthly function fee charged by the telecom providers;

· A share of the transaction fee on purchases made through the mobile payment application

· Monthly rental revenues on POS (Point of Sales) machines deployed by Trunkbow

Table I – Summary of Our Revenue Model

|

Category

|

Product

|

Revenue Model

|

||

|

MVAS Platform

|

Caller Color Ring Back Tone (CRBT)

|

Revenue sharing at 50% for 5 years and renewable

|

||

|

Number Change Notification (NCN)

|

One time sales and 10% annual maintenance fees

|

|||

|

Color Numbering

|

Revenue sharing at 50% for 5 years and renewable

|

|||

|

Mobile Payment System

|

Mobile Payment System (MPS)

|

One time system sales to carriers and corporate clients, RMB 20 per MPS compatible SIM card, revenue sharing on function fee (up to 50%), and/or rental revenue on POS machines and transaction fees

|

Sales and Marketing

We sell our technology platform solutions through our direct sales force and through independent third-party resellers, including telecom operators and electronic payment processors. We also provide services through cooperative efforts with telecom operator affiliated entities as service partners in order to reduce our operating costs and ensure the successful execution of the contracts. These contracts are limited to one transaction and cover a varying number of years, although typically less than 5 years, with renewal provisions. Some contracts contain exclusivity provisions. Those contracts with revenue sharing terms provide that the telecom operators pay us following receipt of funds from subscriber, while those contracts that cover only one time sales allow for only a single payment to us.

Our sales and marketing personnel are based in offices located in six provinces with local coverage responsibilities in Shandong, Hebei, Zhejiang, Henan, Sichuan, Jilin, Xinjiang provinces and in Beijing. Our sales teams have local expertise and relationships to succeed in the fragmented Chinese market. Typically, each sales team includes a general manager, account representatives, business development personnel, sales engineers and customer service representatives with specific product expertise in mobile applications and mobile payment as well as financial transaction operations. Our sales force is supported by our R&D and client support teams in order to provide products and services that are tailored to the specific needs of our customers. We will focus our future sales and marketing efforts on providing mobile payment services platform to the telecom and financial industries.

For the domestic market, our sales team covers the following regions: Shandong, Hebei, Henan, Beijing, Tianjin, Zhejiang, North East China, Inner Mongolia, Xingjiang, Sichun, Yunnan, Anhui, Shanghai, Hunan, Jiangxi, Fujian, Guangdong, and Guangxi. For the international market, we have divided the regions into US, Mexico and the Middle East, although we have made only one sale in the Middle East.

10

As of December 31, 2010, we had 68 sales and marketing employees, representing approximately 32% of our total workforce.

Relationship with VeriFone

Concurrently with the closing of the February 2010 Offering, we entered into a master engagement agreement (“VeriFone Agreement”) with VeriFone, Inc. (“VeriFone”) such that VeriFone is our exclusive provider of point of sale hardware, software and services that are purchased or deployed by us and our affiliates and we have agreed to use our best efforts to ensure that VeriFone will receive at least 80% of the orders for point of sale systems placed by the Company’s mobile operator partners. Pursuant to the terms of the VeriFone Agreement, we submitted a binding, non-cancellable purchase order to VeriFone covering an initial order of $5 million of VeriFone’s point of sale systems for deployment in China as part of its rollout. The full amount of the purchase order was paid upon submission to VeriFone. Additionally, the Master Engagement Agreement contains a non-binding deployment schedule covering a total of 125,000 point of sale systems to be supplied by VeriFone through the end of 2012. VeriFone invested $5 million in the February 2010 Offering. We have granted VeriFone the ability to name one of the directors on our Board of Directors so long as it beneficially owns at least 4.99% of our outstanding Common Stock.

Research and Development

Since inception, we have made substantial investments in research and development. We work with our customers to develop system solutions that address existing and anticipated end-user needs. R&D projects are evaluated by senior management and assigned to our R&D team based upon the potential value of the target markets, as well as the technology, manpower and engineering expertise requirements. Our research and development effort is based primarily in Jinan, the capital of Shandong Province. Jinan is home to several highly ranked universities, allowing us access to a wide range of talent and human resources in order to support our R&D needs.

The market for our products and services are characterized by changing technology, evolving industry standards and frequent product introductions. We believe our future success depends largely upon our ability to continue to introduce and enhance our lineup of products and services. Our research and development goals include:

|

|

•

|

developing new solutions and technologies for the next generation of application enabling platforms;

|

|

|

•

|

continue to improve upon existing application platforms in order to provide the best available technology solutions to our customers;

|

|

|

•

|

continue to seek new applications for our existing technologies and patents; and

|

|

|

•

|

cooperate with other technology companies in the area of chip design and user terminals for mobile payment services and other new applications.

|

As of December 31, 2010, we had 113 research and development employees representing approximately 53% of our total workforce. For the years ended December 31, 2010 and 2009, we spent $1,203,264 and $435,712 on research and development expenses, respectively.

Employees

Together with our subsidiaries, as of December 31, 2010, we had approximately 215 full-time employees, including 113 in R&D; 68 in sales and marketing; 9 members of management and 25 others, including accounting, administration and human resources.

We are compliant with local prevailing wage, contractor licensing and insurance regulations, and have good relations with our employees.

11

As required by PRC regulations, we participate in various employee benefit plans that are organized by municipal and provincial governments, including pension, work-related injury benefits, maternity insurance, medical and unemployment benefit plans. We are required under PRC laws to make contributions to the employee benefit plans at specified percentages of the salaries, bonuses and certain allowances of our employees, up to a maximum amount specified by the local government from time to time. Members of the retirement plan are entitled to a pension equal to a fixed proportion of the salary prevailing at the member’s retirement date.

Competition

The market for MVAS enabling technology platform is highly competitive and fragmented. Within the MVAS Application Platform segment, our principal competitors are: Huawei and ZTE. Within the Mobile Payment System segment, our primary competitors are: UMPay, HiSun Technology, and Guangzhou SmartChina. Some of our competitors are larger and have greater financial resources and greater brand name recognition than we do and may, as a result, be better positioned to adapt to changes in the industry or the economy as a whole.

We compete primarily on the basis of the following factors: commercial viability of our application platforms, time to market, end-to-end system solutions, product features, degree of reliability, total cost of ownership, quality of technical and customer support, and compatibility and interoperability of the platforms. Combined with our patented technology, we believe that we compete favorably with respect to these factors.

We expect competition in our industry will be largely driven by the need to respond to the growing consumer appetite to access an increasing variety of information and solutions through their mobile device. Furthermore, increasingly complex technology combined with ever smaller form factors will also drive competition in our industry.

Our Industry

Overview of the PRC Telecom Market

In May 2008, the Ministry of Industry and Information Technology (“MIIT”), the National Development and Reform Commission (“NDRC”) and the Ministry of Finance carved the PRC telecom industry into three service providers of comparable scale and distribution: China Mobile, China Telecom and China Unicom, or collectively, “The Big Three”.

Two Significant Mobile Revenue Streams: Mobile Value Added Services And Mobile Payment Solutions

Mobile Value Added Services (“MVAS”) is composed of all non-voice services that promote mobile phone usage, the four largest in the PRC being Short Message Service (“SMS”), Multimedia Messaging Service (“MMS”), Wireless Application Protocol (“WAP”), and Color Ring Tone.

Mobile Payment Solutions (“MPS”) allows for the purchase of items with a mobile phone, facilitating both remote mobile payment and point of sale (“POS”) mobile payment. Remote mobile purchases are enabled through SMS, WAP, and WEB interfaces. WAP is a commonly used web browser developed to allow a realistic browsing experience, while WEB usage refers to surfing on the WEB. POS mobile payment allows consumers to pay for items by storing bank, credit, or prepayment card information on a mobile phone.

Key Drivers for MVAS and MPS

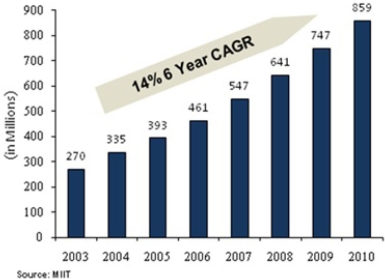

The development of the MVAS and MPS markets in the PRC is highly correlated with the growth of the overall mobile phone industry in the PRC. According to MIIT, 859 million people had a mobile phone account at the end of 2010 and according to iResearch, 233 million of the subscribers had used their mobile phone’s browser at least once. The MIIT data also indicated that total revenue for the telecom sector in the PRC grew to approximately $899 billion for 2010. Positive mobile phone industry trends in China are largely driven by the increasing affluence of the middle class, a growing subscriber base, and 3G deployment, which officially began in 2009. Moreover, iResearch projects that mobile phone browser users could grow 125% to 524 million users by the end of 2012.

12

According to its 2009 Annual Report, China Mobile, which had 70.6% mobile phone user market share at the end of 2009, has experienced dramatic usage growth in its MVAS segment. During 2009, China Mobile’s SMS and MMS volumes, WAP megabyte usage and Color Ring Tone subscriptions have increased by 12.2%, 37.2% 163% and 24.7%, respectively. Total MVAS revenue grew 16.0% in the same time period. As each product matures MVAS product offerings are becoming more affordable for consumers in the PRC.

New MVAS Applications

All of the Big Three are rolling out new MVAS product offerings. For example, China Mobile is offering “Mobile Market”, “Mobile TV”, and “Mobile Reading” MVAS applications. China Unicom is offering mobile office, mobile security, and intelligent public transportation applications. China Telecom is offering “eSurfing reader”, “189 mailbox”, “eSurfing LIVE”, and “eSurfing Video” applications.

China MPS Aggregate Demand Forecasts

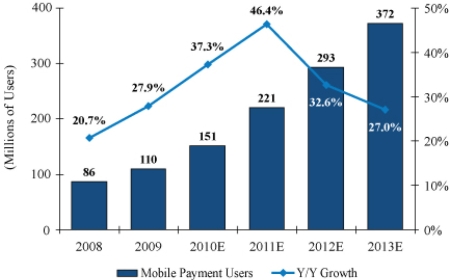

Based on China Computer World research projections, Chinese mobile payment users reached 110 million at the end of 2009, and are estimated to more than triple by the end of 2013. Dramatic increases in demand are expected, as indicated in the graph below, as The Big Three continue their roll-out of MPS networks in each province, in turn, incentivizing third party platforms and vendors.

13

3G Rollout in China Driving Remote MPS

Although our MPS technology is not dependent on 3G capability, the roll out of 3G networks in the PRC and an increase in smartphone use will increase data speeds and thus encourage more remote MPS transactions through WEB. On the network front, China Telecom has the most developed 3G footprint in the PRC, while China Unicom has recently announced it will raise $1.8 billion to accelerate its 3G development. China Mobile’s 2009 Annual Report stated that it already operated in 238 cities, providing service to 70% of urban populations in the PRC, and that it would approach urban population coverage of 100% by the end of 2011. China Telecom’s 2009 Annual Report also signaled that it was almost at full coverage, with 98% of urban populations and 93% of rural populations covered at the close of 2009. China Unicom’s 2009 Annual Report pronounced less ambitious service goals with 282 cities by end of 2009 and 75% of the total population by the end of 2011.

2.5G and 3G enabled smartphones are also part of the remote MPS solution, and are expected to become increasingly affordable. At the high-end, China Unicom is offering the iPhone for RMB 3,899. Meanwhile China Telecom, the third largest mobile network provider by market share, is offering 3G handsets around RMB 1,000. Affordable smartphones with higher browser quality may increase WAP and WEB use and thus encourage greater use of remote MPS payments.

Emergence of POS MPS Market

The key ingredients for creation of successful POS MPS markets are promotion by the telecom carriers, merchant acceptance and ultimately consumer demand. The Big Three are beginning to popularize the concept of the mobile wallet as a convenient cashless alternative to traditional payment methods.

While the technology is already available, consumers must switch to a relatively low cost POS MPS SIM card and the cost is relatively low. For example, China Telecom mobile subscribers can currently switch to a POS MPS SIM card for less than RMB100.

Merchants in China across many verticals, including restaurants, convenience stores and hotels are increasingly offering POS MPS services. Some examples are Lianhua Supermarkets, Wankelong Supermarkets, UBC Coffee, and Formet Laundry. POS MPS services require banks or other third-party vendors to invest in POS payment terminals and merchants to accept POS MPs related transaction fees. Verifone is a manufacturer and provider of POS electronic payment devices and software.

Payment clearing institutions in the PRC are now cooperating in order to develop MPS for mobile phones. For example, on September 28, 2010, China UnionPay announced a Mobile Payment Industry Alliance with eighteen national and local commercial banks in order to establish a set of technical standards. China Unicom has also recently formed alliances with Agricultural Bank of China and Bank of Communication.

14

MPS Security

The Big Three are using NFC (13.56MHz), SIMPass (13.56MHz), and RF-SIM (2.4GHz) wireless communication technology, following the lead of carriers in Japan and Korea. NFC and SIMPass technology, developed by Philips and Watch Data, respectively, enables data exchange between two devices within 20 centimeters of one another while offering greater security capabilities than other current MPS mediums such as SMS and WAP. All three wireless communication technologies can generate encryption codes to authenticate MPS transactions.

Competition Among Third-Party Vendors

Our principal competitors are Huawei, ZTE, UMPay, Hi Sun Technology, Shanghai Huateng, Fujian Fujitsu, and Digital China Si Tech. These companies can be classified into three categories:

|

|

•

|

Financial service solutions companies (Hi Sun Technology and Shanghai Huateng);

|

|

|

•

|

Telecom value-added software and system integration companies (Trunkbow, Huawei, ZTE, Fujian Fujitsu, and Digital China Si Tech); and

|

|

|

•

|

Recently incorporated JV companies (UMPay is a China Mobile and China UnionPay JV).

|

Our largest competitors are telecom value-added software and system integration companies. These competitors already have established relationships with The Big Three. Competitors such as Huawei and ZTE are larger and have greater financial resources and greater brand name recognition than we do and may, as a result, be better positioned to adapt to changes in the industry or the economy as a whole.

Real Property

We do not own any real property. We lease our facilities in the PRC pursuant to leases with terms of generally two to three years.

Intellectual Property

Our technology is the subject of 164 filed patent applications, of which 50 have been granted by the National Intellectual Property Administration of the People’s Republic of China. All of the patents have a duration period of 20 years starting from submission date. Below is a list of some of granted patents responsible for generating majority of the current revenues.

·

Table I: Significant Patents Granted

|

Patent#

|

Description of use

|

Expiration Date

|

||

|

ZL 200410009495.0

|

System and implementation of enabling mobile user to store and search phone book list from network. Provides network phone book store and searching feature from mobile network.

|

August 30, 2024

|

||

|

ZL 200410009525.8

|

Equipment and method for realizing hiding calling number in telephone exchange network.

|

September 8, 2024

|

||

|

ZL 200410009612.3

|

Device and method for realizing transmitting information to computer network real-time communication terminal by telephone.

|

September 28, 2024

|

||

|

ZL 200410009830.7

|

Equipment and method for providing senior secretary service for telephone user.

|

November 22, 2024

|

||

|

ZL 200410103905.8

|

Apparatus and method for intelligent communication based on mobile communication network and Internet.

|

December 31, 2024

|

||

|

ZL 200510011305.3

|

Device and method for selecting and binding telephone number by mobile communication intelligent card.

|

February 4, 2025

|

||

|

ZL 200510011343.9

|

Method for implementing new service of mobile phone based on position renewing operation.

|

February 23, 2025

|

15

|

Patent#

|

Description of use

|

Expiration Date

|

||

|

ZL 200510011525.6

|

System, method and implementation of providing instant communication between mobile phone and computer user. Provides forward function between Instant Message client and mobile phone.

|

April 4, 2025

|

||

|

ZL 200510011542.X

|

Apparatus and method for realizing main calling set ring back tone based on personalized ring back tone.

|

April 8, 2025

|

||

|

ZL 200510012089.4

|

Device and method for realizing to provide short news to mobile phone user and no interference service.

|

July 4, 2025

|

||

|

ZL 200510012090.7

|

Equipment and method for providing virtual facsimile business using mobile telephone number.

|

July 4, 2025

|

||

|

ZL 200610011449.3

|

Apparatus and method for automatic network storage of short message receive by mobile telephone.

|

March 8, 2026

|

||

|

ZL 200610011574.4

|

Device and method for realizing main call customized ring back tone service.

|

March 29, 2026

|

||

|

ZL 200610011725.6

|

Device and method for realizing mobile phone turn-off and short message call transfer.

|

April 4, 2026

|

||

|

ZL 200610112451.X

|

System and method for realizing secrecy of mobile phone number.

|

August 18, 2026

|

||

|

ZL 200710065067.3

|

Method for realizing caller customized ring back tone compatible with called personalized ring back tone.

|

April 2, 2027

|

||

|

ZL 200710063737.8

|

System and method for realizing point-to-point short message encryption and message screening.

|

February 8, 2027

|

||

|

ZL 200710177629.3

|

System and method for realizing personal electronic check card.

|

November 19, 2027

|

||

|

ZL 200810224979.5

|

System and method for adding fixed telephone number to mobile telephone number.

|

October 29, 2028

|

Table II: Significant Patents Pending

|

Patent#

|

Description of use

|

Expiration

Date

|

||

|

ZL 200710121396.5

|

System, method and implementation of enabling communication between mobile client device and mobile client server. Enables communication between mobile client device and mobile client server.

|

September 5, 2027

|

||

|

ZL 200810089411.7

|

System, method and implementation of providing multiple phone numbers in one mobile phone and enabling mobile users to control their multiple mobile phone numbers' feature. Provides multiple phone numbers in one mobile phone and enables mobile users to control their multiple mobile phone numbers' features, such as call, MMS and SMS screening, backup MMS and SMS to E-mail format, and enables users to manage their mobile communication functions.

|

March 28, 2028

|

||

|

ZL 200910091555.0

|

Method and implementation of integrating different bank cards into one special personal payment device. Provides a method to integrate different bank cards such as gate pass, attendance pass and RFID card into one special personalized payment machine for user to easily control.

|

August 26, 2029

|

||

|

ZL 200910092196.0

|

System, method and implementation of providing caller CRBT service based on CRBT service. Provides caller CRBT service based on CRBT service so that callers can receive caller's CRBT when making calls to Non-CRBT users.

|

16

Table II shows patents pending for our intellectual property. Patent requests listed as “pending” have been reviewed by the Chinese Patent Office and will be granted upon the expiration of the two-year waiting period commencing on their respective dates of submission. While pending patents have not been granted, the filings are within the same families as certain patents previously granted to us and as such, we believe that they should result in grants. Trunkbow views this intellectual property as among the core elements of its overall service offerings.

Government Regulations

Each of our PRC subsidiaries, the Shandong WFOE and the Shenzhen WFOE, has obtained all necessary licenses, authorizations, approvals, registrations and permits from PRC government agencies or any other regulatory body having jurisdiction over it (“Authorizations”) for it to own, lease, license and use properties and assets and to conduct its business as described in its business license, to the extent applicable, in so far as such properties and assets and the conduct of such business is governed by PRC laws and regulations, and such Authorizations are in full force and effect. Under the PRC regulations currently in effect, we may operate our business of providing mobile phone technology services and solutions without having to obtain or maintain any Authorizations that are not generally required for all businesses operating under PRC laws.

According to the Provisions on the Administration of Foreign-funded Telecommunications Enterprises of the PRC, ultimate proportion of the foreign investments in any company engaged in telecommunication value-added services shall not exceed 50% of such company’s equity interests. The PRC Telecommunication Regulation further defined “telecommunication value-added services” as providing telecommunication and information services through public networking facilities. As the business operations of our PRC subsidiaries only include the provision of technology support and solutions to the telecom providers and our PRC subsidiaries do not provide any telecom services directly to the end-users, our PRC subsidiaries do not fall into the scope of the “telecommunication value-added service company” defined under the PRC laws. Therefore, the proportion of foreign investments in our PRC subsidiaries is not subject to the restrictions under the PRC laws.

Seasonality

Our quarterly operating results have varied significantly in the past and are likely to continue to vary significantly in the future. Historically, we have generally experienced a slowdown or decrease in generating revenues in the first quarter of the year due to the Chinese Lunar New Year as the majority of the businesses in the PRC shut down for a month-long holiday and slow down for a month prior to the New Year celebration. We believe that this fluctuation will gradually subside as we increase our recurring revenue streams.

Corporation Information

Our principal executive offices are located at Unit 1217-1218, 12F of Tower B, Gemdale Plaza, No. 91 Jianguo Road, Chaoyang District, Beijing, People’s Republic of China 100022, Tel: (86) (10) 8571-2518, Fax: (86) (10) 8571-2528.

17

Item 1A. Risk Factors.

In addition to the other information in this Form 10-K, readers should carefully consider the following important factors. These factors, among others, in some cases have affected, and in the future could affect, our financial condition and results of operations and could cause our future results to differ materially from those expressed or implied in any forward-looking statements that appear in this on Form 10-K or that we have made or will make elsewhere.

Risks Related to Our Business

We have a limited operating history as a separate wholly owned foreign company which makes it difficult to evaluate our business and future prospects.

Our limited operating history following our separation from Trunkbow Shenzhen Technologies Limited in December 2007 and the early stage of development of the mobile payment industry in which we operate makes it difficult to evaluate our business and future prospects. Although our revenues have grown rapidly, we cannot assure you that we will maintain profitability or that we will not incur net losses in the future. Our business model includes recurring revenues from revenue sharing agreements with resellers and the Big Three. To date, less than five percent of our revenues have been derived from these revenue sharing agreements. There is no assurance that we will generate significant revenue from such agreements. We expect that our operating expenses will increase as we expand. Any significant failure to realize anticipated revenue growth could result in significant operating losses. We will continue to encounter risks and difficulties in implementing our business model, including potential failure to:

|

|

•

|

increase awareness of its products, protect its reputation and develop customer loyalty;

|

|

|

•

|

manage its expanding operations and service offerings, including the integration of any future acquisitions;

|

|

|

•

|

maintain adequate control of its expenses; and

|

|

|

•

|

anticipate and adapt to changing conditions in the markets in which it operates as well as the impact of any changes in government regulation, mergers and acquisitions involving its competitors, technological developments and other significant competitive and market dynamics.

|

If we are not successful in addressing any or all of these risks, our business may be materially and adversely affected.

Our business depends to a large extent on mobile telecommunications service providers in the PRC and any deterioration of such relationships may have a material and adverse effect on our results of operations.

We have derived, and believe we will continue to derive, a significant portion of our revenues from a limited number of large customers, such as China Mobile, China Telecom, and China Unicom which are our only major customers and who have been customers for over five years. We have passed a rigorous supplier approval process carried out by each of the three major carriers to become an “approved vendor” to each of them. Our approved vendor status allows us to be eligible to enter into individual customer contracts with the relevant provincial branch of each respective carrier in each province in which we operate. Such individual contracts are similar to purchase orders for our technology platforms, in the form of proprietary software licensing and revenue sharing arrangements with the relevant branch of China Mobile, China Telecom or China Unicom, as the case may be. Currently, China Mobile, China Telecom and China Unicom are the only mobile telecommunications service providers in China that operate mobile payment platforms. Our agreements are generally for a period of less than five years and generally do not have automatic renewal provisions. If any of the carriers is unwilling to continue to cooperate and negotiate with us upon expiration of such agreements, we will not be able to conduct our existing mobile payment business at the levels we anticipate.

Revenues from sales to the Big Three, including revenues generated through the resale of our products to mobile carriers through intermediaries (i.e., direct and indirect sales to these carriers), accounted for approximately 16%, 47% and 20%, and 42%, 15% and 42% of our total revenues for the fiscal years ended December 31, 2010 and 2009. Further, four resellers accounted for approximately 81% and two provincial branches of China Unicom accounted for approximately 81% of our total revenue for the fiscal years ended December 31, 2009 and 2008, respectively. The loss of our status as a approved vendor to any of China Mobile, China Telecom or China Unicom, or our inability to renegotiate our revenue sharing agreements with resellers on terms as favorable as those under which we presently operate, would have a significant negative impact on our business and on our financial results.

18

In addition, if either China Mobile, China Telecom or China Unicom decides to change its content or transaction fees or its share of revenues, our revenues and profitability could also be materially adversely affected.

Our financial condition and results of operations may be materially affected by the changes in policies or guidelines of the mobile telecommunications service providers.

The mobile telecommunications service providers in the PRC may, from time to time, issue certain operating policies or guidelines, requesting or stating their preference for certain actions to be taken in choosing their partners in certain application service platforms. Due to our reliance on the mobile telecommunications service providers, a significant change in their policies or guidelines may have a material adverse effect on our business. Such change in policies or guidelines may result in lower revenue or additional operating costs for us, and as such, we cannot assure you that our financial condition and results of operations will not be materially adversely affected by any such policy or guideline change.

Our customers are concentrated in a limited number of industries and an economic downturn in any of these industries could have a material adverse effect on our results of operations.

Our customers are concentrated primarily in the telecommunications, media and technology industries, and to a lesser extent, the transportation, financial services, and retail industries, where we provide applications for their industries. Our ability to generate revenue depends on the demand for our services in these industries. An economic downturn, or a slowdown or reversal of the tendency in any of these industries to rely on our services could have a material adverse effect on our business, results of operations or financial condition.

The markets in which we operate are highly competitive and we may not be able to maintain market share.

We offer only one Mobile Payment model. Competing technologies from larger, better financed international companies are increasing their effort to gain a foothold in the PRC market. This may result in erosion of our market share in mobile payment services.

Increasing competition among telecommunication companies in greater China has led to a reduction in telecommunication services fees that can be charged by such companies. Within the MVAS Application Platform segment, our principal competitors are Huawei and ZTE. Within the Mobile Payment System segment, our primary competitors are UMPay, HiSun Technology, Shanghai Huateng, Huawei, ZTE, Fujian Fujisu and Digital China Si Tech. If a reduction in telecommunication services fees negatively impacts revenue generated by our customers, they may require us to reduce the price of our services, or seek competitors that charge less, which could reduce our market share. If we must significantly reduce the price of our services, the decrease in revenue could materially and adversely affect our profitability.

Our operating results may fluctuate significantly from quarter to quarter, which could lead to volatility in our stock price.

Our quarterly operating results have varied significantly in the past and are likely to continue to vary significantly in the future. Historically, we have generally experienced a slowdown or decrease in generating revenues in the first and fourth quarter of the year due to the Chinese Lunar New Year. In addition, our quarterly revenues are subject to fluctuation because they substantially depend upon the timing of orders. As a result, you may not be able to rely on period-to-period comparisons of our operating results as an indication of our future performance. Our actual quarterly results may differ from market expectations, which could adversely affect our stock price.

The loss of certain employees that are essential to our business could have a material adverse effect on our results of operations.

Li Qiang, Chief Executive Officer, Hou Wanchun, Chairman, and Ye Yuanjun, Chief Financial Officer are essential to our ability to continue to grow our business. Messrs. Li, Hou and Ms. Ye have established relationships within the industries in which we operate. If either of them were to leave us, our growth strategy might be hindered, which could limit our ability to increase revenue. We do not maintain key-person insurance coverage. In addition, we face competition for attracting skilled personnel. If we fail to attract and retain qualified personnel to meet current and future needs, this could slow our ability to grow our business, which could result in a decrease in market share.

19

International operations require significant management attention, which could detract from the time and attention management spends on our domestic operations and have a material adverse effect on our results of operations.

Our operations in countries outside of the PRC are subject to various unique risks, including the following, which, if not planned and managed properly, could materially adversely affect our business, financial condition and operating results:

|

|

•

|

legal uncertainties or unanticipated changes regarding regulatory requirements, political instability, liability, export and import restrictions, tariffs and other trade barriers;

|

|

|

•

|