Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - HARLAND CLARKE HOLDINGS CORP | form8k_091610.htm |

2010 Credit Suisse

Global Credit Products Conference

September 16, 2010

2

Forward looking statements

Certain information in this presentation may be considered forward-looking

information within the definition of the Private Securities Litigation Reform

Act of 1995. This information is based on the Company's current expectations

and actual results could vary materially depending on risks and uncertainties

that may affect the Company's operations, markets, services, prices and

other factors as discussed in filings with the Securities and Exchange

Commission. These risks and uncertainties include, but are not limited to,

general and economic conditions and declines in the industries in which we

participate. There is no assurance that the Company's expectations will be

realized. All forward-looking statements speak only as of the date of this

presentation. All subsequent written and oral forward-looking statements

attributable to us or any person acting on our behalf are qualified by the

cautionary statements in this section. The Company assumes no obligation to

update any forward-looking information contained in this presentation.

information within the definition of the Private Securities Litigation Reform

Act of 1995. This information is based on the Company's current expectations

and actual results could vary materially depending on risks and uncertainties

that may affect the Company's operations, markets, services, prices and

other factors as discussed in filings with the Securities and Exchange

Commission. These risks and uncertainties include, but are not limited to,

general and economic conditions and declines in the industries in which we

participate. There is no assurance that the Company's expectations will be

realized. All forward-looking statements speak only as of the date of this

presentation. All subsequent written and oral forward-looking statements

attributable to us or any person acting on our behalf are qualified by the

cautionary statements in this section. The Company assumes no obligation to

update any forward-looking information contained in this presentation.

3

Introductions

n Over 34 years of

experience in the financial

services and security

printing industry

experience in the financial

services and security

printing industry

n Over 17 years with Clarke

American / Harland

Clarke

American / Harland

Clarke

n Former Chief Executive

Officer of Rocky Mountain

Bank Note

Officer of Rocky Mountain

Bank Note

n Marketing representative

for IBM out of graduate

school

for IBM out of graduate

school

Chuck Dawson

President & CEO,

Harland Clarke Holdings

n 17 years of experience

with Harland Clarke,

Honeywell, and GE in

various financial and

operations leadership

roles

with Harland Clarke,

Honeywell, and GE in

various financial and

operations leadership

roles

n Over 5 years with Clarke

American / Harland

Clarke

American / Harland

Clarke

n Former Chief Financial

Officer of Honeywell’s

Aircraft Landing Systems

business

Officer of Honeywell’s

Aircraft Landing Systems

business

Peter Fera

EVP & CFO,

Harland Clarke Holdings

4

World class

operations

Leading

presence

Diversified,

blue-chip

client portfolio

n A leading provider of checks and related products, marketing services, and customized

business and home office products

business and home office products

n A leading provider of software and services to financial institutions

n A leading provider of education related products and survey technologies

n $1.7 billion in combined revenues for LTM Q2 2010

n Over 11,000 financial institutions clients such as:

n Harland Clarke: 5 contact centers and 12 plants, supported by a national sales organization

n Harland Financial Solutions: 17 fully networked facilities focused on customer support and

enhancement of software solutions

enhancement of software solutions

n Scantron: 6 facilities, which include manufacturing, technology and services

n 2001 Malcolm Baldrige National Quality Award winner

Strong, long-

term client

relationships

n Trusted, integrated relationships with clients

n Provider of mission-critical software products

n Strong partnerships with long-term contracts

Harland Clarke Holdings

5

Who we are

n Checks and related products

n Marketing Services

n Business and home office

products

products

n Financial and business forms

n Core processing systems

n Internet and mobile banking

applications

applications

n Risk management solutions

n Branch automation solutions

n Lending origination and

compliance

compliance

n Web-based assessment

products

products

n Student Achievement

Management solutions

Management solutions

n Response to Intervention

products

products

n Survey Services

n Scanners and forms

Revenues(1) $1.2B

Revenues(1) $280M

Revenues(1) $203M

(1) LTM Q2 2010; revenues are adjusted to add back acquisition accounting fair value adjustments of deferred revenue.

6

Diversified business and product lines

§ Combined business has four major product lines

– Checks and office products

– Software and related services

– Direct marketing services

– Data collection, testing and survey solutions

$1.7 billion

LTM Q2 2010 Revenue

Revenue for Non-Check Products

Continued success diversifying product lines

7

Diversified and expanded client relationships

Approximately 80% of revenue is under long-term contracts

Direct to Consumer

and Commercial

and Commercial

Financial Institutions

Education

8

Strong history of cost reductions and margin expansion

History of continuous improvement

n Demonstrated track-record of margin

improvement

improvement

n Margin expansion of 4.4 points since 2008

n 16 facility closures since the start of 2007

n Exceeded synergy target of $112.6M from

the John H. Harland acquisition

the John H. Harland acquisition

(1) See page 16 for the calculation of and reconciliation of net income to adjusted EBITDA

9

n A leading provider of checks and office

products and marketing and contact

center services

products and marketing and contact

center services

– 11,000 financial and commercial institution

clients

clients

– More than 80% of revenues under long-term

contract

contract

n Diverse product and service offerings

– Personal and business checks

– Marketing services including database

marketing, eMarketing, creative

development, and strategic services

marketing, eMarketing, creative

development, and strategic services

– Contact center services

– Financial and business forms

– Deposit products including deposit tickets,

security bags, cash straps, coin wraps

security bags, cash straps, coin wraps

– Address labels, self-inking stamps,

checkbook covers, registers

checkbook covers, registers

– Card services

10

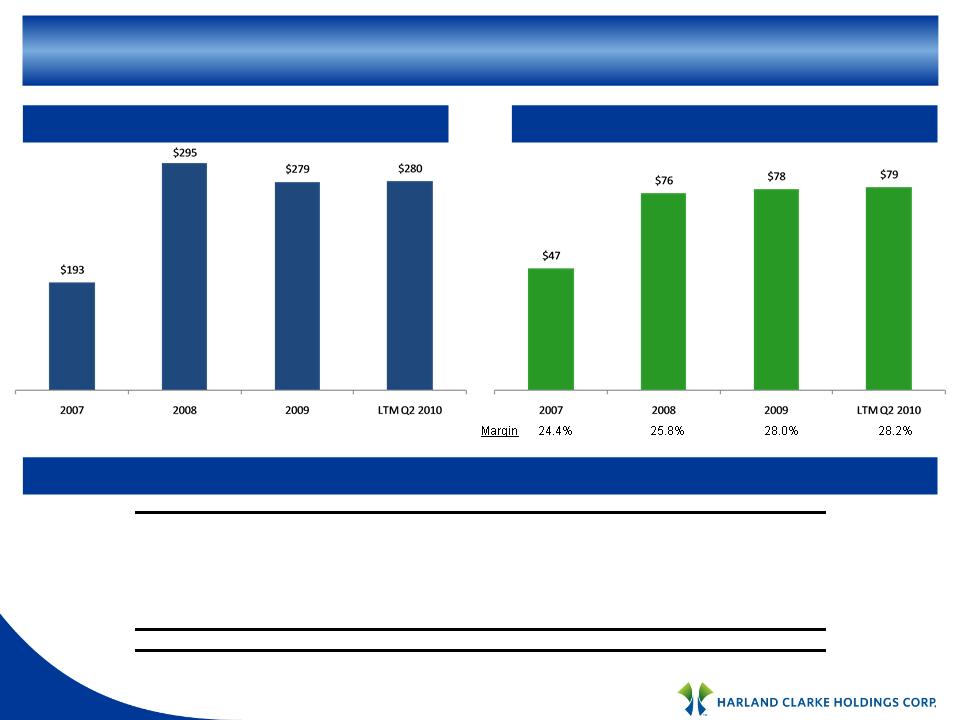

Harland Clarke financial performance

$ in millions

Margin 26.4% 26.3% 29.7% 30.9%

Revenue(1)

Adjusted EBITDA

Reconciliation to Adjusted EBITDA

$ in millions

(1) Revenue is adjusted to add back acquisition accounting fair value adjustments of deferred revenue.

2007

2008

2009

LTM Q2 2010

Operating income

181.1

$

217.1

$

195.8

$

224.5

$

D&A

98.2

112.5

109.3

107.3

Restructuring

5.6

8.3

25.7

10.6

Asset impairment charges

3.1

1.5

33.4

34.0

Impact of acquisition accounting adjustments

1.9

-

-

0.5

Transaction related expenses

2.4

-

-

-

Adjusted EBITDA

292.3

$

339.4

$

364.2

$

376.9

$

11

n A leading supplier of software and services

to financial institutions

to financial institutions

– Core processing systems

– Internet and mobile banking applications

– Risk management solutions

– Branch automation solutions

– Lending origination and compliance

n High switching costs associated with

switching integrated software providers

switching integrated software providers

n Sell to approximately 37% of all financial

institutions in the United States

institutions in the United States

n Top 25 customers < 10% of revenue

n Recurring revenues of more than 75%

Customer Mix

Strong recurring revenue base

12

HFS financial performance

$ in millions

Revenue(1)

Adjusted EBITDA

Reconciliation to Adjusted EBITDA

$ in millions

(1) Revenue is adjusted to add back acquisition accounting fair value adjustments of deferred revenue.

2007

2008

2009

LTM Q2 2010

Operating income

16.8

$

34.1

$

32.8

$

37.0

$

D&A

17.3

28.7

26.9

27.6

Restructuring

-

3.9

3.8

1.0

Asset impairment charges

-

-

10.6

10.6

Deferred purchase price compensation

3.4

8.1

3.5

2.2

Impact of acquisition accounting adjustments

9.6

1.4

0.2

0.1

Adjusted EBITDA

47.1

$

76.2

$

77.8

$

78.5

$

Web-based Education Technology,

School Forms and Testing

13

n Strong brand recognition

– A leading testing provider for over 40 years

n Leading provider of web-based education

technology products

technology products

– Student Achievement Management solutions

– Response to Intervention products

– Special education software solutions

– Web-based assessment products

n Leading provider of scanners and forms

– Provide patent protected scanner to school

– Sales of forms create annuity-like revenue

stream

stream

– Diverse client base - education, commercial,

government

government

n Large installed base

– 80% of the largest school districts

– 65,000+ scanning machines

n Customer diversification

– 100,000+ accounts

– Largest account approximately 5% of

revenue

revenue

n Focus on being a leading provider of

enterprise-wide testing and surveying

technology

enterprise-wide testing and surveying

technology

Surveys, Forms, and Processing

14

Scantron financial performance

$ in millions

Revenue(1)

Adjusted EBITDA

Reconciliation to Adjusted EBITDA

$ in millions

(1) Revenue is adjusted to add back acquisition accounting fair value adjustments of deferred revenue.

2007

2008

2009

LTM Q2 2010

Operating income

12.4

$

28.4

$

34.5

$

32.1

$

D&A

10.6

23.3

25.9

25.9

Restructuring

-

2.4

3.0

6.4

Asset impairment charges

-

-

0.2

0.2

Impact of acquisition accounting adjustments

5.1

1.6

0.2

0.1

Adjusted EBITDA

28.1

$

55.7

$

63.8

$

64.7

$

15

Harland Clarke Holdings financial highlights

n Strong historical financial performance

n High EBITDA margins

n Low working capital requirements

n Efficient deployment of capital

n Significant cash flow generation

16

Harland Clarke Holdings financial performance

Revenue(1)

Adjusted EBITDA

Reconciliation to Adjusted EBITDA

$ in millions

$ in millions

(1) Revenue is adjusted to add back acquisition accounting fair value adjustments of deferred revenue minus revenue from inter-segment transactions.

2007

2008

2009

LTM Q2 2010

Net income (loss)

(15.4)

$

47.2

$

112.1

$

97.4

$

Interest expense, net

159.9

184.2

135.9

122.6

Provision (benefit) for income taxes

(5.4)

33.0

67.4

64.0

D&A

126.2

164.5

162.1

160.8

Restructuring

5.6

14.6

32.5

18.0

Deferred purchase price compensation

3.4

8.1

3.5

2.2

Asset impairment charges

3.1

1.5

44.2

44.8

(Gain) / loss on early extinguishment of debt

54.6

-

(65.0)

(3.5)

Impact of acquisition accounting adjustments

16.6

3.0

0.4

0.7

Transaction related expenses

2.4

-

-

-

Adjusted EBITDA

351.0

$

456.1

$

493.1

$

507.0

$

17

Harland Clarke Holdings credit strength

n LTM Q2 2010 cash flow from operations $ 261.9 million

n LTM Q2 2010 adjusted EBITDA $ 507.0 million

n Cash/equivalents on hand(1) $ 206.6 million

n Net debt(2) $ 2,022.3 million

n Net debt / LTM Q2 2010 adjusted EBITDA 4.0x

n LTM Q2 2010 adjusted EBITDA / Net interest(3) 4.1x

(1) As of June 30, 2010

(2) Net debt equals total debt of $2,228.9 million less cash and equivalents as of June 30, 2010

(3) Net interest expense of $122.6 million for the LTM Q2 2010