Attached files

| file | filename |

|---|---|

| EX-21 - NEVADA GOLD & CASINOS INC | v191661_ex21.htm |

| EX-31.2 - NEVADA GOLD & CASINOS INC | v191661_ex31-2.htm |

| EX-31.1 - NEVADA GOLD & CASINOS INC | v191661_ex31-1.htm |

| EX-32.2 - NEVADA GOLD & CASINOS INC | v191661_ex32-2.htm |

| EX-32.1 - NEVADA GOLD & CASINOS INC | v191661_ex32-1.htm |

| EX-23.1 - NEVADA GOLD & CASINOS INC | v191661_ex23-1.htm |

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

10-K

|

x

|

Annual

Report Pursuant to Section 13 or 15(d) of the Securities

Exchange Act of 1934

|

for

fiscal year ended April 30, 2010

or

|

o

|

Transition

Report Pursuant to Section 13 or 15(d) of the Securities

Exchange Act of 1934

|

for the

transition period from

to

Commission

File No. 001-15517

Nevada

Gold & Casinos, Inc.

(Exact

Name of Registrant as Specified in Its Charter)

|

Nevada

|

88-0142032

|

|

|

(State

or other jurisdiction of Incorporation or organization)

|

(IRS

Employer Identification No.)

|

|

|

50

Briar Hollow Lane, Suite 500W, Houston, Texas

|

77027

|

|

|

(Address

of principal executive offices)

|

|

(Zip

Code)

|

Registrant’s

telephone number, including area code: (713) 621-2245

Securities

registered pursuant to Section 12(b) of the Act:

|

Title of each class

|

Name of each exchange on which

registered

|

|

|

Common

stock, $0.12 par value

|

|

New

York Stock Exchange AMEX

|

Securities

registered pursuant to Section 12(g) of the Act: None.

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in

Rule 405 of the Securities Act.

o Yes x No

Indicate

by check mark if the registrant is not required to file reports pursuant to

Section 13 or Section 15(d) of the Act.

o Yes x No

Indicate

by check mark whether the registrant: (1) has filed all reports required to be

filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the

preceding 12 months (or for such shorter period that the registrant was required

to file such reports), and (2) has been subject to such filing requirements for

the past 90 days.

x Yes o No

Indicate

by check mark whether the registrant has submitted electronically and posted on

its corporate web site, if any, every Interactive Data File required to be

submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding

twelve months (or for such shorter period that the registrant was required to

submit and post such files).

x Yes o No

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of

Regulation S-K is not contained herein, and will not be contained, to the best

of registrant’s knowledge, in definitive proxy or information statements

incorporated by reference in Part III of this Form 10-K or any amendment to this

Form 10-K. o

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer, or a smaller reporting company. See

definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of

the Exchange Act. (Check one):

Large

accelerated filer o Accelerated

filer o Non-accelerated

filer o Smaller

Reporting Company x

Indicate

by check mark whether the registrant is a shell company (as defined in Rule

12b-2 of the Exchange Act.

o Yes x No

As of

June 30, 2010 the aggregate market value of the voting stock held by

non-affiliates of the registrant based on the closing price per share of $0.88,

as reported on the New York Stock Exchange, was $11,025,751.

As of

July 27, 2010, the registrant had 12,764,130 shares of common stock

outstanding.

DOCUMENTS

INCORPORATED BY REFERENCE

Portions

of the definitive Proxy Statement for the registrant’s 2010 Annual Meeting of

Stockholders to be filed pursuant to Regulation 14A within 120 days after the

registrant’s fiscal year end of April 30, 2010 are incorporated by reference

into Part III of this report.

NEVADA

GOLD & CASINOS, INC.

TABLE

OF CONTENTS

|

Page

|

||||

|

PART

I

|

||||

|

ITEM

1.

|

BUSINESS

|

1

|

||

|

ITEM

1A.

|

RISK

FACTORS

|

6

|

||

|

ITEM

1B.

|

UNRESOLVED

STAFF COMMENTS

|

8

|

||

|

ITEM

2.

|

PROPERTIES

|

8

|

||

|

ITEM

3.

|

LEGAL

PROCEEDINGS

|

8

|

||

|

ITEM

4.

|

REMOVED

AND RESERVED

|

8

|

||

|

PART

II

|

||||

|

ITEM

5.

|

MARKET

FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER

PURCHASES OF EQUITY SECURITIES

|

8

|

||

|

ITEM

6.

|

SELECTED

FINANCIAL DATA

|

10

|

||

|

ITEM

7.

|

MANAGEMENT’S

DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF

OPERATIONS

|

10

|

||

|

ITEM

7A.

|

QUANTITATIVE

AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

|

18

|

||

|

ITEM

8.

|

FINANCIAL

STATEMENTS AND SUPPLEMENTARY DATA

|

18

|

||

|

ITEM

9.

|

CHANGES

IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL

DISCLOSURE

|

18

|

||

|

ITEM

9A.

|

CONTROLS

AND PROCEDURES

|

19

|

||

|

ITEM

9B.

|

OTHER

INFORMATION

|

20

|

||

|

PART

III

|

||||

|

ITEM

10.

|

DIRECTORS,

EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE

|

20

|

||

|

ITEM

11.

|

EXECUTIVE

COMPENSATION

|

20

|

||

|

ITEM

12.

|

SECURITY

OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED

STOCKHOLDER MATTERS

|

20

|

||

|

ITEM

13.

|

CERTAIN

RELATIONSHIPS AND RELATED TRANSACTIONS AND DIRECTOR

INDEPENDENCE

|

20

|

||

|

ITEM

14.

|

PRINCIPAL

ACCOUNTANT FEES AND SERVICES

|

20

|

||

|

PART

IV

|

||||

|

ITEM

15.

|

|

EXHIBITS

AND FINANCIAL STATEMENT SCHEDULES

|

|

20

|

i

FORWARD-LOOKING

STATEMENTS

Factors

that May Affect Future Results

(Cautionary

Statements Under the Private Securities Litigation Reform Act of

1995)

Certain

information included in this Form 10-K and other materials filed or to be filed

by the Company with the Securities and Exchange Commission (as well as

information included in oral statements or other written statements made or to

be made by the Company or its representatives) contains or may contain

forward-looking statements within the meaning of Section 27A of the Securities

Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934,

as amended. These statements can be identified by the fact that they do not

relate strictly to historical or current facts. Statements that include the

words “may,” “could,” “should,” “would,” “believe,” “expect,” “anticipate,”

“estimate,” “intend,” “plan,” or other words or expressions of similar meaning,

may identify forward-looking statements. We have based these forward-looking

statements on our current expectations about future events. Forward-looking

statements include statements that reflect management’s beliefs, plans,

objectives, goals, expectations, anticipations, intentions with respect to the

financial condition, results of operations, future performance and the business

of the Company, including statements relating to our business strategy and our

current and future development plans.

Although

we believe that the assumptions underlying these forward-looking statements are

reasonable, any or all of the forward-looking statements in this report and in

any other public statements that are made may prove to be incorrect. This may

occur as a result of inaccurate assumptions or as a consequence of known or

unknown risks and uncertainties. Many factors discussed in this report, such as

the competitive environment and government regulation, will be important in

determining the Company’s future performance. Consequently, actual results may

differ materially from those that might be anticipated from forward-looking

statements. In light of these and other uncertainties, you should not regard the

inclusion of a forward-looking statement in this report or other public

communications that we might make as a representation by us that our plans and

objectives will be achieved, and you should not place undue reliance on such

forward-looking statements.

We

undertake no obligation to publicly update or revise any forward-looking

statements, whether as a result of new information, future events or otherwise.

Any further disclosures made on related subjects in the Company’s subsequent

reports filed with the Securities and Exchange Commission should be

consulted.

ii

Part

I

|

Item

1.

|

Business

|

Overview

Nevada

Gold & Casinos, Inc., a Nevada corporation, was formed in 1977 and, since

1994 has been primarily a gaming company involved in financing, developing,

owning and operating gaming projects.

Commercial Gaming

Projects.

We own

and operate the Colorado Grande Casino in Cripple Creek, Colorado. On

May 12, 2009, we purchased three mini-casinos in Washington State, the Crazy

Moose-Pasco, Crazy Moose-Mountlake Terrace, and Coyote

Bob’s-Kennewick.

In March

2010, we signed management and technical services contracts for the development

and management of a hotel and casino adjacent to the Las Vegas Motor Speedway in

North Las Vegas. The project will be owned by various limited liability

companies of which Nevada Gold will hold a minority interest and option rights

to acquire additional equity.

In April

2010, we reached an agreement to acquire up to an additional seven mini-casinos

in the state of Washington for $11.1 million, which closed on July 23, 2010. The

casinos were owned by subsidiaries of Evergreen Gaming Corporation

("Evergreen"), a British Columbia corporation, which is under bankruptcy court

protection. The transaction was financed by cash on hand as well as a $5.1

million note issued to Evergreen's current senior lender. See Note 18

of our Consolidated Financial Statements for a pro-forma analysis of the

transaction.

Native American Gaming

Project.

As of May

2007, we owned a 40% interest in Buena Vista Development Company,

LLC (“Buena Vista Development”) which is developing a casino for a Native

American tribe in Amador County, California. Effective November 25,

2008, through our wholly owned subsidiary, Nevada Gold BVR, L.L.C., we sold our

40% interest in Buena Vista Development, L.L.C (BVD) to B.V. Oro, L.L.C. (BVO),

which is owned by our former partner and related parties, for $16 million cash

and a $4 million receivable from BVD which is due no later than two years after

the opening of a gaming/entertainment facility to be built by BVD for the Buena

Vista Rancheria of Me-Wuk Indians. This receivable bears interest at

the rate of prime plus 1% and is guaranteed by our former partner and related

parties. In addition we are entitled to a 5% carried interest in the

Class B membership interest. Should the facility not be developed, the

collectibility of this receivable cannot be assured.

Management

Agreements.

Effective

November 10, 2008, we signed a management contract with Oceans Casino Cruises,

Inc., owner of SunCruz Casinos. The contract was to extend to

December 31, 2010. On December 16, 2009, Ocean Casino Cruises, Inc.

(d/b/a “SunCruz”) discontinued operations. We were paid for our management

fee through that date. On December 28, 2009, SunCruz filed Chapter 7

bankruptcy. On February 10, 2010, we submitted a claim in the United

States Bankruptcy Court for the Southern District of Florida for the $500,000

termination fee due to us per the Management Agreement. At this time, we

do not believe it is likely to collect the termination fee, or any part thereof.

Our

management agreement has been terminated as a result of the bankruptcy

proceedings. The Company continues to pursue outside management

agreements.

We also

have real-estate interests in Colorado which are currently offered for

sale.

We report

our operations in two segments - gaming projects and non-core assets. For a

summary of financial information concerning these two segments, please refer to

the information provided in Note 12 to our Consolidated Financial

Statements.

Objective

and Strategies

Our

primary business objective is to increase long-term returns to shareholders

through appreciation in the value of our common shares. To achieve this

objective, we intend to grow our assets and our earnings by following three

business strategies:

|

|

-

|

enhancing

the return from, and the value of, the gaming properties in which we own

interests;

|

|

|

-

|

acquiring

or developing additional gaming

properties; and

|

1

|

|

-

|

assisting

in finding financing, developing and/or managing of, or providing

consulting services to gaming

projects.

|

Current

Commercial Casino Projects

The

Colorado Grande Casino-Cripple Creek

On April

25, 2005, we acquired the Colorado Grande Casino located in Cripple Creek,

Colorado, from Isle of Capri Black Hawk (IC-BH) for $6.5 million. The Colorado Grande

Casino is located at a primary intersection, near the center of the Cripple

Creek market. The property currently consists of a casino with approximately 191

slot machines, four table games, two restaurants with bars and 44 parking

spaces. The friendly atmosphere is enhanced as good customers are treated to

"comps" in the form of free drinks, free meals, or other benefits. In

November 2008, Colorado passed Amendment 50 which effective July 2, 2009,

increased bet limits from $5 to $100, permits craps, roulette, poker, blackjack,

and other table games, allows 24 hour gaming, and lowered gaming tax

rates. To take advantage of this and remain competitive in the

market, we invested an additional $600,000 in the property to provide blackjack,

roulette, house-banked poker, and a food outlet on the casino

floor.

Cripple

Creek is 40 miles west of Colorado Springs, Colorado, which is 65 miles south of

Denver, Colorado. We believe that the Cripple Creek market attracts customers

primarily from Colorado Springs, Pueblo, Fort Carson and smaller areas south of

Denver.

Nevada

Gold Washington – Washington State

On May

12, 2009, Nevada Gold completed its acquisition of three mini casinos in the

State of Washington, for $15.75 million. The casinos were owned by Gullwing III,

LLC (“sellers”) and the transaction was funded by existing cash as well as a

$4.0 million note issued by the sellers. See Note 7 of our

consolidated financial statements.

The three

casinos are the Crazy Moose Casino, located in Pasco, Coyote Bob's Roadhouse

Casino, located in Kennewick, and the Crazy Moose Casino, located in Mountlake

Terrace in close proximity to Seattle. Combined, the facilities have a total of

40 table games including blackjack, Pai Gow poker, Baccarat, Spanish 21,

Blackjack-Double Action, Ultimate Holdem, and Three and Four card poker. New

games are frequently introduced to keep the customers interested and active.

Additional banked table games are permitted along with poker and pull tabs. Each

casino includes a full service restaurant with bar. The friendly atmosphere is

enhanced as good customers are treated to "comps" in the form of free

non-alcoholic drinks, free meals, or other benefits. The three casinos operate

with approximately 400 employees and have a total of 306 parking

spaces.

As of

January 1, 2009, the maximum bet for each facility was increased from $200 to

$300 and the law was changed to allow casinos to be open 24 rather than 20 hours

per day.

Two of

the casinos are located within 250 miles in the Tri-cities area and one is

located in the Seattle area. We believe that the Crazy Moose Casino

in Mountlake attracts customers from the Seattle area, whereas the Crazy Moose

Pasco and Coyote Bob’s Roadhouse Casino located in the Southeast portion of

Washington state, attracts customers from Walla Walla, southeastern Washington

State, and northeastern Oregon.

Nevada Gold

Washington II – Washington State

On July 23, 2010, the Company acquired six additional casinos, and

their related operating center, in the state of Washington. See Note 18 of

our consolidated financial statements.

Native

American Casino Projects

Buena Vista Rancheria of

Me-Wuk Indians; Ione, Amador County, California

On May 4,

2005, we, through our wholly owned subsidiary, Nevada Gold BVR, L.L.C., acquired

a 20% interest in BVD in exchange for an approximately $14.8 million loan and an

equity investment of approximately $200,000. Our initial 20%

ownership interest in BVD increased by five percentage points at the end of

every six month period the loan remained outstanding, up to a maximum of an

additional 20%, for a total of 40%. At May, 2007, we owned a 40%

interest in BVD.

Effective

November 25, 2008, through our wholly owned subsidiary, Nevada Gold BVR, L.L.C.,

we sold our 40% interest in BVD to BVO, which is owned by our former partner and

related parties, for $16 million cash and a $4 million receivable from BVO which

is due no later than two years after the opening of a gaming/entertainment

facility to be built by BVO for the Buena Vista Rancheria of Me-Wuk

Indians. This receivable bears interest at the rate of prime plus 1%

and is guaranteed by our former partner and related parties. In

addition, we are entitled to a 5% carried interest in the Class B membership

interest.

We cannot

predict the future performance of the casino. We expect the casino’s primary

market to include Sacramento and Stockton, California. In this market, the

casino will most directly compete with the Jackson Rancheria Casino located in

Jackson, California, approximately 10 miles from the proposed Buena Vista

Casino, the Cache Creek Casino located approximately 45 miles northwest of

Sacramento, Thunder Valley Casino located a few miles northeast of Sacramento,

Red Hawk Casino located approximately 40 miles northeast of Sacramento, and the

Shingle Springs Casinos located just east of Sacramento on Highway

50.

2

Other

Casino Projects

Route 66 Casino;

Albuquerque, New Mexico

We owned

a 51% interest in Route 66 which we accounted for using the equity method. We

received no cash distributions from the Route 66 Casinos venture. Our portion of

the earnings of the Route 66 Casinos venture was estimated and recorded based on

available financial information. In April 2008, we signed a settlement agreement

with American Heritage, Inc. and Fred Gillman, the principal of American

Heritage, Inc. (“The Gillmann Group”). Per the agreement, The Gillmann Group

paid us $1 million on May 1, 2008, $1.3 million on June 2, 2008 and was

obligated to pay us $2.3 million by April 15, 2010. There was an

offsetting $0.7 million liability previously netted against the $2.3 million,

resulting in a net balance of $1.6 million. The $2.3 million was not

received as of April 30, 2010, as a result we elected to establish a valuation

allowance against the remaining $1.6 million receivable on the balance

sheet. We are pursuing legal action to collect the

receivable. See Note 16 to the accompanying Consolidated Financial

Statements for a discussion of our current legal position and accounting of the

settlement agreement and our former investment in this joint

venture.

Management

Contracts

Oceans Casino Cruises,

Inc.

On

November 10, 2008, we signed a contract to manage the SunCruz Casinos for Oceans

Casino Cruises, Inc. The contract was to extend to December 31,

2010. On December 16, 2009, SunCruz discontinued operations. We

were paid for our management fee through that date. On December 28, 2009,

SunCruz filed Chapter 7 bankruptcy. On February 10, 2010 we submitted a

claim in the United States Bankruptcy Court for the Southern District of Florida

for the $500,000 termination fee due to us per the Management Agreement.

At this time, we do not believe it is likely to collect the termination fee, or

any part thereof.

Our

management agreement has been terminated as a result of the bankruptcy

proceedings.

Regulation and Licensing

Colorado

The

ownership and operation of gaming facilities in Colorado are subject to

extensive state and local regulations. No gaming may be conducted in Colorado

unless licenses are obtained from the Colorado Limited Gaming Control Commission

(the “Gaming Commission”). In addition, the State of Colorado created the

Division of Gaming (the “CDG”) within its Department of Revenue to license,

implement, regulate, and supervise the conduct of limited stakes gaming. The

Director of the CDG (“CDG Director”), under the supervision of the Gaming

Commission, has been granted broad powers to ensure compliance with the laws and

regulations. The Gaming Commission, CDG and CDG Director that have

responsibility for regulation of gaming are collectively referred to as the

“Colorado Gaming Authorities.”

The laws,

regulations, and supervisory procedures of the Colorado Gaming Authorities seek

to maintain public confidence and trust that licensed limited gaming is

conducted honestly and competitively, that the rights of the creditors of

licensees are protected, and that gaming is free from criminal and corruptive

elements. The Colorado Gaming Authorities’ stated policy is that public

confidence and trust can be maintained only by strict regulation of all persons,

locations, practices, associations, and activities related to the operation of

the licensed gaming establishments and the manufacture and distribution of

gaming devices and equipment.

The

Gaming Commission is empowered to issue five types of gaming and related

licenses. To operate our Colorado casino we are required to maintain a retail

gaming license, which must be renewed each year, and the Colorado Commission has

broad discretion to revoke, suspend, condition, limit, or restrict the licensee

at any time. Under Colorado gaming regulations, no person or entity can have an

ownership interest in more than three retail licenses, and our business

opportunities will be limited accordingly. The Colorado Casinos’ licenses are

renewable annually, subject to continued compliance with gaming regulations. The

failure or inability of the Colorado Grande-Cripple Creek (the "Colorado

Casino"), or the failure or inability of others associated with the Colorado

Casino to maintain necessary gaming licenses or approvals would have a material

adverse effect on our operations.

The

Colorado Casino must meet specified architectural requirements, fire safety

standards and standards for access for disabled persons. It also must not exceed

specified gaming square footage limits as a total of each floor and the full

building. Casinos may operate 24 hours daily. Colorado casinos are permitted to

operate slot machines and various types of table games, such as blackjack,

poker, craps and roulette. Casino patrons must be 21 or older to

gamble in the casino. Effective July 2, 2009, the casino is permitted

to operate 24 hours per day and the maximum bet limit was increased $5 to $100.

No Colorado Casino may provide credit to its gaming patrons.

3

The

Colorado Constitution permits a gaming tax of up to 20% on adjusted gross gaming

proceeds, and authorizes the Gaming Commission to change the rate annually. As

of July 2, 2009, any increase in the gamming tax rate requires statewide voter

approval. The current gaming tax rate is 0.25% on adjusted gross

gaming proceeds of up to and including $2 million, 2% over $2 million up to and

including $5 million, 9% over $5 million up to and including $8 million, 11%

over $8 million up to and including $10 million, 16% over $10 million up to and

including $13 million and 20% on adjusted gross proceeds in excess of $13

million.

Colorado

law requires that every officer, director or stockholder holding either a 5% or

greater interest or controlling interest of a publicly traded corporation, or

owners of an applicant or licensee, shall be a person of good moral character

and submit to a full background investigation conducted by the Gaming

Commission. The Gaming Commission may require any person having an interest in a

license or a licensee to undergo a full background investigation and pay the

cost of investigation in the same manner as an applicant. Persons found

unsuitable by the Gaming Commission may be required to immediately

terminate any interest in, association or agreement with, or relationship to, a

licensee. A finding of unsuitability with respect to any officer, director,

employee, associate, lender or beneficial owner of a licensee or applicant may

also jeopardize the licensee’s license or applicant’s license application.

Licenses may be conditioned upon termination of any relationship with unsuitable

persons.

The rules

impose certain additional restrictions and reporting and filing requirements on

publicly traded entities holding gaming licenses in Colorado. A licensee or

affiliated company or any controlling person of a licensee or affiliated

company, which commences a public offering of voting securities, must notify the

Gaming Commission with regard to a public offering to be registered with the

Securities and Exchange Commission ("SEC"), no later than ten business days

after the initial filing of a registration statement with the SEC, or, with

regard to any other type of public offering, no later than ten business days

prior to the public use or distribution of any offering document, if: 1) the

licensee, affiliated company or a controlling person thereof, intending to issue

the voting securities is not a publicly traded corporation; or 2) if the

licensee, affiliated company or controlling person thereof, intending to issue

the voting securities is a publicly traded corporation, and if the proceeds of

the offering, in whole or in part, are intended to be used: a) to pay for

construction of gaming facilities in Colorado to be owned and operated by the

licensee; b) to acquire any direct or indirect interest in gaming facilities in

Colorado; c) to finance the operation by the licensee of gaming facilities in

Colorado; or d) to retire or extend obligations incurred for one or more of the

purposes set forth in subsections a, b, or c above.

We may

not issue any voting securities except in accordance with the provisions of the

Colorado Limited Gaming Act and the regulations promulgated thereunder. The

issuance of any voting securities in violation will be void and the voting

securities will be deemed not to be issued and outstanding. No voting securities

may be transferred, except in accordance with the provisions of the Colorado

Limited Gaming Act and the regulations promulgated thereunder. Any transfer in

violation of these provisions will be void. If the Colorado Limited Gaming

Control Commission at any time determines that a holder of our voting securities

is unsuitable to hold the securities, then we may, within sixty (60) days after

the finding of unsuitability, purchase the voting securities of the unsuitable

person at the lesser of (a) the cash equivalent of such person’s investment, or

(b) the current market price as of the date of the finding of unsuitability,

unless such voting securities are transferred to a suitable person within sixty

(60) days after the finding of unsuitability. Until our voting securities are

owned by persons found by the Commission to be suitable to own them, (a) we are

not permitted to pay any dividends or interest with regard to the voting

securities, (b) the holder of such voting securities will not be entitled to

vote and the voting securities will not for any purposes be included in the

voting securities entitled to vote, and (c) we may not pay any remuneration in

any form to the holder of the voting securities, except in exchange for the

voting securities.

Washington

The

gaming legislation in Washington State is codified in chapter 9.46 of the

Revised Code of Washington (“RCW”). The gaming legislation stipulates the

Washington State Gambling Commission (the “Commission”) to be the regulator of

gambling activities in this state. The Commission enforces its

authority through an extensive set of rules and regulations promulgated in Title

230 of the Washington Administrative Code. The state of Washington

allows certain gambling activities, such as amusement games, bingo, raffles,

punch boards, pull-tabs, card-rooms, and social card games. In order

to be considered legal, these activities must be operated by either non-profit

organizations or by commercial food and drink establishments. Some

activities may be operated solely by non-profit organizations, such as

raffles. Traditional casino games, such as craps, roulette and keno,

are prohibited. House-banked card-rooms have been authorized in

Washington State since 1997 and, under current law, each establishment is

allowed to have up to 15 tables offering games, such as Blackjack, Ultimate

Texas Hold’em, Three Card Poker, Four Card Poker, Spanish Poker, Texas Shootout,

Spanish 21, Pai Gow Poker, and others. The law allows both

player-sponsored and house-banked card-rooms. As of January 1, 2009,

the Commission increased the maximum bet for house-banked card-rooms’ table game

wager limit to $300 and allowed card-rooms to offer Mini-Baccarat. In addition,

these establishments are allowed to be open 24 hours per day, provided they

close for at least four continuous hours two times per week.

In order

to operate our three “mini casinos,” Crazy Moose Casino in Pasco, Crazy Moose

Casino in Mountlake Terrace and Coyote Bob’s Roadhouse Casino in Kennewick, each

of them is required to maintain a Public Card room license and Punch

Board/Pull-Tab Commercial Stimulant license. These licenses are

renewable annually, subject to continued compliance with applicable gaming

regulations. In addition, the Commission requires, prior to the

licenses being issued, each substantial interest holder in the licensees

(including our officers, directors and owners of five percent or more of any

class of our stock) submit to the Commission certain disclosure forms and be

subject to background investigations. The failure or inability of our

“mini-casinos” to maintain their respective licenses would have a material

adverse effect on our operations.

4

RCW

9.46.110 allows local governments (including cities, counties and towns) to

prohibit any or all gambling activities for which licenses are required as well

as tax such activities. The maximum tax limitations imposed by law

include 20% of gross receipt for card-rooms and either 5% of gross receipts or

10% of net receipt (as chosen by a local authority) for pull-tabs

activities. The current gaming tax rate in the cities of Pasco and

Mountlake Terrace is 10% of table games gross receipts and 5% of pull-tabs gross

receipts while in the city of Kennewick the current gaming tax rate is 10% of

table games gross receipts and 10% of pull-tabs net receipts. In

addition, Washington State charges a business and occupational tax in the amount

of 1.63% of all gaming activities’ net receipts in order to promote responsible

gaming.

Native

American Gaming

Although

it may seek new agreements, the Company does not currently operate gaming

facilities on behalf of any Native American tribe nor is it receiving

compensation pursuant to any consulting, financing or advisory

agreement. Reference is made to “Native American Casino Projects”

above.

General Gaming

Regulations in Other Jurisdictions

If we

become involved in gaming operations in any other jurisdictions, such gaming

operations will subject us and certain of our officers, directors, key

employees, stockholders and other affiliates to strict legal and regulatory

requirements, including mandatory licensing and approval requirements,

suitability requirements, and ongoing regulatory oversight with respect to such

gaming operations. There can be no assurance that we will obtain all of the

necessary licenses, approvals and findings of suitability or that our officers,

directors, key employees, other affiliates and certain other stockholders will

satisfy the suitability requirements in one or more jurisdictions, or that such

licenses, approvals and findings of suitability, if obtained, will not be

revoked, limited, suspended or not renewed in the future.

Failure

by the Company to obtain, or the loss or suspension of, any necessary licenses,

approval or findings of suitability would prevent us from conducting gaming

operations in such jurisdiction and possibly in other

jurisdictions.

Other

Assets

Gold Mountain Development. Through our

wholly-owned subsidiary, Gold Mountain Development, L.L.C., we own approximately

265 acres of real property in the vicinity of Black Hawk, Colorado. In November

2004, the Central City Business Improvement District completed the construction

of a new 8.4 mile four-lane road connecting Interstate 70 to Central City,

Colorado. The new road is adjacent to a portion of our 265 acres.

Nevada

Gold Speedway, LLC. Through our wholly owned subsidiary, NG

Speedway, LLC, we have signed management and technical services contracts for

the development and management of a hotel and casino adjacent to the Las Vegas

Motor Speedway in North Las Vegas. The project will be owned by various limited

liability companies of which Nevada Gold will hold a minority

interest. We will assist in the development and manage the

operation of the property. The development is expected to be completed in

three phases. The first phase, which will include 250 hotel rooms, restaurants,

meeting rooms and a casino with up to 500 gaming positions, is expected to be

completed during 2012. The development remains subject to numerous conditions,

including obtaining financing to repay the outstanding obligations related to

the land and securing financing for the development.

NG Washington II, LLC. Through our

wholly-owned subsidiary, NG Washington II, LLC, we signed an agreement in April

2010 to acquire up to seven mini-casinos in Washington State. We

escrowed $1.0 million as a deposit and as of April 30, 2010, spent $0.3 million

additional funds for licensing and legal matters pertaining to the

acquisition. Closing of the acquisition was subject to the bankruptcy

court process which was finalized May 28, 2010. In addition, the acquisition was

subject to other customary closing conditions, including licensing and necessary

lease transfers, among other conditions.

On July

23, 2010, the Company acquired six of the seven casinos, and their

related operating center. The casinos are the Silver Dollar Seatac, the Silver

Dollar Renton, the Silver Dollar Mill Creek, Club Hollywood, located in

Shoreline, the Royal Casino, located in Everett, and the Golden Nugget Casino,

located in Tukwila, collectively “Silver Dollar Casinos”. All of the casinos are

located in western Washington. The casinos were previously owned by

subsidiaries of Evergreen Gaming Corporation, a British Columbia Corporation,

which is under bankruptcy court protection. The Company purchased the

six casinos from Fortress Credit Opportunities I, LP and Fortress Credit Funding

II, LP, (the “Sellers”) for $11.07 million, $6.0 million which was paid in cash

and $5.07 million by a credit agreement, issued by the Company to the Sellers

that is due July 23, 2012, and bears an interest rate based on the 30 day LIBOR

at the end of each calendar month, plus 9%, with a floor of

11.0%. Interest is due monthly.

Employees

As of

April 30, 2010, we employed 481 people.

5

Available

Information

We make

available on our website (www.nevadagold.com) under “Investor Relations - SEC

Filings,” free of charge, our annual reports on Form 10-K, quarterly reports on

Form 10-Q, current reports on Form 8-K and amendments to those reports, as soon

as reasonably practicable after we electronically file such material with the

Securities and Exchange Commission.

|

Item

1A.

|

Risk

Factors

|

The

following is a description of what we consider our key challenges and

risks:

Financing

future acquisitions may be difficult.

The

principal challenge facing the Company is the necessity to obtain financing in

order to expand gaming operations, generate cash flow, and service debt

obligations. There can be no assurance that such financing will be

obtained.

If

our key personnel leave us, our business could be adversely

affected.

Our

success is largely dependent upon the efforts and skills of our key executive

officers. The loss of the services of any key executive officer could have a

material adverse effect on us. There can be no assurance that we would be able

to attract and hire suitable replacements in the event of any such loss of

services. We currently have employment agreements with our Chief Executive

Officer, Senior Vice President/General Counsel/Chief Compliance Officer, and our

Executive Vice President/Chief Financial Officer.

Indebtedness

could adversely affect our financial health.

As of

April 30, 2010, we had $10.0 million of indebtedness outstanding, consisting of

a $6.0

million interest only promissory note which matures on June 30, 2013 and a

$4.0 million debt for the Washington properties which matures on May 12,

2012. Although we have substantially reduced our debt, our

indebtedness could have important consequences and significant effects on our

business and future operations. For example, it could:

|

·

|

increase

our vulnerability to general adverse economic and industry conditions or a

downturn in our business;

|

|

·

|

limit

our ability to fund future working capital, capital expenditures and other

general operating requirements;

|

|

·

|

place

us at a competitive disadvantage compared to our competitors that have

less debt or greater resources; and

|

|

·

|

limit

our ability to borrow additional

funds.

|

The occurrence of any one of these

events or conditions could have a material adverse effect on our business,

financial condition, results of operations, prospects, ability to service or

otherwise satisfy our obligations.

We

will require cash to service our indebtedness and fund our gaming operations.

Our ability to generate cash depends on many factors beyond our

control.

Our ability to fund our gaming

operations will depend on our ability to generate cash flow from our gaming

operations and borrow or refinance $4.0 million by May 12, 2012 and $6.0 million

by June 30, 2013. Our ability to generate sufficient cash flow to satisfy our

debt obligations will depend on our future operating performance that is subject

to many economic, competitive, regulatory and business factors that are beyond

our control. If we are unable to generate sufficient cash flow to service our

debt obligations, we will need to refinance or restructure our debt, sell

assets, reduce or delay capital investments or seek to raise additional capital.

These measures may not be available to us or, if available, they may not be

sufficient to enable us to satisfy our obligations and may restrict our ability

to pay operating expenses. If our cash flow is insufficient and we are unable to

implement one or more of these alternatives, we may not be able to service our

debt obligations or fund our gaming operations.

We

face significant competition from other gaming operations that could have a

material adverse effect on our future operations.

There is

intense competition among companies in the gaming industry, many of which have

significantly greater resources than we do. We compete with numerous casinos of

varying quality and size in market areas where our properties are located. The

gaming business is characterized by competitors that vary considerably by their

size, quality of facilities, number of operations, brand identities, marketing

and growth strategies, financial strength and capabilities, level of amenities,

management talent and geographic diversity. In most markets, we compete directly

with other casino facilities in the immediate and surrounding market areas. If

our competitors operate more successfully, if competitors' properties are

enhanced or expanded, or if additional casinos are established in and around

locations in which we conduct business, we may lose market share. The expansion

of casino gaming in or near any geographic area from which we attract or expect

to attract a significant number of our customers could have a significant

adverse effect on our business, financial condition and results of

operations.

6

We

are subject to extensive governmental gaming regulation that could adversely

affect us. We could be prevented from pursuing future

development projects due to changes in the laws, regulations and ordinances

(including tribal or local laws) that apply to gaming facilities or the

inability of us or our key personnel, significant shareholders or joint venture

partners to obtain or retain gaming regulatory licenses.

The

gaming industry is highly regulated and we must maintain our licenses in order

to continue our operations. Each of our gaming operations is subject to

extensive regulation under the laws, rules and regulations of the jurisdiction

where located. These laws, rules and regulations generally concern the

responsibility, financial stability and character of the owners, managers, and

persons with financial interests in the gaming operations. Certain

jurisdictions empower their regulators to investigate participation by

licensees in gaming outside their jurisdiction and require access to and

periodic reports concerning the gaming activities. Violations of laws in one

jurisdiction could result in disciplinary action in other jurisdictions.

Regulatory authorities have broad powers with respect to the licensing of casino

operations and may revoke, suspend, condition or limit our gaming or other

licenses, impose substantial fines and take other actions, any one of which

could have a significant adverse effect on our business, financial condition and

results of operations.

The

rapidly changing political and regulatory environment governing the gaming

industry (including gaming operations which are conducted on Indian land) makes

it impossible for us to accurately predict the effects that an adoption of or

changes in the gaming laws, regulations and ordinances will have on

us. However, the failure of us, or any of our key personnel,

significant shareholders or joint venture partners, to obtain or retain required

gaming regulatory licenses could prevent us from expanding into new markets,

prohibit us from generating revenues in certain jurisdictions, and subject us to

sanctions and fines.

Our

business is subject to various federal, state and local laws and regulations in

addition to gaming regulations. These laws and regulations include, but are not

limited to, restrictions and conditions concerning alcoholic beverages,

environmental matters, employees, currency transactions, taxation, zoning and

building codes, and marketing and advertising. Such laws and regulations could

change or could be interpreted differently in the future, or new laws and

regulations could be enacted. Material changes, new laws or regulations, or

material differences in interpretations by courts or governmental authorities

could adversely affect our results of operations and financial

condition.

We cannot

ensure that we will be able to comply with or conduct business in accordance

with applicable regulations.

We

could fail to monetize recorded assets.

The

Company has receivables that are projected to be collected. If the Company is

not able to collect or monetize these assets timely then the lack of such

collection may have a negative impact on the Company’s projected cash flow. The occurrence of

monetizing our recorded assets could have a material adverse effect on our

business, financial condition, results of operations, prospects, ability to

service or otherwise satisfy our obligations.

There

are significant risks in the development and management of commercial and Native

American Casinos that could adversely affect our financial results.

The

development and management of casinos require the satisfaction of various

conditions, many of which are beyond our control. The failure to satisfy any of

such conditions may significantly delay the completion of a project or prevent a

project's completion altogether.

The

opening of any facility will be contingent upon, among other things, the receipt

of all regulatory licenses, permits, approvals and authorizations, the

completion of construction and the hiring and training of sufficient personnel.

The scope of the approvals to construct and open a casino is extensive, and the

failure to obtain such approvals could prevent or delay the completion of

construction or opening of all or part of such casino.

No

assurance can be given that development activities will begin or will be

completed, or that the budget for such a project will not be exceeded, or that

we will have the continuing support of the community.

In

addition, the regulatory approvals necessary for the construction and operation

of casinos are often challenged in litigation brought by government entities,

citizens groups and other organizations and individuals. Such litigation can

significantly delay the construction and opening of casinos.

7

Major

construction projects entail significant risks, including shortages of materials

or skilled labor, unforeseen engineering, environmental and/or geological

problems, work stoppages, weather interference, and unanticipated cost

increases. Delays or difficulties in obtaining any of the requisite licenses,

permits, allocations and authorizations from regulatory authorities could

increase the total cost, delay or prevent the construction or opening of any

casino development. In addition, once developed, no assurances can be given that

we will be able to manage the casino on a profitable basis or to attract a

sufficient number of guests, gaming customers and other visitors to make the

operation profitable.

With each

project, we are subject to the risk that our investment may be lost if the

project cannot obtain adequate financing to complete development and open the

casino successfully. In some cases, we may be forced to provide more financing

than originally planned in order to complete development, increasing the risk to

us.

|

Item

1B.

|

Unresolved

Staff Comments

|

None.

|

Item

2.

|

Properties

|

Colorado Grande Casino-Cripple

Creek. We lease (through our wholly-owned subsidiary, Colorado Grande

Enterprises, Inc.) a portion of a building in Cripple Creek, Colorado, and an

adjacent parking lot, for use in connection with the Colorado Grande Casino

facilities. We lease this property at an annual rent of the greater of $144,000

or 5% of Colorado Grande-Cripple Creek’s adjusted gross gaming revenues, as

defined, with an annual cap of $400,000. On July 7, 2005, we exercised the

option to extend the lease to January 2021. On April 1, 2008 we negotiated an

extension of the lease to January 2033 at a flat annual rent of $400,000 from

February 2021 through January 2033. In addition, we own an additional parcel of

land adjacent to the Colorado Grande, which is used for parking.

Gold Mountain Development.

Through our wholly-owned subsidiary, Gold Mountain Development, L.L.C., we own

approximately 265 acres of real property in the vicinity of Black Hawk,

Colorado. In November 2004, the Central City Business Improvement District

completed the construction of a new 8.4 mile four-lane road connecting

Interstate 70 to Central City, Colorado. The new road is adjacent to a portion

of our 265 acres. The acreage is for sale and will be listed with a

broker.

Washington Casinos. As a

result of acquiring facilities in Washington, the Crazy Moose II Mountlake

Terrace has a building lease which expires May, 2011, with an option to renew

for two additional five year terms. The annual rent is $192,000. The

administrative office has a lease which expires February, 2011 with an option to

renew for one additional term. The annual rent is

$28,800. In addition, the Crazy Moose I Pasco has a parking lot lease

which expires January, 2011 with an option to renew for one more two year

term. The annual rent is $6,300. We own the buildings

for the Crazy Moose Pasco and Coyote Bob’s in Kennewick as well as a parcel of

land at Pasco used as a parking lot.

Office Lease. We currently

lease approximately 6,110 square feet of office space in Houston, Texas. The

lease expires March 31, 2011. The total monthly rent for this office space is

currently $8,700.

|

Item

3.

|

Legal

Proceedings

|

None

|

Item

4.

|

Removed

and Reserved

|

Part

II

|

Item 5.

|

Market For Registrant’s Common

Equity, Related Stockholder

Matters and

Issuer Purchases of Equity

Securities

|

Market

Information

Our

common stock is traded on the New York Stock Exchange-AMEX under the symbol UWN.

The following table sets forth the high and low sales prices per share of the

common stock for the last two fiscal years.

8

|

Fiscal

Years Ended

|

||||||||||||||||

|

April

30, 2010

|

April

30, 2009

|

|||||||||||||||

|

High

|

Low

|

High

|

Low

|

|||||||||||||

|

First

Quarter

|

$ | 1.40 | $ | .80 | $ | 1.34 | $ | 1.02 | ||||||||

|

Second

Quarter

|

1.27 | .97 | 1.29 | .53 | ||||||||||||

|

Third

Quarter

|

1.08 | .83 | .89 | .38 | ||||||||||||

|

Fourth

Quarter

|

1.10 | .74 | .84 | .66 | ||||||||||||

Holders

of Common Stock

As

of June 30, 2010, we had approximately 4,670 shareholders of

record.

Dividends

We have

not paid any dividends during the last four fiscal years and our current policy

is to retain earnings to provide for the growth of the Company. Consequently, no

cash dividends are expected to be paid on our common stock in the foreseeable

future.

Equity

Compensation Plan

The

following table gives information about our shares of common stock that may be

issued upon the exercise of options, warrants, and rights under all of our

existing equity compensation plans as of April 30, 2010 including the 1999 Stock

Option Plan and the 2009 Equity Incentive Plan, as well as shares of our common

stock that may be issued under individual compensation arrangements that were

not approved by our stockholders (such grants, the “Non-Plan

Grants”).

|

Plan Category

|

Number of

Securities

To be Issued Upon

Exercise of

Outstanding

Options, Warrants

and Rights

(A)

|

Weighted Average

Exercise Price of

Outstanding

Options,

Warrants and

Rights

(B)

|

Number of Securities

Remaining Available

for Future Issuance

Under Equity

Compensation Plans

(Excluding Securities

Reflected in Column

(A) (C)

|

||||||||

|

Equity

Compensation Plans Approved by Security Holders

|

1,456,000 | $ | 1.77 | 1,320,000 | |||||||

|

Equity

Compensation Plans Not Approved by Security Holders

|

— | $ | — | — | |||||||

|

Total

|

1,456,000 | $ | 1.77 | 1,320,000 | |||||||

Recent

Sales of Unregistered Securities

Not

applicable.

Issuer

Purchases of Equity Securities

In

December, 2009, in a private transaction, we purchased 175,000 shares of our

common stock at the then prevailing market price of $0.87 per

share. During the years ended April 30, 2010 and April 30, 2009, we

repurchased a total of 175,000 and 0 shares, respectively.

Stock

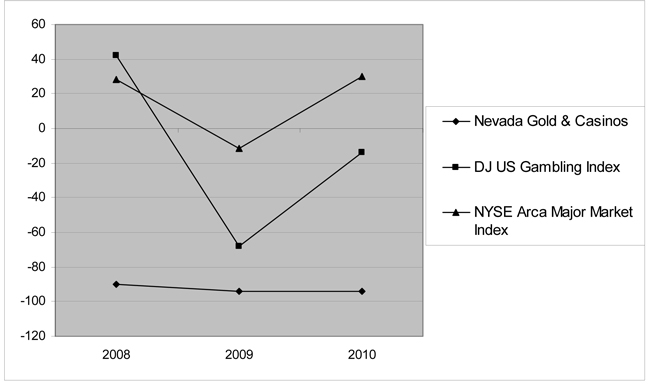

Performance Graph

The

following graph sets forth the cumulative total stockholder return (assuming

reinvestment of dividends) to the Company’s stockholders during the two-year

period ended April 30, 2010, as well as an overall stock market index (NYSE Arca

Major Market Index) and the Company’s peer group index (Dow Jones US Gambling

Index):

9

ASSUMES

$100 INVESTED ON MAR. 31, 2005

ASSUMES

DIVIDEND REINVESTMENT

FISCAL

YEAR ENDING APRIL 30, 2010

|

Item

6.

|

Selected

Financial Data

|

Not

required for smaller reporting companies.

|

Item 7.

|

Management’s Discussion and

Analysis of Financial Condition and Results of

Operations

|

The

following discussion and analysis (“MD&A”) should be read in conjunction

with our Consolidated Financial Statements and Notes thereto contained in Item 8

herein. Management is of the opinion that inflation and changing prices,

including foreign exchange fluctuations, will have little, if any, effect on our

consolidated financial position or results of our operations.

Critical

Accounting Policies and Estimates

Our

critical accounting policies and estimates involve the use of complicated

processes, assumptions, estimates and/or judgments in the preparation of our

consolidated financial statements. An accounting estimate is an approximation

made by management of a financial statement element, item or account in the

consolidated financial statements. Accounting estimates in our historical

consolidated financial statements measure the effects of past business

transactions or events, or the present status of an asset or liability. The

accounting estimates described below require us to make assumptions about

matters that are uncertain at the time the estimate is made. Additionally,

different estimates that we could have used or changes in an accounting estimate

that are reasonably likely to occur could have a material impact on the

presentation of our consolidated financial condition or results of operations.

We base our estimates on historical experience and on various other assumptions

that we believe are reasonable under the circumstances, the results of which

form the basis for making judgments. These estimates may change as new events

occur, as more experience is acquired, as additional information is obtained and

as our operating environment changes. Our significant accounting policies are

discussed in Note 2 to our Consolidated Financial Statements included in Item 8

of this report. We have discussed the development and selection of our critical

accounting policies and related disclosures with the Audit Committee of the

Board of Directors and have identified the following critical accounting

policies for the current fiscal year.

Principles

of Consolidation

We

consolidate entities when we have the ability to control the operating and

financial decisions and policies of that entity and record the portion we do not

own as minority interest. The determination of our ability to control or exert

significant influence over an entity involves the use of judgment. We apply the

equity method of accounting where we can exert significant influence over, but

do not control, the policies and decisions of an entity. We use the cost method

of accounting where we are unable to exert significant influence over the

entity.

10

Capitalized

Development Costs

We

capitalize certain third party legal, professional, and other miscellaneous fees

directly related to the procurement, evaluation and establishment of contracts

for development projects. Development costs are recorded on the cost basis and

are amortized over the estimated economic term of the contract. We review each

project on a quarterly basis to assess whether any changes to our estimates are

appropriate. If accumulated costs of a specific project exceed the net

realizable value of such project or the project is abandoned, the costs are

charged to earnings.

Goodwill,

Other Intangible, and Other Long Lived Assets

In

connection with our acquisition of the Colorado Grande casino on April 25, 2005,

and the acquisition of the Washington casinos on May 12, 2009, we have goodwill

and identifiable intangible assets of $15.3 million, net of

amortization. Goodwill represents a significant portion of our total

assets. We review goodwill for impairment annually and or more frequently if

certain impairment indicators arise under the provisions of authoritative

guidance. We review goodwill at the reporting level unit, which is one level

below an operating segment. We review the carrying value of the net assets of

each reporting unit to the estimated fair value of the reporting unit,

based upon a multiple of estimated earnings. If the carrying value exceeds the

estimated fair value of the reporting unit, an impairment indicator exists and

an estimate of the impairment loss is calculated. The fair value calculation

includes multiple assumptions and estimates, including the projected cash flows

and discount rates applied. Changes in these assumptions and estimates could

result in goodwill impairment that could materially adversely impact our

financial position or results of operations. All of our goodwill is attributable

to reporting units within our gaming segment.

We use

earnings before interest, taxes, depreciation, and amortization (“EBITDA”) as the measure for

future earnings in our impairment test. Management estimates future

EBITDA based primarily on its projections of future revenues. We utilized

comparable industry average multiples of EBITDA rates based on industry

standards ranging from 5.5 to 7.5 times EBITDA when we estimated fair values of

our casinos as of April 30, 2010.

During

the 2010 fiscal there were significant declines in the U.S. economies and in the

casino industry overall, which led to declines in our revenues, margins and cash

flows. Our sales and profitability declined throughout the

year. We considered the impact of these significant adverse changes

in the economic and business climate as we performed our annual impairment

assessment of goodwill as of April 30, 2010. The estimated fair

values of our reporting unit were negatively impacted by significant reductions

in estimated cash flows for the income approach.

Our

goodwill impairment analysis led us to conclude that there was a significant

impairment of goodwill for the Colorado Grande and, accordingly, we recorded a

non-cash charge of $2.8 million to our operating results for the year ended

April 30, 2010, for the impairment of our goodwill. This $2.8 million

expense is included in the “Impairment of Assets” expense on the Consolidated

Statements of Operations. This impairment charge did not

have an impact on our liquidity; however it was a reflection of the overall

downturn in our industry and decline in our projected cash flows.

Long-lived

assets, including property, plant and equipment and amortizable intangible

assets, also comprise a significant portion of our total assets. We evaluate the

carrying value of long-lived assets when impairment indicators are present or

when circumstances indicate that impairment may exist under authoritative

guidance. When management believes impairment indicators may exist, projections

of the undiscounted future cash flows associated with the use of and eventual

disposition of long-lived assets held for use are prepared. If the projections

indicate that the carrying values of the long-lived assets are not recoverable,

we reduce the carrying values to fair value. For long-lived assets held for

sale, we compare the carrying values to an estimate of fair value less selling

costs to determine potential impairment. We test for impairment of long-lived

assets at the lowest level for which cash flows are measurable. These impairment

tests are heavily influenced by assumptions and estimates that are subject to

change as additional information becomes available.

Asset

and Investment Impairments

We

evaluate an asset or investment for impairment when events or circumstances

indicate that its carrying value may not be recovered. These events include

market declines that are believed to be other than temporary, changes in the

manner in which we intend to use a long-lived asset, decisions to sell an asset

or investment and adverse changes in the legal or business environment such as

adverse actions by regulators. When an event occurs, we evaluate the

recoverability of our carrying value based on either (i) the long-lived

asset’s ability to generate future cash flows on an undiscounted basis or

(ii) the fair value of our investment in unconsolidated affiliates. If an

impairment is indicated or if we decide to exit or sell a long-lived asset or

group of assets, we adjust the carrying value of these assets downward, if

necessary, to their estimated fair value, less costs to sell. Our fair value

estimates are generally based on market data obtained through the sales process

or an analysis of expected discounted cash flows. The magnitude of any

impairments are impacted by a number of factors, including the nature of the

assets to be sold and our established time frame for completing the sales, among

other factors. We also reclassify the asset or assets as either held-for-sale or

as discontinued operations, depending on, among other criteria, whether we will

have any continuing involvement in the cash flows of those assets after they are

sold.

11

Allowance

for Doubtful Accounts

We

establish provisions for losses on accounts and notes receivable if we determine

that we will not collect all or part of the outstanding balance. We regularly

review collectibility and establish or adjust our allowance as necessary using

the specific identification method. We make advances to third parties under

executed promissory notes for project costs related to the development of gaming

and entertainment properties. Due diligence is conducted by our management with

the assistance of legal counsel prior to entering into arrangements with third

parties to provide financing in connection with their efforts to secure and

develop the properties. Repayment terms are largely dependent upon the operating

performance of each opportunity for which the funds have been loaned. Interest

income is not accrued until it is reasonably assured that the project will be

completed and that there will be sufficient profits from the facility to cover

the interest to be earned under the respective note. If projected cash flows are

not sufficient to recover amounts due, the note is evaluated to determine the

appropriate discount to be recorded on the note for it to be considered a

performing note. If the note is performing, interest is recorded using the

effective interest method based on the value of the discounted note balance. See

Note 5 to our Consolidated Financial Statements.

We review

on a quarterly basis each of our notes receivable to evaluate whether the

collection of such note receivable is still probable. In our analysis, we review

the economic feasibility and the current financial, legislative and development

status of the project. If our analysis indicates that the project is no longer

economically feasible then the note receivable would be written down to its

estimated fair value. Based on this policy, we established a $1.6

million valuation allowance as of April 30, 2010 in regards to the receivable

due from the Gillman Group.

Revenue

Recognition

We record

revenues from casino operations, management fees, and interest on notes

receivable on the accrual basis as earned. The dates on which payments are

collected may vary depending upon the term of the contracts or note receivable

agreements. Interest income related to notes receivable is recorded when earned

and its collectibility is reasonably certain.

The

retail value of food and beverage and other services furnished to guests without

charge is included in gross revenue and deducted as promotional allowances. Net

revenues do not include the retail amount of food, beverage and other items

provided gratuitously to customers. We record the redemption of coupons and

points for cash as a reduction of revenue. These amounts are included in

promotional allowances in the accompanying consolidated statements of

operations. The estimated cost of providing such complimentary services that is

included in casino expense in the accompanying consolidated statements of

operations was as follows:

|

Fiscal

Year Ended

|

||||||||

|

April

30, 2010

|

April

30, 2009

|

|||||||

|

Food

and beverage

|

$ | 1,120,638 | $ | 595,499 | ||||

|

Other

|

13,601 | 5,994 | ||||||

|

Total

cost of complimentary services

|

$ | 1,134,239 | $ | 601,493 | ||||

Accrued

Jackpot Liability

We accrue

jackpot liability as games are played under a matching concept of

coin-in. As of April 30, 2010, we also maintain approximately

$267,000 in Player Supported Jackpot accrued liability, which are progressive

games that customers fund and when a jackpot is hit it is paid from reserved

funds.

Income

Taxes

Income

taxes are accounted using an asset and liability approach for financial

accounting and reporting for income taxes. Under this approach, deferred tax

assets and liabilities are recognized based on anticipated future tax

consequences, using currently enacted tax laws, attributable to differences

between financial statement carrying amounts of assets and liabilities and their

respective tax basis. We record current income taxes based on our current

taxable income, and we provide for deferred income taxes to reflect estimated

future tax payments and receipts. We account for tax credits under the

flow-through method, which reduces the provision for income taxes in the year

the tax credits first become available. Deferred tax assets are reduced by a

valuation allowance when, based on our estimates, it is more likely than not

that a portion of those assets will not be realized in a future period. The

estimates utilized in recognition of deferred tax assets are subject to

revision, either up or down, in future periods based on new facts or

circumstances.

12

Accrued

Litigation Liability

We assess

our exposure to loss contingencies including legal matters. If the

potential loss is justified to be probable and estimable, we will provide for

the exposure. If the actual loss from a contingency differs from management’s

estimate, operating results could be impacted. As of April 30, 2010, we did not

record any accrued litigation liability.

Share-Based

Compensation

Under ASC

Topic 718, “Compensation - Stock

Compensation”,

the fair value and compensation expense of each option award is estimated as of

the date of grant using a Black-Scholes option pricing formula. Expected

volatility is based on historical volatility of our stock over a preceding

period commensurate with the expected term of the option. The expected

volatility considers factors such as the volatility of our share price. The

risk-free rate for the expected term of the option is based on the

U.S. Treasury yield curve in effect at the time of grant. Expected dividend

yield was not considered in the option pricing formula since we historically

have not paid dividends and have no current plans to do so in the

future.

The

compensation cost related to these share-based awards is recognized over the

requisite service period. The requisite service period is generally the period

during which an employee is required to provide service in exchange for the

award.

Executive

Overview

We were

formed in 1977 and since 1994, have primarily been a gaming company involved in

financing, developing, owning and operating gaming projects. Our gaming facility

operations are located in the United States of America (“U.S.”), specifically in

the states of Colorado and Washington. On April 25, 2005, we acquired the

Colorado Grande Casino from IC-BH. On May 12, 2009, we acquired three

mini-casinos in Washington State. Our business strategy will continue

to focus on gaming projects with a continued emphasis on owning and operating

gaming establishments. If we are successful, both our future revenues and costs

and our profitability can be expected to increase. Our net revenues were $22.0

million and $5.9 million for fiscal years 2010 and 2009,

respectively.

We hold

investments in various development projects that we consolidate. Our net

ownership interest and capitalized development costs in development projects are

as follows (see Note 4 to the Consolidated Financial Statements):

|

Net Ownership Interest

|

Capitalized Development Costs

|

|||||||||||||||

|

Development Projects:

|

April 30,

2010

|

April 30,

2009

|

April 30,

2010

|

April 30,

2009

|

||||||||||||

|

(Percent)

|

||||||||||||||||

|

NG

Washington, LLC (1)

|

100 | 100 | $ | - | $ | 617,071 | ||||||||||

|

Nevada

Gold Speedway, LLC (2)

|

100 | - | 90,652 | - | ||||||||||||

|

NG

Washington II, LLC (3)

|

100 | - | 1,273,731 | - | ||||||||||||

|

Other

(4)

|

54,406 | 128,953 | ||||||||||||||

|

Total

investments– development projects

|

$ | 1,418,789 | $ | 746,024 | ||||||||||||

|

(1)

|

Refundable

deposits and license costs incurred for three mini-casinos in Washington

State; acquisition closed May 12,

2009.

|

|

(2)

|

Deposit

and acquisition costs related to management and technical services

contract for development of Las Vegas Speedway casino and

hotel

|

|

(3)

|

Refundable

deposits and license costs incurred for seven additional mini-casinos in

Washington State

|

|

(4)

|

Development

costs incurred for other development

projects.

|

13

Consolidated

Results of Operations

The

following table sets forth our consolidated results of operations for the fiscal

years ended April 30, 2010, and April 30, 2009:

|

Fiscal

Years Ended

|

||||||||

|

April

30,

|

April

30,

|

|||||||

|

2010

|

2009

|

|||||||

|

Revenues:

|

||||||||

|

Casino

|

$ | 18,822,900 | $ | 5,356,885 | ||||

|

Food

and beverage

|

4,534,744 | 1,395,130 | ||||||

|

Other

|

865,264 | 49,366 | ||||||

|

Management

fees

|

620,968 | 493,382 | ||||||

|

Gross

revenues

|

24,843,876 | 7,294,763 | ||||||

|

Less

promotional allowances

|

(2,817,888 | ) | (1,426,511 | ) | ||||

|

Net

revenues

|

22,025,988 | 5,868,252 | ||||||

|

Operating

expenses:

|

||||||||

|

Casino

|

8,562,284 | 1,750,014 | ||||||

|

Food

and beverage

|