Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

|

þ

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the Fiscal Year Ended December 31, 2010

|

¨

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from to

Commission file number: 001-34090

Tesco Corporation

(Exact name of registrant as specified in its charter)

|

Alberta

|

76-0419312

|

|

(State or Other Jurisdiction

of Incorporation or Organization)

|

(I.R.S. Employer

Identification No.)

|

|

3993 West Sam Houston Parkway North

Suite 100

Houston, Texas

|

77043-1221

|

|

(Address of Principal Executive Offices)

|

(Zip Code)

|

713-359-7000

(Registrant’s telephone number, including area code)

Securities to be registered pursuant to Section 12(b) of the Act:

|

Title of Each Class

|

Name of Each Exchange on Which Registered

|

|

|

Common Shares, without par value

|

Nasdaq Stock Market

|

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes £ No £

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer ¨

|

Accelerated filer þ

|

|

Non-accelerated filer ¨ (Do not check if a smaller reporting company)

|

Smaller reporting company ¨

|

Indicate by check mark whether registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No þ

The aggregate market value of voting and non-voting common equity held by non-affiliates of the registrant at the close of business on June 30, 2010 was $255,597,430 based upon the last sales price reported for such date on the NASDAQ Stock Market. For purposes of this disclosure, shares of common stock held by persons who hold more than 5% of the outstanding shares of common stock and shares held by officers and directors of the registrant as of June 30, 2010 have been excluded as such persons may be deemed to be affiliates. This determination is not necessarily conclusive.

Number of shares of Common Stock outstanding as of February 28, 2011: 38,062,756

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement for the registrant’s 2011 Annual Meeting of Stockholders are incorporated by reference into Part III of this Report on Form 10-K.

|

Page

|

|||||||

|

PART I

|

|||||||

|

Item 1.

|

1

|

||||||

|

Item 1A.

|

7

|

||||||

|

Item 1B.

|

14

|

||||||

|

Item 2.

|

15

|

||||||

|

Item 3.

|

15

|

||||||

|

Item 4.

|

15

|

||||||

|

PART II

|

|||||||

|

Item 5.

|

16

|

||||||

|

Item 6.

|

18

|

||||||

|

Item 7.

|

20

|

||||||

|

Item 7A.

|

31

|

||||||

|

Item 8.

|

32

|

||||||

|

Item 9.

|

32

|

||||||

|

Item 9A.

|

32

|

||||||

|

Item 9B.

|

33

|

||||||

|

PART III

|

|||||||

|

Item 10.

|

34

|

||||||

|

Item 11.

|

34

|

||||||

|

Item 12.

|

34

|

||||||

|

Item 13.

|

34

|

||||||

|

Item 14.

|

34

|

||||||

|

PART IV

|

|||||||

|

Item 15.

|

35

|

||||||

Below is a list of defined terms that are used throughout this document:

|

TESCO CASING DRILLING®

|

= CASING DRILLING

|

|

|

TESCO’s Casing Drive System

|

= CDS™ or CDS

|

|

|

TESCO’s Multiple Control Line Running System

|

= MCLRS™ or MCLRS

|

A list of our trademarks and the countries in which they are registered is presented below:

|

Trademark

|

Country of Registration

|

|

|

TESCO®

|

United States, Canada

|

|

|

TESCO CASING DRILLING®

|

United States

|

|

|

CASING DRILLING®

|

Canada

|

|

|

CASING DRILLING™

|

United States

|

|

|

Casing Drive System™

|

United States, Canada

|

|

|

CDS™

|

United States, Canada

|

|

|

Multiple Control Line Running System™

|

United States, Canada

|

|

|

MCLRS™

|

United States, Canada

|

When we refer to “TESCO”, “we”, “us”, “our”, “ours”, or “the Company”, we are describing Tesco Corporation and our subsidiaries.

PART I

|

Item 1. Business.

|

Business and Strategy

We are a global leader in the design, manufacture and service delivery of technology based solutions for the upstream energy industry. We seek to change the way wells are drilled by delivering safer and more efficient solutions that add real value by reducing the costs of drilling for and producing oil and natural gas. Our product and service offerings consist mainly of equipment sales and services to drilling contractors and oil and natural gas operating companies throughout the world.

We were created on December 1, 1993 through the amalgamation of Shelter Oil and Gas Ltd., Coexco Petroleum Inc., Forewest Industries Ltd. and Tesco Corporation. The amalgamated corporation continued under the name Tesco Corporation, which is organized under the laws of Alberta, Canada.

Our four business segments are:

|

·

|

Top Drives - top drive sales, top drive rentals and after-market sales and services;

|

|

·

|

Tubular Services – proprietary and conventional tubular services;

|

|

·

|

CASING DRILLING – proprietary CASING DRILLING technology; and

|

|

·

|

Research and Engineering – internal research and development activities related to our proprietary tubular services, CASING DRILLING technology and top drive model development.

|

For a further discussion of our business segments, see Part II, Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations and Part II, Item 8, Financial Statements and Supplementary Data, Note 15 included in this Report on Form 10-K.

Top Drive segment

Our Top Drive segment sells equipment and provides services to drilling contractors and oil and natural gas operating companies throughout the world. We provide top drive rental services on a day-rate basis for land and offshore drilling rigs, and we provide after-market sales and service for our customers.

We primarily manufacture top drives that are used in drilling operations to rotate the drill string while suspended from the derrick above the rig floor. Our top drives offer portability and flexibility, permitting drilling companies to conduct top drive drilling for all or any portion of a well. We offer for sale a range of portable and permanently installed top drive products that includes both hydraulically and electrically powered machines capable of delivering 400 to 1,350 horsepower, with a rated lifting capacity of 150 to 750 tons. With each top drive we sell, we offer the services of top drive technicians who provide customers with training, installation and support services.

We offer six distinct model series of top drive systems, using hydraulic, permanent magnet alternating current (“AC”) and induction AC technology. We believe that we are industry leaders in the development and provision of permanent magnet technology in both portable and permanently installed top drive systems. This technology provides very high power density, allowing for high performance and low weight. We use AC induction technology and late generation power electronics in our smaller horsepower systems, such as our EMI machines, allowing the end user to specify its preferred power electronics and motor combination and permitting us to select components from a larger vendor base. EMI top drive units are available with 150 and 250 ton load path configurations. We also developed our EXI system in response to market demands for a high performance compact electric top drive system, commonly required on modern fast moving rigs frequently used in pad drilling operations. The EXI system has a load path rating of 350 tons and generates 600 horsepower at the quill. The HXI is a new generation of our current hydraulic HMI system, incorporating a full suite of operational features and providing a significant gain in performance at the quill. The HXI machine has a load path rating of 250 tons and has a 700 horsepower self-contained diesel driven hydraulic power unit.

In addition to our top drive sales, we rent top drives on a day-rate basis for land and offshore drilling rigs. Our rental fleet offers a range of systems that can be installed in practically any mast configuration, including workover rigs. Our fleet is composed principally of hydraulically powered top drive systems, with power ratings of 475 to 1,350 horsepower and load path ratings of 150 to 750 tons, each equipped with its own independent diesel engine driven hydraulic power unit. This unique combination permits a high level of portability and installation flexibility.

Our top drive rental fleet, which was comprised of 125 units at December 31, 2010, is deployed strategically around the world to be available to customers on a timely basis. Our fleet is highly transportable and we mobilize the top drive units to meet customer requests. In order of size by region from highest to lowest, we currently have rental units in Latin America, the United States and Canada, Russia, Asia-Pacific, the Middle East and Europe. In response to the economic downturn and operating conditions during 2009, we redeployed over 10% of our U.S. fleet to international locations during 2009, including the Middle East, Latin America, Russia and Asia. In 2010, we continued to mobilize top drives to the areas with higher demand and mobilized seven top drives into Russia.

We also provide after-market sales and services to our installed customer base around the globe. We maintain regional stocks of high-demand parts in order to expedite top quality, original replacement parts for top drive systems. Our service offerings include the commissioning of all new units and recertification of working units including top drives, power units and various other top drive product and component repairs. Our field-experienced personnel are responsible for the rig up and installation of all units – both rentals and customer-owned units. Our personnel also provide onsite training and top drive supervision. In addition, technicians are available to perform work under ongoing maintenance contracts.

Markets and Competition

Demand for our top drive products and rental services depends primarily upon capital spending of drilling contractors and oil and natural gas companies and the level of drilling activity. Our customers for top drive sales and after-market sales and service primarily consist of drilling contractors, rig builders and equipment brokers. Occasionally, we may also sell top drives and provide after-market sales and services to major and independent oil and natural gas companies and national oil companies who wish to own and manage their own top drive systems. Our customers for our rental fleet include drilling contractors, major and independent oil and natural gas companies and national oil companies.

We estimate that approximately 60% of land drilling rigs are currently equipped with top drive systems, including the former Soviet Union and China, where few rigs operate with top drives today. By contrast, we estimate that approximately 95% of offshore rigs are equipped with top drives. We were the first top drive manufacturer to provide portable top drives for land drilling rigs. We believe that significant further land-based market potential exists for our top drive drilling system technology, including both portable and permanently installed applications. Further, where many top drive systems approach the end of their useful lives and are inefficient or may not have legacy parts available, we believe that a market for replacement systems will be created. This represents an important opportunity for us.

Our primary competitors in the sale of top drive systems are National Oilwell Varco, Inc. (“NOV”) and Canrig Drilling Technology Ltd., a subsidiary of Nabors Industries Ltd. We believe we have the second largest customer installed base and are the number two global provider of top drives, following NOV. Of the three major top drive system providers, we are the only company that maintains a sizeable fleet of assets solely for the purposes of rental. Competition in the sale of top drive systems takes place primarily on the basis of the features and capacities of the equipment, the quality of the services and technical support offered, delivery lead time and price.

Backlog

We believe that top drive sales backlog is a leading indicator of how our business will be affected by changes in the global macro-economic environment. We consider a product sale order as backlog when the customer has signed a purchase contract, submitted the purchase order and, if required by the purchase agreement, paid a non-refundable deposit. Revenue from services is recognized as the services are rendered, based upon agreed daily, hourly or job rates. Accordingly, we have no backlog for services.

Our top drive sales backlog at December 31, 2010 was 25 units with a total potential revenue value of $33.0 million, compared to 11 units with a total potential revenue value of $16.1 million at December 31, 2009, which reflected a lower order rate as a result of the weakened economic and industry conditions in 2009. Although sales activity has improved in 2010 compared to 2009, our customers have maintained their focus on lowering project costs, and our backlog has not yet returned to pre-recession levels, as evidenced by our backlog of 65 units with a total potential revenue value of $56.9 million at December 31, 2008. Revenues are not recognized until our earnings process is complete, the product has been delivered, collectability is reasonably assured and when title and risk of loss of the equipment is transferred to the customer.

We have the ability to expand or downsize our top drive manufacturing capacity to meet current and expected customer demand. In response to declining demand for our top drives due to industry and operating conditions caused by the recession, we downsized our manufacturing operations substantially during 2009. We maintained a core team, which continues to deliver top drives each month with a current manufacturing capacity of six to eight top drive units per month, depending on system complexity. Current capacity is lower than peak production levels in 2008 of 12 to 16 units per month, which demonstrates the flexibility of our manufacturing operations. We believe that our top drive business needs to maintain manufacturing inventory of one to two quarters of production. This limits our exposure in the event that the sales market softens and allows us to effectively manage our supply chain and workforce, yet allows us to be responsive to our client base.

Tubular Services segment

Our Tubular Services segment includes a suite of proprietary offerings, as well as conventional casing and tubing running services. Casing is steel pipe that is installed in oil, natural gas or geothermal wells to maintain the structural and pressure integrity of the well bore, isolate water bearing surface sands, prevent communication between subsurface strata, and provide structural support of the wellhead and other casing and tubing strings in the well. Most operators and drilling contractors install casing using service companies, like ours, who use specialized equipment and personnel trained for this purpose. Wells can have from two to ten casing strings installed of various sizes. These jobs encompass wells from vertical holes to high angle extended reach wells and include both onshore and offshore applications.

Our proprietary service offerings use certain components of our CASING DRILLING technology, in particular the patented Casing Drive System (“CDS”), to provide a safer and more automated method for running casing and, if required, reaming the casing into the hole. The CDS is a tool which facilitates running and reaming casing into a well bore on any rig equipped with a top drive. This tool offers improved safety and efficiency over traditional methods by eliminating operations that are associated with high risk of personal injury. It also increases the likelihood that the casing can be run to casing point on the first attempt, offers the ability to simultaneously rotate and reciprocate the casing string as required while circulating drilling fluid, and requires fewer people on the rig for casing running operations than traditional methods.

We also offer installation service of deep water smart well completion equipment using our Multiple Control Line Running System (“MCLRS”) proprietary and patented technology. We believe this technology substantially improves the quality of the installation of high-end well completions by eliminating damage and splices to control and injection lines. We also believe this technology improves the speed and safety of the completion process by splitting the work area between personnel making up the tubing and personnel installing completion equipment.

Our conventional service offerings provide equipment and personnel for the installation of tubing and casing, including power tongs, pick-up/lay-down units, torque monitoring services, connection testing services and power swivels for new well construction and in work-over and re-entry operations.

Markets and Competition

Our Tubular Services customers primarily consist of oil and natural gas operating companies, including major and independent companies, national oil companies and, on occasion, other service companies that have contractual obligations to provide tubular running and handling services. Demand for our tubular services strongly depends upon capital spending of oil and natural gas companies and the level of drilling activity.

The conventional tubular services market consists generally of several large, global operators and a large number of small and medium-sized operators that typically operate in limited geographic areas where the market is highly fragmented. The largest global competitors in this market are Weatherford International, Ltd. (“Weatherford International”), Franks International, Inc. and Baker Hughes Incorporated. Competition in the conventional tubular services market takes place primarily on the basis of the quality of the services offered, the quality and utility of the equipment provided, the proximity of the service provider and equipment to the work site and price.

We are aware of competitive technology similar to our CDS tool. We believe that we continue to be the market leader in this technology. Other companies offering similar technology and services include NOV, Weatherford International and Franks International, Inc. Our CDS system is easily and quickly installed on any top drive system and we offer skilled and trained personnel at the field level who have specialized knowledge of top drive drilling system operations.

CASING DRILLING segment

Our CASING DRILLING process uses oilfield casing in place of drill pipe to simultaneously drill and case the well, reducing both drilling time and the chance of unscheduled drilling events. CASING DRILLING technology minimizes the use of conventional drill pipe and drill collars and enables the operators to eliminate pipe trips and case the interval while drilling. This avoids well bore exposure during tripping and mitigates associated risks such as borehole collapse, lost circulation problems and stuck tools or pipe.

The CASING DRILLING retrievable bottomhole assembly, which is comprised of the drill bit and other downhole tools, such as drilling motors, rotary steerable drilling systems, measurement–while–drilling and logging–while–drilling equipment, is lowered via wireline, drill pipe or a tubing string inside the casing and latched to the bottom joint of casing, retaining the ability to maintain the circulation of drilling fluid at all times. Tools are recovered in a similar fashion, by use of wireline, or alternatively drill pipe or a tubing string. Since the casing remains on bottom in the well at all times, wellbore integrity is preserved, and the risk of a well control incident is reduced. Because the well is cased as it is drilled, the potential for unintentional sidetracking is significantly lessened. The risk of tool loss in the hole is also decreased.

Markets and Competition

Our CASING DRILLING customers primarily consist of oil and natural gas operating companies, including major and independent companies, national oil companies and, on occasion, other service companies that have contractual obligations to provide tubular running and handling services. Demand for our CASING DRILLING services strongly depends upon capital spending of oil and natural gas companies and the level of drilling activity.

We are not currently aware of any commercially or technically viable direct competition for our proprietary CASING DRILLING retrievable process, services or products, although several of our competitors are known to have developed prototypes that are similar, and in some cases have deployed them in a field environment. We continue to be the only company offering customers a broad range of tool sizes and the possibility of using casing to drill directional wells combined with specialized equipment that can be readily retrieved when drilling is complete.

We believe that the primary competition to our CASING DRILLING process is the traditional drill pipe drilling process and, to a lesser extent, other methods for casing while drilling that do not involve a retrievable bottom hole assembly. Such alternative methods of casing while drilling offer limited applications because of the cutting structure, and they cannot be combined with directional tools which facilitate the drilling of directional (i.e. non-vertical) wells. While we offer such alternative (i.e. non-retrievable) methods in addition to our proprietary CASING DRILLING process, we believe that Weatherford International has the largest share of the non-retrievable portion of the market.

Research and Engineering segment

As a technology driven company, we continue to invest significantly in research and development activities, primarily related to our proprietary technologies in tubular services, CASING DRILLING and top drive model development. We hold rights, through patents and patent license agreements, to patented and/or patent pending technologies for certain innovations that we believe will have application to our core businesses. We pursue patent protection in appropriate jurisdictions where we believe our innovations could have significant potential application to our core businesses. We hold patents and patent applications in the United States, Canada, Europe, Norway and various other countries. Our patent portfolio currently includes 155 issued patents, comprised of 70 U.S. and 85 foreign patents, and 121 pending patent applications, comprised of 31 U.S. and 90 foreign patent applications. We generally retain all intellectual property rights to our technology through non-disclosure and technology ownership agreements with our employees, suppliers, consultants and other third parties with whom we do business.

The overall design of our portable top drive assembly is protected by patents that will continue in force for several more years. Various specific aspects of the design of the top drive and related equipment are also patented, including the torque track system that improves operational handling by absorbing the torque generated by our top drives. Our CASING DRILLING method and retrievable apparatus are protected by patents that will continue in force for several more years. In addition, we have patents that protect the combination of the retrievable drill bit assembly with a rotary steerable tool. Our CDS is protected by patents on some of the gripping tools and on the “link tilt” system, which is a method used to handle casing. We hold numerous patents related to the installation and utilization of certain accessories for casing for purposes of casing rotation. Various other related methods and tools are patent protected as well.

We have been party to patent infringement claims and we may not be able to protect or enforce our intellectual property rights. For further discussion, see Part I, Item 1A, Risk Factors and Part II, Item 8, Financial Statements and Supplementary Data, Note 11 included in this Report on Form 10-K.

Our research and development costs were $9.1 million, $7.4 million and $11.0 million for the years ended December 31, 2010, 2009 and 2008, respectively. We will continue to invest in the development, commercialization and enhancements of our proprietary technologies.

Financial information about geographic areas

Our Top Drive and CASING DRILLING businesses are distributed globally while our Tubular Services business is more concentrated in the North American markets. We do not track or measure property, plant and equipment by business segment and, as such, this information is not presented. The following table presents our revenue by segment and geographic areas for the years ended December 31, 2010, 2009 and 2008 (in thousands):

|

Top Drive Segment

|

||||||||||||||||||||

|

United States and Canada

|

International

|

Total

|

||||||||||||||||||

|

Revenue

|

%

|

Revenue

|

%

|

Revenue

|

||||||||||||||||

|

2010(1)

|

$ | 137,826 | 57% | $ | 106,107 | 43% | $ | 243,933 | ||||||||||||

|

2009

|

107,348 | 48% | 117,505 | 52% | 224,853 | |||||||||||||||

|

2008

|

187,882 | 55% | 153,550 | 45% | 341,432 | |||||||||||||||

|

Tubular Services Segment

|

||||||||||||||||||||

|

United States and Canada

|

International

|

Total

|

||||||||||||||||||

|

Revenue

|

%

|

Revenue

|

%

|

Revenue

|

||||||||||||||||

|

2010

|

$ | 84,656 | 69% | $ | 37,228 | 31% | $ | 121,884 | ||||||||||||

|

2009

|

78,428 | 66% | 39,871 | 34% | 118,299 | |||||||||||||||

|

2008

|

129,449 | 78% | 37,013 | 22% | 166,463 | |||||||||||||||

|

CASING DRILLING Segment

|

||||||||||||||||||||

|

United Stated and Canada

|

International

|

Total

|

||||||||||||||||||

|

Revenue

|

%

|

Revenue

|

%

|

Revenue

|

||||||||||||||||

|

2010

|

$ | 6,822 | 53% | $ | 6,026 | 47% | $ | 12,848 | ||||||||||||

|

2009

|

6,508 | 48% | 7,188 | 52% | 13,696 | |||||||||||||||

|

2008

|

15,715 | 58% | 11,332 | 42% | 27,047 | |||||||||||||||

|

|

(1) Effective January 1, 2010, we changed the contracts for new top drive sales to generally sell the units directly from our manufacturing facility in Canada. This change increased the amount of top drive revenue recorded in Canada in 2010, compared to 2009 and 2008 presented above.

|

Procurement of Materials and Supplies

For a discussion of the procurement of materials and supplies, see Part II, Item 8, Financial Statements and Supplementary Data, Note 15 included in this Report on Form 10-K.

Seasonality

Our business is subject to seasonal cycles, associated with winter-only, summer-only, dry-season or regulatory-based access to drilling locations. The most significant of these occur in Canada and Russia, where traditionally the first and fourth calendar quarters of each year are the busiest as the contractor fleet can access drilling locations that are only accessible when frozen. As of December 31, 2010, approximately 19% of our top drive rental fleet operated in Canada and Russia.

In certain Asia Pacific and South American regions, we are subject to decline in activities due to seasonal rains. Further, seasonal variations in the demand for hydrocarbons and accessibility of certain drilling locations in North America can affect our business, as our activity follows the active drilling rig count reasonably closely. We actively manage our highly mobile rental fleet around the world to minimize the impact of geographically specific seasonality.

Customers

Our accounts receivable are principally with major international and national oil and natural gas service and exploration and production companies and are subject to normal industry credit risks. We perform ongoing credit evaluations of customers and grant credit based upon past payment history, financial condition and anticipated industry conditions. Customer payments are regularly monitored and a provision for doubtful accounts is established based upon specific situations and overall industry conditions. Many of our customers are located in international areas that are inherently subject to risks of economic, political and civil instabilities, including the effects of currency fluctuations and exchange controls, such as devaluation of foreign currencies and other economic problems, which may impact our ability to collect those accounts receivable. We monitor customers who are at risk for non-payment and, if warranted by the set of circumstances, will lower available credit extended to those customers or establish alternative arrangements, including increased deposit requirements or payment schedules.

No single customer accounted for 10% or more of our consolidated revenue in any of the three years ended December 31, 2010, 2009 and 2008.

Employees

As of December 31, 2010, the total number of our employees worldwide was 1,397. We believe that our relationship with our employees is good. We work to maintain a high level of employee satisfaction and we believe our employee compensation systems are competitive.

Available Information

Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and all amendments thereto, are available free of charge on our internet website at www.tescocorp.com. These reports are posted on our website as soon as reasonably practicable after such reports are electronically filed in the United States (“U.S.”) with the U.S. Securities and Exchange Commission (“SEC”) and in Canada on the System for Electronic Document Analysis and Retrieval (“SEDAR”). Our code of conduct policy is also posted on our website. In addition to our internet website, copies of our U.S. public filings are available at www.sec.gov and copies of our Canadian public filings are available at www.sedar.com.

|

Item 1A. Risk Factors.

|

Cautionary Statement for Purposes of the “Safe Harbor” Provisions of the Private Securities Litigation Reform Act of 1995

This Report on Form 10-K contains forward-looking statements within the meaning of Canadian and United States securities laws, including the United States Private Securities Litigation Reform Act of 1995. From time to time, our public filings, press releases and other communications (such as conference calls and presentations) will contain forward-looking statements. Forward-looking information is often, but not always, identified by the use of words such as “anticipate”, “believe”, “expect”, “plan”, “intend”, “forecast”, “target”, “project”, “may”, “will”, “should”, “could”, “estimate”, “predict” or similar words suggesting future outcomes or language suggesting an outlook. Forward-looking statements in this Report on Form 10-K include, but are not limited to, statements with respect to expectations of our prospects, future revenue, earnings, activities and technical results.

Forward-looking statements and information are based on current beliefs as well as assumptions made by, and information currently available to, us concerning our anticipated financial performance, business prospects, strategies and regulatory developments. Although management considers these assumptions to be reasonable based on information currently available to it, they may prove to be incorrect. The forward-looking statements in this Report on Form 10-K are made as of the date it was issued and we do not undertake any obligation to update publicly or to revise any of the included forward-looking statements, whether as a result of new information, future events or otherwise, except as required by applicable law.

By their very nature, forward-looking statements involve inherent risks and uncertainties, both general and specific, and risks that outcomes implied by forward-looking statements will not be achieved. We caution readers not to place undue reliance on these statements as a number of important factors could cause the actual results to differ materially from the beliefs, plans, objectives, expectations and anticipations, estimates and intentions expressed in such forward-looking statements.

These risks and uncertainties include, but are not limited to, changes in the global economy and credit markets, the impact of changes in oil and natural gas prices and worldwide and domestic economic conditions on drilling activity and demand for and pricing of our products and services, other risks inherent in the drilling services industry (e.g. operational risks, potential delays or changes in customers’ exploration or development projects or capital expenditures, the uncertainty of estimates and projections relating to levels of rental activities, uncertainty of estimates and projections of costs and expenses, risks in conducting foreign operations, the consolidation of our customers, and intense competition in our industry), risks, including litigation risks, associated with our intellectual property and risks associated with the performance of our technology and other risks set forth in Part I, Item 1A, Risk Factors included in this Report on Form 10-K. These risks and uncertainties may cause our actual results, levels of activity, performance or achievements to be materially different from those expressed or implied by any forward-looking statements. When relying on our forward-looking statements to make decisions, investors and others should carefully consider the foregoing factors and other uncertainties and potential events. The forward-looking statements in this document are provided for the limited purpose of enabling current and potential investors to evaluate an investment in us. Readers are cautioned that such statements may not be appropriate, and should not be used, for other purposes.

Risks associated with the global economy

The current global economic and political environment may negatively impact industry fundamentals, and the related decrease in demand for drilling rigs could cause a downturn in the oil and natural gas industry. Such a condition could have a material adverse impact on our business.

An extended deterioration in the global economic environment may impact fundamentals that are critical to our industry, such as the global demand for, and consumption of, oil and natural gas. Reduced demand for oil and natural gas generally results in lower oil and natural gas prices and prolonged weakness in the economy could impact the economics of planned drilling projects, resulting in curtailment, reduction, delay or postponement for an indeterminate period of time. Furthermore, an extended deterioration in the political environment in countries where we operate or that produce significant supply of the world’s demand for oil may also impact fundamentals that are critical to our industry, such as the global supply of oil and natural gas. Constraints in the global supply of oil caused by political turmoil in any of the large oil-producing countries of the world could significantly increase oil and natural gas prices while the removal of such constraints could significantly decrease oil and natural gas prices for an indeterminate period of time. Such volatility in oil and natural gas prices could negatively impact the world economy and our industry. Any long-term reduction in oil and natural gas prices will reduce oil and natural gas drilling and production activity and result in a corresponding decline in the demand for our products and services, which could adversely affect the demand for sales, rentals or services of our top drive units and for our Tubular Services and CASING DRILLING businesses. These reductions could adversely affect the future net realizability of assets, including inventory, fixed assets, goodwill and other intangible assets.

We are exposed to risks associated with the financial markets.

While we intend to finance our operations with existing cash, cash flow from operations and borrowing under our existing credit facility, we may require additional financing to support our growth. If any of the significant lenders, insurance companies or other financial institutions are unable to perform their obligations under our credit agreements, insurance policies or other contracts, and we are unable to find suitable replacements on acceptable terms as a result of recent credit disruptions or otherwise, our results of operations, liquidity and cash flows could be adversely affected.

Many of our customers access the credit markets to finance their oil and natural gas drilling and production activity. The possible inability of these parties to obtain financing on acceptable terms, due to the recent credit disruptions or otherwise, could impair their ability to perform under their agreements with us and lead to various negative effects on us, including business disruption, decreased revenue and increases in bad debt write-offs. A sustained decline in the financial stability of these parties could have an adverse impact on our business and results of operations.

The occurrence or threat of terrorist attacks could materially impact our business.

The occurrence or threat of future terrorist attacks could adversely affect the economies of the United States and other developed countries. A lower level of economic activity could result in a decline in energy consumption, which could cause a decrease in spending by oil and natural gas companies for exploration and development. In addition, these risks could trigger increased volatility in prices for crude oil and natural gas which could also adversely affect spending by oil and natural gas companies. A decrease in spending for any reason could adversely affect the markets for our products and thereby adversely affect our revenue and margins and limit our future growth prospects. Moreover, these risks could cause increased instability in the financial and insurance markets and adversely affect our ability to access capital and to obtain insurance coverage that we consider adequate or are required to obtain by our contracts with third parties.

We face risks related to natural disasters and pandemic diseases, which could materially and adversely disrupt our operations and affect travel required for our worldwide operations.

A portion of our business involves the movement of people and certain parts and supplies to or from foreign locations. Any restrictions on travel or shipments to and from foreign locations, due to the occurrence of natural disasters such as earthquakes; floods or hurricanes; or an epidemic or outbreak of diseases, including the H1N1 virus, in these locations, could significantly disrupt our operations and decrease our ability to provide services to our customers. In addition, our local workforce could be affected by such an occurrence or outbreak which could also significantly disrupt our operations and decrease our ability to provide services to our customers.

Risks associated with the oil and natural gas industry

Our offshore oil and natural gas operations have been, and could be further, adversely impacted by the Deepwater Horizon drilling rig accident and resulting oil spill; changes in and compliance with restrictions or regulations on offshore drilling in the US Gulf of Mexico and in other areas around the world may adversely affect our business and operating results.

On April 20, 2010, a fire and explosion occurred onboard the semisubmersible drilling rig Deepwater Horizon, owned by Transocean Ltd. and under contract to a subsidiary of BP plc. As a result of the incident and related oil spill, the Secretary of the US Department of the Interior directed the Bureau of Ocean Energy Management, Regulation and Enforcement (“BOEMRE”) to issue a suspension, until November 30, 2010, of drilling activities for specified drilling configurations and technologies. Although this moratorium was lifted on October 12, 2010, we cannot predict with certainty when drilling operations will fully resume in the US Gulf of Mexico. The BOEMRE has also issued new guidelines and regulations regarding safety, environmental matters, drilling equipment and decommissioning applicable to drilling in the US Gulf of Mexico, and may take other additional steps that could increase the costs of exploration and production, reduce the area of operations and result in permitting delays.

At this time, we cannot predict with any certainty what further impact, if any, the Deepwater Horizon incident may have on the regulation of offshore oil and natural gas exploration and development activity, or on the cost or availability of insurance coverage to cover the risks of such operations. Ongoing effects of and delays from the lifted suspension of drilling activity in the US Gulf of Mexico, or the enactment of new or stricter regulations in the United States and other countries where we operate, could have a material adverse effect on our financial condition, results of operations or cash flows.

We could be subject to substantial liability claims, which would adversely affect our financial condition, results of operations and cash flows.

Certain equipment and processes are used by us and other companies in the oil and natural gas industry during the delivery of oilfield services in hostile environments, such as exploration, development and production applications. An accident or a failure of a product or process could cause personal injury, loss of life, damage to property, equipment or the environment, and suspension of operations. Our insurance may not protect us against liability for some kinds of events, including events involving pollution, or against losses resulting from business interruption. Moreover, in the future we may not be able to maintain insurance at levels of risk coverage or policy limits that we deem adequate. Substantial claims made under our policies could cause our premiums to increase. Any future damages caused by our products that are not covered by insurance, or are in excess of policy limits or are subject to substantial deductibles, could adversely affect our financial condition, results of operations and cash flows.

We face risks due to the cyclical nature of the energy industry and the corresponding credit risk of our customers.

Changing political, economic or military circumstances throughout the energy producing regions of the world can impact the market price of oil and natural gas for extended periods of time. As most of our accounts receivable are with customers involved in the oil and natural gas industry, any significant change in such circumstances could result in financial exposure in relation to affected customers.

Fluctuations in the demand for and prices of oil and natural gas would negatively impact our business.

Fluctuations in the demand for and prices of oil and natural gas impact the level of drilling activity by our customers and potential customers. The prices are primarily determined by supply, demand, government regulations relating to oil and natural gas production and processing, and international political events, none of which can be accurately predicted. In times of declining activity, not only is there less opportunity for us to sell our products and services but there is increased competitive pressure that tends to reduce our prices and, therefore, our margins.

Possible legislation and regulations related to global warming and climate change could have an adverse effect on our operations and the demand for oil and natural gas.

Foreign, federal, and state authorities and agencies are currently evaluating and promulgating climate-related legislation and regulations that are focused on restricting greenhouse gas (“GHG”) emissions. In the United States, the Environmental Protection Agency (“EPA”) is taking steps to require monitoring and reporting of GHG emissions and to regulate GHGs as pollutants under the Clean Air Act (“CAA”). The EPA’s “Mandatory Reporting of Greenhouse Gases” rule established a comprehensive scheme of regulations that require monitoring and reporting of GHG emissions that began in 2010. Furthermore, the EPA recently proposed additional GHG reporting rules specifically for the oil and natural gas industry. The EPA has also published a final rule, the “Endangerment Finding,” which concluded that GHGs in the atmosphere endanger public health and welfare, and that emissions of GHGs from mobile sources cause or contribute to the GHG pollution. Following issuance of the Endangerment Finding, the EPA promulgated final motor vehicle GHG emission standards on April 1, 2010. The EPA has asserted that the final motor vehicle GHG emission standards will trigger construction and operating permit requirements for stationary sources. In addition, climate change legislation is pending in the United States Congress. These developments may curtail production and demand for fossil fuels such as oil and natural gas in areas of the world where our customers operate and thus adversely affect future demand for our services, which may in turn adversely affect future results of operations. Additionally, federal and/or state legislation to reduce the effects of GHG may potentially have a direct or indirect adverse effect on our operations, including the possible imposition on us and/or our customers of additional operational costs due to carbon emissions generated by oil and gas related activities. Finally, our business could be negatively affected by climate change related physical changes or changes in weather patterns, which could result in damages to or loss of our physical assets, impacts to our ability to conduct operations and/or disruption of our customers’ operations.

Our revenue and earnings are subject to fluctuations period over period and are difficult to forecast.

Our revenue and earnings may vary significantly from quarter to quarter depending upon:

|

·

|

the level of drilling activity worldwide, as well as the particular geographic focus of the activity;

|

|

·

|

the variability of customer orders, which are particularly unpredictable in international markets;

|

|

·

|

the levels of inventories of our products held by end-users and distributors;

|

|

·

|

the mix of our products sold or leased and the margins on those products;

|

|

·

|

new products offered and sold or leased by us or our competitors;

|

|

·

|

weather conditions or other natural disasters that can affect our operations or our customers’ operations;

|

|

·

|

changes in oil and natural gas prices and currency exchange rates, which in some cases affect the costs and prices for our products;

|

|

·

|

the level of capital equipment project orders, which may vary with the level of new rig construction and refurbishment activity in the industry;

|

|

·

|

changes in drilling and exploration plans which can be particularly volatile in international markets;

|

|

·

|

the variability of customer orders or a reduction in customer orders, which may leave us with excess or obsolete inventories;

|

|

·

|

the ability of our vendors to timely supply necessary component parts used for the manufacturing of our products; and

|

|

·

|

the ability to manufacture and timely deliver customer orders, particularly in the top drive segment due to the increasing size and complexity of our models.

|

In addition, our fixed costs cause our margins to decrease when demand is low and service capacity is underutilized.

Any significant consolidation or loss of end-user customers could have a negative impact on our business.

Exploration and production company operators and drilling contractors have undergone substantial consolidation in recent years. Additional consolidation is probable. In addition, many oil and natural gas properties could be transferred over time to different potential customers.

Consolidation of drilling contractors results in fewer end-users for our products and could result in the combined contractor standardizing its equipment preferences in favor of a competitor’s products.

Merger activity among both major and independent oil and natural gas companies also affects exploration, development and production activity, as these consolidated companies attempt to increase efficiency and reduce costs. Generally, only the more promising exploration and development projects from each merged entity are likely to be pursued, which may result in overall lower post-merger exploration and development budgets. Moreover, some end-users prefer not to use relatively new products or premium products in their drilling operations.

We operate in an intensively competitive industry and if we fail to compete effectively our business will suffer.

Our competitors may attempt to increase their market share by reducing prices or our customers may adopt competing technologies. The drilling industry is driven primarily by cost minimization. Our strategy is aimed at reducing drilling costs through the application of new technologies. Our competitors, many of whom have a more diverse product line and access to greater amounts of capital than we do, have the ability to compete against the cost savings generated by our technology by reducing prices and by introducing competing technologies. Our competitors may also have the ability to offer bundles of products and services to customers that we do not offer. We have limited resources to sustain prolonged price competition and maintain the level of investment required to continue the commercialization and development of our new technologies.

To compete in our industry, we must continue to develop new technologies and products.

The markets for our products and services are characterized by continual technological developments and we have identified our products as providing technological advantages over other competitive products. As a result, substantial improvements in the scope and quality of product function and performance can occur over a short period of time. If we are not able to develop commercially competitive products in a timely manner in response to changes in technology, our business may be adversely affected. Our future ability to develop new products depends on our ability to:

|

·

|

design and commercially produce products that meet the needs of our customers,

|

|

·

|

successfully market new products, and

|

|

·

|

obtain and maintain patent protection.

|

We may encounter resource constraints, technical barriers, or other difficulties that would delay introduction of new products and services in the future. Our competitors may introduce new products or obtain patents before we do and achieve a competitive advantage. Additionally, the time and expense invested in product development may not result in commercial applications.

For example, from time to time, we have incurred significant losses in the development of new technologies which were not successful for various commercial or technical reasons. If we are unable to successfully implement technological or research and engineering type activities, our growth prospects may be reduced and our future revenue may be materially and adversely affected. Moreover, we may experience operating losses after new products are introduced and commercialized because of high start-up costs, unexpected manufacturing costs or problems, or lack of demand.

Risks associated with our business

We have been party to patent infringement claims and we may not be able to protect or enforce our intellectual property rights.

In two separate actions, we were sued by VARCO I/P, Inc. and Weatherford International, who have alleged that our CDS tool and other equipment and processes violate certain of their patents. See Part II, Item 8, Financial Statements and Supplementary Data, Note 11 included in this Report on Form 10-K. We settled our lawsuit with Weatherford International, and we believe the suit with VARCO I/P, Inc. is without merit. We intend to continue to defend ourselves vigorously. In the event that we are not successful in defending ourselves in this matter, it may have a material adverse effect on our Tubular Services and CASING DRILLING segments and, therefore, on our business. In addition, in the future we may be subject to other infringement claims and if any of our products were found to be infringing, our consolidated financial results may be adversely affected.

Some of our products and the processes used to produce them have been granted U.S. and international patent protection, or have patent applications pending. Nevertheless, patents may not be granted from our applications and, if patents are issued, the claims allowed may not be sufficient to protect our technology. Recent changes in U.S. patent law may have the effect of making certain of our patents more likely to be the subject of claims for invalidation.

Our competitors may be able to independently develop technology that is similar to ours without infringing on our patents. This is especially true internationally where the protection of intellectual property rights may not be as effective. In addition, obtaining and maintaining intellectual property protection internationally may be significantly more expensive than doing so domestically. We may have to spend substantial time and money defending our patents. After our patents expire, our competitors will not be legally constrained from marketing products substantially similar to ours.

We are subject to legal proceedings and may, in the future, be subject to additional legal proceedings.

We are currently involved in legal proceedings described in Part II, Item 8, Financial Statements and Supplementary Data, Note 11 including in this Report on Form 10-K. From time to time, we may become subject to additional legal proceedings which may include contract, tort, intellectual property, tax, regulatory compliance and other claims.

We are also subject to complaints or allegations from former, current or prospective employees from time to time, alleging violations of employment-related laws. Lawsuits or claims could result in decisions against us which could have a material adverse effect on our financial condition, results of operations or cash flows.

Our products and services are used in hazardous conditions, and we are subject to risks relating to potential liability claims.

Most of our products are used in hazardous drilling and production applications where an accident or a failure of a product can have catastrophic consequences. For example, the unexpected failure of a top drive to rotate a drill string during drilling operations could result in the loss of control over a well, leading to blowout and the discharge of pollutants into the environment. Damages arising from an occurrence at a location where our products are used have in the past and may in the future result in the assertion of potentially large claims against us.

While we attempt to limit our exposure to such risks through contracts with our customers, these measures may not protect us against liability for certain kinds of events, including blowouts, cratering, explosions, fires, loss of well control, loss of hole, damaged or lost drilling equipment, damage or loss from inclement weather or natural disasters, and losses resulting from business interruption. Our insurance coverage generally provides that we assume a portion of the risk in the form of a self-insured retention, and may not be adequate in risk coverage or policy limits to cover all losses or liabilities that we may incur. The occurrence of an event not fully insured or indemnified against, or the failure of a customer or insurer to meet its indemnification or insurance obligations, could result in substantial losses. Moreover, we may not be able in the future to maintain insurance at levels of risk coverage or policy limits that we deem adequate. Any significant claims made under our policies will likely cause our premiums to increase. Any future damages caused by our products or services that are not covered by insurance, are in excess of policy limits or are subject to substantial deductibles, could reduce our earnings and cash available for operations.

Environmental compliance and remediation costs and the costs of environmental liabilities could exceed our estimates.

The energy industry is affected by changes in public policy, federal, state and local laws and regulations. The adoption of laws and regulations curtailing exploration and development drilling for oil and natural gas for economic, environmental and other policy reasons may adversely affect our operations due to our customers having limited drilling and other opportunities in the oil and natural gas exploration and production industry. The operations of our customers, as well as our properties, are subject to increasingly stringent laws and regulations relating to environmental protection, including laws and regulations governing air emissions, water discharges, waste management and workplace safety.

Our credit facility contains restrictions that may limit our ability to finance future operations or capital needs and could accelerate debt payments.

Our credit facility contains restrictive covenants which limit the amount of borrowings available by the maintenance of certain financial ratios. Decreases in our financial performance could prohibit us from borrowing amounts under our credit facility, force us to make repayments of outstanding debt in order to remain in compliance with these restrictive covenants, or accelerate our debt payments and other financing obligations and those of our subsidiaries. Additionally, our credit agreements are collateralized by equity interests in our subsidiaries. A breach of the covenants under these agreements could permit the lenders to exercise their rights to foreclose on these collateral interests. If this were to occur, we might not be able to repay such debt and other financing obligations. These restrictions may negatively impact our ability to finance future operations, implement our business strategy or fund our capital needs. Compliance with these financial ratios may be affected by events beyond our control, including the risks and uncertainties described in the other risk factors discussed elsewhere in this report.

For further discussion of our credit facility, see Part II, Item 8, Financial Statements and Supplementary Data, Note 7 included in this Report on Form 10-K.

We have a revolving credit facility that is not contracted at market rates.

Our credit facility contains provisions for interest rates on borrowings and commitment fees that were established prior to the credit crisis of 2008 and 2009. If we needed to replace our credit facility in today’s bank loan market, for any reason, including an event of default on our part, we may be unable to negotiate lending terms at the same or substantially similar rates, or for the same borrowing capacity, that we currently hold. Any change in the terms of our fees or borrowing capacity could adversely affect our liquidity and results of operations.

At this time it is difficult to forecast the future state of the bank loan market. As a result of the uncertain state of various financial institutions and the credit markets generally, we may be unable to maintain our current borrowing capacity in the event of bank or banks failure to fund any commitments under the current credit facility, and we may not be able to refinance our bank facility in the same amount and on the same terms as we currently hold, which could negatively impact our liquidity and results of operations.

We provide warranties on our products and if our products fail to operate properly our business will suffer.

We provide warranties as to the proper operation and conformance to specifications of the equipment we manufacture. Our products are often deployed in harsh environments including subsea applications. The failure of these products to operate properly or to meet specifications may increase our costs by requiring additional engineering resources and services, replacement of parts and equipment or monetary reimbursement to a customer. We have experienced quality problems with raw material vendors, which required us to recall and replace certain equipment and components. We have also received warranty claims and we expect to continue to receive them in the future. Such claims may exceed the reserve we have set aside for them. To the extent that we incur substantial warranty claims in any period because of quality issues with our products, our reputation, ability to obtain future business and earnings could be materially and adversely affected.

Our foreign operations and investments involve special risks.

We sell products and provide services in parts of the world where the political and legal systems are very different from those in the United States and Canada. In places like Russia, Latin America, the Middle East and Asia/Pacific, we may have difficulty or extra expense in navigating the local bureaucracies and legal systems. We may face challenges in enforcing contracts in local courts or be at a disadvantage when we have a dispute with a customer that is an agency of the state. We may be at a disadvantage to competitors that are not subject to the same international trade and business practice restrictions that U.S. and Canadian laws impose on us.

While diversification is desirable, it can expose us to risks related to cultural, political and economic factors of foreign jurisdictions which are beyond our control. As a general rule, we have elected not to carry political risk insurance against these risks. Such risks include the following:

|

·

|

loss of revenue, property and equipment as a result of hazards such as wars or insurrection;

|

|

·

|

the effects of currency fluctuations and exchange controls, such as devaluation of foreign currencies and other economic problems;

|

|

·

|

changes or interpretations in laws, regulations and policies of foreign governments, including those associated with changes in the governing parties, nationalization, and expropriation; and

|

|

·

|

protracted delays in securing government consents, permits, licenses, or other regulatory approvals necessary to conduct our operations

|

|

·

|

protracted delays in the collection of accounts receivable due to economic, political and civil instabilities.

|

Our profitability is driven to a large extent by our ability to deliver the products we manufacture in a timely manner.

Disruptions to our production schedule may adversely impact our ability to meet delivery commitments. If we fail to deliver products according to contract terms, we may suffer financial penalties and a diminution of our commercial reputation and future product orders.

We rely on the availability of raw materials, component parts and finished products to produce our products.

We buy raw materials, components and precision machining or sub-assembly services from many different vendors located in Canada, the United States, Europe, South East Asia and the Middle East. The price and lead times for some products have fluctuated along with the general changes of steel prices around the world. We also source a substantial

amount of electrical components, including permanent magnet motors and drives as well as a substantial amount of hydraulic components, including hydraulic motors, from suppliers located in the U.S. and abroad. The inability of suppliers to meet performance, quality specifications and delivery schedules could cause delays in manufacturing and make it difficult or impossible for us to meet outstanding orders or accept new orders for the manufacture of the affected equipment.

The design of some of our equipment is based on components provided by specific sole source manufacturers.

Some of our products have been designed around components which are only available from one source of supply. In some cases, a manufacturer has developed or modified the design of a component at our request, and consequently we are the only purchaser of such items. If the manufacturer of such an item should go out of business or cease or refuse to manufacture the component in question, or raise the price of such components unduly, we may have to identify alternative components and redesign portions of our equipment. This could cause delays in manufacturing and make it difficult or impossible for us to meet outstanding orders or accept new orders for the manufacture of the affected equipment.

Our business requires the retention and recruitment of a skilled workforce and key employees, and the loss of such employees could result in the failure to implement our business plans.

As a technology based company, we depend upon skilled engineering and other professionals in order to engage in product innovation and ensure the effective implementation of our innovative technology, especially CASING DRILLING. We compete for these professionals, not only with other companies in the same industry, but with oil and natural gas service companies generally and other industries. In periods of high energy and industrial manufacturing activity, demand for the skills and expertise of these professionals increases, which can make the hiring and retention of these individuals more difficult and expensive. Failure to recruit and retain such individuals may result in our inability to maintain a competitive advantage over other companies and loss of customer satisfaction. The loss or incapacity of certain key employees for any reason, including our President and Chief Executive Officer, Julio M. Quintana, could have a negative impact on our ability to implement our business plan due to the specialized knowledge these individuals possess.

Our business relies on the skills and availability of trained and experienced trades and technicians to provide efficient and necessary services to us and our customers. Hiring and retaining such individuals are critical to the success of our business plan. Retention of staff and the prevention of injury to staff are essential in order to provide a high level of service.

We have identified a material weakness in our internal controls.

Our management has concluded that our disclosure controls and procedures and internal control over financial reporting were not effective as of December 31, 2010. As a result, this Form 10-K includes an adverse opinion from PricewaterhouseCoopers LLP, our independent registered public accounting firm, on our internal control over financial reporting. A description of the material weakness in our internal controls over financial reporting is included in Part II, Item 9A, Controls and Procedures in this Report on Form 10-K.

A material weakness is a deficiency, or a combination of deficiencies, in internal control over financial reporting, such that there is a reasonable possibility that a material misstatement of the company's annual or interim financial statements will not be prevented or detected on a timely basis.

The control deficiency resulted in the identification of several immaterial errors in the income tax provision and related deferred tax balances which impacted the prior period financial statements. Although these errors did not result in the restatement of our consolidated financial statements, this control deficiency could result in a material misstatement of certain tax accounts and disclosures that would not be prevented or detected on a timely basis. Additionally, ineffective internal control over financial reporting could cause investors to lose confidence in our reported financial information, which could have a negative effect on the trading of our securities.

|

Item 1B. Unresolved Staff Comments.

|

None.

|

Item 2. Properties.

|

The following table details our principal facilities, including (i) all properties which we own, and (ii) those leased properties which serve as corporate or regional headquarters.

|

Location

|

Approximate Square Footage (Buildings)

|

Owned or Leased

|

Description

|

|||

|

Houston, Texas

|

26,500

|

Leased

|

Corporate headquarters.

|

|||

|

Houston, Texas

|

67,800

|

Owned

|

Headquarters for North American operations in Top Drive, Tubular Services and CASING DRILLING segments, and our U.S. regional operations base which also provides equipment repair and maintenance for U.S. and certain overseas operations.

|

|||

|

Kilgore, Texas

|

21,900

|

Owned

|

Regional operations base for the Tubular Services segment in east Texas and northern Louisiana.

|

|||

|

Lafayette, Louisiana

|

43,300

|

Owned

|

Regional operations base for the Tubular Services segment in southern Louisiana and the Gulf of Mexico.

|

|||

|

Calgary, Alberta, Canada

|

85,000

|

Owned

|

Manufacturing of top drives and other equipment.

|

|||

|

Mexico City, Mexico

|

1,615

|

Leased

|

Regional headquarters for Latin America, including Mexico.

|

|||

|

Aberdeen, Scotland

|

22,700

|

Leased

|

Regional headquarters for Europe and West Africa.

|

|||

|

Moscow, Russia

|

3,987

|

Leased

|

Regional headquarters for the former Soviet Union.

|

|||

|

Dubai, United Arab Emirates

|

3,800

|

Leased

|

Regional headquarters for the Middle East, North Africa and East Africa.

|

|||

|

Republic of Singapore

|

15,500

|

Leased

|

Regional headquarters for India, China, Japan, Australia and New Zealand.

|

|||

In addition, we lease operational facilities at locations in Texas, Colorado, Pennsylvania, Arkansas, North Dakota and Wyoming. Each of these locations supports operations in its local area, primarily for the Tubular Services segment.

Outside the U.S., we lease additional operating facilities Canada, Mexico, Venezuela, Colombia, Ecuador, Argentina, Brazil, Norway, Russia, Dubai, Indonesia, Australia and New Zealand. The majority of these facilities support the Top Drive, Tubular Services and CASING DRILLING segments.

We consider our existing equipment and facilities to be adequate to support our operations.

|

Item 3. Legal Proceedings.

|

The information with respect to this Item 3 is set forth in Part II, Item 8, Financial Statements and Supplementary Data, Note 11 included in this Report on Form 10-K.

|

Item 4. (Removed and Reserved)

|

PART II

|

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

|

Market Information

Our outstanding shares of common stock are traded on the Nasdaq Stock Market (“NASDAQ”) under the symbol “TESO.” The following table outlines the share price trading range and volume of shares traded by quarter for 2010 and 2009.

|

Share Price Trading Range

|

||||||||

|

High

|

Low

|

|||||||

|

($ per share)

|

||||||||

|

2010

|

||||||||

|

1st Quarter

|

$ | 15.24 | $ | 10.85 | ||||

|

2nd Quarter

|

13.51 | 9.00 | ||||||

|

3rd Quarter

|

14.47 | 9.64 | ||||||

|

4th Quarter

|

16.40 | 11.30 | ||||||

|

2009

|

||||||||

|

1st Quarter

|

$ | 10.34 | $ | 6.25 | ||||

|

2nd Quarter

|

11.41 | 7.55 | ||||||

|

3rd Quarter

|

10.28 | 6.38 | ||||||

|

4th Quarter

|

13.29 | 7.59 | ||||||

As of February 28, 2011, there were approximately 238 holders of record of our common stock, including brokers and other nominees.

Dividend Policy

We have not declared or paid any dividends since 1993 and do not expect to declare or pay dividends in the near future. Any decision to pay dividends on our common shares will be made by our Board of Directors on the basis of our earnings, financial requirements and other relevant conditions existing at the time. Pursuant to our Amended and Restated Credit Agreement, we are currently prohibited from paying dividends to our shareholders.

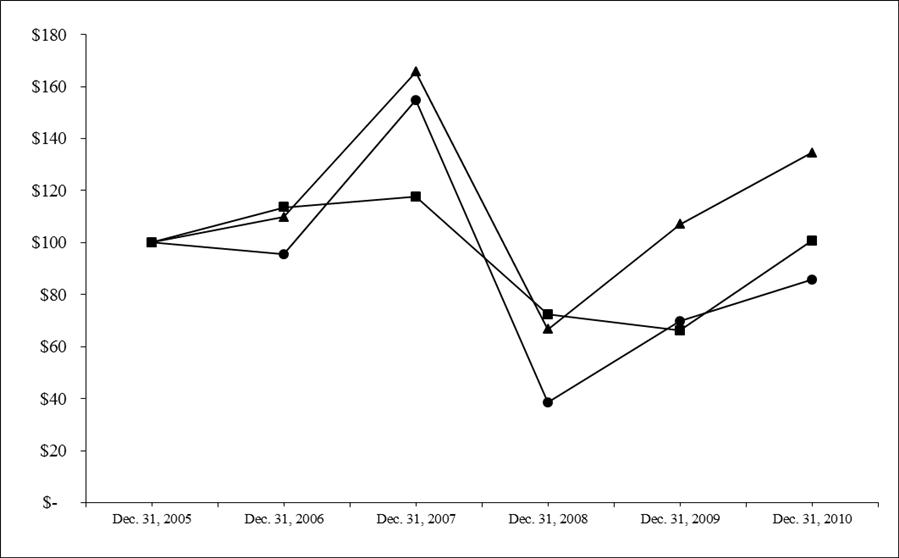

Performance graph

The following performance graph and table compares the yearly percentage change in the cumulative shareholder return for the five year period commencing on December 31, 2005 and ending on December 31, 2010 on our common shares (assuming a $100 investment was made on December 31, 2005) with the total cumulative return of the S&P 500 Composite Index and the Philadelphia Oil Service Sector Index (“OSX”), assuming reinvestment of dividends.

|

Dec. 31, 2005

|

Dec. 31, 2006

|

Dec. 31, 2007

|

Dec. 31, 2008

|

Dec. 31, 2009

|

Dec. 31, 2010

|

|||||||||||||||||||

|

● Tesco Corp.

|

$ | 100 | $ | 95 | $ | 155 | $ | 39 | $ | 70 | $ | 86 | ||||||||||||

|

■ S & P 500

|

$ | 100 | $ | 114 | $ | 118 | $ | 72 | $ | 66 | $ | 101 | ||||||||||||

|

▲ OSX

|

$ | 100 | $ | 110 | $ | 166 | $ | 67 | $ | 107 | $ | 135 | ||||||||||||

|

Item 6. Selected Financial Data.

|

The following selected historical financial data as of December 31, 2010 and 2009 and for each of the years ended December 31, 2010, 2009 and 2008 is derived from the audited consolidated financial statements included in Part II, Item 8, Financial Statements and Supplementary Data in this Report on Form 10-K. The selected financial data as of December 31, 2008, 2007 and 2006 and for each of the years ended December 31, 2007 and 2006 are derived from audited consolidated financial statements. The selected financial data is not necessarily indicative of results to be expected in future periods and should be read in conjunction with Part II, Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations and Item 8, Financial Statements and Supplementary Data included in this Report on Form 10-K.

|

Years Ended December 31,

|

||||||||||||||||||||

|

2010

|

2009

|

2008

|

2007

|

2006

|

||||||||||||||||

|

Statements of income (loss) data:

|