Attached files

| file | filename |

|---|---|

| EX-23 - EXHIBIT 23 - CULP INC | a6355078ex23.htm |

| EX-31.(B) - EXHIBIT 31(B) - CULP INC | a6355078ex31b.htm |

| EX-24.(B) - EXHIBIT 24(B) - CULP INC | a6355078ex24b.htm |

| EX-24.(A) - EXHIBIT 24(A) - CULP INC | a6355078ex24a.htm |

| EX-24.(C) - EXHIBIT 24(C) - CULP INC | a6355078ex24c.htm |

| EX-10.15 - EXHIBIT 10.15 - CULP INC | a6355078ex1015.htm |

| EX-32.(A) - EXHIBIT 32(A) - CULP INC | a6355078ex32a.htm |

| EX-32.(B) - EXHIBIT 32(B) - CULP INC | a6355078ex32b.htm |

| EX-21 - EXHIBIT 21 - CULP INC | a6355078ex21.htm |

| EX-31.(A) - EXHIBIT 31(A) - CULP INC | a6355078ex31a.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended May 2, 2010

Commission File No. 1-12597

CULP, INC.

(Exact name of registrant as specified in its charter)

|

NORTH CAROLINA

(State or other jurisdiction of

incorporation or other organization)

|

56-1001967

(I.R.S. Employer Identification No.)

|

|

1823 Eastchester Drive, High Point, North Carolina

(Address of principal executive offices)

|

27265

(zip code)

|

|

(336) 889-5161

(Registrant’s telephone number, including area code)

|

|

Securities registered pursuant to Section 12(b) of the Act:

|

Title of Each Class

|

Name of Each Exchange

On Which Registered

|

|

Common Stock, par value $.05/ Share

|

New York Stock Exchange

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES o NO x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Securities Exchange Act of 1934. YES o NO x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months and (2) has been subject to the filing requirements for at least the past 90 days. YES x NO o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

YES o NO o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer, accelerated filer, and smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large Accelerated Filer o

|

Accelerated Filer o

|

Non-Accelerated Filer x

|

|

Smaller Reporting Company o

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). YES o NO x

As of May 2, 2010, 13,051,785 shares of common stock were outstanding. As of November 1, 2009, the aggregate market value of the voting stock held by non-affiliates of the registrant on that date was $59,366,318 based on the closing sales price of such stock as quoted on the New York Stock Exchange (NYSE), assuming, for purposes of this report, that all executive officers and directors of the registrant are affiliates.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Proxy Statement to be filed pursuant to Regulation 14A of the Securities and Exchange Commission in connection with its Annual Meeting of Shareholders to be held on September 21, 2010 are incorporated by reference into Part III of this Form 10-K.

CULP, INC.

FORM 10-K REPORT

TABLE OF CONTENTS

| Item No. | Page | ||

| PART I | |||

|

1.

|

|||

|

2

|

|||

|

3

|

|||

|

4

|

|||

|

6

|

|||

|

6

|

|||

|

7

|

|||

|

8

|

|||

|

8

|

|||

|

10

|

|||

|

11

|

|||

|

11

|

|||

|

12

|

|||

|

13

|

|||

|

13

|

|||

|

14

|

|||

|

15

|

|||

|

15

|

|||

|

16

|

|||

|

16

|

|||

|

1A.

|

17

|

||

|

1B.

|

21

|

||

|

2.

|

22

|

||

|

3.

|

23

|

||

|

4.

|

23

|

||

|

5.

|

24

|

||

|

6.

|

26

|

||

|

7.

|

27

|

||

|

7A.

|

59

|

||

|

8.

|

60

|

||

|

9.

|

107

|

||

|

9A(T).

|

107

|

||

|

9B.

|

108

|

||

|

Item No.

|

Page

|

|

|

10.

|

109

|

|

|

11.

|

109

|

|

|

12.

|

109

|

|

|

13.

|

110

|

|

|

14.

|

110

|

|

|

15.

|

111

|

|

|

111

|

||

|

114

|

||

|

114

|

||

|

115

|

||

|

116

|

||

CAUTIONARY STATEMENT CONCERNING FORWARD-LOOKING INFORMATION

Parts I and II of this report contain statements that may be deemed “forward-looking statements” within the meaning of the federal securities laws, including the Private Securities Litigation Reform Act of 1995 (Section 27A of the Securities Act of 1933 and Section 27A of the Securities and Exchange Act of 1934). Such statements are inherently subject to risks and uncertainties. Further, forward-looking statements are intended to speak only as of the date on which they are made. Forward-looking statements are statements that include projections, expectations or beliefs about future events or results or otherwise are not statements of historical fact. Such statements are often but not always characterized by qualifying words such as “expect,” “believe,” “estimate,” “plan” and “project” and their derivatives, and include but are not limited to statements about expectations for the company’s future operations or success, sales, gross profit margins, operating income, SG&A or other expenses, and earnings, as well as any statements regarding future economic or industry trends or future developments. Factors that could influence the matters discussed in such statements include the level of housing starts and sales of existing homes, consumer confidence, trends in disposable income, and general economic conditions. Decreases in these economic indicators could have a negative effect on the company’s business and prospects. Likewise, increases in interest rates, particularly home mortgage rates, and increases in consumer debt or the general rate of inflation, could affect the company adversely. Changes in consumer tastes or preferences toward products not produced by the company could erode demand for the company’s products. Changes in the value of the U.S. dollar versus other currencies can affect the company’s financial results because a significant portion of the company’s operations are located outside the United States. Strengthening of the U.S. dollar against other currencies could make the company’s products less competitive on the basis of price in markets outside the United States, and strengthening of currencies in Canada and China can have a negative impact on the company’s sales in the U.S. of products produced in those countries. Also, economic and political instability in international areas could affect the company’s operations or sources of goods in those areas, as well as demand for the company’s products in international markets. Finally, unanticipated delays or costs in executing restructuring actions could cause the cumulative effect of restructuring actions to fail to meet the objectives set forth by management. Further information about these factors, as well as other factors that could affect the company’s future operations or financial results and the matters discussed in forward-looking statements are included in the “Risk Factors” section of this report in Item 1A.

1

Culp, Inc. manufactures, sources, and markets mattress fabrics used for covering mattresses and box springs, and upholstery fabrics primarily for use in production of upholstered furniture (residential and commercial).

We believe that Culp is the largest producer of mattress fabrics in North America, as measured by total sales, and one of the largest marketers of upholstery fabrics for furniture in North America, again measured by total sales. We have two operating segments – mattress fabrics and upholstery fabrics. The mattress fabric business markets woven and knitted fabrics that are used primarily in the production of bedding products, including mattresses, box springs, and mattress sets. The upholstery fabric business markets a variety of fabric products that are used in the production of residential and commercial upholstered furniture, sofas, recliners, chairs, loveseats, sectionals, sofa-beds, and office seating. Culp primarily markets fabrics that have broad appeal in the “good” and “better” priced categories of furniture and bedding.

Culp markets a variety of fabrics in different categories to its global customer base, including fabrics produced at our manufacturing facilities and fabrics produced by other suppliers. The company had eight active manufacturing plants and distribution facilities as of the end of fiscal 2010, which are located in North and South Carolina, Quebec, Canada, and Shanghai, China. We also source fabrics from other manufacturers, located primarily in China and Turkey, with almost all of those fabrics being produced specifically for the company and created by Culp designers. We operate distribution centers in North Carolina and Shanghai, China to facilitate distribution of our products. In recent fiscal years, the portion of total company sales represented by fabrics produced outside of the U.S. and Canada has increased, while sales of goods produced in the U.S. have decreased. This trend is due to the upholstery fabrics segment, where more than three-fourths of our sales now consist of fabrics produced in Asia.

Total net sales in fiscal 2010 were $206 million. The mattress fabrics segment had net sales of $115 million (56% of total net sales), while the upholstery fabrics segment had net sales of $91 million (44% of total net sales).

Sales increased in our upholstery fabrics segment and declined slightly in our mattress fabric segment during fiscal 2010 as compared to fiscal 2009. Weak business conditions in the home furnishings industry affected both of our business segments in the first half of the fiscal year. Although overall economic conditions remained weak, company performance in the second half of the fiscal year showed significant improvement, as compared to the previous year.

2

In mattress fabrics, knitted fabrics has been a growing portion of our sales, as consumer demand for this type of mattress panel covering has risen significantly. During fiscal 2009, we acquired the knitted fabrics business of Bodet & Horst USA, including its manufacturing operation in High Point, North Carolina, which had served as our primary source of knitted mattress fabric. This acquisition has provided us with more control over our ability to supply bedding customers with this increasingly popular fabric type.

In the upholstery fabrics segment, the majority of our fabrics are produced by other manufacturers, but in most cases the company continues to control important components of the production process, such as design, finishing, quality control and distribution. Microdenier suedes and a variety of other fabrics are sourced in China through our sourcing, finishing and distribution operation located near Shanghai.

In recent years the company has aggressively positioned itself as a more flexible upholstery fabric producer and marketer, with a smaller fixed asset base than in prior fiscal years, and with a more variable cost structure that will allow us to take advantage of opportunities in the bedding and furniture industries as they occur. We believe the improved performance for fiscal 2010 reflects the benefits of a lean and agile operating platform along with a strong competitive position in both businesses.

Additional information about trends and developments in each of our business segments is provided in the “Segments” discussion below.

Culp, Inc. was organized as a North Carolina corporation in 1972 and made its initial public offering in 1983. Since 1997, our stock has been listed on the New York Stock Exchange and traded under the symbol “CFI.” Our fiscal year is the 52 or 53 week period ending on the Sunday closest to April 30. Our executive offices are located in High Point, North Carolina.

Culp maintains an Internet website at www.culp.com. We will make this annual report and our other annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to these reports, available free of charge on our Internet site as soon as reasonably practicable after such material is electronically filed with, or furnished to, the Securities and Exchange Commission. Information included on our website is not incorporated by reference into this annual report.

3

Our two operating segments are mattress fabrics and upholstery fabrics. The following table sets forth certain information for each of our segments.

|

Sales by Fiscal Year ($ in Millions) and

Percentage of Total Company Sales

|

|||||||||||||||

|

Segment

|

Fiscal 2010

|

Fiscal 2009

|

Fiscal 2008

|

||||||||||||

|

Mattress Fabrics

|

$114.8

|

(56%)

|

$115.4

|

(57%)

|

$138.1

|

(54%) | |||||||||

|

Upholstery Fabrics

|

|||||||||||||||

|

Non-U.S.-Produced

|

$77.3

|

(37%)

|

$68.1

|

(33%)

|

$75.9

|

(30%) | |||||||||

|

U.S.-Produced

|

$14.3

|

(7%)

|

$20.4

|

(10%)

|

$40.0

|

(16%)

|

|||||||||

|

Total Upholstery

|

$91.6

|

(44%)

|

$88.5

|

(43%)

|

$115.9

|

(46%) | |||||||||

|

Total company

|

$206.4

|

(100%)

|

$203.9

|

(100%)

|

$254.0

|

(100%) | |||||||||

Additional financial information about our operating segments can be found in Note 20 to the Consolidated Financial Statements included in Item 8 of this report.

Mattress Fabrics. The mattress fabrics segment manufactures and markets mattress fabric to bedding manufacturers. These fabrics encompass woven jacquard fabric and knitted fabric. Culp Home Fashions has manufacturing facilities located in Stokesdale and High Point, North Carolina, and St. Jerome, Quebec, Canada. The Stokesdale and St. Jerome plants manufacture and finish jacquard (damask) fabric. The Stokesdale plant also finishes knit fabrics, as well as houses the division offices and finished goods distribution capabilities. In August 2008, a third manufacturing plant facility was added when we acquired the knitted mattress fabrics business of Bodet & Horst USA, including its manufacturing facilities in High Point. We have also maintained flexibility in our supply of the major categories of mattress fabrics. All woven jacquard and knitted fabrics can be produced in multiple facilities, (internal or external to the company) providing us with mirrored, reactive capacity involving state of the art capabilities across plant facilities.

In recent fiscal years, we have taken significant steps to enhance our competitive position in this segment by consolidating all of our mattress fabrics manufacturing into these three manufacturing facilities. The company had capital expenditures during the period fiscal 2005 through 2010 totaling approximately $27 million, which primarily provided for the purchase of faster and more efficient weaving machines as well as increased knit machine capacity. These capital expenditures also provided high technology finishing equipment for woven and knitted fabrics.

The Bodet & Horst USA, LP acquisition was another step to enhance and secure our competitive position, as we invested $11.4 million to purchase the manufacturing operation that had been serving as our primary source of knitted mattress fabric. Knitted fabrics have been an increasingly important category of mattress fabrics, with industry sales in this type of fabric growing much faster than other categories. The completion of this acquisition during fiscal 2009 not only secured our supply of knitted mattress fabrics, but allowed for improved supply logistics, greater control of product development, and accelerated responsiveness to our customers. Subsequent to this acquisition, the demand for knitted mattress fabrics has continued to grow. During fiscal 2010, we made further investments in knitting machines and finishing equipment.

4

Upholstery Fabrics. The upholstery fabrics segment markets fabrics for residential and commercial furniture, including jacquard woven fabrics, velvets, microdenier suedes, woven dobbies, knitted fabrics, and piece-dyed woven products. Historically, all of our upholstery fabrics had been produced in our U.S. manufacturing plants. However, in fiscal 2007, sales of upholstery fabrics made in non-U.S. locations, including our facilities in China, exceeded U.S.-produced sales for the first time. In fiscal 2010, sales of non-U.S. produced upholstery accounted for almost 84% of our upholstery sales.

The upholstery fabrics segment operates fabric manufacturing facilities in Anderson, South Carolina, and Shanghai, China. We market fabrics produced in these two locations, as well as a variety of upholstery fabrics sourced from third party producers, mostly in China.

As demand for U.S.-produced upholstery declined significantly, we took aggressive steps to reduce our U.S. manufacturing costs, capacity, and selling, general and administrative expenses. Our restructuring actions over the past several years reduced our U.S. upholstery operations to the one manufacturing plant in South Carolina and one upholstery distribution facility in Burlington, North Carolina.

During the time that U.S. upholstery operations were shrinking, we established operations in China and gradually expanded them over time to include a variety of activities. The facilities near Shanghai began operations in 2004 with a finishing and inspection operation, where goods woven in China by selected outside suppliers are treated with finishing processes and subjected to U.S. quality control measures before being distributed to customers. In subsequent fiscal years, a variety of finished goods (with no further finishing needed) began to be sourced through our China operations, and in fiscal 2006 the operation was expanded to include a facility where upholstery fabrics are cut and sewn into “kits” that are made to the specifications of furniture manufacturing customers in the U.S. Cut and sewn “kit” operations have become an important method for furniture producers to reduce production costs by moving a larger percentage of the labor component of furniture manufacturing to lower cost environments. Other recent developments in our China operations include expansion of our product development and design capabilities in China and further strengthening of key strategic partnerships with mills. We also expanded our marketing efforts to sell our China products in countries other than the U.S., including the Chinese local market.

Over the past decade, we have moved our upholstery fabrics business from one that relied on a large fixed capital base that is difficult to adjust to a more flexible and scalable marketer of upholstery fabrics that meets changing levels of customer demand. At the same time, we have attempted to maintain control of the most important “value added” aspects of our business, such as design, finishing, quality control, and logistics. This strategic approach has allowed us to limit our investment of capital in fixed assets and to lower the costs of our products significantly, while continuing to leverage our design and finishing expertise, industry knowledge and important relationships.

5

Despite a very difficult economic backdrop in fiscal 2010, our sales in the upholstery fabric category resulted in an annual increase of 3.4%, representing the first annual gain in ten fiscal years. Increased sales in the upholstery fabrics segment were primarily the result of gains achieved through implementation of a business strategy that included: 1) innovation in a low- cost environment, 2) speed to market execution, 3) consistent quality, 4) reliable service and lead times, and 5) increased recognition of and reliance on the Culp brand. A return to profitability in upholstery fabrics has been achieved through development of a unique business model that has enabled the upholstery segment to execute a strategy that we believe is clearly differentiated from competitors. In this way, we have maintained our ability to provide furniture manufacturers with products from every category of fabric used to cover upholstered furniture, and to meet continually changing demand levels and consumer preferences.

Culp markets products primarily to manufacturers that operate in three principal markets. The mattress fabrics segment supplies the bedding industry, which produces mattress sets (mattresses, box springs, and foundations). The upholstery fabrics segment supplies the residential furniture industry and, to a lesser extent, the commercial furniture industry. The residential furniture market includes upholstered furniture sold to consumers for household use, including sofas, sofa-beds, chairs, recliners and sectionals. The commercial furniture and fabrics market includes upholstered office seating and modular office systems sold primarily for use in offices and other institutional settings, and commercial textile wall covering. The principal industries into which the company sells products are described below.

After many years of steady growth, both in unit volume and average selling prices, the bedding industry experienced a decrease in overall sales in calendar 2009 and 2008, due to the weak economy and an especially weak housing market. According to the International Sleep Products Association (ISPA), a trade association, the U.S. wholesale bedding industry accounted for an estimated $5.7 billion in sales in 2009, an 8.4% decrease from 2008. According to industry statistics, specialty bedding producers, which produce mattresses that do not use inner spring construction, saw sales decrease by 11.7% in 2009. The industry is comprised of several hundred manufacturers, but the largest five manufacturers accounted for more than 63% of the total wholesale shipments in 2009, while the top fifteen accounted for approximately 81%. Until recently, the bedding industry has been mature and stable. However, during the past two fiscal years it has weakened due to economic pressures. On a long-term basis, the stability of this market has been due in part to replacement purchases, which account for the majority of bedding industry sales. The overall weakness in the bedding market during 2008 and 2009 reflected a slight decline in average selling prices for mattresses sold in the U.S. According to ISPA, wholesale sales of bedding decreased 8.4% in 2009 and the number of units sold decreased by 11.0%. However, more recent interim industry reports show year-over-year growth, with units and dollars increasing by 12.8% and 10.7%, respectively, on a year-to-date basis as of May 2010.

6

Unlike the residential furniture industry, which has faced intense competition from imports, the bedding industry has largely remained a North American based business with limited competition from imports. The primary reasons for this fact include: 1) the short lead times demanded by mattress manufacturers and retailers due to their quick service delivery model, 2) the limited inventories carried by manufacturers and retailers requires “just-in-time” delivery of product, 3) the customized nature of each manufacturer and retailer’s product lines, 4) high shipping and import duty costs, 5) the relatively low direct labor content in mattresses, and 6) strong brand recognition.

Other key trends in the bedding industry include:

|

·

|

Consumers have become increasingly aware of and are concerned with the health benefits of better sleep. This has caused an increased focus on the quality of bedding products and an apparent willingness on the part of consumers to pay more for bedding.

|

|

·

|

While mattress fabrics serve the functional purpose of providing a soft and durable cover, there is a growing emphasis on the design knitted or woven into the fabrics to appeal to the customer’s visual attraction and perceived value of the mattress on the retail floor. Mattress fabric design efforts are based on current trends in home décor and fashion.

|

|

·

|

Growth in non-traditional sources for retail mattress sales is now an important factor in home furnishings forecasts. These sales outlets, such as wholesale warehouse clubs and the internet, have the potential to increase overall consumption of goods due to convenience and high traffic volume which in turn result in higher turnover of product.

|

|

·

|

Increased popularity of knitted mattress fabric has continued. Knitted fabric was initially used primarily on premium mattresses, but these products are now being placed increasingly on mattresses at mid-range retail price points.

|

The residential furniture industry has been severely affected by the global economic downturn. Declines in consumer spending and a very weak housing market led to significantly lower sales of residential furniture in 2008, a trend that continued into 2009. According to data published by the American Home Furnishings Alliance (AHFA), a trade association, prior to 2008 the residential furniture industry was mature and stable, with growth rates at or below the overall growth rate of the U.S. economy. However, shipments declined by 14.8% in 2008 compared to the prior year, and in 2009 retail furniture shipments dropped 18.1% compared to 2008. The overall weak demand for residential furniture has continued to affect the residential furniture industry, creating significant challenges for suppliers to the industry.

Other important trends and issues facing the residential furniture industry include:

|

·

|

The sourcing of components and fully assembled furniture from overseas continues to play a major role in the residential furniture industry, although in 2008 and to a greater extent in 2009, the import rate declined. According to Furniture/Today, an industry trade publication, imports of residential furniture into the U.S. fell by 21% in 2009, following a decrease of 6% in 2008. By far, the largest source for these imports continues to be China, which now accounts for approximately 57% of total U.S. furniture imports. In past years, a large majority of furniture imports from China were wooden “casegoods,” but there has been significant recent growth in imports of upholstered furniture components, including upholstery fabric and “cut and sewn kits” for furniture covers. This trend has been especially strong for leather furniture, and it now extends to other coverings, including microdenier suedes and the more traditional types of fabrics manufactured by the company. The shift to offshore sourcing has led to significant deflation in retail furniture prices.

|

7

|

·

|

Imports of upholstery fabric, both in roll and in “kit” form, have increased in recent years. Fabrics entering the U.S. from China and other low labor cost countries are resulting in increased price competition in the upholstery fabric and upholstered furniture markets.

|

|

·

|

Leather and suede upholstered furniture has been gaining market share over the last ten years. This trend has increased over the last six years in large part because selling prices of leather furniture have been declining significantly over this time period.

|

|

·

|

The residential furniture industry has been consolidating at the manufacturing level for several years. The result of this trend is fewer, but larger, customers for marketers of upholstery fabrics.

|

The market for commercial furniture - furniture used in offices and other institutional settings - declined approximately 29.7% from 2008 to 2009, following a 2.3% decline the previous year. The decline in 2009 reflects economic trends affecting businesses, which are the ultimate customers in this industry. This trend appears to be continuing into 2010 along with weak overall business conditions. According to the Business and Institutional Furniture Manufacturer’s Association (BIFMA), a trade association, the commercial furniture market in the U.S. totaled approximately $7.8 billion in 2009 in wholesale shipments by manufacturers, a substantial decline from the $11.2 billion total for 2008. This total represents a significant decrease from the industry’s peak of $13.3 billion in 2000.

As described above, our products include mattress fabrics and upholstery fabrics, which are the company’s identified operating segments.

Mattress Fabrics Segment

Mattress fabrics segment sales constituted 56% of sales in fiscal 2010, and 57% in fiscal 2009. The company has emphasized fabrics that have broad appeal at prices generally ranging from $1.35 to $7.50 per yard.

8

Upholstery Fabrics Segment

Upholstery fabrics segment sales totaled 44% of sales for fiscal 2010, and 43% in fiscal 2009. The company has emphasized fabrics that have broad appeal at “good” and “better” prices, generally ranging from $2.75 to $8.00 per yard.

Culp Fabric Categories by Segment

We market products in most categories of fabric that manufacturers currently use for bedding and furniture. The following table indicates the product lines within each segment, and a brief description of their characteristics.

Mattress Fabrics

|

Woven jacquards

|

Florals and other intricate designs. Woven on complex looms using a variety of synthetic and natural yarns.

|

|

Specialty

|

Suedes, velours, and other specialty type products are sourced to offer diversity for higher end mattresses.

|

|

Knitted Fabric

|

Floral and other intricate designs produced on special-width circular knit machines utilizing a variety of synthetic and natural yarns. Knitted mattress fabrics have inherent stretching properties and spongy softness, which conforms well with layered foam packages.

|

Upholstery Fabrics

|

Woven jacquards

|

Elaborate, complex designs such as florals and tapestries in traditional, transitional and contemporary styles. Woven on intricate looms using a wide variety of synthetic and natural yarns.

|

|

Woven dobbies

|

Fabrics that use straight lines to produce geometric designs such as plaids, stripes and solids in traditional and country styles. Woven on less complicated looms using a variety of weaving constructions and primarily synthetic yarns.

|

|

Velvets

|

Soft fabrics with a plush feel. Produced with synthetic yarns, either by weaving or by “tufting” yarn into a base fabric. Basic designs such as plaids in both traditional and contemporary styles.

|

|

Suede fabrics

|

Fabrics woven or knitted using microdenier polyester yarns, which are piece dyed and finished, usually by sanding. The fabrics are typically plain or small jacquard designs, with some being printed. These are sometimes referred to as microdenier suedes, and some are “leather look” fabrics.

|

9

Mattress Fabrics Segment

Our mattress fabrics segment operates three manufacturing plants, located in Stokesdale, North Carolina; High Point, North Carolina and St. Jerome, Quebec, Canada. Over the past six fiscal years, we made capital expenditures of approximately $27 million to consolidate all of our production of woven jacquards, or damask fabric, to two of these plants and to modernize the equipment, enhance and provide finishing capabilities and expand capacity in each of these facilities. The result has been an increase in manufacturing efficiency and a substantial reduction in operating costs. Jacquard mattress fabric is woven at the Stokesdale and St. Jerome plants, and knitted fabrics are produced at the High Point facility. Most finishing and inspection processes for mattress fabrics are conducted at the Stokesdale plant.

In addition to the mattress fabrics we manufacture, we have important supply arrangements in place that allow us to source mattress fabric from strategic suppliers. A portion of our woven jacquard fabric and knitted fabric is obtained from a supplier located in Turkey, based on designs created by Culp designers, and we are sourcing certain specialty fabric products (such as suedes and embroidered fabrics) through our China platform.

Upholstery Fabrics Segment

We currently operate one upholstery manufacturing facility in the U.S. and three in China. The U.S. plant is located in Anderson, South Carolina, and mainly produces velvet upholstery fabrics with some production of certain decorative fabrics.

Our upholstery manufacturing facilities in China are all located within the same industrial area near Shanghai. At these plants, we apply strategic value-added finishing processes to fabrics sourced from a limited number of strategic suppliers in China, and we inspect sourced fabric there as well. In addition, the Shanghai operations include facilities where sourced fabric is cut and sewn to provide “kits” that are designed to be placed on specific furniture frames designated by our customers.

A large portion of our upholstery fabric products, as well as certain elements of our production processes, are being sourced from outside suppliers. The development of our facilities in China has provided a base from which to access a variety of products, including certain fabrics (such as microdenier suedes) that are not produced anywhere within the U.S. We have found opportunities to develop significant relationships with key overseas suppliers that allow us to source products on a cost-effective basis while at the same time limiting our investment of capital in manufacturing assets. We source unfinished and finished fabrics from a limited number of strategic suppliers in China who are willing to commit significant capacity to meet our needs while working with our product development team to meet the demands of our customers. We also source a substantial portion of our yarns, both for U.S. and China upholstery operations, through our China facilities. The remainder of our yarn is obtained from other suppliers around the world, as we have eliminated our internal yarn production capabilities.

10

Consumer tastes and preferences related to bedding and upholstered furniture change over time. The use of new fabrics and designs remains an important consideration for manufacturers to distinguish their products at retail and to capitalize on changes in preferred colors, patterns and textures. Culp’s success is largely dependent on our ability to market fabrics with appealing designs and patterns. The process of developing new designs involves maintaining an awareness of broad fashion and color trends both in the United States and internationally.

Mattress Fabrics Segment

Design is an important element of producing mattress fabrics. Price point delineation is accomplished through fabric quality as well as variation in design. Additionally, a consumer will be drawn to the mattress that is most visually appealing when walking into the retail showroom. Fibers also play an important part in design. Rayon, organic cotton and recycled fibers are incorporated into the design process to allow the retailer to offer the consumer additional benefits related to their sleeping experience. Mattress fabric designs are not introduced on a scheduled season. More frequently, designs are introduced upon customer request as they plan introduction to their retailers. Additionally, we work closely with our customers on new design offerings around the major furniture markets such as High Point and Las Vegas.

Upholstery Fabrics Segment

The company has developed an upholstery fabrics design and product development team (with staff located in the U.S. and in China) with focus on designing for value primarily on body cloths, while promoting style leadership with pillow fabrics and color. The team searches continually for new ideas and for the best sources of raw materials, yarns and fabrics utilizing a China supply network. Using these design elements, they develop product offerings using ideas and materials which take both fashion trends and cost considerations into account, to offer products designed to meet the needs of furniture manufacturers and ultimately the desires of consumers. Upholstery fabric designs are introduced at major fabric trade conferences that occur twice a year in the United States (June and December). Recently we have become more aggressive in registering copyrights for popular fabric patterns and taking steps to discourage the illegal copying of our proprietary designs.

Mattress Fabrics Segment

All of our shipments of mattress fabrics originate from our manufacturing facility in Stokesdale. Through arrangements with major customers and in accordance with industry practice, we maintain a significant inventory of mattress fabrics at our distribution facility in Stokesdale (“make to stock”), so that products may be shipped to customers with short lead times and on a “just in time” basis.

Upholstery Fabrics Segment

The majority of our upholstery fabrics are marketed on a “make to order” basis and are shipped directly from our distribution facilities in Burlington and Shanghai. In addition, an inventory comprising of a limited number of sourced fabric patterns is held at our distribution facilities in Burlington and Shanghai from which our customers can obtain quick delivery of sourced fabrics through a program known as “Culp Express.” We have developed a revised marketing strategy for our U.S.-produced upholstery products, providing customers with very quick delivery on target products at key price points. This program, known as “Store House,” is aimed at driving higher sales volume per fabric pattern and thus should result in improved manufacturing performance and lower unit costs for our U.S. upholstery operations, while employing a smaller fixed asset base. During fiscal 2010, market share opportunities have been expanded through strategic selling partnerships.

11

Mattress Fabrics Segment

Raw materials account for approximately 70% of mattress fabric production costs. The mattress fabrics segment purchases synthetic yarns (polypropylene, polyester and rayon), certain greige (unfinished) goods, latex adhesives, laminates, dyes and other chemicals. Most of these materials are available from several suppliers, and prices fluctuate based on supply and demand, the general rate of inflation, and particularly on the price of petrochemical products. The mattress fabrics segment has generally not had significant difficulty in obtaining raw materials.

Upholstery Fabrics Segment

Raw materials account for approximately 50%-60% of upholstery fabric manufacturing costs for products the company manufactures. This segment purchases synthetic yarns (polypropylene, polyester, acrylic and rayon), acrylic staple fiber, latex adhesives, dyes and other chemicals from various suppliers.

The upholstery fabric segment has outsourced all of its yarn requirements, and thus it has become more dependent upon suppliers for components yarn. In addition, we have outsourced a number of our U.S. upholstery fabric manufacturing services to suppliers, such as extrusion of yarn and upholstery fabric finishing. Although U.S. produced fabrics are a decreasing portion of our upholstery business, increased reliance by both our U.S. and China upholstery operations on outside suppliers for basic production needs such as base fabrics, yarns, and finishing services has caused the upholstery fabrics segment to become more vulnerable to price increases, delays, or production interruptions caused by problems within businesses that we do not control.

Both Segments

Many of our basic raw materials are petrochemical products or are produced from such products. For this reason, our material costs are especially sensitive to changes in prices for petrochemicals and the underlying price of oil. In addition, the financial condition and performance of a number of U.S.-based yarn suppliers has been severely impacted by the reductions in the overall size of the U.S. textile industry over the last several years. These conditions have increased the risk of business failures or further consolidations among the suppliers to the North American-based portions of our business. This situation could cause additional disruptions and pricing pressures in our supply of certain raw materials, yarns, and textile services obtained in the U.S. as overall demand for textiles produced in the U.S. declines.

12

Mattress Fabrics Segment

The mattress fabrics business and the bedding industry in general are slightly seasonal, with sales being the highest in late spring and late summer, with another peak in mid-winter.

Upholstery Fabrics Segment

The upholstery fabrics business is somewhat seasonal, with increased sales during our second and fourth fiscal quarters. This seasonality results from one-week closings of our manufacturing facilities and the facilities of most of our customers in the United States during our first and third fiscal quarters for the holiday weeks of July 4th and Christmas. This effect is becoming less pronounced as a larger portion of our fabrics are produced or sold in locations outside of the United States. However, the Chinese New Year (which occurs in January or February each year) can cause increased demand for products produced in China during the period immediately preceding the holiday.

Competition for our products is high and is based primarily on price, design, quality, timing of delivery and service.

Mattress Fabrics Segment

The mattress fabrics market is concentrated in a few relatively large suppliers. We believe our principal mattress fabric competitors are Bekaert Textiles B.V., Global Textile Alliance and several smaller companies producing knitted and other fabric.

Upholstery Fabrics Segment

In the upholstery fabric market, we compete against a large number of companies, ranging from a few large manufacturers comparable in size to the company to small producers, and a growing number of “converters” of fabrics (companies who buy and re-sell, but do not manufacture fabrics). We believe our principal upholstery fabric competitors are Richloom Fabrics, Merrimack Fabrics, Morgan Fabrics, and Specialty Textile, Inc. (or STI), plus a large number of smaller competitors (both manufacturers and converters).

Today, there is significant increased competition in U.S. markets by foreign producers of upholstery fabric, furniture components and finished upholstery furniture (as well as sales in the U.S. of leather furniture produced overseas which competes with upholstered furniture for market share). Foreign manufacturers often are able to produce upholstery fabric and other components of furniture with significantly lower raw material and production costs (especially labor) than those of our U.S. operations and other U.S.-based manufacturers. We compete with lower cost foreign goods on the basis of design, quality, reliability and speed of delivery. In addition, our operations in China allow us to facilitate the sourcing and marketing of goods produced in China.

13

The trend in the upholstery fabrics industry to greater overseas competition and the entry of more converters has caused the upholstery fabrics industry to become substantially more fragmented in recent years, with lower barriers to entry. This has resulted in a larger number of competitors selling upholstery fabrics, with an increase in competition based on price.

We are subject to various federal and state laws and regulations, including the Occupational Safety and Health Act (“OSHA”) and federal and state environmental laws, as well as similar laws governing our manufacturing facilities in China and Canada. We periodically review our compliance with these laws and regulations in an attempt to minimize the risk of violations.

Our operations involve a variety of materials and processes that are subject to environmental regulation. Under current law, environmental liability can arise from previously owned properties, leased properties and properties owned by third parties, as well as from properties currently owned and leased by the company. Environmental liabilities can also be asserted by adjacent landowners or other third parties in toxic tort litigation.

In addition, under the Comprehensive Environmental Response, Compensation, and Liability Act of 1980, as amended (“CERCLA”), and analogous state statutes, liability can be imposed for the disposal of waste at sites targeted for cleanup by federal and state regulatory authorities. Liability under CERCLA is strict as well as joint and several.

The U.S. Congress is currently considering legislation to address climate change that is intended to reduce overall green house gas emissions, including carbon dioxide. In addition, the U.S. Environmental Protection Agency has made a determination that green house gas emissions may be a threat to human health and the environment. International agreements may also result in new regulations on green house gas emissions. It is uncertain if, when, and in what form, a mandatory carbon dioxide emissions reduction program may be enacted either through legislation or regulation. However, if enacted, this type of program could materially increase our operating costs, including costs of raw materials, transportation and electricity. It is difficult to predict the extent to which any new rules or regulations would impact our business, but we would expect the effect on our operations to be similar to that for other manufacturers, particularly those in our industry.

We are periodically involved in environmental claims or litigation and requests for information from environmental regulators. Each of these matters is carefully evaluated, and the company provides for environmental matters based on information presently available. Based on this information, we do not believe that environmental matters will have a material adverse effect on either the company’s financial condition or results of operations. However, there can be no assurance that the costs associated with environmental matters will not increase in the future. See the discussion of a current environmental claim against the company below in Item 3 — “Legal Proceedings.”

14

As of May 2, 2010, we had 1,085 employees, compared to 1,047 at the end of fiscal 2009, and 1,187 at the end of fiscal 2008. Overall, the number of employees decreased over the past last five fiscal years in connection with our restructuring initiatives and efforts to reduce U.S. upholstery fabrics manufacturing costs, as well as initiatives to outsource certain operations. The number of employees located in the U.S. has decreased even more dramatically, while the number of employees in China has increased (see table below).

The hourly employees at our manufacturing facility in Canada (approximately 16% of the company’s workforce) are represented by a local, unaffiliated union. The collective bargaining agreement for these employees expires on February 1, 2011. We are not aware of any efforts to organize any more of our employees, and we believe our relations with our employees are good.

The following table illustrates the changes in the location of our workforce and number of employees, as of year-end, over the past five fiscal years.

|

Number of Employees

|

|||||||||||||||||||||

|

Fiscal 2010

|

Fiscal 2009

|

Fiscal 2008

|

Fiscal 2007

|

Fiscal 2006

|

|||||||||||||||||

|

Mattress Fabrics Segment

|

430 | 420 | 373 | 361 | 351 | ||||||||||||||||

|

Upholstery Fabrics Segment

|

|||||||||||||||||||||

|

United States

|

123 | 119 | 230 | 297 | 659 | ||||||||||||||||

|

China

|

528 | 504 | 481 | 479 | 270 | ||||||||||||||||

|

Total Upholstery Fabrics Segment

|

651 | 623 | 711 | 776 | 929 | ||||||||||||||||

|

Unallocated corporate

|

4 | 4 | 3 | 3 | 3 | ||||||||||||||||

|

Total

|

1,085 | 1,047 | 1,087 | 1,140 | 1,283 | ||||||||||||||||

Mattress Fabrics Segment

Major customers for our mattress fabrics include the leading bedding manufacturers: Sealy, Serta (National Bedding), and Simmons. The loss of one or more of these customers would have a material adverse effect on the company. Our largest customer in the mattress fabrics segment is the parent company of Serta and Simmons (controlled by Ares Management, LLC and Ontario Teachers&apos), accounting for approximately 22% of the company’s overall sales in fiscal 2010. Our mattress fabrics customers also include many small and medium-size bedding manufacturers.

Upholstery Fabrics Segment

Our major customers for upholstery fabrics are leading manufacturers of upholstered furniture, including Ashley, Bassett, Berkline/Benchcraft, Best Home Furnishings, Flexsteel, Furniture Brands International (Broyhill and Lane), Klaussner Furniture, La-Z-Boy (La-Z-Boy Residential, Bauhaus, and England) and Southern Motion. Major customers for the company’s fabrics for commercial furniture include HON Industries. Our largest customer in the upholstery fabrics segment is La-Z-Boy Incorporated, the loss of which would have a material adverse effect on the company. Our sales to La-Z-Boy accounted for approximately 12% of the company’s total net sales in fiscal 2010.

15

The following table sets forth the company’s net sales by geographic area by amount and percentage of total net sales for the three most recent fiscal years.

(dollars in thousands)

|

Fiscal 2010

|

Fiscal 2009

|

Fiscal 2008

|

||||||||||||||||||||||

|

United States

|

160,360 | 77.7 | % | $ | 160,290 | 78.6 | % | $ | 202,701 | 79.8 | % | |||||||||||||

|

North America

(Excluding USA)

|

11,654 | 5.6 | 14,440 | 7.1 | 18,880 | 7.4 | ||||||||||||||||||

|

Far East and Asia

|

31,856 | 15.4 | 27,509 | 13.5 | 28,465 | 11.2 | ||||||||||||||||||

|

All other areas

|

2,546 | 1.2 | 1,699 | 0.8 | 4,000 | 1.6 | ||||||||||||||||||

|

Subtotal (International)

|

46,056 | 22.3 | 43,648 | 21.4 | 51,435 | 20.2 | ||||||||||||||||||

|

Total

|

206,416 | 100 | % | $ | 203,938 | 100.0 | % | $ | 254,046 | 100.0 | % | |||||||||||||

For additional segment information, see Note 20 in the consolidated financial statements.

Mattress Fabrics Segment

The backlog for mattress fabric is not a reliable predictor of future shipments because the majority of sales are on a just-in-time basis.

Upholstery Fabrics Segment

Although it is difficult to predict the amount of backlog that is “firm,” we have reported the portion of the upholstery fabric backlog from customers with confirmed shipping dates within five weeks of the end of the fiscal year. On May 2, 2010, the portion of the upholstery fabric backlog with confirmed shipping dates prior to June 6, 2010 was $9.0 million, all of which are expected to be filled early during fiscal 2010, as compared to $8.3 million as of the end of fiscal 2009 (for confirmed shipping dates prior to June 7, 2009).

16

Our business is subject to risks and uncertainties. In addition to the matters described above under “Cautionary Statement Concerning Forward-Looking Information,” set forth below are some of the risks and uncertainties that could cause a material adverse change in our results of operations or financial condition.

A continuation of the current economic downturn could result in declines in our sales and earnings.

Overall demand for our products depends upon consumer demand for furniture and bedding, which is subject to variations in the general economy. Because purchases of furniture or bedding are discretionary purchases for most individuals and businesses, demand for these products is sometimes more easily influenced by economic trends than demand for other products. Economic downturns can affect consumer spending habits and demand for home furnishings, which reduces the demand for our products and therefore could cause a decrease in our sales and earnings. The ongoing economic slowdown has caused a decrease in consumer spending and demand for home furnishings, including goods that incorporate our products.

It has been difficult to maintain and increase sales levels in the upholstery fabrics segment.

Although sales increased in fiscal 2010 for our upholstery fabrics segment, this was the first annual increase in sales for this business in ten fiscal years. Increased competition and fragmentation of the upholstery fabrics business, including a dramatic shift to imported fabrics and resulting price deflation for upholstery fabrics, have led to a significant reduction in the size of our upholstery business. The growth and profitability achieved by this segment in fiscal 2010 are encouraging, but there is no assurance that we will be able to maintain or consistently grow this business in the future.

Increased reliance on offshore operations and foreign sources of products or raw materials increases the likelihood of disruptions to our supply chain or our ability to deliver products to our customers on a timely basis.

We now rely significantly on operations in distant locations, particularly China, and in addition we have been purchasing an increasing share of our products and raw materials from offshore sources. At the same time, our domestic manufacturing capacity for the upholstery fabrics segment has been greatly reduced. These changes have caused us to place greater reliance on a much longer supply chain and on a larger number of suppliers that we do not control, both of which are inherently subject to greater risks of delay or disruption. In addition, operations and sourcing in foreign areas are subject to the risk of changing local governmental rules, taxes, changes in import rules or customs, potential political unrest, or other threats that could disrupt or increase the costs of operating in foreign areas or sourcing products overseas. Changes in the value of the U.S. dollar versus other currencies can affect our financial results because a significant portion of our operations are located outside the United States. Strengthening of the U.S. dollar against other currencies can have a negative impact on our sales of products produced in those countries. Any of the risks associated with foreign operations and sources could cause unanticipated increases in operating costs or disruptions in business, which could negatively impact our ultimate financial results.

17

We may have difficulty managing the outsourcing arrangements increasingly being used for products and services.

We are relying more on outside sources for various products and services, including yarn and other raw materials, greige (unfinished) fabrics, finished fabrics, and services such as weaving and finishing. Increased reliance on outsourcing lowers our capital investment and fixed costs, but it decreases the amount of control that we have over certain elements of our production capacity. Interruptions in our ability to obtain raw materials or other required products or services from our outside suppliers on a timely and cost effective basis, especially if alternative suppliers cannot be immediately obtained, could disrupt our production and damage our financial results.

Further write-offs or write-downs of assets would result in a decrease in our earnings and shareholders’ equity.

The company has long-lived assets, consisting mainly of property, plant and equipment and goodwill. ASC Topic 360 establishes an impairment accounting model for long-lived assets such as property, plant, and equipment and requires the company to assess for impairment whenever events or changes in circumstances indicate that the carrying value of the asset may not be recovered. ASC Topic 350 requires that goodwill be tested at least annually for impairment or whenever events or changes in circumstances indicate that the carrying value of the asset may not be recovered. Restructuring activities and other tests for impairment have resulted and could in the future result in the write-down of a portion of our long-lived assets and a corresponding reduction in earnings and net worth. In fiscal 2008, the company experienced asset write-downs of property, plant and equipment of $792,000, of which $503,000 related to the upholstery fabrics segment and $289,000 related to the mattress fabrics segment. In fiscal 2009, we experienced an additional $8 million in similar write-downs in the upholstery fabrics segment. Although no write-downs were experienced in fiscal 2010, there is no assurance that future write-downs of fixed assets or goodwill will not occur if business conditions deteriorate.

18

Changes in the price, availability and quality of raw materials could increase our costs or cause production delays and sales interruptions, which would result in decreased earnings.

We depend upon outside suppliers for most of our raw material needs, and increasingly we rely upon outside suppliers for component materials such as yarn and unfinished fabrics, as well as for certain services such as finishing and weaving. Fluctuations in the price, availability and quality of these goods and services could have a negative effect on our production costs and ability to meet the demands of our customers, which would affect our ability to generate sales and earnings. In many cases, we are not able to pass through increased costs of raw materials or increased production costs to our customers through price increases. In particular, many of our basic raw materials are petrochemical products or are produced from such products. For this reason, our material costs are especially sensitive to changes in prices for petrochemicals and the underlying price of oil. Increases in prices for oil, petrochemical products or other raw materials and services provided by outside suppliers could significantly increase our costs and negatively affect earnings.

Increases in energy costs would increase our operating costs and could adversely affect earnings.

Higher prices for electricity, natural gas and fuel increase our production and shipping costs. A significant shortage, increased prices, or interruptions in the availability of these energy sources would increase the costs of producing and delivering products to our customers, and would be likely to adversely affect our earnings. In many cases, we are not able to pass along the full extent of increases in our production costs to customers through price increases. During fiscal 2008, energy prices increased significantly, in part due to increases in the price of oil and other petrochemical products. Although some price increases were implemented to offset the effect of these increased costs, we were not able to fully recoup these costs, and operating margins were negatively affected. Energy costs eased somewhat in fiscal 2009 and 2010, but remain a volatile element of our costs. Further increases in energy costs could have a negative effect on our earnings.

Business difficulties or failures of large customers could result in a decrease in our sales and earnings.

We currently have several customers that account for a substantial portion of our sales. In the mattress fabric segment, several large bedding manufacturers have large market shares and comprise a significant portion of our mattress fabric sales, with Sealy, Inc. and Serta (National Bedding) accounting for approximately 22% of consolidated net sales in fiscal 2010. In the upholstery fabrics segment, La-Z-Boy Incorporated accounted for approximately 12% of consolidated net sales during fiscal 2010, and several other large furniture manufacturers comprised a significant portion of sales. A business failure or other significant financial difficulty by one or more of our major customers could cause a significant loss in sales, an adverse effect on our earnings, and difficulty in collection of our trade accounts receivable.

19

Loss of market share due to competition would result in declines in sales and could result in losses or decreases in earnings.

Our business is highly competitive, and in particular the upholstery fabric industry is fragmented and is experiencing an increase in the number of competitors. As a result, we face significant competition from a large number of competitors, both foreign and domestic. We compete with many other manufacturers of fabric, as well as converters who source fabrics from various producers and market them to manufacturers of furniture and bedding. In many cases, these fabrics are sourced from foreign suppliers who have a lower cost structure than the company. The highly competitive nature of our business means we are constantly subject to the risk of losing market share. Our sales of upholstery fabrics have decreased significantly over the past ten fiscal years due in part to the increased number of competitors in the marketplace, especially foreign sources of fabric. As a result of increased competition, there have been deflationary pressures on the prices for many of our products, which make it more difficult to pass along increased operating costs such as raw materials, energy or labor in the form of price increases and puts downward pressure on our profit margins. Also, the large number of competitors and wide range of product offerings in our business can make it more difficult to differentiate our products through design, styling, finish and other techniques.

If we fail to anticipate and respond to changes in consumer tastes and fashion trends, our sales and earnings may decline.

Demand for various types of upholstery fabrics and mattress coverings change over time due to fashion trends and changing consumer tastes for furniture and bedding. Our success in marketing our fabrics depends upon our ability to anticipate and respond in a timely manner to fashion trends in home furnishings. If we fail to identify and respond to these changes, our sales of these products may decline. In addition, incorrect projections about the demand for certain products could cause the accumulation of excess raw material or finished goods inventory, which could lead to inventory mark-downs and further decreases in earnings.

Restructuring initiatives create short-term costs that may not be offset by increased savings or efficiencies.

Over several years prior to the most recent fiscal year, we undertook significant restructuring activities, which involved closing manufacturing plants, realigning manufacturing assets, and changes in product strategy. These actions lowered our manufacturing costs and increased efficiency, but they also involved significant costs, including inventory markdowns, the write-off or write-down of assets, severance costs for terminated employees, contract termination costs, equipment moving costs, and similar charges. These charges caused significant decreases in earnings in prior fiscal years. There were no new restructuring initiatives in fiscal 2010, and we do not have any current plans for additional restructuring activities, but a significant and unanticipated downturn in business could lead to additional restructuring changes in the future.

20

We are subject to litigation and environmental regulations that could adversely impact our sales and earnings.

We are, and in the future may be, a party to legal proceedings and claims, including environmental matters, product liability and employment disputes, some of which claim significant damages. We face the continual business risk of exposure to claims that our business operations have caused personal injury or property damage. We maintain insurance against product liability claims and in some cases have indemnification agreements with regard to environmental claims, but there can be no assurance that these arrangements will continue to be available on acceptable terms or that such arrangements will be adequate for liabilities actually incurred. Given the inherent uncertainty of litigation, there can be no assurance that claims against the company will not have a material adverse impact on our earnings or financial condition. We are also subject to various laws and regulations in our business, including those relating to environmental protection and the discharge of materials into the environment. We could incur substantial costs as a result of noncompliance with or liability for cleanup or other costs or damages under environmental laws or other regulations.

We must comply with a number of governmental regulations applicable to our business, and changes in those regulations could adversely affect our business.

Our products and raw materials are and will continue to be subject to regulation in the United States by various federal, state and local regulatory authorities. In addition, other governments and agencies in other jurisdictions regulate the manufacture, sale and distribution of our products and raw materials. For example, standards for flame resistance of fabrics have been recently adopted on a nationwide basis. Also, rules and restrictions regarding the importation of fabrics and other materials, including custom duties, quotas and other regulations, are continually changing. Environmental laws, labor laws, tax regulations and other regulations continually affect our business. All of these rules and regulations can and do change from time to time, which can increase our costs or require us to make changes in our manufacturing processes, product mix, sources of products and raw materials, or distribution. Changes in the rules and regulations applicable to our business may negatively impact our sales and earnings.

None.

21

Our headquarters are located in High Point, North Carolina. As of the end of fiscal 2010, we owned or leased eight active manufacturing and distribution facilities and our corporate headquarters. The following is a list of our principal administrative, manufacturing and distribution facilities. The manufacturing facilities and distribution centers are organized by segment.

|

Approx.

|

|||||

|

Total Area

|

Expiration

|

||||

|

Location

|

Principal Use

|

(Sq. Ft.)

|

of Lease (1)

|

||

|

· Administrative:

|

|||||

|

High Point, North Carolina (2)

|

Upholstery fabric division

offices and corporate headquarters

|

56,880

|

2019

|

||

|

· Mattress Fabrics:

|

|||||

|

Stokesdale, North Carolina

|

Manufacturing, distribution,

and division offices

|

230,000

|

Owned

|

||

|

High Point, North Carolina

|

Manufacturing

|

63,522

|

2010

|

||

|

St. Jerome, Quebec, Canada

|

Manufacturing

|

202,500

|

Owned

|

||

|

· Upholstery Fabrics:

|

|||||

|

Anderson, South Carolina

|

Manufacturing

|

99,000

|

Owned

|

||

|

Burlington, North Carolina

|

Finished goods distribution

|

67,330

|

2010

|

||

|

Shanghai, China

|

Manufacturing and offices

|

69,000

|

2012

|

||

|

Shanghai, China

|

Manufacturing and warehousing

|

90,000

|

2012

|

||

|

Shanghai, China

|

Manufacturing and warehousing

|

101,632

|

2013

|

||

____________________________________________________

|

(1)

|

Includes all options to renew.

|

|

(2)

|

We are currently occupying the entire building. In the event we elect to renew the lease on April 1, 2012, the leased premises during any renewal period (see note 4 to the consolidated financial statements) will be 1/3 of the current occupied space of 56,880 square feet.

|

We believe that our facilities are in good condition, well-maintained and suitable and adequate for present utilization. In the upholstery fabrics segment, we have the ability to source upholstery fabric from outside suppliers to meet current and expected demand trends and further increase our output of finished goods. This ability to source upholstery fabric is part of our long-term strategy to have a low-cost platform that is scalable, but not capital intensive. In the mattress fabrics segment, management has estimated that it is currently performing at near capacity. In response, we had capital expenditures of $6.6 million in fiscal 2010 and plan to continue our significant level of capital spending in fiscal 2011 for modernizing and expanding our woven and knit capacities. Also, we have the ability to source additional mattress fabric from outside suppliers to further increase our ultimate output of finished goods.

22

A lawsuit was filed against the company and other defendants (Chromatex, Inc., Rossville Industries, Inc., Rossville Companies, Inc. and Rossville Investments, Inc.) on February 5, 2008 in United States District Court for the Middle District of Pennsylvania. The plaintiffs are Alan Shulman, Stanley Siegel, Ruth Cherenson as Personal Representative of Estate of Alan Cherenson, and Adrienne Rolla and M.F. Rolla as Executors of the Estate of Joseph Byrnes. The plaintiffs were partners in a general partnership that formerly owned a manufacturing plant in West Hazleton, Pennsylvania (the “Site”). Approximately two years after this general partnership sold the Site to defendants Chromatex, Inc. and Rossville Industries, Inc. the company leased and operated the Site as part of the company’s Rossville/Chromatex division. The lawsuit involves court judgments that have been entered against the plaintiffs and against defendant Chromatex, Inc. requiring them to pay costs incurred by the United States Environmental Protection Agency (“USEPA”) responding to environmental contamination at the Site, in amounts approximating $8.6 million, plus unspecified future environmental costs. Neither USEPA nor any other governmental authority has asserted any claim against the company on account of these matters. The plaintiffs seek contribution from the company and other defendants and a declaration that the company and the other defendants are responsible for environmental response costs under environmental laws and certain agreements. The plaintiffs also assert that the company tortiously interfered with contracts between them and other defendants in the case and diverted assets to prevent the plaintiffs from being paid monies owed to them. The company does not believe it has any liability for the matters described in this litigation and intends to defend itself vigorously. In addition, the company has an indemnification agreement with certain other defendants in the litigation pursuant to which the other defendants agreed to indemnify the company for any damages it incurs as a result of the environmental matters that are subject of this litigation. For these reasons, no reserve has been recorded.

23

EQUITY, RELATED STOCKHOLDER MATTERS, AND

ISSUER PURCHASES OF EQUITY SECURITIES

Registrar and Transfer Agent

Computershare Trust Company, N.A.

c/o Computershare Investor Services

Post Office Box 43078

Providence, Rhode Island 02940-3078

(800) 254-5196

(781) 575-2879 (Foreign shareholders)

www.computershare.com/investor

Stock Listing

Culp, Inc. common stock is traded on the New York Stock Exchange (“NYSE”) under the symbol CFI. As of May 2, 2010, Culp, Inc. had approximately 2,200 shareholders based on the number of holders of record and an estimate of individual participants represented by security position listings.

On January 29, 2010, we received notification from the NYSE that we regained compliance with the NYSE’s quantitative continued listing standards. In accordance with the NYSE’s Listed Company Manual, the company will be subject to a 12-month follow up period of review to ensure the company does not once again fall below the NYSE’s continued listing standards. We received a letter of noncompliance from the NYSE on December 11, 2008, notifying us that we had fallen below both the minimum shareholders’ equity and market capitalization requirements for continued listing on the NYSE. According to the January 2010 letter from the NYSE, our reinstatement to compliance comes as a result of our consistent and positive performance commensurate with the business plan submitted to the NYSE, and our compliance with the NYSE’s minimum market capitalization and shareholders’ equity requirements over the past two quarters.

Analyst Coverage

These analysts cover Culp, Inc.:

Raymond, James & Associates - Budd Bugatch, CFA

Value Line - Craig Sirois

Dividends and Share Repurchases; Sales of Unregistered Securities

We have not paid a cash dividend nor repurchased any of our common stock from our shareholders during the past three fiscal years. There were no sales of unregistered securities during fiscal 2010.

24

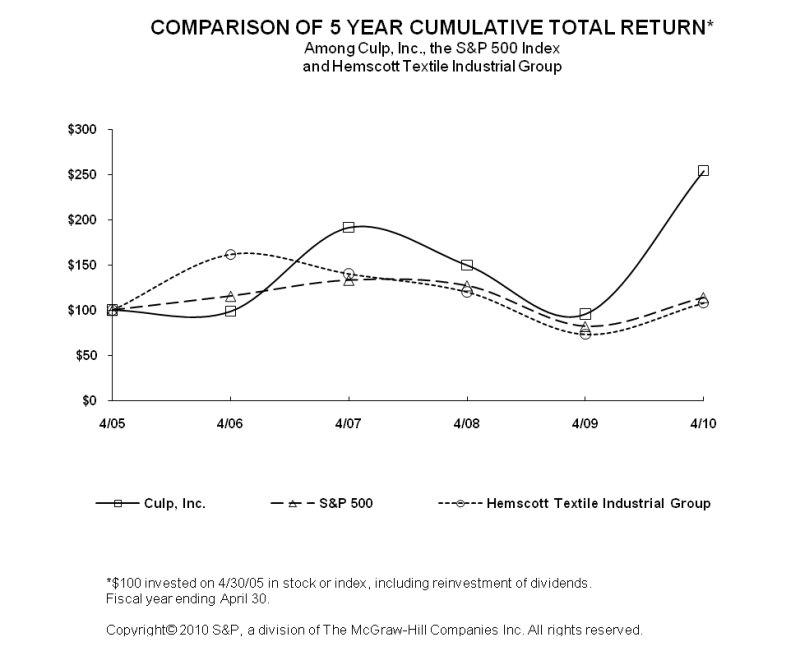

Performance Comparison

The following graph shows changes over the five fiscal years ending May 2, 2010 in the value of $100 invested in (1) the common stock of the company, (2) the Hemscott Textile Manufacturing Group Index (formerly named Core Data Textile Manufacturing Group Index) reported by Standard and Poor’s, consisting of twelve companies (including the company) in the textile industry, and (3) the Standard & Poor’s 500 Index.

The graph assumes an initial investment of $100 at the end of fiscal 2005 and the reinvestment of all dividends during the periods identified.

Market Information

See Item 6, Selected Financial Data, and Selected Quarterly Data in Item 8, for market information regarding the company’s common stock.

25

|

percent

|

|||||||||||||||||||||||

|

fiscal

|

fiscal

|

fiscal

|

fiscal

|

fiscal

|

change

|

||||||||||||||||||

|

(amounts in thousands)

|

2010

|

2009

|

2008

|

2007

|

2006

|

2010/2009 | |||||||||||||||||

| INCOME (LOSS) STATEMENT DATA | |||||||||||||||||||||||

|

net sales

|

$ | 206,416 | 203,938 | 254,046 | 250,533 | 261,101 | 1.2 | ||||||||||||||||

|

cost of sales (6)

|

167,639 | 179,286 | 220,887 | 219,328 | 237,233 | (6.5 | ) | ||||||||||||||||

|

gross profit

|

38,777 | 24,652 | 33,159 | 31,205 | 23,868 | 57.3 | |||||||||||||||||

|

selling, general, and administrative expenses (6)

|

22,805 | 19,751 | 23,973 | 27,030 | 28,954 | 15.5 | |||||||||||||||||

|

restructuring (credit) expense (6)

|

(370 | ) | 9,471 | 886 | 3,534 | 10,273 |

N.M.

|

||||||||||||||||

|

income (loss) from operations

|

16,342 | (4,570 | ) | 8,300 | 641 | (15,359 | ) |

N.M.

|

|||||||||||||||

|

interest expense

|

1,314 | 2,359 | 2,975 | 3,781 | 4,010 | (44.3 | ) | ||||||||||||||||

|

interest income

|

(116 | ) | (89 | ) | (254 | ) | (207 | ) | (126 | ) | 30.3 | ||||||||||||

|

other expense

|

828 | 43 | 736 | 68 | 634 |

N.M.

|

|||||||||||||||||

|

income (loss) before income taxes

|

14,316 | (6,883 | ) | 4,843 | (3,001 | ) | (19,877 | ) | (308.0 | ) | |||||||||||||

|

income taxes

|

1,128 | 31,959 | (542 | ) | (1,685 | ) | (8,081 | ) |

N.M.

|

||||||||||||||

|

net income (loss)

|

$ | 13,188 | (38,842 | ) | 5,385 | (1,316 | ) | (11,796 | ) | (134.0 | ) | ||||||||||||