UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| |

|

|

| þ |

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2010

or

| |

|

|

| o |

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 333-158111 (1933 Act)

GRUBB & ELLIS HEALTHCARE REIT II, INC.

(Exact name of registrant as specified in its charter)

| |

|

|

|

| Maryland

|

|

26-4008719 |

| (State or other jurisdiction of

|

|

(I.R.S. Employer |

| incorporation or organization)

|

|

Identification No.) |

| |

|

|

| 1551 N. Tustin Avenue, Suite 300, Santa Ana, California

|

|

92705 |

| (Address of principal executive offices)

|

|

(Zip Code) |

Registrant’s telephone number, including area code: (714) 667-8252

Securities registered pursuant to Section 12(b) of the Act:

| |

|

|

|

| Title of each class

|

|

Name of each exchange on which registered |

| None

|

|

None |

Securities registered pursuant to Section 12(g) of the Act:

None

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule

405 of the Securities Act. o Yes þ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section

13 or Section 15(d) of the Act. o Yes þ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed

by Sections 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or

for such shorter period that the registrant was required to file such reports), and (2) has been

subject to such filing requirements for the past 90 days. þ Yes o No

Indicate by check mark whether the registrant has submitted electronically and posted on its

corporate Web site, if any, every Interactive Data File required to be submitted and posted

pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months

(or for such shorter period that the registrant was required to submit and post such files). o Yes o No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation

S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of

registrant’s knowledge, in definitive proxy or information statements incorporated by reference in

Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated

filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large

accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the

Exchange Act. (Check one):

| |

|

|

|

|

|

|

|

| Large accelerated filer o

|

|

Accelerated filer o

|

|

Non-accelerated filer þ

|

|

Smaller reporting company o |

|

|

|

|

|

(Do not check if a smaller reporting company) |

|

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of

the Exchange Act). o Yes þ No

There

is no established market for the registrant’s shares of common

stock. The registrant is currently conducting an ongoing initial

public offering of its shares of common stock pursuant to a

Registration Statement of Form S-11, which shares are being sold at

$10.00 per share, with discounts available for certain categories of

purchasers. There were approximately 7,098,490 shares of

common stock held by non-affiliates as of June 30, 2010, the last

business day of the registrant’s most recently completed second

fiscal quarter, for an aggregate market value of $70,985,000,

assuming a market value of $10.00 per share.

As of February 28, 2011, there were 18,869,725 shares of common stock of Grubb & Ellis

Healthcare REIT II, Inc. outstanding.

Documents Incorporated by Reference: Portions of the registrant’s proxy statement for the 2011

annual stockholders meeting which is expected to be filed no later than May 2, 2011 are

incorporated by reference in Part III, Items 10, 11, 12, 13 and 14.

GRUBB & ELLIS HEALTHCARE REIT II, INC.

(A Maryland Corporation)

TABLE OF CONTENTS

2

PART I

The use of the words “we,” “us” or “our” refers to Grubb & Ellis Healthcare REIT II, Inc. and

its subsidiaries, including Grubb & Ellis Healthcare REIT II Holdings, LP, except where the context

otherwise requires.

Our Company

Grubb & Ellis Healthcare REIT II, Inc., a Maryland corporation, was incorporated on January 7,

2009 and therefore we consider that our date of inception. We were initially capitalized on

February 4, 2009. We intend to invest in a diversified portfolio of real estate properties,

focusing primarily on medical office buildings and healthcare-related facilities. We may also

originate and acquire secured loans and other real estate-related investments. We generally will

seek investments that produce current income. We intend to elect to be treated as a real estate

investment trust, or REIT, under the Internal Revenue Code of 1986, as amended, or the Code, for

federal income tax purposes for our taxable year ended December 31, 2010.

We are conducting a best efforts initial public offering, or our offering, in which we are

offering to the public up to 300,000,000 shares of our common stock for $10.00 per share in our

primary offering and 30,000,000 shares of our common stock pursuant to our distribution

reinvestment plan, or the DRIP, for $9.50 per share, for a maximum offering of up to

$3,285,000,000, or the maximum offering. The United States, or U.S., Securities and Exchange

Commission, or the SEC, declared our registration statement effective as of August 24, 2009. As of

December 31, 2010, we had received and accepted subscriptions in our offering for 15,222,213 shares

of our common stock, or $151,862,000, excluding subscriptions from residents of Pennsylvania (who

were not admitted as stockholders until January 21, 2011, when we had received and accepted

subscriptions aggregating at least $164,250,000) and shares of our common stock issued pursuant to

the DRIP.

We conduct substantially all of our operations through Grubb & Ellis Healthcare REIT

II Holdings, LP, or our operating partnership. We are externally advised by Grubb & Ellis

Healthcare REIT II Advisor, LLC, or our advisor, pursuant to an advisory agreement, or the Advisory

Agreement, between us and our advisor that has a one-year term that expires June 1, 2011 and is

subject to successive one-year renewals upon the mutual consent of the parties. Our advisor

supervises and manages our day-to-day operations and selects the properties and real estate-related

investments we acquire, subject to the oversight and approval of our board of directors. Our

advisor also provides marketing, sales and client services on our behalf. Our advisor engages

affiliated entities to provide various services to us. Our advisor is managed by and is a wholly

owned subsidiary of Grubb & Ellis Equity Advisors, LLC, or Grubb & Ellis Equity Advisors, which is

a wholly owned subsidiary of Grubb & Ellis Company, or Grubb & Ellis, or our sponsor.

3

Key Developments during 2010 and 2011

| |

• |

|

On July 19, 2010, we entered into a loan agreement with Bank of America, N.A., to

obtain a secured revolving credit facility in an aggregate maximum principal amount of

$25,000,000, or the line of credit. The line of credit matures on July 19, 2012 and may

be extended by one 12-month period subject to satisfaction of certain conditions,

including payment of an extension fee. The proceeds of loans made under the line of

credit may be used to finance the purchase of properties, for working capital or may be

used for any other lawful purpose. |

| |

• |

|

As of March 10, 2011, we had completed 14 acquisitions, 10 of which were acquisitions

of medical office buildings, three of which were acquisitions of hospitals and one of

which was an acquisition of skilled nursing facilities. The aggregate purchase price of

these properties was $205,865,000 and was comprised of 26 buildings and 904,000 square

feet of gross leasable area, or GLA. |

| |

• |

|

As of February 28, 2011, we had received and accepted subscriptions in our offering for

18,559,580 shares of our common stock, or $185,142,000, excluding shares of our common

stock issued pursuant to the DRIP. |

4

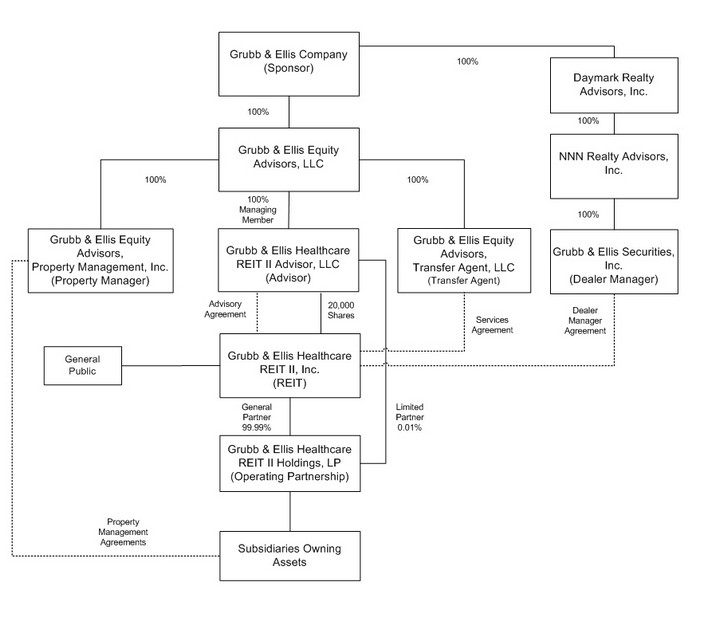

Our Structure

The following is a summary of our organizational structure as of March 10, 2011:

Our principal executive offices are located at 1551 N. Tustin Avenue, Suite 300, Santa Ana,

California 92705 and the telephone number is (714) 667-8252. Our sponsor maintains a web site at

www.gbe-reits.com/healthcare2, at which there is additional information about us and our

affiliates. The contents of that site are not incorporated by reference in, or otherwise a part of,

this filing. We make our periodic and current reports, as well as our Registration Statement on

Form S-11 (File No. 333-158111), amendments to our registration statement and supplements to our

prospectus, available at www.gbe-reits.com/healthcare2 as soon as reasonably practicable after such

materials are electronically filed with the SEC. They are also available for printing by any

stockholder upon request.

Investment Objectives

Our investment objectives are:

| |

• |

|

to preserve, protect and return our stockholders’ capital contributions; |

| |

• |

|

to pay regular cash distributions; and |

| |

• |

|

to realize growth in the value of our investments upon our ultimate sale of such

investments. |

5

We may not attain these objectives. Our board of directors may change our investment

objectives if it determines it is advisable and in the best interest of our stockholders.

During the term of the Advisory Agreement, decisions relating to the purchase or sale of

investments will be made by our advisor, subject to the oversight and approval by our board of

directors.

Investment Strategy

We intend to use substantially all of the net proceeds from our offering to invest in a

diversified portfolio of real estate properties, focusing primarily on medical office buildings and

healthcare-related facilities. We also may originate or acquire real estate-related investments

such as mortgage, mezzanine, bridge and other loans, common and preferred stock of, or other

interests in, public or private unaffiliated real estate companies, commercial mortgage-backed

securities, and certain other securities, including collateralized debt obligations and foreign

securities. We generally seek investments that produce current income. In order to maintain our

exemption from regulation as an investment company under the Investment Company Act of 1940, as

amended, or the Investment Company Act, we may be required to limit our investments in certain

types of real estate-related investments.

We seek to maximize long-term stockholder value by generating sustainable growth in cash flows

and portfolio value. In order to achieve these objectives, we may invest using a number of

investment structures which may include direct acquisitions, joint ventures, leveraged investments,

issuing securities for property and direct and indirect investments in real estate.

In addition, when and as determined appropriate by our advisor, our portfolio may also include

properties in various stages of development other than those producing current income. These stages

include, without limitation, unimproved land both with and without entitlements and permits,

property to be redeveloped and repositioned, newly constructed properties and properties in

lease-up or other stabilization scenarios, all of which have limited or no relevant operating

histories and no current income. Our advisor will make this determination based upon a variety of

factors, including the available risk adjusted returns for such properties when compared with other

available properties, the appropriate diversification of the portfolio, and our objectives of

realizing both current income and capital appreciation upon the ultimate sale of properties.

For each of our investments, regardless of property type, we seek to invest in properties with

the following attributes:

| |

• |

|

Quality. We seek to acquire properties that are suitable for their intended use

with a quality of construction that is capable of sustaining the property’s investment

potential for the long-term, assuming funding of budgeted maintenance, repairs and

capital improvements. |

| |

• |

|

Location. We seek to acquire properties that are located in established or

otherwise appropriate markets for comparable properties, with access and visibility

suitable to meet the needs of its occupants. |

| |

• |

|

Market; Supply and Demand. We focus on local or regional markets that have

potential for stable and growing property level cash flows over the long-term. These

determinations will be based in part on an evaluation of local economic, demographic and

regulatory factors affecting the property. For instance, we favor markets that indicate a

growing population and employment base or markets that exhibit potential limitations on

additions to supply, such as barriers to new construction. Barriers to new construction

include lack of available land and stringent zoning restrictions. In addition, we

generally will seek to limit our investments in areas that have limited potential for

growth. |

| |

• |

|

Predictable Capital Needs. We seek to acquire properties where the future expected

capital needs can be reasonably projected in a manner that would enable us to meet our

objectives of growth in cash flows and preservation of capital and stability. |

| |

• |

|

Cash Flows. We seek to acquire properties where the current and projected cash

flows, including the potential for appreciation in value, would enable us to meet our

overall investment objectives. We evaluate cash flows as well as expected growth and the

potential for appreciation. |

6

We will not invest more than 10.0% of the offering proceeds available for investment in

unimproved or non-income producing properties or in other investments relating to unimproved or

non-income producing property. A property will be considered unimproved or non-income producing

property for purposes of this limitation if it: (1) is not acquired for the purpose of producing

rental or other operating income, or (2) has no development or construction in process at the date

of acquisition or planned in good faith to commence within one year of the date of acquisition.

We will not invest more than 10.0% of the offering proceeds available for investment in

commercial mortgage-backed securities. In addition, we will not invest more than 10.0% of the

offering proceeds available for investment in equity securities of public or private real estate

companies.

We are not limited as to the geographic area where we may acquire properties. We are not

specifically limited in the number or size of properties we may acquire or on the percentage of our

assets that we may invest in a single property or investment. The number and mix of properties and

real estate-related investments we will acquire will depend upon real estate and market conditions

and other circumstances existing at the time we are acquiring our properties and making our

investments, and the amount of proceeds we raise in our offering and potential future offerings.

Real Estate Investments

We intend to invest in a diversified portfolio of real estate investments, focusing primarily

on medical office buildings and healthcare-related facilities. We generally seek investments that

produce current income. Our investments may include:

| |

• |

|

medical office buildings; |

| |

• |

|

assisted living facilities; |

| |

• |

|

skilled nursing facilities; |

| |

• |

|

long-term acute care facilities; |

| |

• |

|

memory care facilities; |

| |

• |

|

specialty medical and diagnostic service facilities; |

| |

• |

|

laboratories and research facilities; |

| |

• |

|

pharmaceutical and medical supply manufacturing facilities; and |

| |

• |

|

offices leased to tenants in healthcare-related industries. |

We generally seek to acquire real estate of the types described above that will best enable us

to meet our investment objectives, taking into account the diversification of our portfolio at the

time, relevant real estate and financial factors, the location, the income-producing capacity, and

the prospects for long-term appreciation of a particular property and other considerations. As a

result, we may acquire properties other than the types described above. In addition, we may acquire

properties that vary from the parameters described above for a particular property type.

7

The consideration for each real estate investment must be authorized by a majority of our

independent directors or a duly authorized committee of our board of directors, ordinarily based on

the fair market value of the investment. If the majority of our independent directors or a duly

authorized committee of our board of directors so determines, or if the investment is to be

acquired from an affiliate, the fair market value determination must be supported by an appraisal

obtained from a qualified, independent appraiser selected by a majority of our independent

directors.

Our real estate investments generally take the form of holding fee title or long-term

leasehold interests. Our investments may be made either directly through our operating partnership

or indirectly through investments in joint ventures, limited liability companies, general

partnerships or other co-ownership arrangements with the developers of the properties, affiliates

of our advisor or other persons.

In addition, we may purchase real estate investments and lease them back to the sellers of

such properties. Our advisor will use its best efforts to structure any such sale-leaseback

transaction such that the lease will be characterized as a “true lease” and so that we will be

treated as the owner of the property for federal income tax purposes. However, we cannot assure our

stockholders that the Internal Revenue Service, or the IRS, will not challenge such

characterization. In the event that any such sale-leaseback transaction is re-characterized as a

financing transaction for federal income tax purposes, deductions for depreciation and cost

recovery relating to such real estate investment would be disallowed or significantly reduced.

Our obligation to close a transaction involving the purchase of real estate is generally

conditioned upon the delivery and verification of certain documents from the seller or developer,

including, where appropriate:

| |

• |

|

plans and specifications; |

| |

• |

|

environmental reports (generally a minimum of a Phase I investigation); |

| |

• |

|

building condition reports; |

| |

• |

|

evidence of marketable title subject to such liens and encumbrances as are

acceptable to our advisor; |

| |

• |

|

audited financial statements covering recent operations of real properties having

operating histories or audited financial statements or summarized financial information

of the lessee or guarantor, unless such statements are not required to be filed with the

SEC and delivered to stockholders; |

| |

• |

|

title insurance policies; |

| |

• |

|

liability insurance policies; and |

| |

• |

|

tenant leases and operating agreements. |

In determining whether to purchase a particular real estate investment, we may, in

circumstances in which our advisor deems it appropriate, obtain an option on such property,

including land suitable for development. The amount paid for an option is normally surrendered if

the real estate is not purchased, and is normally credited against the purchase price if the real

estate is purchased. We also may enter into arrangements with the seller or developer of a real

estate investment whereby the seller or developer agrees that if, during a stated period, the real

estate investment does not generate specified cash flows, the seller or developer will pay us cash

in an amount necessary to reach the specified cash flow level, subject in some cases to negotiated

dollar limitations.

We will not purchase or lease real estate in which our sponsor, our advisor, our directors or

any of their affiliates have an interest without a determination by a majority of our disinterested

directors and a majority of our disinterested independent directors that such transaction is fair

and reasonable to us and at a price to us no greater than the cost of the real estate investment to

the affiliated seller or lessor, unless there is substantial justification for the excess amount

and the excess amount is reasonable. In no event will we acquire any such real estate investment at

an amount in excess of its current appraised value as determined by an independent expert selected

by our disinterested independent directors.

8

We intend to obtain adequate insurance coverage for all real estate investments in which

we invest. However, there are types of losses, generally catastrophic in nature, for which we do

not intend to obtain insurance unless we are required to do so by mortgage lenders. See Item 1A.

Risk Factors, Risks Related to Investments in Real Estate — Uninsured losses relating to real

estate and lender requirements to obtain insurance may reduce our stockholders’ returns.

We intend to acquire leased properties with long-term leases in place and we do not intend to operate

any healthcare-related facilities directly. As a REIT, we would be prohibited from operating

healthcare-related facilities directly, however from time to time we may lease a healthcare-related

facility that we acquire to a wholly owned taxable REIT subsidiary, or TRS. In such an event, our

TRS will engage a third party in the business of operating healthcare-related facilities to manage

the property.

Joint Ventures

We may enter into joint ventures, general partnerships and other arrangements with one or

more institutions or individuals, including real estate developers, operators, owners, investors

and others, some of whom may be affiliates of our advisor, for the purpose of acquiring real

estate. Such joint ventures may be leveraged with debt financing or unleveraged. We may enter into

joint ventures to further diversify our investments or to access investments which meet our

investment criteria that would otherwise be unavailable to us. In determining whether to invest in

a particular joint venture, our advisor will evaluate the real estate that such joint venture owns

or is being formed to own under the same criteria used in the selection of our other properties.

However, we will not participate in tenant-in-common syndications or transactions.

Joint ventures with unaffiliated third parties may be structured such that the investment

made by us and the co-venturer are on substantially different terms and conditions. For example,

while we and a co-venturer may invest an equal amount of capital in an investment, the investment

may be structured such that we have a right to priority distributions of cash flows up to a certain

target return while the co-venturer may receive a disproportionately greater share of cash flows

than we are to receive once such target return has been achieved. This type of investment structure

may result in the co-venturer receiving more of the cash flows, including appreciation, of an

investment than we would receive.

We may only enter into joint ventures with other real estate investment programs

sponsored or managed by our advisor or its affiliates, or Grubb & Ellis Group programs, or any of

our directors for the acquisition of properties if:

| |

• |

|

a majority of our directors, including a majority of our independent directors, not

otherwise interested in such transaction, approves the transaction as being fair and

reasonable to us; and |

| |

• |

|

the investment by us and such affiliate are on substantially the same terms and

conditions. |

We may invest in general partnerships or joint ventures with other Grubb & Ellis Group

programs or affiliates of our advisor to enable us to increase our equity participation in such

venture as additional proceeds of our offering are received, so that ultimately we own a larger

equity percentage of the property. Our entering into joint ventures with our advisor or any of its

affiliates will result in certain conflicts of interest. See Item 1A. Risk Factors, Risks Related

to Conflicts of Interest — If we enter into joint ventures with affiliates, we may face conflicts

of interest or disagreements with our joint venture partners that may not be resolved as quickly or

on terms as advantageous to us as would be the case if the joint venture had been negotiated at

arm’s length with an independent joint venture partner.

9

Real Estate-Related Investments

In addition to our acquisition of medical office buildings and healthcare-related facilities,

we also may invest in real estate-related investments, including loans (mortgage, mezzanine, bridge

and other loans) and securities investments (common and preferred stock of or other interests in

public or private unaffiliated real estate companies, commercial mortgage-backed securities, and

certain other securities, including collateralized debt obligations and foreign securities).

Investing In and Originating Loans

We may originate loans from mortgage brokers or personal solicitations of suitable borrowers,

or may purchase existing loans that were originated by other lenders. We may purchase existing

loans from affiliates and we may make or invest in loans in which the borrower is an affiliate. Our

advisor will evaluate all potential loan investments to determine if the security for the loan and

the loan-to-value ratio meets our investment criteria and objectives. Most loans that we will

consider for investment would provide for monthly payments of interest and some may also provide

for principal amortization, although many loans of the nature that we will consider provide for

payments of interest only and a payment of principal in full at the end of the loan term. We will

not originate loans with negative amortization provisions.

Securities Investments

We may invest in the following types of securities: (1) equity securities such as common

stocks, preferred stocks and convertible preferred securities of public or private unaffiliated

real estate companies (including other REITs, real estate operating companies and other real estate

companies); (2) debt securities such as commercial mortgage-backed securities and debt securities

issued by other unaffiliated real estate companies; and (3) certain other types of securities that

may help us reach our diversification and other investment objectives. These other securities may

include, but are not limited to, various types of collateralized debt obligations and certain

non-U.S. dollar denominated securities.

We have substantial discretion with respect to the selection of specific securities

investments. Our charter provides that we may not invest in equity securities unless a majority of

our directors, including a majority of our independent directors, not otherwise interested in the

transaction approve such investment as being fair, competitive and commercially reasonable.

Consistent with such requirements, in determining the types of securities investments to make, our

advisor will adhere to a board approved asset allocation framework consisting primarily of

components such as: (1) target mix of securities across a range of risk/reward characteristics; (2)

exposure limits to individual securities; and (3) exposure limits to securities subclasses (such as

common equities, debt securities and foreign securities). Within this framework, our advisor will

evaluate specific criteria for each prospective securities investment including:

| |

• |

|

positioning the overall portfolio to achieve an optimal mix of real estate and real

estate-related investments; |

| |

• |

|

diversification benefits relative to the rest of the securities assets within our

portfolio; |

| |

• |

|

fundamental securities analysis; |

| |

• |

|

quality and sustainability of underlying property cash flows; |

| |

• |

|

broad assessment of macroeconomic data and regional property level supply and

demand dynamics; |

| |

• |

|

potential for delivering high current income and attractive risk-adjusted total

returns; and |

| |

• |

|

additional factors considered important to meeting our investment objectives. |

10

We will not invest more than 10.0% of the offering proceeds available for investment in equity

securities of public or private real estate companies. The specific number and mix of securities in

which we invest will depend upon real estate market conditions, other circumstances existing at the

time we are investing in our securities and the amount of proceeds we raise in our offering. We

will not invest in securities of other issuers for the purpose of exercising control and the first

or second mortgages in which we intend to invest will likely not be insured by the Federal Housing

Administration or guaranteed by the Veterans Administration or otherwise guaranteed or insured.

Real estate-related equity securities are generally unsecured and also may be subordinated to other

obligations of the issuer. Our investments in real estate-related equity securities will involve

special risks relating to the particular issuer of the equity securities, including the financial

condition and business outlook of the issuer.

Development Strategy

We may engage our advisor or an affiliate of our advisor to provide development-related

services for all or some of the properties that we acquire for development or refurbishment. In

those cases, we will pay our advisor or its affiliate a development fee that is usual and customary

for comparable services rendered for similar projects in the geographic market where the services

are provided if a majority of our independent directors determines that such development fees are

fair and reasonable and on terms and conditions not less favorable than those available from

unaffiliated third parties. However, we will not pay a development fee to our advisor or its

affiliate if our advisor or any of its affiliates elects to receive an acquisition fee based on the

cost of such development. In the event that our advisor assists with planning and coordinating the

construction of any tenant improvements or capital improvements, our advisor may be paid a

construction management fee of up to 5.0% of the cost of such improvements.

Disposition Strategy

We intend to hold each property or real estate-related investment we acquire for an extended

period. However, circumstances might arise which could result in a shortened holding period for

certain investments. In general, the holding period for real estate-related investments other than

real property is expected to be shorter than the holding period for real property assets. A

property or real estate-related investment may be sold before the end of the expected holding

period if:

| |

• |

|

diversification benefits exist associated with disposing of the investment and

rebalancing our investment portfolio; |

| |

• |

|

an opportunity arises to pursue a more attractive investment; |

| |

• |

|

in the judgment of our advisor, the value of the investment might decline; |

| |

• |

|

with respect to properties, a major tenant involuntarily liquidates or is in

default under its lease; |

| |

• |

|

the investment was acquired as part of a portfolio acquisition and does not meet

our general acquisition criteria; |

| |

• |

|

an opportunity exists to enhance overall investment returns by raising capital

through sale of the investment; or |

| |

• |

|

in the judgment of our advisor, the sale of the investment is in the best interest

of our stockholders. |

The determination of whether a particular property or real estate-related investment

should be sold or otherwise disposed of will be made after consideration of relevant factors,

including prevailing economic conditions, with a view toward maximizing our investment objectives.

We cannot assure our stockholders that this objective will be realized. The selling price of a

property which is net leased will be determined in large part by the amount of rent payable under

the lease(s) for such property. If a tenant has a repurchase option at a formula price, we may be

limited in realizing any appreciation. In connection with our sales of properties, we may lend the

purchaser all or a portion of the purchase price. In these instances, our taxable income may exceed

the cash received in the sale. The terms of payment will be affected by custom practices in the

area in which the investment being sold is located and the then-prevailing economic

conditions.

11

Borrowing Policies

We intend to use secured and unsecured debt as a means of providing additional funds for the

acquisition of properties and other real estate-related assets. Our ability to enhance our

investment returns and to increase our diversification by acquiring assets using additional funds

provided through borrowing could be adversely affected if banks and other lending institutions

reduce the amount of funds available for the types of loans we seek. When interest rates are high

or financing is otherwise unavailable on a timely basis, we may purchase certain assets for cash

with the intention of obtaining debt financing at a later time. We may also utilize derivative

financial instruments such as fixed interest rate swaps and caps to add stability to interest

expense and to manage our exposure to interest rate movements.

We anticipate that after our initial phase of operations (prior to the investment of all of

the net proceeds of our offerings of shares of our common stock) when we may employ greater amounts

of leverage, aggregate borrowings, both secured and unsecured, will not exceed 60.0% of the

combined fair market value of all of our real estate and real estate-related investments, as

determined at the end of each calendar year beginning with our first full year of operations. For

these purposes, the fair market value of each asset will be equal to the purchase price paid for

the asset or, if the asset was appraised subsequent to the date of purchase, then the fair market

value will be equal to the value reported in the most recent independent appraisal of the asset.

Our policies do not limit the amount we may borrow with respect to any individual investment. As of

December 31, 2010, our aggregate borrowings were 36.5% of the combined fair market value of all of

our real estate and real estate-related investments.

Our board of directors reviews our aggregate borrowings at least quarterly to ensure that such

borrowings are reasonable in relation to our net assets. Our borrowing policies provide that the

maximum amount of such borrowings in relation to our net assets will not exceed 300.0% of our net

assets, unless any excess in such borrowing is approved by a majority of our directors and is

disclosed in our next quarterly report along with the justification for such excess. For purposes

of this determination, net assets are our total assets, other than intangibles, valued at cost

before deducting depreciation, amortization, bad debt and other similar non-cash reserves, less

total liabilities. We compute our leverage at least quarterly on a

consistently applied basis.

Generally, the preceding calculation is expected to approximate 75.0% of the sum of the aggregate

cost of our real estate and real estate-related assets before depreciation, amortization, bad debt

and other similar non-cash reserves. As of March 10, 2011 and December 31, 2010, our leverage did

not exceed 300.0% of the value of our net assets.

By operating on a leveraged basis, we will have more funds available for our investments. This

generally allows us to make more investments than would otherwise be possible, potentially

resulting in enhanced investment returns and a more diversified portfolio. However, our use of

leverage increases the risk of default on loan payments and the resulting foreclosure of a

particular asset. In addition, lenders may have recourse to assets other than those specifically

securing the repayment of the indebtedness.

We will use our best efforts to obtain financing on the most favorable terms available to us

and we will refinance assets during the term of a loan only in limited circumstances, such as when

a decline in interest rates makes it beneficial to prepay an existing loan, when an existing loan

matures or if an attractive investment becomes available and the proceeds from the refinancing can

be used to purchase such investment. The benefits of the refinancing may include an increased cash

flow resulting from reduced debt service requirements, an increase in distributions from proceeds

of the refinancing and an increase in diversification of assets owned if all or a portion of the

refinancing proceeds are reinvested.

Our charter restricts us from borrowing money from any of our directors or from our advisor or

its affiliates unless such loan is approved by a majority of our directors, including a majority of

the independent directors, not otherwise interested in the transaction, as fair, competitive and

commercially reasonable and no less favorable to us than comparable loans between unaffiliated

parties.

Board Review of Our Investment Policies

Our board of directors has established written policies on investments and borrowing. Our

board of directors is responsible for monitoring the administrative procedures, investment

operations and performance of our company and our advisor to ensure such policies are carried out.

Our charter requires that our independent directors review our investment policies at least

annually to determine that our policies are in the best interest of our stockholders. Each

determination and the basis thereof is required to be set forth in the minutes of our applicable

meetings of our directors. Implementation of our investment policies also may vary as new

investment techniques are developed. Our investment policies may not be altered by our board of

directors without the approval of our stockholders.

12

As required by our charter, our independent directors have reviewed our policies outlined

above and determined that they are in the best interest of our stockholders because: (1) they

increase the likelihood that we will be able to acquire a diversified portfolio of income-producing

properties, thereby reducing risk in our portfolio; (2) there are sufficient property acquisition

opportunities with the attributes that we seek; (3) our executive officers, directors and

affiliates of our advisor have expertise with the type of real estate investments we seek; and (4)

our borrowings will enable us to purchase assets and earn rental income more quickly, thereby

increasing our likelihood of generating income for our stockholders and preserving stockholder

capital.

Tax Status

We have not yet elected to be taxed as a REIT under the Code. We intend to make an election to

be taxed as a REIT under Sections 856 through 860 of the Code, and we intend to be taxed as such

beginning with our taxable year ended December 31, 2010. To qualify or maintain our qualification

as a REIT, we must meet certain organizational and operational requirements, including a

requirement to currently distribute at least 90.0% of our annual taxable income, excluding net

capital gains, to our stockholders. As a REIT, we generally will not be subject to federal income

tax on taxable income that we distribute to our stockholders.

If we fail to qualify or maintain our qualification as a REIT in any taxable year, we will

then be subject to federal income taxes on our taxable income at regular corporate rates and will

not be permitted to qualify for treatment as a REIT for federal income tax purposes for four years

following the year during which qualification is lost unless the IRS grants us relief under certain

statutory provisions. Such an event could materially adversely affect our net income and net cash

available for distribution to our stockholders.

Distribution Policy

In order to qualify or maintain our qualification as a REIT for federal income tax purposes,

among other things, we are required to distribute 90.0% of our annual taxable income, excluding net

capital gains, to our stockholders. We cannot predict if we will generate sufficient cash flow to

pay cash distributions to our stockholders on an ongoing basis or at all. The amount of any cash

distributions will be determined by our board of directors and will depend on the amount of

distributable funds, current and projected cash requirements, tax considerations, any limitations

imposed by the terms of indebtedness we may incur and other factors. If our investments produce

sufficient cash flow, we expect to pay distributions to our stockholders on a monthly basis.

Because our cash available for distribution in any year may be less than 90.0% of our annual

taxable income, excluding net capital gains, for the year, we may be required to borrow money, use

proceeds from the issuance of securities (in our offering or subsequent offerings, if any) or sell

assets to pay out enough of our taxable income to satisfy the distribution requirement. These

methods of obtaining funds could affect future distributions by increasing operating costs. We have

not established any limit on the amount of offering proceeds that may be used to fund

distributions, except that, in accordance with our organizational documents and Maryland law, we

may not make distributions that would: (1) cause us to be unable to pay our debts as they become

due in the usual course of business; (2) cause our total assets to be less than the sum of our

total liabilities plus senior liquidation preferences; or (3) jeopardize our ability to maintain

our qualification as a REIT.

To the extent that distributions to our stockholders are paid out of our current or

accumulated earnings and profits, such distributions are taxable as ordinary income. To the extent

that our distributions exceed our current and accumulated earnings and profits, such amounts

constitute a return of capital to our stockholders for federal income tax purposes, to the extent

of their basis in their stock, and thereafter will constitute capital gain. All or a portion of a

distribution to stockholders may be paid from net offering proceeds and thus, constitute a return

of capital to our stockholders.

Monthly distributions are calculated with daily record dates so distribution benefits

begin to accrue immediately upon becoming a stockholder. However, our board of directors could, at

any time, elect to pay distributions quarterly to reduce administrative costs. Subject to

applicable REIT rules, generally we intend to reinvest proceeds from the sale, financing,

refinancing or other disposition of our properties through the purchase of additional properties,

although we cannot assure our stockholders that we will be able to do so.

13

The amount of distributions we pay to our stockholders is determined by our board of

directors and is dependent on a number of factors, including funds available for payment of

distributions, our financial condition,

capital expenditure requirements, annual distribution requirements needed to maintain our

status as a REIT under the Code and restrictions imposed by our organizational documents and

Maryland Law.

See Part II, Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters

and Issuer Purchases of Equity Securities — Distributions, for a further discussion on

distribution rates approved by our board of directors.

Competition

We compete with many other entities engaged in real estate investment activities for

acquisitions of medical office buildings and healthcare-related facilities, including national,

regional and local operators, acquirers and developers of healthcare real estate properties. The

competition for healthcare real estate properties may significantly increase the price we must pay

for medical office buildings and healthcare-related facilities or other assets we seek to acquire,

and our competitors may succeed in acquiring those properties or assets themselves. In addition,

our potential acquisition targets may find our competitors to be more attractive because they may

have greater resources, may be willing to pay more for the properties or may have a more compatible

operating philosophy. In particular, larger healthcare real estate REITs may enjoy significant

competitive advantages that result from, among other things, a lower cost of capital and enhanced

operating efficiencies. In addition, the number of entities and the amount of funds competing for

suitable investment properties may increase. This competition will result in increased demand for

these assets, and therefore, increased prices paid for them. Due to an increased interest in

single-property acquisitions among tax-motivated individual purchasers, we may pay higher prices if

we purchase single properties in comparison with portfolio acquisitions. If we pay higher prices

for medical office buildings or healthcare-related facilities, our business, financial condition,

results of operations and our ability to pay distributions to our stockholders may be materially

and adversely affected and our stockholders may experience a lower return on their investment.

Government Regulations

Many laws and governmental regulations are applicable to our properties and changes in these

laws and regulations, or their interpretation by agencies and the courts, occur frequently.

Costs of Compliance with the Americans with Disabilities Act. Under the Americans with

Disabilities Act of 1990, as amended, or the ADA, all public accommodations must meet federal

requirements for access and use by disabled persons. Although we believe that we are in substantial

compliance with present requirements of the ADA, none of our properties have been audited, nor have

investigations of our properties been conducted to determine compliance. Additional federal, state

and local laws also may require modifications to our properties or restrict our ability to renovate

our properties. We cannot predict the cost of compliance with the ADA or other legislation. We may

incur substantial costs to comply with the ADA or any other legislation.

Costs of Government Environmental Regulation and Private Litigation. Environmental laws and

regulations hold us liable for the costs of removal or remediation of certain hazardous or toxic

substances which may be on our properties. These laws could impose liability without regard to

whether we are responsible for the presence or release of the hazardous materials. Government

investigations and remediation actions may have substantial costs and the presence of hazardous

substances on a property could result in personal injury or similar claims by private plaintiffs.

Various laws also impose liability on a person who arranges for the disposal or treatment of

hazardous or toxic substances and such person often must incur the cost of removal or remediation

of hazardous substances at the disposal or treatment facility. These laws often impose liability

whether or not the person arranging for the disposal ever owned or operated the disposal facility.

As the owner and operator of our properties, we may be deemed to have arranged for the disposal or

treatment of hazardous or toxic substances.

14

Other Federal, State and Local Regulations. Our properties will be subject to various federal,

state and local regulatory requirements, such as state and local fire and life safety requirements.

If we fail to comply with these

various requirements, we may incur governmental fines or private damage awards. While we

believe that our properties will be in material compliance with all of these regulatory

requirements, we do not know whether existing requirements will change or whether future

requirements will require us to make significant unanticipated expenditures that will adversely

affect our ability to make distributions to our stockholders. We believe, based in part on

engineering reports which are generally obtained at the time we acquire the properties, that all of

our properties comply in all material respects with current regulations. However, if we were

required to make significant expenditures under applicable regulations, our financial condition,

results of operations, cash flows and ability to satisfy our debt service obligations and to pay

distributions could be adversely affected.

Significant Tenants

As of December 31, 2010, three of our tenants at our consolidated properties accounted

for 10.0% or more of our aggregate annualized base rent, as follows:

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

Percentage of |

|

|

|

|

|

|

|

|

|

| |

|

Annualized |

|

|

Annualized |

|

|

|

|

GLA |

|

|

Lease Expiration |

| Tenant |

|

Base Rent(1) |

|

|

Base Rent |

|

|

Property |

|

(Square Feet) |

|

|

Date |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Landmark Holdings of

Missouri, LLC |

|

$ |

2,620,000 |

|

|

|

14.4 |

% |

|

Monument Long-Term Acute Care Hospital Portfolio |

|

|

85,000 |

|

|

10/31/25 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Kissito Healthcare |

|

$ |

2,249,000 |

|

|

|

12.4 |

% |

|

Virginia Skilled Nursing Facility Portfolio |

|

|

144,000 |

|

|

01/31/25 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Laurel Health Care Company |

|

$ |

2,034,000 |

|

|

|

11.2 |

% |

|

Virginia Skilled Nursing Facility Portfolio |

|

|

88,000 |

|

|

various - 2016

to 2025 |

| |

|

|

| (1) |

|

Annualized base rent is based on contractual base rent from leases in

effect as of December 31, 2010. The loss of any of these tenants or

their inability to pay rent could have a material adverse effect on

our business and results of operations. |

Geographic Concentration

Based on leases in effect as of December 31, 2010, we owned properties in four states for

which each state accounted for 10.0% or more of our annualized base rent. Virginia accounted for

23.6% of annualized base rent, Ohio accounted for 16.0% of annualized

base rent, Texas accounted

for 13.0% of annualized base rent and Oklahoma accounted for 10.7% of annualized base rent.

Accordingly, there is a geographic concentration of risk subject to fluctuations in each state’s

economy. For a further discussion, see Item 2. Properties — Geographic

Diversification/Concentration Table.

Employees

We have no employees and our executive officers are all employees of our advisor and/or its

affiliates. Our day-to-day management is performed by our advisor and its affiliates. We cannot

determine at this time if or when we might hire any employees, although we do not anticipate hiring

any employees for the next twelve months. We do not directly compensate our executive officers for

services rendered to us. However, our executive officers, consultants and the executive officers

and key employees of our advisor are eligible for awards pursuant to the 2009 Incentive Plan, or

our incentive plan. As of December 31, 2010, no awards had been granted to our executive officers,

consultants or the executive officers or key employees of our advisor under this plan.

Financial Information About Industry Segments

Financial Accounting Standards Board, or FASB, Accounting Standards Codification, or ASC,

Topic 280, Segment Reporting, establishes standards for reporting financial and descriptive

information about a public entity’s reportable segments. We have determined that we have one

reportable segment, with activities related to investing in medical office buildings,

healthcare-related facilities and commercial office properties. Our investments in real estate are

in different geographic regions, and management evaluates operating performance on an individual

asset level. However, as each of our assets have similar economic characteristics, tenants,

products and services, our assets have been aggregated into one reportable segment for the year

ended December 31, 2010 and for the period from January 7, 2009 (Date of Inception) through

December 31, 2009.

15

Investment Risks

There is no public market for the shares of our common stock. Therefore, it will be difficult for

our stockholders to sell their shares of our common stock and, if our stockholders are able to sell

their shares of our common stock, they will likely sell them at a substantial discount.

There currently is no public market for shares of our common stock. We do not expect a public

market for our stock to develop prior to the listing of the shares of our common stock on a

national securities exchange, which we do not expect to occur in the near future and which may not

occur at all. Additionally, our charter contains restrictions on the ownership and transfer of

shares of our stock, and these restrictions may inhibit our stockholders’ ability to sell their

shares of our common stock. Our charter provides that no person may own more than 9.9% in value of

our issued and outstanding shares of capital stock or more than 9.9% in value or in number of

shares, whichever is more restrictive, of the issued and outstanding shares of our common stock.

Any purported transfer of the shares of our common stock that would result in a violation of either

of these limits will result in such shares being transferred to a trust for the benefit of a

charitable beneficiary or such transfer being declared null and void. We have adopted a share

repurchase plan, but it is limited in terms of the amount of shares of our common stock which may

be repurchased annually and subject to our board of directors’ discretion. Our board of directors

may also amend, suspend or terminate our share repurchase plan upon 30 days written notice.

Therefore, it will be difficult for our stockholders to sell their shares of our common stock

promptly or at all. If our stockholders are able to sell their shares of our common stock, they may

only be able to sell them at a substantial discount from the price they paid. This may be the

result, in part, of the fact that, at the time we make our investments, the amount of funds

available for investment may be reduced by up to 11.0% of the gross offering proceeds, which will

be used to pay selling commissions, a dealer manager fee and other organizational and offering

expenses. We also will be required to use the gross proceeds from our offering to pay acquisition

fees, acquisition expenses and asset management fees. Unless our aggregate investments increase in

value to compensate for these fees and expenses, which may not occur, it is unlikely that our

stockholders will be able to sell their shares of our common stock, whether pursuant to our share

repurchase plan or otherwise, without incurring a substantial loss. We cannot assure our

stockholders that their shares of our common stock will ever appreciate in value to equal the price

they paid for their shares of our common stock. Therefore, our stockholders should consider the

purchase of shares of our common stock as illiquid and a long-term investment, and they must be

prepared to hold their shares of our common stock for an indefinite length of time.

Our offering is considered a “blind pool” offering because we have not identified all of the real

estate or real estate-related investments to acquire with the net proceeds from our offering.

We have not identified all of the real estate or real estate-related investments to acquire

with the net proceeds of our offering. As a result, our offering is considered a “blind pool”

offering because investors in our offering are unable to evaluate the manner in which our net

proceeds are invested and the economic merits of our investments prior to subscribing for shares of

our common stock. Additionally, stockholders will not have the opportunity to evaluate the

transaction terms or other financial or operational data concerning the real estate or real

estate-related investments we acquire in the future.

We have a limited operating history. Therefore, our stockholders may not be able to adequately

evaluate our ability to achieve our investment objectives, and the prior performance of other Grubb

& Ellis Group programs may not be an accurate predictor of our future results.

We were formed in January 2009, and our offering was declared effective by the SEC on August

24, 2009, and therefore, we have a limited operating history. As a result, an investment in shares

of our common stock may entail more risks than the shares of common stock of a REIT with a

substantial operating history, and our stockholders should not rely on the past performance of

other Grubb & Ellis Group programs to predict our future results. Our stockholders should consider

our prospects in light of the risks, uncertainties and difficulties frequently encountered by

companies like ours that do not have a substantial operating history, many of which may be beyond

our control. Therefore, to be successful in this market, we must, among other things:

| |

• |

|

identify and acquire investments that further our investment strategy; |

| |

• |

|

rely on our dealer manager to build, expand and maintain its network of licensed

securities brokers and other agents in order to sell shares of our common stock; |

16

| |

• |

|

respond to competition both for investment opportunities and potential investors in

us; and |

| |

• |

|

build and expand our operations structure to support our business. |

We cannot guarantee that we will succeed in achieving these goals, and our failure to do so

could cause our stockholders to lose all or a portion of their investment.

We have experienced losses in the past, and we may experience additional losses in the future.

Historically, we have experienced net losses and we may not be profitable or realize

growth in the value of our investments. Many of our losses can be attributed to start-up costs and

general and administrative expenses, as well as acquisition expenses incurred in connection with

purchasing properties or making other investments. For a further discussion of our operational

history and the factors for our losses, see Part II, Item 7. Management’s Discussion and Analysis

of Financial Condition and Results of Operations and our consolidated financial statements and the

notes thereto.

If we raise substantially less than the maximum offering, we may not be able to invest in a diverse

portfolio of real estate and real estate-related investments, and the value of our stockholders’

investments may fluctuate more widely with the performance of specific investments.

We are dependent upon the net proceeds to be received from our offering to conduct our

proposed activities. Our stockholders, rather than our management or our affiliates, will incur the

bulk of the risk if we are unable to raise substantial funds. Our offering is being made on a “best

efforts” basis, whereby our dealer manager and the broker-dealers participating in our offering are

only required to use their best efforts to sell shares of our common stock and have no firm

commitment or obligation to purchase any of the shares of our common stock. As a result, we cannot

assure our stockholders as to the amount of proceeds that will be raised in our offering or that we

will achieve sales of the maximum offering amount. If we are unable to raise substantially more

than the amount we have raised to date, we will have limited diversification in terms of the number

of investments owned, the geographic regions in which our investments are located and the types of

investments that we make. An investment in shares of our common stock will be subject to greater

risk to the extent that we lack a diversified portfolio of investments. In such event, the

likelihood of our profitability being affected by the poor performance of any single investment

will increase. In addition, our fixed operating expenses, as a percentage of gross income, would be

higher, and our financial condition and ability to pay distributions could be adversely affected if

we are unable to raise substantial funds.

If we are unable to find suitable investments, we may not have sufficient cash flows available

for distributions to our stockholders.

Our ability to achieve our investment objectives and to pay distributions to our stockholders

is dependent upon the performance of our advisor in selecting investments for us to acquire,

selecting tenants for our properties and securing financing arrangements. Except for stockholders

who purchased shares of our common stock in our offering after such time as we supplemented our

prospectus to describe one or more identified investments, our stockholders generally have no

opportunity to evaluate the terms of transactions or other economic or financial data concerning

our investments. Our stockholders must rely entirely on the management ability of our advisor and

the oversight of our board of directors. Our advisor may not be successful in identifying suitable

investments on financially attractive terms or that, if it identifies suitable investments, our

investment objectives will be achieved. If we, through our advisor, are unable to find suitable

investments, we will hold the net proceeds of our offering in an interest-bearing account or invest

the net proceeds in short-term, investment-grade investments. In such an event, our ability to pay

distributions to our stockholders would be adversely affected.

17

We face competition for the acquisition of medical office buildings and other healthcare-related

facilities, which may impede our ability to make acquisitions or may increase the cost of these

acquisitions and may reduce our profitability and could cause our stockholders to experience a

lower return on their investment.

We compete with many other entities engaged in real estate investment activities for

acquisitions of medical office buildings and healthcare-related facilities, including national,

regional and local operators, acquirers and developers of healthcare real estate properties. The

competition for healthcare real estate properties may significantly increase the price we must pay

for medical office buildings and healthcare-related facilities or other assets we seek to acquire,

and our competitors may succeed in acquiring those properties or assets themselves. In addition,

our potential acquisition targets may find our competitors to be more attractive because they may

have greater resources, may be willing to pay more for the properties or may have a more compatible

operating philosophy. In particular, larger healthcare real estate REITs may enjoy significant

competitive advantages that result from, among other things, a lower cost of capital and enhanced

operating efficiencies. In addition, the number of entities and the amount of funds competing for

suitable investment properties may increase. This competition will result in increased demand for

these assets, and therefore, increased prices paid for them. Due to an increased interest in

single-property acquisitions among tax-motivated individual purchasers, we may pay higher prices if

we purchase single properties in comparison with portfolio acquisitions. If we pay higher prices

for medical office buildings or healthcare-related facilities, our business, financial condition

and results of operations and our ability to pay distributions to our stockholders may be

materially and adversely affected and our stockholders may experience a lower return on their

investment.

Our stockholders may be unable to sell their shares of our common stock because their ability to

have their shares of our common stock repurchased pursuant to our share repurchase plan is subject

to significant restrictions and limitations.

Our share repurchase plan includes significant restrictions and limitations. Except in cases

of death or qualifying disability, our stockholders must hold their shares of our common stock for

at least one year. Requesting stockholders must present at least 25.0% of their shares of our

common stock for repurchase and until they have held their shares of our common stock for at least

four years, repurchases will be made for less than they paid for their shares of our common stock.

Shares of our common stock may be repurchased quarterly, at our discretion, on a pro rata basis,

and are limited during any calendar year to 5.0% of the weighted average number of shares of our

common stock outstanding during the prior calendar year. Funds for the repurchase of shares of our

common stock come exclusively from the cumulative proceeds we receive from the sale of shares of

our common stock pursuant to the DRIP. In addition, our board of directors may reject share

repurchase requests in its sole discretion and reserves the right to amend, suspend or terminate

our share repurchase plan at any time upon 30 days written notice. Therefore, in making a decision

to purchase shares of our common stock, our stockholders should not assume that they will be able

to sell any of their shares of our common stock back to us pursuant to our share repurchase plan

and they also should understand that the repurchase price will not necessarily correlate to the

value of our real estate holdings or other assets. If our board of directors terminates our share

repurchase plan, our stockholders may not be able to sell their shares of our common stock even if

they deem it necessary or desirable to do so.

Our advisor may be entitled to receive significant compensation in the event of our liquidation or

in connection with a termination of the Advisory Agreement.

We are externally advised by our advisor pursuant to an Advisory Agreement between us and

our advisor, which has a one-year term that expires June 1, 2011 and is subject to successive

one-year renewals upon the mutual consent of the parties. In the event of a partial or full

liquidation of our assets, our advisor will be entitled to receive an incentive distribution equal

to 15.0% of the net proceeds of the liquidation, after we have received and paid to our

stockholders the sum of the gross proceeds from the sale of shares of our common stock and any

shortfall in an annual 8.0% cumulative, non-compounded return to stockholders in the aggregate. In

the event of a termination of the Advisory Agreement in connection with the listing of our common

stock, the Advisory Agreement provides that our advisor will receive an incentive distribution

equal to 15.0% of the amount, if any, by which (1) the market value of our outstanding common stock

plus distributions paid by us prior to the listing of the shares of our common

stock on a national

18

securities exchange, exceeds (2) the sum of the gross proceeds from the sale of shares of our

common stock plus an annual 8.0% cumulative, non-compounded return on the gross proceeds from the

sale of shares of our common stock. Upon our advisor’s receipt of the incentive distribution upon

listing, our advisor’s

limited partnership units will be redeemed and our advisor will not be entitled to receive any

further incentive distributions upon sales of our properties. Further, in connection with the

termination of the Advisory Agreement other than due to a listing of the shares of our common stock

on a national securities exchange, our advisor shall be entitled to receive a distribution equal to

the amount that would be payable as an incentive distribution upon sales of properties, which

equals 15.0% of the net proceeds if we liquidated all of our assets at fair market value, after we

have received and paid to our stockholders the sum of the gross proceeds from the sale of shares of

our common stock and any shortfall in the annual 8.0% cumulative, non-compounded return to our

stockholders in the aggregate. Upon our advisor’s receipt of this distribution, our advisor’s

limited partnership units will be redeemed and our advisor will not be entitled to receive any

further incentive distributions upon sales of our properties. Any amounts to be paid to our advisor

in connection with the termination of the Advisory Agreement cannot be determined at the present

time, but such amounts, if paid, will reduce the cash available for distribution to our

stockholders.

We may not effect a liquidity event within our targeted time frame of five years after the

completion of our offering stage, or at all. If we do not effect a liquidity event, our

stockholders may have to hold their investment in shares of our common stock for an indefinite

period of time.

On a limited basis, our stockholders may be able to sell shares of our common stock through

our share repurchase plan. However, in the future we may also consider various forms of liquidity

events, including but not limited to: (1) the listing of the shares of our common stock on a

national securities exchange; (2) our sale or merger in a transaction that provides our

stockholders with a combination of cash and/or securities of a publicly traded company; and (3) the

sale of all or substantially all of our real estate and real estate-related investments for cash or

other consideration. We presently intend to effect a liquidity event within five years after the

completion of our offering stage, which we deem to be the completion of our offering and any

subsequent public offerings, or our offerings, excluding any offerings pursuant to the DRIP or that

is limited to any benefit plans. However, we are not obligated, through our charter or otherwise,

to effectuate a liquidity event and may not effect a liquidity event within such time or at all. If

we do not effect a liquidity event, it will be very difficult for our stockholders to have

liquidity for their investment in the shares of our common stock other than limited liquidity

through our share repurchase plan.

Because a portion of the offering price from the sale of shares of our common stock in our

offering is used to pay expenses and fees, the full offering price paid by our stockholders is not

invested in real estate investments. As a result, our stockholders will only receive a full return

of their invested capital if we either (1) sell our assets or our company for a sufficient amount

in excess of the original purchase price of our assets, or (2) list the shares of our common stock

on a national securities exchange and the market value of our company after we list is

substantially in excess of the original purchase price of our assets.

Our board of directors may change our investment objectives without seeking our stockholders’

approval.

Our board of directors may change our investment objectives without seeking our

stockholders’ approval if our directors, in accordance with their fiduciary duties to our

stockholders, determine that a change is in our stockholders’ best interest. A change in our

investment objectives could reduce our payment of cash distributions to our stockholders or cause a

decline in the value of our investments.

Risks Related to Our Business

We have not had sufficient cash available from operations to pay distributions, and, therefore, we

have paid distributions from the net proceeds of our offering, from borrowings in anticipation of

future cash flows or from other sources, such as our sponsor. Any such distributions may reduce the

amount of capital we ultimately invest in assets and negatively impact the value of our

stockholders’ investment.

Distributions payable to our stockholders may include a return of capital, rather than a

return on capital. We have not established any limit on the amount of proceeds from our offering

that may be used to fund distributions, except that, in accordance with our organizational

documents and Maryland law, we may not make distributions that would: (1) cause us to be unable to

pay our debts as they become due in the usual course of business; (2) cause our total assets to be

less than the sum of our total liabilities plus senior liquidation preferences; or (3) jeopardize

our ability to qualify or maintain our qualification as a REIT. The actual amount and timing of